Abstract

The phenomenon of stock price crash events (SPCs) has always attracted market attention, but existing research mainly focuses on its causes or determinants and rarely examines the consequences of SPCs. This study aims to fill this gap by examining the consequences of firm-specific stock price crash events (SPCs) on analyst forecast accuracy. Using the sample of analysts and listed companies from 2001 to 2020 and employing a difference-in-differences design, we find that after the company’s stock price crashed, the analyst forecast error decreased and the accuracy increased. For analysts who have not conducted site visits before SPC, and have no geographical advantages, this effect is more obvious, thus validating our hypothesis following analyst attention theory. Additional analysis shows that SPCs stimulate forecast accuracy more significantly for lowly-reputed analysts than for highly-reputed analysts. Channel analysis documents that, for the aforementioned group of analysts, the enhancement effect of SPCs on analyst forecasts is mediated by analyst effort increasing. This study adds to the evidence that SPCs bring positive externalities from the analyst perspective, that is, SPCs attract the attention of some analysts and improve their forecast accuracy. This study also enhances our understanding of analyst behavior under uncertainty, finally enriching the literature on the determinants of analyst forecast accuracy.

Similar content being viewed by others

Introduction

Stock price jumps and stock price crashes are an important phenomenon in the capital market. Stock price jumps will enable investors to obtain high returns, but they will also accumulate wealth bubbles in the capital market. The consequences of SPCs will not only shake investors’ confidence in the capital market but also cause misallocation of resources in the real economy question. There are many reasons for the collapse of a company’s stock price. In recent years, a large number of studies on the causes of SPCs have emerged. SPCs have become a hot topic among academics and regulators. Although there is an enormous amount of literature exploring the causes or determinants of SPCs, papers examining the consequences of SPCs are still rare.Footnote 1The only published paper on the consequences of SPCs is Kim et al. (2022) who document that SPCs could trigger investor rational attention and thus stimulate market information efficiency. But beyond this, nothing is known as yet about the consequences of SPCs on other economic agents’ behavior. To fulfill this gap, this study examines how analyst forecasts are affected by firm-specific stock price crashes (SPCs). Because analysts are deemed as information intermediaries who provide investment advice and enhance market efficiency by interpreting, digging, and disseminating information, their forecasts are especially more important under high uncertainty (Amiram et al. 2018). Therefore, it is self-evident that how SPCs influence analyst forecasts is meaningful for market participants.

Following prior literature, we postulate two competing predictions on the relationship between SPCs and analyst forecast accuracy. On the one hand, SPCs may improve analyst forecast accuracy by attracting analysts’ attention which is beneficial for the information environment. A firm’s SPC is a rare event of stock price collapse (Kim et al. 2022). Extreme fluctuation in stock price can trigger analysts’ attention which is a limited resource for improving the firm’s information environment (Bourveau et al. 2022). As improved information environment is beneficial for analysts to enhance forecast accuracy (Lang et al. 2003), it is reasonable to expect that SPCs may enhance analyst forecast accuracy. On the other hand, the collusion view predicts a negative relationship between SPCs and analyst forecast accuracy. SPCs send negative signals of corporate governance to the market. In order to raise share price and maintain the company’s image, company executives would try to lobby analysts to make optimistic forecasts. Analysts may be willing to collude with company executives for the sake of maintaining good relations with company executives and obtaining better access to private information (Hu et al. 2021; El Ghoul et al. 2023). Thus, the collusion view suggests that SPCs may deteriorate analyst forecast accuracy. Which effect will dominate depends on how analysts choose between pandering to management or pandering to investors. Thus, it is essential to empirically evaluate the effects of SPCs on analyst forecasts.

We conduct our empirical analysis using a large sample of listed companies in China during the period from 2001 to 2020. Our identification strategy builds on Kim et al. (2022) by evaluating the treatment effect by means of a difference-in-difference (DID) analysis. In particular, we first identify SPC events as firm-specific weekly returns fall more than 3.20 standard deviations below the mean for the 12-month estimation period (Kim et al. 2011a, 2011b). Next, we use the propensity score matching method to match these SPC firms to non-SPC firms with similar SPC-score in the same industry and period. Then, we set the month of each SPC as the baseline point (T = 0) and evaluate analyst forecasts accuracy changes in a 1-year window surrounding the SPC from pre-SPC period (i.e. 6 months previous to the SPC (T = −6)) to post-SPC period (i.e. 6 months after the SPC (T = + 6)). Specifically, we contrast changes in analyst forecast accuracy from pre- to post- SPC period for SPC observations in the treatment sample versus non-SPC observations in the matched sample.

Our DID analysis shows that analyst forecast accuracy for the treatment group of SPC firms increases significantly for the post-SPC period compared with the control group of non-SPC firms. This finding is robust to a series of tests including parallel trend tests, placebo tests, instrumental variable tests, and alternative measure of forecast accuracy. These results are consistent with analyst attention view, suggesting that SPCs prompt analyst forecast accuracy.

We then implement a series of validation tests to reinforce our argument. We test the analyst attention hypothesis from on-the-spot investigations and geographical proximity. Consistent with our expectation, we find that forecast accuracy increases more pronounced for these two types of analysts with information disadvantage, reinforcing that SPCs improve analyst attention and thus enhance forecast accuracy.

Our additional analysis documents the moderate effect of analyst reputation on the relationship between SPCs and analyst forecast accuracy. Star analysts are more concerned about their reputation (Jackson, 2005). To prevent reputational damage, they would pay more attention to their forecast reports, and thus make more accurate pre-SPCs predictions. Consistent with our expectation, we find that the enhancement effect of SPCs on forecast accuracy is less pronounced for star analysts than for non-star analysts.

Further, we conduct channel analysis to examine the mechanism through which the enhancement effect of SPCs on forecast accuracy functions. SPCs are accompanied by a sudden release of the firm’s accumulated bad news. As the firm’s hidden bad news is disclosed, the ability and impartiality of analysts who are not aware of the bad news beforehand would be doubted by investors. Consequently, these analysts would make greater efforts to preserve their image (He et al. 2020). To verify this argument, we focus on analyst efforts as specific types of behavior that analysts may conduct. Our evidence suggests that analysts at a disadvantage in information work harder after SPCs, but the effect is not significant for analysts at an advantage in information. Therefore, our results suggest that SPCs improve analyst forecast accuracy by influencing the behavior of analysts in disadvantage in information, especially by increasing their efforts.

This study makes three major contributions to prior literature. First, to our knowledge, it is the first to examine the consequences of SPCs on analysts’ behavior. Although the detrimental effects of SPCs on shareholder wealth and investor confidence are well-known, Kim et al. (2022) first reveal positive externalities of SPCs on investor attention. Our study supplements evidence of SPCs’ positive externalities from analysts’ perspective. We find that this positive externality of SPCs is particularly significant for analysts who have not conducted on-the-spot investigations before SPC, do not have geographical proximity, and are not star analysts.

Second, our study enhances our understanding of analyst behavior under uncertainty. Because analyst reports provide valuable information for market participants to make investment decisions, the role of analysts is even more important in an uncertain environment (Amiram et al. 2018). Our study helps to understand analysts’ reactions to SPCs which are extreme collapses in stock price. Through channel analysis, we find that some analysts become more diligent in obtaining private information when face with sudden events such as SPCs. This is driven by analyst reputation.

Third, we enrich knowledge of determinants of analyst forecasts accuracy. We find that analyst attention is also one of the factors affecting analyst forecast accuracy. Analyst forecast accuracy is the premise and foundation for analysts to play the role of governance. Career concern (Lourie, 2019), irrationality (Song et al. 2009), and culture (Pacelli, 2019) are documented as influences on forecast accuracy. Our results verify SPCs as a new driver of analyst forecasts accuracy, thus also provide new insight into circumstances under which analyst trade off reputation and collusion incentives.

Figure 1 is the roadmap of this article. Section 2 discusses the literature review and hypotheses. Section 3 discusses the research design and variable measurement. Sections 4, 5, 6, and 7 present the empirical research results, including main regression analysis, validation analysis, additional analysis and channel analysis. Section 8 is the discussion, and Section 9 is the conclusion.

Section 1 is the induction. Section 2 discusses the literature review and hypotheses. Section 3 discusses the research design. Sections 4, 5, 6, and 7 present the empirical research results. Section 8 is the discussion, and Section 9 is the conclusion.

Literature review and hypothesis development

Literature review

Despite the determinants of firm-specific SPCs have been extensively discussed (e.g. Jin and Myers, 2006; Hutton et al. 2009; Kim et al. 2011a; Fang et al. 2021), the consequences of SPCs have only recently begun to be discussed in literature. According to the differences in research object and research design, the literature on the consequences of SPCs could be divided into two categories. One category refers to the literature on the consequences of firm-specific SPCs risk (An and Zhang, 2013; Harper et al. 2020; Lee, 2022; Benkraiem et al. 2023). The research object in this body of literature is SPCs risk, which means the degree of “crash-prone” of a stock and measured as a negative coefficient of skewness, down-to-up volatility, and indicator of SPCs.Footnote 2 The research design of this kind of literature depends on a regression model in which explanatory variables including SPCs risk variables and control variables are one-year lagged to the explained variables. Collectively, this strand of literature aims to reveal one-year lagged consequences of firm-specific degree of “crash-prone”.

The other category of literature focuses on the consequences of SPCs events. The only published study in this category is Kim et al. (2022), in which the research object is the event itself rather than the likelihood of the event. Instead of establishing a regression model with one-year lagged SPCs risk measures as explanatory variables of interest, Kim et al. (2022) identify SPCs events and then conduct a DID analysis to evaluate consequences of the SPCs events. This methodology could reveal the immediate consequences of SPCs events within a specific time span. In particular, Kim et al. (2022) evaluate the consequences of SPCs events on market information efficiency within six months. Therefore, this category of literature focuses on SPCs events and is more flexible in capturing consequences of SPCs within a specific time span. As the consequences of SPCs within a short time span (e.g., less than one year) are undoubtedly important for investors and regulators, follow-up studies of Kim et al. (2022) are urgently needed.

As information intermediaries in the financial market, analysts provide investors with investment decision-making references by interpreting market information and publishing research reports. As a key dimension in evaluating analysts’ professional capabilities, earnings forecasts have a huge impact on analysts’ careers. At the same time, analysts pursue higher forecast accuracy because of career considerations (Lourie, 2019).

Analysts’ forecast accuracy is closely related to the company’s information environment. On the one hand, the quantity and quality of a company’s public information directly affects the accuracy of analysts’ forecasts. For example, the higher the company’s disclosure transparency (Dhaliwal et al. 2012), the higher the audit quality (Xie et al. 2012), the higher the readability of the annual report (Lehavy et al. 2011), etc., the more accurate analysts’ forecasts will be. On the other hand, media reports (Kim et al. 2017), the opening of high-speed rail (Kong et al. (2020), and analysts’ on-the-spot investigations (Cheng et al. 2016) have improved the ability and quality of analysts to obtain information, making analysts’ predictions more accurate.

At the same time, there is a large amount of literature showing that analysts are not completely rational in forecasting and there are biases in earnings forecasts. For example, Ke and Yu (2006) find that analysts tend to use biased earnings forecasts to satisfy company management needs; Pacelli (2019) found that analysts employed by companies with weak cultures produce lower-quality forecast reports for their retail investors; Song et al (2009) find that when a company’s earnings uncertainty is low, analysts have a higher incentive to issue herding forecasts, etc.

When SPCs occur, whether analysts can still make accurate predictions has become an urgent practical issue that needs to be solved. Therefore, our study fills this gap by examining the effects of SPCs on analyst forecasts accuracy.

Hypothesis development

Stock price crashes and analyst forecast accuracy

According to prior literature, it is reasonable to expect two competing predictions on the relationship between SPCs and analyst forecasts accuracy. On the one hand, analyst attention theory predicts a stimulating effect of SPCs on analyst forecasts accuracy. In particular, firm-specific SPC is a rare event of stock price collapse (Kim et al. 2022). Analysts’ attention which is a limited resource for improving the firm’s information environment tends to be allocated to firms whose share prices experience extreme fluctuation recently (Bourveau et al. 2022). Thus, it is straightforward that analysts would pay more attention to firms with recent SPCs, leading to improvement of the firm’s information environment. As improved information environment facilitate analysts forecasting (Lang et al. 2003), firm-specific SPCs may stimulate analyst forecasts accuracy with respect to that firm. Given these considerations, we postulate Hypothesis 1A as below:

Hypothesis 1A: Firm-specific SPCs stimulate analyst forecast accuracy with respect to the firm.

On the other hand, analyst collusion view predicts a deteriorating effect of SPCs on analyst forecasts accuracy. This is because SPCs are widely regarded as negative signals of the firm’s corporate governance (e.g., Bauer et al. 2021; Deng et al. 2020; Guan et al. forthcoming). On behalf of raising share price and preserving the company’s market image, company executives may seek help from analysts to make optimistic forecasts. Analysts may take delight in colluding with company executives for the sake of maintaining good relations with company executives and obtaining better access to private information (Hu et al. 2021; El Ghoul et al. 2023). Thus, following analyst collusion view, it is reasonable that firm-specific SPCs deteriorate analyst forecasts accuracy. Given these considerations, we formulate the following Hypothesis 1B as below:

Hypothesis 1B: Firm-specific SPCs deteriorate analyst forecast accuracy with respect to the firm.

Overall, both the analyst attention theory and analyst collusion theory may play a role in driving changes in analyst forecast accuracy. Which effect will dominate depends on how analysts choose between pandering to management or pandering to investors. Thus, the ultimate effect is an open empirical matter that depends on how analysts facing firm-specific SPCs balance these two competing incentives.

Stock price crashes and analyst forecast accuracy: The role of analyst site visits

Analyst site visit is an important way for analysts to directly face the management of listed companies, understand the actual situation of production and operation of listed companies, such as the implementation of major asset restructuring and the latest information, and obtain information sources of listed companies (Cheng et al. 2016; Han et al. 2018). At the same time, analyst site visits can also avoid the lag of public information (Cao et al. 2023). That is to say, analyst site visits can help analysts obtain information by observing business operations, and to a certain extent alleviate the non-local Analysts’ information disadvantages, thereby improving forecast accuracy. Therefore, if SPCs stimulate analyst forecast accuracy (as analyst attention theory predicts), we expect that analysts who have conducted site visits before SPC will be able to make accurate forecasts by their information advantages before SPC; while analysts without site visits will be able to make accurate forecasts only after the information environment improves after SPC. The prediction accuracy improvement of the former before and after SPC is not as good as that of the latter. Thus, we propose hypothesis 2 as follows:

Hypothesis 2: (As analyst attention theory predicts,) firm-specific stock price crashes stimulate forecast accuracy of analysts who have not conducted site visits.

Stock price crashes and analyst forecast accuracy: The role of geographical proximity

From previous research, we find that the distance between the geographical location of securities companies and listed companies or target companies has also become one of the judgment factors that affect the accuracy of analysts’ forecasts (Comiran and Siriviriyakul, 2019; Koenig, 2016). This is mainly because the cost of obtaining private information will have a great impact due to the closeness and distance at the geographical level (Comiran and Siriviriyakul, 2019). For companies that are relatively close, the cost for securities analysts to obtain private information will be significantly reduced, the communication with all parties in the company will be smoother, and the speed of obtaining information will be faster, which naturally has a positive effect on the accuracy of predictions. Therefore, if SPCs stimulate analyst forecast accuracy (as analyst attention theory predicts), analysts with geographical advantages can also make more accurate forecasts before SPC, while analysts without geographical advantages can only wait until the information environment improves. The prediction accuracy improvement of the former before and after SPC is not as good as that of the latter (Table 1). Given these considerations, we put forward Hypothesis 3:

Hypothesis 3: (As analyst attention theory predicts,) firm-specific stock price crashes stimulate forecast accuracy of analysts without geographical advantages.Footnote 3

Research design and variable measurement

Identification strategy and sample construction

We use the China Stock Market and Accounting Research (CSMAR) database to collect data on financial analysts and firm financial information. We remove observations of financial firms, public utility firms, firms with special treatment or particular transfer, and those with missing data. Our sample period spans from 2001 to 2020 for several reasons. First, the year 2001 is known as the “Year of Supervision” in the history of A-shares market. Since then, regulators have cracked down on financial fraud. Thus, our sample begins from 2001 to exclude structure change around 2001. Second, this time period covers 20 years, which is conducive to obtaining robust research results.

We first identify SPCs of all companies during this period. Following Kim et al. (2022), we define a SPC event as taking place when weekly firm-specific returns fall below a threshold level. Specifically, we calculate weekly firm-specific returns using the time-series regression shown below:

where rjt is the return of stock j in week t, rmt is the market return in week t in a given year. We include the lead and lag terms for the market index return to allow for nonsynchronous trading (Dimson, 1979). The firm-specific weekly return for firm j in week t (denoted as wjt) is calculated with the residuals from Eq. (2) as follows:

Following prior literature (e.g. Kim et al. 2011a, Kim et al. 2011b, Kim et al. 2022), we define a SPC as taking place when wjt falls 3.20 standard deviations below the firm’s mean over the estimation period.Footnote 4We obtain 2781 SPCs during our sample period. These SPCs observations are defined as treatment observations.

Then we apply the propensity score matching (PSM) method to match each of the treatment firms to an industry-peer firm which has the nearest-neighbor distribution of matching variables and does not experience SPC in the year. Following Kim et al. (2022), our matching variables are lagged one-year and include DTURN, which is defined as detrended average monthly stock turnover; NCSKEW, which is defined as negative skewness of firm-specific weekly returns; RETLAG, which is defined as the mean of firm-specific weekly returns; SIGMA, which is defined as the standard deviation of firm-specific weekly returns; SALESG, which is defined as sales growth rate; AGE; which is defined as the natural logarithm of the number of years the company has been listed; TANG, which is defined as asset tangibility; SIZE, which is defined as firm size. These variables are chosen based on their relevance and significance in the existing literature. For example, Chen et al. (2001) find that increasing trading volume and positive past returns can be used to predict negative skewness. Boyer et al. (2010) point out that firm characteristics such as firm size and idiosyncratic volatility are also important predictors of future idiosyncratic skewness. Conrad et al (2014) find that young and fast-growing firms with fewer tangible assets may experience extremely high returns.

Table 2 presents the PSM matching results using logistic regression. Columns 1 and 2 show the estimated results of the logistic regression on propensity score. The dependent variable is a dummy variable CRASH, which is set to 1 when a SPC occurs and 0 otherwise. The signs of the regressor variables are consistent with prior literature (e.g. Kim et al. 2011a; Fang et al. 2021). We use the nearest neighbor method to match firms with SPC with non-SPC firms on a one-to-one basis based on the propensity score. Columns 3 and 4 in Table 2 present the mean values of the matching variables of the treatment firms and the control firms, respectively. Column 5 in Table 2 shows the T-test for the mean difference between the treatment firms and the control firms. The mean of matching variables does not have significant differences between them. Thus, the treatment and control firms in the study are comparable in terms of their probability of experiencing SPCs and are subject to similar unidentified industry and temporal factors, with the only distinction being the treatment received by the intervention group. Our initial matched sample includes 2127 treatment firms and 2127 control firms.Footnote 5

We use a DID analysis as our primary identification approach to investigate if and how SPCs affect analyst forecast accuracy. For each treatment firm in the matched sample above, we identify the month when SPC occurs as our baseline point (t = 0), analyst forecasts are analyzed within a 1-year timeframe that includes the month of occurrence of SPC as the midpoint. The window spans from 6 months before occurrence of SPC (t = −6) to 6 months after occurrence of SPC (t = +6). For the control firm, we choose the same window period around its matching treatment company to observe changes in analyst forecasts. Finally, we obtain 56837 firm-month-analyst observations covering 2127 treatment firms and 2127 control firms from 2001 to 2020.

Model specification

We compare changes in analyst forecast accuracy from pre- to post-SPC for the treatment versus control sample in a one-year window surrounding the SPC month from 6 months before the SPC (t = −6) to 6 months after the SPC (t = +6). This comparison allows us to examine if there are any differences in analyst forecast accuracy. Specifically, we construct the following regression model to examine the effect of SPCs on analyst forecast accuracy:

where CRASH is a dummy variable that is equal to 1 if the firm belongs to the treatment group, and 0 otherwise. POST is a dummy variable that is equal to 1 during the post-SPC period (t = 0, +1, +2, +3, +4, +5, +6) of treatment firms and equal to 0 for the pre-SPC period (t = −1, −2, −3, −4, −5, −6). In the case of matched control firms, this variable is equal to 1 if it is the hypothetical post-SPC period (t = 0, +1, +2, +3, +4, +5, +6) that coincides with the actual post-SPC period of the matched SPC firms, and 0 if it is the pseudo pre-SPC period (t = −1, −2, −3, −4, −5, −6). The interaction of CRASH × POST is our main variable of interest. We expect α3 < 0, that is analysts will improve the forecast accuracy for firms that have an SPC compared to those that do not. δijt is the random error term. Controls refer to control variables discussed below.

Variable measurement

Drawing on Liu and Liu (2022), we define analyst forecast accuracy as the deviation of the earnings forecast for firm j in year T.

where \({{FEPS}}_{i,j,T}\) is earnings per share forecasts provided by analyst i for firm j for year T. \({{AEPS}}_{j,T}\) is the real earnings per share of firm i in year T. On the one hand, in order to prevent negative earnings in a specific year, this will lead to changes in the calculation of analyst forecast errors. On the other hand, when stock prices fall, analysts may face greater pressure to publish more optimistic earnings, causing price-scale forecast error to mechanically rise. Therefore, we choose \(\left|{{AEPS}}_{j,T}\right|\) as the denominator. A higher value of \({{Ferror}}_{i,j,T}\) means analyst forecast is less accurate.

A number of controls are included in our model at the analyst, firm, and audit levels. We first control for a number of variables that may influence the accuracy of analyst forecasts, such as analyst experience (EXP); months separating the release of actual year-end earnings from the time of the analyst forecast (HORIZON); the total number of years analysts track companies (SPECIFIC); the total number of firms an analyst follows in a given year (TFOLLOWING); an indicator of analyst team (TEAM); the number of analysts employed by a brokerage business in a given year. (BSIZE).

Our firm-level controls include firm size (SIZE); returns on assets (ROA); the book value of all liabilities divided by total assets (LEV); log value of board size (LNBOARD); proportion of independent directors (INDENP); shareholding ratio of the firm’s largest shareholder (SHRCR); shareholding ratio of institutional investors (INST); an indicator of state-owned enterprise (SOE).

Audit level controls include audit fees (AUDITFEE); an indicator of the presence of a board audit committee (COMMITTEE); an indicator of the Big 4 audit firm (BIG4).

Descriptive statistics

Panel A of Table 3 shows descriptive statistics. The mean value of FERROR is 0.552, the median is 0.160, the 25th percentile is 0.053, and the 75th percentile is 0.479, which shows that the accuracy of analysts’ earnings forecasts for different listed companies is quite different, and it also shows that most analysts’ forecasts are less accurate. Panel B of Table 3 presents the correlation matrix of the key variables. The data structure of the remaining control variables is within a reasonable range, which is relatively close to the prior research on the stock market in China (e.g. He et al. 2020).

Empirical results

Main results

The estimated results of SPCs on analyst forecasts accuracy are shown in Table 4. The coefficient of CRASH*POST is significantly negative at the 1% level (coef. = −0.186, t-stat = −4.471). This result reveals that the improvement in analyst forecasts accuracy in the post-SPC period is significantly larger for SPC firms than non-SPC firms. It is consistent with hypothesis H1a suggesting that SPCs improve analyst forecasts accuracy.

In terms of control variables, the coefficients of ROA and INST are significantly negative, indicating that analysts forecasts errors will reduce when analysts predict companies with high returns on assets or large institutional shareholding ratios. Furthermore, there is a positive correlation between forecast horizon (HORIZON) and forecast error, but the number of analysts hired by a brokerage firm (BSIZE) and the analyst team (TEAM) are negatively correlated with analyst forecast error.

Robustness test

Parallel trends analysis

In order to further support our DID method, we conduct a parallel trend test. Figure 2 shows the results of the parallel trend test. The abscissa is from d_6 (t = −6) to d6 (t = 6), corresponding to the above-mentioned SPC year estimated period. The endpoints of the line segments on the vertical axis represent the estimated coefficients of FERROR corresponding to each time point, and the length of the line segments represents the confidence intervals at the corresponding 90% confidence levels. If the confidence interval of the dummy variable includes 0, it means that the coefficient of the dummy variable is not significant; otherwise, it is significant. The sixth period before the SPC happens is eliminated because we utilize the base period as the benchmark group to avoid collinearity. The results in Fig. 2 show that all the monthly dummy variable coefficients are not significant in the first 5 months of the SPC, implying that there is no significant difference in the analyst forecast accuracy between the treatment group and the control group before the SPC, and the parallel trend hypothesis is established. In the month when the SPC occurs and after the SPC, the coefficient of each dummy variable is less than 0, indicating that the occurrence of SPC makes the analyst’s forecast more accurate. Thus, the results of parallel trends analysis support the appropriateness of our DID approach.

The terminal points of the vertical line segments indicate the estimated coefficients of FERROR for each time point, while the length of these segments reflects the confidence intervals at the respective 90% confidence levels. If the confidence interval of the dummy variable includes 0, the coefficient is insignificant; otherwise, it is significant.

Alternative measurements of analyst forecast accuracy

We adopt a different metric for analyst forecast accuracy following Francis et al. (2019) to evaluate the robustness of our main results. The alternative measure designated is calculated as follows:

The numerator is still the absolute value of the difference between the analyst forecast earnings per share and the actual earnings per share, and the denominator P is the opening stock price in the estimation period. This measurement can alleviate the impact of stock style differences. Stocks in high-growth industries (i.e. growth style stocks) often have higher price-earnings ratios. Thus, for the same AEPS, companies with higher growth potential often have higher stock prices. Meanwhile, higher growth potential relates to greater volatility in AEPS, making it more difficult for analysts to predict. Therefore, \(|{{FEPS}}_{i,j,T}-{{AEPS}}_{j,T}|\) is interfered by stock style, making it unreasonably biased towards growth-style stocks. By using P as a scaling, this impact is alleviated. As a result, stock price is also a widely used scaling variable in calculating analyst forecast errors. As shown in Table 5, the FERROR_P coefficient is significantly negative at the 5% level (coef. = −0.002, t-stat = −2.433). Therefore, consistent with H1a, our results still hold when we use the opening stock price as a proxy scaling variable, suggesting that SPC improves analyst forecasts accuracy.

Instrumental variable approach

We also used two-stage least-squares instrumental variables (2SLS) to address potential endogeneity, which also provides further evidence for the causality of our main results. Following Kim et al. (2022), we use mutual fund flow redemption pressure based on its hypothetical sales (MFHS) as an instrumental variable. Edmans et al. (2012) suggest measuring a stock’s hypothetical sales by mutual funds that experience outflows of at least 5% of the fund’s total assets. MFHS is a measure of mutual fund flow pressure that could trigger stock price collapse but is unrelated to firm fundamentals, and is often employed as an exogenous shock of stock price movement (e.g. Edmans et al. 2012; Kim et al. 2022). As analyst forecasts are focused on firm fundamentals, it is intuitive to expect that MFHS is correlated to SPCs but is unlikely to influence analyst forecast accuracy.

Panel A of Table 6 shows the first stage results of our 2SLS approach. Consistent with our expectations, the coefficient of CRASH*POST is positive and significant at the 5% level (coef. = 0.002, z-stat = 1.976), indicating that mutual fund redemption pressure is positively related to SPCs. Panel B is the second stage results of the 2SLS approach. We first generate the fitted value of CRASH in the first stage, and then introduce the fitted CRASH into our main regression model Eq. (3) and re-estimate it. We find that the coefficient of the fitted CRASH*POST is negative and significant at the 5% level (coef. = −0.874, t-stat = −1.967). Consistent with H1a, these findings suggest that SPCs driven exogenously by redeemed mutual fund stress drive the increase in analyst forecast precision, further supporting the causality of our main findings.

Placebo tests

Additionally, we conduct placebo tests to rule out the possibility that our findings were due to contemporaneous unobserved factors. We create two fictitious SPCs incidence times. First, we conduct a placebo test to compare the changes in analyst forecast accuracy within one year before the occurrence of SPCs. The fictitious SPCs occurred 6 months before the actual SPCs occurred (T = −6) and the time window spans from 12 months before the occurrence of SPCs (T = −12) to the month of the occurrence of SPCs (T = 0). Second, we set the fictional SPCs incidence time as six months after the actual SPCs (T = 6). The corresponding time window spans from the month of the occurrence of SPCs (T = 0) to 12 months after the occurrence of SPCs (T = 12). We conduct these placebo tests using the same groups of treatment and control firms to ensure comparability. To confirm that our main results are caused by SPCs and not by other contemporary unobserved factors, we compare the changes in analyst forecast accuracy for treatment and control firms before and after these two fictitious SPCs. If SPCs are the driving force, we should not see significant changes in analyst forecast accuracy in the placebo tests.

Table 7 shows that the test period in column 1 is one year after the actual occurrence of SPC (T = 0 to T = 12), and the test period in column 2 is the year before the actual occurrence of SPC (T = −12 to T = 0), the CRASH*POST coefficients in column 1 and 2 are not significant. This falsification analysis further confirms our inference.

Validation analysis

If SPCs increase analyst forecast accuracy by stimulating analyst attention, we expect that forecast accuracy should increase more pronounced after SPCs for analysts at a disadvantage in information. It is reasonable because that, analyst selectively reduces her attention to companies on which she has information disadvantages (Bourveau et al. 2022). Thus, if SPCs function as stimulating analyst attention, the change of analyst attention from pre-SPCs to post-SPCs should be more significant for analysts with information disadvantage, resulting in a more pronounced enhancement effect of SPCs on analyst accuracy. Therefore, we selected on-the-spot investigation (Cheng et al. 2016) and geographical proximity (O’Brien and Tan, 2015), two variables that can affect analysts’ information acquisition, to test the analyst attention hypothesis.

As discussed in Section 2, the underlying notion of the positive relationship between SPCs and analyst forecast accuracy depends on analysts striving for information environment improvement. If this notion is true, it is expected that analysts with information disadvantages improve the accuracy of their forecasts much more than those with information advantages. Next, we conduct several validation analyses to reinforce this underlying notion, including site visits and geographical proximity.

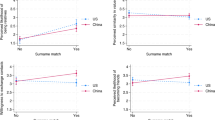

Existing studies have found that analysts can communicate and interact with management through on-the-spot investigations, making them obtain company-specific information and improve the quality of earnings forecasts (Cheng et al. 2016). We divide the sample (including treatment group and control group samples) into “visit” group and “non-visit” group based on whether the analyst conducts on-the-spot investigations on listed companies within 6 months before the release of forecasts before SPC. Analysts in the “visit” group can communicate and interact with management through on-the-spot investigations, making them obtain company-specific information and improve the quality of earnings forecasts (Cheng et al. 2016). The “visit” group contains 5574 observations, and the “non-visit” group contains 51263 observations. We expect the positive relationship between SPCs and analyst forecasts accuracy to be more pronounced for the group without on-the-spot investigation. The empirical results are shown in Columns 1 and 2 in Table 8. Consistent with our expectation of Hypothesis 2, the coefficient of CRASH*POST is only significantly negative for the group without on-the-spot investigation.

Prior literature documents that geographical proximity decreases the cost of analyst gathering information on listed companies (O’Brien and Tan, 2015). Thus, if analysts and listed companies are located in the same province, the geographical advantage will help reduce the cost of analyzing and obtaining information on listed companies, because it is easier for them to obtain company information. They can obtain private information faster and more easily recognize the true situation of the company, which will help improve the accuracy of forecasts. Thus, we divide the sample (including treatment group and control group samples) into “local” group and “non-local” group based on whether the registered place of the listed company and the registered place of the brokerage are in the same province. We expect that SPCs stimulate analyst forecasts accuracy more pronounced for the “local” group. The “local” group contains 4412 observations, and the “non-local” contains 52425 observations. The empirical results are exhibited in Columns 3 and 4 in Table 8. Consistent with our expectation of Hypothesis 3, the coefficient of CRASH*POST is only significant for the group of analysts and listed companies located in different provinces.

Above all, consistent with Hypothesis 2 and 3, our empirical results demonstrate that the improvement effects of SPCs on analyst forecast accuracy only exist in the group of analysts who did not conduct on-the-spot investigations prior to SPC, and do not have geographic advantages. These results reinforce the underlying notion that the effects of SPCs on analyst forecasts accuracy are rooted in analysts striving for information environment improvement.

Additional analysis: Analyst reputation

As mentioned above, we find that SPCs can attract the attention of some analysts, thereby enabling analysts to improve the information environment and improve forecast accuracy. In other words, there are some analysts who can pay attention to companies with SPC risks and make accurate predictions before SPC. Therefore, we further explore the reasons why this type of analysts are not significantly affected by SPCs. Professional reputation has long been recognized as an effective disciplinary mechanism in the labor market (Fama, 1980). Analysts’ focus on reputation drives them to provide higher-quality and less optimistic forecasts. Among them, star analysts pay more attention to their own reputation. To protect their reputation, they tend to have more accurate predictions (Jackson, 2005). Star analysts rely on stronger private information mining capabilities, such as on-the-spot investigations, telephone interviews, etc., as well as their more thorough interpretation of information, and motivation of maintaining reputation, they are more likely to identify hidden dangers in the company before the company’s SPC occurs, and make accurate predictions. Therefore, star analysts are more motivated and capable of making accurate predictions before SPC, while ordinary analysts can only wait until the information environment improves. We expect that the prediction accuracy improvement of the former before and after SPC is not as good as that of the latter.

Zhang et al. (2015) believe that the most outstanding analysts in China are rated as star analysts by “New Fortune” magazine, and the ranking represents the analyst’s reputation in the market. We define star analysts based on whether the analyst is ranked among the top 5 analysts by Fortune magazine in a given year. We divide our sample (including treatment group and control group samples) into “star” group and “non-star” group based on whether analyst forecasts are made by star analysts, the “star” group contains 3863 observations, and the “non-star” group contains 52974 observations. As mentioned above, reputation drives analysts in the “star” group to make more accurate predictions before the SPC, while analysts in “non-star” group can only wait until the SPC occurs before they can take action. We expect that the positive relationship between SPCs and analyst forecast accuracy is more pronounced for the group of non-star analysts. The empirical results are shown in Columns 1 and 2 in Table 9. Consistent with our expectation, the coefficient of CRASH*POST is only significant for the group of non-star analysts.

Channel analysis: Analyst efforts

Next, we further examine the mechanism of the enhanced effect of SPC on prediction accuracy. The abilities of analysts who fail to spot the firm’s hoarding bad news that leads to SPC will be questioned by investors who experience wealth losses. Thus, analysts are motivated to improve their forecasts since they want to repair their reputations. As a result, we anticipate SPCs will make analysts put up more effort to obtain private information for making accurate earnings forecasts. To test this mechanism, we focus on analyst effort.

Following Altschuler et al. (2015), we use the amount of private information in analyst forecasts to measure analysts’ efforts to obtain private information. In particular, it is measured as follows:

where Vi,T is the variance of all analysts’ forecasts on company i; Ni,T is the total number of analysts’ forecasts who follow the company i; Ei,T is the squared error of the consensus average forecast. In order to avoid the skewness problem that may exist in the measurement of private information acquisition, we follow Park et al. (2017) to take the logarithm of the aforementioned private information acquisition index to obtain \({{PRIVACY}}_{i,T}\).The larger value of \({{PRIVACY}}_{i,T}\) means the more private information the analyst obtains.

We divide our sample into two groups based on whether analysts have information advantages before SPCs. We use the same method as in Section 5 to distinguish analysts with information advantages and disadvantages. In particular, we divide our sample based on whether analysts have conducted on-the-spot investigations before SPCs, have geographical advantages, and are star analysts, respectively. If SPCs could make analysts pay more effort to obtain private information for improving earnings forecast, there should be a more pronounced positive relationship between SPCs and \({{PRIVACY}}_{i,T}\) for the sub-samples of analysts with information disadvantages.

We regress \({{PRIVACY}}_{i,T}\) for each group on explanatory variables as in Eq. (3). Table 10 shows our split-sample results. The coefficients in the sub-samples of analysts with information disadvantage are all positive and more significant than those in the sub-samples of analysts with information disadvantage. In particular, the coefficients of CRASH*POST in the subsamples of analysts who do not conduct on-the-spot investigations, analysts without geographic advantage, and non-star analysts are all positive and significant at 1% level, whereas the corresponding coefficients in the subsamples of analysts with geographic advantage and star analysts are not significant. Meanwhile, the corresponding coefficient in the subsample of analysts who conduct on-the-spot investigations is just significant at the 5% level. Overall, our empirical results demonstrate that when analysts have an information disadvantage, they will make greater efforts to obtain private information after SPC to improve forecast accuracy.

Discussion

This study explores the impact of SPCs on analyst forecast accuracy. Empirical research results show that analyst forecast accuracy increases after the occurrence of SPCs, especially for the analysts with information disadvantages. Our empirical evidence also verifies that this effect stems from the fact that SPCs stimulate analyst attention. Channel analysis finds that the enhancement effect of SPCs on analyst forecasts is mediated by analyst effort.

By applying analyst attention to explain the impact of SPCs on analyst forecast accuracy, this paper improves our understanding of analysts’ reactions and subsequent behavior in uncertain information environments. We argue that changes in analyst forecast accuracy are affected by an improvement in attracting analysts’ attention caused by SPCs. It is worth noting that SPCs do not attract the attention of all analysts. SPCs only benefit analysts who do not conduct on-site investigations before SPCs, have no geographical advantages, and are non-star analysts. Because these analysts do not have sufficient information before SPCs, they have greater incentives to pay more attention to improving their forecasts after SPCs. Our paper thus enriches the theory of analyst attention (e.g. Bourveau et al. 2022).

This study also enhances our understanding of the reputation theory. Occupational reputation is considered an effective disciplinary mechanism in the labor market (Fama, 1980). Consistent with the reputation theory, analysts pursue high forecast accuracy to safeguard their reputation because reputation damage can lead to long-term losses in career prospects and financial benefits (Jackson, 2005). Our evidence also supports this argument. Our findings explain how analysts act to improve forecast accuracy to manage a crisis in which personal reputation is damaged when firms face sudden SPCs.

Therefore, according to our research conclusions, analysts’ regulatory agencies should strengthen supervision and establish an effective reputation reward mechanism, which will help analysts strengthen self-discipline. Analysts are motivated to be diligent and responsible during the information acquisition phase for the sake of personal reputation and long-term career development. At the same time, analysts should fully obtain information before issuing forecasts, and the forms of obtaining information are not limited to on-the-spot investigations, telephone interviews, etc.

Our study opens up some new and potentially fruitful research avenues. First, how SPCs influence analyst forecast accuracy in the long run. Our research focuses on the short-term impact of SPCs on analyst forecast accuracy within a one-year time span. However, in the long run the picture could be very different. Although an information-inferior analyst could pay more attention to enhance forecast accuracy immediately after SPCs, her/his forecast accuracy may still decrease at some point in future for several reasons. For example, constrained by limited attention, analysts may later turn their attention to other companies, leading to forecast accuracy decreases again. Thus, it is also interesting to investigate the long-term path of analyst forecast accuracy fluctuation under the influence of SPCs.

Second, since the Chinese stock market is still immature, the market power and role of analysts in China are different from those in developed markets. Thus, it remains to be seen whether SPCs can still attract analysts’ attention and effectively improve the accuracy of their forecasts. Therefore, future research could utilize a cross-country design to examine the impact of SPCs on analyst forecasts.

Conclusion

Although SPC is one of the hot issues that academic research and regulatory authorities have paid attention to in recent years, there is few research on its consequences. We examine whether SPC affects the economic consequences of analyst forecasts. Following analyst attention theory and analyst collusion theory, we postulate two competing arguments on the relationship between SPCs and forecast accuracy. Empirical findings show that after the company’s SPC, analyst forecast error decreases and forecast accuracy improves. Through parallel trend test, replacement of explained variables, instrumental variable method, and placebo test, it is discovered that the increase of analyst forecast accuracy after SPC is robust. These results support the view of analyst attention theory, implying that SPCs make analysts prefer to pander to investors rather than pander to management. In other word, SPCs can bring certain positive externalities to the capital market. We hope that our findings will inspire more research on the positive externalities of SPCs.

Data availability

The data that support the findings of this study are available on request from the corresponding author. The data are not publicly available due to privacy or ethical restrictions.

Notes

It is worth noting that there is a body of literature on the consequences of firm-specific SPC risk (An et al., 2015; Harper et al., 2020; Lee, 2022; Benkraiem et al. 2023). However, this body of literature is different from the literature of firm-specific SPC events. We discuss the differences in detail in Section 2. Unless otherwise specified, the following SPCs refer to SPC events.

The detailed definitions of these measures are provided in these literature mentioned above.

Table 1 shows the contribution of analysts’ attention before and after SPC under hypotheses 2 and 3.

Hutton et al. (2009) who present the measure of SPC for the first time use 3.09 standard deviations as threshold value. Kim et al. (2011a) employ a stricter standard of 3.2 standard deviations. The stricter criterion alleviates the problem of data deviation from the standard normal distribution and is widely used in later literature (e.g. Kim et al. 2011b, Kim et al. 2022).

For instance, assuming that the SPC for a firm in a treatment group occurred in June 2010, we take June 2010 as the base point and then examine the changes in analyst forecast accuracy during the one-year window period from December 2009 to December 2010. For the companies in the control group that match this treatment group, we also use June 2010 as the base point, and determine the same one-year window period as the treatment group companies.

References

Altschuler D, Chen G, Zhou J (2015) Anticipation of management forecasts and analysts’ private information search. Rev Account Stud 20(2):803–838

Amiram D, Landsman WR, Owens EL, Stubben SR (2018) How are analysts’ forecasts affected by high uncertainty? J Bus Financ Account 45(3-4):295–318

An H, Zhang T (2013) Stock price synchronicity, crash risk, and institutional investors. J Corp Financ 21:1–15

Bauer AM, Fang XH, Pittman JA (2021) The importance of IRS enforcement to stock price crash risk: The Role of CEO power and incentives. Account Rev 96(4):81–109

Benkraiem R, Ben-Nasr H, Nechi S, Rjiba H (2023) Stock price crash risk and leverage dynamics: Evidence from the GCC countries. Finance Res Lett 54:103688

Bourveau T, Garel A, Joos P, Petit-Romec A (2022) When attention is away, analysts misplay: distraction and analyst forecast performance. Rev Account Stud 29:916–958

Boyer B, Mitton T, Vorkink K (2010) Expected idiosyncratic skewness. Rev Financ Stud 23:169–202

Cao Z, Wang R, Xiao X, Yin C (2023) Disseminating information across connected firms-Analyst site visits can help. J Empir Financ 72:510–531

Chen J, Hong H, Stein J (2001) Forecasting crashes: trading volume, past returns, and conditional skewness in stock prices. J Financ Econ 61:345–381

Cheng Q, Du F, Wang X, Wang YT (2016) Seeing is believing: analysts’ corporate site visits. Rev Account Stud 21(4):1245–1286

Comiran F, Siriviriyakul S (2019) Analyst earnings forecast precision and local advantage: evidence from American depositary receipt firms. Account Financ 59:481–510

Conrad J, Kapadia N, Xing Y (2014) Death and jackpot: why do individual investors hold overpriced stocks? J Financ Econ 113:455–475

Deng XH, Gao L, Kim JB (2020) Short-sale constraints and stock price crash risk: Causal evidence from a natural experiment. J Corp Finance 60:101498

Dhaliwal DS, Radhakrishnan S, Tsang A, Yang YG (2012) Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. Account Rev 87(3):723–759

Dimson E (1979) Risk measurement when shares are subject to infrequent trading. J Financ Econ 7:197–226

El Ghoul S, Guedhami O, Wei Z, Zhu Y (2023) Does public corruption affect analyst forecast quality? J Bank Financ 154:106860

Edmans A, Goldstein I, Jiang W (2012) The real effects of financial markets: The impact of prices on takeovers. J Financ 67(3):933–971

Fama E (1980) Agency problems and the theory of the firm. J Polit Econ 88:288–307

Fang XH, Pittman J, Zhao YP (2021) The Importance of Director external social networks to stock price crash risk*. Contemp Account Res 38(2):903–941

Francis JR, Neuman SS, Newton NJ (2019) Does tax planning affect analysts’ forecast accuracy? Contemp Account Res 36(4):2663–2694

Han B, Kong D, Liu S (2018) Do analysts gain an informational advantage by visiting listed companies? Contemp Account Res 35(4):1843–1867

Harper J, Johnson G, Sun L (2020) Stock price crash risk and CEO power: Firm-level analysis. Res Int Bus Finance 51:101094

He LR, Conyon MJ, Chen J (2020) Signaling via earnings downgrades: How reputational concerns shape analyst responses to corporate fraud? Corp Gov- Int Rev 28(4):240–263

Hu J, Long W, Luo L, Peng Y (2021) Share pledging and optimism in analyst earnings forecasts: Evidence from China. J Bank Financ 132:106245

Hutton AP, Marcus AJ, Tehranian H (2009) Opaque financial reports, R-2, and crash risk. J Financ Econ 94(1):67–86

Jackson AR (2005) Trade generation, reputation, and sell-side analysts. J Financ 60(2):673–717

Jin L, Myers SC (2006) R-2 around the world: New theory and new tests. J Financ Econ 79(2):257–292

Ke B, Yu Y (2006) The effect of issuing biased earnings forecasts on analysts’ access to management and survival. J Account Res 44(5):965–999

Kim JB, Lee E, Zhu ZM (2022) Do firm-specific stock price crashes lead to a stimulation or distortion of market information efficiency? Contemp Account Res 39(3):2175–2211

Kim JB, Li L, Zhang H (2017) Analyst forecast accuracy and media independence. Financ Manag 46(4):1023–1051

Kim JB, Li YH, Zhang LD (2011a) CFOs versus CEOs: Equity incentives and crashes. J Financ Econ 101(3):713–730

Kim JB, Li YH, Zhang LD (2011b) Corporate tax avoidance and stock price crash risk: Firm-level analysis. J Financ Econ 100(3):639–662

Koenig F (2016) Analyst behavior: the geography of social interaction. J Behav Financ 17(3):201–216

Kong DM, Liu LH, Liu SS (2020) Market information traveling on high-speed rails: The case of analyst forecasts. Pac-Basin Finance J 61:101320

Lang MH, Lins KV, Miller DP (2003) ADRs, analysts, and accuracy: Does cross listing in the United States improve a firm’s information environment and increase market value? J Account Res 41(2):317–345

Lee KY (2022) Stock price crashes and auditors’ client-retention decisions. J Account Audit Financ 37(2):493–517

Lehavy R, Li F, Merkley K (2011) The effect of annual report readability on analyst following and the properties of their earnings forecasts. Account Rev 86(3):1087–1115

Liu G, Liu T (2022) Does individual investors’ dividend tax influence analyst forecast? Evidence from a quasi-natural experiment in China. Financ Res Lett 50:103263

Lourie B (2019) The revolving door of sell-side analysts. Account Rev 94(1):249–270. https://doi.org/10.2308/accr-52110

O’Brien PC, Tan HP (2015) Geographic proximity and analyst coverage decisions: Evidence from IPOs. J Account Econ 59(1):41–59

Pacelli J (2019) Corporate culture and analyst catering. J Account Econ 67(1):120–143

Park K, Tinaikar S, Shin YC (2017) Managerial control divergence and analysts’ information precision. Corp Gov- Int Rev 25(5):294–311

Song M, Kim D, Won C (2009) Earnings uncertainty and analyst forecast herding. Asia-Pac J Financ Stud 38(4):545–574

Xie Y, Zhang Y, Zhou J (2012) National level, city level auditor industry specialization and analyst forecast properties. Int J Audit 16(3):248–267

Zhang M, Tong LJ, Su J, Cui ZP (2015) Analyst coverage and corporate social performance: Evidence from China. Pacific-Basin Finance. Journal 32:76–94

Author information

Authors and Affiliations

Contributions

YF: Conceptualization, methodology, validation, supervision, and writing-review. YZ: Data collection, formal analysis, validation, and writing-original draft.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Fan, Y., Zhang, Y. Consequences of firm-specific stock price crashes on analyst forecasts: Evidence from China. Humanit Soc Sci Commun 11, 367 (2024). https://doi.org/10.1057/s41599-024-02874-0

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-024-02874-0