Abstract

In recent times, a strand of macro-stabilization experts has been expressing great concern about the move towards fiscal federalism being embraced by many countries over the past three decades. They argue that it could endanger fiscal discipline because it is incompatible with prudent fiscal management. However, some other experts disagree and believe the impact on fiscal discipline could be positive. But, despite the lack of unanimity in the theoretical discourse on the fiscal discipline impact of fiscal federalism, empirical studies on the relationship are still scarce and mixed in conclusions. Using a panel quantile regression estimation approach for a sample of twenty countries over the period 1996–2018, this study establishes that the impact of fiscal federalism on fiscal discipline may not be constant on the conditional mean of the fiscal discipline but varies along its conditional distribution. Moreover, it reveals that quality institutional framework and federalism, each improves the fiscal discipline impact of fiscal federalism, and that countries with a history of low fiscal discipline stand to benefit more from this. The policy implication of this is that in the design and operation of the fiscal federalism apparatus, policy decision-makers should take into consideration the fiscal discipline history of the country. The design of fiscal decentralization apparatus should be appropriately tailored towards each country’s peculiar characteristics and government fiscal stance. Also, it is essential that a quality institutional framework be put in place to support the fiscal decentralization apparatus.

Similar content being viewed by others

Introduction

There has been an increase in fiscal federalism, and the fiscal authority of the subnational governments in most countries over the last three decades (Stossberg et al., 2016). The testament to this is the active and ambitious fiscal decentralization programs being embarked upon by an increasing number of countries around the World in recent years. The fiscal decentralization programs consist of transferring more revenue sources to the subcentral government and reassigning expenditure functions between the central and subcentral governments. This requires the decentralization of fiscal policy decision-making, which involves greater subcentral government autonomy in tax administration, debt management, and budget execution (De Mello, 2000). The motivation for this is the need to bring governance closer to the constituents with the potential advantages of increased government efficiency and overall welfare, and decreased political instability (World Bank, 2000).

However, the increased fiscal federalism across countries has been a matter of much concern among macro-stabilization experts (Shah, 2005). It is argued that fiscal federalism poses a threat to macro-stability because it is not compatible with prudent fiscal management (Prud’homme, 1995; Tanzi, 1995). Expenditure competition among subcentral governments could lead to the subnational governments incurring more debt to finance the expenditure. The propensity for this increases when the subcentral governments are certain they will be bailed out by the central government when they are unable to finance their deficit budgets or pay back their debts. Inappropriate subnational debt management and uncontrolled subnational budget deficit would adversely affect the general government budget balance. Also, when the property rights over revenue generation and expenditure responsibilities are not well defined among the tiers of government, the potential “tragedy of the common” would lead to fiscal indiscipline. This is because, any policy outcome from this would mostly be a result of an intergovernmental bargaining process, rather than an evolution from sound economic principles (Shah, 2005). This argument is, however, mostly theoretical with no empirical corroboration.

On the other hand, other strands of literature argue that fiscal federalism could improve fiscal discipline by ensuring that public goods and services are produced at lower costs. They opined that the closeness of the subnational governments to the final beneficiaries would foster accountability because their constituents would put pressure on them to provide public goods at minimum cost. Also, competition among subnational governments can foster cost-effectiveness, and in circumstances where there is the need to limit expenditures, the subnational governments are in a better position to prioritize the public goods and services to be provided (Sow and Razafimahefa, 2017). The reason for this is that the subnational government information advantage would help determine appropriately the preferences of the constituents, minimize the negative impacts of expenditure cuts on the populace, and reduce the social resistance to the expenditure cuts. The lack of unanimity on the fiscal discipline impact of fiscal federalism in the theoretical literature necessitates empirical studies of the fiscal discipline-fiscal federalism nexus because any adverse macro-stability impact of fiscal federalism will impact negatively on any allocative efficiency and distributive efficiency gain, it could produce. But so far, empirical studies on the relationship are limited, and also without consensus.

Moreover, Neyapti, (2013) argued that the potential of fiscal federalism to deliver fiscal discipline can be enhanced by a supportive institutional framework with well-defined and enforced fiscal policy rules at the aggregate level. Also, Shah, (2005) opines that the ability of fiscal federalism to foster fiscal discipline is more likely in a federation than in a non-federation. However, from available literature, there has been no empirical work yet on the influence of institutional framework on the fiscal discipline impact of fiscal federalism, nor on whether the fiscal discipline impact of fiscal federalism varies across federal and non-federal countries. This study attempts to fill these gaps. Moreover, fiscal balance in a country and across countries fluctuates over time, hence, the impact of fiscal federalism on fiscal discipline could vary across the distributions of fiscal discipline, within and across countries over time. In other words, the fiscal discipline impact of fiscal federalism may not be constant on the conditional mean of the fiscal discipline but vary along its conditional distribution. Economically, this implies that the fiscal discipline impact of fiscal federalism in a country may depend on its fiscal discipline history, and this could also account for the difference in the fiscal discipline impact of fiscal federalism across countries. This is a factor no previous study on fiscal discipline impact of fiscal federalism has put into consideration. Hence, this motivates the use of a panel quantile regression estimation approach in the analysis of the fiscal discipline-fiscal federalism nexus in this study.

Against this background, this study aims to shed more light on the relationship between fiscal federalism and fiscal discipline from a cross-country viewpoint. Particularly, the study contributes to the existing literature by (i) investigating the impact of fiscal federalism on fiscal discipline; (ii) exploring the influence of institutional framework on the fiscal discipline impact of fiscal federalism; (iii) investigating whether the fiscal discipline impact of fiscal federalism is boosted if a nation is a federal-state; and, (iv) analyzing the variation of the fiscal discipline impact of fiscal federalism across the distributions of the fiscal discipline. The rest of the paper is structured as follows. “Literature review” reviews the theoretical and empirical literature on the relationship between fiscal federalism and fiscal discipline. “Data and Methodology” describes the data and variables used in the empirical analysis and presents the empirical methodology used for the analysis. “Empirical results and discussion” discusses the empirical results, followed by a conclusion and policy implications in “Conclusion”.

Literature review

There is no unanimity on the effects of fiscal federalism on fiscal discipline in both theoretical and empirical literature. The classical theory of fiscal federalism assigns macro-stabilization responsibilities to the central government (Oates, 1972; Musgrave, 1959). It is argued that the subcentral governments may not be able to implement macro-stabilization policies effectively, due to their expenditure competition which could elicit a tendency not to commit fully to fiscal discipline. Hence, it is opined that fiscal federalism has the potential to endanger macro-stability because it is not compatible with prudent fiscal management (Prud’homme, 1995; Tanzi, 1995). The theoretical argument on the adverse impacts of fiscal federalism on fiscal discipline is based on the concepts of “soft budget constraints”, “coordination failure”, and “intergovernmental transfer”. A strand of literature argues that fiscal federalism, especially expenditure autonomy could result in over-borrowing by the subcentral governments, more so, if the social cost of debt is not fully internalized by the subcentral governments (Wildasin, 1997; Goodspeed, 2002). This strand of literature believes that subcentral governments will face strong incentives to over-borrow in situations where they expect a bailout from the central government, and when the central government finds it difficult to impose a “hard budget constraint” due to political reasons. De Mello, (2000) argues that coordinating intergovernmental fiscal relations becomes more complex and difficult when the subcentral governments have greater autonomy in policy decision-making. This situation which occurs as a result of the existence of several independent governments that can make revenue and expenditure decisions at their discretion could make it impossible to maintain a concerted fiscal policy and result in a lack of fiscal discipline at both the subcentral and central government levels (Baskaran, 2010). It is also argued that fiscal federalism will impede fiscal discipline when the subcentral governments are dependent on intergovernmental transfer (Rodden, 2002; Rodden, 2006). This is based on the notion that the “common pool problem” could be exacerbated by vertical transfer (Baskaran, 2010).

On the other hand, some other strands of literature argue that fiscal federalism may have a favorable impact on fiscal discipline (Weingast, 1995; Oates, 1999; Rodden and Wibbels, 2002). Their argument is derived mainly from the public choice theory (Brennan and Buchanan, 1980). They argued that fiscal federalism by bringing the policy decision-makers closer to the final beneficiaries would foster accountability because their constituents would put pressure on them to provide public goods with minimum cost. Competitions among subnational governments can also enhance cost-effectiveness, and in circumstances where there is the need to limit expenditures, the subnational governments are in a better position to prioritize the public goods and services to be provided (Sow and Razafimahefa, 2017).

Even though, the theoretical arguments on the fiscal discipline-fiscal federalism nexus are gaining more attention, empirical studies on the relationship are limited and their conclusions are mixed (Baskaran and Hessami, 2013). De Mello, (2000), Rodden, (2002), and Baskaran and Hessami, (2013) reveal that fiscal federalism has an adverse effect on fiscal discipline. De Mello, (2000) using a panel of seventeen OECD and thirteen non-OECD countries concludes that due to coordination failure, fiscal federalism worsens fiscal discipline. Rodden, (2002) shows that fiscal federalism leads to more instability in both subcentral and central government budgets. Baskaran and Hessami, (2013) used a sample of twenty-three OECD countries and concluded that both revenue and expenditure decentralization lead to higher budget deficits and worsen budgetary problems. Using the data from a panel of twenty-eight OECD countries over the period 1969–2007, Eyraud and Lusinyan, (2014) reveal that fiscal discipline is inversely related to expenditure decentralization.

Few empirical studies establish a positive relationship between fiscal federalism and fiscal discipline (Shah, 2005; Baskaran, 2010; Neyapti, 2010; Escolano et al., 2012; Governatori and Yim, 2012; Sow and Razafimahefa, 2017). Shah, (2005) using a cross-section of forty countries over the period 1995–2000 shows that fiscal federalism improves fiscal discipline. Baskaran, (2010) used a panel of seventeen OECD countries and a sample covering 1975–2001 and concluded that expenditure decentralization improves fiscal discipline while the effect of revenue decentralization is insignificant. Neyapti, (2010) using a panel sample of sixteen countries over the period 1980-1998 reveals that revenue and expenditure decentralization boost budget discipline. Escolano et al. (2012) and Governatori and Yim, (2012) establish a positive relationship between fiscal federalism and fiscal discipline for a group of European Union Member countries. Governatori and Yim, (2012) reveal that expenditure decentralization increases primary budget balance through lower expenditures and higher revenues. Sow and Razafimahefa, (2017) analyzed the panel data for a sample of 64 countries over the period 1990–2012 and concluded that fiscal federalism strengthens fiscal discipline. Neyapti, (2013) shows that fiscal federalism has a positive impact on fiscal discipline and that the effect is enhanced by fiscal rule. Presbitero et al. (2014) using a panel sample of twenty-two countries over the period 1973–2011 reveal that revenue decentralization enhances budget discipline. Asatryan et al. (2015) used a sample of twenty-three OECD countries over the 1975–2000 period, and concluded that revenue decentralization is associated with improved fiscal discipline. They further cross-validate this finding using a novel, independent dataset consisting of all thirty-four OECD member countries over the period 2000–2008.

Moreover, Freitag and Vatter, (2008) using panel data of the Swiss cantons for the period 1984–2000 reveal that fiscal decentralization has a positive impact on fiscal discipline during economically challenging times, but has no significant impact on fiscal discipline during the period of prosperous economic development in Switzerland. The reason being that during the economic recession phase, the administratively decentralized cantons were found to implement a more economical budgetary policy than the centralized Swiss member states. Also, Akin et al. (2016) conclude that fiscal decentralization promotes fiscal discipline if the budgetary constraint is binding. Thornton (2009) used a panel of nineteen OECD countries and a sample covering 1980–2000 and concluded that revenue decentralization has no significant impact on fiscal discipline.

The lack of unanimity on the effects of fiscal federalism on fiscal discipline in both theoretical and empirical literature motivates the need for more studies on the fiscal discipline impact of fiscal federalism. Also, the very little attention that has been given in the existing literature to investigating this relationship empirically leaves a number of theoretical propositions or claims on factors that could influence the fiscal discipline impact of fiscal federalism unverified. Some of these unverified propositions include; the influence of institutional framework on the fiscal discipline impact of fiscal federalism, variation of the fiscal discipline impact of fiscal federalism across federal and non-federal states, and the possible variation of the fiscal discipline impact of fiscal federalism across the distributions of the fiscal discipline. Hence, this paper in addition to investigating the relationship between fiscal federalism explores the aforementioned hitherto unverified propositions on the fiscal discipline-fiscal federalism nexus. In this regard, this study chooses to provide answers to the following research questions: what is the impact of fiscal federalism on fiscal discipline? How does institutional framework affect the fiscal discipline impact of fiscal federalism? What is the influence of a nation being a federation on fiscal discipline impact of fiscal federalism? How does each of the fiscal discipline impact of fiscal federalism, the effect of federation on fiscal discipline impact of fiscal federalism, and the influence of institutional framework on fiscal discipline impact of fiscal federalism, vary along the distribution of the fiscal discipline? These relationships were analyzed using the panel two-stage least squares technique as a baseline estimation technique and panel quantile regression as the main estimation technique.

Data and methodology

Data and variables definition

The study employs data for twenty selected countries over the period 1996–2018 to investigate the relationship between fiscal federalism and fiscal discipline. The twenty selected countries are Australia, Austria, Belgium, Canada, Chile, Estonia, Germany, Hungary, Israel, Japan, Latvia, Netherlands, Nigeria, Norway, Peru, South Africa, Spain, Switzerland, Thailand, and the United States of America. The choice of the sample under investigation is dictated by the issue of data availability, particularly because of the lack of sufficient fiscal federalism and fiscal discipline indicators data for most of the other countries. The countries consist of eight federations and twelve non-federations. The data used for the empirical analysis are sourced from the World Bank online database, IMF’s Government Finance Statistics, and World Economic Outlook. The main goal of the study is to investigate the impact of fiscal federalism on fiscal discipline while controlling for other determinants of fiscal discipline. The variables used in the analysis are described below.

Dependent variables

The dependent variables are the measures of fiscal discipline. Two variants of the general government fiscal balance are used as the measures of fiscal discipline in the study, and they include the primary budget balance (PBB) and structural budget balance (SBB) of the general government. Each of the indicators was used separately as a dependent variable in the various estimations. The general government fiscal or budget balance is the difference between the combined revenue and combined expenditure of the central and subcentral governments. It could be positive, in which case it is a surplus; negative, which is a deficit; or zero, in which case it is said to be balanced because the revenue is equal to the expenditure. The primary budget balance refers to the fiscal balance excluding the net interest payments on public debt. In other words, it is the difference between the amount of revenue generated by the government and the amount spent by the government in providing public goods and services. It is an indicator of the short-term sustainability of the government’s finances (OECD, 2021).

The structural budget balance represents what the fiscal balance will be when output is at its potential level. In other words, it is the fiscal balance that would be realized if the economy were to grow steadily at its maximum sustainable rate of employment. This implies that the structural budget balance is a cyclically adjusted fiscal balance. The adjustment is done by correcting for temporary factors that could affect the balance and thereby conceal the real fiscal position. Some of the factors the fiscal balance is corrected for are commodity shocks, asset prices, output composition and absorption effects, and one-off factors. This adjustment which is necessary for fiscal sustainability makes the structural budget balance superior to the primary budget balance. Also, by purging out the cyclical and temporal effects in the fiscal balance, the structural budget balance serves as a better measure of the discretionary actions of fiscal authorities. It is partly designed to provide an indication of the medium-term orientation of fiscal policy (Hagemann, 1999).

Fiscal balance and the level of national debt are the standard and most popular indicators of fiscal discipline in the literature. However, the former is preferred because it is a flow variable, and could well capture the variations over time of fiscal discipline. Fiscal discipline could also be captured by an ability to meet a specified fiscal objective. In that sense, deviation from a target would be a measure of fiscal discipline. The ability to meet a given fiscal objective in terms of fiscal discipline could also be captured by fiscal balance, in which case fiscal balance could be a target, and a deviation from it, especially deficit balance, could be a sign of fiscal indiscipline. However, using a deviation from the target level of a chosen fiscal objective could be difficult to employ in a cross-country analysis, since different countries could have different fiscal objectives at a point in time. Also, the data for such targets could be limited. However, this will be worth exploring as consideration for future study, especially in individual country analysis, where such data may be available, and the country’s peculiarity could be put into consideration in the analysis. Hence, this has been included in this study as a limitation of the study.

Independent variables

The main regressors of interest are the fiscal federalism indicators. The study makes use of the two most widely used indicators: “revenue decentralization” (RDEC)- the ratio of subnational (regional). government revenue to total government revenue (sum of subnational and federal governments revenue), and “expenditure decentralization” (EDEC)- the ratio of subnational government expenditure to total government expenditure (sum of subnational and federal governments expenditure). These indices denote the overall extent of fiscal decentralization, that is, the size of resources controlled by the subnational government. The indicators are used sequentially in the regression analyses to avoid multicollinearity.

Control variables

The control variables used are the commonly used determinants of general government fiscal balance in the literature (Neyapti, 2010; Baskaran and Hessami, 2013; Sow and Razafimahefa, 2017). The main control variables used include government size, gross domestic product per capita growth rate, population growth rate, public debt, inflation rate, and current account balance.

-

Government size (GOVSIZE): This is the general government’s final consumption expenditure as a percentage of the gross domestic product. The general government’s final consumption expenditure is made up of all government current expenditures for purchases of goods and services, including compensation of employees and most expenditures on national defense and security. The a priori expectation is that large government tends to have an adverse impact on fiscal balance.

-

Gross domestic product per capita growth rate (GDPPCGR): This is the annual percentage growth rate of gross domestic product per capita based on constant local currency. The aggregates are based on constant 2010 U.S. dollars. GDP per capita refers to the gross domestic product divided by midyear population. Based on the World Bank computation, the gross domestic product is calculated in terms of the purchaser’s prices. This is the sum of gross value added by all resident producers in the economy. Product taxes are included, and subsidies are excluded from the value of the products. In the calculation, no deductions are made for depreciation of fabricated assets or for depletion and degradation of natural resources. The economic growth rate accounts for business cycle, and it is expected to have a positive effect on the government’s fiscal stance.

-

Population growth rate (POPRATE): This is annual percentage growth in population. The annual population growth rate for a given year is the exponential rate of growth of the midyear population between the prior year and the given year. It is expressed as a percentage. All residents regardless of their legal status or citizenship are included in the population. In other words, the de facto definition of population is used. Population serves as a measure of heterogeneity in preferences.

-

Public debt (PUBDEBT): This is the net debt of the general government as a percentage of the gross domestic product. General government debt refers to the entire stock of direct general government (central and subcentral governments) fixed-term contractual obligations to other entities, which are outstanding on a particular date. This includes domestic and foreign liabilities such as currency and money deposits, securities other than shares, and loans. It is the total amount of government liabilities reduced by the amount of equity and financial derivatives held by the government. Being a stock rather than a flow, debt is measured as of a given date, usually the last day of the fiscal year. The net debt is the gross debt minus those financial assets which correspond to debt instruments. The impact of the general debt on fiscal discipline depends on the level of the public debt. The European Union Commission recommends a maximum debt-to-GDP ratio of 60%.

-

Inflation rate (INFR): The inflation rate used is the annual growth rate of the gross domestic product implicit deflator. This shows the rate of price change in the economy as a whole. The GDP implicit deflator is the ratio of the gross domestic product in current local currency to the gross domestic product in constant local currency.

-

Current account balance (CABAL): This is the government’s current account balance as a percentage of the GDP. The current account balance is the sum of net exports of goods and services, net primary income, and net secondary income.

Other variables used in the empirical analysis in this study are the federation dummy, the institutional framework measure (INSTQ), and the polity index (POLINDEX). The federation dummy takes a value of one if the country is a federation and zero otherwise. It is used in an interaction with each of the fiscal federalism measures to assess the variation of the fiscal discipline impact of fiscal federalism across federal and non-federal countries. The measure of institutional framework used is the World Bank’s “quality of governance” index. This is the World Bank’s Worldwide Governance Indicators (WGI) computed by Kaufmann et al. (2010). The WGI comprises aggregate indicators of six broad governance dimensions: Voice and Accountability (VNA), Political Stability and Absence of Violence/Terrorism (PS), Government Effectiveness (GE), Regulatory Quality (RQ), Rule of Law (ROL), and Control of Corruption (COC). The six aggregate indicators are based on several hundred individual underlying variables, from a wide variety of existing data sources which report the perceptions of governance of many respondents and expert assessments worldwide (Kaufmann et al., 2010). The “quality of governance” index ranges from −2.5 (weak institutional framework) to 2.5 (strong institutional framework), so by adding up, one gets a scale of +15 to −15. The aggregate index is used in an interaction with each of the fiscal federalism measures to explore the influence of institutional framework on the fiscal discipline impact of fiscal federalism. The choice of the “quality of governance” index over other measures of institutional framework is based on the fact that it includes not only economic component, but also, political, legal, and social components. In other words, it captures a broader spectrum of institutional quality assessment. Furthermore, it involves actions from both the policy decision-makers and the citizens. In fact, Islam and Montenegro, (2002) succinctly opine that the advantage of the WGI over other measures of institutional quality is that it aggregates information from different sources, and probably contains less measurement error.

The polity index is the revised combined polity score, and it is used as an additional instrument in the panel two-stage least squares estimation and the panel quantile regression. The polity index is a measure of the governing authority spectrum of a country. It spans from fully institutionalized autocracies at one extreme to fully institutionalized democracies at the other, with mixed or incoherent authority regimes in between. Hence, rather than treating autocracy and democracy as discreet and mutually exclusive, it examines the concomitant qualities of both in governing institutions (Polity IV, the Centre for the Systemic Peace). The 21-scale index ranges from −10 (hereditary monarchy) to +10 (consolidated democracy). It is introduced as an additional instrumental variable to strengthen the instrumental variable estimations because it is correlated with fiscal federalism, and exogenous with respect to fiscal balance. Moreover, while it is opined that each of autocratic and democratic regimes could impact fiscal discipline, there is no unanimity in the literature on whether the impact of one is positive while that of the other is negative. In other words, each could have a positive or negative impact depending on the willpower of the incumbent government at a point in time. Moreso, a democratic rule could impact positively fiscal discipline in a strong democracy than in a weak democracy (Beyala and Owoundi, 2025). This factor also justifies the choice of the type of polity index used in this study. The summary statistics for the variables are shown in Table 1 below.

Empirical methodology

The study makes use of a number of panel estimation techniques for the empirical analysis. The panel two-stage least squares (2SLS) technique was used as the baseline estimation technique, and the panel quantile regression technique was used as the main technique of interest. Both techniques are used within an instrumental variable estimation framework in order to account for potential endogeneity, which could arise as a result of the possible reversed causality between fiscal discipline and fiscal federalism, or due to the presence of the lagged dependent variable in the dynamic model. The instruments used are all the control variables in addition to the polity index. The first lag of each of the indicators of fiscal discipline was controlled for in their respective models, so as to eliminate any potential estimation bias that could arise from the autoregressive structure of the fiscal balance variables.

Two-stage least squares technique

In line with Neyapti, (2013) and Sow and Razafimahefa, (2017), the study used the two-stage least squares instrumental variable technique to investigate the relationship between fiscal federalism and fiscal discipline. Unlike Neyapti, (2013) and Sow and Razafimahefa, (2017) who used the technique as their main estimation technique, this study used the technique as a baseline estimation technique. The rationale for the use of the two-stage least squares instrumental variable technique is the potential endogeneity of the fiscal federalism indicators, and possible endogeneity due to the lagged dependent variable in the dynamic model. The technique also helps to deal with any issue of possible reverse causality between the fiscal discipline indicators and the fiscal federalism measures. The instruments used are all the control variables in addition to the polity index. The first lag of each of the indicators of fiscal discipline was also controlled for in their respective models, so as to eliminate any potential estimation bias that could arise from the autoregressive structure of the fiscal balance variables. The panel two-stage least squares was estimated using the fixed effect (FE) and the random effect (RE) specifications. The choice of the preferred estimator in each estimation being decided using the Hausman test-statistics. Specifically, in order to investigate the impact of fiscal federalism on fiscal discipline the following benchmark regression model was considered:

where, the subscript it stands for country (i)-year (t) observation; \({{FD}}_{{it}}\) is the fiscal discipline for country i, which is proxied by the primary budget balance and the structural budget balance; \({{FD}}_{{it}-1}\) is the lagged of the measure of fiscal discipline; \({{FF}}_{{it}}\) is the measure of fiscal federalism, which include the revenue decentralization and the expenditure decentralization; \({Z}_{{it}}\) is a vector of control variables; \(\beta\) is the autoregressive coefficient; \(\delta\) measures the impact of fiscal federalism on fiscal discipline; \({\gamma }_{i}\) and \({\mu }_{t}\) denote sets of country and time fixed effects respectively; and \({\varepsilon }_{{it}}\) is a stochastic error term.

The first stage in the 2SLS estimation involves an OLS regression of the fiscal federalism indicator (endogenous regressor) on the other control variables and the instrumental variable. This is to get predicted values for the fiscal federalism indicator, which will no longer be endogenous or correlated with the error term. The second stage is the OLS estimation of the fiscal discipline indicator on the predicted fiscal federalism values, and the control variables, and then correcting the standard errors to account for the substitution of the actual values of the fiscal federalism indicator by its predicted values. The main coefficients of interest are the coefficients of the regressors in the second stage. The “xtivregress” command in Stata used for the analysis in this study help to achieve the two stages in a single estimation, and gives the corrected standard error directly. However, the first stage regression is also separately estimated in order to determine the suitability of the chosen instrumental variables, which are the polity index, and the first and second lags of each of revenue decentralization and expenditure decentralization respectively. The first stage regression equation is as shown below:

where, \({{IV}}_{{it}}\) is a vector of instrumental variables; \(\sigma\) measures the impact of the instrumental variable on fiscal federalism.

Panel quantile regression

The study makes use of the panel quantile regression technique as the main estimation technique. The motivation for this is that since fiscal balance fluctuates over time and across countries, the fiscal discipline impact of fiscal federalism could vary across the distributions of the fiscal discipline. The standard least squares regression techniques summarize the average relationship between a set of regressors or independent variables and the dependent or outcome variable based on the conditional mean function. In other words, the standard least squares techniques provide estimates based on the average effect of the independent variable(s) on the average dependent variable. This only gives a partial view of the relationship between the dependent and the independent variables (Baum, 2013). It might be necessary to describe the relationship at different points in the conditional distribution of the dependent variable. The quantile regression technique is a useful tool in such instance. Quantile regression allows for the effects of the independent variables to vary over the quantiles of the dependent variable. The quantile regression technique has a number of advantages over the standard least squares techniques: (i) it is more robust to outliers and non-normal errors, (ii) it describes the entire conditional distribution of the dependent variable, and (iii) it is invariant to monotonic transformations (Baum, 2013). In line with Koenker and Bassett, (1978), the quantile regression model is presented thus:

where \({{FD}}_{{it}}\) is fiscal discipline; \({x}_{{it}}\) is a vector of regressors, which include the fiscal federalism indicators, the control variables and additional instrument; \(\beta\) is the vector of the parameters to be estimated; \(u\) is a vector of residuals. \({{Quant}}_{\theta }({{FD}}_{{it}}/{x}_{{it}})\) identifies the \(\theta {th}\) conditional quantile of FD given x.

Specifically, the study estimates a quantile regression model for panel data (qregpd) with nonadditive fixed effects (Baker et al., 2016; Powell, 2016). The non-separable disturbance term commonly associated with quantile estimation is maintained and the model is estimated in an instrumental variable framework to account for potential endogeneity. The 25th, 50th, and 75th quantiles were estimated for the various models.

In order to address the research focus, a number of different models were estimated using both the baseline and main estimation techniques. This started with the benchmark model, which involves each of the fiscal discipline measure, each measure of fiscal federalism, the control variables, and the additional instrument. The intent of this is to investigate the impact of fiscal federalism on fiscal discipline. Then in order to explore the influence of institutional framework on the fiscal discipline impact of fiscal federalism, two interaction variables (IRDEC and IEDEC) were generated using the institutional framework indicator and each of the measures of fiscal federalism. Each interaction variable was then introduced into the benchmark model appropriately. Similarly, in order to investigate if the fiscal discipline impact of fiscal federalism varies across federation and non-federation countries, interaction terms (RDECF and EDECF) involving the federation dummy and each of the measures of fiscal federalism were introduced appropriately into the benchmark model. In each scenario, the coefficient of the interaction term is the parameter of interest for decision making. The panel quantile regressions help to determine if the fiscal discipline impact of fiscal federalism varies across the distribution of the fiscal discipline in the various models.

Empirical results and discussion

This section discusses the results of the empirical estimations performed in the study. The analysis started with the preliminary data analysis involving the summary statistics, pairwise correlation, and graphical examination of the relationship between fiscal discipline and fiscal federalism. Thereafter, the baseline regression analysis using the panel two-stage least squares technique follows. Then main regression of interest using the panel quantile estimation technique was then performed.

Pairwise correlation and graphical relationship

A preliminary pairwise correlation analysis reveals a negative correlation between revenue decentralization and primary budget balance, and a positive correlation with structural budget balance. This seem to suggest that revenue decentralization is only positively correlated with fiscal discipline when the cyclical and temporary components of the fiscal discipline are controlled for. Expenditure decentralization is shown to be positively correlated with both primary budget balance and structural budget balance. However, the correlations were weak in all the cases. Regarding the correlation between the fiscal discipline indicators and the control variables, all except the correlation with inflation rate are appropriately signed based on a priori expectations. The correlation between each of the indicators of fiscal discipline (PBB and SBB) and inflation rate is also very weak. The result of the pairwise correlation is shown in Table 2 below. Also, Fig. 1 shows the scatter plots and fitted lines of the various fiscal discipline indicator against the different measures of fiscal federalism. It gives a first impression of the relationships between the fiscal discipline indicators and the measures of fiscal federalism. For each pair of the fiscal discipline indicators against the fiscal federalism measures, the graphs were plotted without controlling for the control variables, and by controlling for the control variables. Without the control variables, the best fit lines show that that each of RDEC and EDEC are nearly invariant with each of PBB and SBB. This is in line with the weak correlation obtained between the fiscal discipline indicators and the fiscal federalism measures. However, when the control variables are controlled for, the relationship between each of RDEC and EDEC, and with each of PBB and SBB became more glaring. This signifies that the exact relationship between fiscal federalism and fiscal discipline still has to be investigated empirically to account for confounding factors.

a PBB vs RDEC (without control variables) b PBB vs EDEC (without control variables). c SBB vs RDEC (without control variables) d SBB vs EDEC (without control variables). e PBB vs RDEC (with control variables). f PBB vs EDEC (with control variables). g SBB vs RDEC (with control variables). h SBB vs EDEC (with control variables).

Results of panel two-stage least squares instrumental variable (2SLS-IV) estimations

The Hausman test-statistic results show the panel 2SLS-IV with random effect estimator (2SLS-IV-RE) as the preferred estimation technique in the benchmark model involving the primary budget balance, revenue decentralization, control variables and other instrument. 2SLS-IV-RE is also found to be the preferred model in all the models involving the federation-fiscal federalism interaction term. The panel 2SLS-IV with fixed effect estimator (2SLS-IV-FE) is the preferred estimation technique in all the other models. The results show that revenue decentralization has a statistically significant positive impact on primary budget balance, but no significant impact on structural budget balance. Expenditure decentralization is shown not to have any statistically significant impact on both primary budget balance and structural budget balance. It is also revealed that institutional framework does not influence the fiscal discipline impact of fiscal federalism. However, being a federation is found to have an adverse influence on the impact of each of revenue decentralization and expenditure decentralization on the general government primary budget balance, but a positive influence on the impact of each of revenue decentralization and expenditure decentralization on the general government structural budget balance. This suggests that being a federation only has positive influence on the fiscal discipline impact of fiscal federalism when the cyclical and transitory components of the general government fiscal balance are controlled for.

It is worthy of note that the models with the statistically significant impacts are where the 2SLS-IV-RE is the preferred estimator, while none of the models where the 2SLS-IV-FE is the preferred estimator gives any statistically significant relationship between fiscal discipline and fiscal federalism. This is suggestive of the fact that the mixed results in the limited empirical literature on the fiscal discipline-fiscal federalism nexus could be due to the choice of estimation technique. It could also be an indication that the impact of fiscal federalism on fiscal discipline might not be constant on average but varies at different points in the conditional distribution of the fiscal discipline, and as such calls for the use of the panel quantile regression estimation technique. Also, the autoregressive coefficient is statistically significant in all the estimations. The implication of this is that past values of fiscal discipline influence its present value, and the impact of fiscal federalism on fiscal discipline could vary at different levels along the distribution of the fiscal discipline. The results of the two-stage least squares estimations are presented in Tables A1–A6 in the Appendix.

The result of the first stage regression of the two-stage least squared estimation shows that the polity index has a statistically significant negative impact on revenue decentralization and statistically significant positive impact on expenditure decentralization. This means that the polity index is a good instrument for both the revenue decentralization and the expenditure decentralization. Also, the first and second lags of each of revenue decentralization and expenditure decentralization are positively related to each of them respectively. Overall, the instrumental variables used for the two-stage least squared estimations are appropriate. The result also reveals that none of the control variables has a significant impact on either the revenue decentralization or expenditure decentralization. This shows that the control variables are strictly exogenous. The result is presented in Tables A7 in the Appendix.

Panel quantile regression results

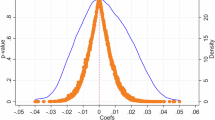

Figure 2 below shows the quantile plots for the primary budget balance and the structural budget balance. The symmetric nature of the graphs justifies the use of the quantile regression technique. The results of the quantile regression estimations for various models are presented in Tables A8 to A13 in the Appendix. The results of the benchmark models revealed that both revenue decentralization and expenditure decentralization have statistically significant impacts on each of primary budget balance and structural budget balance at all estimated quantile levels. The impact is negative at the lower quantile level (25th quantile) and positive at the upper quantile level (75th quantile). This implies that fiscal federalism has an adverse impact on fiscal discipline at the lower quantile level in the conditional distribution of the fiscal discipline, and fiscal federalism improves fiscal discipline at the upper quantile level in the conditional distribution of the fiscal discipline. This suggests that the fiscal discipline impact of fiscal federalism depends on the level of fiscal discipline that is in existence in a country at a point time, and that it is beneficial in a country that is already fiscally disciplined, and not one with the history of fiscal indiscipline. This confirms the endogeneity concerns in the empirical methodology.

a Primary budget balance. b Structural budget balance.

The results of the models involving the institutional framework-fiscal federalism interaction term show that institutional framework positively influenced the fiscal discipline impact of fiscal federalism along all estimated quantile levels of fiscal discipline. This is suggestive of the fact that the fiscal discipline impact of fiscal federalism is improved when governments and policy decision-makers at all levels become more effective, accountable, transparent, less corrupt, and in a country with political stability, well enshrined rule of law, effective regulatory quality, and where the citizens have a voice on policy decisions. This is in line with Acemoglu and Robinson, (2010) argument that better institutional framework boosts transparency, accountability, and responsibility of policy decision making. Also, this findings agrees with Neyapti theoretical argument that supportive institutional framework could improve the fiscal discipline impact of fiscal federalism. Moreover, the results revealed that the positive influence of institutional framework on the fiscal discipline impact of fiscal federalism is higher at the lower quantile level than at the higher quantile level of fiscal discipline. This could be expected because countries with higher level of fiscal discipline would have had some reasonable degree of institutional quality already in place. For the countries initially with low level of fiscal discipline, a quality institutional framework will not only enhance the effectiveness of their fiscal federalism apparatus, but also, directly boost their level of fiscal discipline.

On the variation of the fiscal discipline impact of fiscal federalism across federal and non-federal states, this study reveals that being a federation has a positive influence on the fiscal discipline impact of fiscal federalism. This is in consonance with Shah, (2005) argument that the ability of fiscal federalism to foster fiscal discipline is more likely in a federation than a non-federation. According to Shah, (2005) “experiences of federal countries indicate significant learning and adaptation of fiscal systems to create incentives compatible with fair play and to overcome incomplete contracts”. This means that the relatively more autonomy of the subcentral governments in a federation could lead to a better design and application of the fiscal decentralization apparatus, than in non-federations where the subcentral governments could just be an administrative unit of the central government. Furthermore, the results show that the positive influence is more elastic at the lower quantile level than the higher quantile of fiscal discipline.

Conclusion

The impact of fiscal federalism on government’s fiscal discipline has become a matter of serious concern among a number of macro-stabilization experts in recent times due to the paradigm shift towards fiscal decentralization across countries over the last three decades. The early literature on the issue argues that fiscal federalism works against fiscal discipline because it is not compatible with prudent fiscal management. However, some other strands of literature disagree with this view and argue that fiscal federalism could actually improve fiscal discipline because it brings the policy decision-makers closer to the scrutinizing eyes of the final beneficiaries of public goods and services, who could ask policymakers for accountability. However, the arguments for and against the fiscal discipline impact of fiscal federalism have been mostly theoretical, and empirical studies on the relationship are still quite limited and mixed. Therefore, this research contributes to the fiscal discipline-fiscal federalism literature by shedding more light on the relationship by empirically investigating some of the hitherto theoretical propositions on the fiscal discipline-fiscal federalism nexus.

This study reveals that the impact of fiscal federalism on fiscal discipline varies along the conditional distribution of the fiscal discipline, being negative at the lower quantile level and positive at the upper quantile level. The economic meaning of this is that fiscal federalism will adversely impact fiscal discipline in a country with a previous history of fiscal indiscipline, and further boost fiscal discipline if the country has a history of being fiscally disciplined. It is also shown that a supportive institutional framework positively influences the fiscal discipline impact of fiscal federalism and that this is more so at the lower quantile level than at the higher quantile level of the conditional distribution of the fiscal discipline. Furthermore, a country being a federation is also found to boost the fiscal discipline impact of fiscal federalism at all levels of the conditional distribution of the fiscal discipline, with the impact being more elastic at the lower quantile level than at the upper quantile level of fiscal discipline.

More generally, this study establishes that there exists a link between fiscal federalism and fiscal discipline. Specifically, the study concludes that the impact of fiscal federalism on fiscal discipline may not be constant on the conditional mean of the fiscal discipline, but vary along its conditional distribution. Hence, the study is in line with both the arguments for and against the fiscal discipline impact of fiscal federalism in the existing literature and concludes that the impact could be either positive or negative depending on the history and initial level of fiscal discipline in a country. In other words, while fiscal federalism may boost fiscal discipline in a country with a history of fiscal prudence, it may worsen the fiscal discipline, if the country is initially fiscally imprudent. Moreover, better institutional framework and federalism improve the fiscal discipline impact of fiscal federalism, and countries with a history of low fiscal discipline stand to benefit more from this. The policy implication of this is that in the design and operation of the fiscal federalism apparatus, policy decision-makers should take into consideration the fiscal discipline history of the country. The design of fiscal decentralization apparatus should be appropriately tailored towards each country’s peculiar characteristics and government fiscal stance. Also, it is essential that a quality institutional framework be put in place to support the fiscal decentralization apparatus. Therefore, it is recommended that in the design and operation of fiscal federalism apparatus in a country with a history of low levels of fiscal prudence, a good institutional framework should also be put in place, if the positive impact of fiscal federalism on fiscal discipline is to be realized. Also, for a country with a history of high levels of fiscal discipline, the adoption and proper operation of a well-designed fiscal federalism apparatus will be a blessing and not a curse, because it will strengthen fiscal discipline.

Limitations of the study

As a measure of fiscal discipline, the study made use of fiscal balance, which is one of the two commonly used indicators of fiscal discipline in the literature, the other being the level of national debt. However, the degree of adherence to or deviation from a targeted fiscal objective could also be considered a measure of fiscal discipline, especially in a single-country analysis. This could be difficult to employ in a cross-country analysis as each country could have different fiscal objectives.

Data availability

The data used for the empirical analysis are secondary data sourced from the World Bank online database, IMF’s Government Finance Statistics, and World Economic Outlook. The datasets are available from the corresponding author upon reasonable request.

References

Acemoglu D, Robinson J (2010) The role of institutions in growth and development. Review of Economics and Institutions, 1(2), https://doi.org/10.5202/rei.v1i2.1. Retrieved from http://www.rei.unipg.it/rei/article/view/14

Akin Z, Bulut-Cevik ZB, Neyapti B (2016) Does fiscal decentralization promote fiscal discipline. Emerging Markets Finance Trade 52:690–705

Asatryan Z, Feld LP, Geys B (2015) Partial fiscal decentralization and sub-national government fiscal discipline: empirical evidence from OECD countries. Public Choice 163:307–320. https://doi.org/10.1007/s11127-015-0250-2

Baker M, Powell D, Smith TA (2016) QREGPD: stata module to perform quantile regression for panel data. Statistical Software Components S458157, Boston College Department of Economics, Boston College, MA, USA

Baskaran T (2010) On the link between fiscal decentralization and public debt in OECD countries. Public Choice 145(3):351–378

Baskaran T, Hessami, Z (2013) Fiscal decentralization and budgetary stability: transitory effects and long-run equilibria. European Commission Workshop 2012-11-27. https://ec.europa.eu

Baum CF (2013) Lecture on Quantile regression. Personal collection of Christopher F. Baum, Boston College, Chestnut Hill, Massachusetts, USA

Beyala BCN, Owoundi JPF (2025) The effects of fiscal rule on budget deficit does democracy matter? J Compar Econ https://doi.org/10.1016/j.jce.2025.01.005

Brennan G, Buchanan J (1980) The power to tax: analytical foundations of a fiscal constitution. Cambridge: Cambridge University Press

De Mello LR (2000) Fiscal decentralization and intergovernmental fiscal relations: a cross country analysis. World Dev 28(2):365–380

Escolano J, Eyraud L, Moreno-Badia M, Sarnes J, Tuladhar A (2012) Fiscal performance, institutional design and decentralization in European Union Countries. IMF Working Paper WP/12/45. International Monetary Fund; Washington DC, USA

Eyraud L, Lusinyan L (2014) Vertical fiscal imbalances and fiscal performance in advanced economies. J Monetary Econ 60:571–587

Freitag M, Vatter A (2008) Decentralization and fiscal discipline in subnational governments: evidence from the Swiss federal system. Publius: The Journal of Federalism 38(2):272–294. https://doi.org/10.1093/publius/pjm038

Goodspeed TJ (2002) Bailouts in a federation. Int Tax Public Finance 9(4):409–421

Governatori M, Yim D (2012) Fiscal decentralization and fiscal outcome. Economic Papers 2008–2015, 468. Directorate General Economic and Financial Affairs (DG ECFIN), European Commission

Hagemann R (1999) The structural budget balance: the IMF methodology. IMF Working Paper WP/99/95. International Monetary Fund; Washington DC, USA

Islam R, Montenegro CE (2002) What determines the Quality of Institutions? Background paper for World Development Report 2002. Policy research working paper 2764

Kaufmann D, Kraay A, Mastruzzi M (2010) “The Worldwide Governance Indicators: a Summary of Methodology, Data, and Analytical Issues”. World Bank Policy Research Working Paper No. 5430. World Bank; Washington DC, USA. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1682130

Koenker R, Bassett G (1978) Regression quantiles. Econometrica 46:33–50

Musgrave RA (1959) The Theory of Public Finance: A Study in Public Economy. New York: McGraw-Hill

Neyapti B (2010) Fiscal decentralization and deficits: international evidence. Eur J Polit Econ 26(2):155–166

Neyapti B (2013) Fiscal decentralization, fiscal rules, and fiscal discipline. Econ Lett 121(3):528–532

Oates WE (1972) Fiscal Federalism. New York: Harcourt Brace Jovanovich

Oates WE (1999) An essay on fiscal federalism. J Econ Literature 37:1120–1149

OECD (2021) General government fiscal balance. Government at a glance 2021. OECD Library

Powell D (2016) Quantile Regression with Nonadditive Fixed Effects. Retrieved from http://works.bepress.com/david_powell/1/

Presbitero AF, Sacchi A, Zazzaro A (2014) Property tax and fiscal discipline in OECD countries. Econ Lett 124(3):428–433

Prud’Homme R (1995) The dangers of decentralization. World Bank Res Observer 10:201–220

Rodden J (2002) The dilemma of fiscal federalism: grants and fiscal performance around the world. Am J Polit Sci 46(3):670–687

Rodden J (2006) Hamilton’s Paradox: The promise and peril of fiscal federalism. Cambridge: Cambridge University Press

Rodden J, Wibbels E (2002) Beyond the fiction of federalism Macroeconomic management in multitiered systems. World Politics 54(3):494–531

Shah A (2005) Fiscal decentralization and fiscal performance. IMF Policy Research Working Paper 3786. International Monetary Fund; Washington DC, USA

Sow M, Razafimahefa I (2017) Fiscal decentralization and fiscal policy performance. IMF Working Paper WP/17/64. International Monetary Fund; Washington DC, USA

Stossberg S, Bartolini D, Blochliger H (2016) Fiscal decentralisation and income inequality: empirical evidence from OECD Countries. OECD Economics Department Working Papers No 1331. OECD Publishing, Paris, France

Tanzi V (1995) Fiscal federalism and decentralization: a review of some efficiency and macroeconomic aspects. In: Proceedings of the Annual World Bank conference on development economics, 1–2:295–330

Thornton J (2009) The (non)impact of revenue decentralization on fiscal deficits: some evidence from OECD countries. Appl Econ Lett 16(14):1461–1466

Weingast B (1995) The economic role of political institutions. Market preserving federalism and economic development. J Law Econ Organization 11:1–31

Wildasin D (1997) Externalities and bailouts: hard and soft budget constraints in intergovernmental fiscal relation. World Bank Policy Research Working Paper No. 1843. World Bank; Washington DC, USA

World Bank (2000) World Development Report 1999/2000. Entering the 21st century. New York: Oxford University Press

Author information

Authors and Affiliations

Contributions

This paper was written by Kayode Olaide under the supervision of Beatrice D. Simo-Kengne and Josine Uwilingiye. Data collection and empirical analysis were carried out by Kayode Olaide. The first and final drafts were also written by Kayode Olaide. The two supervisors were responsible for proof-reading and correction of the manuscript. The three authors brainstormed on the estimation technique and agreed on the use of the Panel Quantile Regression technique. All authors have read and agreed to the published version of the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Informed consent

Informed consent is not required for this study because it made use of publicly available secondary data and does not involve human or animal participants.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Olaide, K., Uwilingiye, J. & Simo-Kengne, B.D. The relationship between fiscal federalism and fiscal discipline: panel quantile regression approach. Humanit Soc Sci Commun 12, 161 (2025). https://doi.org/10.1057/s41599-025-04489-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-025-04489-5