Abstract

Import restrictions on deforestation-linked commodities have been enacted with the goal of reducing global deforestation and emissions. However, the limited market share of importers imposing such restrictions and the potential for emissions leakage could reduce their effectiveness. Moreover, they could result in negative economic implications for producers and consumers. We quantify future emissions and economic implications of oil palm and soybean import restrictions. Current EU restrictions are likely to have minimal impact due to the EU’s otherwise small and declining share of global palm and soy demand. If extended beyond the EU, import restrictions could lead to reductions in cumulative land use change (LUC) emissions by 2050 in key oil crop exporting regions - up to 1.6% in Indonesia, 2.1% in the rest of Southeast Asia, 4.6% in Argentina, and 8.3% in Brazil compared to a no restrictions scenario. Globally, however, direct forest protection could be more effective than indirect protection through import restrictions due to emissions leakage. Meanwhile, import restrictions could cause major exporters to lose $0.1-$280 billion in cumulative agricultural production revenues by 2050. More broadly, our study highlights that the effectiveness of import restriction policies in reducing global emissions will likely depend on coordinated action across major oil crop producing and consuming regions.

Similar content being viewed by others

Introduction

In accordance with the Paris Agreement goals of limiting warming to below 1.5–2 °C, countries are individually responsible for meeting their nationally determined contributions (NDCs) and long-term strategies. At the same time, each country’s economy is linked to others through international trade. Therefore, trade policies are increasingly being considered as part of emissions reduction strategies1,2. Meanwhile, targets to combat emissions from land-use are gaining traction. The Glasgow Leaders’ Declaration on Forests and Land Use was signed by 145 countries at COP26 in 2021 committing to halt and reverse deforestation and land degradation by 20303. COP28 in 2023 saw countries strengthening this commitment. Nevertheless, halting deforestation has remained a major policy gap towards achieving Paris Agreement goals, with deforestation continuing to increase in recent years4.

The production of globally traded ‘forest-risk commodities’ is the largest driver of tropical deforestation5,6. To combat this, a number of zero-deforestation commitments (ZDCs) have been initiated, ranging from voluntary actions in the private sector (e.g., certification standards and moratoria)7,8 to government-led import restrictions. Import restrictions have been proposed in several countries, like the US9 and UK10, but EU policies have been the most extensive in this regard. As of 2023, the EU’s deforestation regulation prevents imports into the EU of seven commodities produced on post-2020 deforested land: cattle, cocoa, coffee, oil palm, rubber, soy, and wood, as well as products derived from these commodities11. This regulation, initially scheduled to take effect in 2024, has been postponed to 2025–202612. As of 2022, both palm and soybean oil have been designated as high-induced land-use change (ILUC) biofuels, and the EU has set targets to phase out their use by 203013. Oil palm and soybean commodities have the potential to be substituted with other oil crops (particularly for bioenergy), as well as a range of other agricultural crops for use in food, non-food, and animal feed.

However, open questions remain regarding (1) the effectiveness of import-side restrictions in reducing deforestation, and (2) the economic implications of such restrictions for producers and consumers. Private sector initiatives have faced challenges in being effective due to emissions leakage to other commodities or regions, lack of transparency and traceability, and small-scale producer marginalization7,14,15. The EU’s deforestation regulation could face similar issues. Meanwhile, the EU’s deforestation and biofuel regulations have been criticized by exporter countries in the Global South and have been brought forward to the World Trade Organization (WTO) for arbitration on grounds of discrimination16. Exporter countries are concerned that such regulations could have severe economic consequences for producers, particularly small-scale farmers, and will hinder progress on sustainable development goals7,17,18,19. Moreover, exporter countries have raised concerns that deforestation regulations may function as protectionist measures, e.g., favoring EU-grown oil crops (e.g. rapeseed and sunflower oil) over imported oil crops like oil palm and soy18,20.

Several impact assessments of EU’s deforestation regulations21,22,23,24,25 have been conducted (Supplementary Information Table S1). However, these assessments rely on simplified assumptions on commodity demand growth rates and deforestation and LUC emission intensities. Moreover, these assessments do not account for demand changes in other regions, interactions between competing land uses, or the potential for emissions leakage. Meanwhile, several global economic modeling studies26,27,28,29,30,31 (Table S2) have dynamically evaluated the impacts of either palm or soy trade restrictions individually on land-use change and LUC emissions, especially in key export producer regions. Studies have highlighted the potential for local leakage within a region when ZDCs cover a limited area26 and assessed the upper extent to which LUC emissions could be reduced if ZDCs are fully adopted globally26,29 (i.e., no leakage). However, the extent to which global leakage could dilute the effectiveness of import restrictions has not been quantified. Many studies, including those evaluating economic impacts28, have represented palm or soy demand in a historical counterfactual context26,27,28, not accounting for changes in future demands. Therefore, no studies have quantified the future economic implications of import restrictions. More importantly, no studies have explored the role of import restrictions as a potential climate policy mechanism within the context of countries’ emissions reduction commitments. We address these gaps by quantifying the extent to which import restrictions on oil palm and soybean (as currently structured or with potential extensions) could reduce future deforestation and LUC emissions and their broader economic impacts in key oil crop-producing and consuming regions. See Section S1 for additional details.

We develop the capability to model bilateral trade within the Global Change Analysis Model (GCAM), an integrated model representing multiple systems, including socioeconomics, energy, water, land-use, emissions, and climate (Methods). We represent bilateral trade of oil palm and soybean markets globally and explore a series of scenarios representing varying levels of import restrictions on oil palm and soy from deforesting regions through 2050 (Table 1). Our reference scenario (REF) includes no import restrictions and represents a scenario consistent with achieving 2 °C through carbon pricing on fossil fuel and industrial (FFI) carbon emissions but not on LUC emissions. The EU freeze scenario imposes a ceiling on EU imports of oil palm and soy products from deforesting regions at 2020 levels in all future periods, consistent with currently enacted regulations prohibiting imports of commodities linked to post-2020 deforested land11. The HighInc freeze scenario extends these import restrictions to high-income regions, thus representing an extension in which similar high-income countries follow the EU’s lead. Alternatively, the EU/Top 5 freeze scenario represents an extension in which import restrictions are imposed by the EU and the top five net importing GCAM regions for oil palm and soy, respectively, many of which are emerging economies projected to face increased oil crop demands in the coming decades. The EU ban scenario, in which the EU fully bans all imports of oil palm and soy from deforesting regions, represents a potential extension of the EU’s high ILUC biofuel phaseout policy13. Finally, a counterfactual Land protect scenario protects additional forest land in each deforesting region equivalent to land reduced from oil palm and soy production in the HighInc Freeze scenario compared to REF. This scenario enables a comparison of the economic and emissions implications of directly protecting forest land versus indirectly via import restrictions. See Section S2 for additional details.

Results

Production and consumption shifts resulting from import restrictions

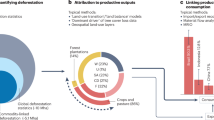

Oil palm and soy have different market characteristics. While oil palm can only be grown in tropical climates, soybeans can grow in both tropical and temperate climates. 57% and 32% of global oil palm in 2015 were produced in Indonesia and the rest of Southeast Asia (RO SEAsia), respectively (Fig. 1), both of which have been undergoing deforestation. Meanwhile, soybean production in 2015 was split largely between Brazil (30%) and Argentina (17%), which have been undergoing deforestation, and the USA (34%), which has not.

Panels A and B present commodity volume flows, in million tonnes primary equivalent, from producers to consumers (both domestic and international), indicated by arrows, for oil palm (A) and soy (B), respectively, in 2015. Panels C and D present projections of production volumes, in million tonnes primary equivalent, in key producers decomposed by destination market (color-filled bars) by scenario for oil palm (C) and soy (D), respectively. For each producing region, the left subpanel shows production in 2015 and 2050 REF, and the right subpanel shows the change in production between import restriction scenarios and REF in 2050. Domestic market volumes are consumed within the indicated producing region. 2030 results are shown in Fig. S4. Data source: GCAM simulations. Note that GCAM uses a 2015 calibration base year.

A key finding from our analysis is that current EU import restriction policies are unlikely to shift oil crop production levels. In the absence of import restrictions (under the REF scenario), the EU experiences smaller increases in soy demand relative to other regions and sees decreases in oil palm demand by 2050 relative to 2020 levels (Table S4). Under the EU freeze scenario, there are negligible changes in oil palm and soybean production. This is because the EU alone makes up a small and diminishing fraction of global palm and soy import demand.

Extensions of import restriction policies, beyond the current implementation, could have larger impacts. Under extended import restriction scenarios (the HighInc freeze, EU/Top 5 freeze, and EU ban scenarios), key deforesting oil crop exporters—Indonesia, RO SEAsia, Brazil, and Argentina—experience declines in oil palm or soy production. Across these extended import restriction scenarios, Indonesia and RO SEAsia face net decreases of 2–6% and 6–13%, respectively, in oil palm production relative to REF in 2050. Brazil and Argentina face net decreases of 5–22% and 3–8%, respectively, in soybean production relative to REF in 2050. Indonesia’s relatively smaller declines in production due to import restrictions are because of the larger share of its production supplied to domestic markets. Brazil’s relatively larger declines in production under the HighInc freeze and EU/Top 5 freeze scenarios are due to the large share of its production that would otherwise be exported to a single import-restricting country, China. In contrast, other major deforesting exporters have a relatively more diversified set of export markets, including markets not enacting import restrictions.

Despite the overall net reductions in total oil palm and soybean production in key deforesting exporting regions, there is some market-switching leakage, as exporters increase exports to unrestricted markets and/or increase domestic consumption. We calculate a market-switching leakage rate for each deforesting producer region (see Box 1). This market-switching leakage rate ranges between 8–13% and 8–13% across extended import restriction scenarios for oil palm in Indonesia and RO SEAsia, respectively, and 10–65% and 17–64% for soy in Brazil and Argentina, respectively in 2050. This leakage rate is particularly high for Brazil and Argentina under the EU ban scenario, as they can divert considerable volumes of soy production to China and the rest of the world. In addition, across scenarios, import-restricting regions also shift to meet some of their demand domestically or from unrestricted exporters. In particular, the USA increases in soy production between 3–5% across extended import restriction scenarios relative to REF in 2050.

Land-use change and emissions implications of import restrictions

In Indonesia, RO SEAsia, Brazil, and Argentina, the EU freeze scenario results in negligible changes in land-use across regions, due to the EU’s small and diminishing market share for oil palm and soy. However, extended import restrictions could reduce deforestation (Fig. 2). In the extended import restrictions scenarios, forest land replaces some of the land used to grow oil palm or soybean crops under REF and, as a result, reduces LUC emissions in these four key exporter regions relative to REF (Fig. 3).

The bars show changes in land-use in 2050 across GCAM regions relative to REF (million Ha) by scenarios (subpanels). 2030 results are shown in Fig. S5.

The maps show cumulative land-use change (LUC) CO2 emissions (2020–2050) across GCAM regions relative to REF (MtCO2) by scenarios (subpanels). % changes in cumulative LUC CO2 emissions (2020–2050) for the key deforesting oil crop-exporting regions (Brazil, Argentina, Indonesia, and RO SEAsia) are indicated in each figure. % changes in cumulative LUC emissions through 2075 and 2100 are shown in Table S5.

However, a majority of the land saved from growing oil palm or soy is allocated to other (i.e. non-forest) land types, including other crops and pasture, representing another key mechanism of emissions leakage. We calculated a land-switching leakage rate for each deforesting producer region (see Box 1). Across extended import restriction scenarios in 2050, this land-switching leakage rate ranges between 94–96% and 77–79% for soy in Argentina and Brazil, respectively, and 55–68% and 20–78% for oil palm in Indonesia and RO SEAsia. Land-switching leakage rates vary widely across regions and basins depending on the alternative economic uses for a given area of land. In addition, other regions also compensate for the import restrictions, e.g., the USA increases land for soy production, and several regions increase land for other crop production. As a result, several regions have less afforestation and, consequently, higher LUC emissions.

A key insight from our study is that oil crop import restrictions might have negligible impacts if imposed by EU alone (due to the EU’s small and diminishing market share) but could achieve larger emissions reductions in key deforesting regions if imposed more broadly (Fig. 3). For example, Brazil achieves 1070 MtCO2 (6.3%) and 1380 MtCO2 (8.3%) reductions in cumulative LUC emissions between 2020–2050 under the HighInc freeze and EU/Top 5 freeze scenarios, respectively, compared to REF. However, globally, impacts across import restriction cases remain small due to emissions leakage. The HighInc freeze and EU/Top 5 freeze cases achieve 712 MtCO2 (0.6%) and 868 MtCO2 (0.8%) reductions in global cumulative LUC emissions between 2020–2050.

As a point of comparison, we show LUC and LUC emissions implications in our Land protect scenario. This direct forest protection scenario achieves larger reductions in cumulative LUC emissions (2430 MtCO2 or 2.2%) compared to all import restriction scenarios globally, and in most cases in the key deforesting export regions. Directly protecting forest land is more effective than indirect protection via import restrictions because land-switching leakage rates under import restriction scenarios are high.

Economic implications of import restrictions

Major oil crop exporters subject to import restrictions (Brazil, Argentina, Indonesia, and RO SEAsia) may experience losses in oil crop production revenue, mediated only slightly by substitution to producing other agricultural commodities (Fig. 4). Under the EU freeze scenario, Brazil, Argentina, and Indonesia experience relatively small losses of $27 billion, $4 billion, and $0.1 billion (in 2020$) in cumulative primary agricultural production revenue relative to REF from 2020–2050, while RO SEAsia does not experience losses. These small impacts are observed, consistent with minimal changes in oil palm and soy production in the EU freeze scenario. Under extended import restrictions, Brazil, Argentina, Indonesia, and RO SEAsia experience relatively larger losses of $89–280 billion, $23–67 billion, $19–59 billion, and $24–43 billion, respectively, in cumulative primary agricultural production revenue relative to REF from 2020–2050.

In Table S6, we calculate a price (per ton-CO2) that, applied to LUC emissions, would result in equivalent values to the level of agricultural revenue lost in each of these key deforesting oil crop-exporting regions under extended import restrictions. This price ranges from $201-$782 per ton-CO2 across key export regions and scenarios. These prices give an indication of the level of redistribution that would be needed to counteract inequities among producers resulting from extended import restrictions. Across regions, Brazil has the lowest price values, implying that there is higher “policy efficiency” of import restrictions in achieving LUC emissions reductions in Brazil than in other key exporting regions.

Meanwhile, substitute producer regions like the USA and import regions like the EU, China, and India receive increases in production revenue (in at least some extended import restriction scenarios) as they substitute oil crop production (oil palm, soy, or rapeseed or sunflower crops), or other crops more generally. EU oil crop producers receive increases in cumulative oil crop production revenue between $26–151 billion as a result of import restrictions.

However, importers also face increases in cumulative total primary agricultural expenditures relative to REF from 2020–2050. For example, the EU faces increases of $175 billion under the EU ban, while China and India face increases of $210–220 billion and $143 billion, respectively, when they are part of the set of regions enacting import restrictions. Such increases in primary agricultural expenditures could hurt consumers and cause food security concerns, particularly in low to lower-middle-income regions. These results highlight why low to lower-middle income regions, like India, which are major consumers of imported oil crops, are unlikely to follow EU’s suit in imposing import restrictions, and therefore why the EU/Top 5 freeze scenario could be considered a less plausible extension than the HighInc freeze scenario. In contrast to import restriction scenarios, the direct Land Protect scenario has minimal economic impact changes relative to REF (see Section S2.3 for additional discussion on Land Protect).

Discussion

In this study, we assess how multiple mechanisms of emissions leakage across the agricultural production supply chain could dilute the effectiveness of import restriction policies, thus lowering their LUC emissions reductions. When faced with trade restrictions on their products, producers could instead sell commodities in non-restricted markets (to other international importers or in domestic markets). Meanwhile, the production of oil crops or other substitute crops could spill over to other regions. Only a fraction of the land saved from crop production may be forested, as producers can switch to other agricultural commodities entirely (those not covered under import restrictions), or allocate lands to other uses (which could have lower land carbon than forests). We find that leakage at the end stages of the supply chain, i.e., leakage of oil palm or soy production to other markets, is lower than at the early stages of the supply chain, i.e., leakage of land allocation to other crops or uses entirely. This is reflected in the fact that land-switching leakage rates are higher than market-switching leakage rates across key deforesting producing regions.

Our results highlight that currently enacted deforestation regulations in the EU alone have a minimal impact on global oil palm or soy trade flows, land-use changes, emissions, or economic impacts. Yet, our results highlight that even if the EU were to fully ban imports of oil palm and soy across all producers within countries undergoing deforestation, as in the EU ban case, the impact on reducing global LUC emissions would still be minimal. This is because the EU alone represents a small and diminishing share of global demand for oil palm and soy commodities. Nevertheless, the EU’s deforestation regulations could play an important role in setting global standards for other regions to follow. Additionally, these policies can enable a more level-playing field for companies pursuing sustainable production practices32.

If extended beyond the EU, import restrictions could still have a limited impact in reducing LUC emissions globally, due to the multiple mechanisms of leakage. However, these broader import restrictions could drive larger impacts in a few key deforestation-prone export regions, especially Brazil. LUC emissions reductions in these exporting regions could be particularly important, given the large share of LUC emissions in these countries’ overall total GHG emissions33. LUC emissions reductions could free up emissions in other difficult-to-abate sectors or those requiring negative emissions technologies, helping these countries achieve their near and longer-term emission reduction goals33. Meanwhile, in regions like the USA, which could face increased soybean production and lowered carbon sinks due to broader import restrictions, additional mitigation efforts may be needed in other sectors to compensate. As shown in our results, the effectiveness of import restrictions in reducing LUC emissions in key regions will likely rely on a substantial fraction of the market share imposing such restrictions. More broadly, the effectiveness of such policies in reducing emissions globally will likely depend on coordinated action across major oil-crop producing and consuming regions21 and across sectors.

Our study also highlights the negative economic impacts on exporting regions in the Global South resulting from import restrictions, raising concerns about equity. Declines in production revenue could exacerbate the vulnerabilities that small-scale oil crop producers in these regions already face. Furthermore, our study captures oil palm or soybean producers’ full economic responses to switch to other commodities or markets, inherently assuming producers would have access to market information, when in reality, producers (particularly small-scale farmers) often lack awareness about their market options7. Negative economic impacts in key exporter regions could be worse than shown here and could concentrate on small-scale producers. Our results validate protectionism concerns voiced by exporters from the Global South, in that oil crop producers in the EU could benefit from import restrictions and receive higher production revenues. Importers like the EU or China may face increases in agricultural revenue as a result of import bans, while the U.S. may benefit as a substitute soybean exporter whose supply chains are not linked to deforestation. More broadly, inequitable import restrictions, which exacerbate current global inequities between Global North and Global South regions, could undermine international relations and hinder climate mitigation progress.

To avoid negative economic impacts faced by exporters in deforestation-prone regions, additional or alternative land-use policies and/or financing are needed. Alternative policies, as exemplified by our Land Protect scenario could be more effective and economically efficient, while not exacerbating global inequities between countries. This could include REDD+ schemes and agricultural intensification programs. Previous research has highlighted the effectiveness of moratoria (i.e., sector-wide sanctions on the conversion of specific forest lands) alongside improved local governance in reducing deforestation7. Additional financing for forest conservation, such as the “Tropical Forests Forever” fund announced by Brazil at COP28, could be an important mechanism for ensuring the economic livelihoods of people who live in and protect tropical forests34. Further cooperation is needed, between exporting regions concerned about negative economic impacts on their producers and importing regions seeking to limit their indirect deforestation impact, to help incentivize forest protection and avoid negative economic impacts for oil crop producers.

The capabilities developed for this study could be extended to track bilateral trade of additional commodities, e.g., all seven commodities covered by the EU’s recent deforestation regulation. The estimated impacts of import restrictions could be larger when accounting for these commodities. Beyond deforestation and LUC emissions, import restrictions could have consequences on other planetary boundaries35 (e.g., local water scarcity). This is an important area for future work.

Methods

Global change analysis model

The global change analysis model is open-source and available at https://github.com/JGCRI/gcam-core. GCAM is a global, integrated multi-sectoral model that links together socioeconomic, energy, land, water, and climate sectors. The version of the model used here is based on GCAM 7, calibrated to a 2015 base year. 2015 is the latest 5-year timestep for which comprehensive data across all of GCAM’s systems is currently available (in the format used for model input), hence it is used as the current base year. GCAM solves for commodity prices in 5-year time steps such that supply and demand are in equilibrium in all energy, agriculture, and water markets. GCAM has been used for several decades in major studies assessing global climate mitigation policy progress36, alternative land protection policies37, and impacts of global trade38.

In GCAM, the world is disaggregated into 32 economic regions, the resolution at which socioeconomic and trade processes are modeled. The world is also disaggregated into 235 large water basins, the resolution at which water supply-demand balances are met. The intersection of economic regions and large water basins forms 384 land-use regions, the resolution at which land-use allocations are modeled. In GCAM, Malaysia is contained within the rest of the Southeast Asia region (referred to in the paper as RO SEAsia). Indonesia is represented as a standalone GCAM region.

Land allocation

Land is allocated to commercial and non-commercial (unmanaged) uses of pasture, forest, grass and shrub, and crops based on a nested logit sharing model of the relative profitability of land for different competing uses. Logit parameters govern land-switching between different land uses, with a higher degree of switching possible for similar land types (e.g., between different crops, than between crop and forest land). In GCAM 7, a portion of land (around 30% of natural land globally) is prohibited from switching land uses based on regional unsuitability or land conservation39. Land allocation parameters are consistent with ref. 40, which were updated and are consistent with the broader literature.

Land-use change emissions

Land-use change (LUC) CO2 emissions are tracked by accounting for changes in vegetation and soil stocks resulting from changes in land-use across time periods. Vegetation and soil carbon densities are specified explicitly for each GCAM land-use region, processed from global gridded data39. LUC emissions in GCAM do not account for changes in agricultural or land management practices.

Agricultural trade

GCAM accounts for the production of crop and livestock commodities aggregated from FAOSTAT data41,42 (see Table S3). A primary equivalent approach was employed to aggregate commodities along the supply chain, ensuring balances across supply-utilization, space, time, and vertical processing sectors. For instance, oil palm and soybean products are represented in palm fruit equivalent and soybean equivalent, respectively. This approach establishes physically traceable connections from land-use to nutrient accounts, forming the basis for calibrating the GCAM base year. Regions can consume agricultural commodities from domestic or traded sources. For this study, we implemented a logit-based Armington bilateral trade framework (Fig. S1) within GCAM to track the source and destination of oil palm and soybean products. All other agricultural crops are modeled with an Armington global pool trade approach, in which each region consumes agricultural commodities from a mix of domestic and imported supplies (imported from a single global market)43. Both bilateral trade (for oil palm and soybean products) and gross trade (for all other agricultural commodities) are calibrated to FAO data in 2015. Bilateral trade flows between two regions in the base year imply that bilateral trade flows can continue between these regions in future periods, except for when specific trade flows are restricted by our import restrictions.

Agricultural demand

Agricultural commodities are demanded in several sectors (see Figs. S8–S11), including food (staples and non-staples), non-food, animal feed (which is linked as an input to livestock sectors), and bioenergy (which is linked as an input to energy sectors). Demand substitution is governed by a set of logit parameters44. In this study, we allow for increased flexibility of substitution in food and non-food demand sectors.

Scenario design

Our baseline REF scenario is consistent with limiting warming to 2 °C by 2100. This scenario includes emission constraints on FFI emissions for each GCAM region, consistent with “NDC++” pathways in ref. 45. Further, we included a global bioenergy constraint, limiting first and second-generation bioenergy to less than 33.4 EJ in 2020, increasing linearly to 58.4 EJ in 2050 (100 EJ in 2100). We include no emission constraints or carbon prices on land sectors. We use SSP2 socioeconomic assumptions.

We modeled the import restriction scenarios by including import constraints between source and destination markets for oil palm and soybean trade. Restricted export markets were defined as regions deforesting between 2015–2050 in the REF scenario (see Fig. S3).

We modeled the Land Protect scenario by calculating the reduction in oil palm or soybean land in each deforesting (export-restricted) region under the HighInc freeze scenario. This value was added to forest land value in the REF scenario in each region to form a set of explicit land protection constraints for each deforesting region from 2025 to 2050.

Leakage rate calculations

We calculate rates of leakage occurring for each key deforesting oil crop producing region in early (land-switching leakage) and end (market-switching) stages of the supply chain. In the paper results, leakage rates are calculated for the year 2050.

Market-switching leakage

The market-switching leakage rate represents the extent to which reductions in oil crop (oil palm or soybean) production in deforesting regions due to import restrictions are offset by increases in oil crop production for other destination markets. For an oil crop producing region, \(p\), the total “net” oil crop supply change, \(\triangle {Q}_{p,s}^{{{{Net}}}}\), between a scenario (\(s\)) and the REF scenario can be calculated as the sum of changes in the bilateral supply flows (\({Q}_{p,r,s}\)) across all the bilateral destinations (\(r\)), see Eq. (1).

When only accounting for the destinations that imposing import restrictions, the total “gross” oil crop supply change, \(\triangle {Q}_{p,s}^{{Gross}}\), is calculated in Eq. (2):

whereas the indicator function, \(I(\cdot )\), takes the value of 1 if \({Q}_{p,r,s}-{Q}_{p,r,{{{{\mathrm{REF}}}}}} < 0\) and 0 otherwise. Thus, the market-switching leakage rate, \({\gamma }_{p,s}^{{{{Market}}}-{{{switching}}}}\), for deforesting oil crop producer region p, under scenario \(s\), can be calculated as:

Most of the trade reduction due to import restrictions is absorbed by other destinations if \({\gamma }_{p,s}^{{{{Market}}}-{{{switching}}}}\) is closer to 100%, and most of the trade reduction is absorbed by production if \({\gamma }_{p,s}^{{{{{Market}}}}-{{{{switching}}}}}\) is closer to 0%.

Land-switching leakage

The land-switching leakage rate represents the extent to which reductions in oil crop (oil palm or soybean) land allocation in deforesting regions due to import restrictions are substituted with non-forest land allocation in the same region. The land-switching leakage rate for deforesting producer regions, under scenario \(s\), can be calculated as:

Whereas \({L}_{p,s}^{{{{Forest}}}}\) and \({L}_{p,s}^{{{{Oil}}\; {{crop}}}}\) represent the land allocation in region \(p\) and scenario \(s\) for forest and oil crop, respectively. When \({\gamma }_{p,s}^{{{{Land}}}-{{{switching}}}}\) is closer to 100%, reductions in oil crop land are absorbed by other (non-forest) land uses. When \({\gamma }_{p,s}^{{{{Land}}}-{{{switching}}}}\) is closer to 0%, reductions in oil crop land encourages higher afforestation.

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

The model output data were available at Zenodo (https://doi.org/10.5281/zenodo.10849930). The figures presented in the paper can be generated using the workflow at https://github.com/brinday/oilcrop-trade-deforestation-leakage (https://doi.org/10.5281/zenodo.14679830)46. Maps were generated using the open-source “rmap” R package47.

Code availability

GCAM is an open-source community model available at https://github.com/JGCRI/gcam-core/releases. The version of GCAM and additional input files associated with this study are available at https://doi.org/10.5281/zenodo.10840364.

References

Burney, J., Costello, C., Davidson, M. R., Li, H. ‘Harry’ & Rauch, J. E. The Role of Trade in Addressing Climate Change: Recommendations for Policies and Practices. https://ccd.ucsd.edu/_files/2021-report_role-of-trade-in-addressing-climate-change.pdf (2021).

Clora, F., Yu, W. & Corong, E. Alternative carbon border adjustment mechanisms in the European Union and international responses: aggregate and within-coalition results. Energy Policy 174, 113454 (2023).

Glasgow Leaders’ Declaration on Forests and Land Use - UN Climate Change Conference (COP26) at the SEC – Glasgow 2021. The National Archives https://webarchive.nationalarchives.gov.uk/ukgwa/20230418175226/https://ukcop26.org/glasgow-leaders-declaration-on-forests-and-land-use/ (2021).

Iyer, G. et al. Taking stock of nationally determined contributions: continued ratcheting of ambition is critical to limit global warming to 1.5 °C. One Earth 6, 1089–1092 (2023).

Curtis, P. G., Slay, C. M., Harris, N. L., Tyukavina, A. & Hansen, M. C. Classifying drivers of global forest loss. Science 361, 1108–1111 (2018).

Pendrill, F. et al. Agricultural and forestry trade drives large share of tropical deforestation emissions. Glob. Environ. Change 56, 1–10 (2019).

Lambin, E. F. et al. The role of supply-chain initiatives in reducing deforestation. Nat. Clim. Change 8, 109–116 (2018).

Gibbs, H. K. et al. Brazil’s soy moratorium. Science 347, 377–378 (2015).

Sen. Schatz, S B. [D-H]. S.2950 - 117th Congress (2021–2022): FOREST Act of 2021. (2021).

McGrath, M. Climate change: New UK law to curb deforestation in supply chains. BBC (2020).

European Parliament. European Parliament legislative resolution of 19 April 2023 on the proposal for a regulation of the European Parliament and of the Council on making available on the Union market as well as export from the Union of certain commodities and products associated with deforestation and forest degradation and repealing Regulation (EU) No 995/2010 (COM(2021)0706 – C9-0430/2021 – 2021/0366(COD)). https://www.europarl.europa.eu/doceo/document/TA-9-2023-0109_EN.html (2023).

Access2Markets. Application of EUDR Regulation on deforestation-free products delayed until December 2025. https://trade.ec.europa.eu/access-to-markets/en/news/application-eudr-regulation-deforestation-free-products-delayed-until-december-2025 (2024).

European Union. Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources (recast). Official J. Eur Union L328, 82–209 (2018).

DeFries, R. S., Fanzo, J., Mondal, P., Remans, R. & Wood, S. A. Is voluntary certification of tropical agricultural commodities achieving sustainability goals for small-scale producers? A review of the evidence. Environ. Res. Lett. 12, 033001 (2017).

Driving sustainable palm oil in Europe: 5 takeaways from #SPOD2020. Roundtable on Sustainable Palm Oil (RSPO) https://rspo.org/driving-sustainable-palm-oil-in-europe-5-takeaways-from-spod2020/ (2020).

Joint Letter on European Union Proposal for a Regulation on Deforestation-free Products Submission by Indonesia and Brazil to Committee on Agriculture. World Trade Organization (2022).

Marques da Silva, I. Why the Global South is against the EU’s anti-deforestation law. euronews (2023).

Mano, A. Brazil official defends progress on protecting forests, blasts EU ban. Reuters (2023).

Indonesia accuses EU of ‘regulatory imperialism’ with deforestation law. The Straits Times (2023).

Nangoy, F. Indonesia reviewing terms of EU trade deal as WTO palm oil spat brews: vice foreign minister. Reuters (2019).

Bougas, K. et al. Service Contract on EU Policy on Forest Products and Deforestation Task 3 - Impact Assessment on Demand-Side Measures to Address Deforestation. https://circabc.europa.eu/ui/group/34861680-e799-4d7c-bbad-da83c45da458/library/5d098237-8bab-48a6-a6c8-2a907d80c791/details?download=true (2023).

IDH. The Urgency of Action to Tackle Tropical Deforestation: Protecting Forests and Fostering Sustainable Agriculture. https://www.idhsustainabletrade.com/uploaded/2020/02/IDH_The-UoA-to-Tackle-Tropical-Deforestation_2020-web.pdf (2020).

Heflich, A. An EU Legal Framework to Halt and Reverse EU-Driven Global Deforestation: European Added Value Assessment. (Publications Office, LU, 2020).

COWI. Feasibility Study on Options to Step up EU Action against Deforestation: PART I, Background Analysis, Scale and Trends of Global Deforestation and Assessment of EU Contribution and PART II, a Potential EU Initiative on Deforestation, Possible Interventions. https://data.europa.eu/doi/10.2779/97793 (2018).

Cuypers, D. et al. The Impact of EU Consumption on Deforestation (2013).

Villoria, N., Garrett, R., Gollnow, F. & Carlson, K. Leakage does not fully offset soy supply-chain efforts to reduce deforestation in Brazil. Nat. Commun. 13, 5476 (2022).

Busch, J. et al. Effects of demand-side restrictions on high-deforestation palm oil in Europe on deforestation and emissions in Indonesia. Environ. Res. Lett. 17, 014035 (2022).

Taheripour, F., Hertel, T. W. & Ramankutty, N. Market-mediated responses confound policies to limit deforestation from oil palm expansion in Malaysia and Indonesia. Proc. Natl Acad. Sci. USA 116, 19193–19199 (2019).

Leijten, F., Baldos, U. L. C., Johnson, J. A., Sim, S. & Verburg, P. H. Projecting global oil palm expansion under zero-deforestation commitments: Direct and indirect land use change impacts. iScience 26, 106971 (2023).

Delzeit, R., Heimann, T., Schünemann, F. & Söder, M. Who Benefits Really from Phasing out Palmoil-Based Biodiesel in the EU? (Kiel Institute for the World Economy, 2021).

Valin, H. et al. The land use change impact of biofuels consumed in the EU. (2015).

Commission Staff Working Document Executive Summary of the Impact Assessment Report minimising the risk of deforestation and forest degradation associated with products placed on the EU market. (2021).

Soterroni, A. C. et al. Nature-based solutions are critical for putting Brazil on track towards net-zero emissions by 2050. Glob. Change Biol. https://doi.org/10.1111/gcb.16984 (2023).

Paraguassu, L. Brazil proposes global forest conservation fund at COP28. Reuters (2023).

Richardson, K. et al. Earth beyond six of nine planetary boundaries. Sci. Adv. 9, eadh2458 (2023).

Ou, Y. et al. Can updated climate pledges limit warming well below 2 °C? Science 374, 693–695 (2021).

Calvin, K. et al. Trade-offs of different land and bioenergy policies on the path to achieving climate targets. Clim. Change 123, 691–704 (2014).

Graham, N. T. et al. Agricultural market integration preserves future global water resources. One Earth 6, 1235–1245 (2023).

Narayan, K., Vernon, C., Vittorio, A. D. & Margiotta, E. JGCRI/moirai: Moirai v3.1.1. Zenodo https://doi.org/10.5281/zenodo.6632745 (2022).

Zhao, X., Mignone, B. K., Wise, M. A. & McJeon, H. C. Trade-offs in land-based carbon removal measures under 1.5 °C and 2 °C futures. Nat. Commun. 15, 2297 (2024).

Food and Agriculture Organization of the United Nations. Guidelines for the Compilation of Food Balance Sheets. https://www.fao.org/3/ca6404en/ca6404en.pdf (2017).

Zhao, X. et al. gcamfaostat: an R package to prepare, process, and synthesize FAOSTAT data for global agroeconomic and multisector dynamic modeling. J. Open Source Softw. 9, 6388 (2024).

Zhao, X. et al. The impact of agricultural trade approaches on global economic modeling. Glob. Environ. Change 73, 102413 (2022).

Edmonds, J., Link, R., Waldhoff, S. & Cui, R. A global food demand model for the assessment of complex human-earth systems. Clim. Change Econ. 8, 1–22 (2017).

Iyer, G. et al. Ratcheting of climate pledges needed to limit peak global warming. Nat. Clim. Change 12, 1129–1135 (2022).

Yarlagadda, B. brinday/oilcrop-trade-deforestation-leakage: v1.0. Zenodo https://doi.org/10.5281/zenodo.14679830 (2025).

Khan, Z., Zhao, M., Vernon, C. R., Wild, T. & Yarlagadda, B. rmap: an R package to plot and compare tabular data on customizable maps across scenarios and time. J. Open Source Softw. 7, 4015 (2022).

Acknowledgements

This material is based upon work supported by the National Science Foundation under Grant 1855982. Any opinions, findings, conclusions, or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the National Science Foundation. We thank Maridee Weber for their valuable feedback on the study.

Author information

Authors and Affiliations

Contributions

T.W. and J.L. acquired funding for the project. B.Y., X.Z., and G.I. designed the research. X.Z. and B.Y. developed the modeling and analysis tools. B.Y. conducted the simulations, analyzed the results, and wrote the first draft of the paper. X.Z., G.I., T.W., N.H., and J.L. contributed to the interpretation of the results and the writing of the paper.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Communications thanks the anonymous reviewers for their contribution to the peer review of this work. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Yarlagadda, B., Zhao, X., Iyer, G. et al. Emissions leakage and economic losses may undermine deforestation-linked oil crop import restrictions. Nat Commun 16, 1520 (2025). https://doi.org/10.1038/s41467-025-56693-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s41467-025-56693-1