Abstract

Since public support is critical for implementing carbon pricing policies, we conduct a systematic review and meta-analysis to examine the survey-based literature on change in public support for direct and indirect carbon pricing policies with and without revenue recycling options. Following a comprehensive and transparent machine-learning assisted screening of the literature, our dataset comprises 35 studies containing 70 surveys across 26 countries with over 100,000 respondents. We find that the introduction of any type of revenue recycling option increases public support for carbon pricing. Results from our meta-regression indicate that green spending (i.e. using revenues for climate-friendly projects) is the only revenue recycling option associated with a statistically significant increase in public support. Our findings moreover suggest that the effects may depend on which region the survey was carried out, highlighting the need for additional research in countries in the regions of Africa and Latin America and the Caribbean.

Similar content being viewed by others

Introduction

To achieve ambitious climate change mitigation, it is crucial to address the current mispricing of fossil fuel based goods. This can be achieved by removing fossil fuel subsidies (i.e. indirect carbon pricing policy abolishing negative carbon prices) and by putting a price on carbon (i.e. direct carbon pricing policy introducing a positive price associated with carbon emissions)1,2,3,4. Such policies result in salient price increases passed on to consumers which, without additional compensatory policies, could lead to strong public opposition. Recent examples of protests against fuel price increases include the ‘yellow vests’ in France in 2018, as well as protests in Nigeria in 2020, and in India in 2021. To address some of the public’s concerns and to increase support for carbon pricing, studies in economics, behavioural psychology and political science recommend policymakers to introduce complementary policies with clear benefits intended for their constituents3,5,6. Such complementary policies are often referred to as revenue recycling schemes and can vary in design. For example, revenue recycling could reduce the financial impact of increased fossil fuel prices by redistributing some of the revenues back to all or a targeted segment of the population. Other types of revenue recycling include investing in low-carbon infrastructure projects, or agreeing to reduce other types of taxes.

Current survey-based evidence on the effect of revenue recycling on public support for direct and indirect carbon pricing policies is mostly comprised of ex-ante studies with scattered and at times contradictory results. These studies elicit attitudes for different types of direct and indirect carbon pricing policies (e.g. carbon tax, fossil fuel taxes, fossil fuel subsidy reform, environmental taxes, and congestion charges), vary by the type of revenue recycling presented to respondents, and are conducted in countries with diverse socio-economic and political contexts. Several studies find an overall tendency for respondents to prefer investing revenues towards climate-friendly activities, such as renewable energy projects, expanding public infrastructure, or further climate research7,8,9. Some detect favourable responses for applying tax cuts for income or labour taxes to counterbalance the increase in costs10,11. Yet other survey studies reveal that respondents prefer to compensate all households equally or specifically target low-income households and highly affected population groups, such as workers or the elderly, for financial compensation12,13. Real-world examples of carbon pricing with complementary revenue recycling are limited14. Moreover, the ex-post survey-based literature is even smaller and also reveals some scepticism on the effects of revenue recycling to increase public support15,16.

Given the varying conclusions from the existing studies, this study aims to synthesise and reconcile the available knowledge from primary ex-ante survey literature in a systematic, transparent and rigorous way. Our aim is to understand the change in public attitude – and the determinants of this change – towards a direct or indirect carbon pricing policy after revenue recycling schemes are presented to survey respondents. By conducting a machine-learning assisted systematic review and meta-analysis, we provide robust evidence on how the levels of support vary systematically for different pricing policies, revenue recycling options, and sampling regions of the existing survey literature.

The results from our study indicate that the introduction of any type of revenue recycling scheme increases public support for carbon pricing. When comparing the different schemes to each other using a logistic meta-regression we find that only green spending increases public support at a statistically significant level for carbon pricing when compared to using revenues for public finance. The effect of other revenue recycling schemes on public support, including uniform cash transfers, remain statistically insignificant. Our meta-regression findings moreover suggest that the effect of revenue recycling on public support depends on the region in which the survey is conducted, and is stronger in Africa, Asia and Pacific, and Latin America and Caribbean than in the baseline region North America. However, the small sample size for studies on this topic conducted in regions from low- and middle-income countries urgently beckons for further research.

Results

Systematic review – data and sample

We perform a comprehensive machine-learning assisted search and selection strategy and identify a final data sample of 35 primary studies from a total of 3542 retrieved search records (Web of Science, Scopus, snowballing), which comprise 70 surveys representative at the general population level, with 113,356 respondents spanning 26 countries6 (see Supplementary Table 3 for an overview of all included studies). Surveys were conducted between 2005 and 2022 and 87% of the sample comes from surveys conducted after 2016. We note that 20 surveys (close to a third of our sample) come from one working paper published in 2022, which allowed to expand regional variations in Latin America and the Caribbean as well as in Africa17. Our complete review methodology is described in the Methods section.

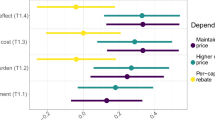

We categorise the different revenue recycling schemes presented in the 70 surveys into seven categories (see Fig. 1), namely (1) uniform cash transfers; (2) targeted cash transfers; (3) green spending; (4) tax cuts; (5); corporate tax cuts; (6) public finance; and (7) miscellaneous. We classify any scheme as revenue recycling which specifies how revenues generated from a direct carbon price or saved from a fossil fuel subsidy reform would be explicitly used (or recycled) to benefit households or society as a whole. Although using revenue towards public finance does not directly benefit households, often surveys explicitly ask respondents their support for a carbon pricing policy when revenues would be used to manage government expenditures and debts.

The category green spending captures all schemes that reference infrastructure, energy efficiency, research and development, and other types of environmental projects. Cash transfers – both uniform and targeted – refer to schemes that explicitly state a redistribution scheme to all or some portion of the population. Tax cuts refer to schemes whereby individual people would benefit, either through income or labour tax cuts, consumption tax cuts, or a tax rebate. Corporate tax cuts refer to tax cuts that benefit companies. Public finance refers to schemes that explicitly state that revenues would go towards a general government budget or explicitly to reduce government debt/budget deficit. The category miscellaneous refers to revenue recycling schemes that were presented as a combination of two categories, or that were did not fit the other categories.

In terms of regional distribution, 44% of surveys were sampled in Europe and West Asia, 24% in North America, 23% in Asia and Pacific, 6% in Latin America and the Caribbean, and 3% in Africa. Regarding country distribution, the majority of surveys were conducted in the USA (19%), followed by Switzerland (7%), Canada (6%), China (6%), and Spain (6%) (Fig. 2). The survey evidence for different revenue recycling schemes is scattered unevenly across surveys. 83% of surveys in our sample elicit responses for green spending, 68% for tax cuts, 58% for targeted cash transfers, 47% for uniform cash transfers, 35% for corporate tax cuts, 11% for public finance, and 16% for miscellaneous.

This figure indicates which revenue recycling options are elicited by country and the country as well as regional shares represented in the final sample. In each country, one or more surveys elicited preferences for green spending, and targeted cash transfers. Surveys in all countries except for Norway and Ecuador elicited for uniform cash transfers. Surveys in all countries except for Norway elicit for tax cuts. Surveys elicit corporate tax cuts in all countries except for Egypt, Norway, Sweden, and Ecuador. Miscellaneous types of revenue recycling options are elicited only in Egypt, India, Indonesia, Spain, Sweden Switzerland, Ecuador, Mexico, and USA. Countries marked in bold and with the check mark are represented in the quantitative analysis. This is because for those countries, our sample includes surveys that provide descriptive statistics and use an unspecified baseline before presenting respondents with revenue recycling options.

The type of carbon pricing policy elicited also varies across the surveys, whereby 67% of surveys elicit support for carbon taxes, 12% for fossil fuel taxes, 10% for fossil fuel subsidy reforms, and less than 10% for environmental taxes or congestion charges. Furthermore, we find that the majority of surveys (77%) specify that a carbon pricing policy is intended towards a specific fuel, specifically gasoline, whereas the rest did not specify.

Regarding the measure of public attitudes, 66% of papers focus on support while the rest use acceptance, acceptability, willingness to pay, or other measures, such as preferences. However, a clear definition of the attitude measurement is often not provided in the primary studies. Conceptually, the different attitude measures appear to be used interchangeably or as potentially equivalent terms in the identified studies. While the exact definitions of these public attitude terms have potential implications for decision-making based on their different meanings, we interpret them as an overarching measurement concept to reveal respondents’ favour or disfavour for a certain policy in the primary study18.

Quantitative results

To ensure comparability between effect sizes, in our quantitative analysis we only include papers that provide effect sizes when the change of public support with a revenue recycling options is compared to a baseline of “unspecified revenue use” (i.e. when surveys do not initially specify how generated revenues would be used). Moreover, this allows us to rule out potential effects from respondents being primed or prompted to compare revenue recycling to different baselines. Due to wider availability and to ensure comparability of effect sizes, we use summary statistics rather than results from econometric analyses in the primary studies. For the quantitative analysis, since very few studies conducted econometric analyses on the impact of revenue recycling, we expanded our dataset by including those that provide summary statistics. This also reduces the risk of comparing results from econometric analyses that are of different quality and potentially subject to biases. Our sample for the meta-regression thus includes 259 effect sizes from nine studies, 36 surveys, 68,043 respondents, spanning 22 countries. The surveys in our sample use different support measures, such as Likert-scales (with different levels across the studies), binary scales (support-not support), or stated preferences among policy alternatives. Although we may lose some important information from binning scaled responses into a binary system, to harmonise the different scales across the primary studies we standardise the effects by testing for the direction of the aggregated effect found for each revenue recycling scheme (that is, increase vs. decrease in public support), similar to comparable meta-analyses19,20.

Our descriptive analysis reveals that presenting revenue recycling to respondents increase support for a given carbon pricing policy when compared to ”unspecified revenue use” (see Fig. 3a). Revenue recycling options for which at least 80% of the available effect sizes report an increase in support for carbon pricing policies include green spending (97%), targeted cash transfers (86%), and corporate tax cuts (80%). In contrast, for uniform cash transfers only about two thirds of available effect sizes reported an increase in support, and labour and consumptions tax cuts and public finance about 80% of the effect sizes report an increase in support when compared to our baseline.

This figure shows the share of positive and negative effect sizes for all regions and individually by each region. a For all surveys included in the quantitative analysis, the share of positive effect sizes is largest for green spending (97%) and lowest for uniform cash (67%). b In the Africa region, all effect sizes for all revenue recycling options are positive, but the sample is small. c In the Asia and Pacific region, effect sizes are positive for public finance (100%) followed by targeted cash transfers (95%). d In the Europe and West Asia region, only for green spending (100%) show over 90% of effect sizes are positive. The lowest positive share is found for uniform cash transfers (64%). e In the Latin America and Caribbean region, all effect sizes are positive for uniform cash transfers, green spending, corporate tax cuts and public finance. The share of positive effect sizes is lowest for tax cuts (75%). f In the North America region, the effect of targeted cash transfers is always positive. For uniform cash transfers, corporate tax cuts and public finance half of the effect sizes are positive (50%), and more than 80% of the effect sizes are positive for green spending and tax cuts.

Regionally (see Fig. 3b–f), we find that in North America the reported effect sizes for at least three out of six types of revenue recycling schemes result in an increase in public support for a given carbon pricing policy. With regards to Africa, we find that all effect sizes reported for revenue recycling options are positive. For Asia and Pacific, we find that the reported effect sizes for public finance, targeted cash transfers, and green spending are over 90% positive. The revenue recycling option with the lowest share of positive effects in the Asia and Pacific region is uniform cash transfers (67%). For Europe and West Asia, we find that all effect sizes for green spending are positive; uniform cash transfers seem to have the least positive impact with only 64% positive effect sizes. In Latin America and the Caribbean, we find that effect sizes for uniform cash transfers, green spending, and corporate tax cuts, and public finance are all positive. However, for targeted cash transfers to low-income households or disproportionally affected population segments shows lower positive effects sizes (88%) as well as for income and consumption tax cuts (75%), which indicate potentially lowest impact on public support in that region. The evidence base, however, is very limited for some regions such as Africa and Latin America and the Caribbean.

Next, we run a logistic meta-regression on the same sample to compare the different revenue recycling schemes with each other, taking the allocation of revenues to public finance as a baseline (see Table 1). We find that targeted cash transfers and green spending increase public support for carbon pricing, but only the latter is statistically significant at the 1% level (3.09; standard error 1.08; p < 1%, two-tailed test). Our results suggest that redistributing revenues equally to all households via uniform cash transfers (−0.60; standard error 0.86; p > 10%, two-tailed test) is associated with a decrease in public support. We also find that corporate tax cuts (−0.51; standards error 0.47; p > 10%, two-tailed test) are associated with a decrease in support, but none of the effects is significant at conventional level.

We control for the type of policy, whether a direct carbon pricing policy was in place at the time of the survey, regional variation and study design, but find only few significant effects – probably related to the limited sample size, which is a common problem in meta-regression21 (see Supplementary Table 4 for details on variance inflation factors). Due to insufficient variation across observations, we did not control for other potentially interesting features, such as the year the sample was collected or the article was published, the gender of the lead author, the timing of the survey in relation to upcoming elections or a forthcoming introduction of a carbon pricing policy, the type of rating scales used to measure support, or other elements of the survey, such as checking for communication effects.

Our regional dummies suggest that – compared to North America – increases in public support through revenue recycling are significantly higher in regions mainly composed out of developing countries, i.e. Africa (significant at the 1% level, two-tailed test), East Asia and Pacific (significant at the 5% level, two-tailed test), and Latin America and Caribbean (significant at the 1% level, two-tailed test). The reported effect is also nominally positive for Europe and West Asia and Asia and Pacific, but comparatively small and not statistically significant. Non-experimental surveys tend to inflate estimates when compared to surveys with an experimental component (significant at the 1% level, two-tailed test), highlighting the importance of the choice of survey design22. Applying revenue recycling to carbon and environmental taxes compared to fossil fuel subsidy removal policies shows to increase support, but the effect is not statistically significant at conventional level.

Since all surveys underlying our analysis are representative for the general population, we decided against the use of sample weights in our main regression. However, we provide results from a weighted regression in the Supplementary Information (see Supplementary Table 5). Additional robustness checks are also included in the Supplementary, such as an additional indicator variable (see Supplementary Table 6) to control for the influence of the working paper which provides our dataset with 20 surveys17 in our logit results, publication bias (see Supplementary Table 7) and a logit specification by OLS regressions (see Supplementary Table 8).

Discussion

The existing literature has identified various channels on how the use of revenues generated from indirect and direct carbon pricing policies could positively change public perception by highlighting the role of ‘perceived fairness’ and ‘effectiveness’6,20. Specifically, questions of personal and distributional effects have shown to influence public perception of fairness and acceptability of carbon pricing policies. This is also why in theoretical analyses, uniform cash transfers are often touted as the optimal revenue recycling option with regards to the impact on acceptability, equity, and efficiency3. Regarding effectiveness, specifically effectiveness in reducing greenhouse gas emissions, using revenues to go towards climate-friendly and environmental purposes can also have positive effects on policy acceptability. Building on our systematic review and meta-analysis of the survey based literature, our regression results indicate that compared to using revenue towards public finance, only those schemes for environmental purposes (green spending) are associated with a statistically significant positive effect on public support.

While traditional economics as well as behavioural and political science suggest uniform cash transfer to increase public acceptability, our analysis of empirical studies indicate a decrease in support for this revenue recycling scheme when compared to public finance. One of the reasons why uniform cash transfers decrease support (if they have any effect) may be that respondents are averse to inequity and more concerned with distributional fairness23,24. Thus, rather than providing all households with equal amount of compensation, respondents may prefer to target and compensate narrowly defined groups. Indeed, our analysis suggests that respondents systematically prefer targeted cash transfers when compared to revenue use for public finance, though none of the effects show statistical significance. This is well in-line with another recent meta-analysis, which finds that distributional fairness of climate change taxes and laws is the most important factor influencing public attitudes20.

One way to interpret our findings for the substantial positive effect of green spending is that survey participants may not fully understand the incentive effects of Pigouvian taxes to reduce actions that have negative externalities, in this case change behaviour away from using fossil fuels to reduce greenhouse gas emissions25. The concept of linking the ineffectiveness of carbon pricing policies with a preference for using revenues explicitly towards environmental purposes is known as “issue-linkage”8. Thus, the perceived ineffectiveness of such pricing policies might be a driver in our findings of why the general public prefers revenues to be used for programs to improve the environment1,26. The concept of issue-linkage also applies to other Pigouvian taxes, such as red meat taxes. For example, a survey in Norway found that earmarking revenues from a red meat tax for environmentally friendly technology increased public acceptability more than using revenues for income tax27. Similarly for tobacco taxes, a study conducted in the US showed that public support for the tobacco increased when revenues were earmarked for health purposes28. Both in the case of red meat and tobacco taxes, respondents favoured revenue recycling options which aimed to reduce the negative externality targeted by the policy to begin with.

Our analysis generally reveals a low amount of primary studies that analyse the relationship between public support for carbon pricing schemes and revenue recycling options. Despite statistically significant results that certain revenue recycling options increase public support for carbon pricing policies when compared to unspecified revenue use, the relatively small sample size makes it difficult to draw definitive conclusions for policy-making. For instance, uniform cash transfers has one of the lowest number of observations in our meta-analysis and we observe a high variability for support in the primary studies. To further illustrate, uniform cash transfers are found to be the most popular revenue option in the studies by Nowlin et al.7 and Beiser-McGrath & Bernauer29, while it is comparatively the least popular option identified in studies by Douenne & Fabre30 and Ewald et al.31. This might underline the contextual importance of such research – depending on a country’s trust in institutions, recent economic history, regulatory traditions, political messaging and many other factors which we cannot control due to limited information in primary studies, certain revenue schemes might be more popular in one country and highly contested somewhere else. Moreover, unlike observational data or revealed preferences, a survey is an inherently controlled environment that identifies only the specified variations but cannot control for all potential biases and factors that may influence public opinion. This could also explain the perceived popularity of green spending as a potential artifact of surveys. When a survey intends to elicit support for green spending, the questions and information provided to respondents may create a more obvious link between carbon pricing policies and their environmental purpose, thus influencing “issue-linkage”.

We tried to increase the sample size in several ways. First, we looked at other regional databases in other languages. For example, given by the large number of Spanish-speaking countries and their low representation in our data base, we conducted a search for relevant studies in a major Spanish-language database called “La Referencia”. We used the same policies and public attitude keywords as we did in the English-language query and translated it into Spanish (see Supplementary Table 2). We retrieved 535 articles; however, none fit our inclusion criteria. We would not expect that including search queries in additional languages would significantly increase our sample. Another way we increased our sample size is by including results from 20 surveys (close to a third of our sample) from one working paper published in 202217. Our main results remain unaltered when including an additional indicator variable to control for the influence of this paper in our meta-regression (see Supplementary Table 6). Although we could have expanded our sample size for the meta-regression by assuming that respondents perceive “unspecified revenue use” to automatically imply public finance, we decided to treat those two concepts differently. We know from studies that wording and additional information can influence public support, for example when calling a policy a “carbon tax” or a “carbon contribution”1. Since we did not find any study that analyses what respondents imagine revenues are used for when the survey does not specify its usage, and to rule out any potential effects priming might have on respondents who receive information on how revenues are used (e.g., public finance) versus those that do not (e.g. “unspecified revenue use”), we decided to only included studies in our meta-regression which use a baseline without revenue recycling. This reveals a research gap on the cognitive-based effects of framing, additional information, political messaging and other priming methods on the responses from respondents.

Ultimately, our systematic review and meta-analysis show that the existing evidence on how revenue recycling influences public support for carbon pricing is relatively scarce. This points to a general gap in the empirical research of revenue recycling and public support for direct and indirect pricing policies. For example, the overwhelming majority of the surveys we identified are conducted ex-ante to introducing any type of carbon pricing policy. Although there is a limited number of countries and jurisdictions that have carbon pricing policies with revenue recycling, even fewer studies analyse ex-post the public support for these policies14,15,16. Moreover, our overall sample elicits support for a carbon tax (67%) and only few analyse public attitudes for fossil fuel subsidy reform (10%). Since fossil fuel subsidy reforms also lead to highly visible price increases for consumers, our study reveals a gap in empirical understanding how revenue recycling could increase support for this indirect carbon pricing policies. Moreover, most empirical studies in our dataset have been conducted in North America, Europe and West Asia, and Asia and Pacific, revealing a lack of research on how to increase support for carbon pricing policies with revenue recycling schemes in low-and middle-income countries in regions such as Latin America and the Caribbean and Africa. Given the number of countries in Latin America and the Caribbean which are implementing a direct and indirect carbon pricing policy and considering that protest responses are a form of active civic engagement in the region, additional empirical evidence could help inform policy-makers32,33. Moreover, very few of the revenue recycling schemes in our dataset consider other types of socio-economic and welfare policies beyond uniform- or targeted cash transfers. This points to another gap in the empirical literature to consider what types of revenue recycling policies could increase public support specifically in low- and middle-income countries.

Methods

Literature search and data extraction

There is a large literature that discusses systematic reviews and meta-analyses and how to conduct them in a methodologically sound way in social sciences. This systematic review broadly follows the guidelines by the Collaboration for Environmental Evidence34. We make use of machine-learning at the title and abstract screening stage to enable a comprehensive study identification. In particular, after screening a random sample of 100 publications, we train a support vector machine to rank the studies according to their probability of being relevant for our study. This is commonly known as “prioritised screening” that has been shown to substantially reduce workload without significant loss of recall35,36. In fact, we argue that it enables the design of comprehensive search string with high-levels of recall that would not be feasible otherwise.

For the literature identification, we conducted a query search in February 2022 and 2023 in the Web of Science and the Scopus literature databases. We connect three groups of keywords with boolean operators filtering for research on (1) explicit carbon pricing policies (carbon, CO2, GHG, ecological, environmental AND pricing, tax, trading, market, certificate, levy, allowance) and (2) implicit carbon pricing policies (fuel, diesel, gas, oil, kerosene, energy, LPG AND subsidy reform, tax) investigating (3) impacts on the general public attitudes (people, public, social AND attitudes, response, perception, resistance, support, fair, fairness, acceptance, acceptability, opinion, belief, willingness, willing, opposition, willingness to pay) (see Supplementary Table 1).

In order to ensure that our search query has a high recall of relevant research, we assembled a benchmark list of 53 studies of known relevance from a previous review which focuses more broadly on factors influencing public support of carbon pricing policies but does not focus on revenue recycling37. Our final search string located 51 out 53 benchmark studies. The searches were performed in Web of Science and Scopus identifying 3721 articles after correcting for duplicates. We also included all the references from the paper which were included by using citation chaser, which added an additional 1137 papers. All the results were exported and combined in the NACSOS review management tool38 for screening. The NACSOS review tool automatically removes duplicate records using trigram similarity-based fuzzy title matching. The meta-data is automatically recorded from the bibliographic databases using the NACSOS software38. A coding tool was used to systematically extract data from all eligible studies (codebook available upon request).

Records were screened at two levels (1) title and abstract, and (2) full-text. At an abstract-level, we screened all abstracts jointly by two people to minimise bias. When reviewing abstracts, all discrepancies between the two people were discussed and inclusion/exclusion criteria were further clarified prior to completing the screening. For the meta-analysis, we added additional inclusion criteria, that is we only included studies that also provided descriptive statistics and used the “unspecified” baseline before presenting respondents with revenue recycling options.

To screen the articles at an abstract level, the following eligibility criteria were followed by all reviewers:

Inclusion criteria

-

1.

Studies that conduct a public opinion survey towards different types of direct and indirect carbon pricing policies, e.g. Carbon -pricing, -tax, -trading, -levy, -allowance; or fuel –subsidy reform, -tax (including, diesel, gas, oil, kerosene, energy, or LPG). Congestion and pollution pricing policies are also included if the study reference carbon emissions reductions.

-

2.

Studies that are empirical, conducting surveys on a randomised set and representative sample of the general population.

-

3.

Studies that include a specified a measure of public opinion toward accepting carbon pricing policies, such as acceptance, acceptability, support, and willingness to pay.

-

4.

Studies that analyse some form of revenue recycling option as part of survey analysis using quantitative methods.

-

5.

Studies that collect data from the population through primary survey or representative sample through secondary data.

-

6.

Studies need either regression analyses and/or summary statistics indicating a change in public attitude.

Exclusion criteria

-

1.

Studies that assess unspecified tax or pricing policies (e.g. “Pigouvian taxes”) which do not reference carbon emissions. Studies were also excluded if they analysed public opinion on waste or water management, sulphur dioxide related policies, food, attitude toward specific technologies, housing, plastic tax, corporate social responsibility, reforestation, geoengineering, or personal and voluntary carbon trading.

-

2.

Studies that present no revenue use options to survey respondents.

-

3.

Studies using focus groups, in a laboratory setting, collecting responses from specific groups, such as farmers, policy makers, industry representatives, or students rather than the general population.

After the first screening of 200 random studies, we included 20 studies. These 20 studies plus the benchmark studies from prior literature searches are then used to train a machine learning classifier using terms from the titles, abstracts, and keywords. As a result, the remaining documents in the NACSOS management tool are ordered according to their predicted relevance based on the previous inclusion decisions. After each subsequent round of abstract screening, the machine learning classifier gets re-trained. As more documents are manually screened, the machine learning algorithm is updated using these additional labels, and the remaining documents are reordered by predicted relevance score. See Fig. 4 for an overview of the search and screening process.

Adapted from the ROSES flow diagram for systematic reviews.40

Methods for meta-analysis

Dependent variable

The dependent variable of our econometric analysis is the change in public support of a carbon pricing policy following the introduction of a revenue recycling option. One main obstacle for the comparison of surveys is that they use different measures of public support. This results from the variety of rating scales such as Likert- scales (with different levels across the studies), binary scales (support-not support), or stated preferences among policy alternatives makes meaningful comparisons of the effect sizes found in different studies difficult. We therefore take the direction of the effect (that is, increase vs. decrease in public support) as the dependent variable in our regression analysis, similar to meta-analyses conducted by refs. 19,20.

Moderator variables

Different moderator variables in our model account for the variation in the effects of revenue uses reported in our sample of studies. First, we create indicator variables, which capture the different survey designs that were presented to the respondents. For this, we include variables for the different revenue use options. We distinguish between redistribution schemes to the whole population or targeted to parts of it (uniform cash transfers and targeted cash transfers), infrastructure and other environmental and climate projects (green spending), tax-related relief mechanisms that could directly benefit populations (income and consumption captured in tax cuts), and relief mechanisms for firms (corporate tax cuts). We use public finance as a reference category for the regression. Hence, this meta-regression allows us to make statements about the impact of different revenue use options on the observed changes in public support relative to the effect of transferring it to the government budget.

In addition to variables that account for the revenue recycling schemes tested, our specifications account for the design of the survey type (survey questionnaire or choice experiment). It also accounts for the type of policy respondents support (carbon tax, fuel tax, or fossil fuel subsidy reform policy). We also include a dummy that indicates whether a carbon policy was already in place in the country under study at the time of the survey, and region fixed effects. We assume fixed effects for country region groups instead of single countries to decrease the risk of multi-collinearity and imprecise results in our regression analysis. Other interesting aspects of the survey designs such as the mode of data collection or the different measures of acceptance do not show enough variation to be included in our analysis.

Logistic regression for meta-analysis

We run a logit regression to determine the relationship between the dependent variable and the moderator variables. Suppressing the observation-specific index, the logit model assumes a continuous latent variable \({y}^{* }\) to measure the propensity for a study to find an increase in support caused by the introduction of a revenue recycling scheme. \({y}^{* }\) is supposed to react continuously to the characteristics gathered in the vector of moderator variables \({\bf{x}}\). However, we cannot observe \({y}^{* }\), but a binary variable \(y\) equal to 1 if the unobserved latent variable \({y}^{* }\) breaks a threshold theta, and 0 otherwise. Denoting \(\alpha\) the constant and \(\varepsilon\) the normally distributed error term, the model we want to estimate can be expressed as follows:

We can set \(\theta =0\) without a loss of generality. The resulting probability of a survey indicating a decrease in public support caused by the introduction of a revenue recycling scheme can be written as follows:

Using straightforward algebra, this equation can be transformed to:

We cluster standard errors on survey level to account for non-independence of observations. We then estimate our model with the maximum likelihood method. The \(\beta\)-coefficients and their p-values provide the direction and the significance of the effects of the moderator variables: A positive \(\beta\) suggests that a moderator variable increases the probability of obtaining an increase in public support when introducing a revenue recycling mechanism \(\Pr (y=1)\). We provide marginal effects at mean, which show the magnitude of the probability change for the two possible outcomes induced by the moderator variables. We report the Pseudo R2 as a measure of fit39. We also test the validity of the logit specification by OLS regressions (see Supplementary Table 8).

Data availability

The data and codebook of this study are made available in a public repository and can be accessed here: https://github.com/farahmkv/PublicSupport_RR_CP.

Code availability

The code used for the meta-analysis can be accessed here: https://github.com/farahmkv/PublicSupport_RR_CP.

Change history

25 November 2024

A Correction to this paper has been published: https://doi.org/10.1038/s44168-024-00199-x

References

Baranzini, A. & Carattini, S. Effectiveness, earmarking and labeling: testing the acceptability of carbon taxes with survey data. Environ. Econ. Policy Stud. 19, 197–227 (2017).

High-Level Commission on Carbon Prices. Report of the High-Level Commission on Carbon Prices. (2017).

Klenert, D. et al. Making carbon pricing work for citizens. Nat. Clim. Change 8, 669–677 (2018).

Pigou, A. The Economics of Welfare. (Macmillan, 1920).

Baranzini, A., Goldemberg, J. & Speck, S. A future for carbon taxes. Ecol. Econ. 32, 395–412 (2000).

Maestre-Andrés, S., Drews, S. & van den Bergh, J. Perceived fairness and public acceptability of carbon pricing: a review of the literature. Clim. Policy 19, 1186–1204 (2019).

Nowlin, M. C., Gupta, K. & Ripberger, J. T. Revenue use and public support for a carbon tax. Environ. Res. Lett. 15, 084032 (2020).

Sælen, H. & Kallbekken, S. A choice experiment on fuel taxation and earmarking in Norway. Ecol. Econ. 70, 2181–2190 (2011).

Sommer, S., Mattauch, L. & Pahle, M. Supporting carbon taxes: The role of fairness. Ecol. Econ. 195, 107359 (2022).

Jagers, S. C., Lachapelle, E., Martinsson, J. & Matti, S. Bridging the ideological gap? How fairness perceptions mediate the effect of revenue recycling on public support for carbon taxes in the United States. Canada and Germany. Rev. Policy Res. 38, 529–554 (2021).

Kaplowitz, S. A. & McCright, A. M. Effects of policy characteristics and justifications on acceptance of a gasoline tax increase. Energy Policy 87, 370–381 (2015).

Dolšak, N., Adolph, C. & Prakash, A. Policy design and public support for carbon tax: Evidence from a 2018 US national online survey experiment. Public Adm. 98, 905–921 (2020).

Maestre-Andrés, S., Drews, S., Savin, I. & van den Bergh, J. Carbon tax acceptability with information provision and mixed revenue uses. Nat. Commun. 12, 7017 (2021).

Carl, J. & Fedor, D. Tracking global carbon revenues: A survey of carbon taxes versus cap-and-trade in the real world. Energy Policy 96, 50–77 (2016).

Mildenberger, M., Lachapelle, E., Harrison, K. & Stadelmann-Steffen, I. Limited impacts of carbon tax rebate programmes on public support for carbon pricing. Nat. Clim. Change 12, 141–147 (2022).

Fremstad, A., Mildenberger, M., Paul, M. & Stadelmann-Steffen, I. The role of rebates in public support for carbon taxes. Environ. Res. Lett. 17, 084040 (2022).

Dechezleprêtre, A. et al. Fighting Climate Change: International Attitudes Toward Climate Policies. w30265 http://www.nber.org/papers/w30265.pdfhttps://doi.org/10.3386/w30265. (2022).

Kyselá, E., Ščasný, M. & Zvěřinová, I. Attitudes toward climate change mitigation policies: a review of measures and a construct of policy attitudes. Clim. Policy 19, 878–892 (2019).

Ohlendorf, N., Jakob, M., Minx, J. C., Schröder, C. & Steckel, J. C. Distributional Impacts of Carbon Pricing: A Meta-Analysis. Environ. Resour. Econ. 78, 1–42 (2021).

Bergquist, M., Nilsson, A., Harring, N. & Jagers, S. C. Meta-analyses of fifteen determinants of public opinion about climate change taxes and laws. Nat. Clim. Change 12, 235–240 (2022).

Higgins, J. et al. Cochrane Handbook for Systematic Reviews of Interventions. (John Wilsey & Sons, 2019).

Stantcheva, S. How to Run Surveys: A guide to creating your own identifying variation and revealing the invisible.

Kallbekken, S. & Sælen, H. Public acceptance for environmental taxes: Self-interest, environmental and distributional concerns. Energy Policy 39, 2966–2973 (2011).

Douenne, T. & Fabre, A. French attitudes on climate change, carbon taxation and other climate policies. Ecol. Econ. 169, 106496 (2020).

Kallbekken, S., Kroll, S. & Cherry, T. L. Do you not like Pigou, or do you not understand him? Tax aversion and revenue recycling in the lab. J. Environ. Econ. Manag. 62, 53–64 (2011).

Dresner, S., Dunne, L., Clinch, P. & Beuermann, C. Social and political responses to ecological tax reform in Europe: an introduction to the special issue. Energy Policy 34, 895–904 (2006).

Grimsrud, K. M., Lindhjem, H., Sem, I. V. & Rosendahl, K. E. Public acceptance and willingness to pay cost-effective taxes on red meat and city traffic in Norway. J. Environ. Econ. Policy 9, 251–268 (2020).

Hamilton, W. L., Biener, L. & Rodger, C. N. Who Supports Tobacco Excise Taxes? Factors Associated With Towns’ and Individuals’ Support in Massachusetts. J. Public Health Manag. Pract. 11, 333 (2005).

Beiser-McGrath, L. F. & Bernauer, T. Could revenue recycling make effective carbon taxation politically feasible? Science Advances. https://doi.org/10.1126/sciadv.aax3323 (2019).

Douenne, T. & Fabre, A. Yellow Vests, Pessimistic Beliefs, and Carbon Tax Aversion. American Economic Journal: Economic Policy, 14, 81–110 (2022). https://doi.org/10.1257/pol.20200092.

Ewald, J., Sterner, T. & Sterner, E. Understanding the resistance to carbon taxes: Drivers and barriers among the general public and fuel-tax protesters. Resource and Energy Economics, 70, 101331 (2022). https://doi.org/10.1016/j.reseneeco.2022.101331.

Moseley, M. W. Contentious Engagement: Understanding Protest Participation in Latin American Democracies. J. Polit. Lat. Am. 7, 3–48 (2015).

Bank, W. State and Trends of Carbon Pricing 2022. (Washington, DC: World Bank, 2022). https://doi.org/10.1596/978-1-4648-1895-0.

Pullin, A., Frampton, G., Livoreil, B. & Petrokofsky, G. Guidelines and Standards for Evidence Synthesis in Environmental Management. Version 5.0. (2018).

Callaghan, M. W. & Müller-Hansen, F. Statistical stopping criteria for automated screening in systematic reviews. Syst. Rev. 9, 273 (2020).

van de Schoot, R. et al. An open source machine learning framework for efficient and transparent systematic reviews. Nat. Mach. Intell. 3, 125–133 (2021).

Muhammad, I., Mohd Hasnu, N. N. & Ekins, P. Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review. Environments 8, 109 (2021).

Callaghan, M., Müller-Hansen, F., Hilaire, J. & Lee, Y. T. NACSOS: NLP Assisted Classification. Synthesis and Online Screening. Zenodo https://doi.org/10.5281/ZENODO.4121526 (2020).

McFadden, D. Frontiers in Econometrics, Chapter Conditional Logit Analysis of Qualitative Choice Behavior. (Academic Press New York, NY, USA, 1974).

Haddaway, N., Macura, B., Whaley, P. & Pullin, A. ROSES flow diagram for systematic reviews. Version 1.0 https://figshare.com/articles/ROSES_Flow_Diagram_Version_1_0/5897389 (2018).

Acknowledgements

F.M.V. is supported by a PhD stipend from the Heinrich Böll Stiftung. We further acknowledge funding from the European Union’s Horizon Europe Research and Innovation Programme (ELEVATE project – Grant No. 101056873 and CAPABLE project – Grant No. 101056891) as well as the International Development Research Centre (Supporting Low-Carbon Transition and Gender Equity in the Global South project). We also thank the participants of the workshop “Environmental policy attitudes in an era of crises” held during the 2022 Nordic Environmental Social Science conference for their helpful comments and suggestions. The funders had no role in study design, data collection and analysis, decision to publish or preparation of the manuscript. Views and opinions expressed are only those of the authors.

Author information

Authors and Affiliations

Contributions

F.M.V., J.C.S., J.C.M., and A.R. designed the research. F.M.V., A.R., and C.M. developed the literature screening strategy. F.M.V., C.M., A.R., and M.M. manually screened the literature and extracted the data. F.M.V. and A.R. performed the machine learning-enabled screening. C.M. and A.R. performed the meta-analysis. F.M.V., C.M., and J.C.S. analysed the results. F.M.V., C.M., and J.C.S. wrote the manuscript with contributions from all authors.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Mohammadzadeh Valencia, F., Mohren, C., Ramakrishnan, A. et al. Public support for carbon pricing policies and revenue recycling options: a systematic review and meta-analysis of the survey literature. npj Clim. Action 3, 74 (2024). https://doi.org/10.1038/s44168-024-00153-x

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s44168-024-00153-x

This article is cited by

-

Boosting public support for climate policy through information provision: insights from German survey experiments

npj Climate Action (2025)

-

Public support for carbon taxes varies across countries and policy design must consider the national context

Communications Earth & Environment (2025)

-

Global warming expectations of German firm representatives are overly optimistic, uncertain, and easily influenced

npj Climate Action (2025)

-

Unraveling the conditions for post-adoption contestation over hard climate policy in OECD countries

npj Climate Action (2025)

-

Political enablers of ambitious climate policies: a framework and thematic review

npj Climate Action (2025)