Abstract

This study aims to offer insight on the national cultural differences, public health expenditures, and economic freedom that persisted in life insurance expenditure across 28 advanced economies and 21 emerging and developing economies from 2002 to 2017. Our system GMM estimator’s analysis reveals that cultural factors, public health spending, economic freedom, financial development, human development, life expectancy, dependency ratio, and the Muslim religion are the major determinants of life insurance consumption at the aggregate level (i.e., for all sample economies). Between the group of advanced economies and the group of emerging and developing economies, these results, however, differ dramatically. It is noteworthy that cultural factors, such as masculinity and uncertainty avoidance, do not account for life insurance spending in advanced economies but have a statistically significant impact on life insurance consumption in emerging and developing economies. One point of interest is that our findings demonstrate that consumers in advanced nations as well as emerging and developing economies with a higher degree of public health spending and economic freedom tend to spend more on life insurance products. Both international life insurance businesses and governments from all around the world can benefit from the findings.

Similar content being viewed by others

Introduction

Both life insurance and non-life insurance play a significant role in economic growth and sustainable development due to their special property of risk diversification and the large pool of funds that they produce which can fuel business activities (Patrick 1966; Arena 2008; Lee 2011). Patrick (1966) claimed that the development of the financial services sector, including contributions from life and non-life insurance, contributed significantly to the economy growth. In particular, during the COVID-19 pandemic, the insurance industry made an essential contribution to the economic activities. Goodell (2020) mentioned that foreseeable pandemics such as COVID-19 are insurable. Subsequent analyses by Arena (2008), Haiss and Sümegi (2008), Curak et al. (2009), Chen et al. (2012), Outreville (2013), Lee et al. (2013), and Sawadogo et al. (2018), which are based on data samples from different countries in different periods, all confirm the positive influence of the development of the life insurance market on the economic growth. In this perspective, it is important to understand what drives the development of insurance spending, as this in turn can help participants in this sector (insurers and their customers and governments) to formulate their decision-making process better.

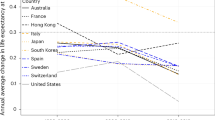

Whilst there have been some limited attempts to explain the determinants of non-life insurance demand (see our literature review in the next section), there have been very few papers devoted exclusively to socio-economic drivers impacting life insurance purchases across economies despite its health-socio-economic significance. As Swiss Re (2019) reported, global total life insurance premiums amounted to US$2820.18 billion in 2018, representing 3.22% of the world GDP. However, life insurance development differs greatly across economies. For instance, the life insurance’s premiums per capita was US$0.30 for Angola, but US$8204.30 for Hong Kong in 2018 (Swiss Re 2019). Life insurance consumption even differs considerably among economies with a comparable degree of per capita GDP. For example, even though both nations’ per capita GDPs were similar, Hong Kong’s average life insurance premiums in 2018 were 22 times higher than New Zealand’s. Figure 1 shows the trends of the average premium per capita for the life insurance consumption in all sample countries and per capita income. (See Table A2 for the list of these economies). Notably, after 2007, both average life insurance spending and per capita GDP changed. Figure 2 depicts the trends of the average premium per capita for the life insurance consumption in advanced countries, as well as emerging and developing economies. This further indicates that the patterns of life insurance expenditure are also different over time in these two groups of economies.

Source: Computed by the authors using data from Swiss Re (2019).

A number of earlier studies have investigated determinants of life insurance spending both theoretically and empirically (e.g. Yaari 1965; Hammond et al. 1967; Fischer 1973; Headen and Lee 1974; Beenstock et al. 1986; Browne and Kim 1993; Outreville 1996; Beck and Webb 2003; Li et al. 2007; Park and Lemaire 2011; Dragoş et al. 2017; Lee et al. 2018). These studies conclude that socio-economic drivers such as income, financial development, human development, inflation, education, life expectancy and social security contribution are the key factors of life insurance spending. However, heterogeneities associated with those factors as highlighted by previous papers can be attributable to other factors of the life insurance consumption. Cultural factors, particularly the latest cultural dimensions of Hofstede et al. (2010), and Minkov (2011), can be among the potential candidates. Trinh et al. (2021) claimed that these dimensions represent specific characteristics of individuals, and they can affect the perception of risks on the insurance consumption. In addition, Outreville (2018) mentioned that cultural traits can influence the perceived risk amount, and also impact people’s attitudes.

To the best of our knowledge, national culture has received little attention in the literature concerning the determinants of the life insurance spending. The only exceptions are three recent papers by Chui and Kwok (2008), Park and Lemaire (2011) and Outreville (2018), which attempt to investigate the determinants of life insurance spending across economies. However, as we mentioned above, newly introduced cultural dimensions by Hofstede et al. (2010), and Minkov (2011), specifically indulgence and hypometropia, have been excluded from these studies. These cultural factors represent the level of optimism and violence in countries and may thus explain the life insurance spending pattern. Neglecting them may lead to the issue of endogeneity owing to the omitted variables.Footnote 1 In addition, the cross-sectional dependence issue has been ignored by these papers.

Public health spending can also be another main driver in expanding life insurance consumption across economies. The positive effects of public health expenditure on economic growth, health outcomes and per capita income have been confirmed by several studies (e.g., Anand and Ravallion, 1993; Self and Grabowski, 2003; Amaghionyeodiwe 2008; Rizk 2012; Edeme et al. 2017; Boachie et al. 2018; Ifa and Guetat 2019; Patrick et al. 2020; Mustafa et al. 2021; Torche and Rauf 2021). Although there does not seem to be a direct link between the influence of public health expenditure life insurance purchases, a rise of wealth and income due to health improvements may impact the intention of individuals on life insurance consumption. Similarly, economic freedom can impact life insurance consumption because changes in economic freedom can lead to changes in the market price of life insurance products as well as income improvement. In addition, economic freedom can affect the life satisfaction or happiness of individuals, hence it may influence individuals’ demand for life insurance products.Footnote 2 To the best of our knowledge, there are not many papers devoted exclusively to cultural factors, public health expenditure and economic freedom that influence life insurance purchases across countries.

In this empirical study, we undertake a comprehensive empirical analysis of factors impacting life insurance spending based on a panel dataset encompassing 28 advanced countries and 21 emerging and developing countries during the period from 2002 to 2017. At the aggregated level (that is, for all countries), our GMM estimator-based analysis finds a rich list of factors influencing life insurance consumption, including economic indicators such as public health expenditure, economic freedom, financial development, human development index, life expectancy, dependency ratio, and Muslim region, as well as cultural variables such as indulgence, individualism, masculinity and uncertainty avoidance. However, the influences of these drivers differ noticeably between advanced, emerging and developing economies, proposing that the heterogeneity among economies may play a significant role in terms of the development level. Notably, cultural variables, namely masculinity and uncertainty avoidance, fail to explain life insurance spending in advanced economies, whereas these variables present a significant influence on life insurance expenditure in emerging and developing countries. Our study is the first to endeavour an international comparison of factors influencing life insurance purchases across a cluster of economies, segmented based on their level of development.

Our paper has contributed to the existing literature in several ways. First, it uses a system GMM estimator, which allows the treatments of the potential endogeneity problem, and the cross-sectional dependence issue in earlier studies has been adopted, to incorporate a thorough empirical framework of the determinants influencing life insurance spending across economies. Second, we extend our results to compare between two groups of economies based on the development level, advanced economies and emerging and developing economies, and have identified key differences in the way in which those drivers of life insurance spending behave. Third, we utilise the latest and comprehensive cultural data from Minkov (2011) and Hofstede et al. (2010) in our empirical analysis, including newly-developed cultural dimensions such as hypometropia and indulgence which have been neglected in previous studies. Finally, we examine how economic freedom and public health spending impact the life insurance expenditure pattern at the international level. Our results provide important information for government policies as well as business firms who are involved in the life insurance markets. Specifically, they propose a spectrum of policy recommendations for life insurers intending to penetrate new markets. Additionally, they could assist governments worldwide in revising their regulations and policies to foster the life insurance market, which is a cornerstone of prosperity and economic growth.

The subsequent sections of this paper are structured as follows: Section 2 offers an overview of relevant literature. Section 3 introduces the data, methodology, and hypotheses. Empirical results, discussions, and implications are covered in Section 4. The paper concludes with final remarks in Section 5.

Literature review

A number of previous studies have investigated determinants of life insurance consumption in both theoretical models and empirical regressions.Footnote 3 On the theoretical front, many models about the demand for life insurance have been developed by Yaari (1965), Fischer (1973), Headen and Lee (1974), Bernheim (1991) and Meier (1998).

Yaari (1965) applies a continuous time model and proves that customers can separate the spending decision from the bequest decision when life insurance is available to them. Fischer (1973) uses a discrete-time model to examine life-cycle patterns of expenditure, saving and insurance purchases. The author found that the probability of death has a positive effect on the life expenditure while an individual living from the proceeds of his/her wealth may not purchase the life insurance. Headen and Lee (1974) applied the model which was derived from a cost model of the process of portfolio adjustment and concluded that the life insurance demand function would consider factors including savings and financial market price conditions. Bernheim (1991) found that purchasing life insurance has an increase in the presence of social security annuity among elderly individuals. The author also provided evidence of the link between life insurance consumption and total resources. Meier (1998) studied the interaction between life insurance and long-term care insurance markets, concluding that an individual would invest in life insurance only if they are not overly wealthy and are sufficiently altruistic. Meier also proved that both life insurance and long-term insurance consumption will increase if the utility shock arising from disability declines.

On the empirical front, Hammond et al. (1967) seem to be the first to examine the determinants of life insurance consumption. The authors found that differences in households’ income strongly contribute to variations in life insurance expenditure. They revealed that households with higher net worth may increase life insurance product spending and factors such as education, age, and race significantly explain life insurance expenditure. This approach has been adopted by various authors (e.g. Beenstock et al. 1986; Browne and Kim 1993; Outreville 1996; Beck and Webb 2003; Li et al. 2007; Park and Lemaire 2011; Sen and Madheswaran 2013; Zerriaa and Noubbigh 2016; Alhassan and Biekpe 2016; Emamgholipour et al. 2017; Dragos et al. 2017; Lee et al. 2018; Outreville 2018; Sanjeewa et al. 2019; Dragoş et al. 2019; Akhter et al. 2020; Gaganis et al. 2020) who have explored factors of life insurance consumption by incorporating a wider set of explanatory variables in their analyses.

Cultural factors

Several related studies (e.g., Mooij 2003; Johar et al. 2006) have argued that culture can significantly impact consumption behaviour over time and across economies. Because people’s perceptions of the advantages of life insurance and their sense of security can differ, life insurance businesses need to be aware of cultural attitudes (Hofstede 1995). Hofstede’s (1983, 2001) cultural dimensions dataset has primarily been employed in both life and non-life insurance sectors due to its extensive coverage of many economies and its relevance to the insurance industry (Park et al. 2002; Chui and Kwok 2008).

Although there is an increasing number of empirical studies on the factors influencing the life insurance spending, none, to our knowledge, have solely focused on the influence of cultural traits on life insurance expenditure. Exceptions include recent papers by Chui and Kwok (2008, 2009), Park and Lemaire (2011), and Outreville (2018), which examined the influences of cultural factors on life insurance spending. However, these studies neglected hypometropia, a cultural element introduced by Minkov (2011) that measures the degree of risk acceptance in a country with high murder rates. Using Hofstede’s four cultural dimensions (individualism, uncertainty avoidance, power distance, and masculinity), Chui and Kwok (2008) examined the effect of cultural factors on life insurance expenditure across 41 countries from 1976 to 2001. They found that power distance and masculinity negatively influenced life insurance consumption, while individualism exerted a significant positive influence. Chui and Kwok (2009) included seven additional cultural variables from the GLOBE project, not covered in Hofstede’s analysis, and further unveiled a strong link between life insurance spending, in-group collectivism, and power distance.

Park and Lemaire (2011) extended Chui and Kwok’s (2008) study by including Hofstede’s fifth cultural dimension, long-term orientation, in their analysis across 27 countries from 2000 to 2008. They confirmed that long-term orientation strongly and positively influenced life insurance consumption. Outreville (2018) explored how national culture and the socio-political environment affect the pervasiveness of life insurance in 15 emerging countries from 2000, 2010, and 2015. The author used the four original cultural dimensions of Hofstede and the three cultural dimensions of Schwartz, finding that life insurance spending is positively associated with individualism while negatively associated with uncertainty avoidance.

Public health spending

There is widespread agreement that investing in public health has favourable effects on health outcomes, income, and economic growth (Self and Grabowski, 2003; Amaghionyeodiwe 2008; Rizk 2012; Edeme et al. 2017; Boachie et al. 2018; Ifa and Guetat 2019; Patrick et al. 2020; Mustafa et al. 2021; Torche and Rauf 2021). Mustafa et al. (2021) reported that public health spending indirectly influences the infant mortality rate in the West African Sub-region. This positive correlation between public health spending and individual health outcomes is also evident in Nigeria (Edeme et al. 2017). According to Edeme et al. (2017), enhancements in public health expenditure lead to improvements in life expectancy at birth and reductions in infant mortality in Nigeria. Patrick et al. (2020) found that public health programs in Florida have an effectiveness in decreasing maternal mortality rates. Ifa and Guetat (2019) discovered that public health spending and economic growth in Tunisia and Morocco are positively correlated. Boachie et al. (2018) explored the connection between public health expenditure and people’s health outcomes in Ghana from 1980 to 2014, confirming that public health spending was a significant contributor to better health outcomes. Self and Grabowski (2003) inferred that while there is limited evidence showing that greater public health spending improves health outcomes in wealthier economies, it can contribute to better health outcomes in middle- to less-developed economies.

Rizk (2012) stated that a 1% increase in government health spending is related to a 0.8% improvement in human poverty. Amaghionyeodiwe (2008) claimed that public health expenditure reduces the income disparity between the affluent and the poor, albeit it does not enhance health infrastructure. Hence, even if a direct relationship between public health spending and life insurance purchases is elusive, improvements in health leading to increased wealth and income could affect individuals’ intention to spend on life insurance.

Economic freedom factors

The degree to which a country’s economy is deemed to be a market economy with little to no government intervention in the form of ownership, rules, or taxation is known as economic freedom (Berggren, 2003).Footnote 4 In relation to life insurance demand and its purchase in these countries, it is still questionable as to how this economic freedom has any influence on it (Horng et al. 2012; Li et al. 2007; Shaar and Ariff 2016). However, in the literature now available, the significance of economic freedom for economic development has been demonstrated (e.g., Dawson 2003; Gwartney et al. 2004; Justesen 2008; Azman-Saini et al. 2010; Ciftci and Durusu-Ciftci 2022). Although several studies investigate the relationship between economic freedom and the non-life insurance sector, none of them focuses on the influence of the economic freedom on life insurance spending.Footnote 5

Per capita income

An abundance of earlier studies (e.g., Beenstock et al. 1986; Browne and Kim 1993; Outreville 1996; Beck and Webb 2003; Li et al. 2007; Park and Lemaire 2011; Zerriaa and Noubbigh 2016; Emamgholipour et al. 2017; Dragos et al. 2017; Lee et al. 2018; Outreville 2018; Gaganis et al. 2020) have demonstrated a consistently positive correlation between per capita income and life insurance consumption. These findings clearly support the theoretical models that per capita income positively influences life insurance consumption. People with a large income may cause a greater loss of expected utility for their dependants in the case of their deaths. As such, this effect may contribute significantly to the positive link with income by promoting the affordability of life insurance products (Li et al. 2007).

Financial development factors

Financial development can help households to be able to secure their future income through the financial assets’ ownership due to its widespread securitisation of cash flows (Li et al. 2007). Many earlier papers (e.g., Outreville 1996; Beck and Webb 2003; Li et al. 2007; Park and Lemaire 2011; Sen and Madheswaran 2013; Zerriaa and Noubbigh 2016; Alhassan and Biekpe 2016; Sanjeewa et al. 2019; Akhter et al. 2020; and Gaganis et al. 2020) investigate the link between financial development factors and life insurance spending and find it to be positively influenced. These findings prove that life insurance is anticipated to promote higher sales in economies with a high degree of financial development.

Urbanisation

Beck and Webb (2003) argued that insurers operating in areas with higher level of urbanisation may reduce the costs with regard to marketing, underwriting and claims handling, hence the insurers have an advantage in the distribution of life insurance products for customers in these areas due to their concentration. This results in more consuming on life insurance products.

Families in urban areas become smaller than those in regional areas, hence these families no longer have economic security within a family or village, and this may lead to a demand for additional forms of financial safeguards such as life insurance (Beck and Webb 2003; Park and Lemaire 2011). A number of studies (e.g., Park and Lemaire 2011; Sen and Madheswaran 2013; Zerriaa and Noubbigh 2016; Alhassan and Biekpe 2016; Dragos et al. 2017; Lee et al. 2018; Outreville 2018; Sanjeewa et al. 2019; and Akhter et al. 2020) examine the effect of urbanisation on life insurance consumption. The studies of Alhassan and Biekpe (2016), Lee et al. (2018), Sanjeewa et al. (2019), and Akhter et al. (2020), among others, find a negative influence of urbanisation on life insurance spending and are in contrast with their expectation.

The level of education

People with higher education would perceive more benefits of the use of life insurance and may be willing to choose various life insurance products as the way to protect their dependants (Truett and Truett 1990; Browne and Kim 1993). As such, a higher degree of education may promote life insurance consumption. Various previous papers (e.g., Browne and Kim 1993; Outreville 1996; Beck and Webb 2003; Li et al. 2007; Zerriaa and Noubbigh 2016; Alhassan and Biekpe 2016; Emamgholipour et al. 2017; Dragos et al. 2017; Lee et al. 2018; Outreville 2018; Sanjeewa et al. 2019; Akhter et al. 2020) explored the impact of education level on life insurance expenditure. While some, such as Li et al. (2007), Zerriaa and Noubbigh (2016), Emamgholipour et al. (2017), Dragos et al. (2017), and Sanjeewa et al. (2019), found a positive correlation, others such as Outreville (1996), Alhassan and Biekpe (2016), and Lee et al. (2018) reported a negative correlation.

Human development index

The impact of this variable on life insurance consumption has been explored by researchers such as Outreville (1996, 2018), Beck and Webb (2003), and Gaganis et al. (2020). Their findings suggest no substantial correlation.

Life expectancy

Both theoretical and empirical models by Beenstock et al. (1986) suggested that life expectancy has a positive influence on the life insurance demand. This might be the case because the actuarial cost of cover falls with increasing life expectancy; hence it decreases the price for life insurance. Outreville (1996) argued that a long lifespan may lead to increasing incentives for human capital accumulation and found a positive influence of life expectancy on life insurance spending. Consistent with these results, Park and Lemaire (2011) and Sen and Madheswaran (2013) also found a positive influence of this variable on life insurance demand. However, life expectancy may have a significantly negative influence on life insurance consumption because of its correlation with the death probability in a country (Alhassan and Biekpe, 2016; Gaganis et al. 2020). These authors argued that a higher life expectancy that implies low the death probability may lower the motivation for life insurance consumption. The negative relationship between life expectancy and life insurance spending has been found in the empirical papers by Li et al. (2007), Alhassan and Biekpe (2016), Sanjeewa et al. (2019), and Gaganis et al. (2020).

Dependency ratio

According to theoretical studies by Campbell (1980) and Lewis (1989), main earners often opt for life insurance products as a way to protect their dependants in the case of their future deaths. Most households can anticipate the large transfer from life insurers after their main earners die. However, the findings of empirical studies are mixed. Some papers (e.g., Beenstock et al. 1986; Beck and Webb 2003; Li et al. 2007; Park and Lemaire 2011) indicate a positive influence of the dependency ratio on life insurance spending, while others (e.g., Sen and Madheswaran 2013; Zerriaa and Noubbigh 2016; Alhassan and Biekpe 2016; Lee et al. 2018) find a negative influence of this factor on life insurance spending.

Social security contributions

Rejda and Schmidt (1979) concluded that social security contributions have a negative influence on fully insured pension contributions. Following this point, Beenstock et al. (1986) found that social security contributions can serve as an alternative to private security arrangements. The authors concluded that social security contributions may reduce life insurance demand. This approach has been employed in a number of studies where a more comprehensive collection of explanatory variables was used to examine the impact of social security contributions on life insurance spending. These involve the studies by Outreville (1996), Beck and Webb (2003), Li et al. (2007), Zerriaa and Noubbigh (2016), Alhassan and Biekpe (2016), and Sanjeewa, Hongbing and Hashmi (2019). Their results support a negative relationship between social security contributions and life insurance spending. However, Browne and Kim (1993) argued that households’ assets may be increased due to the social security benefits, hence increasing family consumption, including spending on life insurance. They also discovered that social security contributions have a positive effect on life insurance expenditures.

Legal system factors

Legal systems, particularly those following Common law, provide a higher degree of protection for creditors and shareholders (La Porta et al. 1999). Park et al. (2010) concluded that the legal system is the main driver in explaining the variation of auto insurance bonus-malus systems across Asian nations. Park and Lemaire (2011) investigated the impact of Common law on life insurance demand and found a positive influence.

Religion

Religious beliefs in a country may affect the population’s risk aversion, hence it affects spending on life insurance. Browne and Kim (1993) investigated the influence of Islamic country factor using a dummy variable on life insurance spending and the author found a negative impact. Following this approach, Outreville (1996), Beck and Webb (2003), Park and Lemaire (2011), Zerriaa and Noubbigh (2016), Outreville (2018), and Gaganis et al. (2020) examined how religious beliefs impact life insurance demand. Park and Lemaire (2011) found a negative influence of total Christian and Islamic beliefs on life insurance demand while Outreville (1996), Beck and Webb (2003), Zerriaa and Noubbigh (2016), Outreville (2018), and Gaganis et al. (2020) found a negative impact of Islamic beliefs on life insurance consumption.

Data, methodology and hypotheses

Data and methodology

Following Trinh et al. (2020), this study employs the system GMM estimator introduced by Holtz-Eakin, Newey and Rosen (1988), Arellano and Bond (1991), Arellano and Bover (1995) and Blundell and Bond (1998). We take into account the subsequent regression model:

where: lnINSi,t denotes life insurance consumption (density) (with “ln” referring to the natural logarithm); lnINSi,t−1 denotes the initial life insurance consumption (density); lnINCi,t denotes per capita GDP; lnEFIi,t denotes the index of economic freedom; lnPHSi,t denotes the public health spending; lnCULi denotes cultural variables that are time invariant, only varying across nations; FDVi,t denotes the financial development; HDIi,t denotes the school enrolment, tertiary (% gross); URBi,t denotes the urbanisation; DEPi,t denotes the dependency ratio; SSEi,t denotes the social security contribution; CMLi denotes dummy variables (Common law); MUSi denotes the percentages of Muslim population; at represents a year fixed effect; α, β1 to β11 are vectors of coefficients and εit is the error term.

A panel dataset, including 49 countries spanning the period from 2002 to 2017, is utilized (the list of specific economies is listed in Table A2)Footnote 6. We follow the World Economic Outlook (IMF) to classify our sample of countries into 28 advanced economies, and 21 emerging and developing countries.Footnote 7 Variables definitions, summary statistics, and the correlation matrix in the analysis are detailed in Tables A1, and A3 to A6.

In this paper, life insurance consumption is proxied by the density of life insurance as provided by Sigma (Swiss Re), measured as direct domestic premiums per capita in US dollars. This variable indicates the average amount or consumption that an individual consumes on the life insurance.Footnote 8 For data on national culture, which is the first main explanatory variable, we rely on the cultural dimensions of Minkov and Hofstede including hypometropia, individualism, masculinity, uncertainty avoidance, power distance, long-term orientation and indulgence. Our second main explanatory variable is the public health spending, which is measured by domestic general government expenditure per capita (current $US). The economic freedom variable, which is our third main explanatory variable, is measured by the Fraser Institute’s economic freedom index.Footnote 9

The usual control variables for life insurance consumption, employed frequently in previous literature, are also included in our model. These include per capita GDP, financial development, urbanisation, human development indexFootnote 10, dependency ratio, life expectancy, social security contributions, common law and Muslim religion.

Estimation strategy

For statistical tests, we first check the endogeneity issue which can occur due to omitted variables and reverse causality (see Trinh et al. 2016; 2020; 2021). We next check the cross-sectional dependence problem in our sample data. For regressions, we first run the pooled OLS regression. After that, the system GMM estimation is applied to overcome the disadvantages of the OLS regression including the endogeneity caused by the causality and omitted variables and cross-sectional dependence issue.Footnote 11 In this paper, the system GMM estimators using xtabond2 with the robust option in STATA, as created by Roodman (2009), are carried out. We also employ two specification tests to evaluate the consistency of the system GMM estimator: the Hansen test for the joint validity of the instruments and a test of second-order serial correlation.

In line with Beck and Webb (2003), among others, the natural logarithms of the dependent and most independent variables are used. This approach enables us to have direct comparison with earlier studies’ results.

Hypotheses

Drawing from the literature review, this study proposes the following hypotheses:

H1: The higher the level of the one-year lagged life insurance spending, the per capita income, public health spending, economic freedom, financial development, urbanisation and dependency ratio in a country, the higher the life insurance consumption is.

H2: The lower the level of the human development, life expectancy and the proportion of Muslim population in a country, the higher the life insurance consumption is.

H3: The lower the degree of masculinity and power distance in a country, the higher the life insurance consumption is.

H4: The higher the degree of hypometropia, indulgence, individualism, long-term orientation and uncertainty avoidance in a country, the higher the life insurance consumption is.

H5: Common Law has a positive impact on the life insurance consumption.

Results and discussion

Statistic tests

The endogeneity issue

We apply the Durbin-Wu-Hausman test to check the endogeneity issue which may be triggered by the economic freedom index and GDP per capita (see also Trinh et al. 2016; 2020; 2021).Footnote 12 The results of the test for endogeneity in Table 1 show that these variables are endogenous.

The cross-sectional dependence issue

Groups of sample countries sharing similar levels of development and geographical regions, such as developing Southeast Asian nations (Malaysia, Indonesia, Philippines, Thailand) and developed European countries (Finland, France, Germany, Greece, Italy, Spain, Sweden, Switzerland, and Norway), may exhibit shared economic traits, history, and culture.

Therefore, while cross-sectional dependence may exist, the growth-enhancing factors for these countries may not be uniform, given the disparities in policies and institutions across nations. If cross-sectional dependence is present in our data, the effects of cultural factors on the purchase of life insurance for advanced economies and emerging and developing economies will be specifically addressed later.

Our sample countries may some group of countries belonging to the similar levels of development and same geographical areas such as developing countries in Southeast Asia (e.g., Malaysia, Indonesia, Philippines, and Thailand) and developed countries in Europe (e.g., Finland, France, Germany, Greece, Italy, Spain, Sweden, Switzerland, and Norway) and these groups of countries can move together with respect to economic features, common history, and culture. Despite these shared characteristics, unique national policies and varied economic, political, and legal institutions could introduce heterogeneity, affecting the growth drivers in each country (Cooray et al. 2013). In other words, the existence of cross-sectional dependence does not suggest that sets of countries possess the same growth-enhancing factors mainly due to institutional and policy differences among nations. If cross-sectional dependence is present in our data, the effects of cultural factors on the two categories of economies’ life insurance spending based on their levels of development - advanced economies and emerging and developing economies - will be specifically addressed later.

A cross-sectional dependence (CD) test (Cooray et al. 2013) helps explore the similarity among countries. We use the CD test for cross-sectional dependence (Pesaran 2004). The finding in Table 2 rejects the null hypothesis of cross-section independence. For the robustness check, we have examined the cross-sectional dependence problem in our sample data in accordance with the study by Sarafidis et al. (2009).Footnote 13 The authors proposed a new testing procedure for detecting error cross section dependence using the system GMM estimator by adopting Sargan’s difference tests for heterogeneous error cross section dependence based on the system GMM estimator (namely DSYS2). Sargan’s difference tests, based on the system GMM estimator for heterogeneous error cross section dependency, reject the null hypothesis of homogeneous error cross section dependence, as shown by the P-value of 0.00001 in Table 3. This demonstrates that the cross-sectional dependence problem exists in our sample data and is in line with the results of the CD test shown in Table 2.

We adopted Sarafidis et al. (2009) and Sarafidis and Wansbeek (2012)’s usage of the system GMM estimator, which is only based on partial instruments made up of the regressors, to address the cross-sectional dependence issue. Under the condition of heterogeneous error cross section dependency, this estimator offers a trustworthy substitute for the conventional GMM estimators.

Statistic tests of the system GMM estimator

Table 4 provides the summary of statistic tests of the system GMM estimator that relies solely on partial instruments consisting of the regressors. The outcomes of the Hansen test are consistent with the null hypothesis concerning the validity of the instruments. Likewise, the Arellano-Bond tests’ p-values indicate that the errors in the difference equation do not display the second-order (or the third-order) autocorrelation. These outcomes support the selection of the system GMM estimator as the benchmark model for addressing endogeneity and cross-sectional dependence issues.

Determinants of the life insurance consumption in all sample economies

We have investigated the cultural-social-economic drivers on the life insurance spending using an unbalanced panel dataset covering 49 economies over the years from 2002 to 2017. In addition to the system GMM estimator based on partial instruments as our main regression, we also include the pooled OLS regression and the system GMM estimator based on full instruments to illustrate differences in coefficients amongst these regressions, attributable to cross-sectional dependence and endogeneity problem.

Results from the GMM estimator, seen in column (3) of Table 5, indicate that a one-year lag in life insurance expenditure positively impacts current spending on life insurance, corroborating our hypothesis H1. This finding aligns with those of Alhassan and Biekpe (2016) and Dragoş et al. (2019). Indeed, prior-year expenditure on life insurance products ensures continuity in current-year spending on the same offerings. Continuous purchasing of life insurance products helps individuals uphold their contracts effectively. In addition, they may introduce these life insurance products to their relatives or friends to get further benefits such as commissions or discounts, and this can lead to the increase in spending on life insurance products. We also discover that economic freedom positively influences life insurance acquisition. This finding endorses our hypothesis H1, emphasizing the role of economic freedom in stimulating economic activities via investment channels and promoting long-term economic prosperity (Dawson 2003; Gwartney et al. 2004; Justesen 2008; Azman-Saini et al. 2010), and thus, increasing life insurance expenditure. While numerous studies have analyzed the link between economic freedom and non-life insurance, none have focused on the impact of economic freedom on life insurance consumption (Horng et al. 2012; Li et al. 2007; Shaar and Ariff 2016).Footnote 14 Our finding addresses this gap.

As expected, public health spending has a significantly positive effect on life insurance consumption, in alignment with our hypothesis H1 and confirms that residents of a country with higher degree of public health spending may expend more on life insurance spurred by a rise of wealth and income caused by health improvements.Footnote 15 Indeed, people who live in countries with high degree of public health spending may enjoy better public health care services such as health protection, health promotion, disease prevention and health improvement, but they also receive death compensation. They are willing to consume more on life insurance to be protected by private insurers because compensation for death is not covered by the public health services. In addition, life insurance policies contain saving meaning. When a life insurance policy is due, the insured receives back the face amount of policy value plus some interest earnings, which encourages the participation of more people in life insurance.

Table 5 provides an interesting (and new) result with regard to the cultural variable. Individualism has a significant and negative impact on life insurance consumption in all sample economies. This result contradicts our hypothesis H4 and is not in line with the studies of Chui and Kwok (2008) and Outreville (2018). This can be due to the fact that people in economies with high degrees of individualism may choose other investment channels such as investments on stock, bonds and properties rather than consuming on the life insurance products as a means of protecting their family members.

With regard to other socio-economic factors, Table 5 provides information that financial development has a significantly negative influence on life insurance expenditure, a result not aligned with our hypothesis H1. However, this result is consistent with the study by Trinh et al. (2020). A possible explanation for the negative effect of financial development is that it may be attributed to the repercussions of the global financial crisis (GFC) on the insurance sector (Trinh et al. 2020).

Table 5 additionally shows that while the human development index negatively affects life insurance consumption, life expectancy positively impacts it. The negative impact of the index of human development on life insurance consumption supports our hypothesis H2, which is consistent with earlier papers, and confirms that a higher degree in human development index may lead to lowering the life insurance consumption. People leading a long and healthy life, with knowledge and a decent standard of living may have less risk aversion on their deaths. These could result in decreased life insurance expenditure. Notably, while Outreville (1996, 2018), Beck and Webb (2003) and Gaganis et al. (2020) found no significant influence of human development index on life insurance consumption, this variable in our study appears to be statistically significant. The positive influence of life expectancy does not support our hypothesis H2 and is not in line with the earlier studies (e.g., Li et al. 2007; Alhassan and Biekpe 2016; Sanjeewa et al. 2019; and Gaganis et al. 2020). This can be explained in the following way: the actuarial cost of cover falls with increasing life expectancy, hence it decreases the price for life insurance (Beenstock et al. 1986). Outreville (1996) argued that a long-life span may lead to increased incentives for human capital accumulation. Our finding is in line with Outreville (1996), Park and Lemaire (2011), and Sen and Madheswaran (2013), who found a positive influence of life expectancy on life insurance consumption.

Table 5 also reveals that dependency ratio has a negative effect on the life insurance expenditure. This outcome does not support our hypothesis H1 and findings of Beenstock et al. (1986), Beck and Webb (2003), Li et al. (2007), and Park and Lemaire (2011). This could be attributed to a high dependency ratio potentially placing significant strain on current income levels, resulting in lower spending on the life insurance products (Alhassan and Biekpe 2016). The main earner in each household may use health insurance products to substitute life insurance. This can be illustrated by an increasing number of countries providing health insurance for children and the poor (Camacho and Conover 2013). This can be also due to the domination of the proportion of young dependency ratio aged below 15 in our all-sample economies compared to the proportion of old dependency ratio aged above 64. Zerriaa and Noubbigh (2016) suggested that the population is too young to begin saving, a finding supported by Sen and Madheswaran (2013), Zerriaa and Noubbigh (2016), Alhassan and Biekpe (2016), and Lee et al. (2018).

Finally, Table 5 presents the positive influence of common law on life insurance consumption, supporting our hypothesis H5 and is consistent with the study by Park and Lemaire (2011). This finding confirms the view that people living in a country with the common law may consume more on life insurance products, as this law provides them with the highest protection.

Given the heterogeneity among economies in our sample, particularly concerning development levels, the coefficients on cultural variables and other socio-economic variables might exhibit bias. Therefore, we will subsequently highlight the effects of cultural factors on life insurance consumption for two groups of economies based on development levels: advanced economies and emerging and developing economies.Footnote 16 Results will be discussed in turn.

Determinants of the life insurance consumption in the advanced economies

This section delves into the results for advanced economies solely. Column (3) of Table 6 illustrates that the life insurance consumption from the previous year and economic freedom are the main factors of life insurance consumption for this sample. These factors’ significantly positive coefficients support our H1 hypothesis and are consistent with the findings of all sample economies. These outcomes reiterate the crucial impacts of one-year lagged spending and economic freedom on life insurance purchase.

When considering the cultural variables of Minkov and Hofstede, the results derived from the system GMM estimator indicate that indulgence negatively impacts life insurance consumption in advanced economies, a finding that contradicts our hypothesis H4. This could potentially be attributed to individuals residing in advanced countries with high indulgence, who may be more accepting of risks due to their optimistic outlook, thus leading to a decrease in life insurance spending (Minkov 2011, Trinh et al. 2016). Another plausible interpretation is that the average indulgence score in advanced economies is lower than that in all sample countries, and emerging and developing economies.

With regard to other socio-economic factors, Table 6 reveals that financial development exerts a negative influence on life insurance expenditure, a result that does not align with our hypothesis H1. In a similar manner to the situation with all sample economies, this outcome may be chiefly attributed to the influences of the GFC on the insurance market in advanced economies. Furthermore, we observe that human development negatively affects life insurance consumption, a finding supporting our hypothesis H2 and is in line with the outcome from all sample economies. This could possibly suggest that individuals leading long, healthy lives, educated and maintaining a decent standard of living, may be less concerned about their mortality risks, resulting in a decline in life insurance consumption.

Determinants of the life insurance consumption in the emerging and developing economies

The factors influencing the life insurance spending in emerging and developing economies are investigated using a test identical to the one used for all sample economies and advanced economies. As reported in column (3) of Table 7, the statistically significant signs of one-year lagged spending on life insurance, economics freedom, public health spending, and human development index are in line with the findings in the case of all sample economies and advanced economies.

Table 7 reveals several interesting (and new) outcomes related to the cultural variables. The consumption of life insurance is considerably impacted negatively by masculinity, which aligns with our expectations, and is consistent with the study by Chui and Kwok (2008). This outcome corroborates the idea that in high masculine societies, men concentrate on their occupations while women focus on family care, which may lead to reduced life insurance spending due to restricted income (Trinh et al. 2016). Notably, uncertainty avoidance has a significantly negative impact on life insurance consumption, a finding that contradicts our expectation. The negative influence of uncertainty avoidance on life insurance consumption in emerging and developing economies can be explained as follows. Residents of emerging and developing economies may reduce life insurance spending due to their acceptance of risk. Previous studies by Park et al. (2002) and Shaw (2006) propose that inhabitants of emerging and developing economies might embrace risks due to their optimistic outlook. For instance, Shaw (2006) claimed that individuals in developing economies usually take into account the benefits of floods, such as the notion that they bring fish and create new, rich agricultural land, and as a result, the local people and communities accept the concept of "living with the flood" or "coping with the flood". Another explanation is that individuals in developing economies may choose self-insurance plans over traditional insurance policies (Trinh et al. 2021). Additionally, Balli et al. (2011) suggests that people in these economies can shield their income from risks by investing in foreign assets and domestic channels, hence they may end up spending less on life insurance products.

Concerning other socio-economic factors, the negative influence of the dependency ratio on life insurance consumption supports our hypothesis H2 and is in line with the study by Alhassan and Biekpe (2016). Finally, Table 7 presents the negative impact of the proportion of the Muslim population on the life insurance consumption in emerging and developing economies, supporting our hypothesis H2 and aligning with previous studies (Outreville 1996; Beck and Webb 2003; Park and Lemaire 2011; Zerriaa and Noubbigh 2016; Outreville 2018; Gaganis et al. 2020). This finding confirms the view that religious beliefs in a country may affect the population’s risk aversion, hence it affects life insurance spending.

Robustness check

To check the robustness of our results further, in addition to the system GMM estimator based on partial instruments, we have performed Instrumental Variable (IV) regression and the feasible generalised least squares (FGLS) estimates.Footnote 17 While IV regression can address the endogeneity issue, FGLS can overcome the cross-sectional dependence problem (Trinh et al. 2016; Reed and Ye 2011). We have also followed Rafiq et al. (2016, 2017) to adopt models with heterogeneous slope coefficients using the Augmented Mean Group (AMG) estimators, which can account for the cross-sectional dependence issue, for the robustness check.Footnote 18 Based on three different estimators in Table 8, the results indicate that cultural variables and public health spending - our main key variables – are significant and in the same directions. Therefore, the results of our robustness tests agree with our prior major conclusions, which were based on the system GMM.Footnote 19

Implications

The insights garnered from this research hold crucial implications for multinational life insurers and governments. With respect to economic implications regarding the selection of potential markets, multinational life insurers can consider expanding their business into economies with specific cultural dimensions: potential markets should be in emerging and developing economies with lower levels of uncertainty avoidance (e.g., South Africa, Iran and Thailand); for advanced nations, potential markets should be in economies exhibiting lower degree of indulgence (e.g., South Africa and Estonia).

Additionally, life insurers can leverage the findings pertaining to the effects of other socio-economic factors, including economic freedom, public health spending, financial development, human development, urbanisation, life expectancy, dependency ratio, and Muslim religion. This would facilitate their decision-making process concerning factors driving life insurance product spending. For instance, potential markets for life insurance products could be advanced economies with high degrees of economic freedom (e.g. Singapore, Australia, and Japan), and lower human development indices (such as Latvia and Slovakia), or emerging and developing countries with high degrees of economic freedom and public health spending (e.g. Kuwait and Jordan), and lower dependency ratios and Muslim populations (e.g. India, China, and El Salvador).

Conclusion

In this study, we have developed a system GMM analysis utilizing a comprehensive dataset that covers 49 countries from 2002 to 2017. This research investigates the impacts of culture, public health spending, economic freedom, and other socio-economic factors on life insurance consumption. Our findings highlight a diverse array of factors influencing life insurance expenditure, which includes socio-economic elements such as public health spending, economic freedom, financial development, human development index, urbanisation, life expectancy, dependency ratio, and Muslim religion. Cultural factors such as indulgence, individualism, masculinity, and uncertainty avoidance are also included in this list. However, these influences of these factors demonstrate significant variation between advanced economies and emerging and developing economies, suggesting that the heterogeneity among economies is a critical aspect concerning their developmental level. Interestingly, cultural variables, namely masculinity and uncertainty avoidance, do not account for life insurance expenditure in advanced economies, yet these variables manifest a statistically significant impact on life insurance spending in emerging and developing economies. This study is the first that attempts this international comparison of the determinants of life insurance purchases across groups of countries based on their level of development.

This study contributes to the existing body of literature in several significant ways. First, a comprehensive empirical analysis of the determinants of life insurance consumption across countries using the system GMM estimator based on partial instruments, which allows the treatments of the potential endogeneity problem and cross-sectional dependence issue in earlier studies, has been adopted. Second, we have extended our results to compare between two groups of countries based on development level, advanced economies, and emerging and developing economies, and have identified key differences in the way in which those drivers of life insurance spending behave. Third, we utilise the latest and comprehensive cultural data from Minkov (2011) and Hofstede et al. (2010) in our empirical analysis, including newly developed cultural dimensions such as hypometropia and indulgence, which have been neglected in previous studies. Finally, we examine how public health spending and economic freedom impact life insurance consumption pattern at the international level.

Our results provide important information for government policies as well as business firms who are involved in the life insurance markets. Specifically, they provide actionable recommendations for life insurers looking to penetrate new potential markets. Moreover, these results aid governments in refining their regulatory measures and policies to stimulate and nurture the life insurance market, a crucial sector for fostering prosperity and economic growth.

Limitations and future research

Although this study’s empirical findings provide helpful economic and policy implications for both multinational life insurers and governments, this study has a certain limitation with regard on research methodology that can be addressed in future research. The use of the GMM estimator has room for improvement due to the use of internal instruments less effective and this may potentially lead to biased analysis results. Therefore, future studies can improve the current study’s research methodology to address the endogeneity issue more efficiently by using alternative estimators such as three-stage least squares (3SLS) estimator and empirical model based on the one period lagged value of all the exogenous variables.

Notes

In non-life insurance sector, Trinh et al. (2021) claimed that economic freedom can foster non-life insurance demand.

Chow and Fung (2013) claimed that economic freedom can facilitate capital mobility and promote the efficiency of the financial system.

To the best of our knowledge, the only study by Park et al. (2002) examines the effect of the economic freedom on total insurance (both life and non-life) demand and finds it to be positive.

We select this dataset because of its availability.

Based on analytical standards that take into account the make-up of export revenues and make a distinction between net creditor and net debtor economies, emerging market and developing economies are categorized (IMF 2019).

We followed previous studies of Outreville (1996, 2018), Li et al. (2007), Chui and Kwok (2008), Dragos et al. (2017), Dragoş et al. (2019), and Sanjeewa et al. (2019) to use life insurance density as proxied for the life insurance consumption. The second indication of life insurance consumption is known as penetration. This is calculated as the ratio of life insurance premiums to the size of the economy (GDP), and it is not a perfect predictor of consumption because life insurance is a combination of price and quantity (Sanjeewa et al. 2019).

The education data collected by the World Bank is not available for all the years for most of the economies, and this may impact the reliability of our findings. Therefore, we have used the Human Development Index which is available for most of the countries on an annual basis.

To the best of our knowledge, only the study by Park et al. (2002) has examined the influence of the economic freedom on total insurance (both life and non-life) demand and claimed it to be positive.

In nonlife insurance sector, Trinh et al. (2023) also reported that public health spending could stimulate private health insurance consumption in the OECD countries.

A sub-sample analysis was carried out, where separate regressions were run on samples from advanced countries and emerging and developing countries. The intent behind this was: to check the sensitivity of our findings across varied sample sets and to account for potential omitted variable bias resulting from the inclusion of certain groups of countries, as suggested by Nabin et al., 2021.

We followed Trinh et al. (2016) to use the 1-year lagged economic freedom index and the 1-year lagged per capita GDP as instrumental variables for IV regression. We also took the 1-year lagged value of economic freedom index and per capita GDP for FGLS estimator to deal with the endogeneity issue (see also Rafiq et al., 2017).

Time-invariant variables including cultural variables, Common law variable and Muslim variable are dropped before conducting Mean Group estimators to ensure that the number of observations after conducting regression must be at least as large as the number of panels in the current estimation sample. Having these variables leads to dropping a large number of observations and therefore the “xtmg” Stata command cannot perform.

Results for robustness check in two groups of countries are presented in Tables A7 and A8 in Appendix A.

References

Akhter W, Pappas V, Khan SU (2020) Insurance demand in emerging Asian and OECD countries: a comparative perspective. Int J Soc Econ 47(3):350–364

Alhassan AL, Biekpe N (2016) Determinants of life insurance consumption in Africa. Res Int Bus Finance 37:17–27

Amaghionyeodiwe LA (2008) Determinants of the choice of health care provider in Nigeria. Health Care Manag Sci 11(3):215–227

Anand S, Ravallion M (1993) Human development in poor countries: on the role of private incomes and public services. J Econ Perspect 7(1):133–150

Arellano M, Bond S (1991) Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev Econ Stud 58(2):277–297

Arellano M, Bover O (1995) Another look at the instrumental variable estimation of error-components models. J Econom 68(1):29–51

Arena M (2008) Does insurance market promote economic growth? A cross country study for industrialized and developing countries. J Risk Insurance 75(4):921–946

Azman-Saini WNW, Baharumshah AZ, Law SH (2010) Foreign direct investment, economic freedom and economic growth: international evidence. Econ Model 27(5):1079–1089

Balli F, Basher SA, Balli HO (2011) Income insurance and the determinants of income insurance via foreign asset revenues and foreign liability payments. Econ Model 28(5):2296–2306

Beck T, Webb I (2003) Economic, demographic, and institutional determinants of life insurance consumption across countries. World Bank Econ Rev 17(1):51–88

Beenstock M, Dickinson G, Khajuria S (1986) The determination of life premiums: an international cross-section analysis 1970–1981. Insurance: Math Econ 5(4):261–270

Berggren N (2003) The benefits of economic freedom: a survey. Indep Rev 8(2):193–211

World Bank (2020) World Development Indicators. World Bank, Washington, DC

Bernheim BD (1991) How strong are bequest motives? Evidence based on estimates of the demand for life insurance and annuities. J Political Econ 99(5):899–927

Swiss Re (2019) Annual Report: Various Years. Sigma, Zurich

Blundell R, Bond S (1998) Initial conditions and moment restrictions in dynamic panel data models. J Econom 87(1):115–143

Boachie MK, Ramu K, Põlajeva T (2018) Public health expenditures and health outcomes: new evidence from Ghana. Economies 6(4):58

Browne MJ, Kim K (1993) An international analysis of life insurance demand. J Risk Insurance 60(4):616–634

Camacho A, Conover E (2013) Effects of subsidized health insurance on newborn health in a developing country. Econ Dev Cult Change 61(3):633–658

Campbell RA (1980) The demand for life insurance: An application of the economics of uncertainty. J Finance 35(5):1155–1172

Chen PF, Lee CC, Lee CF (2012) How does the development of the life insurance market affect economic growth? Some international evidence. J Int Dev 24(7):865–893

Chow WW, Fung MK (2013) Financial development and growth: a clustering and causality analysis. J Int Trade Econ Dev 22(3):430–453

Chui AC, Kwok CC (2008) National culture and life insurance consumption. J Int Bus Stud 39(1):88–101

Chui AC, Kwok CC (2009) Cultural practices and life insurance consumption: an international analysis using GLOBE scores. J Multinatl Financial Manag 19(4):273–290

Ciftci C, Durusu-Ciftci D (2022) Economic freedom, foreign direct investment, and economic growth: the role of sub-components of freedom. J Int Trade Econ Dev 31(2):233–254

Cooray A, Paradiso A, Truglia FG (2013) Do countries belonging to the same region suggest the same growth enhancing variables? Evidence from selected South Asian countries. Econ Model 33:772–779

Curak M, Loncar S, Poposki K (2009) Insurance sector development and economic growth in transition countries. Int Res J Finance Econ 34(1):29–41

Dawson JW (2003) Causality in the freedom–growth relationship. Euro J Political Econ 19(3):479–495

Doucouliagos C, Ulubasoglu MA (2006) Economic freedom and economic growth: does specification make a difference? Euro J Political Econ 22(1):60–81

Dragos SL, Mare C, Dragota IM, Dragos CM, Muresan GM (2017) The nexus between the demand for life insurance and institutional factors in Europe: new evidence from a panel data approach. Econ Res-Ekon Istraž 30(1):1477–1496

Dragoş SL, Mare C, Dragoş CM (2019) Institutional drivers of life insurance consumption: a dynamic panel approach for European countries. Geneva Papers Risk Insurance-Issues Pract 44(1):36–66

Edeme R, Emecheta C, Omeje M (2017) Public health expenditure and health outcomes in Nigeria. Am J Biomed Life Sci 5(5):96–102

Emamgholipour S, Arab M, Mohajerzadeh Z (2017) Life insurance demand: Middle East and North Africa. Int J Soc Econ 44(4):521–529

Fischer S (1973) A life cycle model of life insurance purchases. Int Econ Rev 14(1):132–152

Gaganis C, Hasan I, Pasiouras F (2020) Cross-country evidence on the relationship between regulations and the development of the life insurance sector. Econ Model 89:256–272

Goodell JW (2020) COVID-19 and finance: agendas for future research. Finance Res Lett 35:1–5

Gwartney JD, Holcombe RG, Lawson RA (2004) Economic freedom, institutional quality, and cross-country differences in income and growth. Cato J 24(3):205–223

De Haan J, Lundström S, Sturm JE (2006) Market‐oriented institutions and policies and economic growth: a critical survey. J Econ Surv 20(2):157–191

Haiss P, Sümegi K (2008) The relationship between insurance and economic growth in. Eur: Theor Empir Anal Empir 35(4):405–431

Hammond JD, Houston DB, Melander ER (1967) Determinants of household life insurance premium expenditures: an empirical investigation. J Risk Insurance 34(3):397–408

Headen RS, Lee JF (1974) Life insurance demand and household portfolio behavior. J Risk Insurance 41(4):685–698

Hofstede G (1983) The cultural relativity of organizational practices and theories. J Int Bus Stud 14(2):75–89

Hofstede G (1995) Insurance as a product of national values. Geneva Papers Risk Insurance-Issues Pract 20(4):423–429

Hofstede G (2001) Culture’s consequences: comparing values, behaviors, institutions, and organizations across nations, 2nd ed. Sage Publications, Thousand Oaks, CA

Hofstede G, Hofstede GJ, Minkov M (2010) Cultures and organizations: Software of the Mind: Intercultural cooperation and its importance for survival, 3rd ed. McGrawHill, New York

Holtz-Eakin D, Newey W, Rosen HS (1988) Estimating vector autoregressions with panel data. Econometrica 56(6):1371–1395

Horng MS, Chang YW, Wu TY (2012) Does insurance demand or financial development promote economic growth? Evidence from Taiwan. Appl Econ Lett 19(2):105–111

Ifa A, Guetat I (2019) The short and long-run causality relationship between public health spending and economic growth: evidence fromTunisia and Morocco. J Econ Dev 44(3):19–39

IMF (International Monetary Fund) (2019) World Economic Outlook: Growth Slowdown, Precarious Recovery. Washington, DC, April

Johar GV, Maheswaran D, Peracchio LA (2006) MAP ping the frontiers: theoretical advances in consumer research on memory, affect, and persuasion. J Consum Res 33(1):139–149

Justesen MK (2008) The effect of economic freedom on growth revisited: new evidence on causality from a panel of countries 1970–1999. Euro J Political Econ 24(3):642–660

Lee CC (2011) Does insurance matter for growth: Empirical evidence from OECD countries. BE J Macroecon 11(1):1–26

Lee CC, Lee CC, Chiu YB (2013) The link between life insurance activities and economic growth: some new evidence. J Int Money Finance 32:405–427

Lee HS, Chong SC, Sia BK (2018) Influence of secondary and tertiary literacy on life insurance consumption: case of selected ASEAN countries. Geneva Papers Risk Insurance-Issues Pract 43(1):1–15

Lewis FD (1989) Dependents and the demand for life insurance. Am Econ Rev 79(3):452–467

Li D, Moshirian F, Nguyen P, Wee T (2007) The demand for life insurance in OECD countries. J Risk Insurance 74(3):637–652

Meier V (1998) Long-term care insurance and life insurance demand. Geneva Papers Risk Insurance Theory 23(1):49–61

Minkov M (2011) Cultural differences in a globalizing world. Emerald Group Publishing, Bingley

Mooij MD (2003) Convergence and divergence in consumer behaviour: implications for global advertising. Int J Advert 22(2):183–202

Mustafa R, Onikosi-Alliyu SO, Babalola A (2021) Impact of government health expenditures on health outcomes in the West African Sub-Region. Folia Oeconomica Stetinensia 21(1):48–59

Nabin MH, Chowdhury MTH, Bhattacharya S (2021) It matters to be in good hands: the relationship between good governance and pandemic spread inferred from cross-country COVID-19 data. Human Soc Sci Commun 8(1):1–15

Outreville JF (1996) Life insurance markets in developing countries. J Risk Insurance 63(2):263–278

Outreville JF (2013) The relationship between insurance and economic development: 85 empirical papers for a review of the literature. Risk Manag Insurance Rev 16(1):71–122

Outreville JF (2018) Culture and life insurance ownership: is it an issue? J Insurance Issues 41,2:168–192

Park H, Borde SF, Choi Y (2002) Determinants of insurance pervasiveness: a cross-national analysis. Int Bus Rev 11(1):79–96

Park S, Lemaire J (2011) Culture matters: long-term orientation and the demand for life insurance. Asia-Pacific J Risk Insurance 5(2):1–21

Park SC, Lemaire J, Chua CT (2010) Is the design of bonus-malus systems influenced by insurance maturity or national culture? Evidence from Asia. Geneva Papers Risk Insurance-Issues Pract 35(1):S7–S27

Patrick B, Gulcin G, Sharmila V (2020) Maternal mortality and public health programs: evidence from Florida. Milbank Quarterly March 98(1):150–171

Patrick HT (1966) Financial development and economic growth in underdeveloped countries. Econ Dev Cult Change 14(2):174–189

Pesaran HM (2004) General diagnostic tests for cross section dependence in panels, CESifo Working Paper, No. 1229, Center for Economic Studies and ifo Institute (CESifo), Munich

La Porta R, Lopez-de-Silanes F, Shleifer A, Vishny R (1999) The quality of government. J Law Econ Organ 15(1):222–279

Rafiq S, Sgro P, Apergis N (2016) Asymmetric oil shocks and external balances of major oil exporting and importing countries. Energy Econ 56:42–50

Rafiq S, Nielsen I, Smyth R (2017) Effect of internal migration on the environment in China. Energy Econ 64:31–44

Reed WR, Ye H (2011) Which panel data estimator should I use? Appl Econ 43(8):985–1000

Rejda GE, Schmidt JR (1979) The impact of the social security program or private pension contributions. J Risk Insurance 46(4):636–651

Rizk R (2012) Governance and its impact on poverty reduction: is there a role for KM. Int J Innov Knowl Manag Middle East North Africa 1(1):81

Rode M, Coll S (2012) Economic freedom and growth. Which policies matter the most? Const Political Econ 23(2):95–133

Roodman D (2009) How to do xtabond2: an introduction to difference and system GMM in Stata. Stata J 9(1):86–136

Sanjeewa WS, Hongbing O, Hashmi SH (2019) Determinants of life insurance consumption in emerging insurance markets of South-Asia. Int J Inf Bus Manag 11(4):109–129

Sarafidis V, Wansbeek T (2012) Cross-sectional dependence in panel data analysis. Econom Rev 31(5):483–531

Sarafidis V, Yamagata T, Robertson D (2009) A test of cross section dependence for a linear dynamic panel model with regressors. J Econom 148(2):149–161

Sawadogo R, Guérineau S, Ouedraogo IM (2018) Life insurance development and economic growth: evidence from developing countries. J Econ Dev 43(2):1–28

Self S, Grabowski R (2003) How effective is public health expenditure in improving overall health? A cross–country analysis. Appl Econ 35(7):835–845

Sen S, Madheswaran S (2013) Regional determinants of life insurance consumption: evidence from selected Asian economies. Asian‐Pacific Econ Literature 27(2):86–103

Shaar K, Ariff M (2016) Re-examination of price level differentials using economic freedom index. J Int Trade Econ Dev 25(6):880–896

Shaw R (2006) Critical issues of community-based flood mitigation: examples from Bangladesh and Vietnam. J Sci Cult 72(1-2):1–17

Torche F, Rauf T (2021) The political context and infant health in the United States. Am Sociolog Rev 86(3):377–405

Trinh CT, Nguyen X, Sgro P (2021) Culture and the demand for non-life insurance: Empirical evidences from middle-income and high-income economies. Econ Transit Inst Change 29(3):431–458

Trinh CT, Chao CC, Ho NQ (2023) Private health insurance consumption and public health-care provision in OECD countries: impact of culture, finance, and the pandemic. North American J Econ Finance 64:101849

Trinh CT, Nguyen X, Sgro P, Pham CS (2020) Culture, financial crisis and the demand for property, accident and health insurance in the OECD countries. Econ Model 93:480–498

Trinh T, Nguyen X, Sgro P (2016) Determinants of non-life insurance expenditure in developed and developing countries: an empirical investigation. Appl Econ 48(58):5639–5653

Truett DB, Truett LJ (1990) The demand for life insurance in Mexico and the United States: a comparative study. J Risk Insurance 57(2):321–328

Yaari ME (1965) Uncertain lifetime, life insurance, and the theory of the consumer. Rev Econ Stud 32(2):137–150

Zerriaa M, Noubbigh H (2016) Determinants of life insurance demand in the MENA region. Geneva Papers Risk Insurance-Issues Pract 41(3):491–511

Zietz EN (2003) An examination of the demand for life insurance. Risk Manag Insurance Rev 6(2):159–191

Acknowledgements

We are grateful to the participants at the 38th EBES Conference held at Faculty of Economics Sciences, University of Warsaw, Poland on January 14th, 2022, for their useful comments. We are especially grateful to Viorela Ligia Vaidean for discussing our paper at the EBES-2022 and providing us with invaluable advice and feedback. We would like to thank Vasilis Sarafidis for his useful comments and suggestions in relation to addressing cross-sectional dependency issue. We are especially grateful to Swiss Re for supplying us with the data on life insurance. This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Trinh, C.T., Ha, MT., Ho, N.Q. et al. National culture, public health spending and life insurance consumption: an international comparison. Humanit Soc Sci Commun 10, 470 (2023). https://doi.org/10.1057/s41599-023-01990-7

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-01990-7