Abstract

In recent years, Taiwan’s high-tech chip industry has experienced vigorous growth, with the telecommunications sector being the largest consumer of chips. Since the global outbreak of the pandemic in 2019, the telecommunications industry has played a major role in shaping human life and commercial activities. Moreover, advancements in chip technology are making telecommunications-related Artificial Intelligence (AI) increasingly powerful. Taiwan’s telecommunications AI industry has secured a significant position globally; however, its production processes often generate toxic substances, posing environmental risks. Therefore, companies should emphasize both operational profitability and sustainable development. This study covers a five-year period from 2018 to 2022, using Taiwan’s telecommunications AI industry as the research sample. The main contribution of this study lies in applying the Dynamic Network Directional Distance Function (DN-DDF) to analyze efficiency across four stages: profitability, sustainability, market performance, and overall efficiency. The study aims to enhance technical capabilities and promote rational resource allocation to assist businesses in making decisions that balance profitability with environmental protection, social responsibility, and corporate governance. It also considers market value, which is highly regarded by investors, to improve overall efficiency. Empirical results indicate that the average overall dynamic efficiency is highest at the market stage, followed by the profitability stage, and lowest at the sustainability stage. When dividing the industry into four major segments, branded terminals exhibit the highest average dynamic efficiency, followed by design, manufacturing, assembly, and key semiconductor chips. In contrast, telecommunications companies, being at the most downstream end, show the greatest need for improvement in the future.

Similar content being viewed by others

Introduction

In recent years, there has been rapid global development in technology, with Information and Communication Technology (ICT) extensively employed in communication products (Fettweis & Zimmerman1). The increasing adoption of Artificial Intelligence (AI) has notably enhanced the capabilities of these products. From key semiconductor chips to design, manufacturing, assembly, branded terminal products, and downstream telecommunication companies, the telecommunication industry has undergone extensive specialization and manufacturing processes, contributing significantly to societal progress. Taiwan’s telecommunication industry boasts an output value of approximately 4.3 trillion NTD, capturing a substantial 15.6% of the global market. Taiwan’s leadership in the global arena is primarily credited to its semiconductor industry. According to statistics from the Taiwan Semiconductor Industry Association, the global semiconductor market reached $547.1 billion USD in 2022, with Taiwan’s semiconductor industry generating $149.1 billion USD, accounting for 27.3% of the global market share and securing its top position worldwide. According to Fettweis et al.1the production of semiconductor chips consumes substantial amounts of energy, water, and electricity while emitting significant quantities of carbon dioxide. The failure to conserve energy could result in water shortages, electricity deficits, and environmental pollution. Furthermore, due to the chemical substances generated from the production process and the stress from the competitive market on the physical well-being of employees, environmental protection (E), social responsibility (S), and corporate governance (G) are crucial issues that enterprises face in achieving sustainable development.

Globally, there is increasing emphasis on Environmental, Social, and Governance (ESG) issues, and therefore, how to achieve sustainable development becomes a crucial agenda alongside financial performance for businesses. The Telecommunication AI industry, being both high-tech and high-polluting industries, attracts significant scrutiny regarding its ESG practices from all sectors of the community. Despite this, research on the ESG performance of Taiwan telecommunication AI industry is relatively limited, often focusing narrowly on static analyses, lacking in-depth exploration of dynamic efficiency changes. For this reason, apart from pursuing higher commercial profits, we expect Taiwan’s communication AI industries to retain their world-leading position. This paper applies advanced DDF DEA, which subdivides efficiencies into three stages to more clearly understand how much room there is for improvement from the standard efficiency. This will distinguish from the past use of DEA literature and will become a major contribution to enterprises. Therefore, this study adopts a quantitative modeling approach to examine the efficiency of Taiwan’s telecommunication AI industry across three key stages: profitability, sustainability, and market. By incorporating the Dynamic Network Directional Distance Function (DN-DDF), we aim to provide a more rigorous empirical analysis that distinguishes performance variations across these interconnected stages.

The primary goal is to evaluate the dynamic efficiency of 24 firms in this industry from 2018 to 2022. Specifically, the study investigates (1) how efficiency evolves across the three stages, (2) how company types differ in performance, and (3) what key factors influence efficiency outcomes. This research seeks to offer insights that help firms balance profit generation with environmental protection, social responsibility, and sound corporate governance.

This study pioneers the application of the Dynamic Network Directional Distance Function (DN-DDF) in analyzing the efficiency of Taiwan telecommunication AI industry across three distinct stages: profitability, sustainability, and market from 2018 to 2022. Through empirical investigation, it comprehensively discloses the dynamic efficiency fluctuations of companies within the three stages of profitability, sustainability and market. This multi-stage analysis can more accurately reflect the performance of a company in different operational segments and its changing trends. Drawing from the study’s findings, a series of policy recommendations are proposed to assist businesses in balancing economic profitability with environmental protection and social responsibility objectives. These research results serve as crucial reference points for industry stakeholders, governmental entities, and investors seeking informed decisions.

This is followed by the introduction of the relevant literature in “Literature review and theoretical framework”, the research methodology in “Research methodology”, the empirical findings in “Empirical research”, and finally the conclusions and policy implications.

Literature review and theoretical framework

ESG-oriented performance evaluation in emerging industries

In recent years, there has been rapid global development in corporate sustainability reporting, with ESG (Environmental, Social, and Governance) performance becoming a crucial component of strategic business evaluation. Taiwan’s high-tech chip industry, characterized by rapid innovation and global market demand, has gradually integrated ESG into its core performance metrics. Enterprises in this sector are increasingly evaluated based on financial profitability, their ESG disclosures, and real performance in social and environmental responsibility.

Zhou et al.2 studied listed companies in China and found that ESG practices significantly enhance a firm’s market value and financial performance. Similarly, Egorova et al.3emphasized that ESG actions in IT enterprises improve reputation and operational performance. These findings reinforce the importance of including ESG indicators in performance evaluation frameworks, particularly in high-tech sectors such as telecommunications and AI.

However, while ESG adoption is gaining momentum, many firms still face challenges translating ESG disclosures into measurable operational outcomes. This gap necessitates using models linking ESG actions with firm-level efficiency indicators.

DEA-based approaches for ESG and efficiency measurement

The evaluation of firm-level efficiency has long relied on the Data Envelopment Analysis (DEA) framework. While classical DEA models, such as CCR and BCC, effectively assess input-output efficiency, they cannot often decompose performance into temporal or stage-specific dimensions. This limitation has prompted researchers to explore more sophisticated variants.

Čiković et al.4 applied a DEA approach to evaluate efficiency during the COVID-19 pandemic in the information technology sector. Their findings illustrate the vulnerability of static models in capturing crisis-related performance variations. Wang et al.5utilized the Malmquist Productivity Index (MPI) to forecast firm growth; however, their model did not incorporate sustainability measures.

Pan et al.6 used the Non-Radial Directional Distance Function (NDDF) to assess the environmental performance of power enterprises in Eastern China. Although NDDF improved environmental measurement accuracy, its model lacked market and governance dimensions. Hossin et al.7 adopted a two-phase DEA model (BCC and CCR) to evaluate AI efficiency in MENA countries under ESG frameworks. Yet, these models did not incorporate firm-level, multi-stage performance tracking over time.

Rezaee et al.8 emphasized the need for interpretability in DEA models, particularly when applied in the context of AI and ESG evaluation. Their study proposed an AI-assisted DEA architecture to make target-setting and benchmark interpretation more transparent and aligned with strategic goals.

These recent studies highlight the evolution of DEA-based approaches in sustainability research. However, most remain limited to static, one-stage assessments or two-phase models that fail to account for dynamic and interrelated efficiency pathways within firms.

Dynamic network DEA: extending classical theory and enhancing ESG evaluation

To address the limitations of conventional DEA models in assessing complex, multi-dimensional performance, particularly in ESG contexts, this study adopts the Dynamic Network Directional Distance Function (DN-DDF) framework. DN-DDF enables multi-stage decomposition of firm efficiency while incorporating intertemporal dynamics, such as carry-over variables and link effects across stages. This modeling flexibility is especially suited to ESG-linked performance, which often involves overlapping investment cycles, delayed outcome realization, and stage-wise dependencies across financial, sustainability, and market dimensions.

The DN-DDF model builds upon foundational concepts in production frontier theory, notably the directional distance function (DDF) developed by Chambers et al.9 and the network DEA extensions by Färe and Grosskopf10. Unlike traditional radial DEA models that assume proportional improvement in all inputs or outputs, DDF allows customized directional vectors, reflecting realistic trade-offs, such as balancing ESG investment against short-term profitability or aligning social expenditures with intangible value creation. The network structure of DN-DDF allows system-wide performance to be decomposed into interrelated production stages, each defined by distinct input-output combinations.

In line with recent advancements, studies such as Pan et al.6 and Rezaee et al.8 have highlighted the potential of DDF-based models in evaluating ESG outcomes and AI sector dynamics. However, these applications remain limited to two-stage models or static configurations, lacking the capacity to trace performance evolution across time and stages. By operationalizing a three-stage DN-DDF model, this study expands the applicability of this theoretical framework. It demonstrates its robustness in ESG-integrated performance evaluation, particularly at the firm level.

Specifically, this research models firm behavior in the Taiwan Telecommunication AI Industry, presenting a rich empirical ESG complexity setting. Firms in this sector typically function across three ESG-relevant stages: (1) Profitability, reflecting internal operational efficiency through resource utilization (e.g., employees, R&D, output); (2) Sustainability, capturing environmental and social engagement (e.g., ESG scores, social welfare expenses, executive compensation); and (3) Market, representing external validation through investor and consumer response (e.g., earnings per share, market value, intangible assets).

In addition, intermediate link variables such as patents, brand value, and other factors such as fixed assets are incorporated to model the intertemporal and structural continuity of ESG-related inputs and outcomes.

By applying this model to a panel of 24 firms over five years (2018–2022), this study offers granular insight into how ESG drivers operate across internal processes and external performance metrics. It also allows for inter-firm comparisons, policy benchmarking, and the identification of stage-specific inefficiencies that may inform strategic ESG investment decisions. Ultimately, this framework retains the theoretical rigor of classical frontier analysis while demonstrating its extended relevance and adaptability to modern ESG performance challenges in AI-driven industries.

Research methodology

To effectively examine how firms in Taiwan’s telecommunication AI industry perform across three interrelated dimensions—profitability, sustainability, and market competitiveness—this study employs a quantitative analytical framework that integrates both temporal and structural complexities. These three dimensions reflect a sequential process along the corporate value chain and dynamic interdependencies that evolve. Traditional Data Envelopment Analysis (DEA) models, including radial, non-radial, or two-stage network variants, are limited in their ability to simultaneously account for such temporal and multi-stage relationships, especially in Environmental, Social, and Governance (ESG) evaluation.

In response to these limitations, this study adopts the Dynamic Network Directional Distance Function (DN-DDF) model. This advanced approach offers several methodological advantages that align well with the study’s objectives. First, it allows for evaluating firm-level efficiency across three logically connected stages—profit generation, ESG performance, and market outcomes—providing a disaggregated view of operational and sustainability-related capabilities. Second, the model explicitly incorporates inter-stage link variables (such as fixed assets and ESG disclosure scores) and carry-over variables that reflect investment or structural continuity across periods. Third, the dynamic nature of the DN-DDF model enables tracking performance changes over the study period (2018–2022), capturing not only cross-sectional variation among firms but also longitudinal trends in efficiency.

By applying this model, the analysis provides a nuanced understanding of how ESG-related inputs and outputs interact with corporate strategy and performance. The DN-DDF framework thus serves as a suitable and robust methodological tool to investigate the multi-dimensional efficiency of firms in an ESG-sensitive, technology-driven industry context.

Data Envelopment Analysis (DEA), based on the concept of Pareto Optimal Solution, has developed into a widely employed linear programming technique used to evaluate the relative efficiency of each Decision Making Unit (DMU). Originating from Farrell11DEA initially utilized the concept of frontier production functions to gauge the production levels of decision-making units. These functions connect the most efficient production points to form the production frontier, with the gap between points and the frontier indicating inefficiencies in production. Following Farrell’s theory, subsequent scholars have continued to evolve DEA methodology. In 1978, Charnes et al.12 introduced the CCR (Charnes, Cooper, and Rhodes) model, which assumes constant returns to scale. In 1984, Banker et al.13 developed the constant returns to scale into variable returns to scale, named as BCC (Banker, Charnes and Rhodes) model, which is very different from the input (output) oriented efficiency measures by the earlier scholars. Tone14 was the first to introduce the Slacks-Based Measure (SBM), a departure from the radial and input (output) oriented measures, considering the difference (slack) between non-radial and non-oriented. But the oriented DEA models overlook non-oriented slack variables in efficiency assessments, while non-oriented DEA models (like SBM) do not incorporate orientation characteristics in assessing efficiency. In 2007, Färe et al.15 introduced the Network Data Envelopment Analysis (Network DEA), which considers secondary production technologies as sub-decision-making units (Sub-DMUs) within the production process. This approach contrasts with traditional DEA models that treat a production unit as a “black box”. Instead, it focuses on how input allocations and intermediate goods influence the production process, thereby includes them into the assessment.

Tone and Tsutsui16 introduced the SBM Network DEA model, which leverages the interconnections among departments within a DMU as the foundation for Network DEA analysis, and then employs the SBM model to determine the optimal solution. In 2014, Tone and Tsutsui17 proposed the Weighted Dynamic Network DEA model, integrating cross-period variables as connections.

Distance functions were introduced separately by Malmquist and Shephard18,19 in 1953. They are widely used to describe production technologies and serve as a method for measuring efficiency and productivity. Distance functions can be divided into input distance functions and output distance functions. The former measures the minimum reduction in inputs while keeping outputs fixed, whereas the latter measures the maximum expansion in outputs while keeping inputs fixed. In cases where there are undesirable outputs between inputs or outputs, DDF-oriented models use the same ratio to calculate efficiency to add expected outputs and reduce non-desirable outputs. This assumption implies that all inputs and outputs share the same degree of inefficiency. Shephard’s distance function, as proposed, allows for proportional scaling of both desired and undesired outputs within feasible bounds, but it cannot simultaneously measure the increase in desired outputs while decreasing undesired outputs. On the other hand, the Directional Distance Function (DDF) can handle reductions in inputs and increases in outputs concurrently. Compared to Shephard’s approach, DDF is more adaptable. DDF can be categorized into Radial DDF (RDDF) and Non-Radial DDF (NDDF). RDDF adjusts non-desirable outputs and inputs proportionally while increasing desired outputs, yet it may overlook non-radial slack, potentially inflating efficiency estimates. Conversely, NDDF does not require proportional adjustments in inputs and outputs simultaneously, distinguishing it from traditional radial methods. Thus, NDDF evaluates efficiency from any direction, unlike radial methods, which measure efficiency along fixed directions.

The Directional Distance Function (DDF) model can be divided into Constant Returns to Scale (CRS) and Variable Returns to Scale (VRS) models. Here’s an explanation:

-

(1)

Non-oriented directional distance function model for CRS:

-

(2)

Non-oriented directional distance function model for VRS:

This research employs the DDF model proposed by Chung et al.20 and the RN-DDF model introduced by Fried et al.21 to adjust the efficiency measurement methods for the first and third stages. Specifically, given many influencing factors in the second stage, environmental factors are excluded before proceeding to the third stage. This study evaluates the Taiwan telecommunication AI industry across three stages using DN-DDF as the research method. This approach aims to address issues associated with static and single-stage models, providing a more objective and comprehensive view of overall efficiency and mitigating any potential underestimation or overestimation of efficiency levels.

In this paper, we use the (2 − 1) dynamic DDF (constant returns to scale) model to define a set (x, y), where x has m input vectors and y is s output vectors. \(\:\text{L}\left(\text{y}\right)=\left\{\left(\text{x},\:\text{y}\right)\right|\text{x}\:\:\text{c}\text{a}\text{n}\:\text{g}\text{e}\text{n}\text{e}\text{r}\text{a}\text{t}\text{e}\:\text{y}\}\). Considering each input-output directional vector \(\:(\text{x},\text{y})\left|\right({g}^{x}{g}^{y}),\) Chung et al. (1997) Proposed Directional Distance Function (DDF):

\(\:\text{D}\:\left(\text{x},\text{y},{g}^{x}{,g}^{y}\right)=\text{s}\text{u}\text{p}\{{\upalpha\:},|(\text{x}-{\upalpha\:}{g}^{x},\:\text{y}+{\upalpha\:}{g}^{y})\in\:\text{L}\left(\text{y}\right).\left({g}_{j}^{x},{g}_{j}^{y}\right)=({g}_{ij}^{x}{\dots\:,g}_{mj}^{x},{g}_{ij}^{y}\)…\(\:{g}_{xj}^{y})\:\text{a}\text{n}\text{d}\:\stackrel{\sim}{D}\left({x}_{j}{,y}_{j,}{g}^{x}{,g}^{y}\right):\) associated with the jth DMU input-output directional vector and directional distance function (\(\:{x}_{j},{y}_{j}\)). The input and output of the DMU’s direction vector \(\:\left({g}_{p}^{x},{g}_{p}^{y}\right)\) are usually positive.

In our three-stage model, we denoted as S1, S2, and S3 in each period t. Therefore, t = 1, ., T represents different periods for each stage. S1 has \(\:I\) inputs, denoted as \(\:{x}_{ij}^{t}\left(i=1,\dots\:,I\right)\), that generate K desirable output \(\:{y}_{kj}^{t}\left(k=1,\dots\:,\text{K}\right)\), and through the intermediate goods \(\:{z}_{dj}^{t}\left(d=1,\dots\:,\text{D}\right)\) to connect S2. S2 has inputs\(\:\:{f}_{bj}^{t}\left(b=1,\dots\:,\text{B}\right)\) and desirable output\(\:{\:n}_{aj}^{t}\left(a=1,\dots\:,\text{A}\right)\). Using the intermediate goods\(\:{\:\:h}_{oj}^{t}\left(o=1\dots\:.O\right)\) in S2, connecting to the third stage generates the desired output\(\:\:\:{q}_{cj}^{t}\:\left(c=1\dots\:.C\right)\), S3 also has \(\:D\) inputs \(\:\:{E}_{gj}^{t}\left(g=1,\dots\:,\text{G}\right)\). Moreover, \(\:{c}_{hj}^{t}\left(h=1,\dots\:,\text{H}\right)\) is the carry-over.

The objective function of the DMU’s efficiency is:

Subject to:

Stage 1: Profit stage

.

Stage 2: Sustainability stage

.

Stage 3: Market stage

.

The link between the two periods

.

The link between multiple stages:

where \(\:{\gamma\:}_{t}\) is the weight of time t. \(\:{w}_{1}^{t}\), \(\:{w}_{2}^{t}\:\), and \(\:{w}_{3}^{t}\) are the weights assigned to S1, S2, and S3. For every t and weight, we set equal to one.

The following efficiency groups can be calculated using linear programming models based on the above equations.

-

(1)

Stage efficiency.

The efficiency of stage \(\:l\) (\(\:l=1,\:2,\:3\)) for the evaluated DMU is relative to each period t (t=1, 2,\(\:\:\dots\:\), T). The stage one efficiency is:

The stage two efficiency is:

The stage three efficiency is:

-

(2)

Period efficiency.

The overall efficiency for each period t of the DMU being evaluated is expressed as follows: \(\:{\rho\:}^{t}\)=\(\:{{w}_{1}^{t}\theta\:}_{1}^{t}{{+w}_{2}^{t}\theta\:}_{2}^{t}{{+w}_{3}^{t}\theta\:}_{3}^{t};\:\:\:\:t\)=\(\:1,\:2,\:\dots\:,\text{{\rm\:T}}\)

-

(3)

Overall stage efficiency.

The overall efficiency is the weighted sum of the periodic efficiency at t, which is expressed as:

Empirical research

The data of this research is mainly adopted from Taiwan Economic Journal Co. (TEJ) and Sustainability Report for the period of 2018–2022. A three-phase analysis is adopted to examine the efficiency of 24 companies in the telecommunication industry in profitability stage, sustainability stage and market stage.

Variable description

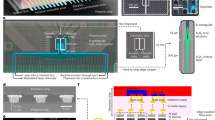

The 24 companies in Taiwan telecommunication industry are summarized as follows (please refer to Fig. 1; Table 1):

-

(1)

First Stage (profitability stage).

Input: number of employees, R&D expenses.

Output: Revenue, number of patents.

-

(2)

Second Stage (sustainability stage).

Input: directors’ remuneration and employee benefits, social welfare expenses.

Output: environmental component, social component, and corporate component.

-

(3)

Third Stage (market stage).

Input: market share, gross profit margin.

Output: ordinary share price, earnings per share.

-

(4)

Link: Fixed assets.

Research flowchart.

Descriptive statistics

In Table 2, Number of Employees: the average number of employees in the period of 2018–2022 is 65,524. The number of employees employed in the telecommunication industry is increasing year by year, with a decreasing trend in 2022.

R&D expenses: the average amount is 16,464,363 thousand in the period of 2018–2022, with a very significant increase year by year.

Revenue: the average amount is 586,166,045 thousand in the period of 2018–2022, showing a very significant increase year by year (1.01%, 1.04%, 1.11%, 1.11%).

Number of patents: the average number of patents in the period of 2018–2022 is 8623, with an increase of 200% in 2019 compared to 2018, and is steady in the period of 2018–2022.

Directors’ remuneration and employee benefits: the average amount is $27,989,763 thousand in the period of 2018–2022, showing a significant growth which is closely related to the increase in revenue and the increase in EPS year by year.

Social welfare expenses: the average amount in the period of 2018–2022 is $137,801 thousand, showing a significant growth year by year. However, in 2022, due to the pandemic, all economic activities were suspended, so the social welfare expenses of each company were relatively reduced.

Profit: the average amount in the period of 2018–2022 is $137,801 thousand. Due to the advanced chip technology in Taiwan, the profit has been growing significantly year by year, and in 2022, it grew about 2.5 times compared with that of 2018.

Environmental component score: the average in the period of 2018–2022 is 75.74; showing year-over-year growth and the industry invested more to improve the environment.

Social component score: the average in the period of 2018–2022 is 71.65, showing year-over-year growth and the industry invested more to improve the social structure.

Corporate governance component score: the average in the period of 2018–2022 is 62.89, showing year-over-year growth and the industry invested more to improve the corporate governance structure.

Market share: the average in the period of 2018–2022 is 0.823, showing year-over-year growth and this paper finds that Taiwan telecommunication industry is becoming more and more concentrated.

Gross profit margin: the average in the period of 2018–2022 is 18.48, showing year-over-year growth and the telecommunication industry has a tendency toward economies of scale in operating costs.

Ordinary share price: the average in the period of 2018–2022 is 127.50, showing year-over-year growth, but in 2022 due to the impact of the epidemic, business behavior is not enthusiastic, so the share price is unsatisfactory.

Earnings per share: the average in the period of 2018–2022 is 9.17, showing year-over-year growth, but in 2022 due to the impact of the epidemic, the earnings per share decreased slightly.

Fixed assets: The average amount in the period of 2018–2022 is $191,980,323 thousand, with growth rates of 10%, 114%, 16%, and 25%.

Empirical analysis

Overall dynamic efficiency value analysis (see Table 3)

This study examined the dynamic efficiency of 24 Taiwan telecommunication AI companies from 2018 to 2022, focusing on three stages: profitability, sustainability, and market performance. The findings reveal significant variations in the overall dynamic efficiency values of these companies across different years and stages. Specifically, Kinpo Electronics (2312), Compal Electronics (2324), and ASUS (2357) consistently achieved the highest efficiency value of 1 throughout the period from 2018 to 2022. This indicates that these companies demonstrated exceptional operational efficiency at all stages. Their success may be attributed to their superior performance in technological innovation, management strategies, and market responsiveness. Conversely, Chunghwa Telecom (2412), Lite-On Technology (2301), and TECO (1504) recorded the lowest overall dynamic efficiency values during the study period, with figures of 0.3994, 0.3926, and 0.3376, respectively. These companies are encountering considerable challenges in enhancing their operational efficiency and may require substantial improvements in technological advancements, management execution, and market development.

Throughout the study period, the companies with the lowest efficiency in 2018 were Mediatek (2454), TECO (1504), and Lite-On Technology (2301). From 2019 to 2022, Chunghwa Telecom (2412), TECO (1504), and Lite-On Technology (2301) consistently had the lowest efficiency. This suggests that these companies did not manage to significantly improve their operational efficiency over the years, likely due to challenges related to internal management and external market conditions. In contrast, ASRock (3515) and Mediatek (2454) demonstrated the most substantial progress, with their efficiency values increasing each year and eventually reaching 1. Their remarkable improvements illustrate how effective strategic planning and implementation can greatly enhance operational efficiency, providing valuable lessons for other companies in the industry.

Furthermore, when the 24 telecommunication companies are categorized into four groups: key semiconductor chip companies, design manufacturing and assembly companies, brand terminal companies, and downstream telecommunication companies, there are notable differences in their average dynamic efficiency values. Key semiconductor chip companies have an average dynamic efficiency of 0.8019. Design manufacturing and assembly companies show an average dynamic efficiency of 0.7383. In contrast, brand terminal companies achieve an average dynamic efficiency of 0.9071, reflecting their strong performance in market promotion and brand management. The average dynamic efficiency of downstream telecommunication companies is only 0.3994, indicating that these companies may have significant room for improvement in service quality and market-related aspects.

Analyzing efficiency values at each stage

In Tables 4 and 5 First stage—profitability stage: The overall dynamic average efficiency for the profit stage from 2018 to 2022 is 0.8105. Companies such as Kinpo Electronics (2312), Compal Electronics (2324), TSMC (2330), Acer (2353), ASUS (2357), MSI (2377), Realtek Semiconductor (2379), Foxlink (2392), and Chunghwa Telecom (2412) all achieved an efficiency value of 1, marking the highest performance. This indicates that these companies are highly efficient in generating profits, likely due to their strong market presence, effective cost management, and continuous technological advancements. In comparison, TECO (1504), Chicony Power Technology (6412), and Lite-On Technology (2301) have the lowest efficiency values in the profitability stage, with respective values of 0.5584, 0.5139, and 0.4290. Further analysis will be carried out to determine the areas that are most in need of improvement across different inputs and outputs. Overall, while the pandemic negatively affected the operations of many companies, most saw a rebound in their efficiency values by 2022. Among the top revenue earners—TSMC, Chunghwa Telecom, and Foxconn (2317)—their efficiency values at the profitability stage were 1 (ranked 1st), 1 (ranked 1st), and 0.6984 (ranked 16th), respectively. This suggests that despite having the highest revenues, Foxconn still has potential for improvement.

Second Stage - sustainability stage: The average efficiency value from 2018 to 2022 is 0.781, with the highest performers achieving a value of 1, including Kinpo Electronics, Compal Electronics, TSMC, ASUS, GUC, ASRock, Arcadyan, Primax, Pegatron, and WNC. The lowest performers are Chunghwa Telecom (0.2549), Realtek Semiconductor (0.2486), and Lite-On Technology (0.1925). Among the top revenue earners—TSMC, Chunghwa Telecom, and Foxconn—their efficiency rankings are 1 (1), 22 (0.2549), and 15 (0.7635), respectively. This indicates that TSMC excels in areas such as carbon emissions, water usage, wastewater energy management, community relations disclosure, board and employee welfare, social welfare expenses, and employee diversity disclosure.

Third Stage—market stage: Between 2018 and 2022, the average efficiency score was 0.8357, with a perfect score being 1. Among the companies, Kinpo Electronics, Compal Electronics, Accton Technology, ASUS, Quanta Computer, GUC, ASRock, Arcadyan, Primax, Pegatron, and WNC performed the best. On the other hand, Qisda (0.4120), Chunghua Telecom (0.2731), and TECO (0.2285) ranked the lowest three, indicating these companies need to put in more efforts to improve their market competitiveness and market share. The companies with the highest operating income were TSMC, Chunghua Telecom, and Foxconn, ranking 19th (0.7778), 23rd (0.2731), and 15th (0.9263) respectively in efficiency scores. This suggests that despite their strong revenue performance, these companies still have opportunities to enhance their market operational efficiency.

Analysis of the difference between the target value and each variable

In Tables 6, 7, 8, 9 and 10, Number of employees: From 2018 to 2022, 10 companies such as Kinpo Electronics, Compal Electronics, TSMC, Acer, ASUS, MSI, Realtek Semiconductor, Chunghwa Telecom, GUC, and ASRock—had actual numbers of employees that aligned with their target figures. This suggests that these companies did not hire excessively, avoiding inefficiencies. In contrast, Foxconn’s data indicates a need to reduce its workforce. Analysis shows that the top 10 companies in terms of overall efficiency have actual numbers of employees closely matching their target values, highlighting the significant impact of number of employees on operational efficiency.

R&D expenses: From 2018 to 2022, nine companies such as Kinpo Electronics, Compal Electronics, TSMC, Acer, ASUS, MSI, Realtek Semiconductor, Foxlink, and Chunghua Telecom met their R&D expenditure targets, while the remaining 15 companies exceeded their targets, with Foxconn notably surpassing its target by a significant margin during the same period. Given that R&D expenditures may have a lag effect spanning several years, the domestic telecommunication AI industry prioritizes sustainable development and therefore invests substantial amounts in research and development.

Directors’ Remuneration and Employee Benefits: Between 2018 and 2022, six companies such as Kinpo Electronics, TSMC, GUC, ASRock, Primax, and Pegatron met their target values, while the remaining 18 companies surpassed their targets, with Chunghua Telecom exceeding its targets by the most, with excess values of 27,482,573, 27,130,514, 26,305,221, 25,087,489, and 26,073,214 thousand NT dollars over the years. This variable is the input under the Second Stage of sustainability. Clearly, the high executive compensation and employee benefits at Chunghua Telecom have contributed to its inefficiency, placing it at 22nd in the rankings.

Social welfare expenses: From 2018 to 2022, six companies such as Kinpo Electronics, GUC, ASRock, Primax, Pegatron, WNC met their targets, while the remaining 18 companies exceeded theirs. Notably, Chunghua Telecom exceeded its targets by 731,257, 692,299, 1,033,783, 1,070,008, and 794,163 thousand NT dollars during this period. This variable is the input under the Second Stage of sustainability, which does not impact ESG scores.

Market share: From 2018 to 2022, 11 companies such as Kinpo Electronics, Compal Electronics, Accton Technology, ASUS, Quanta Computer, GUC, ASRock, Arcadyan, Primax, Pegatron, and WNC met their targets, while the remaining 13 companies exceeded their targets, with Foxconn notably surpassing its targets by 4.1736, 4.4388, and 6.8285 during 2019–2021. This indicates that Foxconn has substantial potential for improvement in its ordinary share price and earnings per share within its established market share.

Gross Profit Margin: Between 2018 and 2022, 11 companies such as Kinpo Electronics, Compal Electronics, Accton Technology, ASUS, Quanta Computer, GUC, ASRock, Arcadyan, Primax, Pegatron, WNC met their targets, while the remaining 13 companies exceeded their targets, indicating that these 13 companies did not translate their performance into improvements in ordinary share price or earnings per share under their existing operating profit margins. During this period, TSMC exceeded its targets with 11.39%, 12.99% in 2018–2019, and 2.69%, 17.10% in 2021–2022, but its ordinary share price remained too low, suggesting that the true value of TSMC’s ordinary share was not reflected in the market. Meanwhile, despite Chunghua Telecom surpassing its targets with 13.03%, 10.28%, 9.43%, 9.49%, and 10.11% in 2018–2022, its earnings per share remained low, indicating inefficient operational management due to high operating costs.

Revenue: From 2018 to 2022, nine companies such as Kinpo Electronics, Foxconn, Compal Electronics, Accton Technology, ASUS, MSI, Foxlink, Primax, Pegatron achieved their revenue targets, while the remaining 15 companies failed to meet their targets, highlighting the need for these 15 companies to boost their revenue generation.

Number of patents: From 2018 to 2022, nine companies such as Kinpo Electronics, Compal Electronics, TSMC, Acer, ASUS, MSI, Realtek Semiconductor, Foxlink, Chunghua Telecom met their targets on patent counts, while the remaining 15 companies must increase their number of patents.

Ordinary share price: Between 2018 and 2022, 11 companies such as Kinpo Electronics, Compal Electronics, Accton Technology, ASUS, Quanta Computer, GUC, ASRock, Primax, Pegatron, WNC achieved their targets, while the remaining 13 companies such as TECO, Foxconn, TSMC, Qisda, Acer, Realtek Semiconductor, Foxlink, Chunghua Telecom, Wistron etc. fell short of their targets. TSMC notably missed its target by 56.72%, leading to an increase in its stock price in 2014, while other telecommunication companies generally experienced an overall rise in 2014.

Earnings per share: Between 2018 and 2022, ten companies such as Kinpo Electronics, Compal Electronics, ASUS, Quanta Computer, GUC, ASRock, Arcadyan, Primax, Pegatron, WNC met their earnings per share targets. However, the remaining 14 companies such as TECO, Foxconn, TSMC, Qisda, Acer, Realtek Semiconductor, Foxlink, Chunghua Telecom, Wistron had lower-than-expected earnings per share. Chunghua Telecom showed the largest shortfall from its targets (− 3.63, − 6.04, − 9.69, − 19.29, − 21.30), indicating significant challenges in achieving their earnings goals during this period.

Profitability: From 2018 to 2022, 17 companies such as TECO achieved their targets, while the remaining seven fell short. By 2022, only four companies such as Quanta Computer were still below their targets.

Environmental component score (output): From 2018 to 2022, nine companies such as Kinpo Electronics achieved their targets, while the remaining 15 companies still require improvement. TSMC needs to improve during 2018–2022 with − 45.23, − 17.03, 0, − 25.95, and − 12.32, whereas Realtek Semiconductor needs improvement during 2018–2022 with − 30.59, − 26.45, − 27.54, − 24.53, and − 19.90.

Social component score (output): From 2018 to 2022, nine companies such as Kinpo Electronics met their targets, while the remaining 15 companies still need to make improvements. TECO (− 13.65, − 9.58, − 13.09, − 22.85, − 20.29), Foxconn (− 19.70, − 20.39, − 11.04, − 9.48, − 17.62), Realtek Semiconductor (− 27.66, − 32.60, − 24.80, − 19.42, − 18.72), and Foxlink (0, − 12.21, − 12.87, − 17.93, − 20.10) still have a ways to go to reach the standard values.

Corporate governance component score (output): From 2018 to 2022, 15 companies such as Kinpo Electronics and 8 other companies achieved their targets, while the remaining 15 companies still need to improve. Four companies such as TECO (− 20.05, − 17.52, − 20.36, − 13.90, − 14.47), Acer (− 21.84, − 8.15, − 26.57, − 24.95, − 22.59), Realtek Semiconductor (− 40.04, − 32.36, − 28.56, − 29.90, − 12.94) have yet to reach the standard values.

Conclusion and implications

This study investigates the dynamic efficiency of 24 telecommunication AI companies in Taiwan from 2018 to 2022, employing a three-stage Dynamic Network Directional Distance Function (DN-DDF) model. The three stages—profitability, sustainability, and market performance—correspond to firms’ capacity to generate profit, implement ESG practices, and achieve market recognition. The empirical results directly respond to the study’s research. First, we find that efficiency varies significantly across stages, with the sustainability stage consistently exhibiting the lowest average efficiency, reflecting limited ESG integration. Second, branded terminal and chip companies (e.g., Kinpo, Compal, ASUS) show strong performance with overall dynamic efficiency values reaching 1. At the same time, downstream service providers (e.g., Chunghwa Telecom, Lite-On, TECO) exhibit persistent inefficiency across years, particularly in ESG-related dimensions. This demonstrates apparent structural differences in how firms manage ESG resources relating to financial and market outcomes.

A closer examination of firm-specific patterns reveals that Kinpo, Compal, and ASUS consistently achieved optimal efficiency across all three stages, likely due to effective R&D investment, operational management, and brand value. In contrast, Chunghwa Telecom, Lite-On, and TECO consistently ranked at the bottom, showing stagnation or decline in performance. For example, Chunghwa Telecom’s high compensatory social welfare spending, without corresponding ESG or market output, may explain its sustainability and market strategy. Meanwhile, firms like ASRock and Mediatek demonstrated marked year-over-year improvement, suggesting that strategic transformation, innovation, and ESG realignment can lead to notable efficiency gains.

Compared with previous literature, this study contributes both methodologically and empirically. Earlier works, such as Čiković et al.4Wang et al.5and Hossin et al.7primarily employed one-stage or two-phase DEA models, often ignoring the temporal and structural complexity of ESG activities. This study’s three-stage DN-DDF allows for a granular decomposition of operational, sustainability, and market performance, capturing firm-specific inefficiencies and dynamics across time. In addition, while Rezaee et al.8 emphasized the interpretability of AI-DEA models, their studies remained general in scope; our firm-level focus provides direct managerial relevance within the ESG context of AI-intensive industries.

The results offer several practical implications. For regulators, the findings underscore the need to strengthen ESG disclosure standards, particularly among downstream telecom firms, where efficiency remains low. The analysis provides diagnostic insights for corporate managers regarding specific variables—such as fixed assets, social welfare costs, executive remuneration, and R&D allocation—that influence performance at different stages. Addressing inefficiencies in these areas may improve ESG scores and enhance firm value and market recognition.

Nevertheless, this study has several limitations. First, ESG data availability across firms remains uneven, especially for environmental metrics like greenhouse gas emissions and water contamination. This limits the scope and precision of sustainability-related measurements. Second, external contextual variables—such as regulatory shocks, macroeconomic instability, or global supply chain disruptions—were not explicitly modeled, which may affect dynamic performance. Third, the study does not evaluate the outcomes of specific policy measures, such as ESG incentives or penalties, leaving the effectiveness of regulatory interventions unexamined.

Future research may build upon this framework by applying the DN-DDF model to cross-national or industry-wide comparisons, where variations in institutional context and ESG maturity may yield further insights. Integrating explainable AI approaches would also enhance interpretability and transparency in DEA target-setting. Finally, longitudinal studies assessing how firms respond to specific policy changes—such as climate regulations or disclosure mandates—can provide more actionable recommendations for practitioners and policymakers.

Data availability

No datasets were generated or analysed during the current study.

References

Fettweis, G. & Zimmermann, E. ICT energy consumption—trends and challenges. In The 11th International Symposium on Wireless Personal Multimedia Communications (WPMC 2008), 1–4 (2008).

Zhou, R., Liu, L. & Luo, S. Sustainable development, ESG performance and company market value: mediating effect of financial performance. Bus. Strategy Environ. 31 (7), 3371–3387 (2022).

Egorova, A. A., Grishunin, S. V. & Karminsky, A. M. The impact of ESG factors on the performance of information technology companies. Proc. Comput. Sci. 199, 339–345 (2022).

Čiković, K. F. & Lozić, J. Application of data envelopment analysis (DEA) in information and communication technologies. Tech. J. 16 (1), 129–134 (2022).

Wang, C. N., Yang, F. C., VO, N. T. M., Duong, C. T. & Nguyen, V. T. T. Enhancing operational efficiency in industrial systems: A DEA-grey integration. IEEE Access. 12 (1), 58532–58549 (2024).

Pan, Y., Zhang, C. C., Lee, C. C. & Lv, S. Environmental performance evaluation of electric enterprises during a power crisis: evidence from DEA methods and AI prediction algorithms. Energy Econ. 130, 1–13 (2024).

Hossin, M. A., Alemzero, D., Wang, R., Kamruzzaman, M. M. & Mhlanga M. N. Examining artificial intelligence and energy efficiency in the MENA region: the dual approach of DEA and SFA. Energy Rep. 9, 4984–4994 (2023).

Rezaee, M. J., Onari, M. A. & Saberi, M. A data-driven decision support framework for DEA target setting: an explainable AI approach. Eng. Appl. Artif. Intell. 127, 1–14 (2024).

Chambers, R. G., Chung, Y. & Färe, R. Benefit and distance functions. J. Econ. Theory. 70 (2), 407–419 (1996).

Färe, R. & Grosskopf, S. New directions: efficiency and productivity. Springer Sci. & Bus. Media 3 (2006).

Farrell, M. J. The measurement of productive efficiency. J. R. Stat. Soc. Ser. (Gen.). 120 (3), 253–281 (1957).

Charnes, A., Cooper, W. W. & Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 2 (6), 429–444 (1978).

Banker, R. D., Charnes, A. & Cooper, W. W. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Manag. Sci. 30 (9), 1078–1092 (1984).

Färe, R., Grosskopf, S. & Pasurkajr, C. A. Environmental production functions and environmental directional distance functions. Engerey. 32 (7), 1055–1066 (2007).

Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 130 (3), 498–509 (2001). 2001.

Tone, K., Tsutsui, M. & Network, D. E. A. A slacks-based measure approach. Eur. J. Oper. Res. 197 (1), 243–252 (2009).

Tone, K. & Tsutsui, M. Dynamic DEA with network structure: A slacks-based measure approach. Omega. 42 (1), 124–131 (2014).

Malmquist, S. Index numbers and indifference surfaces. Trabajos De Estadística. 4 (1), 209–242 (1953). (1953).

Shephard, R. W. Cost and Production Functions (Princeton University Press, 1953).

Chung, Y. H., Färe, R. & Grosskopf, S. Productivity and undesirable outputs: A directional distance function approach. J. Environ. Manage. 51 (3), 229–240 (1997).

Fried, H. O., Lovell, C. A. K., Schmidt, S. S. & Yaisawarng, S. Accounting for environmental effects and statistical noise in data envelopment analysis. Journal of productivity analysis. J. Prod. Anal. 17, 157–174 (2002).

Author information

Authors and Affiliations

Contributions

S.-Y.H., S.-Y.C. and Y.-H.C. wrote the main manuscript text. All authors reviewed the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Hsu, SY., Chiu, SY. & Chiu, Yh. Taiwan telecommunication AI industry ESG disclosure. Sci Rep 15, 20043 (2025). https://doi.org/10.1038/s41598-025-04585-1

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s41598-025-04585-1