Abstract

This perspective piece addresses several challenges towards enabling gigatonne-scale CCS-based CO2 reductions and removals, including the lack of carbon market cohesiveness, weak price signals, to issues of public perception against engineered-solutions. The article briefly explores future prospects of enhancing CO2 sequestration in the techno-sphere that has the potential to store durably about 2 Gt CO2 per year by 2050 and offers four recommendations for potential derisking of CCS buildouts.

Similar content being viewed by others

Introduction

Achieving net-zero by the mid-century will require the buildout of carbon capture and sequestration (CCS) to enable the abatement of CO2 from emission sources and the enhancement of removal by sinks. Many leading, credible scenarios that chart our transition to net-zero include CCS as a key enabling technology, reaching gigatonne scale within a few decades1,2,3,4, with estimates of at least 6–8 Gt CO2 capture capacity per year by 20505. According to the IEA’s CCS Tracker, in 2023, the total CO2 capture capacity in operation is about 50 Mt, which is two orders of magnitude below what is required by 2050 to be aligned with the Paris Agreement. To a large extent, technology is not the biggest hurdle: CO2 emissions have been captured since the 1930s for use in carbonated drinks and other industrial applications, meanwhile the capture of CO2 from natural gas processing facilities to enhance oil recoveries (EOR) began from the 1970s, and with dedicated geological storages, for example in Norway and Canada, from the year 2000 onwards. The reality is that carbon capture technologies are fairly mature, have a high technology-readiness level (TRL), and can be scaled-up, but they often lack commercial viability.

A study by the consultancy group, McKinsey, estimates that the global investment in CCS has to reach 120 billion USD in annual average between now to 2050 to be aligned with the Paris goal6. However, CCS struggles to attract capital since it is not a traditional investment in the strict business sense given that there are limited revenue potentials from CCS. Deployment of CCS requires large upfront private capital and high operational costs to capture, condition, compress/liquify, transport, store, and monitor/verify CO27, and all of these in a commercial environment where emissions are an externality to private cost. Ensuring CCS is on-track to deliver on its promises for climate change mitigation requires innovation in business models and policy instruments. Trends in climate policy discussions have largely focused on the use of carbon pricing instruments to promote the buildout of CCS7. The generation of carbon credits through emissions reductions or removals can subsequently be traded to meet compliance obligations or voluntary objectives. The problem is, though, the market itself lacks cohesiveness as it is still shaping up, independently, in different geographies to serve different purposes.

CCS in a fragmented carbon market

For a start, there are two types of carbon markets, voluntary and compliance. The major global compliance markets, under a cap-and-trade or emissions trading system, totaled close to 1 trillion USD in 20238, with over 80% attributable to the world’s most valuable carbon market today, the European Union’s Emissions Trading System (EU ETS)8. The voluntary market, where buyers voluntarily purchase and trade in carbon offsets, are estimated to be about 2 billion USD in 20229,10. However, the voluntary markets have been under intense scrutiny given that the CO2 credits are mainly generated through CO2 avoidance projects, which are often criticized as being insufficient to address the climate challenge11,12,13,14.

This adds another layer of complexity to the existing carbon markets. The nature of projects generating CO2 credits can involve either CO2 avoidance, reduction, or removal, each addressing different aspects in the transition to net-zero. An avoidance project (e.g., avoided deforestation) prevents the prospective release of CO2, which is measured relative to a counterfactual world had the avoidance project not intervened. While an avoidance project clearly has value in abating future rises in CO2, it does not necessarily mitigate current sources of emissions nor enhance removal sinks. However, a reduction project (occasionally conflated with an avoidance project) abates existing CO2 sources, for example, through the deployments of CCS in contemporary facilities. While a reduction project realizes emission abatement, which is measurable relative to a historical baseline, it does nothing to enhance the CO2 sink. The enhancement of removal sinks is effectively the realm of CO2 drawdown projects, like afforestation/reforestation and direct capture of CO2 from the atmosphere. Despite the vital differences between credit generation projects, and the different impacts they have on climate change mitigation, the market generally treats 1 tonne of CO2 as 1 tonne of CO211, regardless of how real, measurable, and durable the CO2 captured and sequestered are. The current markets fail to account for the variability in CO2 credits11, whether the CO2 is sequestered for a few decades, centuries, or millennia, and how confident we are in the measurements of the CO2 avoided, reduced, or removed.

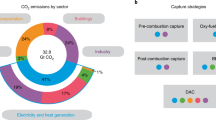

Given its much lower cost, it comes as no surprise, therefore, that the voluntary markets are priced very low, typically below $5/t CO2 for avoidance projects to about $20/t CO2 for nature-based removal projects15,16,17 – both of which are nowhere near a blue-chip, technology-based CO2 reduction or removal cost (Fig. 1). Notably, even the compliance market, like the prized EU ETS, has low CO2 allowance prices, currently ranging between $55–80/t CO2, while breaking the $100/t CO2 barrier only momentarily in 202318. To put this into context, the cost of CO2 capture from concentrated sources, like an ammonia or ethanol plant, is slightly below $50/t CO219,20,21,22. With CO2 concentrations of 50–90%, these are generally the cheapest to capture, but they account for less than 5% of worldwide emissions23. The greatest share of CO2 emissions worldwide, however, are from power generations, petrochemicals and cements, containing a lower CO2 concentration of 5–15%, with a capture cost in the range of $70–150/t CO219,20,21,22. On the other end of the cost spectrum is the capture of CO2 directly from air. Given that the CO2 concentration in air is about 0.04%, the current cost of capture is reportedly much higher, with some estimating it to be in excess of $500/t CO2, but with a potential to be reduced much further24,25,26. With these cost ranges in mind, the prices of CO2 in existing carbon markets are insufficient to attract private capital, therefore it is unsurprising that, to the best of the author’s knowledge, not a single CCS-based CO2 reduction, nor removal, project has been fully financed by the carbon market alone, neither voluntary nor compliance.

Indicative price ranges for different CO2 avoidance, reduction, and removal approaches.

Today, the carbon market is highly fragmented. Further to the supply-side diversity in CO2 credits, demands for offsets are equally varied. On the one hand, countries will increasingly rely on CO2 credits that are correspondingly adjusted to meet pledges made under their nationally determined contributions (NDC). Conversely, demands for offsets are rising to meet corporate climate ambitions, sectoral compliance like CORSIA for the aviation sector, and product CO2 claims, each with their own accounting standards, rules, and guidelines. National, corporate, sectoral, and product CO2 accountings can differ fundamentally in their penchant for incorporating CO2 offsets: some disallowing the use of offsets altogether, others limiting offsets to scopes 1 and 2, while still others also permitting the use of offsets for scope 3 emissions. The development of a harmonized, transparent, and globally fungible carbon market could be key to addressing the confusion arising from an increasingly fragmented market, while minimizing the risks of double-issuance, double-use, and double-claiming. In this case, Article 6 of the Paris Agreement may prove to be a much-needed piece of the puzzle for a collaborative crediting framework that cuts across jurisdictions, either as bilateral agreements (Article 6.2), or the creation of a centralized carbon market for international trading between entities (Article 6.4)27. The cooperative nature of Article 6 could offer a pragmatic and cost-effective approach to decarbonization by enabling entities to do more than what they would have been able to do had they implemented their decarbonization plans independently27.

De-risking CCS buildout

The preceding CCS business model often involves a single entity controlling the capture, transport, and storage of CO2. Although this is expected in the early technology demonstration phase, longer term it could pose a risk to scaling up. The emergence of CCS hubs worldwide is a de-risking strategy with multiple entities partaking in different nodes of the CO2 capture, transport, and storage supply chains. However, it is important to note that existing market pricing instruments often provide incentives at the regulated point of CO2 emissions28, and so the entire CCS value chain, including the business cases for CO2 transport and storage, are solely reliant on the value realizable by the CO2 capturer. There are proposals, however, for addressing cross-chain and market risks, including specific government incentives7,28, the creation of a tradeable CO2-sequestration credit market (known as Carbon Storage Units, CSU)29, a carbon contract for difference (CCfD) regulation to ensure revenue stability30, and innovations in business models7 including CCS-as-a-service offering.

Early estimates suggest that there is a potential to develop over 160 hubs globally, with the capacity to capture and store 4.2 Gt CO2 per year at costs of less than $85/t CO231. As of July 2023, the cumulative CO2 storage capacity in various stages of development exceeds 300 Mt per annum31. As the CCS hubs grow to meet global demands for CO2 storage, the issues of liability associated with pollution export will be even more pressing and need urgent consideration particularly for transboundary projects. In the event of any reversal, either accidental or due to a laxer regulation, there isn’t yet a global consensus on which entity will be liable for the emissions released: whether this contributes to the national CO2 inventory of the capturing or storing country, and how this affects the emissions scope of the capturing and storing company.

Then, there is also the question of public acceptance. The well-documented naturalism bias32,33,34,35 of the public means that there is a general tendency to favor biogenic approaches to CO2 reductions and removals at the expense of engineered solutions. Nature-based approaches allow for direct public participation, offering a sense of being part of the solution and affording greater agency to local communities32. While a more grounded familiarity with ecosystem-based practices breeds confidence in biogenic approaches32,35, the lack of agency and the gap in technical understanding in engineered solutions could bring the issues of trust-deficit in government-industry ties to the fore32. Importantly, this should not be dismissed as NIMBY-ism (Not-In-My-Back-Yard, NIMBY)32, as public acceptance or opposition are not simply a question of proximity or aesthetics, rather it includes a sense of (un-)familiarity with the infrastructure, vulnerability to (un-)known hazards, and (dis-)trust in governing institutions. Thus, public perception could complicate issues of consultation, consent, and compensation arising from siting decisions. This suggests that the social license to operate an engineering-based CO2 reduction and removal technology, no matter how effective, should avoid taking a purely technocratic approach.

Sequestration prospect of the technosphere

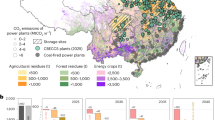

The intensification and extensification of anthropogenic activities since the industrial revolution, whilst directly responsible for humanity’s improved overall quality of life, has also led to the undesirable accumulation of CO2 in the atmosphere. Preventing the net accumulation of CO2, while still providing the energy, food, and material needs of society, will necessitate a careful engineering of the carbon cycle to abate the emissions at the source and enhance the removal by sinks. The natural carbon cycle involves multiple interconnected global spheres: atmosphere, biosphere, geosphere, and hydrosphere. Currently, carbon avoidance, reduction, or removal, whether nature-based or engineered, involves the sequestration of carbon in the bio-, hydro-, or geosphere (Fig. 2). In the case of CCS, whether point source or direct air capture, often this involves underground storage in deep-geological formations. A key, valuable feature of a high-integrity carbon storage is the durability, or permanence, of the CO2 sequestered, which opens a new opportunity to engineer a durable technosphere: sustainable plastics.

The figure depicts the average carbon stocks and anthropogenic flows by the different global spheres between the year 2013 to 2022 (with a reported imbalance of about 0.4 GtC)52 and the CO2 sequestration prospects of the geo- and techno-spheres in 2050.

Today, the world produces over 400 Mt of plastics a year, up from 2 Mt in 1950, and it is projected to grow significantly into the future, exceeding 1000 Mt by 205036,37. Plastic is ubiquitous in our daily lives, with major uses in packaging, building and construction, textiles, and transport applications37. Replacing plastics with commercial alternatives is not easy, and in most cases, it would lead to higher overall life cycle GHG emissions37. Due to their long carbon-carbon bonds, aromatic structure, or presences of functional groups38, plastics are not easily degradable, and therefore plastic wastes tend to linger in the environment for long, posing risks to marine ecosystems and human health. However, the non-degradability of plastics is also what makes it a durable carbon sequester. If all of today’s plastics are produced from captured CO2, they could be storing, durably, the equivalent of more than 1 Gt of CO2 per year38; by 2050, with the projected annual demand of over 1000 Mt, plastics have the potential to store over 2.5 Gt of CO2 per year.

Sequestering captured CO2 as sustainable plastics could be engineered in several ways. The conversion of CO2 into carbon-based building blocks for subsequent plastics manufacturing will require a novel chemical industry, organic chemistry, and a catalytic system to be engineered. Conversely, CO2 can also be converted to syngas, methane, methanol, or dimethyl ether, which can be used as feedstocks for producing the targeted carbon products. Unlocking the potential of CO2 as a building block for the plastics industry requires the integrative developments of green chemistry and green engineering to activate the transformation of a relatively unreactive molecule39. Access to CO2 sources based on a regional environmental merit order must be complemented by a corresponding growth in a low-carbon hydrogen economy to enable CO2 reductions to valuable base chemicals40. Sustainable conversion of CO2, however, requires large quantities of renewable electricity, which is not always accessible everywhere nor consistently available at an affordable cost. The creation of a global transition framework should aim to facilitate the export of low-carbon electricity from renewable-rich regions with high potentials for lower-cost generations, to energy demand centers that are renewable-scarce. This involves the buildout of renewable electricity generation capacity in geographies with high solar and wind generation potentials as well as the developments of cost-effective and efficient means for delivering low-carbon electricity across distances: whether via high-voltage direct currents (HVDC) or using intermediary e-molecules like hydrogen, methane, or methanol.

Cost is an equally important consideration. Given that plastics is ubiquitous in our modern daily lives, including its widespread use in the medical and food industries, an exorbitant green premium associated with carbon sequestered plastics could risk impeding global progress on several of the UN’s SDGs41,42. Although plastics could have significant importance across the 17 SDGs41,42, of particular relevance are SDG 2 and SDG 3, whereby plastics play a vital role in agriculture and the prevention of food wastage37,42, as well as its critical use in the provision of global healthcare41,42. R&D efforts, therefore, must drive the green premium lower to improve the commercial viability of sustainable plastics while increasing its appeal to consumers. While multiple CO2 conversion pathways are ongoing developments, ultimately prioritization should not only consider their costs but also the overall ecological impacts using a life cycle assessment (LCA) approach. Moreover, design for sustainability means following a circular path that incorporates an expanded sustainability function39 going beyond the traditional, narrow focus on material performance, nor on global warming impact alone, to stay within the planetary boundaries.

However, like other sequestration methods, whether the geosphere or biosphere, there is a risk of carbon leakage with the technosphere, too. Globally, only 9% of plastic wastes are recycled, meanwhile about 12% are incinerated43, releasing the captured CO2 from the technosphere to the atmosphere. Significantly, 79% are discarded and lost, either in landfills or the natural environment43. While this does not lead to CO2 leakage to the atmosphere, it does contribute to the overall ecological risks of plastic wastes. Realizing plastics’ CO2 sequestration potential will require the establishment of waste collection and sorting ecosystem, recycling infrastructures, and the engineering of sustainable, self-contained landfills to prevent leakages from the technosphere to other global spheres. For this to happen, there needs to be a clear market signal to incentivize the production buildout of CO2 sequestered plastics in combination with the creation of a sustainable end-of-life plastics ecosystem. Similar to earlier proposals for the creation of a Zero Emissions Credit (ZEC) by the WBCSD, or the Carbon Storage Unit (CSU) credit by Zakkour and Heidug29, perhaps in the not-too-distant future, like-minded entities could consider establishing a credit market for Carbon Sequestered Plastics (CSP), which are awarded for every tonne of CO2-equivalent sustainable plastic recovered at the end of its life. The CSP represents real and measurable tonnes of carbon sequestered as plastics that can be monitored, verified, and transferred to sustainable plastics producers to generate fungible CO2 reduction or removal credits, perhaps under a voluntary or compliance carbon market, or even integrated under the Article 6 framework.

Nevertheless, for a successful roll-out of carbon sequestered plastics, social acceptance is indispensable44. Public and consumer acceptance relate to individual perception of risks and benefits associated with the infrastructure and novel CO2-derived products45. A recent survey in the UK suggests that the public is not yet familiar with the concept of CO2 capture and utilization46. Despite the low-level of self-reported awareness, respondents are willing to express uninformed opinions46, whereby previous studies indicate that this could change with greater exposure to information. This requires a targeted communication strategy that adopts a differentiated approach to addressing the concerns of the general public as well as the local community. Whereas communication that targets the benefit-perception of the technology is more effective for the general public, local communities require information that specifically addresses their perception of risk45. This involves not only factual, transparent, and comprehensive information on health and environmental risks, but also a focus on trust-enhancing measures45.

Towards a gigatonne-scale carbon capture

Engineering the global transition to a sustainable future demands a radical departure in our thinking, from CO2 as waste to CO2 as building blocks. This is a global challenge that will require the engineering of chemical, policy, and behavioral solutions, which, if successful, could offer a real, measurable, and durable sequestration option for captured CO2 - while still delivering the material needs of our carbon-based society. This necessitates the creation of a viable, gigatonne-scale CO2 capture economy to decarbonize existing assets while also delivering CO2 as feedstock. Unleashing the potential of gigatonne-scale carbon capture will require a multitude of enablers, key amongst which include the following.

First, carbon financing has to be redesigned to favor quality over quantity. From the numerous carbon projects, very few are directed towards blue-chip CO2 reductions and removals. Price signals must reflect the durability, reliability, and verifiability of carbon projects. Addressing the fragmented carbon markets due to supply-side diversity and demand-side ambiguity could partly be done through a coherent international framework afforded by Article 6. This means that the international community also needs to work out a consensus on the criteria of acceptable use of CO2 credits for national, sectoral, corporate and product offsets. Equally critical is that these discussions must be informed by scientific evidence and at least in the near-term, are guided by pragmatism as opposed to chasing ideals.

Second, the buildout of CCS projects across geographical borders and national jurisdictions is bound to create friction. While some of the issues of pollution export could partly be resolved with the 2009 amendments to the London Protocol47,48,49, which now enables transboundary CO2 shipments, there still remain other areas requiring consensus building. Lessons learned must be made accessible to other project developers and international negotiators to prevent future untoward incidents, particularly if or when there are unintended reversals due to accidental leakages or a result of operational mismanagement. Article 6.8 of the Paris Agreement on capacity building and technology transfers could provide the underlying framework for sharing of best management practices for upscaling transboundary CCS projects.

Third is the importance of early engagements with the public as part of community education and outreach. Ensuring the social license to operate an engineering-based CO2 reduction and removal technology cannot be a purely technocratic endeavor. Siting decisions could aim to adopt key elements from the international framework on FPIC (free, prior, informed consent)50. Although FPIC was developed mainly to protect indigenous rights for projects involving local communities, the broad framework is still very relevant50, where (a) consent is given voluntarily without coercion, intimidation, or manipulation, (b) consent is sought in advance of project commencement to give sufficient time to the community to consider the proposal, and (c) information provided to inform the local communities are accessible, clear, consistent, accurate, and transparent. Notably, public acceptance is often easier when there is familiarity with the infrastructure, understanding of the potentials and risks, and trust in governing institutions to uphold public interest above all else.

Last but not least, a just and inclusive energy transition could not be achieved without the upskilling, reskilling, and redeployments of talents. The energy workforce today is more skilled than the average workforce globally51. In 2019, the oil supply sector alone employed nearly 8 million workers, comprising 5 million in extraction and production, and 1.4 million each in transport and refining respectively51. In reality, many of the skillsets in the oil and gas industry are transferable to support the energy transition. The scale-up of CCS will require skilled talents in CO2 chemistry, process and mechanical engineering designs, material scientists to ensure pipeline integrity, and geologists for the developments of durable underground storage. Over the years, the oil and gas industry has developed in-depth knowledge and skills in these technical areas as evidenced by many successful executions of large-scale and complex engineering constructions onshore and offshore, including developments of safe, reliable, and efficient distribution networks, as well as upscaling sophisticated chemical conversion processes. Moreover, over three-quarters of existing carbon capture capacity today are operated within an oil and gas facility31, and so there is already a buildup of experiences and expertise within the industry. It is only prudent, therefore, that efforts to upscale CCS should leverage the existing know-how within the industry. This presents a unique opportunity for pioneering oil and gas players to step-up and offer crosscutting CCS leadership while disrupting the sector from within.

Data availability

No datasets were generated or analyzed during the current study.

References

IEA, “Net Zero Roadmap. A global pathway to keep the 1.5degC goal in reach., International Energy Agency, Update. (2023)

Bacilieri, A., Black, R. & Way, R. “Assessing the relative costs of high-CCS and low-CCS pathways to 1.5 degrees,” Oxford Smith School of Enterprise and the Environment | Working Paper No. 23-08, 4 December (2023).

ETC, “Carbon Capture, Utilisation & Storage in the Energy Transition: Vital but Limited,” Energy Transition Commission, (2022).

IPCC, “Ch. 8. Strengthening and implementing the global response,” Intergovernmental Panel on Climate Change, https://doi.org/10.1017/9781009157940.006 (2022).

IEF, “Outlooks Comparison Report,” International Energy Forum, (2024).

McKinsey, “Global Energy Perspective 2023: CCUS outlook,” https://www.mckinsey.com/industries/oil-and-gas/our-insights/global-energy-perspective-2023-ccus-outlook, 24 January (2024).

Fattouh, B., Muslemani, H. & Jewad, R. “Capture Carbon, Capture Value: An Overview of CCS Business Models,” Oxford Institute for Energy Studies, (2024).

Twidale, S. “Global carbon markets value hit record $949 bln last year - LSEG,” Reuters, 12 February 2024. [Online]. Available: https://www.reuters.com/markets/commodities/global-carbon-markets-value-hit-record-949-bln-last-year-lseg-2024-02-12/#:~:text=LONDON%2C%20Feb%2012%20(Reuters),at%20LSEG%20said%20on%20Monday. [Accessed 23 May 2024].

WEF, “Better Carbon Credits on the Horizon? How Article 6 Can Build Trust and What it Means for Business Leaders. Briefing Paper,” World Economic Forum., (2023).

Shell & BCG, “The voluntary carbon market: 2022 insights and trends,” A report by Shell and BCG, (2022).

Boyd, P. W., Bach, L., Holden, R. & Turney, C. Carbon offsets aren’t helping the planet — four ways to fix them. Nature 620, 947–949 (2023).

Lakhani, N. Revealed: top carbon offset projects may not cut planet-heating emissions, The Guardian, pp. https://www.theguardian.com/environment/2023/sep/19/do-carbon-credit-reduce-emissions-greenhouse-gases, 19 September (2023).

Haya, B. K. et al. “Quality Assessment of REDD+ Carbon Credit Projects,” Berkeley Carbon Trading, https://gspp.berkeley.edu/assets/uploads/page/Quality-Assessment-of-REDD+-Carbon-Crediting.pdf (2023).

The Economist. Trees alone will not save the world. The Economist, (2023). 20 November.

S&P Global, “Commodities 2024: Price slump in 2023 clouds outlook for voluntary carbon market,” S&P Global, 5 1 2024. [Online]. Available: https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/energy-transition/010524-price-slump-in-2023-clouds-outlook-for-voluntary-carbon-market. [Accessed 3 6 2024].

Allied Offsets, “Navigating the Future of Carbon Markets through Supply, Demand, and Price Forecasting Scenarios,” Allied Offsets, (2023).

Argus, “Voluntary Carbon Markets. Market Prices, news and analysis. Issue 24-18,” Argus Media Group, 2 May 2024.

EU ETS, “EU Carbon Permits,” Trading Economics, [Online]. Available: https://tradingeconomics.com/commodity/carbon#:~:text=Historically%2C%20EU%20Carbon%20Permits%20reached,on%20June%203%20of%202024. [Accessed 6 3 2024].

Baylin-Stern, A. and Berghout, N. “Is carbon capture too expensive? - Commentary,” Internal Energy Agency (IEA), 17 February 2021. [Online]. Available: https://www.iea.org/commentaries/is-carbon-capture-too-expensive. [Accessed 6 April 2024].

Budinis, S., Krevor, S., Mac Dowell, N., Brandon, N. & Hawkes, A. An assessment of CCS costs, barriers and potential. Energy Strat. Rev. 22, 61–81 (2018).

Sievert, K., Cameron, L. and Carter, A. “Why the Cost of Carbon Capture and Storage Remains Persistently High,” International Institute for Sustainable Development (IISD), (2023).

CBO, “Carbon Capture and Storage in the United States,” Congressional Budget Office, http://www.cbo.gov/publication/59345 (2023).

McKinsey, “The world needs to capture, use, and store gigatons of CO2: Where and how?,” McKinsey & Co., https://www.mckinsey.com/industries/oil-and-gas/our-insights/the-world-needs-to-capture-use-and-store-gigatons-of-co2-where-and-how (2023).

Erans, M. et al. Direct air capture: process technology, techno-economic and socio-political challenges. Energy Environ. Sci. 15, 1360–1405 (2022).

Ozkan, M., Priyadarshi Nayak, S., Ruiz, A. D. & Jiang, W. Current status and pillars of direct air capture technologies. iScience https://doi.org/10.1016/j.isci (2022).

Young, J. et al. The cost of direct air capture and storage can be reduced via strategic deployment but is unlikely to fall below stated cost targets. One Earth 6, 899–917 (2023).

Cook, G., Zakkour, P., Neades, S. & Dixon, T. CCS under Article 6 of the Paris Agreement, Int. J. Greenhouse Gas Control, 134, no. https://doi.org/10.1016/j.ijggc.2024.104110 (2024).

Fattouh, B., Muslemani, H., Maino, A. & Zakkour, P.“The Role of Carbon Markets in Enabling Carbon Capture and Storage (CCS),” Oxford Institute for Energy Studies, (2024).

Zakkour, P. et al. “Carbon storage units and carbon storage obligations: a review of policy approaches,” in 16th International Conference on Greenhouse Gas Control Technologies, GHGT-16, Lyon, France, (2022).

CATF, “Designing Carbon Contracts for Difference,” Clean Air Task Force, (2024).

Global CCS Institute, “GLOBAL STATUS OF CCS 2023. SCALING UP THROUGH 2030,” Global CCS Institute, (2023).

Low, S., Fritz, L., Baum, C. M. & Sovacool, B. K. Public perceptions on carbon removal from focus groups in 22 countries. Nat. Commun. 15, 3453 (2024).

Wolske, K. S., Raimi, K. T., Campbell-Arvai, V. & Hart, P. S. Public support for carbon dioxide removal strategies: The role of tampering with nature perceptions. Clim. Change 152, 345–361 (2019).

Baum, C. M., Fritz, L., Low, S. & Sovacool, B. K. Public perceptions and support of climate intervention technologies across the Global North and Global South. Nat. Commun. 15, 2060 (2024).

Sweet, S. K., Schuldt, J. P., Lehmann, J., Bossio, D. A. & Woolf, D. Perceptions of naturalness predict US public support for Soil Carbon Storage as a climate solution. Clim. Change 166, 22 (2021).

Gabrielli, P. et al. Net-zero emissions chemical industry in a world of limited resources. One Earth 6, 682–704 (2023).

Meng, F., Brandao, M. & Cullen, J. M. Replacing plastics with alternatives is worse for greenhouse gas emissions in most cases. Environ. Sci. Technol. 58, 2716–2727 (2024).

Ryan, A. J. & Rothman, R. H. Engineering chemistry to meet COP26 targets. Nat. Rev. Chem. 6, 1–3 (2022).

Zimmerman, J. B., Anastas, P. T., Erythropel, H. C. & Leitner, W. Designing for a green chemistry future. Science 367, 397–400 (2020).

Huo, J., Wang, Z., Oberschelp, C., Guillen-Gosalbez, G. & Hellweg, S. Net-zero transition of the global chemical industry with CO2-feedstock by 2050: feasible yet challenging. Green. Chem. 25, 415–430 (2023).

de Sousa, F. D. B. The role of plastic concerning the sustainable development goals: The literature point of view, Cleaner and Responsible Consumption, 3, no. https://doi.org/10.1016/j.clrc.2021.100020 (2021).

Kent, R. “The role of plastics in achieving the UN Sustainable Development Goals,” Discussion Paper Prepared by Tangram Technology for the BPF Sustainability Committee 2019, (2019).

Geyer, R,. Jambeck, J. R. & Law, K. L. Production, use, and fate of all plastics ever made, SCIENCE ADVANCES, 1-5,https://doi.org/10.1126/sciadv.1700782 (2017).

Jones, C. R., Olfe-Krautlein, B., Naims, H. & Armstrong, K. The social acceptance of carbon dioxide utilisation: a review and research agenda, Front. Energy Res. 5, https://doi.org/10.3389/fenrg.2017.00011 (2017).

Arning, K., Offerman-van Heek, J., Sternberg, A., Bardow, A. & Ziefle, M. Risk-benefit perceptions and public acceptance of Carbon Capture and Utilization. Environ. Innov. Soc. Transit. 35, 292–308 (2020).

Perdan, S., Jones, C. R. & Azapagic, A. Public awareness and acceptance of carbon capture and utilisation in the UK. Sustain. Prod. Consum. 10, 74–84 (2017).

IEA, “Carbon Capture and Storage and the London Protocol,” International Energy Agency, (2011).

Havercroft, I. & Consoli, C. “Perspective. Developments and Opportunities - A review of national responses to CCS under the London Protocol,” Global CCS Institute, (2022).

Lampert, E. “The London Protocol is key to unlocking international CO2 shipping,” Riviera Maritime Media, 14 September 2023. [Online]. Available: https://www.rivieramm.com/news-content-hub/news-content-hub/the-london-protocol-is-key-to-unlocking-international-co2-shipping-77700. [Accessed 11 June 2024].

UN, “Free Prior and Informed Consent. An indigenous peoples’ right and a good practice for local communities. Manual for project practitioners.,” Food and Agriculture Organization (FAO) of the United Nations (UN), (2016).

IEA, “Skills Development and Inclusivity for Clean Energy Transitions,” International Energy Agency, September (2022).

Friedlingstein, P. et al. Global carbon budget 2023. Earth Syst. Sci. Data 15, 5301–5369 (2023).

Author information

Authors and Affiliations

Contributions

A.A.M. wrote the manuscript and prepared the figures.

Corresponding author

Ethics declarations

Competing interests

The author declares the following financial interests/personal relationships which may be considered aspotential competing interests: Author A. Abdul-Manan is employed by Saudi Aramco.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Abdul-Manan, A.F.N. Enabling gigatonne scale engineering based carbon capture solutions and novel chemical based CO2 sequestrations. npj Clean Energy 1, 4 (2025). https://doi.org/10.1038/s44406-025-00004-6

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s44406-025-00004-6