Abstract

This paper examines the effectiveness of China’s Environmental Protection Tax in reducing regional carbon emissions. Using a difference-in-differences empirical strategy, we analyze panel data from 287 Chinese cities over the period from 2009 to 2021. The results demonstrate that the Environmental Protection Tax has led to a significant reduction of 5.63% in carbon emissions. Mechanism analysis reveals that this reduction is primarily driven by increased investment in green research and development, improved energy efficiency, and industrial upgrading. Further heterogeneity analysis shows that the policy is more effective in eastern regions, Non-old traditional industrial areas, strong government concern areas, and energy-intensive areas. In addition to reducing carbon emissions, the Environmental Protection Tax has also lowered other air pollutants, improved air quality, and enhanced residents’ subjective well-being. These findings provide robust empirical support for the optimization of environmental tax policies to further strengthen China’s transition to a low-carbon economy and advance its sustainable development objectives.

Similar content being viewed by others

Introduction

Climate change is one of the most pressing global challenges facing humanity. The substantial emission of greenhouse gases, such as carbon dioxide, has led to a rise in global average temperatures, triggering a series of environmental and economic issues, including glacier melting and sea level rise1,2,3. To effectively control carbon dioxide emissions, the 21 st Conference of the Parties (COP21) set a goal of limiting the global average temperature increase to within 2 °C above pre-industrial levels by the end of this century, to keep the temperature rise below 1.5 °C to mitigate environmental risks. As the most populous country in the world and the largest emitter of carbon emissions4 China has actively engaged in global environmental governance. At the 75th United Nations General Assembly in 2020, China announced its commitment to peak carbon dioxide emissions by 2030 and to achieve carbon neutrality by 2060. On July 11, 2023, the Central Committee for Deepening Reform approved the “Opinions on Promoting the Transition from Energy Consumption Control to Carbon Emission Control,” further emphasizing the need to balance development with emission reduction and to strengthen the foundational capacity for carbon emission control, creating favorable conditions for the establishment and implementation of a dual carbon control systemFootnote 1.

In recent years, to accelerate the construction of an ecological civilization and achieve carbon reduction targets, China has implemented a series of environmental governance policies. These include the establishment of “dual control zones,” dynamic adjustments to pollution discharge fee standards, the 2011 “Notice on Launching Pilot Carbon Emission Trading Programs,” the 2013 Air Pollution Prevention and Control Action Plan, and the Central Environmental Protection Inspection5,6,7,8,9,10. While China has adopted numerous policies to promote carbon reduction and environmental protection, most of these policies focus on administrative controls, regulation, and market mechanisms such as pollution discharge permits, pollution fees, and carbon trading11,12,13,14. However, tax policies, as market-based economic incentives, have not been fully emphasized or utilized. The Environmental Protection Tax works by imposing taxes on pollution emissions, thereby increasing the operational costs of polluting enterprises and encouraging them to adopt more environmentally friendly production methods and cleaner technologies. Unlike traditional administrative measures, tax policies, through market mechanisms, guide enterprises to actively invest in low-carbon technologies and optimize pollution emissions, offering greater flexibility and long-term benefits. Since its implementation in 2018, China’s Environmental Protection Tax has primarily targeted emissions from air and water pollutants. Although it has achieved some progress in controlling traditional pollutants15,16,17there is still a lack of research on its specific impact on carbon emissions. Unlike other pollutants, carbon emissions have cross-regional and long-term impacts, which require tax policies to be more targeted and flexible in design. As an indirect incentive tool, the Environmental Protection Tax can effectively motivate market entities to reduce emissions, not only helping to lower overall emission levels but also promoting green technological innovation and industrial restructuring. Therefore, in the process of achieving carbon peak and carbon neutrality targets, optimizing the Environmental Protection Tax policy and enhancing its incentive effects on carbon reduction is both crucial and urgent.

Existing research has examined the impacts of the Environmental Protection Tax on various factors, including the economy, environment, innovation, and labor18,19,20,21,22. However, there are significant differences between the Environmental Protection Tax in China and those in other countries. For example, the European Union’s Emissions Trading System (EU ETS) focuses on directly pricing carbon emissions through market-based mechanisms, aiming to encourage businesses to adopt emission reduction measures through price signals or to facilitate the green transformation of businesses by increasing carbon taxes, thus achieving carbon reduction23,24,25,26. Internationally, environmental taxes mainly focus on pricing or directly taxing carbon to reduce emissions, while China’s Environmental Protection Tax primarily targets air pollutants such as sulfur dioxide and nitrogen oxides, with no clear focus on carbon emission control. Despite these differences, China’s Environmental Protection Tax system still plays a significant role in promoting carbon reduction and green transformation. While China’s tax focuses primarily on traditional pollutants, such as sulfur dioxide and nitrogen oxides, these pollutants are closely linked to carbon emissions. Therefore, by reducing pollutant emissions, the Environmental Protection Tax indirectly contributes to carbon reduction.

Globally, many countries have effectively promoted the development of a low-carbon economy through carbon pricing mechanisms, particularly the carbon emissions trading systems and carbon tax policies in the European Union and Sweden, which have successfully facilitated energy transition and greenhouse gas reduction23,24,25,26. However, as the largest developing country in the world, China’s economic and energy structures are complex, and its carbon emission reduction path significantly differs from that of developed nations. China’s unique national circumstances offer the international community a distinct perspective, especially in the context of economic transformation, where balancing economic growth with environmental protection has become a focal point of global attention. Investigating the impact of China’s Environmental Protection Tax on carbon emissions not only provides empirical support for China’s environmental tax reform, addressing the gap in research on carbon emissions taxation but also offers valuable insights for other developing countries in formulating carbon reduction tax policies suited to their national conditions. Therefore, in the process of achieving the “carbon peak and carbon neutrality” targets, optimizing existing green tax policies, further advancing carbon pricing mechanisms, and integrating domestic green technological innovation with policy design is a critical issue in the current global environmental governance discourse.

To strengthen environmental protection and promote ecological civilization, China enacted the Environmental Protection Tax Law of the People’s Republic of China, which came into effect on January 1, 2018. While this tax does not directly target carbon dioxide, there is a close relationship between the two. Coal consumption, a major source of air pollutants and solid waste, is subject to the tax, which specifically levies charges on pollutants such as sulfur dioxide, nitrogen oxides, carbon monoxide, fly ash, and coal gangue. The emissions of these taxed pollutants often coincide with carbon dioxide emissions, creating an incentive for enterprises to adopt green technologies or install pollution control equipment to mitigate these pollutants. The environmental benefits of such innovations, along with the spillover effects from technological upgrades, are likely to contribute to a significant reduction in carbon dioxide emissions27,28,29. In the context of China’s “dual carbon” targets, which guide the nation’s transition to a low-carbon economy and the advancement of ecological civilization, the Environmental Protection Tax—China’s first tax explicitly focused on environmental protection—plays a crucial role in steering enterprises toward green production and enhancing their economic value30,31,32. Thus, leveraging the reform of the Environmental Protection Tax provides a key opportunity to evaluate the effectiveness and mechanisms of tax policies in achieving carbon emission reductions.

This paper uses panel data from 287 cities between 2009 and 2021 and applies a difference-in-differences empirical framework to assess the impact of the Environmental Protection Tax on regional carbon emissions, as well as the underlying mechanisms driving emission reductions. The study yields the following key findings: First, the Environmental Protection Tax leads to a significant reduction in regional carbon emissions, with an average decrease of 5.63%. Second, the tax promotes carbon reduction by stimulating regional investment in green research and development (R&D), enhancing energy efficiency, and facilitating industrial upgrades. Third, the Environmental Protection Tax is more effective in reducing carbon emissions in eastern regions, Non-old traditional industrial areas, strong government concern areas, and energy-intensive areas, while its impact is pronounced in central and western regions, older industrial areas, weaker government focus, and Non-energy-intensive areas. Fourth, the tax also contributes to reductions in pollutant emissions, improvements in air quality, and enhancements in residents’ subjective well-beingFootnote 2.

This study makes several incremental contributions beyond the existing literature.

First, this study contributes to the literature on the impact of environmental regulation policies on carbon emissions in developing countries. While China implemented its first explicit Environmental Protection Tax in 2018, the tax’s effect on regional carbon emissions remains underexplored. Most existing research focuses on the Environmental Protection Tax’s impact on pollution reduction and economic performance21,32,33,34,35,36with relatively few studies examining its effect on carbon emissions. This study enhances the understanding of how tax-based environmental regulation policies can contribute to regional carbon reduction.

Second, this study provides empirical evidence on the emission reduction mechanisms of the Environmental Protection Tax. Given that China has not implemented a carbon tax, and since the Environmental Protection Tax targets pollutants rather than carbon directly, most research on carbon reduction focuses on carbon emission trading systems or on models such as Computable General Equilibrium (CGE) and Dynamic Stochastic General Equilibrium (DSGE) that simulate the effects of carbon taxes37,38,39,40,41,42,43. However, because the Environmental Protection Tax is closely linked to pollutants, it influences industrial production and operations, potentially affecting firms’ carbon emission behaviors. This perspective offers new insights into the emission reduction effects and mechanisms of tax-based environmental policies in developing countries without a carbon tax.

Third, this study provides empirical support for strengthening environmental regulation policies in developing countries and aligning them with green, sustainable economic development. In the context of “carbon peaking and carbon neutrality,” and the approach of “pollution reduction, carbon reduction, greening, and efficiency improvement,” developing innovative green and low-carbon mechanisms, and improving ecological governance systems, have become essential long-term strategies44,45,46. This paper offers valuable insights from a tax policy perspective for designing carbon reduction mechanisms and enhancing ecological governance frameworks.

The structure of the following paper is arranged as follows: The second part provides the policy background and outlines the research hypotheses; The third part details the research design, including the methodology and data sources used; The fourth part presents the analysis of the empirical results, highlighting key findings from the data; The fifth part focuses on the heterogeneity analysis, exploring variations across different regions or groups; The sixth part discusses the implications of the findings, with insights into the broader context and policy recommendations.

Policy background and research hypotheses

Policy background

Broadly speaking, Environmental Protection Taxes encompass both taxes specifically designed for environmental protection and those that, while not primarily aimed at this goal, still contribute to it. Examples of the latter include the Urban Maintenance and Construction Tax, the Urban Land Use Tax, the Vehicle and Vessel Tax, and tax expenditure policies with environmental functions. More narrowly, the term “Environmental Protection Tax” refers to taxes specifically levied to combat environmental degradation, particularly targeting pollutant and carbon dioxide emissions. This narrower definition includes taxes such as the Air Pollution Tax, Sulfur Dioxide Tax, Nitrogen Tax, Wastewater Tax, Garbage Tax, Noise Tax, Carbon Tax, and Greenhouse Gas Emission Tax. Before 2018, China did not have formal pollution taxation policies. This paper focuses on the narrower scope of the Environmental Protection Tax, specifically targeting pollutant emissions.

China began imposing pollutant discharge fees in 1982, and 2003, the State Council issued the Regulations on the Collection and Use of Pollutant Discharge Fees. This regulation shifted the focus from charging only for excess emissions to a system that combined fees for all emissions with additional charges for exceeding environmental standards. It also clarified the budget management of pollutant discharge fee funds and established fee standards for air and water pollutants. To further enhance environmental protection, reduce emissions, and promote ecological civilization, the 25th session of the Standing Committee of the 12th National People’s Congress passed the Environmental Protection Tax Law of the People’s Republic of China on December 25, 2016, which took effect on January 1, 2018. The Environmental Protection Tax aims to regulate pollution by taxing specific pollutants, with 89.27% of the revenue derived from air pollutants (State Taxation Administration, 2020). Before 2018, the pollutant discharge fee system faced several challenges, including a narrow scope of collection, weak enforcement, and local government interference, which hindered effective environmental governance47. As a result, the pollutant discharge fee system did not function as a true environmental tax. The 2018 Environmental Protection Tax introduced the principle of tax legality, meaning that companies evading or underpaying taxes would face both administrative penalties and criminal charges. Under the new law, provincial governments are authorized to set tax rates within a statutory range, with some local governments raising the standards. For example, Beijing increased the sulfur dioxide tax rate from 10 yuan per kilogram in 2017 to 12 yuan per kilogram in 2018, while Liaoning Province maintained a rate of 1.26 yuan per kilogram.

The implementation of the Environmental Protection Tax provides a clear framework for evaluating the policy’s effects, resembling a quasi-natural experiment in economics. Thus, constructing a difference-in-differences model to assess its impact on regional carbon emissions is appropriate48,49. Table 1 reports the changes in the pollution discharge fee and Environmental Protection Tax rates across 31 provinces in China from 2017 to 2018. In 2018, some provinces and municipalities increased their Environmental Protection Tax rates. This offers an effective identification method for the study, akin to a quasi-natural experiment. We classify regions with increased tax rates as the experimental group and those without as the control group.

Research hypotheses

To protect and improve the environment, reduce pollutant emissions, and promote the construction of an ecological civilization, China enacted the Environmental Protection Tax Law in 2018. This law primarily taxes air, water, solid, and noise pollutants. The specific tax rates for taxable air and water pollutants are determined and adjusted by the provincial, autonomous region, and municipality governments based on the local environmental carrying capacity, current pollutant emission levels, and the economic, social, and ecological development goals. Some provinces and cities have already raised the environmental protection tax rates50. The Environmental Protection Tax follows the principle of “the more emissions, the more tax; the fewer emissions, the less tax; no emissions, no tax.” Compared to the pollution discharge fees, in addition to changes in the tax rates, the Environmental Protection Tax has undergone significant changes in terms of collection authority, revenue distribution, tax reduction policies, and the use of tax revenues. Specifically, the responsibility for tax collection was shifted from environmental protection departments to tax authorities, enhancing the enforcement and transparency of tax collection. Regarding revenue distribution, while pollution discharge fees were previously shared between the central and local governments in a 1:9 ratio, now all environmental protection tax revenues are allocated to local governments, with no share for the central government51. In terms of tax reduction policies, if the concentration of taxable air or water pollutants emitted by taxpayers is below 30% of the national or local emission standards, they can be taxed at a reduced rate of 75%; if the concentration is below 50% of the standards, they are taxed at a reduced rate of 50%. As for the use of revenue, while pollution discharge fees had specific purposes, the Environmental Protection Tax does not have clear allocation guidelines, providing local governments with more flexibility. Moreover, compared to the previous system of separate administrative penalties, the shift to tax authorities and the possibility of criminal charges for violations significantly enhance the rigor and enforcement of supervision. The implementation of the Environmental Protection Tax poses greater challenges to local governments’ green development, while also providing enterprises with incentives for pollution reduction through more tax reductions when actively engaging in environmental governance52,53. Based on the above theory, the paper proposes Research Hypothesis 1:

Hypothesis 1

The Environmental Protection Tax can effectively reduce corporate carbon emissions.

Green innovation, as a key driver of environmental quality improvement and economic transformation, occupies a central position in the mechanism of environmental regulation. According to the Porter Hypothesis, appropriate environmental regulation can encourage firms to internalize environmental costs, break existing path dependencies, and stimulate green technological innovation54. As a typical market-based environmental policy, the Environmental Protection Tax significantly alters the cost-benefit trade-off for enterprises by increasing emission costs, thereby prompting firms to incorporate green innovation into their core strategies to cope with the additional tax burden and environmental compliance pressures. From the microeconomic perspective of firm decision-making, the Environmental Protection Tax raises the marginal costs of traditional high-pollution production models, lowers pollution tolerance, and forces companies to accelerate the development and application of green technologies16. Enterprises can adopt advanced technologies and facilities such as coking, coal preparation, and gas purification to achieve ultra-low concentration emissions of pollutants. Green innovation not only directly reduces pollutant emissions and lowers tax burdens but also brings long-term competitive advantages through optimizing production processes and developing green products. Therefore, the Environmental Protection Tax creates an intrinsic incentive chain of “regulatory pressure - innovation investment - pollution reduction” by enhancing the relative returns on green innovation55. At the regional level, green innovation exhibits significant knowledge spillover effects across different enterprises and industries. Breakthroughs by leading firms in green technologies can spread through supply chain diffusion, imitation learning, and professional labor mobility, thereby improving the overall green technology level of the region and generating large-scale, systematic carbon emission reduction effects. The Environmental Protection Tax, by incentivizing leading firms to take the lead in green transformation, indirectly promotes the accumulation and expansion of regional green innovation capacity, accelerating the systemic process of low-carbon transformation. Moreover, when facing environmental taxes, firms are more likely to invest in substantial emission reduction, energy efficiency improvements, and clean production technologies rather than merely complying with the minimum emission standards56. This high-quality green innovation becomes a key force in continually reducing carbon emission intensity. Based on the above theory, the paper proposes research hypothesis 2:

Hypothesis 2

The Environmental Protection Tax effectively reduces carbon emissions by improving green research and development.

Carbon dioxide emissions primarily stem from the use of fossil fuels, which make up a significant portion of China’s energy mix. In 2023, coal consumption accounted for 55.3% of the total energy consumption in China (National Bureau of Statistics of China). Traditional fossil fuels result in higher pollutant emissions, which, in turn, lead to increased penalties for companies that exceed pollution limits. To avoid these fines, profit-driven companies may adjust their input structures to reduce reliance on high-pollution, low-energy-value fuels. Improving coal energy efficiency or optimizing the energy mix is essential for reducing carbon emissions. Research has found that enhancing energy efficiency can lead to a 25% reduction in pollutant emissions57. The Environmental Protection Tax, which imposes taxes on pollutants such as sulfur dioxide, incentivize companies to adopt energy-saving and emission-reduction technologies. With strong government oversight and tax incentives, this policy is likely to drive innovations that improve energy utilization efficiency and reduce energy consumption per unit of GDP. Technological advancements and better optimization of the energy mix will lower carbon dioxide emissions per unit of fossil energy and increase the adoption of clean energy. Since fossil fuel combustion contributes to both pollutants and carbon emissions, improving energy efficiency or restructuring the energy mix can reduce both pollution and carbon emissions simultaneously27,28,29. Based on the above theory, the paper proposes research hypothesis 3:

Hypothesis 3

The Environmental Protection Tax effectively reduces carbon emissions by improving energy efficiency.

Reasonable environmental regulations can drive technological innovation, with such advancements helping to offset the costs of environmental governance (Porter and Van Der Linde, 1995)55. The Environmental Protection Tax encourages companies to use resources more efficiently, conserve energy, and improve production processes. By investing in pollution control technologies, green production methods, and research and development (R&D) in green technologies, companies can enhance market share, increase product value, and advance technological sophistication. Furthermore, the Environmental Protection Tax disrupts reliance on traditional, pollution-intensive industries, fostering innovation in green technologies and boosting total factor productivity in green sectors. This shift supports the development of higher-level industries59,60, transitioning towards technology-intensive sectors and facilitating carbon reduction through industrial upgrading. Additionally, the Environmental Protection Tax affects energy input prices and pollution costs, raising production costs for high-energy-consuming industries. This may lead to the reduction or closure of such industries, prompting firms to reallocate resources to cleaner, higher-return sectors, such as finance, services, or green industries. This optimization of resource allocation fosters a more rational industrial structure, increases the share of the tertiary sector, and reduces investment in high-carbon production. As a result, the tax promotes industrial upgrading, specialization, and the growth of emerging green industries, effectively lowering carbon emissions. Based on the above theory, the paper proposes research hypothesis 4.

Hypothesis 4

The Environmental Protection Tax effectively reduces carbon emissions by optimizing the industrial structure.

Research design

Data sources

This study uses panel data from 287 cities in China, spanning the period from 2009 to 2021, to examine the impact of the Environmental Protection Tax on regional carbon emissions. Since industrial production is a major source of carbon dioxide emissions and the financial crisis significantly impacted domestic industrial production and demand, the analysis begins in 2009. The data were sourced from the Express Professional Superior (EPS) database, the China Energy Statistical Yearbook, and the China City Statistical Yearbook. To ensure the robustness of the results, the data underwent 1% winsorization and logarithmic transformation for absolute indicators. The empirical analysis was conducted using STATA 15.0.

Variable selection

Explained variables

Urban carbon emissions encompass emissions from both direct energy consumption, such as gas and Liquefied Petroleum Gas (LPG), and indirect sources like electricity and heat consumption. The emissions from direct energy consumption can be calculated using the relevant conversion coefficients provided by IPCC2006 guidelines. Follow the existing research methods60the total carbon emissions of a city are determined by summing the emissions from electricity, gas, LPG, transportation, and thermal energy consumption. This approach is consistent with the calculations used in previous studies61,62,63.

Explanatory variables

The Environmental Protection Tax was officially implemented on January 1, 2018. To analyze its impact, we define a time dummy variable, post, where years after 2017 are assigned a value of 1, and all other years are assigned a value of 0. Additionally, we introduce a policy dummy variable, treat, where regions that experienced an increase in environmental protection tax rates on taxable pollutants are assigned a value of 1, otherwise, as to 065,66,67. The interaction term of these two variables, serves as the core explanatory variable in this study, capturing the net effect of the Environmental Protection Tax on regional carbon emissions. Most provinces raised their Environmental Protection Tax rates, and the corresponding municipal-level cities maintained the same rates as their provinces. However, some cities did not align with the provincial tax rates. For example, Hebei Province classified its cities into three categories: First-class cities with a tax rate of 9.6 yuan per kilogram, second-class cities with a tax rate of 6.6 yuan per kilogram, and third-class cities with a tax rate of 4.8 yuan per kilogram. The specific tax rates for provinces and cities are presented in Table 1. The treat variable is based on the environmental protection tax rates of individual cities.

Control variables

To ensure the accuracy of the empirical results, the study controls for various factors that may influence regional carbon emissions. Regions with more developed economies generally consume more energy, which can lead to higher carbon dioxide emissions. Therefore, the study includes controls for regional economic growth, represented by the logarithm of GDP. Since economic development is closely associated with industrial expansion, and service sector growth is positively related to carbon reduction, the study also controls for the development of these sectors. This is measured by the proportion of secondary industry value-added to GDP and the proportion of tertiary industry value-added to GDP, respectively. Trade development is another key driver of economic growth, so the study controls regional openness, captured by the ratio of total imports and exports to GDP. In line with the “pollution haven” hypothesis67,68which suggests that pollution-intensive industries are often located in regions with more lenient environmental regulations, the study controls for foreign direct investment (FDI), measured by the logarithm of actual foreign capital utilized. Population size, which reflects regional density and associated production activities, is controlled using the logarithm of the resident population. The study also controls for the regional tax burden, measured by the ratio of general budgetary revenue to GDP, as tax levels can influence business operations. Government intervention, which can affect regional production and operational behavior, is controlled by using the proportion of general budgetary expenditure to GDP. Finally, recognizing that passenger transportation contributes significantly to emissions, the study includes a control for passenger transport, measured by the logarithm of the number of taxis at year-end. Given the variation in Environmental Protection Tax rates across different regions, the study controls for the environmental protection tax rate (SO2). Before 2018, this was the pollutant discharge fee rate, and from 2018 onwards, it became the Environmental Protection Tax rate. Additionally, the study controls for provincial-level environmental protection tax (or pollutant discharge fee) revenue. Before 2018, this was revenue from pollutant discharge fees, and from 2018 onwards, it became revenue from environmental protection taxes. This revenue is logged to adjust for scale effects. Since energy structure plays a key role in regional carbon emissions, the study also controls for regional energy structure, using the ratio of coal consumption to total energy consumption as a proxy. The specific variable definitions are detailed in Table 2.

Table 3 presents the descriptive statistics for the variables, including the number of observations, means, standard deviations, minimum values, and maximum values. For carbon emissions, the minimum value observed during the sample period is 3.0032, while the maximum value reaches 9.523. The standard deviation of 1.1115 indicates considerable variability in carbon emissions across the different regions. This relatively large standard deviation underscores the significant differences in carbon emissions between regions in the study.

Model construction

To identify the actual impact of the Environmental Protection Tax on regional carbon emissions, this study employs a difference-in-differences (DID) model for analysis. The specific model specification is presented in Eq. (1):

.

In Eq. (1), \(\:\text{i}\) represents the city, and \(\:\text{t}\) represents the year. y is the dependent variable, which measures regional carbon emissions, expressed as the logarithm of regional carbon emissions. \(\:{\text{D}\text{I}\text{D}}_{\text{i}\text{t}}\) is the key explanatory variable, reflecting the Environmental Protection Tax, and is composed of two dummy variables: \(\:{\text{p}\text{o}\text{s}\text{t}}_{\text{t}}\) and \(\:{\text{t}\text{r}\text{e}\text{a}\text{t}}_{\text{i}}\). Specifically, \(\:{\text{p}\text{o}\text{s}\text{t}}_{\text{t}}\) takes the value of 1 for years after 2017, and 0 otherwise. \(\:{\text{t}\text{r}\text{e}\text{a}\text{t}}_{\text{i}}\) is set to 1 for regions that raised the tax rate on taxable pollutants, and 0 otherwise64,65,66. control includes a set of control variables, which account for factors such as economic development, industrial development, service sector growth, openness, foreign direct investment, population size, tax burden, government intervention, passenger transport, the Environmental Protection Tax rate (SO2), environmental tax (pollution fee) revenue, and energy structure. \(\:{year}_{t}\) represents year-fixed effects, controlling for macroeconomic factors and policy changes that affect all cities in a given year. \(\:{ciyt}_{i}\) represents city-fixed effects, which control for factors that do not change over time, such as city location and cultural factors. \(\:{\epsilon\:}_{it}\) is the error term.

Empirical results analysis

Baseline regression

Table 4 presents the impact of the Environmental Protection Tax on regional carbon emissions. Columns (1) and (4) display the results for the two-way fixed effects model, both without and with control variables, respectively. Columns (2) and (3) provide the results with time-fixed effects and city-fixed effects, both incorporating control variables. The empirical findings show that the Environmental Protection Tax significantly reduces regional carbon emissions, with results passing significance tests at the 5% level. This indicates that the implementation of the Environmental Protection Tax has a positive effect on regional carbon emission reduction. Using the estimated coefficient from Column (4) as a baseline, we estimate that the Environmental Protection Tax results in an average reduction of 10.63% in regional carbon emissions. Hypothesis 1 is thus verified, confirming that the Environmental Protection Tax can significantly decrease regional carbon emissions.

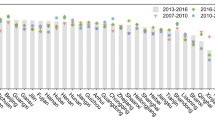

Parallel trend test

The parallel trend test is a critical aspect of ensuring that the results derived from the difference-in-differences (DID) model are unbiased. The baseline regression has already provided evidence that the Environmental Protection Tax significantly reduces carbon emissions. However, to confirm that this reduction can be attributed to the policy itself, the study uses an event study method to conduct the parallel trend test. The key assumption of the parallel trend test is that, before the policy’s implementation, the experimental and control groups should follow similar trends in carbon emissions. A significant divergence between the two groups after the policy is implemented indicates that the policy may have had an effect. Figure 1 presents the results of the parallel trend test. The findings indicate that, before the policy implementation, there was no significant difference in carbon emissions between the experimental group (cities where the Environmental Protection Tax rate increased) and the control group (cities where the tax rate remained unchanged). However, after the policy’s implementation, the experimental group experienced a significant reduction in carbon emissions, suggesting that the Environmental Protection Tax was effective in reducing emissions. These results support the parallel trend assumption, further validating the empirical findings and reinforcing the conclusion that the observed decrease in carbon emissions is indeed due to the implementation of the Environmental Protection Tax.

Parallel trend test.

Robustness test

Alternative administrative levels

In Column (1) of Table 5, the analysis excludes municipalities, sub-provincial cities, and provincial capital cities to account for the influence of these higher-level cities, which typically have superior economic development and social endowments compared to other cities. The findings indicate that, even after controlling for the higher administrative status of these cities, the Environmental Protection Tax still has a significant effect on reducing carbon emissions in the remaining cities. This suggests that the tax’s impact on carbon emissions is not solely driven by the economic and social advantages of these higher-level cities.

Alternative identification method

In the previous empirical strategy, the study classified cities that increased the tax rate on taxable pollutants under the Environmental Protection Tax as the treatment group, while the remaining cities were designated as the control group. However, in some cities, although the Environmental Protection Tax rate was not increased, stricter tax enforcement and enhanced environmental regulations were implemented. First, when companies evade or underpay the Environmental Protection Tax, they now face criminal penalties rather than just administrative fines. Even in regions that did not increase the tax rate, stricter environmental regulations are still enforced. Second, while some provinces did not raise the Environmental Protection Tax rate, they already had higher base rates in place. For instance, Tianjin (a municipality directly under the central government) maintained an Environmental Protection Tax rate of 6, while other provinces that did not raise their rates kept the rate at 1.2. Given these considerations, some provinces that did not increase their Environmental Protection Tax rates might still have experienced policy shocks. Therefore, the study uses an intensity-based difference-in-differences (DID) model for identification. Column (2) of Table 5 uses the 2017 Environmental Protection Tax rate as an intensity variable for analysis. Column (3) of Table 5 distinguishes between the treatment and control groups based on the median 2018 Environmental Protection Tax rate. Cities with tax rates above the median for taxable pollutants (1.8) are classified as the treatment group, while those below the median are classified as the control groupFootnote 3. The empirical results indicate that, even with these alternative identification methods, the Environmental Protection Tax continues to significantly reduce carbon emissions in cities.

Changing the explained variable

Column (4) of Table 5 addresses the potential influence of regional population factors by using per capita carbon emissions as the dependent variable. Per capita, carbon emissions are calculated by dividing total carbon emissions by the total population of the region. This adjustment allows the study to account for the population size and its potential impact on overall carbon emissions. The empirical results presented in Column (4) demonstrate that, even after controlling for population effects, the Environmental Protection Tax still significantly reduces carbon emissions in cities. This suggests that the observed reduction in carbon emissions is not merely a result of population differences across regions, but rather an effect directly attributable to the implementation of the Environmental Protection Tax.

Changing the clustering

In response to potential correlations among cities within the same province, which could be influenced by provincial policy documents, the study applies robust clustering at the provincial level to adjust for intra-provincial correlations. This approach ensures that the standard errors are more accurately estimated, accounting for the fact that cities within the same province may be exposed to similar provincial policies that could affect their carbon emissions. Column (5) of Table 5 presents the results with robust clustering at the provincial level. It is important to note that while the standard errors are adjusted in this specification, the estimated coefficients of the core explanatory variables remain unchanged. As such, the coefficients in Column (5) are consistent with those in Column (4) of Table 4, which presents the baseline regression results. The empirical findings show that, even after applying robust clustering at the provincial level, the Environmental Protection Tax continues to have a significant and negative impact on regional carbon emissions. This reinforces the reliability of the results, confirming that the observed reduction in carbon emissions can still be attributed to the implementation of the Environmental Protection Tax, even after addressing potential intra-provincial correlations.

PSM-DID

To address potential biases arising from the discretion that provincial governments have in setting Environmental Protection Tax rates, the study employs a more robust identification method: Propensity Score Matching with Difference-in-Differences (PSM-DID). This method is designed to account for the possibility that economically developed regions may opt for higher tax rates as a means to set an example, while less developed regions may avoid raising tax rates to prioritize economic growth. The PSM-DID method is implemented by first applying a Logit regression with 1:1 matching, using all control variables as covariates for the matching process. Cities that do not match well based on their propensity scores are excluded from the DID regression analysis, ensuring that the treated and control groups are more comparable. This matching process helps mitigate biases related to the decision of whether or not to raise the Environmental Protection Tax rates in different regions. Column (6) of Table 5 presents the results from the PSM-DID estimationFootnote 4. The findings confirm that, even after addressing this potential bias through matching, the Environmental Protection Tax still significantly reduces carbon emissions in cities. This provides further validation of the robustness of the results and reinforces the conclusion that the implementation of the Environmental Protection Tax leads to a meaningful reduction in regional carbon emissions.

Policy uniqueness test

In the study, several factors and policies that may influence carbon emissions are considered to ensure the robustness of the results and account for potential confounding effects. Column (1) of Table 6: This column excludes cities that participated in the carbon emissions trading pilot program, introduced in 2011 across seven provinces and cities. Since this market-based mechanism incentivizes enterprises to reduce carbon emissions, it could potentially affect the carbon dioxide emissions in those cities. By excluding these cities, the analysis isolates the impact of the Environmental Protection Tax from that of the emissions trading program. Column (2) of Table 6: This column shortens the study period to 2016–2020 to mitigate the potential effects of dynamic adjustments to pollution discharge fee standards, which were made by provinces and cities before 2015. This adjustment period may have affected emissions, and this column helps isolate the impact of the Environmental Protection Tax by excluding the earlier period. Column (3) of Table 6: The inclusion of a dummy variable for low-carbon cities in this column controls for cities with initiatives aimed at reducing emissions through low-carbon buildings, transportation, and emerging energy-saving industries. These cities may have already been undertaking significant efforts to reduce carbon emissions, so this variable accounts for their potential effect. Column (4) of Table 6: This column includes a dummy variable for innovative cities, which reflects the impact of technological innovation on reducing carbon emissions. Technological advancements can drive improvements in energy efficiency and production processes, potentially influencing the carbon emissions reduction observed in these cities. Column (5) of Table 6: This column controls for industrial clusters, which play a role in optimizing industrial structures and promoting low-carbon development. As industrial clusters often lead to economies of scale and specialization, they can influence the rate at which industries shift toward greener practices. Column (6) of Table 6: This column includes a control for the green finance reform pilot launched by the People’s Bank of China and other ministries in 2017. This initiative, which applies to certain regions such as Zhejiang, Jiangxi, Guangdong, Guizhou, and Xinjiang, could impact companies’ investments in green technologies due to the availability of green credit. By including this variable, the analysis controls for the potential influence of green finance policies. Despite controlling for these additional factors and related policies, the results consistently show that the Environmental Protection Tax remains effective in reducing regional carbon emissions. This strengthens the conclusion that the tax contributes significantly to the reduction of carbon emissions, independent of other policies and factors that might also play a role.

Placebo test

To address the potential influence of unobservable factors that could lead to spurious conclusions, this study employs a placebo test to assess the robustness of the empirical results. The placebo test involves randomly assigning policy implementation dates and selecting policy regions, with the regression process repeated 500 times. Figure 2A and B present the probability density of the estimated coefficients and p-values from the placebo tests, respectively. The figures show that the placebo test coefficients generally follow a normal distribution centered around a mean of zero. In contrast, the actual estimated coefficients significantly deviate from these placebo values, suggesting that the empirical results are robust and not due to random chance.

Placebo test.

IV Estimation

This study employs a Difference-in-Differences (DID) model to analyze the impact of the Environmental Protection Tax on regional carbon emissions. However, the increase in regional tax rates may be influenced by local environmental and economic factors, potentially leading to endogeneity. To address this concern, the study applies Instrumental Variables (IV) estimation. Drawing on the research design of Zhang et al. (2025), river density is used as an instrumental variable for the implementation of the Environmental Protection Tax policy. First, regions with higher river density tend to have larger water areas and stronger public oversight. As a result, local governments in these areas are more likely to adopt stricter pollution control measures due to public pressure. Therefore, regions with higher river density are more inclined to implement stricter Environmental Protection Tax policies, which in turn result in higher tax rates on taxable pollutants. This relationship satisfies the homogeneity assumption between river density and the Environmental Protection Tax rate. Second, river density is generally considered an exogenous factor, largely determined by large-scale weather systems, thus satisfying the homogeneity assumption between river density and urban carbon emissions. Given that river density data is cross-sectional, its direct use would prevent estimation in a two-way fixed effects model. To address this limitation, the study follows the existing methods by interacting river density with time dummy variables and constructing a time-varying river density instrumental variable (IV)69.

The estimation results in Table 7 show that the F-statistic of the first-stage regression is 1221.3452, which is significantly greater than the critical value of 10. The estimated coefficients of the instrumental variable are all significant, indicating a strong correlation between the instrument and the endogenous variable, thereby eliminating concerns about the “weak instrument” problem. The Kleibergen-Paap rk LM statistic passes the 1% significance test, rejecting the null hypothesis of “under-identification” of the instrument. This confirms the validity of the selected instrument. Furthermore, the coefficient of the core explanatory variable (DID) remains significantly negative and passes the 1% significance test, indicating that even after addressing potential endogeneity, the Environmental Protection Tax continues to significantly reduce regional carbon emissions.

Mechanism test

Green research and development

Column (1) of Table 8 examines the mechanism of the impact of green technological innovation. Green technological innovation is measured by the proportion of green patents in the region, with a higher value indicating stronger green technological innovationFootnote 5. As shown in Column (1), the Environmental Protection Tax significantly promotes green technological innovation, passing the 5% significance level test. The low-carbon transition requires technological progress, such as investments in green production equipment at the front end and carbon capture and storage at the end. The Environmental Protection Tax plays an important role in increasing investment in green research and development, thus supporting carbon reduction efforts. Hypothesis 2 is thus verified.

Energy efficiency

Column (2) of Table 8 examines the mechanism of energy efficiency. Energy efficiency is measured by the coal consumption per unit of energy in the region, where a smaller value indicates that less coal is consumed per unit of output, reflecting higher energy efficiency. From Column (2), it can be seen that the Environmental Protection Tax significantly improves regional energy efficiency, passing the 5% significance level test. Energy transition and improving energy efficiency are the primary ways to reduce greenhouse gas emissions, and the improvement in energy efficiency plays a key role in achieving the net-zero emission target. Hypothesis 3 is thus verified.

Industrial structure

Column (3) of Table 8 examines the mechanism of industrial structure. The industrial structure is measured by the ratio of the value-added of the tertiary sector to the value-added of the secondary sector, where a higher value indicates that the regional industrial structure has been optimized and upgraded. From Column (3), it can be seen that the Environmental Protection Tax significantly promotes the optimization and upgrading of the industrial structure, passing the 5% significance level test. The implementation of the Environmental Protection Tax imposes pressure on high-pollution enterprises while also fostering the development of green emerging industries, which is of significant importance for regional carbon reduction. Hypothesis 4 is thus verified.

Heterogeneity analysis

Regional heterogeneity

China is vast, with diverse resource endowments and varying levels of economic development across regions. Specifically, the eastern region includes Hebei, Liaoning, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong, and Hainan; the central region includes Shanxi, Jilin, Heilongjiang, Anhui, Jiangxi, Henan, Hubei, and Hunan; the western region includes Inner Mongolia, Guangxi, Sichuan, Guizhou, Yunnan, Tibet, Shaanxi, Gansu, Qinghai, Ningxia, and XinjiangFootnote 6. Table 9 reports results based on regional heterogeneity. The findings indicate that the Environmental Protection Tax has a significant impact on reducing carbon emissions in the eastern region, passing the 5% significance level test, while its effect on the central and western regions is not as pronounced. The possible reasons for this discrepancy are as follows: the eastern region is primarily composed of high-end manufacturing and service industries, but traditional high-energy-consuming industries still account for a certain proportion. These enterprises have a large base of pollutant emissions, making them more sensitive to the marginal cost of the Environmental Protection Tax, thereby forcing them to accelerate technological upgrades or exit the market. Additionally, environmental protection tax rates in eastern provinces are generally higher (for example, the air pollutant tax rate in the Beijing-Tianjin-Hebei region is set at 9.6 yuan per pollution equivalent, close to the national maximum), and government oversight is stricter. In contrast, the central and western regions have smaller energy-consuming industries and relatively lower environmental protection tax rates, which explains the significant regional differences in the impact of the Environmental Protection Tax on carbon reduction.

Industrial regional heterogeneity

The rapid industrialization of China has been a key driver of its economic growth, with industrial development playing a significant role in the increase of carbon dioxide emissions. This study examines the heterogeneous effects of the Environmental Protection Tax on different industrial regions, specifically comparing the old industrial areas with the non-old industrial areasFootnote 7. Columns (1) and (2) of Table 10 present the differential impacts of the Environmental Protection Tax on these regions. The results show that the tax significantly reduces carbon emissions in non-old industrial areas, with the effect passing the 5% significance level test. However, the Environmental Protection Tax does not have a significant impact on carbon emissions in old industrial areas. Old industrial areas, which were primarily developed during the planned economy era with state investments, have relatively complete industrial sectors. These regions are often highly resource-dependent and constrained by their existing infrastructure, making it more challenging to implement substantial technological upgrades. In contrast, non-old industrial areas typically have better access to modern technologies and greater innovation potential, enabling them to more effectively reduce carbon emissions. Consequently, the Environmental Protection Tax has a more pronounced effect on carbon emission reduction in non-old industrial areas.

Government attention heterogeneity

Government attention refers to the selective focus of decision-makers on significant issues while disregarding others. The allocation of government attention plays a crucial role in national strategic development and the effectiveness of macroeconomic policies. Specifically, attention to environmental issues directly influences local governments’ environmental governance. In China, the “Government Work Report” is a key policy document that reflects the government’s administrative direction and priorities, guiding resource allocation and social development. It acts as a “command baton” for setting and adjusting governmental focus. In contrast, local government work reports reflect the policy goals of local leaders and demonstrate how attention is allocated at the regional level70. Based on the currently used methods71this study measures the intensity of local government environmental regulation by counting the number of environment-related terms in annual government work reports. Keywords include terms such as “environment,” “energy consumption,” “pollution,” “emission reduction,” “environmental protection,” “pollutant emissions,” “ecology,” “green,” “low carbon,” “air,” “smog,” “carbon dioxide,” “sulfur dioxide,” “PM10,” and “PM2.5.” The intensity of government attention is quantified by the total number and proportion of these 15 environmental terms mentioned in the reports. Regions with a higher proportion of these terms than the median are classified as having strong government attention, while others are classified as having weak government attention. Columns (1) and (2) of Table 11 examine the heterogeneity of the environmental protection tax’s impact based on government attention. The results show that in regions with strong government attention to environmental issues, the environmental protection tax significantly reduces carbon emissions. In contrast, in regions with weaker government attention, the carbon reduction effect of the environmental protection tax is not significant.

Energy-intensive heterogeneity

Table 12 examines the heterogeneous effects of the Environmental Protection Tax on carbon emissions across different energy consumption sectors (energy-intensive industries). Due to the lack of detailed carbon emissions and energy consumption data from publicly listed companies in China, this study cannot effectively assess the tax’s impact on specific industries (such as the service industry and energy-intensive sectors). To address this, the study classifies regions based on energy consumption intensity at the city level (measured as coal consumption per unit of GDP) to distinguish between energy-intensive and non-energy-intensive regions. Regions with coal consumption per unit of GDP greater than the median are classified as energy-intensive, while those below the median are classified as non-energy-intensive. Columns (1) to (2) of Table 12 estimate this heterogeneity. The results show that in energy-intensive regions, the Environmental Protection Tax significantly reduces carbon emissions. In contrast, the carbon reduction effect is not significant in non-energy-intensive regions. This further confirms that the Environmental Protection Tax has a more pronounced impact on emission reductions in high-energy-consumption, high-pollution areas, effectively encouraging enterprises in energy-intensive regions to enhance pollution control and transition to greener practices.

Conclusion and discussion

Conclusion

This paper utilizes panel data from 287 cities spanning the period from 2009 to 2021 to construct a Difference-in-Differences (DID) empirical framework to evaluate the impact of the Environmental Protection Tax on regional carbon emissions. The empirical analysis reveals that the Environmental Protection Tax effectively promotes carbon emission reductions and drives the green transformation of regional economies through various channels. Specifically, the tax encourages regions to invest in green R&D innovation, improve energy efficiency, and optimize industrial structures, resulting in an average reduction of 5.63% in carbon emissions. These findings underscore the policy’s significant role in promoting sustainable development and reducing emissions, demonstrating notable cross-regional adaptability. However, the study also identifies regional heterogeneity in the effectiveness of the Environmental Protection Tax. The tax has a more pronounced carbon reductioneffect in the eastern regions, non-old industrial areas, and regions with stronger government attention, and energy-intensive areas. In contrast, in the centraland western regions, old industrial bases, and areas with weaker government focus, and Non-energy-intensive areas, the tax’s impact on carbon emissions isless substantial. Furthermore, the Environmental Protection Tax not only aids in carbon reduction but also has a positive effect on urban environmental quality, reducing pollutant emissions, improving air quality, and enhancing residents’ subjective well-being. These results highlight the broader social benefits of green development.

Discussion

To effectively address carbon emissions and promote environmental sustainability, several key measures must be implemented. First, enforcement of the environmental protection tax should be strengthened the enforcement of the environmental protection tax and more reasonable and region-specific tax rates. Currently, some provinces apply the minimum tax rate, which limits its potential for reducing emissions. To further incentivize carbon reduction, tax rates should be gradually increased, particularly in lower-income regions. Additionally, region- and industry-specific pricing structures should be developed to promote coordinated development across various sectors. The establishment of an information tax collection system will also enhance regulatory efficiency and compliance, ensuring the effective enforcement of environmental tax policies. Second, it is necessary to strengthen the collaborative governance system for pollution reduction and carbon mitigation. This includes enhancing coordination between the Ministry of Ecology and Environment, the National Development and Reform Commission, and energy-related departments. A unified governance platform should be established to ensure the simultaneous development and implementation of policies addressing climate change and air pollution. It is also important to improve joint emission reduction policies and evaluation mechanisms. This would involve setting joint reduction targets for carbon emissions and air pollutants, encouraging coordinated reductions in high-emission industries such as electricity, steel, and transportation. Furthermore, local governments should be held accountable for their performance, integrating carbon reduction and pollutant reduction into their performance assessments. A strict accountability system should be implemented to ensure policy enforcement. Optimizing the linkage between carbon markets and pollution control mechanisms is also crucial. Expanding the coverage of carbon markets to include additional sectors such as energy, industry, and buildings, and setting joint reduction targets, would promote the simultaneous reduction of carbon emissions and air pollutants. Strengthening the price signals in the carbon market will incentivize enterprises to reduce both carbon emissions and pollutant emissions. Third, technological innovation plays a pivotal role in carbon reduction efforts. The government should actively guide enterprises to invest in environmental management and technological advancement. Increasing research and development (R&D) efforts, cultivating talent in green technologies, and encouraging innovation are essential to driving progress. Financial support, tax incentives, and green subsidies should be provided to companies involved in environmental technologies and R&D to reduce innovation risks and accelerate the transition to greener technologies. Fourth, optimizing the energy structure is crucial for reducing emissions. Efforts should be made to explore and develop renewable energy sources, increase the share of clean energy in the overall energy mix, and improve energy efficiency. Environmental protection tax policies should be aligned with these objectives by internalizing environmental costs and correcting distorted energy price signals. Promoting the use of renewable energies such as wind and solar power, alongside the adoption of cleaner coal technologies, will further drive emissions reductions. Finally, strengthening top-level design is necessary to optimize the national industrial structure. There should be deliberate efforts to reduce over-reliance on the secondary sector, promote the development of the tertiary sector, and decrease overall energy consumption. This will help transition to a more sustainable, low-carbon economy. By aligning industrial policies with carbon reduction goals, China can foster green growth while achieving carbon decoupling from economic expansion.

Although this study provides valuable insights into the impact of the environmental protection tax on regional carbon emissions in China, several limitations should be considered. First, the research focuses exclusively on the effects of the environmental protection tax within China, and as such, the generalizability of its findings to other developing or developed countries remains unexamined. Different nations possess distinct political, economic, and industrial contexts, which could result in varying outcomes from similar environmental tax policies. Future research could extend this analysis to other countries, offering a comparative perspective on the effectiveness of environmental protection taxes in diverse settings. Second, while the study primarily examines the impact of the environmental protection tax on regional carbon emissions, it does not fully explore the underlying mechanisms through which the tax influences emissions at the micro-enterprise level. While the regional effects of the tax are clear, the micro-level mechanisms, especially for small and medium-sized enterprises (SMEs), remain underexplored. Data limitations, such as challenges in obtaining carbon emission data for publicly listed companies and the lack of data for smaller enterprises beyond 2016, hinder a more in-depth analysis of these mechanisms. Future studies should investigate how the environmental protection tax affects emission reductions within micro-enterprises and SMEs, focusing on factors such as technological innovation, production processes, and resource allocation. This would provide more granular insights into how environmental taxation can stimulate carbon reductions across businesses of different scales. Lastly, urban carbon emissions and environmental protection policies may exhibit spatial spillover effects, particularly concerning the issue of pollution industry relocation. This study solely considers the impact of the environmental protection tax on local carbon emissions, without accounting for the spatial spillover effects induced by the potential relocation of polluting industries. Future research could address this by incorporating spatial Difference-in-Differences (DID) or spatial Durbin models to examine the policy linkages and carbon emission effects in neighboring cities. In summary, while this study significantly contributes to understanding the role of the environmental protection tax in reducing carbon emissions, addressing these limitations in future research could help refine emission reduction strategies and expand their applicability across different countries and business sectors.

Data availability

Data will be made available on request. The data that support the findings of this study are openly available in https://www.epsnet.com.cn/index.html#/Index.

Notes

The “dual control” of emissions refers to the simultaneous control of both total carbon emissions and carbon emission intensity.

The article summarizes the fourth conclusion in the Conclusion section as “Additional benefits of the tax.” The specific empirical results can be found in Appendix 2.

The setting for the treatment variable treat in this model is as follows: cities with an Environmental Protection Tax rate greater than the median of 1.8 in 2018 are assigned a value of 1, while those below the median are assigned a value of 0. The setting for post remains consistent with Eq. (1), while the setting for treat is based on the Environmental Protection Tax rate for each city.

The appendix reports the results of the matching balance test, which shows that all variables have passed the balance test. This indicates that the propensity score matching process has successfully balanced the covariates between the treatment and control groups, ensuring that the groups are comparable before applying the Difference-in-Differences (DID) methodology.

The regional green patent data is sourced from https://www.cnrds.com/.

There are a total of 34 provincial-level administrative regions in China, and Hong Kong, Macao and Taiwan, China, are not included in the sample. In addition, the sample excludes the Tibet Autonomous Region (TAR) due to its truly severe sample.

Old industrial areas refer to specific regions within cities that host a relatively high concentration of industrial enterprises. These areas were primarily established during the “Eleventh Five-Year Plan,” “Twelfth Five-Year Plan,” and the “Third Line” construction periods. They played a crucial role in the development of China’s independent and comprehensive industrial system and made significant contributions to the formation and growth of old industrial cities. Despite their historical significance, these areas remain vital for local economic and social development.

References

Li, W. et al. Combined effects of elevated carbon dioxide and temperature on phytoplankton-zooplankton link: A multi-influence of climate change on freshwater planktonic communities. Sci. Total Environ. 658, 1175–1185 (2019).

Mahajan, M. & Sah, A. Understanding the cyclical patterns of carbon dioxide emissions to mitigate climate change: evidence from the QUAD countries. J. Clean. Prod. 434, 140129 (2024).

Kumar, N. & Maiti, D. Long-run macroeconomic impact of climate change on total factor productivity — Evidence from emerging economies. Struct. Change Econ. Dyn. 68, 204–223 (2024).

Han, W., Chen, Z., Wu, X. & Xie, X. Can a carbon trading system promote the transformation of a low-carbon economy under the framework of the Porter hypothesis? -Empirical analysis based on the PSM-DID method. Energy Policy. 129, 930–938 (2019).

Kong, D. & Qin, N. Does environmental regulation shape entrepreneurship?? Environ. Resour. Econ. 80, 169–196 (2021).

Ji, S., Jiang, F., Li, J., Wang, Y. & Zhang, W. Assessment of the performances of pollutant discharge fee in China. Ecol. Indic. 125, 107468 (2021).

Dong, K., Shahbaz, M. & Zhao, J. How do pollution fees affect environmental quality in china?? Energy Policy. 160, 112695 (2022).

Yu, Y. J., Dai, C., Wei, Y., Ren, H. & Zhou, J. Air pollution prevention and control action plan substantially reduced PM2.5 concentration in China. Energy Econ. 113, 106206 (2022).

Lu Can the central environmental protection inspection reduce transboundary pollution? Evidence from river water quality data in China. J. Clean. Prod. 332, 130030 (2022).

Chen, Z., He, Y. & Liao, N. Can carbon emission trading policy enhance the synergistic emission reduction of carbon dioxide and air pollutants? A comparative study considering different pollutants. Energy 305, 132364 (2024).

Hunag, X. & Tian, P. How does heterogeneous environmental regulation affect net carbon emissions: Spatial and threshold analysis for China. J. Environ. Manage. 330, 117161 (2023).

Ai, H., Tan, X., Zhou, S., Zhou, Y. & Xing, H. The impact of environmental regulation on carbon emissions: evidence from China. Econ. Anal. Policy. 80, 1067–1079 (2023).

Jiang, Z., Liu, Z., Wang, T. & Zhang, X. The impact of environmental regulation on green TFP:A quasi-natural experiment based on china’s carbon emissions trading pilot policy. Energy 306, 132357 (2024).

Tang, Y., Hu, Y. & Cui, A. Research on the synergistic effects of market-oriented environmental regulations on pollution and carbon emission reduction. J. Environ. Manage. 380, 125115 (2025).

Xu, Y., Wen, S. & Tao, C. Impact of environmental tax on pollution control: A sustainable development perspective. Econ. Anal. Policy. 79, 89–106 (2023).

Cui, G. F. How do environmental taxes affect the environmental investment of high-emission enterprises: evidence from China. J. Environ. Manage. 370, 122629 (2024).

Liu, J. X. Can environmental taxes and green technological investment ease environmental pollution in china?? J. Clean. Prod. 474, 143611 (2024).

Hassan, M., Oueslati, W. & Rousselière, D. Environmental taxes, reforms and economic growth: an empirical analysis of panel data. Econ. Syst. 44, 100806 (2020).

Yamazaki, A. Environmental taxes and productivity: lessons from Canadian manufacturing. J. Public. Econ. 205, 104560 (2022).

Wang, X., Wang, S., Wu, K., Zhao, C. & Li, L. Environmental protection tax and enterprises’ green technology innovation: evidence from China. Int. Rev. Econ. Financ. 96, 103617 (2024).

Lu, S. & Yang, Q. Price of going green: the employment effects of the environmental protection tax in China. China Econ. Rev. 87, 102244 (2024).

Iida, T. & Mukherjee, A. Environmental taxes, offshoring and welfare: the effects of environmental damage and pollution intensity. J. Environ. Econ. Manage. 130, 103075 (2025).

Ghaith, A. & Epplin, F. Consequences of a carbon tax on household electricity use and cost, carbon emissions, and economics of household solar and wind. Energy Econ. 67, 159–168 (2017).

Dechezleprêtre, A., Nachtigall, D. & Venmans, F. The joint impact of the European union emissions trading system on carbon emissions and economic performance. J. Environ. Econ. Manage. 118, 102758 (2023).

Gugler, K., Haxhimusa, A. & Liebensteiner, M. Carbon pricing and emissions: causal effects of britain’s carbon tax. Energy Econ. 121, 106655 (2023).

Ahmad, M., Li, X. & Wu, Q. Carbon taxes and emission trading systems: which one is more effective in reducing carbon emissions?—A meta-analysis. J. Clean. Prod. 476, 143761 (2024).

Xu, L., Fan, M., Yang, L. & Shao, S. Heterogeneous green innovations and carbon emission performance: evidence at china’s City level. Energy Econ. 99, 105269 (2022).

Khurshid, A., Rauf, A., Qayyum, S., Calin, A. & Duan, W. Green innovation and carbon emissions: the role of carbon pricing and environmental policies in attaining sustainable development targets of carbon mitigation—evidence from Central-Eastern Europe. Environ. Dev. Sustain. 25, 8777–8798 (2022).

Liao, T., Yan, J. & Zhang, Q. The impact of green technology innovation on carbon emission efficiency: the intermediary role of intellectual capital. Int. Rev. Econ. Financ. 92, 520–532 (2024).

Luo, Y., Mensah, C., Lu, Z. & Wu, C. Environmental regulation and green total factor productivity in china: A perspective of porter’s and compliance hypothesis. Ecol. Indic. 145, 109744 (2022).

Wei, R., Wang, M. & Xia, Y. Environmental protection tax and corporate carbon emissions in china: a perspective of green innovation. Clean. Technol. Environ. Policy. 26, 2625–2641 (2024).

Du, J., Li, Z., Shi, G. & Wang, B. Can environmental protection fee to tax reduce carbon emissions? Evidence from China. Financ Res. Lett. 62, 105184 (2024).

Liu, A., Dai, S. & Wang, Z. Environmental protection tax on enterprise environmental, social and governance performance: A multi-perspective analysis based on financing constraints. J. Asian Econ. 89, 101671 (2023).

Zhang, Y., Xia, F. & Zhang, B. Can Raising environmental tax reduce industrial water pollution? Firm-level evidence from China. Environ. Impact Assess. Rev. 101, 107155 (2024).

Wang, L., Ma, P., Song, Y. & Zhang, M. How does environmental tax affect enterprises’ total factor productivity? Evidence from the reform of environmental fee-to-tax in China. J. Clean. Prod. 413, 137441 (2023).

Wang, X. & Ye, Y. Environmental protection tax and firms’ ESG investment: evidence from China. Econ. Model. 131, 106621 (2024).

Niu, T., Yao, X., Shao, S., Li, D. & Wang, W. Environmental tax shocks and carbon emissions: an estimated DSGE model. Struct. Change Econ. Dyn. 47, 9–17 (2018).

Fu, Y., Huang, G., Liu, L. & Zhai, M. A factorial CGE model for analyzing the impacts of stepped carbon tax on Chinese economy and carbon emission. Sci. Total Environ. 795, 143512 (2021).

Zhang, X. & Fan, D. Research on the synergistic emission reduction effect of carbon emission trading and green financial policy. J. Environ. Manage. 367, 121924 (2024).

Yang, S., Jahanger, A., Hu, J. & Awan, A. Impact of china’s carbon emissions trading scheme on firm-level pollution abatement and employment: evidence from a National panel. Energy Econ. 136, 107744 (2024).

Gan, T., Zhou, Z., Li, S. & Tu, Z. Carbon emission trading, technological progress, synergetic control of environmental pollution and carbon emissions in China. J. Clean. Prod. 442, 141059 (2024).

Xian, B., Wang, Y., Xu, Y., Wang, J. & Li, X. Assessment of the co-benefits of china’s carbon trading policy on carbon emissions reduction and air pollution control in multiple sectors. Econ. Anal. Policy. 81, 1322–1335 (2024).

Wang, F., Wu, M. & Zheng, W. What are the impacts of the carbon peaking and carbon neutrality target constraints on china’s economy? Environ. Impact Assess. Rev. 101, 107107 (2023).

Yu, M. & An, P. How much financing China needs to achieve carbon peak and carbon neutrality goals? Energy Econ. 137, 107791 (2024).

Yu, Z., Wang, Z., Ma, L. & Ma, M. Energy-saving targets and carbon neutrality: A perspective on carbon emissions and carbon substitution in 288 Chinese cities. J. Environ. Manage. 356, 120523 (2024).

Wang, P., Huang, G., Li, Y., Liu, Y. & Li, Y. An ecological input-output CGE model for unveiling CO2 emission metabolism under china’s dual carbon goals. Appl. Energy. 365, 123277 (2024).

Yu, H. et al. Environmental regulation and corporate tax avoidance: A quasi-natural experiments study based on china’s new environmental protection law. J. Environ. Manage. 296, 113160 (2021).

Liu, G., Yang, Z., Zhang, F. & Zhang, N. Environmental tax reform and environmental investment: A quasi-natural experiment based on china’s environmental protection tax law. Energy Econ. 109, 106000 (2022).

Ren, Y., Hu, G. & Wan, Q. Environmental protection tax and diversified transition of heavily polluting enterprises: evidence from a quasi-natural experiment in China econ. Anal. Policy. 81, 1570–1592 (2024).

Zhang, X., Liu, Y., Yu, S., Lin, O. & Meng, L. Impact of environmental protection tax on enterprise digital transformation: evidence from Chinese listed firms. Int. Rev. Econ. Financ. 97, 103743 (2025).

Shao, Y. & Cheng, Y. Impact of Chinese environmental protection tax law on high-pollution firms’ employment growth - A quasi natural experiment. Econ. Anal. Policy. 86, 416–437 (2025).

Song, W., Han, X. & Liu, Q. Patterns of environmental regulation and green innovation in China. Struct. Change Econ. Dyn. 71, 176–192 (2024).

Yan, Z., Yu, Y., Du, K. & Zhang, N. How does environmental regulation promote green technology innovation? Evidence from china’s total emission control policy. Ecol. Econ. 219, 108137 (2024).

Porter, M., Van, D., Linde, C. & Toward a new conception of the environmentcompetitiveness relationship. J. Econ. Perspect. 9, 97–118 (1995).

Yang, Y., Zhang, Y., Zhang, Y., Liu, T. & Xu, H. Environmental taxes promote the synergy between pollution and carbon reduction: provincial evidence from China. J. Environ. Manage. 372, 123378 (2024).

Wang, Y. F., Zhao, H., Shi, M., Liu, J. & Tan, Z. Public environmental concern, government environmental regulation and urban carbon emission reduction—Analyzing the regulating role of green finance and industrial agglomeration. Sci. Total Environ. 924, 171549 (2024).

Cadoret, I. & Padovano, F. The political drivers of renewable energies policies. Energy Econ. 56, 261–269 (2016).

Song, Y., Zhang, X. & Zhang, M. The influence of environmental regulation on industrial structure upgrading: based on the strategic interaction behavior of environmental regulation among local governments. Technol. Forecast. Soc. Change. 170, 120930 (2021).

Lu, W., Wu, H., Yang, S. & Tu, Y. Effect of environmental regulation policy synergy on carbon emissions in China under consideration of the mediating role of industrial structure. J. Environ. Manag. 322, 116053 (2022).