Abstract

Climate change has a profound impact on socio-economic systems, and climate finance stands as one essential tool for combating and alleviating its disastrous effects. This research draws on an OECD project database, identifies 98 countries, and conducts empirical analysis on the deployment of climate finance across the primary, energy, and water sectors over the period 2010–2021. It further delves into climate finance efficacy across different sectors within country groups characterized by distinct features. The findings reveal that, first, climate finance is able to raise the power output of the recipient nations. Second, in the agriculture-based primary industry, adapting climate finance notably boosts the value added. Third, climate finance applied to the water sector does not significantly affect any increase in freshwater withdrawals. Lastly, heterogeneity analysis demonstrates that income and resource endowments significantly influence the effectiveness of climate finance across various sectors. Based on the findings, this paper offers relevant policy recommendations.

Similar content being viewed by others

Introduction

Global climate governance confronts various formidable challenges, as climate change-related disasters have inflicted immense damage upon human society and the economy. In response to this challenge, nations around the world have initiated concerted efforts to combat climate change together. At the most recent Conference of the Parties (COP27 and COP28), the global society has redirected its focus towards the significance of climate finance. The notion of climate finance initially emerged from financial assistance for climate initiatives that developed nations extended to developing countries within the Kyoto Protocol (Cadman, 2014; Gupta, 2016). The Copenhagen Accord of 2009 then specified targets for developed nations to finance climate adaptation and mitigation efforts in developing countries, leading to the formation of two categories of climate finance with different objectives: adaptation funds and mitigation funds (Colenbrander et al., 2018; Khan et al., 2020). These funding categories are extensively allocated to 25 sub-sectors, such as energy, agriculture, and water resources, with the goal of facilitating low-carbon transformations and climate change adaptability on a global scale (Sarr, 2022).

The adaptation and mitigation of climate finance are of paramount importance in combating climate change. Its adaptation is mainly dedicated to bolstering the resilience of fragile nations and regions against climate change by diminishing climate hazards, exemplified by the establishment of flood defense mechanisms and the amelioration of agricultural irrigation networks (Barrett, 2013; Surminski and Oramas-Dorta, 2014). Climate finance mitigation chiefly targets to back initiatives and technologies that curtail carbon emissions, including the advancement of renewable energy sources and the enhancement of energy efficiency (Bhandary et al., 2021; Briera and Lefèvre, 2024; Zhang et al., 2022). The two types of funding not only focus on addressing climate change, but also have synergistic impacts. For example, renewable energy initiatives in developing countries funded by mitigation climate finance both curtail the release of greenhouse gases and also augment the energy provision capacity of these countries, fortifying their climate change adaptability (He et al., 2024; Tian et al., 2024).

The considerable outlay in climate finance and its effectiveness in meeting adaptability and mitigation objectives have attracted the interest of numerous academics (Garschagen and Doshi, 2022; Xie et al., 2023). The literature has generally focused on the efficacy of climate finance (Lee et al., 2022; Li et al., 2020; Zeng et al., 2022). Several investigations have indicated that climate finance helps decrease carbon emissions, and mitigation funding exerts a more substantial influence on emissions compared to adaptation funding (Klöck and Nunn, 2019; Lee et al., 2022). Nevertheless, some studies suggest that not every form of climate finance has a systematic impact on the carbon emissions of recipient nations (Bhandary et al., 2022).

Studies tend to excessively concentrate on the efficacy of climate finance in reducing carbon emissions, overlooking the question of its effectiveness in various sectors (Li et al., 2022; Qi and Qian, 2023). Different sectors face distinct climate challenges, leading to varying investment strategies and efficiency. For example, the energy sector is required to transition to cleaner technologies and enhance efficiency to reduce carbon emissions (Tian et al., 2024), while agriculture emphasizes long-term adaptation, such as improving irrigation and developing drought-resistant crops (Tofa et al., 2021). However, research frequently regards all sectors as an integrated entity when evaluating the efficacy of climate finance (Bhandary et al., 2021; Lee et al., 2022). Such a methodology might result in an overestimation or underestimation of the overall efficacy of climate finance. Undertaking a systematic investigation into the efficacy of funding across various sectors is thus crucial for optimizing financial distribution and improving climate governance.

The primary industry (mainly referring to agriculture, forestry, and fisheries), water, and electricity are fundamental to modern society, but also cover some of the most challenging sectors under climate change (Rasul and Sharma, 2016). Agriculture, forestry, and fishing (AFF) production highly depends on climatic factors such as temperature and precipitation (Junghans and Köhler, 2016). Water resources are also vulnerable to global warming, with significant uncertainty in their distribution and cycle (Kim et al., 2020). The electricity sector, as the largest carbon emitter, needs an urgent transformation to mitigate carbon emissions (Tian et al., 2024). The fluctuations induced by climate change in these sectors not only affect their productivity, but also trigger cascading effects with far-reaching implications for national security and sustainable development trajectories (Rasul and Sharma, 2016). As such, these sectors warrant priority and are crucial areas for climate finance. According to the OECD climate finance project database, the energy sector, commanding 23% of global mitigation funding, represents a critical battleground for reducing emissions, while water resources and agricultural systems (receiving 15% and 11% of adaptation finance, respectively) constitute fundamental pillars of socioeconomic stability and food security. Given their significance, evaluating the effectiveness of these funds is imperative for fostering resilience and achieving sustainable development goals.

Under this context, this study examines climate finance efficacy in primary, water, and electricity sectors across 98 nations globally, utilizing panel data spanning from 2010 to 2021. Observations from the OECD’s climate finance project database are collected and processed to characterize climate financing at the national level. Next, we compare the effects of climate finance in these sectors across major regions worldwide, emphasizing the heterogeneity driven by national characteristics. Lastly, the study investigates the influences of income levels and resource endowments on the effectiveness of climate finance. Our findings provide valuable insights for the distribution and utilization of climate finance.

This research makes several significant contributions to the literature. First, we provide an original systematic evaluation of climate finance effectiveness across primary, energy, and water resource sectors from a global perspective. Empirical studies generally treat climate finance as a unified entity, overlooking the divergent responses of different sectors to climate finance interventions (Han and Jun, 2023; Borghi et al., 2024). Second, we innovatively propose a methodological framework to address the overlap of mitigation and adaptation finance in OECD, effectively resolving the measurement bias prevalent in studies (Lee et al., 2022; Leal et al., 2023). Finally, we examine how countries’ resource endowments moderate climate finance effectiveness, providing a more nuanced understanding of climate finance efficacy and supporting the development of targeted distribution standards.

The rest of this paper runs as follows. Section “Literature review and theoretical analysis” presents a systematic literature review and theoretical analysis. Section “Methodology” sets up the model, the method of addressing data, and the selection of variables. Section “Empirical analysis and discussion” discusses and analyzes the empirical findings. Section “Conclusions and policy recommendations” concludes with policy recommendations.

Literature review and theoretical analysis

Climate finance and its sectoral impacts

The literature has already presented a thorough and systematic analysis of climate finance (Bhandary et al., 2021; Qi and Qian, 2023). Investigations concerning climate finance are predominantly centered on the allocation protocols of climate finance (Khan et al., 2022; Pauw et al., 2022), encompassing viewpoints of capital providers and recipients, as well as its impact on the economy and society (Lee et al., 2022; Lee and Fang, 2025; Zeng et al., 2022). For example, Venner et al. (2024) highlighted that the allocation of climate finance is primarily driven by financial and political interests rather than climate vulnerability, leading to inequalities across multiple scales. Using panel data for 141 countries from 1990 to 2015, Han and Jun (2023) examined the relationships between climate finance and various economic variables, finding significant disparities in climate finance effectiveness across different countries. Borghi et al. (2024) further explored the impact of climate finance on promoting health and enhancing the sustainability of healthcare systems.

Within the literature examining the effects of climate finance on specific sectors, the majority focuses on energy and environmental sectors. It is a common consensus that the allocation of climate finance aids in the shift towards a clean energy transition (Bei and Wang, 2023; Zhang, 2022). Climate finance contributes to enhancing energy justice and equity in recipient nations as they undergo their own energy transition (Yang et al., 2023). Climate finance in energy system additionally exerts a significant influence on the environment (Kouwenberg and Zheng, 2023). A multitude of research has given evidence that climate finance aids in diminishing greenhouse gas emissions, thus actualizing the goals of worldwide carbon emission reduction and environmental conservation (Apergis et al., 2024; Li et al., 2022). Climate finance also supports initiatives for environmental conservation and ecological restoration, contributing to the biodiversity and enhancement of ecosystem health and resilience (Umar and Safi, 2023).

Several studies have examined the effects of climate finance on the agriculture sector, particularly emphasizing its impact on food security (Bureau and Swinnen, 2018; Rahaman and Rahman, 2020). Such discourses generally look into how assistance policies or projects influence the food security of recipient nations or theorize the origins of such impacts (Castro-Nunez, 2018; Chirambo, 2017). For example, Junghans and Köhler (2016) introduced a concept known as “a domestic gatekeeper” to dissect the influence of climate finance within the agricultural sector. Moreover, most studies typically utilize data from specific regions or countries to analyze climate finance’s impact on the food sector (Bureau and Swinnen, 2018; Doku et al., 2022). For example, Doku et al. (2022) evaluated the effects of Germany’s climate finance on the food security of 35 Sub-Saharan African nations and found that GCF enhances food accessibility and overall food security levels in Sub-Saharan Africa.

The impact and efficacy of climate finance in the realm of water resources have not garnered the same emphasis as that in the agriculture sector (Kim et al., 2020). Concerns over the safety of water resources are of crucial importance as it impacts agricultural production, food security, and the socio-economic stability of countries (Scanlon et al., 2023; Shumilova et al., 2023). Research examining the outcomes of climate finance with a focus on water resources concentrates primarily on case analyses and theoretical discourses (Alaerts, 2019). Savage et al. (2015) took Bangladesh, Ethiopia, and Zambia as subjects for case-based analyses to assess the effects of climate finance on their respective water security. The findings revealed in Bangladesh that climate finance effectively tackles this matter.

Drawing upon a review of the existing literature, several critical gaps have emerged in current climate finance research. Extant studies have focused on the benefits of climate finance in promoting energy transition and improving environmental outcomes, but have overlooked the potential impacts on energy production. Despite receiving a substantial share of climate finance, research on water resources and primary industry remains markedly underexplored. Related studies predominantly rely on single-country case studies and theoretical analysis, lacking evidence across diverse national contexts. Moreover, empirical research tends to treat different sectors as homogeneous entities when evaluating the effectiveness of climate finance, resulting in an oversimplified understanding that fails to capture the complex sectoral heterogeneity and varying responses to climate finance interventions.

Theoretical framework and research hypotheses

The primary industry, water, and energy sectors are the most affected by climate change. Unstable temperature and precipitation patterns significantly affect crop growth and the water supply, making it urgently necessary for adaptive strategies to ensure food and water security (Junghans and Köhler, 2016; Kim et al., 2020). At the same time, the energy sector requires urgent transformation to mitigate climate change, particularly in the context of deepening electrification (Tian et al., 2024).

This trend is also evident in the distribution of climate finance. As Fig. 1 shows, the energy sector is one of the largest recipients of mitigation funds, accounting for 23% (II.3. Energy). This implies that energy transition remains a major challenge in mitigating climate change, requiring significant funding. In contrast, the water and primary sectors dominate adaptation funds, with I.4. Water Supply & Sanitation receiving 15% and III.1. Agriculture, Forestry, Fishing receiving 11%. The close link between these sectors and national security makes them the most urgent areas that must adapt to climate change (Rasul and Sharma, 2016). Consequently, this paper presents the impact of these three types of climate finance on relevant outputs.

These two pie charts illustrate the distribution of climate finance across various sectors, differentiated by funding purpose—Mitigation (left chart) and Adaptation (right chart). Each segment within the pie represents a specific sector and its corresponding percentage share of the total climate finance.

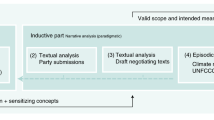

The theoretical framework appears in Fig. 2. The mitigation funds for the energy sector aim to help develop clean and efficient energy systems, which have a profound impact on electricity production. Some scholars argue that intermittency of renewable energy may undermine the stability of electricity supply. Financing restrictions on thermal power plants, driven by climate-oriented investments, also negatively affect overall supply in the short term (Corbera et al., 2016). Meanwhile, the positive impacts of renewable energy are encouraging and have garnered increasing attention. Supporting the development of renewable energy sources, such as solar, wind, and geothermal, directly increases the quantity of electricity supply and also enhances supply diversity, reducing the risks associated with a limited energy mix (Kok and Benli, 2017). Investments in distributed solar power have increased electricity access in rural or remote areas (Akinyele et al., 2015). Additionally, investments in upgrading power equipment and infrastructure contribute to improving grid efficiency and reducing electricity transmission losses, thereby raising electricity production (AbdulRafiu et al., 2022). Importantly, the enhancement of power supply through renewable energy is both sustained and significant, while the intermittency issues can be effectively addressed by energy storage technologies (Cosgrove et al., 2023). Building on these discussions, we formulate the first hypothesis.

These diagrams illustrate the diverse pathways through which climate finance impacts the sectors.

Hypothesis 1. Mitigation funds for the energy sector enhance electricity production.

In agriculture-based primary sectors, adaptation funds are widely recognized as a means to enhance productivity. These funds are invested in the development of climate-resistant crop varieties and the promotion of agricultural technologies, such as soil monitoring and drip irrigation, thereby reducing yield fluctuations caused by climate change (Junghans and Köhler, 2016). Adaptation funds also facilitate the construction of protective infrastructure, such as flood barriers and enhanced irrigation networks, as well as the implementation of risk management mechanisms, including agricultural and forestry insurance, which help safeguard agricultural output (Huang and Wang, 2014). Adaptation funds enable farmers and fishermen to access loans for implementing climate-resilient irrigation technologies and sustainable fishing practices, thereby enhancing producers’ capacity to respond to climate change and ensuring production (Kafle et al., 2022). Drawing from the above analysis, we formulate our second hypothesis.

Hypothesis 2. Adaptation funds for the primary sector improve its output.

The impact of adaptation funds on water extraction is associated with considerable uncertainty. On one hand, these funds support the development and utilization of non-traditional water resources, such as desalination and wastewater treatment, thereby diversifying sources of freshwater extraction (Canning et al., 2021; Dickin et al., 2020). They also contribute to the protection of wetlands and water catchment areas, enhancing natural water storage capacity and water availability (Canning et al., 2021). On the other hand, adaptation funds aim to improve water use efficiency, which reduces pressure on water extraction. For example, some funds are allocated to the rehabilitation of aging water supply infrastructure and the reduction of distribution losses, while others focus on promoting the optimization of water allocation to ensure more sustainable use (Greer, 2020; Greer et al., 2021). Based on the abovementioned analytic mechanisms, we hypothesize the following.

Hypothesis 3a. Adaptation funds for the water sector improve water withdrawals.

Hypothesis 3b. Adaptation funds for the water sector reduce water withdrawals.

Methodology

Model specification

This study employs a panel regression model to verify the efficacy of climate finance. When climate finance investment in a sector is efficient, its positive impact on climate change mitigation, low-carbon development promotion, and climate resilience enhancement across various sectors can be observed in the results. The model settings for the three sectors are shown in Eqs. (1–3).

Here, i denotes the country, t represents the year, and j stands for the sector in which climate finance is applied. CFjit is the climate finance stock in sector j of country i in year t. Energy, Primary, and Water are the output indicators for the energy, primary and water sectors, respectively. \({\alpha }_{i}\) is the individual fixed effect, \({\eta }_{t}\) is the year fixed effect, \({\varepsilon }_{{it}}\) is the error term, and CV represents control variables.

Unobservable factors that cannot be controlled may lead to an estimation bias. Moreover, the government tends to allocate more funding to industries or firms with higher output levels (Venner et al., 2024), which could exacerbate endogeneity issues. Therefore, we employ a two-stage least squares (2SLS) approach to address potential endogeneity concerns and formalize it in Eqs. (4) and (5).

Here, \({{IV}}_{{jit}}\) denotes the instrumental variable for climate finance (\({{CF}}_{{jit}}\)), while \({\widehat{{CF}}}_{{jit}}\) signifies the estimated climate finance derived from Eq. (4) using \({{IV}}_{{jit}}\). Crucially, the chosen instrumental variable must exhibit a strong correlation with CF while remaining uncorrelated with the output indicator, Y, thus ensuring the validity of the endogeneity treatment.

Data

Sample selection and data sources

To better compare the differences between Mitigation and Adaptation funds, this study uniformly uses panel data from 98 countries from 2010 to 2021 to assess the effectiveness of climate finance across different sectors. All variables except for Growth are in logarithmic form.

Dependent variables

This study focuses on the energy, primary, and water sectors to analyze the effectiveness of climate finance, given their significant share of climate finance allocations. When assessing the output of climate finance and referring to studies in the relevant field (Kumar et al., 2021; Lee et al., 2024, 2025; Sharma et al., 2022; Tian et al., 2023), we select three variables, Elec_Gen (electricity generation per capita), Fre_Water (annual freshwater withdrawals per capita), and Prim_Prod (AFF, value added per capita), to measure the output of climate finance in different sectors.Footnote 1

Core independent variables

This study selects the climate finance project database collected by OECD, which contains a total of 16,319 climate finance projects from 2000 to 2021 and is widely used in climate finance literature (Lee et al., 2022; Scandurra et al., 2020; Weiler et al., 2018). The OECD has provided a detailed explanation of the recipient countries, receiving sectors, and purposes of each project. These projects serve two distinct purposes: one is to achieve Mitigation objectives, and the other is to achieve Adaptation objectives. Individual projects may exclusively fulfill one of the goals, or a project may meet both objectives.

The literature typically aggregates investments in each type of project to represent mitigation and adaptation funds (Lee et al., 2022; Han and Jun, 2023; Leal et al., 2023). However, measurement bias caused by multi-objective projects is overlooked. A significant number of projects is designed to meet both mitigation and adaptation objectives. For instance, Germany allocated US$100,000 to train South African technical personnel on using dams and irrigation systems in 2022. In the project record, this project’s purpose encompasses both carbon emission mitigation and climate change adaptation. Notably, over 180,000 such projects exist in the database. As Fig. 3 depicts, the share of this category of funds constitutes roughly a maximum of 1/3 of total funds. As time progresses, the proportion of Both Mitigation and Adaptation funds in the total volume incrementally rises. Consequently, employing the conventional method of exclusion introduces a significant margin of error, undermining the trustworthiness of the ultimate outcomes.

The left figure, a stacked area chart, displays the annual volume of climate finance (US$ billion, constant 2021 prices), disaggregated into “Adaptation only,” “Both Mitigation and Adaptation,” and “Mitigation only” categories. This figure illustrates the overall growth in climate finance and the relative volume of each category. The right figure presents the proportional share of each category over time. This visualization emphasizes the evolving allocation of climate finance, independent of total volume fluctuations.

This study attempts to improve the conventional method according to a detailed classification of climate finance projects. Specifically, a project could potentially lead to any of the following five outcomes concerning the goals of climate finance (as shown in Table 1). As an example, a climate finance project is labeled as “Mitigation only” funds when its Adaptation goal is categorized as Not targeted (Scene 1). Should neither the Adaptation nor the Mitigation goals be classified as Not targeted, the project is designated as “Both Mitigation and Adaptation” funds (Scenes 3–5). In the face of “Both Mitigation and Adaptation” funds, it is imperative to distribute or eliminate this category of funds to guarantee the precision of the ultimate climate finance dataset.

First, we consider a weighted allocation based on the importance of climate finance objectives (hereafter referred to as Weight). The weights for various situations are indicated in Table 1 under the Weight row. In cases of Scenes 1–2, the entire funding is assigned to a specific goal. Should the significance of the climate finance project objectives be identical (Scenes 3–4), the funds are split evenly. In instances where the importance of climate finance project objectives varies (Scene 5), a larger share of the funds is apportioned to the Significant target and assigned a weight of 0.75. In contrast, the other target receives a weight of 0.25.

In addition to the Weight method, since there may be errors in the allocation approach for funds of different significance levels, a second method integrating weighted distribution and exclusion is devised (hereinafter called W&D), which eliminates the funding projects under Scene 5. Ultimately, the exclusion method (hereafter abbreviated as Drop) is employed as well to compare the outcomes of the three approaches.

Figure 4 depicts the ultimate dataset. Blue lines here represent funds for Mitigation objectives, and red lines represent funds for Adaptation objectives. The solid line indicates the outcomes of the weighted distribution (Weight), the dashed line indicates the outcomes of the combined method of distribution and exclusion (W&D), and the dotted line indicates the outcomes of the direct exclusion (Drop). It is evident that, for both Mitigation and Adaptation funds, the Drop method results in a difference of more than 20% versus the Weight and W&D methods, whereas the Weight and W&D methods are more closely aligned.

This figure displays the trends in climate finance from 2000 to 2021, comparing different methods of handling projects classified as serving “Both Mitigation and Adaptation” objectives. The graph shows the yearly climate finance amounts, with separate lines illustrating three different methodologies for Both Adaptation and Mitigation finance.

To minimize information loss and ensure objectivity, this study adopts the W&D method for the treatment of the key explanatory variable. The Weight method, which incorporates subjective weights, is used as a robustness check. Figure 5 displays the allocation (using the W&D method) of mitigation funds within the energy sector. In contrast to the distribution of the overall climate finance among countries, the allocation of climate finance in the energy sector is highly fragmented. This demonstrates the traits of a markedly unbalanced panel dataset.

This heatmap visualizes mitigation finance allocations across different recipient countries from 2000 to 2021. The x-axis lists the recipient countries, while the y-axis represents the year. The color intensity of each cell indicates the amount of mitigation funding received by a specific country in a given year, with darker shades of red representing larger amounts.

Given that the utilization of climate finance by recipient countries for climate adaptability/mitigation infrastructure requires a multi-year period, this study draws on the calculation methods for capital stock and patent depreciation in macroeconomic models, employing the perpetual inventory method to transform the flow data of climate finance into stock data, as illustrated by:

Here, \({{CF}}_{{jit}}\) represents the stock of climate finance in country i’s sector j in year t, while \({\widetilde{{CF}}}_{{jit}}\) denotes the investment in climate finance for the same. The depreciation rate \(\delta\) is set at 10% in accordance with the methods used in macroeconomic data studies (Griliches, 1990; Wan and Qiu, 2022). Although the cycle for investing climate finance in adaptive infrastructure construction may be extended, given the lack of clear regulations in the project-based funding model, this study also employs \(\delta =0.2\) and \(\delta =0.3\) for robustness checks.

Control variables

In selecting control variables, this research draws on the work of Lee et al. (2022) and Wong (2016). Several key control variables are incorporated into the model: Domestic Credit to Private Sector (Finance), Industry Value Added (Industry), Prevalence of Undernourishment (UNNO). In addition, to account for variations in national economic development and population levels, GDP growth rate (Growth) is used as a proxy for economic development, while the logarithm of population (Population) represents population size. These controls are included to effectively isolate the effects of climate finance from broader economic and demographic influences. Table 2 presents the definitions and sources of the main variables herein.

Due to the unique characteristics of the three sectors, it may be necessary to control for variables specific to individual sectors to ensure the robustness of the experiment. Therefore, in the robustness test section, this paper adds two unique control variables for each sector to test the robustness of the experiment. Table 3 lists the descriptive statistics of the model.

Empirical analysis and discussion

Benchmark regression

Table 4 presents the estimation results of the panel fixed effect model, as demonstrated in Eqs. (1–3). The results in columns (1)–(2) indicate that mitigation climate finance in the energy sector enhances a country’s electricity generation, confirming our Hypothesis 1. While climate finance in the energy sector can strengthen the recipient country’s energy system to adapt to climate change (Nock et al., 2020), when discussing the impact of climate finance investment on a country’s total electricity production, a key fact must be considered: the countries receiving climate finance are primarily developing countries, and their primary goal in the energy sector is to ensure energy supply for industrial production and people’s livelihood (Ahmad and Zhang, 2020; Mir et al., 2020). Although the goal of climate finance is mitigation, the investment in climate finance in these countries is often prioritized for improving the efficiency of thermal power generation and constructing new power facilities, such as natural gas power plants (Clark et al., 2020; Vanegas Cantarero, 2020).

Columns (3)–(4) report the effect of climate finance investments in the primary sector under adaptation. The result shows that adapting to climate finance directed toward the AFF sectors significantly boosts a country’s primary sector production. Consequently, investments in climate finance aimed at adaptation are effective, thus confirming Hypothesis 2. Climate finance plays a crucial role in enhancing climate resilience within AFF, leading to increased productivity and sustainability (Digitemie and Ekemezie, 2024; Scandurra et al., 2020). We argue that this growth-enhancing effect stems from proactive interventions addressing climate change’s direct impacts on these sectors. First, climate finance enhances the climatic adaptability of primary sectors via improving water resource management systems in agriculture and aquaculture (Kafle et al., 2022; Mungai et al., 2021), developing climate-resilient livestock breeds and crop varieties (Martey et al., 2020; Tofa et al., 2021), and implementing sustainable forest management practices and soil conservation techniques (Kumar et al., 2022). Second, these adaptive measures help maintain stable production across primary industries and support growth even under extreme weather conditions such as droughts, floods, and heat waves.

As to the water sector, columns (5)–(6) report the effectiveness of climate finance of adaptation investments. Contrary to our expectations, evidence reveals that adapting climate finance aimed at this sector does not significantly impact the acquisition of national water resources. Three potential reasons may account for this phenomenon. First, unlike the power and agricultural sectors, climate adaptation in the water sector involves improving water extraction capacity (Canning et al., 2021), increasing water use efficiency, and reducing extraction pressure (Greer et al., 2021). The first one raises water usage, while the latter two reduce it, potentially leading to an insignificant impact of climate adaptation funds on the volume of freshwater withdrawals.

Second, climate impacts on water resources are more severe and widespread, and the limited amount of climate finance is insufficient to facilitate climate adaptation. Extreme weather events triggered by climate change, such as droughts and floods, significantly influence the availability and distribution of water resources (Gaaloul et al., 2021; Muyambo et al., 2023). During drought periods, despite climate finance investments, the depletion of water sources and water shortages remain challenging to overcome. However, during frequent flood periods, although water resources are abundant, the destructive force of floods reduces the efficiency of water resource utilization (Jongman et al., 2014; Sarker Md et al., 2022; Tauhid and Zawani, 2018). Therefore, climate finance investment in the water sector often struggles to effectively respond to these extreme climate conditions.

Another potential reason may be the ineffective management of climate finance in the water sector (Liu et al., 2024; Mori et al., 2019). Studies have demonstrated that the current allocation of climate finance often does not consider the specific vulnerabilities and needs of water resources, resulting in funds not being effectively invested in areas where water resources are most urgently needed (Betzold and Weiler, 2017; Islam, 2022). This inadequacy in decision-making could lead to a wastage of funds, as they might be invested in areas where water resources are relatively abundant or less affected by climate change, while areas facing severe water shortages and risks of extreme climate events may not receive adequate financial support (Doshi and Garschagen, 2020; Garschagen and Doshi, 2022).

Robustness test

Adjust core dependent variable

In the design of the climate finance measurement method for sub-sectors mentioned earlier, we select a 10% depreciation rate for calculating the stock data. Therefore, the 20% and 30% depreciation rates are applied to measure the robustness of the experiment in accordance with the design method of the previous calculations. In Table 5, column (1) displays the results with a 20% depreciation rate and column (2) gives them with a 30% depreciation rate. Panel A-C represents the results for electricity production, primary sector production, and freshwater withdrawals, respectively. The results suggest that the substitution of the method of processing climate finance does not alter the outcomes of the benchmark model, leading us to believe that the model is robust.

Adjust control variable

In the benchmark regression design, the same control variables are used for all sectors to ensure comparability of the test effects across the three sectors. This may result in the absence of some essential sector-specific control variables that could affect the robustness of the experiment. Consequently, this study adds two control variables that may affect each sector.

For the energy sector, renewable energy consumption as a percentage of total final energy consumption (Renewable) reflects the transition towards sustainable energy and its potential to reduce carbon emissions (Anthopoulos and Kazantzi, 2022; Lee et al., 2024). Additionally, the fixed broadband subscription rate (FBS) is a crucial control variable related to the informatization level and energy efficiency management capability of the energy sector. In the primary sector, arable land area (Arable) and fertilizer consumption (Fertilizer) are critical control variables. The availability of arable land as a percentage of total land area directly impacts agricultural output, influencing the sector’s productivity and food security (Stewart and Roberts, 2012; Yousaf et al., 2017). Fertilizer consumption measures the reliance on chemical inputs to enhance crop yields, affecting agricultural sustainability and environmental health. For the water sector, the control of land under cereal production (Cerealland) and the proportion of agricultural land (Agriculture) is necessary. Areas devoted to cereal production reflect the sector’s dependency on water resources for staple crop cultivation. At the same time, the percentage of land allocated to agriculture indicates the overall demand for water in this sector, affecting water resource management and allocation efficiency (Ellison et al., 2017; Liu et al., 2017). Table 2 presents the names and meanings of the added control variables.

Table 6 presents the results of the robustness tests. Column (1) shows the results obtained by adding the first characteristic control variable. Column (2) presents the outcomes after adding the second characteristic control variable. The results indicate that adding characteristic control variables to each sub-sector does not alter the outcomes of the benchmark regression, suggesting that the empirical design is robust.

Addressing endogenous issues

In the application of the 2SLS regression model, the choice of instrumental variables (IV) is pivotal to address issues of endogeneity that arise from unobservable factors and potential reverse causality. Our strategy is to use the logarithmic value of the average climate finance in the corresponding sectors within the country’s region as an instrumental variable. For example, we use average mitigation funds received by the energy sector in South Asia as an instrument for mitigation funds in the energy sector of Bangladesh. On the one hand, climate finance allocations highly correlate across countries within the same region, as these countries commonly face similar climate issues and share comparable geopolitical and economic contexts (Xie et al., 2023). On the other hand, the output of a country’s energy, primary, and water sectors does not directly relate to the climate finance of neighboring countries, thus ensuring exogeneity of the instrument variable. This selection ensures that each instrumental variable is appropriate for isolating the exogenous component of climate finance in their respective sectors.

Table 7 outlines the robustness of these variables in addressing potential biases in estimation. Panel B reports the first-stage regression results, showing that the instrumental variables are significantly associated with the explanatory variables. Since both the F-statistic and Cragg-Donald Wald F-statistic exceed their respective thresholds, concerns regarding weak instruments are dismissed. Panel A presents the results from the second-stage regression. These findings signify that the estimated results align closely with those of the benchmark model, indicating an absence of significant deviations. This coherence suggests after addressing potential endogeneity issues that the benchmark model remains robust.

Heterogeneity test

Regional heterogeneity

When discussing the effectiveness of climate finance, regional heterogeneity is an essential factor that cannot be overlooked. Factors such as climate conditions, economic development levels, resource endowments, and social structures vary across regions, collectively shaping the impact of climate finance in each area (Román et al., 2018). Therefore, ignoring regional heterogeneity may lead to misunderstandings and biases in assessing the effectiveness of climate finance. This paper classifies the 98 countries in the sample into seven regions based on the classification criteria of the World Bank: Latin America & Caribbean, South Asia, Sub-Saharan Africa, Europe & Central Asia, Middle East & North Africa, East Asia & Pacific, and North America. Among these, the North American region is excluded from the heterogeneity analysis due to insufficient sample size.

Table 8 presents the results for regional heterogeneity. Columns (1)–(6) correspond to the results for the regions of Latin America & Caribbean, South Asia, Sub-Saharan Africa, Europe & Central Asia, Middle East & North Africa, and East Asia & Pacific, respectively. In the examination of the effect of climate finance on electricity production, we observe no significantly positive relationship in column (1) for Latin America & Caribbean and column (4) for Europe & Central Asia. The potential reason is that the effect of climate finance investments in the energy sector for mitigation on promoting electricity production is influenced by specific regional factors. For example, in Europe & Central Asia the electricity market may be undergoing rapid development and transformation, especially in the renewable energy sector. However, due to significant differences in electricity infrastructure and policy environments in these regions, climate finance investment may not have effectively matched local demands and potentials, resulting in a less pronounced effect. Additionally, mitigation funds in East Asia & Pacific exhibit a significantly negative impact, possibly due to the rapid push for clean energy transition in these regions without mature technologies, which have disrupted power generation and reduced electricity output (Yu et al., 2021).

Regarding the impact of climate finance on the primary industry, the results reveal distinct outcomes across regions. Columns (2), (4), (5) and (6) correspondingly represent South Asia, Europe & Central Asia, Middle East & North Africa, and East Asia & Pacific where climate finance significantly benefits the primary sector. However, for Latin America & Caribbean (column (1)) and Sub-Saharan Africa (column (3)), the relationship is not significant. These regional disparities in climate finance effectiveness stem from underlying structural factors. Regions with positive impacts tend to have advantageous conditions such as abundant natural resources, established modern farming methods, and well-integrated industrial frameworks. Conversely, regions with limited impacts face inherent challenges including resource constraints, dependence on traditional agricultural practices, and fragmented industrial structures that affect their capacity to effectively utilize climate finance (Masud et al., 2023; Rasheed et al., 2023).

When examining the impact of climate finance on water resources, no significant effects appear across any subgroups, aligning with the results of the baseline regression. However, this does not appear to be the result of offsetting effects between increased water extraction and water conservation. Even in water-abundant regions such as East Asia & Pacific and Latin America & Caribbean, no significant impact arises. A more convincing explanation is that water resource governance requires substantial, long-term investments that exceed the capacity of climate finance (Alaerts, 2019).

Income heterogeneity

A country’s income level can significantly influence the effectiveness of climate finance. On one hand, income level is closely linked to institutional capacity and infrastructure, which determine a country’s ability to absorb and utilize external funds (Raddatz, 2007; Tosun, 2014). As Hallegatte et al. (2014) note, low-income countries often face implementation challenges and limited local coordination, which hinder the impact of climate finance on mitigation and adaptation. On the other hand, countries at different income levels have varying development priorities, shaping both the allocation and effectiveness of climate finance (Bhandary et al., 2021). For instance, low-income countries tend to favor low-cost, quick-impact projects that meet basic development needs, while high-income countries are more likely to invest in large-scale, high-cost climate initiatives aimed at achieving long-term economic and environmental gains.

Therefore, this section delves into the differences in income heterogeneity among countries. According to the World Bank’s classification system, countries are categorized into four income groups based on their Gross National Income (GNI) per capita. Low income countries are those with a GNI per capita of $1145 or less; Lower middle income countries fall within the range of $1146–$4515; Upper middle income countries have a GNI per capita between $4516 and $14,005; and high income countries are defined as those with a GNI per capita exceeding $14,005. These thresholds are widely used for comparative analyses in development research and policy-making (Mir et al., 2020). Among these, the high-income countries are excluded due to their relatively small sample size.

The results of income heterogeneity appear in Table 9. Columns (1)–(3) correspond to the results for countries with Upper middle, Lower middle, and Low-income levels, respectively. The results indicate that, except for the impact of climate finance in the water resources, in the remaining sectors of primary industries and energy sector, climate finance’s effects on low-income countries differ from those on upper-middle-income countries.

In the energy sector, the results indicate differential impacts of climate finance on electricity generation across varying income levels. For upper-middle-income countries, climate finance in the energy sector is associated with decreased electricity generation, while lower-middle-income and low-income countries demonstrate increased generation capacity with climate finance investment. This divergent pattern stems from the distinct developmental contexts: upper-middle-income nations, with an established power infrastructure meeting domestic demand, often utilize climate finance to transition from traditional fossil fuel facilities to renewable sources, temporarily reducing overall generation during the transition phase. Conversely, in lower-middle-income and low-income countries where energy infrastructure remains insufficient for national requirements, climate finance primarily supports the construction of new generation facilities, reflecting these nations’ fundamental need to expand power supply while simultaneously incorporating sustainable technologies.

The empirical evidence reveals distinct patterns in the impact of climate finance on primary industries across income groups. For upper-middle-income countries, climate finance demonstrates positive associations with value added in primary industries, while lower-middle-income countries and lower-income countries show no significant relationship. This heterogeneous pattern reflects varying capacities in climate adaptation: upper-middle-income nations possess advanced agricultural technologies and robust infrastructure, enabling effective implementation of climate-resilient farming practices and sustainable resource management systems. In contrast, lower-middle-income countries and lower-income countries often encounter institutional barriers and incomplete agricultural modernization processes, potentially hampering the effective translation of climate finance into productive agricultural adaptations (Balasubramanian, 2018; Vermeulen et al., 2012).

Role of resource endowments

A country’s resource endowment profoundly influences its climate action, shaping both its capacity and strategy for addressing climate change, as well as the effectiveness of climate investments (Yanda et al., 2021). Given that countries receiving climate finance exhibit significant variations in their resource endowments, these characteristics become particularly important when examining climate finance effectiveness across different sectors. Pertinent analysis provides insights into the tailored allocation of climate finance.

Climate governance across sectors should focus on different aspects of resource endowments. Fossil fuel endowments have a significant impact on energy transition. For countries rich in coal and oil resources, a low-carbon transition in the power sector is risky and economically unfeasible, as these countries rely heavily on fossil fuels, and the cost of thermal power generation is relatively low (Zhang and Xi, 2024). The availability of arable land largely determines the effectiveness of climate funding in agriculture. In countries with abundant arable land, climate adaptation funds enhance yields by improving infrastructure and leveraging economies of scale. In contrast, land scarcity limits the potential for agricultural expansion and poses challenges to implementing adaptation measures. Similarly, a country’s total freshwater resources may influence water management strategies, thereby affecting the effectiveness of climate finance in the water sector.

This study categorizes countries based on their resource endowments using three distinct metrics: fossil fuel rents per capita, arable land per capita, and renewable internal freshwater per capita.Footnote 2 Using the mean values of these characteristics across our sample countries as benchmarks, we classify nations into high and low endowment groups for each environmental characteristic, analyzing how these endowments moderate climate finance effectiveness in electricity generation, primary industry value added, and freshwater withdrawals.

Table 10 presents the heterogeneity analysis results. Column (1) displays results for countries with high resource endowments, while column (2) shows results for those with low resource endowments. Panel A analyzes the relationship between climate finance and electricity generation in countries with different levels of fossil fuel rents. Panel B examines how climate finance affects primary industry value added across countries with varying amount of arable land. Panel C investigates the connection between climate finance and water accessibility in relation to countries’ total freshwater resources.

For the energy sector, the effectiveness of climate finance exhibits distinct relationships with fossil fuel endowments. Nations with lower fossil fuel rents demonstrate measurable increases in electricity production following climate finance allocation, whereas countries with higher fossil fuel rents show statistically insignificant production changes. This phenomenon aligns with our expectations, as countries with substantial fossil fuel revenues are more likely to maintain their existing energy structure and avoid transitioning to low-carbon or renewable energy sources, further limiting the effectiveness of climate finance. Therefore, in the allocation of climate finance for the energy sector, it is recommended that mitigation funding is recommended for towards countries with relatively weaker fossil fuel endowments.

For the primary sector, climate finance effectiveness demonstrates systematic variation across nations’ arable land. Countries possessing extensive arable land exhibit statistically significant increases in primary value-added following climate finance distribution, while nations with restricted arable land show no substantive productivity changes. This systematic difference suggests that sufficient arable land is a crucial condition for effective agricultural climate adaptation. A large amount of arable land facilitates the cultivation of diverse crops and provides the necessary land base for testing climate-adaptive agricultural technologies, offering greater flexibility for agricultural adaptation. In contrast, nations with limited agricultural land face substantial obstacles in translating climate finance into productivity gains.

For water resource management, the role of climate adaptation funding does not significantly vary with changes in renewable internal freshwater. The results in columns 1 and 2 are consistent with the baseline regression with no significant impact observed.

Conclusions and policy recommendations

A thorough examination of the effectiveness of climate finance in the agriculture, water, and energy sectors can help us understand and optimize global climate change financial strategies and resource allocation. Doing so has a decisive impact on achieving international climate goals, enhancing countries’ capacities for adaptation and mitigation of climate change, and promoting sustainable economic development. Through in-depth analysis of the flow and impact of climate finance, we can ensure that global collective efforts are directed towards substantive progress in the right direction while ensuring that these efforts yield the maximum environmental and social benefits.

This paper designs a data processing method, categorizes countries and funding sectors from the OECD project-based database, and selects 98 countries globally as the research sample to empirically test the application effects of climate finance in the primary, water, and energy sectors from 2010 to 2021. Given the significant differences in the distribution of water resources, agriculture, and energy across countries, the study further groups countries based on their features to explore the heterogeneity of climate finance and to assess its effectiveness in different sectors.

The findings suggest the following. First, in the energy sector, mitigation funds have significantly enhanced electricity output. For the primary sector, investment in adapting climate finance significantly promotes the increase in production. However, in the water sector, climate finance investment does not significantly affect the acquisition of water resources. Second, regional heterogeneity analysis reveals the differences in the effects of climate finance across different regions, reflecting that when climate finance is invested in sectors with scarcity and vulnerability, its impact is more pronounced. Income heterogeneity analysis reveals that income levels have a substantial impact on the effectiveness of climate finance investments, with mitigation funds being more effective in countries with lower incomes. Furthermore, resource endowments, such as fossil fuels and arable land, significantly influence the effectiveness of climate finance across various sectors.

Based on the above conclusions, this paper offers the following recommendations for the allocation of climate finance. First, the allocation of climate finance needs to consider the different characteristics of countries. For countries with more developed economies, climate finance should focus on supporting technological innovation and the transition to renewable energy, facilitating their transition to a low-carbon economy. For countries with lower levels of economic development, especially those regions that are more sensitive and vulnerable to the impacts of climate change, climate finance should be used more for enhancing their adaptive capacity to climate change, including improving infrastructure, enhancing disaster risk management, and supporting sustainable agricultural development.

Second, the allocation of climate finance should balance fairness and effectiveness. The effectiveness of climate finance currently varies across different regions and countries with different characteristics, suggesting the need for a more refined evaluation system to identify the climate finance needs and utilization efficiency. Specifically, an evaluation system should consider a country’s level of economic development, carbon emission intensity, and its sensitivity and vulnerability to climate change. Moreover, an evaluation system should also assess the marginal benefits of climate finance in different sectors to ensure that funds are allocated to areas that generate the most positive impact.

Despite the comprehensive analysis presented in this study, several notable limitations must be addressed. We have outlined the theoretical mechanisms through which climate finance affects different sectors. However, due to data limitations, a thorough empirical analysis to test these potential mechanisms has not been conducted. Comparing these mechanisms helps identify the strengths and potential issues of different types of climate finance, making it an important direction for future research. Furthermore, the reliance on country-level aggregated data may mask important sub-national variations in climate finance effectiveness, while the temporal scope of our analysis (2010–2021) may not fully capture long-term effects and includes the potentially distorting influence of the COVID-19 pandemic. These limitations suggest opportunities for future research to employ more granular data analysis approaches, to develop more nuanced methodological frameworks for climate finance classification, and to extend the temporal scope for better understanding the long-term dynamics of the effectiveness of climate finance.

Data availability

Data are available from the authors upon request.

Notes

We focus on electricity output rather than total energy output, as the low-carbon transition is mainly reflected in changes to the electricity mix.

Fossil fuel rents refer to the sum of fossil rents and fuel rents. A higher value indicates that a country is more dependent on fossil energy sources (Zhang and Xi, 2024).

References

AbdulRafiu A, Sovacool BK, Daniels C (2022) The dynamics of global public research funding on climate change, energy, transport, and industrial decarbonisation. Renew Sustain Energy Rev 162:112420. https://doi.org/10.1016/j.rser.2022.112420

Ahmad T, Zhang D (2020) A critical review of comparative global historical energy consumption and future demand: the story told so far. Energy Rep. 6:1973–1991. https://doi.org/10.1016/j.egyr.2020.07.020

Akinyele DO, Rayudu RK, Nair NKC (2015) Development of photovoltaic power plant for remote residential applications: the socio-technical and economic perspectives. Appl Energy 155:131–149. https://doi.org/10.1016/j.apenergy.2015.05.091

Alaerts GJ (2019) Financing for water—water for financing: a global review of policy and practice. Sustainability 11:821. https://doi.org/10.3390/su11030821

Anthopoulos L, Kazantzi V (2022) Urban energy efficiency assessment models from an AI and big data perspective: tools for policy makers. Sustain Cities Soc 76:103492. https://doi.org/10.1016/j.scs.2021.103492

Apergis N, Pinar M, Unlu E (2024) Does classification of green aid flows matter for environmental quality? Empir Econ 66:53–73. https://doi.org/10.1007/s00181-023-02454-2

Balasubramanian M (2018) Climate change, famine, and low-income communities challenge Sustainable Development Goals. Lancet Planet Health 2:e421–e422. https://doi.org/10.1016/S2542-5196(18)30212-2

Barrett S (2013) Local level climate justice? Adaptation finance and vulnerability reduction. Glob Environ Chang. 23:1819–1829. https://doi.org/10.1016/j.gloenvcha.2013.07.015

Bei J, Wang C (2023) Renewable energy resources and sustainable development goals: evidence based on green finance, clean energy and environmentally friendly investment. Resour Policy 80:103194. https://doi.org/10.1016/j.resourpol.2022.103194

Betzold C, Weiler F (2017) Allocation of aid for adaptation to climate change: do vulnerable countries receive more support? Int Environ Agreem Polit Law Econ 17:17–36. https://doi.org/10.1007/s10784-016-9343-8

Bhandary RR, Gallagher KS, Jaffe AM, Myslikova Z, Zhang F, Petrova M, Barrionuevo A, Fontaine G, Fuentes JL, Karani P, Martinez D, Seitlheko L, Staicu D, Ullah N, Yimere A (2022) Demanding development: the political economy of climate finance and overseas investments from China. Energy Res Soc Sci 93:102816. https://doi.org/10.1016/j.erss.2022.102816

Bhandary RR, Gallagher KS, Zhang F (2021) Climate finance policy in practice: a review of the evidence. Clim Policy 21:529–545. https://doi.org/10.1080/14693062.2020.1871313

Borghi J, Garcia-Dorado SC, Anton B, Gerardo D, Gasparri G, Hanson M, Langlois EV (2024) Climate finance opportunities for health and health systems. Bull World Health Organ 102(5):330

Briera T, Lefèvre J (2024) Reducing the cost of capital through international climate finance to accelerate the renewable energy transition in developing countries. Energy Policy 188:114104. https://doi.org/10.1016/j.enpol.2024.114104

Bureau JC, Swinnen J (2018) EU policies and global food security. Glob Food Secur 16:106–115. https://doi.org/10.1016/j.gfs.2017.12.001

Cadman T (2014) Climate finance in an age of uncertainty. J Sustain Financ Invest 4:351–356. https://doi.org/10.1080/20430795.2014.971097

Canning AD, Jarvis D, Costanza R, Hasan S, Smart JCR, Finisdore J, Lovelock CE, Greenhalgh S, Marr HM, Beck MW, Gillies CL, Waltham NJ (2021) Financial incentives for large-scale wetland restoration: beyond markets to common asset trusts. One Earth 4:937–950. https://doi.org/10.1016/j.oneear.2021.06.006

Castro-Nunez A (2018) Responding to climate change in tropical countries emerging from armed conflicts: harnessing climate finance, peacebuilding, and sustainable food. Forests 9:621. https://doi.org/10.3390/f9100621

Chirambo D (2017) Enhancing climate change resilience through microfinance: redefining the climate finance paradigm to promote inclusive growth in Africa. J Dev Soc 33:150–173. https://doi.org/10.1177/0169796X17692474

Clark R, Zucker N, Urpelainen J (2020) The future of coal-fired power generation in Southeast Asia. Renew Sustain Energy Rev 121:109650. https://doi.org/10.1016/j.rser.2019.109650

Colenbrander S, Dodman D, Mitlin D (2018) Using climate finance to advance climate justice: the politics and practice of channelling resources to the local level. Clim Policy 18:902–915. https://doi.org/10.1080/14693062.2017.1388212

Corbera E, Calvet-Mir L, Hughes H, Paterson M (2016) Patterns of authorship in the IPCC Working Group III report. Nat Clim Change 6:94–99. https://doi.org/10.1038/nclimate2782

Cosgrove P, Roulstone T, Zachary S (2023) Intermittency and periodicity in net-zero renewable energy systems with storage. Renew Energy 212:299–307

Dickin S, Bayoumi M, Giné R, Andersson K, Jiménez A (2020) Sustainable sanitation and gaps in global climate policy and financing. Npj Clean Water 3:1–7. https://doi.org/10.1038/s41545-020-0072-8

Digitemie WN, Ekemezie IO (2024) Assessing the role of climate finance in supporting developing nations: a comprehensive review. Financ Acc Res J 6:408–420. https://doi.org/10.51594/farj.v6i3.926

Doku I, Richardson TE, Essah NK (2022) Bilateral climate finance and food security in developing countries: a look at German donations to Sub-Saharan Africa. Food Energy Secur 11:e412. https://doi.org/10.1002/fes3.412

Doshi D, Garschagen M (2020) Understanding adaptation finance allocation: which factors enable or constrain vulnerable countries to access funding? Sustainability 12:4308. https://doi.org/10.3390/su12104308

Ellison D, Morris CE, Locatelli B, Sheil D, Cohen J, Murdiyarso D, Gutierrez V, Noordwijk M, Creed IF, Pokorny J, Gaveau D, Spracklen DV, Tobella AB, Ilstedt U, Teuling AJ, Gebrehiwot SG, Sands DC, Muys B, Verbist B, Springgay E, Sugandi Y, Sullivan CA (2017) Trees, forests and water: Cool insights for a hot world. Glob Environ Change 43:51–61. https://doi.org/10.1016/j.gloenvcha.2017.01.002

Gaaloul N, Eslamian S, Katlance R (2021) Impacts of climate change and water resources management in the southern mediterranean countries. Water Prod J 1:51–72. https://doi.org/10.22034/wpj.2020.119476

Garschagen M, Doshi D (2022) Does funds-based adaptation finance reach the most vulnerable countries? Glob Environ Chang. 73:102450. https://doi.org/10.1016/j.gloenvcha.2021.102450

Greer RA (2020) A review of public water infrastructure financing in the United States. WIREs Water 7:e1472. https://doi.org/10.1002/wat2.1472

Greer RA, Lee K, Fencl A, Sneegas G (2021) Public–private partnerships in the water sector: the case of desalination. Water Resour Manag 35:3497–3511. https://doi.org/10.1007/s11269-021-02900-9

Griliches Z (1990) Patent statistics as economic indicators: a survey. National Bureau of Economic Research, Cambridge, MA, p. w3301. https://doi.org/10.3386/w3301

Gupta A (2016) Chapter 1—Climate change and kyoto protocol: an overview. In: Ramiah V, Gregoriou GN (eds) Handbook of environmental and sustainable finance. Academic Press, San Diego, pp 3–23. https://doi.org/10.1016/B978-0-12-803615-0.00001-7

Hallegatte S, Bangalore M, Bonzanigo L, Fay M, Narloch U, Rozenberg J, Vogt-Schilb A (2014) Climate change and poverty--an analytical framework. World Bank Policy Research Working Paper 7126. https://ssrn.com/abstract=2531160

Han S, Jun H (2023) Growth, emissions, and climate finance nexus for sustainable development: revisiting the environmental Kuznets curve. Sustain Dev 31:510–527. https://doi.org/10.1002/sd.2406

He K, Shahzadi I, Khan S, Mentel G, Tarczyński W (2024) The dilemma of water, food, and greener energy nexus: a novel context of COP27 for G20 economies. Land Degrad Dev 5110. https://doi.org/10.1002/ldr.5110

Huang J, Wang Y (2014) Financing sustainable agriculture under climate change. J Integr Agric 13:698–712. https://doi.org/10.1016/S2095-3119(13)60698-X

Islam MM (2022) Distributive justice in global climate finance—recipients’ climate vulnerability and the allocation of climate funds. Glob Environ Chang. 73:102475. https://doi.org/10.1016/j.gloenvcha.2022.102475

Jongman B, Hochrainer-Stigler S, Feyen L, Aerts JCJH, Mechler R, Botzen WJW, Bouwer LM, Pflug G, Rojas R, Ward PJ (2014) Increasing stress on disaster-risk finance due to large floods. Nat Clim Chang. 4:264–268. https://doi.org/10.1038/nclimate2124

Junghans L, Köhler M (2016) Cropping and cashing: institutional solutions for synergetic climate finance for mitigation and adaptation in agriculture. Clim Dev 8:207–210. https://doi.org/10.1080/17565529.2015.1085360

Kafle K, Uprety L, Shrestha G, Pandey V, Mukherji A (2022) Are climate finance subsidies equitably distributed among farmers? Assessing socio-demographics of solar irrigation in Nepal. Energy Res Soc Sci 91:102756. https://doi.org/10.1016/j.erss.2022.102756

Khan HR, Usman B, Zaman K, Nassani AA, Haffar M, Muneer G (2022) The impact of carbon pricing, climate financing, and financial literacy on COVID-19 cases: go-for-green healthcare policies. Environ Sci Pollut Res 29:35884–35896. https://doi.org/10.1007/s11356-022-18689-y

Khan M, Robinson S, Weikmans R, Ciplet D, Roberts JT (2020) Twenty-five years of adaptation finance through a climate justice lens. Clim Chang. 161:251–269. https://doi.org/10.1007/s10584-019-02563-x

Kim J, Kim S, Sohn J (2020) Trends in climate finance and ODA for global water infrastructure. J Korean Soc Water Wastewater 34:169–182. https://doi.org/10.11001/jksww.2020.34.3.169

Klöck C, Nunn PD (2019) Adaptation to climate change in small island developing states: a systematic literature review of academic research. J Environ Dev 28:196–218. https://doi.org/10.1177/1070496519835895

Kok B, Benli H (2017) Energy diversity and nuclear energy for sustainable development in Turkey. Renew Energy 111:870–877. https://doi.org/10.1016/j.renene.2017.05.001

Kouwenberg R, Zheng C (2023) A review of the global climate finance literature. Sustainability 15:1255. https://doi.org/10.3390/su15021255

Kumar A, Bhattacharya T, Mukherjee S, Sarkar B (2022) A perspective on biochar for repairing damages in the soil–plant system caused by climate change-driven extreme weather events. Biochar 4:22. https://doi.org/10.1007/s42773-022-00148-z

Kumar P, Sahu NC, Kumar S, Ansari MA (2021) Impact of climate change on cereal production: evidence from lower-middle-income countries. Environ Sci Pollut Res 28:51597–51611. https://doi.org/10.1007/s11356-021-14373-9

Lee C, Li X, Yu CH, Zhao J (2022) The contribution of climate finance toward environmental sustainability: new global evidence. Energy Econ 111:106072. https://doi.org/10.1016/j.eneco.2022.106072

Lee CC, Fang Y (2025) Climate finance for energy security: an empirical analysis from a global perspective. Econ Anal Policy 85:963–978

Lee CC, Fang Y, Quan S, Li X (2024) Leveraging the power of artificial intelligence toward the energy transition: the key role of the digital economy. Energy Econ 135:107654. https://doi.org/10.1016/j.eneco.2024.107654

Lee CC, Li M, Li X, Song H (2025) More green digital finance with less energy poverty? The key role of climate risk. Energy Econ 141:108144

Leal PH, Marques AC, Shahbaz M (2023) Does climate finance and foreign capital inflows drive de-carbonisation in developing economies? J Environ Manag 347:119100

Li C, Chen J, Grydehøj A (2020) Island climate change adaptation and global public goods within the Belt and Road Initiative. Isl Stud J 15:173–192. https://doi.org/10.24043/isj.134

Li N, Shi B, Wu L, Kang R, Gao Q (2022) Climate-related development finance, energy structure transformation and carbon emissions reduction: an analysis from the perspective of developing countries. Front Environ Sci 9:778254. https://doi.org/10.3389/fenvs.2021.778254

Liu X, Chen X, Li R, Long F, Zhang L, Zhang Q, Li J (2017) Water-use efficiency of an old-growth forest in lower subtropical China. Sci Rep. 7:42761. https://doi.org/10.1038/srep42761

Liu Y, Dong K, Nepal R (2024) How does climate vulnerability affect the just allocation of climate aid funds? Int Rev Econ Financ 93:298–317. https://doi.org/10.1016/j.iref.2024.03.036

Martey E, Etwire PM, Kuwornu JKM (2020) Economic impacts of smallholder farmers’ adoption of drought-tolerant maize varieties. Land Use Policy 94:104524. https://doi.org/10.1016/j.landusepol.2020.104524

Masud MAK, Sahara J, Kabir MH (2023) A relationship between climate finance and climate risk: evidence from the South Asian Region. Climate 11:119. https://doi.org/10.3390/cli11060119

Mir AA, Alghassab M, Ullah K, Khan ZA, Lu Y, Imran M (2020) A review of electricity demand forecasting in low and middle income countries: the demand determinants and horizons. Sustainability 12:5931. https://doi.org/10.3390/su12155931

Mori A, Rahman SM, Uddin MN (2019) Climate financing through the adaptation fund: what determines fund allocation? J Environ Dev 28:366–385. https://doi.org/10.1177/1070496519877483

Mungai EM, Ndiritu SW, Da Silva I (2021) Unlocking climate finance potential for climate adaptation: case of climate smart agricultural financing in Sub Saharan Africa. In: Oguge N, Ayal D, Adeleke L, Da Silva I (eds) African handbook of climate change adaptation. Springer International Publishing, Cham, pp 2063–2083. https://doi.org/10.1007/978-3-030-45106-6_172

Muyambo F, Belle J, Nyam YS, Orimoloye IR (2023) Climate-Change-induced weather events and implications for urban water resource management in the Free State Province of South Africa. Environ Manag 71:40–54. https://doi.org/10.1007/s00267-022-01726-4

Nock D, Levin T, Baker E (2020) Changing the policy paradigm: a benefit maximization approach to electricity planning in developing countries. Appl Energy 264:114583. https://doi.org/10.1016/j.apenergy.2020.114583

Pauw WP, Moslener U, Zamarioli LH, Amerasinghe N, Atela J, Affana JPB, Buchner B, Klein RJT, Mbeva KL, Puri J, Roberts JT, Shawoo Z, Watson C, Weikmans R (2022) Post-2025 climate finance target: how much more and how much better? Clim Policy 22:1241–1251. https://doi.org/10.1080/14693062.2022.2114985

Qi J, Qian H (2023) Climate finance at a crossroads: it is high time to use the global solution for global problems. Carbon Neutral 2:31. https://doi.org/10.1007/s43979-023-00071-7

Raddatz C (2007) Are external shocks responsible for the instability of output in low-income countries? J Dev Econ 84(1):155–187. https://doi.org/10.1016/j.jdeveco.2006.11.001

Rahaman MA, Rahman MM (2020) Climate justice and food security. In: Environmental policy. John Wiley & Sons, Ltd, pp 249–268. https://doi.org/10.1002/9781119402619.ch15

Rasheed N, Khan D, Gul A, Magda R (2023) Impact assessment of climate mitigation finance on climate change in South Asia. Sustainability 15:6429. https://doi.org/10.3390/su15086429

Rasul G, Sharma B (2016) The nexus approach to water–energy–food security: an option for adaptation to climate change. Clim Policy 16:682–702

Román MV, Arto I, Ansuategi A (2018) Why do some economies benefit more from climate finance than others? A case study on North-to-South financial flows. Econ Syst Res 30:37–60. https://doi.org/10.1080/09535314.2017.1334629

Sarker Md NI, Peng Y, Khatun Most N, Alam GMM, Shouse RC, Amin MR (2022) Climate finance governance in hazard prone riverine islands in Bangladesh: pathway for promoting climate resilience. Nat Hazards 110:1115–1132. https://doi.org/10.1007/s11069-021-04983-4

Sarr MD (2022) At COP 27, support poorest for climate loss and damage. Nature 611:9–9. https://doi.org/10.1038/d41586-022-03474-1

Savage M, Mujica-Pereira AV, Ross I (2015) Climate finance and water security. ResearchGate. https://doi.org/10.13140/RG.2.2.25571.07207

Scandurra G, Thomas A, Passaro R, Bencini J, Carfora A (2020) Does climate finance reduce vulnerability in Small Island Developing States? An empirical investigation. J Clean Prod 256:120330. https://doi.org/10.1016/j.jclepro.2020.120330

Scanlon BR, Fakhreddine S, Rateb A, de Graaf I, Famiglietti J, Gleeson T, Grafton RQ, Jobbagy E, Kebede S, Kolusu SR, Konikow LF, Long D, Mekonnen M, Schmied HM, Mukherjee A, MacDonald A, Reedy RC, Shamsudduha M, Simmons CT, Sun A, Taylor RG, Villholth KG, Vörösmarty CJ, Zheng C (2023) Global water resources and the role of groundwater in a resilient water future. Nat Rev Earth Environ 4:87–101. https://doi.org/10.1038/s43017-022-00378-6

Sharma RK, Kumar S, Vatta K, Bheemanahalli R, Dhillon J, Reddy KN (2022) Impact of recent climate change on corn, rice, and wheat in southeastern USA. Sci Rep. 12:16928. https://doi.org/10.1038/s41598-022-21454-3

Shumilova O, Tockner K, Sukhodolov A, Khilchevskyi V, De Meester L, Stepanenko S, Trokhymenko G, Hernández-Agüero JA, Gleick P (2023) Impact of the Russia–Ukraine armed conflict on water resources and water infrastructure. Nat Sustain 6:578–586. https://doi.org/10.1038/s41893-023-01068-x

Stewart WM, Roberts TL (2012) Food security and the role of fertilizer in supporting it. Procedia Eng 46:76–82. https://doi.org/10.1016/j.proeng.2012.09.448

Surminski S, Oramas-Dorta D (2014) Flood insurance schemes and climate adaptation in developing countries. Int J Disaster Risk Reduct 7:154–164. https://doi.org/10.1016/j.ijdrr.2013.10.005

Tauhid F, Zawani H (2018) Mitigating climate change related floods in urban poor areas: green infrastructure approach. J Reg City Plan 29:98. https://doi.org/10.5614/jrcp.2018.29.2.2

Tian J, Wang W, Wang Z, Fan W (2024) The interlinkage between land resources, food, water, income, and sustainable environment: evidence from China’s economy with COP27 perspective. Land Degrad Dev 35:2572–2590. https://doi.org/10.1002/ldr.5083

Tian X, An C, Chen Z (2023) The role of clean energy in achieving decarbonization of electricity generation, transportation, and heating sectors by 2050: a meta-analysis review. Renew Sustain Energy Rev 182:113404. https://doi.org/10.1016/j.rser.2023.113404

Tosun J (2014) Absorption of regional funds: a comparative analysis. JCMS: J Common Mark Stud 52(2):371–387. https://doi.org/10.1111/jcms.12088

Tofa AI, Kamara AY, Babaji BA, Akinseye FM, Bebeley JF (2021) Assessing the use of a drought-tolerant variety as adaptation strategy for maize production under climate change in the savannas of Nigeria. Sci Rep. 11:8983. https://doi.org/10.1038/s41598-021-88277-6

Umar M, Safi A (2023) Do green finance and innovation matter for environmental protection? A case of OECD economies. Energy Econ 119:106560. https://doi.org/10.1016/j.eneco.2023.106560

Vanegas Cantarero MM (2020) Of renewable energy, energy democracy, and sustainable development: a roadmap to accelerate the energy transition in developing countries. Energy Res Soc Sci 70:101716. https://doi.org/10.1016/j.erss.2020.101716

Venner K, García-Lamarca M, Olazabal M (2024) The multi-scalar inequities of climate adaptation finance: a critical review. Curr Clim Change Rep. 10:46–59

Vermeulen S, Zougmoré R, Wollenberg E, Thornton P, Nelson G, Kristjanson P, Kinyangi J, Jarvis A, Hansen J, Challinor A, Campbell B, Aggarwal P (2012) Climate change, agriculture and food security: a global partnership to link research and action for low-income agricultural producers and consumers. Curr Opin Environ Sustain 4:128–133. https://doi.org/10.1016/j.cosust.2011.12.004

Wan J, Qiu Q (2022) Depreciation rate by industrial sector and profit after tax in China. Chin Econ 55:111–128. https://doi.org/10.1080/10971475.2021.1930297

Weiler F, Klöck C, Dornan M (2018) Vulnerability, good governance, or donor interests? The allocation of aid for climate change adaptation. World Dev 104:65–77. https://doi.org/10.1016/j.worlddev.2017.11.001

Wong S (2016) Can climate finance contribute to gender equity in developing countries? J Int Dev 28:428–444. https://doi.org/10.1002/jid.3212

Xie L, Scholtens B, Homroy S (2023) Rebalancing climate finance: analysing multilateral development banks’ allocation practices. Energy Res Soc Sci 101:103127. https://doi.org/10.1016/j.erss.2023.103127

Yang S, Wang J, Dong K, Taghizadeh-Hesary F (2023) How justice is our energy future? Assessing the impact of green finance on energy justice in China. Ann Financ Econ 18:2350010. https://doi.org/10.1142/S2010495223500100

Yanda PZ, Mabhuye EB, Mwajombe A (2021) Linking coastal and marine resources endowments and climate change resilience of Tanzania coastal communities. Environ Manag 71:15–28

Yousaf M, Li J, Lu J, Ren T, Cong R, Fahad S, Li X (2017) Effects of fertilization on crop production and nutrient-supplying capacity under rice-oilseed rape rotation system. Sci Rep. 7:1270. https://doi.org/10.1038/s41598-017-01412-0

Yu CH, Wu X, Lee WC, Zhao J (2021) Resource misallocation in the Chinese wind power industry: the role of feed-in tariff policy. Energy Econ 98:105236