Abstract

This study employs an analytical framework that integrates realized moment measures with a TVP-VAR-based extended joint connectedness approach to examine higher-order moment and cross-moment risk spillovers among crude oil futures (CL), Dollar Index futures (DX), and S&P 500 E-mini futures (ES). The findings reveal that the interconnectedness between crude oil, stock, and forex markets is shaped by distributional moments, with realized volatility (RV) spillovers being significantly stronger than those of higher-order moments (RS, RK) and jumps (RJ). Crude oil consistently acts as a net transmitter across all measures, underscoring its dominant role, while the forex and stock markets emerge as the primary net recipients of volatility and kurtosis spillovers, respectively. Spillover dynamics exhibit time-varying behavior and high sensitivity to crises, including the crude oil price collapse, the US‒China trade war, the COVID-19 pandemic, and the ongoing conflicts in Ukraine and the Middle East. Notably, the RV, RJ, and cross-moment joint spillovers react more sharply to health crises, whereas higher-order moments respond more strongly to geopolitical shocks.

Similar content being viewed by others

Introduction

The study of spillovers and connectedness among international markets has gained significant attention, particularly since the development of the spillover index by Diebold and Yilmaz (2009, 2012, 2014). Increasing correlations among financial markets, especially during periods of market turbulence (Bai et al., 2003; Baele, 2005; Karolyi, 2003; Pericoli and Sbracia, 2003), have diminished diversification benefits and reduced risk management effectiveness, prompting investors to explore alternative asset classes (Beine et al., 2010). In this context, crude oil, foreign exchange, and equity markets play pivotal roles due to their deep integration into the global financial system and their influence on macroeconomic stability.

Crude oil is not only a key commodity but also a crucial driver of economic activity, affecting production costs, inflation, and corporate profitability. The foreign exchange market, on the other hand, serves as a transmission channel for global economic shocks, with currency fluctuations influencing trade balances, capital flows, and monetary policies. Equities, as a primary investment vehicle, reflect broader market sentiment and economic conditions.

However, the financialization of commodities, particularly crude oil, has intensified market volatility and strengthened comovements across asset classes (McMillan et al., 2021; Ji et al., 2020). Given the United States’ dominant role in global crude oil production and the Petrodollar System’s influence on currency markets, crude oil prices significantly impact stock and forex market behavior, and the bidirectional relationships among these markets are further shaped by economic conditions, monetary policy, investor sentiment, and geopolitical developments, making them critical for understanding asset pricing and risk transmission. These complexities are especially important in light of recent crises, such as the 2008 subprime mortgage crisis, the COVID-19 pandemic, and the Russia–Ukraine war, all of which have altered the dynamics of financial markets and commodities (Awartani et al., 2016b; Awartani and Maghyereh, 2016; Zhang and Sun, 2023; Zhang and Mao, 2022; Zhang and Wang, 2022; Zhang et al., 2022; Rubbaniy et al., 2024; Pandey, 2024; Lin and Wang, 2024; Zhang et al., 2024).

This paper investigates higher-order moment and cross-moment risk spillovers among the crude oil, forex, and stock markets using a novel analytical framework that integrates realized moment measures with the time-varying parameter vector autoregressive (TVP-VAR) extended joint connectedness approach. Specifically, we analyze crude oil futures (CL: NYMEX/CME GROUP), Dollar Index futures (DX: ICE), and S&P 500 E-mini futures (ES: CME GROUP) to capture the intricate transmission of risk across these major asset classes. Unlike traditional studies that focus on first- and second-moment interactions, we extend our analysis to include skewness, kurtosis, and jumps, providing a more comprehensive perspective on systemic risk.

The literature on spillovers across crude oil, forex, and stock markets primarily examines first- and second-moment interactions. Cassola et al. (2010) suggest that crude oil price shocks affect the stock market, which, in turn, influences exchange rates. In agreement with this finding, Basher et al. (2012) found that crude oil prices significantly impact both exchange rates and stock markets, often amplifying market volatility. Similarly, Cassola and Morana (2009) argue that crude oil prices play a significant role in stock price and exchange rate dynamics, although these relationships are not always symmetric across different market conditions, and Hamilton (2008, 2009) maintains that crude oil price increases tend to lead to a depreciation of the USD and lower stock market returns, primarily through reduced expectations of future economic growth and higher inflation. O’Neill et al. (2016) highlight that the interdependence between crude oil prices, exchange rates, and stock markets becomes particularly evident during periods of financial uncertainty. Despite these contributions, a gap remains in terms of the understanding of how higher-order moment spillovers propagate across major futures markets.

Our paper makes several significant contributions to the literature on cross-market risk transmission. First, we extend the existing research by analyzing spillovers across all four moments of the distribution—volatility, skewness, kurtosis, and jumps—whereas previous studies typically focused only on the first two moments. Each moment captures distinct aspects of market behavior: volatility measures the intensity of price fluctuations, skewness reflects the distributional asymmetry, kurtosis indicates tail risks and the likelihood of extreme events, and jumps represent sudden, large price movements. Our comprehensive approach reveals how these different risk factors coevolve and interact across markets, uncovering systemic risks that may remain hidden when examining each moment in isolation.

Second, we demonstrate the complex, nonlinear interconnections between crude oil, stock, and forex markets, where a price surge in one market can trigger distinct effects across different moments. For example, an increase in crude oil prices may heighten forex volatility while inducing negative skewness in equity, while higher-order moments, particularly skewness and kurtosis, provide deeper crisis insights than traditional volatility measures do. From a theoretical perspective, prospect theory (Kahneman and Tversky, 1979) suggests that investors exhibit loss aversion, making them highly sensitive to negative skewness, which reflects the probability of large downside risks. During crises, left-skewed returns amplify panic-driven selling, exacerbating market downturns. Additionally, the leverage effect (Black, 1976) explains how negative shocks increase financial leverage and perceived risk, leading to further declines in asset prices and left skewness.

Similarly, extreme value theory highlights kurtosis’s role in terms of identifying extreme tail risks, which intensify during crises, and liquidity spirals (Brunnermeier and Pedersen, 2009) illustrate how stress-induced forced liquidations amplify price swings. Traditional models such as GARCH, which assume normal return distributions, fail to capture these crisis-induced asymmetries and tail risks. By incorporating skewness and kurtosis, we offer a more comprehensive framework for assessing systemic risk and market stability.

Third, our analysis reveals that different types of crises produce distinct spillover patterns. While traditional volatility models capture some aspects of market linkages, they systematically underestimate the full extent of risk transmission. Examining cross-moment spillovers provides a more nuanced understanding of the coevolution and interaction among these risk factors, uncovering systemic risks that may remain hidden when analyzing each moment separately. The relationships between the crude oil, stock, and forex markets are highly nonlinear. For example, a sharp price jump in crude oil might cause a sudden shift in skewness or kurtosis in equity or forex markets. Cross-moment spillovers allow us to capture these nonlinear dynamics and better understand how different types of market shocks propagate across asset classes. By integrating all four moments into a unified framework, our study provides a more comprehensive understanding of financial contagion mechanisms, offering valuable insights for risk management, portfolio allocation, and financial regulation.

Fourth, our methodological contributions lie in the adoption of a TVP-VAR extended joint framework, which addresses the key limitations of traditional spillover measures. Unlike the original Diebold and Yilmaz (2009) approach, which relies on an arbitrarily chosen rolling window size, our method dynamically estimates spillovers without losing data points and effectively identifies variables as net receivers or contributors of shocks. This approach provides deeper insights into the magnitude and direction of risk transmission, allowing policy-makers to design targeted interventions that enhance financial stability.

Finally, we emphasize the role of futures markets in shaping spillovers. Unlike spot prices, futures markets embed expectations regarding future economic conditions and are highly sensitive to sentiment and risk appetite. This increased sensitivity amplifies shock transmission across asset classes, offering a richer understanding of interconnected risk.

Our findings reveal distinct risk transmission patterns among the crude oil, stock, and forex markets. The realized volatility (RV) results in significantly stronger spillovers (33.43% in the joint system) than higher-order moments (RS, RK) or jumps (RJ), and crude oil emerges as the dominant net transmitter across all risk measures. Forex markets primarily receive volatility and jump spillovers, while stock markets absorb kurtosis shocks. The spillover dynamics exhibit clear time-varying patterns, with higher sensitivity during major crises. Notably, the RV, RJ, and joint spillovers respond most strongly to health crises (e.g., COVID-19), whereas higher-order moments react more strongly to geopolitical events (e.g., trade wars and regional conflicts). This differential sensitivity underscores the importance of examining multiple risk dimensions, as traditional volatility-focused approaches may overlook crucial aspects of market interconnectedness during systemic shocks. Furthermore, the results highlight crude oil’s central role in cross-market risk transmission and demonstrate how crisis characteristics shape financial contagion patterns across asset classes.

This work is organized as follows: Sections “Literature review” to “Methodology” review the literature and methodology, Section “Data and descriptive statistics” presents the data, Section “Connectedness results” analyzes the results, and Section “Conclusions and implications” provides conclusions.

Literature review

Understanding the interconnections among crude oil, foreign exchange (forex), and stock markets is crucial for financial economists, policy-makers, and investors seeking to navigate global financial systems. These markets are deeply intertwined, with linkages shaped by macroeconomic fundamentals, monetary policy, and geopolitical events, and their dynamic relationships influence portfolio diversification, risk management, and asset pricing (Basher et al., 2012).

From a theoretical perspective, crude oil prices impact production costs, inflation, and economic growth, which, in turn, affect currency valuations and stock market performance. The transmission channels from crude oil price shocks to financial markets are extensively analyzed through asset pricing theories such as the consumption-based capital asset pricing model and the intertemporal CAPM (Merton, 1973), which emphasize how macroeconomic risk factors shape expected returns.

Stock market movements reflect investor sentiment and macroeconomic expectations, and rising equity markets typically signal investor confidence, attracting foreign capital inflows and strengthening the domestic currency. Conversely, a declining stock market can trigger capital flight and currency depreciation (Auboin and Ruta, 2013; Fratzscher et al., 2014). Forex markets also respond to energy price fluctuations, as crude oil is predominantly traded in U.S. dollars (USD) under the petrodollar system, creating a link between oil prices and exchange rate dynamics (Reboredo et al., 2021), and an increase in crude oil prices can drive global demand for USD, strengthening the currency. However, some studies highlight bidirectional causality: higher crude oil prices may weaken the USD by worsening trade balances, whereas a weaker USD can make crude oil more affordable for non-dollar economies, increasing demand and prices (Fratzscher et al., 2014).

Within the energy finance literature and asset-class linkage research, most studies have focused on interactions within the first and second moments of the distribution. Numerous studies have analyzed the relationship between crude oil and equities (e.g., Awartani et al., 2016b; Du and He, 2015; Awartani and Maghyereh, 2016; Liu et al., 2017; Wang and Wu, 2018; Demirer et al., 2020; Mensi et al., 2021, 2022; Ziadat et al., 2024). Similarly, other research has examined forex interactions with other asset classes (Baruník and Kočenda, 2019; Reboredo et al., 2021; Nekhili et al., 2021; Antonakakis et al., 2020; Ding et al., 2021; Asadi et al., 2022; Yahya et al., 2024; Huang et al., 2025). However, the neglect of higher-order moments in these analyses overlooks critical dimensions of the market dynamics despite requiring less computational complexity.

A smaller but growing body of research explores higher-moment interactions. Studies such as those by Bouri et al. (2021, 2023), Ahmed (2022), Gomez-Gonzalez et al. (2022), Nekhili and Bouri (2023), Zhang et al. (2023a), Cui and Maghyereh (2024), and Mensi et al. (2024) investigated higher-moment dynamics in commodities and equities, while parallel research efforts, such as those published by Do et al. (2016) and Zhang et al. (2023b), have examined these interactions between forex and equities.

While these studies have significantly advanced our understanding of higher-moment dynamics, our study addresses three critical gaps in the literature. First, whereas existing research has predominantly examined pairwise relationships (e.g., commodities-equities or forex-equities), we analyze the tripartite interaction among crude oil, forex, and stock futures—a crucial extension given the Petrodollar System’s role in interconnecting these markets. Second, moving beyond conventional static and rolling-window methodologies, we employ a TVP-VAR framework to more accurately capture dynamic spillover effects. This approach builds on recent methodological innovations in time-varying connectedness analysis (Antonakakis et al., 2020), extending their application to higher-moment risk transmission. Third, while prior research has focused primarily on spot markets, we center our analysis on futures contracts, which better reflect market expectations, risk premia, and price discovery during crises.

Methodology

Realized higher-order moments and jumps

We constructed the realized moment measures based on the intraday logarithmic returns. Compared with the ex-post moment measures used in Hau et al. (2024) and Cui and Maghyereh (2024), realized higher-order moments offer several advantages. First, intraday high-frequency data capture price fluctuations and trading activity within a day, providing a finer reflection of market dynamics. In contrast, ex-post moments based on daily data, which rely only on opening and closing prices, miss intraday volatility and market microstructure details. Second, high-frequency data are more sensitive in terms of detecting the market’s response to sudden events, allowing for a more accurate assessment of instantaneous volatility and risk changes. In contrast, daily data may smooth out or lag behind these reactions. Third, high-frequency data capture market microstructure characteristics, which significantly influence price formation and volatility. Realized higher-order moment measures, which are based on high-frequency data, effectively account for these microstructure effects, whereas ex-post daily-based moments do not. Thus, realized higher-order moments derived from high-frequency data offer deeper insights into market dynamics.

Before computing the realized moment measures, we detected outliers in the raw intraday high-frequency data using the interquartile range (IQR) method, and the results indicate that no outliers are present in the original 5-min high-frequency data. For details on the data preprocessing process, see Fig. A13.

We calculated the intraday returns for the \({i}^{{th}}\) intraday price as the natural logarithmic difference between two continuous price observations within a trading day.

Following Andersen and Bollerslev (1998), the RV can be computed as follows:

where \(i=(\mathrm{1,2},\ldots ,T)\) and where \(T\) denotes the number of intraday logarithmic returns.

Following Amaya et al. (2015), the realized skewness (RS) and kurtosis (RK) are computed as follows:

Barndorff-Nielsen and Shephard (2004, 2006) derived bipower variation (BV) as an estimator for the continuous component of RV, which helps to isolate the effects of jumps. The BV for a given time \(t\) is defined as:

Here, \({r}_{i,t}\) denotes high-frequency returns within day t, \(M\) represents the number of observations per day, and \({\mu }_{1}\) is the expected absolute value of a standard normal random variable. The constant \({\mu }_{a}\) in the context of bipower variation is expressed as:

Here, \({\mu }_{a}\) represents the expected value of the absolute value of a standard normal random variable raised to the power \(a\). Once we have defined the continuous component of RV, we can derive the unadjusted jump contribution, which is expressed as follows:

We define the realized jump (RJ) as follows (Zhou and Zhu, 2012; Bonato et al., 2020):Footnote 1

TVP-VAR extended joint connectedness

We employed the newly proposed TVP-VAR extended joint connectedness approach introduced by Balcilar et al. (2021) to conduct our spillover analysis. This method builds on the TVP-VAR connectedness approach from Antonakakis et al. (2020) and the joint spillover technique from Lastrapes and Wiesen (2021). Unlike conventional rolling-window VAR models, which suffer from data loss and sensitivity to extreme values, this approach mitigates overfitting risks through several key mechanisms. First, the framework employs Bayesian estimation within the Kalman filter, which inherently applies shrinkage regularization to time-varying parameters. This approach dampens excessive coefficient fluctuations, ensuring more stable and economically plausible parameter evolution (Durbin and Koopman, 2012; Koop and Korobilis, 2018). Second, the model imposes specific priors on the covariance matrices of state innovations, limiting parameter changes driven by noise rather than structural shifts. Third, while rolling-window methods amplify estimation errors due to short subsamples, the full-sample Kalman filter smooths the parameter evolution by leveraging all available information, reducing spurious fluctuations.

Moreover, unlike rolling-window approaches, the Kalman filter-based TVP-VAR model does not require stationarity, making it more suitable for spillover analysis among weakly stationary variables. Additionally, the generalized variance decomposition used for spillover calculations mitigates overfitting by focusing on forecast error variance shares rather than solely on the point estimates of coefficients. These features collectively ensure that the model captures genuine connectedness dynamics without overinterpreting transient noise—a critical advantage when analyzing small samples or high-frequency financial data, where overfitting risks are particularly pronounced.

We start by estimating a TVP-VAR model with a lag length of one.Footnote 2

where \({y}_{t}\) is an \(N\) vector representing the conditional volatilities of the variables in the system at time \(t\). \({y}_{t-1}\) is an \({N}_{p}\times 1\) vector containing lagged values of \({y}_{t}\), where \(p\) represents the number of lags in the VAR model. \({C}_{t}\) is an \(N\times {N}_{p}\) time-varying coefficient matrix that evolves over time, and \({\varepsilon }_{t}\) is an \(N\times 1\) disturbance term that follows a normal distribution with a time-varying variance‒covariance matrix \({\sum }_{t}\). The parameters \({C}_{t}\) follow a random walk process, depending on their own past values \(\left({C}_{t-1}\right)\) and an error term \({\mu }_{t}\), which follows a normal distribution with mean zero and variance \({R}_{t}\). \({\sum }_{t}\) is an \(N\times 1\) time-varying variance‒covariance matrix.

The TVP-VMA representation of the TVP-VAR can be expressed as:

Next, the H-step ahead generalized forecast error variance decomposition (GFEVD) is calculated by using:

where \({e}_{i}\) represents an \(k\times 1\) zero selection vector and where \({\xi }_{{ij},t}^{{gen}}\left(H\right)\) denotes the proportional reduction in the H-step forecast error variance of variable \(i.\)

where \({{gSOT}}_{{ij},t}\) is the scaled GFEVD.

Under the joint spillover framework, \({S}_{i\leftarrow \bullet ,t}^{{jnt},{from}}\) is defined as follows:

where \({M}_{i}\) represents an \(K\times K-1\) rectangular matrix that equals the identity matrix with the \({ith}\) column eliminated and where \({e}_{i}\) denotes a selection vector containing all zeroes except for a 1 in the \({ith}\) element.

Then, we can define the joint total connectedness index as:

The joint connectedness transmitted to others is computed as follows:

Balcilar et al. (2021) expanded upon the scaling method initially introduced by Lastrapes and Wiesen (2021). As a result, the scaling factor varies for each row and can be articulated as follows:

The scaling method introduced by Balcilar et al. (2021) improves efficiency by assigning a unique scaling factor to each row. The resulting spillover metrics can then be calculated as follows:

Finally, the total “FROM” (\({S}_{i\leftarrow \bullet ,t}^{{jnt},{from}}\)), “TO” (\({S}_{i\to \bullet ,t}^{{jnt},{to}}\)), total connectedness (\({jSO}{I}_{t}\)), net connectedness (\({S}_{i,t}^{{jnt},{net}}\)), and net-pairwise connectedness (\({S}_{{ij},t}^{{jnt},{net}}\)) measures are defined as:

Data and descriptive statistics

This paper examines higher-order moment and cross-moment risk spillovers among the crude oil, forex, and stock markets. Specifically, we select crude oil futures (CL: NYMEX/CME GROUP), Dollar Index futures (DX: ICE), and S&P 500 E-mini futures (ES: CME GROUP) as representative benchmarks for these markets.

Crude oil futures serve as the global standard for crude oil pricing and rank among the most actively traded energy instruments. The NYMEX crude oil futures contract captures global supply and demand dynamics and is highly responsive to geopolitical, economic, and market-specific factors, making it an essential proxy for the crude oil market (Alquist et al., 2013; Kilian and Murphy, 2014).

Dollar Index futures measure the value of the U.S. dollar relative to a basket of six major world currencies, serving as a widely recognized benchmark for global currency markets. Driven by macroeconomic factors, central bank policies, and global trade patterns, the dollar index provides a comprehensive measure of forex market dynamics (Reboredo and Rivera-Castro, 2014; Antonakakis and Kizys, 2015).

Finally, the S&P 500 E-mini Futures contract, a highly liquid derivative of the S&P 500 index, reflects the performance of 500 leading U.S. companies. Extensively used for hedging, speculation, and investment, it serves as a reliable indicator of broader U.S. equity market trends (Barunik et al., 2016; Awartani et al., 2016b).

Our sample period spans from January 3, 2010, to August 30, 2024, covering 4548 common trading days. This period encompasses several major global crises, including the Eurozone debt crisis, the Arab Spring, the Syrian Civil War, the Brexit referendum, the Chinese stock market crash, the US‒China trade war, the COVID-19 pandemic, the Russia-Ukraine war, and the Israeli-Palestinian conflict. We obtained 5-min intraday high-frequency data from Tick DataFootnote 3, as the adverse effects of microstructure noise can be significantly mitigated by using 5-min high-frequency data. As a result, the majority of studies have adopted this approach (see Amaya et al., 2015; Bonato et al., 2020; Bouri et al., 2021; Nekhili and Bouri, 2023; Wu et al., 2024; Mensi et al., 2024; Nekhili et al., 2024; Liu et al., 2025, among others).

Figures 1–4 illustrate the daily realized moment and jump measures over the sample period. Crude oil exhibited the highest RV in early 2020, coinciding with the onset of the COVID-19 pandemic and the Russia–Saudi crude oil price war. During this period, crude oil futures prices experienced a sharp decline due to reduced global demand and increased economic uncertainty, leading to significant price volatility. Similarly, the RV for the U.S. stock market spikes in early 2020.

Daily realized volatility series (RV)-Standardized.

Daily realized skewness series (RS)-Standardized.

Daily realized kurtosis series (RK)-Standardized.

Daily realized jump series (RJ)-Standardized.

The realized RS sequence displays notable time-varying characteristics and is approximately symmetrical around the zero axis. The realized RK for crude oil sharply increased following the onset of the COVID-19 pandemic, whereas the RK for the U.S. stock market rose significantly after the outbreak of the Russia–Ukraine war and the Israel–Hamas conflict. These phenomena suggest that geopolitical crises substantially increase the probability of extreme risk in the U.S. stock market. Moreover, RJ for the crude oil, forex, and stock markets exhibited significant spikes following the COVID-19 pandemic and the Russia–Ukraine war, indicating that these major crises triggered large and sudden price jumps across markets.

Table 1 presents the descriptive statistics for the RV, RS, RK, and jump (RJ) series. The mean values for the RV are approximately equal to zero, and the maximum value of the crude oil RV is significantly larger than that of the forex and stock markets. Additionally, the RV for crude oil exhibits the highest volatility, as indicated by its standard deviation. The mean values for the RS series are all negative, suggesting a greater likelihood of large downward price movements, and the RS for the forex market shows the strongest volatility, followed by crude oil futures. The mean values for the RK range from 8.3 to 10, with the maximum RK for crude oil being the highest, driven by the sharp decline in crude oil prices in early 2020; the RK for the forex market also displays the strongest volatility. The mean values for the RJ series are also approximately zero, with crude oil exhibiting the greatest fluctuations. Furthermore, the results of the ADF and PP tests indicate that all of the RV, RS, RK, and RJ series are stationary, thus meeting the modeling requirements.

Connectedness results

In this section, in addition to RV spillovers, this paper also explores the spillovers of the higher-order moments (RS and RK) and realized jumps among the crude oil, forex, and stock markets. Traditional volatility spillover models typically assume that risk transmission is linear; however, in actual markets, extreme events often trigger nonlinear risk jumps and tail dependencies—characteristics that cannot be adequately captured by second-order moments. Skewness (the third moment) in higher-order moments can characterize the asymmetric response of the market to positive and negative shocks, whereas traditional volatility spillover studies cannot distinguish between positive and negative shocks. Kurtosis (the fourth moment) and jump risk capture the clustering effect of extreme market fluctuations, which is crucial for understanding the risk transmission mechanisms of “black swan” events.

Extreme events, such as the 2008 financial crisis, the 2020 negative crude oil price event, and the COVID-19 pandemic, demonstrate that risk transmission among crude oil, forex, and stock markets often occurs through jumps and nonlinear mechanisms rather than simple volatility spillovers. Research on higher-order moments and jump risk can more accurately characterize the risk transmission paths of these extreme events. Investors and regulators are increasingly focused on managing tail risks, and higher-order moments can provide more comprehensive risk information, helping to build a more robust risk management framework. Furthermore, as core components of the global financial market, the higher-order moments and jump risk spillover effects of crude oil, exchange rates, and stock markets can offer valuable insights for cross-market risk monitoring and macroprudential policy.

Average connectedness table

Tables 2–3 show the average connectedness results for the RV, RS, RK, and RJ, respectively. The total spillovers of the RV, skewness, kurtosis, and jumps are 35.77%, 8.04%, 12.93%, and 18.16%, respectively, indicating that total volatility spillovers among crude oil, forex, and stock markets are significantly greater than those of higher-order moments and jumps. There is significantly greater interdependence in RV among the three asset classes than in higher-order moments (skewness and kurtosis) and jumps.

A potential explanation for this result lies in the fact that RV captures current market conditions and serves as a critical measure of uncertainty, directly influencing asset prices and investor behavior. In contrast, higher-order moments and jumps reflect asymmetric and extreme market characteristics, which occur less frequently. Skewness and kurtosis spillovers are relatively lower, underscoring their episodic nature, as they primarily emerge during directional market shifts or extreme events. Realized jumps, while more interconnected than skewness and kurtosis, remain less significant than volatility spillovers, likely due to their association with abrupt market reactions to unexpected news or geopolitical shocks. As Zhang and Ding (2018, 2021) asserted, liquidity is a key determinant of volatility spillovers across different markets; enhanced liquidity significantly intensifies volatility spillovers between crude oil, forex, and stock markets through the market linkage between fund flows and investor behavior. Specifically, high liquidity promotes the free flow of funds between the three markets, accelerates the dissemination of information and emotional contagion, and makes prices and risks more closely linked. These findings underscore the central role of RV as the dominant channel for risk transmission across markets, whereas higher-order moments and jumps provide additional insights into market behavior during periods of heightened stress or crises. This finding is consistent with several notable studies, such as Cui and Maghyereh (2023a, 2023b), Bouri et al. (2023), Bouri and Jalkh (2023), Cui et al. (2024), and Alomari et al. (2024).

The analysis of total spillovers reveals significant dynamics in risk transmission among the crude oil, forex, and stock markets. Crude oil consistently generates the strongest spillovers in RV, underscoring its pivotal role in global economic activity. Fluctuations in crude oil prices directly affect production costs, inflation, and market uncertainty, making the crude oil market a critical transmitter of volatility to other asset classes. Moreover, the U.S. stock market has emerged as the dominant transmitter of RS, reflecting its substantial influence on market asymmetry, which highlights how macroeconomic news, earnings announcements, and policy decisions originating in the stock market shape global investor sentiment. Both the forex and stock markets exhibit notable spillovers in RK, which captures the frequency and intensity of extreme market events. Moreover, the stock market leads to transmitting jump (RJ) spillovers, illustrating its heightened sensitivity to sudden shocks, such as geopolitical crises or unexpected policy changes.

On the receiving end, the forex and stock markets absorb significantly greater spillovers than crude oil across all measures, including the RV, RS, RK, and RJ, demonstrating their greater integration and interdependence within the global financial system. This increased susceptibility reflects the forex market’s exposure to macroeconomic fundamentals and monetary policies, whereas the stock market’s responsiveness to investor sentiment and economic performance amplifies its role as a risk absorber. These findings emphasize the systemic importance of these markets in risk propagation, offering valuable insights for policy-makers and investors in terms of managing cross-market risk exposure.

By calculating the differences between the “TO” and “FROM” spillovers, we derived the net spillovers for each market, which are displayed in the last row of the connectedness tables. Crude oil functions as the largest net transmitter of the RV (21.78%), whereas the forex (-18.56%) and stock (-3.22%) markets are net recipients. Notably, crude oil also acts as the net spreader of RS, RK, and RJ spillovers. This finding indicates that crude oil dominates the risk spillovers within the crude oil-forex-stock system. Fluctuations in crude oil prices have substantial ripple effects on other markets, highlighting for investors and policy-makers the importance of closely monitoring the crude oil market as a key risk driver. The U.S. stock market acts as a net receiver of RS and RK spillovers while transforming into a net transmitter of RJ spillovers, and the forex market functions as a net receiver of RK and RJ spillovers, reflecting its sensitivity to extreme risks emanating from both the crude oil and stock markets. Furthermore, the net spillovers of the RV and RJ are larger than those of higher-order moments.

Notably, in addition to the spillovers at the same moment, we also quantified the cross-moment spillovers (RV-RS-RK-RJ) among the crude oil, forex, and stock markets within a joint system. As shown in Table 3, the total number of spillovers within the cross-moment joint system is 33.43%, which is remarkably greater than the total RS, RK, and RJ spillovers. This finding indicates that the interplay between RV, skewness, kurtosis, and jumps collectively plays a more significant role in driving the overall risk transmission across crude oil, forex, and stock markets than any single higher-order moment in isolation. The cross-moment joint risk spillover reflects the interaction and synergistic effects between different risk dimensions (such as volatility and skewness, kurtosis and jumps), and since these risk dimensions capture market uncertainty (volatility), asymmetry (skewness), extreme risk (kurtosis), and sudden shocks (jumps), their combined effects can more comprehensively characterize the overall attributes of market risks, thereby resulting in a stronger spillover effect. For example, crude oil volatility significantly affects asymmetry and tail risks in the forex and stock markets.

These relationships highlight the importance of considering the interconnectedness of these different aspects of market behavior rather than analyzing them in isolation. The crude oil RV, forex RV, and forex RJ spread relatively higher spillovers to the joint system, whereas the forex RJ and stock RJ receive stronger spillovers from other markets. Regarding net connectedness, we observe that the crude oil RV is the largest net transmitter of risk among the assessed moments, with a net spillover value of 31.15%. This finding suggests that fluctuations in crude oil volatility significantly influence other markets, making it a key driver of systemic risk. Additionally, the crude oil RS and RK also act as net transmitters, although to a lesser extent, with values of 7.42% and 6.62%, respectively. Overall, these findings emphasize the dominant role of crude oil in terms of transmitting volatility, skewness, and tail risk to other markets, suggesting that changes in crude oil dynamics are likely to have considerable implications for investors and policy-makers monitoring interconnected financial systems.

Dynamic total connectedness

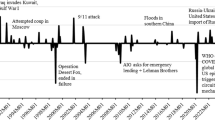

Our analysis of the dynamic evolutionary trends in total spillovers reveals significant temporal variability, as shown in Fig. 5, with spillovers displaying heightened sensitivity to major crises. Notably, the dynamic total RV spillovers fluctuate between 15% and 70%. A particularly sharp rise occurred between late 2014 and early 2015, increasing from 25% to 68%; this period corresponds to the crude oil price collapse and escalating geopolitical tensions in the Middle East. The sharp decline in crude oil prices during this time negatively impacted U.S. energy companies such as ExxonMobil and Chevron, leading to substantial losses in the energy sector’s stock prices. Furthermore, falling crude oil prices triggered broader concerns about global economic growth, amplifying uncertainty in financial markets. Concurrently, conflicts in the Middle East heightened fears of crude oil supply disruptions, leading to increased volatility in crude oil prices. Geopolitical risks during this period also drove investors toward safe-haven assets such as the U.S. dollar, boosting demand for the currency and adding to volatility in the forex market. These interlinked events highlight the intricate relationships between the crude oil, forex, and stock markets, underscoring their interconnectedness and collective response to external shocks.

Dynamic total spillover index.

Another notable sharp rise in total RV spillovers (from 28% to 70%) occurred in early 2020, coinciding with the onset of the COVID-19 pandemic, which suggests that the global health crisis significantly intensified the total volatility spillovers across the crude oil, forex, and stock markets. The sudden onset of the pandemic sparked investor panic and uncertainty, driving volatility in these markets due to fears of economic shutdowns, decreased consumer spending, and global supply chain disruptions. Several empirical studies have confirmed the substantial impacts of this event on volatility spillovers across various markets (see Cui and Maghyereh, 2023a, 2023b; Bouri and Jalkh, 2023; Alomari et al., 2024; He and Hamori, 2024).

The dynamic total RS and RK spillovers show similar trends. In late 2011, the total RS spillovers rose from 2% to 30%, whereas the total RK spillovers increased from 5% to 42%. During this period, the European sovereign debt crisis reached its peak, generating considerable anxiety about the stability of various Eurozone nations. Uncertainty from the debt crisis fueled investor risk aversion, leading to greater skewness and kurtosis in markets, indicating heavier tails and more pronounced outliers. Notably, the total RS and RK spillovers also experienced a sharp increase in mid-2022, reaching their highest levels. This surge can be attributed to the outbreak of the Russia–Ukraine war, which disrupted crude oil and natural gas supply chains, increasing energy prices. This geopolitical risk event introduced significant uncertainty into both the crude oil and stock markets. Compared with the COVID-19 pandemic in 2020, our findings indicate that the total RS and RK spillovers are more sensitive to the onset of the Russia–Ukraine war, as geopolitical tensions rapidly shift investor sentiment, triggering abrupt transitions from risk-on to risk-off behaviors and leading to asymmetric market reactions that increase skewness. Furthermore, the unpredictability of such conflicts amplifies the likelihood of extreme market movements, increasing kurtosis. Our findings align with several studies that also reported that this geopolitical risk event significantly intensified spillovers of higher-order moment risks across various markets (see Cui and Maghyereh, 2023a, 2023b; Zhang et al., 2023a; Cui et al., 2024; Chu et al., 2024; Gao et al., 2024).

Another notable observation is the sharp increase in the total realized RS and RK spillovers in October 2023, corresponding to the outbreak of the Israeli–Hamas war. This conflict introduced substantial uncertainty into both regional and global geopolitical dynamics. Such events often lead to heightened speculation among investors, resulting in abrupt market movements as they adjust to perceived risks. These reactions amplify spillovers as markets respond to shifts in sentiment and risk assessment, emphasizing the sensitivity of higher-order moments to geopolitical shocks. Our findings are supported by recent studies, such as Cui and Maghyereh (2024), Khan et al. (2024), and Lin et al. (2024).

The dynamic total RJ spillovers fluctuate between 5% and 62%, with several significant spikes occurring in late 2014, early 2018, 2020, and 2022. These spikes align with major events such as the onset of the crude oil price collapse, the US‒China trade war, the COVID-19 pandemic, and the Russia-Ukraine war. This finding suggests that these crises significantly enhanced cross-market transmission due to extreme price fluctuations.

Furthermore, the dynamic total cross-moment spillovers range between 10% and 85%. A significant spike from 20% to 85% occurred following the onset of the COVID-19 pandemic, and an additional important rise was noted in early 2015, coinciding with the crude oil price crisis. Furthermore, there was a substantial increase in total cross-moment spillovers after the onset of the Russia–Ukraine war, rising from 50% to 78%. In general, the sharp rise in early 2020 was the most striking. This finding demonstrates that the cross-moment joint spillovers among the crude oil, forex, and stock markets increased sharply due to the COVID-19 pandemic. The pandemic triggered extreme price movements across these markets, amplifying realized skewness and kurtosis, which caused asymmetric market reactions, with extreme downside risks dominating returns. Additionally, the pandemic led to fat-tailed return distributions, meaning that large price swings became more frequent. Suddenly, discontinuous price changes (realized jumps) occurred in all three markets, driven by unexpected news, policy announcements, and shifts in investor sentiment. Since cross-moment joint spillovers capture interactions between various risk dimensions, the impact of the COVID-19 outbreak on dynamic spillovers was particularly profound.

In summary, the dynamic total spillovers for the RV, RS, RK, and RJ, as well as the cross-moment joint system, are time-variant and highly responsive to major crises such as the crude oil price crisis, the US–China trade war, the COVID-19 pandemic, the Russia–Ukraine war, and the Israeli–Hamas war. Notably, the total RV, RJ, and cross-moment joint spillovers are more sensitive to global health crises, whereas the higher-order moment risk spillovers are more responsive to geopolitical events. The outbreak of COVID-19, for example, introduced significant uncertainty into the crude oil, forex, and stock markets. This uncertainty was influenced by factors such as the expected progress of the outbreak, government responses, and the global spread of the epidemic, and as a result, wild price fluctuations occurred, especially during the early stages of the pandemic. Therefore, the stock and commodity markets experienced sharp declines and rallies. During such crises, rapid and volatile changes in market sentiment often lead to spikes in volatility and the creation of jump effects, where prices change drastically in short periods. At the start of the outbreak, global lockdowns and quarantine measures caused a sharp economic slowdown, resulting in noticeable short-term jump effects, such as price collapses or surges, in the stock market, crude oil, and forex markets, and panic among market participants drove rapid changes in asset prices, particularly in the early days of the epidemic, when markets were highly sensitive to information. This increased volatility aligns with the observed spillovers in the RV and RJ, which were amplified by heightened uncertainty during global health crises. Several studies have highlighted the significant impacts of the COVID-19 pandemic on total volatility spillovers (Dai et al., 2022; Samitas et al., 2022; Cui and Maghyereh, 2023b; Zhang et al., 2023a, b; Yuan and Du, 2023; Cui et al., 2024).

In contrast, geopolitical events such as the Russia–Ukraine war tend to trigger extreme asymmetric reactions in the crude oil, forex, and stock markets; such extreme events cause sharp asset price fluctuations in short periods, significantly increasing tail risks (Hu et al., 2024). The Russia–Ukraine war has directly impacted the global energy market, particularly the crude oil supply. As a major exporter, Russia’s involvement in the war disrupted supply and increased uncertainty, leading to sharp fluctuations in crude oil prices and affecting the skewness and kurtosis of the crude oil futures market. These types of geopolitical risks typically introduce long-term uncertainty, with market volatility peaking after unexpected events, and the war has disrupted global supply chains, particularly energy, agricultural products, and metals (Cui et al., 2023), further intensifying uncertainty in the crude oil and stock markets. Many studies have also shown that the Russia–Ukraine war has significantly increased the total spillovers related to higher-order moments (Cui and Maghyereh, 2023a, 2023b, 2024; Cui et al., 2024; Zhang et al., 2023a, b; Chu et al., 2024; Ahmed et al., 2024; Banerjee et al., 2024).

Dynamic net connectedness

Figures 6–9 depict the dynamic net spillovers related to the RV, RS, RK, and RJ across the crude oil, forex, and stock markets. Focusing on the RV, Fig. 6 reveals that crude oil often acts as a net spreader of volatility spillovers during periods of heightened market activity. From 2010 to 2014 and again in 2022, crude oil consistently transmitted more volatility spillovers to other markets. This pattern is particularly notable in 2010 and 2011, a period of robust economic growth and rising energy demand, which drove higher crude oil prices and increased price fluctuations. These dynamics spilled over into equity and currency markets, amplifying cross-market volatility.

Dynamic net connectedness-RV.

Dynamic net connectedness-RS.

Dynamic net connectedness-RK.

Dynamic net connectedness-RJ.

Following the outbreak of the COVID-19 pandemic, net RV spillovers surged sharply due to the collapse in crude oil prices, driven by plummeting demand and the Russia–Saudi crude oil price war. Similarly, during the Russia–Ukraine war, crude oil continued to spread greater net RV spillovers, reflecting the market’s sensitivity to geopolitical tensions and energy supply risks.

In contrast, the U.S. stock market functioned primarily as a net receiver of RV spillovers from 2010 to 2014, particularly in 2010 and 2011. However, during 2015 and 2016, it shifted roles and became a notable spreader of spillovers, driven by major geopolitical and economic shocks. The 2015 Iran nuclear deal, which lifted sanctions and flooded global markets with Iranian oil, plunged crude prices. This event hit U.S. energy stocks and credit markets particularly hard, sending shockwaves through other sectors and across borders. At the same time, escalating conflicts in Syria and Ukraine, along with U.S. sanctions and military involvement, turned Wall Street into a barometer for global risk, and investors piled into U.S. assets as safe havens, strengthening the link between American markets and the rest of the world. Moreover, China’s 2015 stock crash and sudden yuan devaluation unsettled investors, causing U.S. markets to overreact to signs of slowing global growth, further amplifying spillovers.

The COVID-19 pandemic later intensified this trend. When the markets cratered in March 2020, the Federal Reserve’s massive stimulus helped U.S. stocks rebound faster than others did, creating a lopsided recovery that magnified volatility spillovers to lagging economies. Tech giants such as Apple and Amazon—already dominant in U.S. indices—became even more influential during the pandemic, meaning that their wild swings rippled through tech-heavy markets worldwide. Additionally, the dollar’s dual role as a safe-haven asset and a reflation trade anchor further tightened global financial conditions to U.S. market movements, particularly during the Treasury yield spikes in 2021.

Moreover, the forex market consistently functioned as a net receiver of RV spillovers throughout the study period. It exhibited particularly strong spillover reception in 2010 and 2011, likely due to heightened volatility in the crude oil and equity markets during this time. These findings align with existing research (Mohammed et al., 2023; Gong et al., 2021), further highlighting the intricate interdependence among crude oil, stock, and forex markets during periods of economic and geopolitical turmoil.

Figures 6–9 illustrate the dynamic net spillovers for the RS, RK, and RJ, revealing discontinuous patterns and shifting roles among the crude oil, forex, and stock markets. In terms of the RS, the net spillovers (Fig. 7) oscillate between positive and negative values, signifying transitions between roles as net transmitters and receivers. The U.S. stock market has primarily functioned as a net receiver of RS spillovers, except during events such as the crude oil price crisis in March 2015, when crude oil emerged as the dominant transmitter. Similarly, the forex market exhibited strong net RS spillover transmission during the European debt crisis in March 2012 and the onset of the COVID-19 pandemic in early 2020, both of which were marked by heightened uncertainty.

In terms of the RK (Fig. 8), crude oil has predominantly acted as a net transmitter, particularly in March 2014 and March 2015 during the Crimean crisis and the crude oil price crisis. Significant net RK spillovers from crude oil were also observed in mid-2012 amid rising tensions over Iran’s nuclear program and potential Middle East conflicts, which intensified concerns about crude oil supply disruptions. Similarly, crude oil transmitted substantial RK spillovers during the Russia–Ukraine war.

In contrast, the forex and stock markets functioned as net receivers of RK spillovers in mid-2014 and March 2015, a period marked by sharp declines in crude oil prices that propagated risks across these markets. The forex market also exhibited heightened RK spillovers between March and June 2012. These findings align with those of previous studies, including those of Gomez-Gonzalez et al. (2022), Dai and Zhu (2023), Banerjee et al. (2024), and Wang et al. (2024), which highlight the significant spillover effects of crude oil kurtosis on financial markets.

In terms of the RJ (Fig. 9), crude oil emerges as the primary transmitter of jump spillovers, with the U.S. stock and forex markets receiving notable spillovers during the European debt crisis in early 2010. This finding aligns with Bouri et al. (2021), which identified crude oil as a key driver of RJ spillovers. During the COVID-19 pandemic (2020–2021), the stock market consistently functioned as a net transmitter of RJ spillovers, whereas the forex market acted as a net receiver. This finding suggests that sudden, extreme price fluctuations in stock markets had pronounced effects on other markets, with the forex market absorbing shocks from jumps in both crude oil and stock prices. These results underscore crude oil’s critical role as a primary transmitter of higher-order moment spillovers and highlight the distinct responses of stock and forex markets during periods of heightened market stress.

Figure 10 illustrates the dynamic net spillovers at each moment for the crude oil, stock, and forex markets, and we find that the crude oil RV, RS, and RK consistently act as net transmitters throughout most of the sample period. Notably, the crude oil RV generated the most significant net spillovers to the cross-moment joint system in 2020 and 2021, coinciding with the COVID-19 pandemic and suggesting that crude oil volatility played a major role in driving uncertainty and extreme fluctuations during the pandemic, as reflected in the interconnectedness of various statistical moments across these markets.

Dynamic net connectedness-Cross-moments.

The crude oil RJ predominantly received net spillovers throughout the sample period, except at the onset of the COVID-19 pandemic, while the forex RV presents relatively greater net spillovers in 2021 and 2022. Forex RJ consistently functioned as a net recipient from 2010 to 2020 but transitioned into a net spreader from 2021 to 2024. In the aftermath of the COVID-19 pandemic, the RK experienced stronger net spillovers from other markets, and the stock RV and RJ received considerable net spillovers in 2020 and 2021. Finally, we observe that the magnitude of the net RS and RK spillovers is relatively lower than that of the RV and RJ spillovers.

Dynamic net pairwise connectedness

Section “Dynamic net connectedness” demonstrates that crude oil transmits significant net spillovers of RV, RS, RK, and RJ throughout the integrated “crude oil-forex-stock” system. Notably, the RV, RS, and RK of crude oil consistently acted as net transmitters for most of the sample period, reaffirming its dominant role in cross-market risk transmission. Given this phenomenon, quantifying the net spillovers from crude oil to forex and stock markets becomes critically important. This section specifically addresses three key objectives: first, it precisely measures the magnitude and directionality of net spillovers across multiple risk dimensions (RV, RS, RK, RJ, and cross-moments) from crude oil to U.S. financial markets, filling a crucial gap in understanding commodity‒financial market linkages. Second, it examines how these spillover patterns evolve over time, with a particular focus on periods of geopolitical crises that affect the oil supply, financial market turbulence, and macroeconomic instability. Third, it differentiates spillover effects between forex markets (particularly USD pairs) and equity markets (focusing on S&P 500 components), providing nuanced insights into market-specific vulnerability patterns.

The empirical results for the RV, RS, RK, RJ, and cross-moments are presented in Figs. 11–18. Our analysis reveals that these dynamic net pairwise spillovers are time-varying and exhibit heightened sensitivity to major crises. As shown in Fig. 11, crude oil transmitted the strongest net RV spillovers to the forex and stock markets, particularly in 2010 and 2011, while the forex market consistently acted as a net receiver of RV spillovers from crude oil throughout the sample period. Following the onset of COVID-19 and the Russia–Ukraine war, crude oil’s net RV spillovers to both forex and equities intensified. Notably, in the second half of 2015, the U.S. stock market transmitted significant net RV spillovers back to crude oil, marking a rare reversal in the spillover direction.

Dynamic net-pairwise connectedness-RV.

Dynamic net-pairwise connectedness-RS.

Dynamic net-pairwise connectedness-RK.

Dynamic net-pairwise connectedness-RJ.

Dynamic net-pairwise connectedness-Cross-moments-Crude Oil.RV.

Dynamic net-pairwise connectedness-Cross-moments-Crude Oil.RS.

Dynamic net-pairwise connectedness-Cross-moments-Crude Oil.RK.

Dynamic net-pairwise connectedness-Cross-moments-Crude Oil.RJ.

Figure 12 shows that the magnitude of the dynamic net RS (skewness) spillovers from crude oil to forex and equities is significantly weaker than that of RV spillovers. However, crude oil conveys relatively stronger net skewness spillovers to the U.S. stock market in early 2013, 2014, and 2015, indicating a period in which oil prices exerted an asymmetric and economically meaningful influence on equities. Another key finding is that the forex market transmitted comparatively stronger net RS spillovers to crude oil in early 2012, suggesting a pronounced asymmetric impact of currencies on oil during that phase. This finding aligns with significant fluctuations in major currencies (especially the USD) in 2012, which directly affected crude oil prices, given that oil is denominated in dollars.

As presented in Fig. 13, crude oil transmitted stronger net RK spillovers to the forex and stock markets during 2014 and 2015, coinciding with the crude oil price collapse. Among these markets, the dynamic net RK spillovers transmitted to the stock market are relatively stronger, which suggests that extreme downside risks in crude oil significantly increase the likelihood of extreme events in both the forex and stock markets. Similar to the RS spillovers, the forex market exhibited the strongest net RK spillovers to crude oil in the first half of 2012. During this period, extreme fluctuations in the U.S. dollar exchange rate significantly affected the crude oil futures market.

Figure 14 highlights that crude oil exhibited notably stronger net RJ spillovers to the forex market in the years 2010, 2015, 2018, and 2022, aligning with key events such as the European debt crisis, the crude oil price crisis, the US‒China trade war, and the Russia-Ukraine war. Furthermore, following the onset of the COVID-19 pandemic, crude oil also conveyed substantial net RJ spillovers to the forex market. In contrast, with respect to the stock market, crude oil transmitted relatively stronger net RJ spillovers, primarily in 2010 and 2022.

Figures 15–18 show the dynamic net pairwise spillovers transmitted from crude oil’s realized moments to the realized moments of the U.S. stock and forex markets. As illustrated in Fig. 15, the crude oil RV conveyed relatively stronger net spillovers to its own realized RS, RK, and RJ, as well as to the realized moments of the U.S. stock and forex markets, particularly during 2020, 2021, and 2022. Fluctuations in crude oil volatility significantly amplified asymmetric and extreme tail risks, not only within the crude oil market but also in the U.S. stock and forex markets. This period, marked by the collapse of crude oil prices during the COVID-19 pandemic and their subsequent surge amid the Russia–Ukraine war, highlights how heightened volatility can skew asset returns, signaling elevated downside risk and prompting more conservative strategies that may trigger market sell-offs. Such volatility also increased the frequency of outlier events and dramatic price swings, increasing kurtosis values and reflecting a heightened risk of substantial market movements. Moreover, the crude oil RV consistently spread net spillovers to its own RJ from 2010 to 2022, and the highest net spillovers from the crude oil RV occurred to the forex RJ and stock RV in 2010. Our findings diverge from those of Awartani et al. (2016b), Chen and Zhang (2023), Mohammed et al. (2023), Cui and Maghyereh (2023b), and Gong et al. (2021), as we uncovered specific net spillovers from crude oil volatility to the realized RS, realized RK, and RJ in both the stock and forex markets.

Figure 16 shows that crude oil’s realized RS also transmits considerable spillovers to the realized moments of the forex and stock markets during specific periods. Specifically, the crude oil RS transmitted strong net spillovers to the forex RS, realized RK, and RJ, as well as the stock RJ, in 2020, 2021, and 2022. The crude oil RS conveyed notably greater net spillovers to the forex RV in 2018, the forex RJ from 2010 to 2012, and the stock RJ in 2017. This observation suggests that downside risk in crude oil significantly impacts volatility, extreme risk, and jumps in the forex and stock markets. Another noteworthy result is that the crude oil RK transmitted consistent net spillovers to its own RS from 2010 to 2019, which implies that when there are shifts in the extremity of crude oil returns, these shifts also influence the asymmetry of the return distribution.

As illustrated in Fig. 17, during the crude oil price crisis, the crude oil realized RK generated significant net spillovers to its own jumps as well as to the RV and jumps in the foreign exchange market and the RV, kurtosis, and jumps in the stock market, suggesting that the dramatic decline in crude oil prices impacted volatility, extreme risk, and jump risk in both the forex and stock markets. The crude oil RK spread stronger net spillovers to its own jumps and to the stock market’s jumps in 2017, likely influenced by Qatar’s diplomatic crisis that year. Although the crisis did not lead to dramatic fluctuations in crude oil prices, its heightened market awareness of geopolitical risks in the Middle East subsequently affected the international crude oil market. Furthermore, the crude oil RK also exhibited considerable net spillovers to the forex RK, stock RV, and RJ in 2020, 2021, and 2022, and this period witnessed both extreme collapses and sharp increases in crude oil prices. Consequently, the extreme risks associated with crude oil significantly influenced the tail risks and jump dynamics in both the forex and stock markets. Figure 18 illustrates that, although less consistently, the crude oil RJ transmitted notable net spillovers to the forex RV and RJ during the crude oil price crisis. In contrast, during the COVID-19 pandemic, the crude oil RJ experienced significant net spillovers from the forex RV, RS, RK, and RJ while also transmitting substantial net spillovers to the stock market, particularly to its RS, RK, and RJ. All of the above results demonstrate that crude oil volatility not only significantly affects volatility in the forex and stock markets but also impacts realized skewness, kurtosis, and jumps. Moreover, the crude oil RS and RK also transmit notable net spillovers to the forex and stock market moments during specific periods.

In conclusion, the empirical findings confirm that crude oil plays a dominant role in transmitting risk spillovers to the forex and stock markets, particularly through the RV, RS, RK, and RJ. It consistently acts as a net transmitter, with spillovers intensifying during major crises such as the 2014–2015 oil price collapse, the COVID-19 pandemic, and the Russia–Ukraine war. The forex market, especially USD pairs, receives strong RV spillovers, whereas RS and RK spillovers exhibit asymmetry, most notably in 2012 due to fluctuations in the U.S. dollar. Extreme downside risks in crude oil heighten financial market instability, particularly during oil price crises, and RJ spillovers surged during key events such as the European debt crisis and the US‒China trade war, further illustrating the influence of crude oil on global financial markets. Crude oil volatility amplifies tail and jump risks, significantly affecting asset return distributions, and the sharp fluctuations in oil prices from 2020 to 2022 further underscore its destabilizing effects, reinforcing crude oil’s central role in financial market risk dynamics.

Robustness check

To further validate the robustness of the dynamic spillover results, we reselected the lag order of the VAR model and the forecast horizon and then recalculated the dynamic spillover index. Specifically, five different lag orders (1, 2, 3, 4, and 5) were tested while keeping the forecast horizon fixed at 20 days. The results are shown in Figs. A1–A5. Next, five different forecast horizons (10, 20, 30, 40, and 50 days) were examined while maintaining a lag order of 1, with the results presented in Figs. A6–A10. As observed in the figures, despite variations in lag orders and forecast horizons, the dynamic total spillover indices exhibit a highly similar trend to the original total spillover index, particularly showing a significant increase following major crises. Overall, these findings confirm the robustness of the dynamic total spillover results.

We further employed the TVP-SV-VAR model to assess the impact of geopolitical events on the total spillovers of the RV, RS, RK, RJ, and the cross-moment joint system.Footnote 4 Fig. A11 illustrates the dynamic time-varying trend of the TCIs following a one-unit standard positive shock to the GPR at three different lead times (4, 8, and 12 periods ahead). As shown in Fig. A11, the time-varying equal-interval impulse response results indicate that geopolitical risks exert a positive effect on higher-order moment spillovers (RS and RK), with the intensity of the shock increasing significantly after the outbreak of the Russia–Ukraine war in February 2022. Following the onset of the COVID-19 pandemic, geopolitical risks also contributed to an increase in total RV spillovers, although with a relatively lower magnitude. With respect to the total RJ and cross-moment spillovers, geopolitical risks exert notable positive shocks between 2010 and 2014. However, after the Russia–Ukraine war erupted, the impact of geopolitical risk on the total RJ spillovers became distinctly positive.

To further examine the effects of geopolitical risks on total spillover indices at specific points in time, we analyze Fig. A12, which presents three key time points: March 2020 (COVID-19 outbreak), February 2022 (Russia–Ukraine war), and October 2023 (Israel–Hamas war). As depicted in Fig. A12, geopolitical risks have significantly influenced the total spillovers of the RV, RS, RK, and RJ at these time points, except for the total cross-moment joint spillovers. Overall, these impulse response findings strongly support the dynamic spillover analysis results presented in Section “Dynamic total connectedness”.

Conclusions and implications

In this study, we examined the interconnectedness of the crude oil, stock, and forex markets through higher-order moment and cross-moment spillovers, offering valuable insights into their dynamic relationships and risk transmission mechanisms. By integrating realized moment measures with the TVP-VAR extended joint connectedness approach, we derived several key findings.

First, our spillover analysis revealed that the magnitude of total spillovers varies across the RV, RS, RK, and RJ. Among these, the RV exhibited the highest spillovers at 35.77%, followed by the RJ at 18.16%, the RK at 12.93%, and the RS at 8.04%. Additionally, the total spillover within the RV-RS-RK-RJ cross-moment joint system was notably high at 33.43%, highlighting the complex interdependencies among these risk measures.

Second, crude oil consistently serves as a major net transmitter of spillovers across all realized moments, with the RV (21.78%) and the RJ (11.33%) playing particularly dominant roles. This result underscores crude oil’s critical influence on the crude oil-forex-stock system’s risk transmission. Moreover, the forex market emerges as the largest net receiver of RV and realized jump spillovers, whereas the stock market primarily absorbs realized kurtosis spillovers. Within the cross-moment joint system, the RV of crude oil is the most significant net transmitter, followed by realized skewness and kurtosis.

Third, our dynamic spillover analysis reveals substantial time-varying characteristics, with spillovers intensifying during major crises such as the crude oil price collapse, the US‒China trade war, the COVID-19 pandemic, the Russia-Ukraine war, and the Israel–Hamas war. Notably, RV, RJ, and cross-moment joint spillovers were more reactive to global health crises, whereas higher-order moments (RS and RK) were more sensitive to geopolitical events. These findings underscore how different types of risks propagate across markets under varying crisis conditions.

Finally, the dynamic net-pairwise connectedness results indicate that crude oil transmitted the strongest net RV and RJ spillovers to the forex and stock markets in 2010 and 2011, coinciding with the European debt crisis and the Arab Spring. The magnitude of these spillovers rose sharply following the outbreak of COVID-19 in early 2020. Additionally, crude oil conveyed the highest RK spillovers to the forex and stock markets in 2014 and 2015, aligning with the crude oil price collapse, and after the Russia–Ukraine war erupted, crude oil transmitted elevated net RJ spillovers to these markets. In terms of cross-moment spillovers, crude oil RV exerted the strongest spillover effect on the forex and stock market moments in 2020 and 2021, marking the COVID-19 pandemic. Furthermore, the crude oil RS, RK, and RJ exhibited notable spillovers to other market moments during specific periods.

The findings of this study offer valuable insights for policy-makers, investors, and market regulators in terms of managing financial market risk amid economic and geopolitical uncertainty. Given the crucial role of crude oil in volatility transmission across stock and forex markets, targeted policy responses should be tailored to the nature of each crisis. For policy-makers, closely monitoring crude oil price fluctuations is essential, but a more proactive, scenario-based approach is needed to mitigate systemic risk. During health crises such as the COVID-19 pandemic, when RV and jump spillovers are pronounced, exchanges should introduce volatility circuit breakers to prevent extreme price swings and stabilize markets. Conversely, during geopolitical crises such as the Russia–Ukraine war or the Israel–Hamas conflict, when higher-order moments such as realized skewness and kurtosis dominate, multinational financial institutions should develop energy-forex risk hedging tools to help investors manage cross-market exposure. Additionally, central banks could intervene to stabilize currency markets when crude oil-driven spillovers threaten forex stability.

For investors, understanding the crisis-specific dynamics of crude oil spillovers is crucial for effective portfolio risk management. During health crises, when RV and jumps in crude oil prices surge, investors should adopt defensive strategies, such as increasing liquidity buffers and hedging against crude oil price shocks using energy derivatives. In contrast, during geopolitical events, which primarily impact realized skewness and kurtosis, investors may need to adjust portfolio allocations, such as increasing exposure to safe-haven assets or diversifying across asset classes that are less sensitive to crude oil fluctuations. Recognizing the role of crude oil in systemic risk transmission enables investors to develop tailored hedging strategies based on the type of crisis affecting the global markets.

For market regulators, treating crude oil as a systemic risk factor is critical to maintaining financial stability, and regulatory measures should be adapted to different crisis scenarios. For example, during periods of heightened crude oil price volatility, such as the crude oil price collapse of 2014–2015 or the surge following the Russia–Ukraine war, commodity exchanges should implement price bands to curb excessive speculation. In crises in which crude oil-driven spillovers threaten stock and forex market stability, regulators should enforce stress testing for financial institutions with high energy market exposure. Furthermore, increasing transparency in energy market trading activities could help prevent excessive speculation from exacerbating systemic risk.

Given that RV and jump risks in crude oil prices significantly spill over into the forex market, we recommend that regulators dynamically adjust crude oil futures margin requirements in response to forex market conditions. Specifically, during periods of heightened forex volatility, such as currency crises or major geopolitical events, higher margin requirements may be necessary to curb speculative behavior and systemic risk. Conversely, during stable forex conditions, easing margin constraints could enhance market efficiency without introducing undue risk. These measures help ensure that derivative markets remain resilient to cross-market volatility spillovers, maintaining both liquidity and price stability in crude oil futures trading.

Finally, future research could extend this analysis by examining higher-order and cross-moment spillovers across different frequency bands using the TVP-VAR frequency connectedness approach, which would provide a more granular understanding of how spillovers evolve over different time scales, potentially revealing hidden dynamics that are not immediately apparent in aggregate measures. Additionally, leveraging advanced machine learning techniques, such as explainable artificial intelligence (AI), could help identify the key drivers of these spillovers, offering deeper insights into the underlying mechanisms of risk transmission.

Data availability

The data that support the findings of this study are available from Tick Data but restrictions apply to the availability of these data, which were used under licence for the current study, and so are not publicly available. Data are however available from the authors upon reasonable request and with permission of LSEG Data & Analytics.

Notes

The difference \({J}_{t}=R{V}_{t}-B{V}_{t}\) represents the portion of variability due to jumps or sudden price changes. However, due to estimation noise, \(B{V}_{t}\) can sometimes slightly exceed \(R{V}_{t}\), leading to negative \({J}_{t}\) values. Negative values of \({J}_{t}\) have no meaningful interpretation in the context of jump measures because a “jump” cannot have a negative magnitude. To avoid this issue, the realized jump is set to zero whenever \({J}_{t}\) is negative, ensuring nonnegativity. Jumps in financial markets represent abrupt, large price movements caused by market shocks, news, or other unexpected events. These movements cannot logically “reduce” variance, so negative values of \({J}_{t}\) would contradict their real-world meaning. By defining \(R{J}_{t}\) as max (\({J}_{t}\),0), the measure reflects only meaningful, positive contributions of jumps to the total variance.

We provide essential details of the model estimation, following Antonakakis et al. (2020). For a more comprehensive discussion of methodological considerations, we refer readers to the established literature on TVP-VAR frameworks, particularly the foundational works of Primiceri (2005), Lubik and Matthes (2015), Del Negro and Primiceri (2015), and Petrova (2019).

We greatly appreciate the reviewer’s constructive comment, which has opened up new avenues for our research. To save space and highlight the key points of this paper, the parameter estimates and other results of the TVP-SV-VAR model are not reported here.

References

Ahmed R, Bouri E, Hosseini S, Shahzad SJH (2024) Spillover in higher-order moments across carbon and energy markets: a portfolio view. Eur Financ Manag 30(5):2556–2595. https://doi.org/10.1111/eufm.12456

Ahmed WM (2022) On the higher-order moment interdependence of stock and commodity markets: a wavelet coherence analysis. Q Rev Econ Financ 83:135–151. https://doi.org/10.1016/j.qref.2021.11.011

Alomari M, Selmi R, Mensi W, Ko H-U, Kang SH (2024) Dynamic spillovers in higher moments and jumps across ETFs and economic and financial uncertainty factors in the context of successive shocks. Q Rev Econ Financ 93:210–228. https://doi.org/10.1016/j.qref.2023.11.003

Alquist R, Kilian L, Vigfusson RJ (2013) Forecasting the price of oil. Handb Econ Forecast 2:427–507. https://doi.org/10.1016/B978-0-444-53683-9.00008-6

Amaya D, Christoffersen P, Jacobs K, Vasquez A (2015) Does realized skewness predict the cross-section of equity returns? J Financ Econ 118(1):135–167. https://doi.org/10.1016/j.jfineco.2015.07.003

Andersen TG, Bollerslev T (1998) Answering the skeptics: yes, standard volatility models do provide accurate forecasts. Int Econ Rev 39(4):885–905. https://doi.org/10.2307/2527343

Antonakakis N, Chatziantoniou I, Gabauer D (2020) Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions. J Risk Financ Manag 13(4):84. https://doi.org/10.3390/jrfm13040084

Antonakakis N, Kizys R (2015) Dynamic spillovers between commodity and currency markets. Int Rev Financ Anal 41:303–319. https://doi.org/10.1016/j.irfa.2015.05.005

Asadi M, Roubaud D, Tiwari AK (2022) Volatility spillovers amid crude oil, natural gas, coal, stock, and currency markets in the US and China based on time and frequency domain connectedness. Energy Econ 109:105961. https://doi.org/10.1016/j.eneco.2022.105961

Auboin M, Ruta M (2013) The relationship between exchange rates and international trade: a literature review. World Trade Rev 12(3):577–605. https://doi.org/10.1017/S1474745613000025

Awartani B, Maghyereh A, Cherif G (2016b) The connectedness between crude oil and financial markets: evidence from implied volatility indices. J Commod Mark 4(1):56–69. https://doi.org/10.1016/j.jcomm.2016.06.001

Awartani B, Maghyereh A (2016) Dynamic spillovers between oil and stock markets in the Gulf Cooperation Council countries. Energy Econ 56:36–45. https://doi.org/10.1016/j.eneco.2016.02.023

Baele L (2005) Volatility spillover effects in European equity markets. J Financ Quant Anal 40(2):373–401. https://doi.org/10.1017/S0022109000002341

Bai DM, Wei Q, Yan ZH, Zhao XM, Li XG, Xu SM (2003) Fed-batch fermentation of Lactobacillus lactis for hyper-production of l-lactic acid. Biotechnol Lett 25:1833–1835. https://doi.org/10.1023/A:1026276925649

Balcilar M, Gabauer D, Umar Z (2021) Crude Oil futures contracts and commodity markets: new evidence from a TVP-VAR extended joint connectedness approach. Resour Policy 73:102219. https://doi.org/10.1016/j.resourpol.2021.102219

Banerjee AK, Dionisio A, Sensoy A, Goodell JW (2024) Extant linkages between Shanghai crude oil and US energy futures: insights from spillovers of higher-order moments. Energy Econ 107683. https://doi.org/10.1016/j.eneco.2024.107683

Barndorff-Nielsen OE, Shephard N (2004) Power and bipower variation with stochastic volatility and jumps. J Financ Econ 2(1):1–37. https://doi.org/10.1093/jjfinec/nbh001

Barndorff-Nielsen OE, Shephard N (2006) Econometrics of testing for jumps in financial economics using bipower variation. J Financ Econ 4(1):1–30. https://doi.org/10.1093/jjfinec/nbi022

Baruník J, Kočenda E (2019) Total, asymmetric and frequency connectedness between oil and forex markets. Energy J 40(2_suppl):157–174. https://doi.org/10.5547/01956574.40.SI2.jbar