Abstract

Carbon trading plays an important role in improving the quality of technological innovation and suppressing innovation bubbles. We use patent data and financial data from Chinese firms from 2010 to 2021 and apply a difference-in-differences-in-differences (DDD) model to analyse the causal relationship between the carbon trading and technological innovation of manufacturing firms to demonstrate the inhibitory effect of manufacturing firms’ participation in carbon trading on innovation bubbles and to consider the synergistic effect of government intervention. The conclusions of the study are as follows. First, the participation of manufacturing enterprises in carbon trading increases their R&D investment, which does not increase the quantity of innovation but significantly improves the quality of their innovation, thus suppressing the creation of innovation bubbles. Second, government intervention can effectively play a synergistic role in improving the quality of technological innovation in manufacturing enterprises. Finally, the impact of carbon trading on technological innovation is more pronounced for large enterprises and high-tech manufacturing enterprises.

Similar content being viewed by others

Introduction

The Synthesis Report of the Sixth Assessment Report (2023) highlights that global greenhouse gas (GHG) emissions have continued to grow between 2010 and 2021, resulting in global surface temperatures that are 1.1 °C above those of 1850–1900. Its purpose is to achieve significant and sustained emission reductions and ensure a liveable and sustainable future for all. The environmental Kuznets curve shows that at a certain stage of economic development, economic growth and environmental pollution naturally follow an inverted U-shaped pattern. Promoting the harmonious development of the economy and the environment has always been an important economic issue.

In recent years, China’s total energy consumption has been increasing. We plotted Fig. 1 based on the National Economic and Social Development Statistical Bulletin issued by the China Statistics Bureau and found that China’s total energy consumption maintains an increasing trend from 2015 to 2022, while at the same time, the share of coal consumption clearly decreases. As the leading industry of China’s national economy, the manufacturing industry, which is in the process of driving rapid and sustained economic growth, has long followed a crude development model of high energy consumption and high pollution, which has placed enormous pressure on China’s society, resources and environment. According to China Energy Statistics, the manufacturing sector energy consumption in 2021 was 2931 million tonnes of standard coal, accounting for 55.94% of China’s total energy consumption.

Total energy consumption and coal weight in China from 2015–2022.

Driven by China’s major strategic goals of ‘carbon peaking’ by 2030 and ‘carbon neutrality’ by 2060, adapting to the new normal of green, low-carbon and high-quality development for the traditional manufacturing industry to realise a major transformation to ‘low energy consumption, low pollution and low emission’ through innovative means has become inevitable1. In the early days, China implemented a command-and-control-based emission reduction policy, which played a certain role in carbon emission reduction and environmental protection, but the implementation cost of administrative order and penalty-based measures was high and easily resisted by enterprises. Carbon trading is a type of market transaction that promotes the reduction of global greenhouse gas emissions and uses greenhouse gas emission quotas or greenhouse gas emission reduction credits as the subject matter. As a market-based environmental regulatory tool, it relies more on the current market environment, using supply and demand and price mechanisms to freely trade carbon allowances. Against the backdrop of the market-based emission reduction approach based on carbon trading being implemented globally, China, as the world’s largest developing country and largest carbon emitter, is also actively promoting the development of the carbon trading market and becoming an important participant in global climate governance. Since June 2013, China has established seven carbon trading pilot provinces and one voluntary carbon market in Beijing, Guangdong, Shanghai, Shenzhen, Chongqing, Hubei, Tianjin and Fujian. The official launch of China’s national carbon emissions trading market in 2021 marked an important step in China’s efforts to reduce emissions.

Currently, the manufacturing industry has become the main force of China’s innovation-driven development. In 2021, R&D investment in the manufacturing industry reached 16,914 billion yuan, which was 60% of the country’s total R&D investment. With the continuous improvement of R&D investment, the number of Chinese patents has exploded in recent years, and in 2019, it surpassed the United States for the first time to become the largest source country for submitting international patent applications. However, China’s innovation strength has not improved with the growth in the number of patent applications, and the proportion of high-quality patents is low. According to the Global Innovation Index 2021 report released by the World Intellectual Property Organisation (WIPO), China’s scientific and technological innovation strength is ranked only 12th globally, which indicates that the quality of patents is not high and shows a ‘bubble’ and ‘innovation bubble’ in patents. This finding indicates that the quality of patents is not high, showing patent ‘bubbles’ and ‘innovation illusions’.

Ideally, the carbon market can provide effective incentives for companies to save energy and reduce carbon emissions through carbon trading, and according to Porter’s hypothesis, appropriate environmental regulation will compensate for the cost of environmental compliance through the effect of ‘compensation for innovation’2. There are problems such as a lack of a functional market3, insufficient liquidity4, and poor information transparency5, and most companies regard participation in the carbon market as a means to improve their relationship with the government as well as to win a good social reputation6. China’s carbon trading market has failed to achieve the expected effect and is only weakly efficient7. Thus, what is the policy effect of implementing carbon trading to drive manufacturing firms’ technological innovation in China? What is the marginal effect of carbon trading at different stages of manufacturing firms’ technological innovation? The answers to these questions can help manufacturing firms improve productivity while achieving energy savings and emission reduction in the face of the dual constraints of resources and the environment.

There are some gaps in the literature concerning the impact of environmental regulatory instruments such as carbon trading on corporate technological innovation. The possible contributions of this paper are as follows. First, we focus on the dual attributes of manufacturing enterprises, aiming at the contradiction between them as the main body of high carbon emission and the main force of innovation, based on the micro-data of manufacturing industries in pilot areas, to provide further evidence for whether carbon trading can improve the technological innovation level of manufacturing enterprises, and make up for the shortcomings of existing studies that focus on regional macro-analysis. Second, we discuss the new issues of patent ‘bubbles’ and ‘innovation illusions’ in the context of carbon trading as a market-based environmental regulation tool. At present, China is experiencing explosive growth in the number of patents, but the proportion of high-quality patents is low. Under the stimulation of the market mechanism of carbon trading, enterprises may focus on the depth and effect of technological innovation rather than pure quantity, thus improving the patent ‘bubble’ and ‘innovation illusion’, and this paper provides a new explanation for this problem. Third, we test the synergy between market mechanisms and government intervention. From the perspective of market failure and emissions regulation, government regulation and policy incentives are introduced to further reveal the effect of government intervention in driving technological innovation in manufacturing enterprises through carbon trading.

Literature review

Coase noted in The Problem of Social Cost in 1960 that low transaction costs and clear property rights are the basis for realising free trade8. The Coase theorem provides a new way to solve the problem of carbon emissions; that is, the government can set the total amount of carbon emissions, distribute carbon quotas to different subjects, and allow different subjects to trade carbon quotas according to their own needs, allocating resources effectively to achieve the optimal cost and benefit; thus, carbon trading has emerged. As the world’s largest and first multinational carbon market for greenhouse gases, the EU Emission Trading Scheme (EU ETS) aims to realise established greenhouse gas emissions at the lowest possible cost while providing incentives for innovation, which in the long run may be the most important means of achieving the significant reductions in greenhouse gas emissions that are needed9.

Compared with the EU ETS, the Chinese carbon trading market is still in its infancy. In recent years, there have been an increasing number of studies on the emission reduction effects surrounding China’s carbon trading policy, with several scholars arguing that China’s carbon trading market, as an important market tool to promote growth and CO2 emission reduction in China’s industrial sector10, can provide effective incentives for energy-saving and carbon-reducing behaviours of firms, which can both promote economic growth11 and, through external technological breakthroughs, reduce carbon emissions12, improve energy efficiency13, achieve carbon reduction targets14, and enhance corporate environmental performance15. Another group of scholars believe that, affected by liquidity, quantity, carbon price and allocated quotas16, China’s carbon trading market has not achieved the expected effect, is only weakly efficient, and has not yet reached semistrong and strong efficiency7.The possible reasons for China’s low efficiency in the carbon trading market include irrational behaviours, poor transparency of information, imperfections in the market mechanism, and transaction costs5.

Research on corporate participation in carbon trading and technological innovation has a long history. On the one hand, carbon trading is a type of environmental regulation. According to the neoclassical theory, after enterprises are included in the carbon market, they may need to take measures to reduce emissions, use cleaner technology or raw materials, update equipment, improve the waste treatment system, etc., which will lead to an increase in the costs of pollution control and production costs of enterprises, produce a ‘cost-following’ effect, and increase the cost pressure, forcing enterprises to transfer part of their investment to the pollution reduction sector, crowding out capital that could have been used for R&D and innovation. Cost pressure forces enterprises to transfer part of their inputs to the pollution abatement sector, crowding out capital that could have been used for R&D and innovation, and inhibiting corporate innovation17. This is verified by Zhang et al.18 and Lyu et al.19, who similarly argue that carbon trading inhibits the development of low-carbon technological innovations in the short term. On the other hand, Porter’s hypothesis suggests that properly designed environmental regulation, especially market-based instruments, can have an ‘innovation compensation’ effect, which not only improves environmental performance but also partially, and sometimes completely, offsets additional regulatory costs and compensates for the costs of environmental compliance2. A number of studies support Porter’s hypothesis that environmental regulations such as carbon trading can promote technological innovation20,21,22 because innovation plays a key role in sustainable economic development23, and technological change is seen as the most important determinant of long-term abatement costs24.

In recent years, carbon trading and enterprise technological innovation have been significant topics in academic research, and there are differences in the ‘cost-to-follow’ effect and ‘innovation compensation’ effect. Although the existing research has achieved relatively rich results, some still need to be explored in depth. First, most of the existing relevant empirical studies use whether enterprises are in carbon trading pilot provinces or cities as a proxy variable; however, the main body of carbon trading is emission-control enterprises. The use of data from all enterprises in the pilot region is not precise enough to clearly define the effect of carbon trading. Second, the R&D innovation of enterprises includes two aspects: R&D input and R&D output. R&D input, as a preinvestment of resources, is affected by the high failure rate, uncertainty and other risks that exist in the R&D process; thus, innovation output can more intuitively and effectively reflect the level of technological innovation of enterprises. Most of the current studies focus on the quantity of technological innovation25,26,27 and lack research on the quality of enterprise technological innovation. Finally, the government and the market are the two main means of resource allocation, and there is a lack of research on the synergistic effect of government intervention.

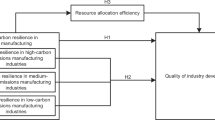

Research hypotheses

Carbon trading, as a market adjustment mechanism, allows enterprises to sell excess carbon emission allowances to enterprises lacking allowances at market prices18. The carbon trading market is built based on differential marginal carbon abatement costs, whereby enterprises with surplus emission rights gain externality benefits by selling allowances, and enterprises with excess emissions bear higher emission costs, thus pushing enterprises to reduce carbon emissions through the cost effect. Traditional neoclassical economic theory argues that environmental impacts inevitably generate additional production costs, forcing firms to shift some of their inputs to the pollution abatement sector, while the internalisation of external environmental costs inevitably increases firms’ cost pressures. Meanwhile, cost pressures and operational constraints consume firms’ R&D investments28, thus inhibiting firms’ innovation29.

With the continuous development of environmental economics, the cost-compliance effect of the neoclassical school has gradually been gradually questioned by scholars. Porter’s hypothesis proposes that appropriate environmental regulation compensates for environmental compliance costs through the ‘innovation compensation’ effect2, precisely because environmental policies can guide innovative activities to shift to low-carbon technologies, which not only reduces compliance costs4 but also eliminates the cost of purchasing carbon emission allowances in the long term. The environmental costs of each firm under carbon trading policies are internalised30, forcing firms to explore cleaner and more efficient production methods and innovative energy solutions. Under mature carbon trading market conditions, enterprises pay attention to environmental technology innovation, which can effectively reduce carbon emissions and thus occupy a favourable position in the carbon trading market21.

Based on the Porter Hypotheses, the carbon trading system transforms carbon emissions into explicit costs through allowance allocation and carbon price fluctuations. When a firm’s marginal abatement cost exceeds the carbon price, it chooses to purchase allowances; otherwise, it triggers technological innovation. This market signal changes the cost function of firms, forcing management to incorporate innovation into strategic considerations and phase out low-quality innovation projects. Secondly, carbon allowances are tradable, enabling firms to generate cash flow by selling surplus allowances in the carbon market, providing funds for R&D investment. Meanwhile, China’s carbon allowance allocation rules are dominated by the benchmarking approach, which includes requirements for technological advancement. Under the benchmarking approach, firms whose actual emissions are lower than the benchmark value can obtain surplus allowances, driving technological upgrades. The benchmark value is set based on the industry’s average advanced level and relies on verifiable data, which reduces firms’ incentives for misreporting. To obtain more free allowances, firms must adopt cutting-edge technologies, which directly incentivizes high-quality low-carbon patent outputs, while low-quality innovations are phased out as they cannot reduce emissions per unit of output. On this basis, the following hypothesis is proposed:

H1

Carbon trading can effectively enhance the technological innovation level of enterprises.

The government and the market are the two main means of resource allocation31, and the theory of market failure argues that it is impossible to achieve Pareto optimality by relying only on the price mechanism to allocate resources, which provides a theoretical basis for government intervention32. The government is an important contributor to solving market failure, but in carbon trading and corporate innovation, government intervention may have positive and negative effects. On the one hand, government intervention can promote compliance and incentivise firms to engage in technological innovation. Since China’s carbon market system has not been fully established, there may be carbon leakage and a ‘pollution paradise’ effect33, and government supervision is needed to ensure that the inefficiently operated carbon market maintains a high rate of compliance. From the perspective of technological innovation, government policy is particularly important because of the high-risk characteristics of technological innovation behaviour, the lack of initiative of enterprises in technological innovation, and the difficulty of achieving technological progress through market mechanisms alone. The government can provide enterprises with a variety of guidance and support, including financial support, as well as a more efficient and stricter regulatory environment34, and regulatory pressure may influence the layout and adjustment of the industrial structure, enhance technological innovation35, and promote fair and equitable carbon trading.

On the other hand, government intervention may be characterised by ‘government failure’ due to incomplete information and weak monitoring. Firms may invest in low-quality patenting activities to obtain policy subsidies36, and many firms may choose to apply for low-cost, low-quality patents rather than improve patent quality37. The inability to distinguish between outcome and process assessments at the government review stage leads government officials to place greater emphasis on the number of observable patent applications, thus exacerbating policy distortions and leading to patent bubbles. Many low-quality enterprises that do not have the ability to innovate disguise themselves as targets for policy incentives through ‘packaging’, and to obtain policy incentives, they intentionally cater to the requirements of the policy to seize the policy support quota, which makes it difficult for truly high-quality enterprises to obtain funding and thus results in a distortion of the policy objectives. On this basis, the following research hypothesis is proposed:

H2

Government intervention can play a synergistic role in influencing the level of technological innovation of enterprises.

Models, data and methods

Models and variables

The main trading organisations in the carbon trading market are priority emission units (emission-control enterprises), and according to the provisions of the carbon trading market, enterprises entering the carbon trading market are allocated carbon emission quotas by the government at the initial stage. Therefore, under the carbon trading market framework, we use whether enterprises are included in the priority emission list for carbon trading as a quasinatural experiment. We use the DDD model to investigate the impact of carbon trading on firms’ technological innovation. The difference-in-differences (DID) and DDD methods are common approaches used for policy evaluation. The DID model, while able to assess the causal facilitation effect of a policy by stripping out the dispositional effects of the policy by eliminating confounding factors that are not time-varying and unobservable, may be unable to eliminate the interference of other policy interventions during the pilot period as well as the time-varying regional characteristics. For this reason, we use the DDD model to exclude factors that are not time-varying, unobservable, or outside of the pilot policy and to refine the causal facilitation effect of carbon trading on firms’ technological innovation.

The manufacturing sector is the most important major energy consumption category in China. According to China Energy Statistics, the energy consumption of the manufacturing sector in 2021 was 2931 million tonnes of standard coal, accounting for 55.94% of China’s total energy consumption. Considering the dual goals of carbon emission reduction and economic development, China’s manufacturing sector faces enormous pressure to save energy and reduce emissions, and manufacturing companies may be forced to shut down production because of excessive emissions or high energy costs38. Since carbon trading puts much more pressure on manufacturing firms to reduce carbon emissions than nonmanufacturing firms do, in addition to controlling for time and group effects, we use the DDD model to further control for industry differences, and the model is constructed as follows. In this model, \(\:{Innovation}_{iktj}\) represents the level of technological innovation of the sample firms, both quantitatively and qualitatively.

In this model, the subscript i represents the firm, and t represents the year. treat is a grouping dummy variable, portraying the difference between the experimental group and the control group, with the experimental group of emission control enterprises participating in carbon trading taking the value of 1, and the control group of enterprises not participating in carbon trading taking the value of 0. Post is a dummy variable for the experimental period, portraying the difference between the enterprises before and after they enter the carbon trading market and the difference between the enterprises before and after entering the carbon trading market, with the value of 1 taken when the financial year is later than that of the year when they are included in the list of the national key emission enterprises in the first time of carbon trading; otherwise, it is 0. Production is an industry attribute indicator, which takes a value of 1 if it belongs to the manufacturing industry; otherwise, it is 0. \(\:{treat}_{i}\times\:{post}_{t}\times\:\:{production}_{k}\) is the key variable in the DDD model, which truly measures the innovation incentive effect of the experimental group subjected to carbon trading.

Quantity of technological innovations (quantity). Corporate technological innovation is measured based on patent information; we use the number of patents granted per sample firm as a proxy variable for innovation.

Quality of technological innovation (quality). The number of patent citations can reflect the degree of patent innovation and knowledge transfer path and is one of the earliest indicators used to evaluate the quality of patents; however, it is also one of the more classic indicators, important and reasonable indicators, which have been continuously proven in the subsequent period39. Therefore, we use the number of citations of patents to measure the quality of technological innovation. Owing to the potential for ‘tailing off’ in patent citations, we use citations within five years of patent filing as a proxy variable for innovation quality as well.

Control variables (control). We select company financial indicators, including research staff ratio, R&D expense ratio, ROE, ROA, etc. \(\:{\rho\:}_{i}\) is the Firm fixed effect, \(\:{\sigma\:}_{t}\) is the year fixed effect, and τiktj is the random disturbance term.

Data

We use patent-related data from the Wingo database and PatSnap global patent database and corporate financial data from the Wind database. The sample period selected is from 2010 to 2021, because the core explanatory variable of innovation quality is the citations of patents within 5 years, and we need a five-year observation period. and the following treatments are applied to the enterprise data: (1) delete ST and *ST enterprises; and (2) delete companies with zero patents in the sample period. To reduce the impact of outliers on the regression, this paper performs bilateral shrinkage at the 1% and 99% quartiles of the relevant sample data, obtaining 16,912 observations. The relevant variables are shown in Table 1.

Empirical results and discussion

Baseline test

The results of the DDD model are shown in Table 2. Column (1) reports the changes in the quantity of corporate technological innovation, and Columns (2) and (3) report the changes in the quality of innovation of manufacturing firms after they participate in carbon trading. First, the coefficient of the variable \(\:{treat}_{i}\times\:{post}_{t}\times\:\:{production}_{k}\) in Column (1) is insignificant, whereas the coefficients of the variables in Columns (2) and (3) are significantly positive, indicating that, compared with nonmanufacturing firms, manufacturing firms do not experience a significant change in the number of their patent applications after they participate in carbon trading. However, there is a significant increase in the number of patent citations and the number of patent citations within five years, which suggests that carbon trading does not increase the quantity of innovation of manufacturing firms, but it significantly increases the quality of their innovation. It can be found that RD_P coefficient is significantly negative, and RD_S coefficient, ROA coefficient and Cost coefficient are significantly positive, indicating that when manufacturing enterprises participate in carbon trading, management expenses and R&D investment continue to rise. Under cost pressure, R&D personnel investment is reduced slightly, and return on assets is improved, thus promoting the improvement of innovation quality.

To encourage innovation, Chinese governments at all levels support corporate technological innovation mainly through financial subsidies and other incentive policies. Under the premise of information asymmetry between the government and enterprises on the real quality of patents, these innovation support policies usually provide partial or full funding based on the number of patents applied for or granted by enterprises. This induces and motivates enterprises to cater to relevant policies through low-quality or even worthless patents to make profits, thus resulting in an overall decline in the quality of Chinese enterprises’ patents, especially the quality of patent applications, which has led to the problem of innovation bubbles and the illusion of innovation. Carbon trading follows the Coase theorem, the core of which is to use the market economy to solve the problem of carbon emissions. Emission-control enterprises save carbon quotas through a series of measures and trade them, thereby overcoming the problem of carbon emission externalities; thus, carbon trading can prompt enterprises to incorporate carbon emission reduction into their decision-making, force them to realise energy savings and emission reduction through corporate technological innovation, and benefit from the market mechanism.

Robustness tests and endogeneity treatment

Parallel trend test

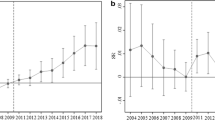

Our benchmarking results show that carbon trading significantly contributes to improving the quality of innovation in manufacturing enterprises. The prerequisite for the validity of the DDD model is to satisfy the parallel trend assumption that the trend of change in the treatment group and the control group should be the same before they are admitted to the carbon trading market.

The results of the parallel trend test for the variable quality are shown in Fig. 2, and the results of the parallel trend test for quality_5 are shown in Fig. 3. The results show that the confidence intervals of the period before enterprises are included in the carbon trading market are 0, and the coefficient estimation is not significant, which indicates that there is no significant systematic difference between the experimental and control groups before they are included in the carbon trading market and that it meets the assumption of a parallel trend. After the enterprises entered the carbon market, the confidence interval gradually shifted from 0, and the coefficient estimate was positive and significant, which further verified the robustness of the baseline regression test results, indicating that carbon trading can significantly encourage manufacturing enterprises to improve the quality of innovation.

Parallel trend test for quality.

Parallel trend test for quality_5.

Placebo test

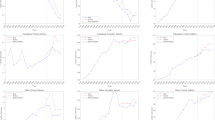

In addition to the impact of carbon trading, the quality of firms’ innovations may be affected by other policies or unobservable random factors, and to rule out such effects, this paper constructs counterfactual events for the placebo test via the methodology from scholars such as Abadie and Gardeazabal40. In this paper, 50% of the sample firms are randomly selected from the sample as the fictitious experimental group, and the remaining 50% are automatically categorised as the fictitious control group. Since the fictitious experimental group is randomly generated, the fictitious interaction term theoretically has no significant effect on the model explanatory variables.

To avoid interference from other small probability events on the estimation results, the random shock process is repeated 300 times in this paper. Figures 4 and 5 show the results of the placebo test for the variables quality and quality_5, indicating that the values of the core coefficients of the DDD set over the 300 random shocks are indeed concentrated around zero. After further plotting the p values, most of the estimated coefficients have p values greater than 0.1, suggesting that most of the placebo estimated coefficients are insignificant, whereas the coefficients of \(\:{treat}_{i}\times\:{post}_{t}\times\:\:{production}_{k}\) in the baseline regressions of 0.871 and 0.67 are outside of the range of simulated coefficients for the simulation of 300 occasions. This suggests that our conclusions are not consistent with chance unobserved factors. This can be inferred from the fact that ‘fictitious inclusion in carbon trading lists’ does not have a significant effect on the quality of firms’ innovations.

Placebo testing for quality.

Placebo testing for quality_5.

Supplementary robustness test

We conduct supplementary robustness tests using two methods. First, we modify the proxy variable for innovation quality. Patents are typically categorized into invention patents, utility model patents, and design patents, with invention patents being the most innovative and valuable. Thus, the number of invention patents can serve as a proxy for the innovation quality of enterprises. In the robustness test, we use two measures: the total number of invention patents (ipatent_1) and the number of invention patents approved within one year (ipatent_2) to represent innovation quality. The regression results are presented in Table 3 columns (1) and (2). Second, we shorten the sample period by excluding the year 2020, during which China was significantly impacted by the COVID-19 pandemic. The experiment is then repeated with the data excluding 2020, and the results are shown in columns (3) to (5). The robustness test results are consistent with the baseline regression, confirming the reliability of our findings.

Endogenous processing

To address the possible endogeneity problem between manufacturing firms’ participation in carbon trading and their technology, this paper adopts two options. First, the combination of propensity score matching (PSM) and DDD is adopted; PSM can solve the endogeneity problem arising from sample selection bias, and DDD can avoid the endogeneity problem arising from the omission of variables. Second, the instrumental variables approach is further used to overcome the effect of endogeneity as much as possible.

-

(1)

PSM - DDD

First, to solve the endogeneity problem caused by sample selection bias, we use PSM to match emission control firms with similar characteristics in multiple dimensions to obtain a control group and then use the DDD model to obtain the net effect excluding the influence of other covariates. The specific procedures are as follows. (1) Calculate the propensity score value (Pscore). To establish a regression model, the dependent variable is a dummy variable, the treatment group is set to 1, and the control group is set to 0. The independent variable is the number of evaluations of the similarity of the two groups of indicators, which include the following control variables, to calculate the probability of a certain enterprise as a treatment group, i.e., the Pscore. (2) According to the Pscore, for each enterprise determined to be a treatment group, find the enterprise from the control group that has the closest similarity to the Pscore as a control group. as the control group. To further compare the effects before and after propensity score matching, this paper also plots the kernel density before and after matching, as shown in Figs. 6 and 7.

Kernel density before matching.

Kernel density after matching.

As shown in Fig. 6, the probability density distributions of the experimental group and the control group before propensity score matching are relatively large, and the distributions of the two are basically similar, as shown in Fig. 7, which also confirms the better effect of propensity score matching. In this paper, the propensity score matching method can better solve the problem of selection bias that may exist in the triple difference model. Using PSM matching after the sample for regression analysis, the test results of the DDD model are shown in Table 4, which are consistent with those of the benchmark regression; thus, our empirical conclusions are robust.

-

(2)

Instrumental variable test

For the instrumental variable method, we used the frequency of inversions as an instrumental variable, with data from the National Aeronautics and Space Administration (NASA) of the United States. The reasons for choosing this instrumental variable are as follows. First, inversions indicate an anomaly in the atmospheric structure above the ground where the temperature increases with height, which is not conducive to the transport and dispersion of pollutants from the near-surface layer to higher altitudes or even farther away, thus leading to an increase in the level of air pollution in the region. Therefore, the greater the frequency of inversions is, the stricter the environmental regulations, and the greater the probability of establishing a carbon trading market in the region, which is in line with the correlation hypothesis of instrumental variables. Second, the frequency of inversions is determined by meteorological and geographical conditions and can meet the exogeneity assumption of the instrumental variables. As shown in Column (1) of Table 5, in the first stage of the test, the positive significance of the instrumental variables confirms the correlation hypothesis of the instrumental variables, and the F value of the first stage is 53.26, which indicates that there is no weak instrumental variable problem. In the second stage, as shown in Columns (2) and (3), after the endogeneity problem is mitigated, the test results remain consistent with the baseline regression results.

Marginal effect test

The linear regression results show that overall, manufacturing firms’ participation in carbon trading significantly improves the quality of innovation. However, theoretically, the extent to which firms are affected by carbon trading varies depending on where they are in their different stages of innovation. Based on the benchmark regression, this chapter further explores the average effect of carbon trading at different stages of development of firms’ innovation. The fixed effects term in traditional panel quantile models decomposes the random perturbation term into distinct parts, which makes it difficult to interpret the estimation results for each quantile. Powell (2022) proposed a nonadditive fixed effects panel quantile model (QRPD) that uses intraindividual variation for identification so that the random perturbation term includes fixed effects, which ensures that the random perturbation term is not separable41. Thus, the advantage of the QRPD model over the traditional panel quantile model is that the estimated coefficients are more accurate, and the estimates are more robust. In this paper, the panel quantile function model of the QRPD is constructed as follows:

where τ denotes the corresponding quantile and where \(\:{Innovation}_{iktj}\) indicates the level of innovation under the corresponding quartile. In the QRPD model, the regression coefficients at quantile τ describe the effects of the explanatory variables on the explanatory variables at quantile τ rather than describing the effects of the explanatory variables under the control variable conditions. We visualise the marginal effects of carbon trading by plotting the coefficients and 95% confidence intervals of θ(τ) at different stages of development of firms’ innovation quality, thus demonstrating the marginal effects of carbon trading in detail.

As shown in Fig. 8, when using the number of patent citations as the measurement standard, the coefficients across all quartiles are positive, and the 95% confidence intervals do not include zero. This suggests that carbon trading significantly promotes the increase in patent citations for manufacturing enterprises at various stages of innovation and development. Given that the number of citations tends to increase over time, we focus particularly on citations within five years of patent issuance. As illustrated in Fig. 9, the coefficient of θ(τ) is positive for quartiles above 60%, initially rising and then decreasing. The 95% confidence interval again does not include zero, indicating that carbon trading has the greatest impact on enhancing innovation quality for manufacturing enterprises in the mid-stage of their innovation development. Moreover, the effect of carbon trading diminishes as the enterprise’s innovation moves toward the maturity stage.

Quality quartile regression results.

Quality_5 quartile regression results.

Synergistic effect of government intervention

The compliance behaviour of emission controllers in China’s carbon market is not only based on the carbon trading incentive mechanism but also subject to government administrative control, which may be reflected in the government’s direct supervision of emission controllers’ compliance through government intervention in the carbon market. Corporate compliance behaviour is not only based on carbon trading market incentives but also on government regulation and policy incentives. Since 1978, the Chinese government has been committed to various types of environmental governance work and has achieved certain results. It has gradually formed a diversified environmental regulation system with Chinese characteristics, which is mainly based on government administrative directives and combines market-oriented methods, providing policy guarantees for environmental quality improvement and green economic growth42. Therefore, we select the degree of attention to the environmental governance of each regional government to explore the impact of government intervention on the carbon trading mechanism to promote corporate technological innovation.

Considering the degree of importance attached to environmental governance by the government (Env), the proportion of the frequency of words related to the term ‘environmental protection’ in the local government work reports from 2010 to 2021 to the number of words in the full reports is used as a proxy variable for environmental governance. The results are shown in Columns (1) to (3) of Table 6. The coefficients of the cross-multiplier terms are significantly positive, indicating that the government’s environmental governance significantly strengthens the effect of the carbon trading mechanism in improving corporate technological innovation. This is not only reflected in the performance of innovation quality, but also can be found that under the condition of high government environmental governance, the number of enterprise innovation is also significantly increased. Carbon emissions, as enterprise behaviour with negative externalities, require the government to play a synergistic role in government intervention to compensate for ‘market failure’, and when faced with the pressure of carbon emission reduction, the government can ensure the compliance of emission-control enterprises through the functions of guidance and supervision.

Heterogeneity analysis

Although we have demonstrated the effectiveness of the carbon trading market in enhancing the quality of corporate innovation, there may be some differences in the response to policy shocks between the internal environment of different firms and the external environment within the pilot scope. Therefore, this paper discusses the heterogeneity of the effects of carbon trading on corporate technological innovation from the aspects of firms’ internal and external characteristics.

Analysis of enterprise size

To investigate the differential impact of company size, we categorize the sample based on the median of firm asset size into large and small enterprises. The results are shown in Table 7, where columns (1) to (3) represent the results for small firms, and columns (4) to (6) represent the results for large firms. It can be observed that large manufacturing firms experience a significant improvement in innovation quality after participating in carbon trading, whereas this effect is not significant for small manufacturing firms.

This disparity can be attributed to several factors. First, large firms typically have advantages in terms of capital and resources, which provide them with greater financial support for innovation activities. Second, large firms may benefit from economies of scale, enabling them to optimize costs, which can be further reinvested into technological innovation, thereby enhancing innovation quality. Finally, large firms often face greater social responsibility and regulatory pressures. In response to carbon trading policies and market changes, they are more inclined to invest in technological innovations that align with future development trends. In contrast, small enterprises are more likely to face challenges such as financial constraints, insufficient technological reserves, and limited managerial and organizational capabilities. Although the carbon trading mechanism offers market incentives, it is the large enterprises, with their advantages in resources, capital, and technology, that are better positioned to leverage these incentives to improve innovation quality. Small firms, on the other hand, may struggle to fully capitalize on the innovation potential offered by carbon trading due to resource limitations.

Analysis of the nature of the industry

Corporate technological innovation is the basic force driving the development of technological innovation. Because technological innovation exists in the technology itself and information asymmetry of the double risk, technological enterprises are faced with financing difficulties, and there may be a lack of incentive to innovate and a greater need for the stimulating effect of market-type environmental regulation. To verify the heterogeneous impact of carbon trading on the technological innovation of high-tech manufacturing enterprises and nonhigh-tech enterprises, we define high-tech industries in this paper according to the high-tech fields stipulated in China’s ‘Administrative Measures for the Recognition of High-tech Enterprises’, corresponding to the broad categories of the ‘Guidelines for the Industry Classification of Listed Enterprises’ revised by the Securities and Exchange Commission in 2012, as shown in the Appendix B. The regression results are shown in Table 8, with Columns (1) to (3) reporting the regression results for high-tech manufacturing firms and Columns (4) to (6) reporting the regression results for nonhigh-tech firms. Compared with that of nonhigh-tech manufacturing firms, the quality of innovation significantly improves in high-tech manufacturing firms after they participate in carbon trading, whereas this effect is not significant in nonhigh-tech firms.

One of the important purposes of carbon trading is to incentivise corporate technological innovation in pollution control, whereas technology enterprises, as the basic force driving the development of technological innovation, are more likely to be stimulated by market-based environmental regulation to carry out technological innovation in pollution control and achieve technological progress. China’s high-tech manufacturing industry, stimulated by carbon trading, has significantly improved the quality of its innovation, although the quantity of its innovation has not changed significantly, which has effectively suppressed the innovation bubble phenomenon.

Research conclusions

Using Chinese corporate patent data and financial data from 2010 to 2021, this paper uses the DDD model to analyse the causal relationship between carbon trading and corporate technological innovation in manufacturing companies and demonstrates the inhibitory effect of manufacturing companies’ participation in carbon trading on innovation bubbles, considering the synergistic effect of government intervention.

The study conclusions are as follows. (1) The participation of manufacturing enterprises in carbon trading increases their R&D investment, which does not increase the quantity of innovation but significantly improves the quality of innovation, thus suppressing the emergence of innovation bubbles. This phenomenon is closely related to the fact that carbon trading can internalise the problem of carbon emission externalities, and this conclusion is still valid after the parallel trend test, placebo test, propensity score matching, and instrumental variable method. (2) The analysis of the marginal effect shows that carbon trading has the greatest effect on the improvement of innovation quality in the middle stage of the innovation development of manufacturing enterprises, and the effect of carbon trading gradually diminishes as enterprise innovation moves towards the maturity stage. (3) The compliance behaviour of emission control subjects in China’s carbon market is not only based on the carbon trading incentive mechanism but also subject to the government’s administrative control. Under the synergistic effect of China’s market mechanism and the government’s intervention, the carbon trading mechanism can enhance the quality of corporate technological innovation more effectively. (4) Heterogeneity analysis reveals that the impact of carbon trading on corporate technological innovation is more significant for large enterprises and high-tech manufacturing enterprises.

Based on the above analysis, we propose the following policy recommendations. First, deepen the development of China’s carbon market system, with a focus on strengthening the positive driving effect of carbon trading mechanisms on technological R&D in the manufacturing sector. This involves establishing a market-incentive-oriented pathway for technological innovation transmission and fostering a sustainable innovation ecosystem. Second, at the policy framework design level, it is essential to dynamically balance the relationship between government guidance and market autonomy. By creating a synergistic model that integrates government regulation with market mechanisms, the carbon pricing system should gradually evolve from policy-driven to market-led. This approach will harness institutional synergies to stimulate innovation vitality. Finally, prioritize leading enterprises and high-tech manufacturing firms to deepen their participation in the carbon market, particularly by guiding them to internalize carbon costs into their innovation strategies. By enhancing the precision and continuity of R&D investments, inefficient innovation inputs can be effectively curbed, thereby achieving simultaneous improvements in innovation quality and risk resilience.

We analyse the impact of carbon trading on corporate technological innovation in manufacturing firms as comprehensively as possible within the existing data conditions and research methodology, using a variety of robustness tests and endogeneity treatments, supplementing the empirical evidence on this research question and considering the synergistic effect of government intervention. With the increasing maturity of China’s carbon trading market, we can consider the spatial effect and diffusion mechanism through which carbon trading affects corporate innovation and look for a more suitable econometric model for this research question. Therefore, this issue needs further in-depth research.

Data availability

The data can be obtained from the corresponding author upon request. The calculated data used to support the findings of this study are included within the article.

References

He, L., Zhong, T. & Gan, S. Green finance and corporate environmental responsibility: Evidence from heavily polluting listed enterprises in China. Environ. Sci. Pollut. Res. 29(49), 74081–74096 (2022).

Porter, M. E. & Linde, C. V. D. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9(4), 97–118 (1995).

Liu, L., Chen, C., Zhao, Y. & Zhao, E. China׳ s carbon-emissions trading: Overview, challenges and future. Renew. Sustain. Energy Rev. 49, 254–266 (2015).

Zhu, J., Fan, Y., Deng, X. & Xue, L. Low-carbon innovation induced by emissions trading in China. Nat. Commun. 10(1), 4088 (2019).

Wang, X. Q., Su, C. W., Lobonţ, O. R., Li, H. & Nicoleta-Claudia, M. Is China’s carbon trading market efficient? Evidence from emissions trading scheme pilots. Energy 245, 123240 (2022).

Yang, L., Li, F. & Zhang, X. Chinese companies’ awareness and perceptions of the emissions trading scheme (ETS): Evidence from a national survey in China. Energy Policy 98, 254–265 (2016).

Zhao, X. G., Wu, L. & Li, A. Research on the efficiency of carbon trading market in China. Renew. Sustain. Energy Rev. 79, 1–8 (2017).

Coase, R. H. The problem of social cost. J. Law Econ. 3, 1–44 (1960).

Rogge, K. S., Schneider, M. & Hoffmann, V. H. The innovation impact of the EU emission trading system—Findings of company case studies in the German power sector. Ecol. Econ. 70(3), 513–523 (2011).

Zhang, C., Wang, Q., Shi, D., Li, P. & Cai, W. Scenario-based potential effects of carbon trading in China: An integrated approach. Appl. Energy 182, 177–190 (2016).

Liu, B., Ding, C. J., Hu, J., Su, Y. & Qin, C. Carbon trading and regional carbon productivity. J. Clean. Prod. 420, 138395 (2023).

Tan, R. & Lin, B. The long term effects of carbon trading markets in China: Evidence from energy intensive industries. Sci. Total Environ. 806, 150311 (2022).

Zhou, C. & Qi, S. Has the pilot carbon trading policy improved China’s green total factor energy efficiency?. Energy Econ. 114, 106268 (2022).

Shi, B., Li, N., Gao, Q. & Li, G. Market incentives, carbon quota allocation and carbon emission reduction: Evidence from China’s carbon trading pilot policy. J. Environ. Manag. 319, 115650 (2022).

Yu, X., Shi, J., Wan, K. & Chang, T. Carbon trading market policies and corporate environmental performance in China. J. Clean. Prod. 371, 133683 (2022).

Zhou, J., Huo, X., Jin, B. & Yu, X. The efficiency of carbon trading market in China: Evidence from variance ratio tests. Environ. Sci. Pollut. Res. 26, 14362–14372 (2019).

Petroni, G., Bigliardi, B. & Galati, F. Rethinking the Porter hypothesis: The underappreciated importance of value appropriation and pollution intensity. Rev. Policy Res. 36(1), 121–140 (2019).

Zhang, W., Li, G. & Guo, F. Does carbon emissions trading promote green technology innovation in China?. Appl. Energy 315, 119012 (2022).

Lyu, X., Shi, A. & Wang, X. Research on the impact of carbon emission trading system on low-carbon technology innovation. Carbon Manag. 11(2), 183–193 (2020).

Wang, C., Wang, L., Wang, W., Xiong, Y. & Du, C. Does carbon emission trading policy promote the corporate technological innovation? Empirical evidence from China’s high-carbon industries. J. Clean. Prod. 411, 137286 (2023).

Liu, M., Shan, Y. & Li, Y. Study on the effect of carbon trading regulation on green innovation and heterogeneity analysis from China. Energy Policy 171, 113290 (2022).

Li, C., Li, X., Song, D. & Tian, M. Does a carbon emissions trading scheme spur urban green innovation? Evidence from a quasi-natural experiment in China. Energy Environ. 33(4), 640–662 (2022).

Borghesi, S., Crespi, F., D’Amato, A., Mazzanti, M. & Silvestri, F. Carbon abatement, sector heterogeneity and policy responses: Evidence on induced eco innovations in the EU. Environ. Sci. Policy 54, 377–388 (2015).

Mandaroux, R., Schindelhauer, K. & Mama, H. B. How to reinforce the effectiveness of the EU emissions trading system in stimulating low-carbon technological change? Taking stock and future directions. Energy Policy 181, 113697 (2023).

Guo, B., Feng, Y. & Hu, F. Have carbon emission trading pilot policy improved urban innovation capacity? Evidence from a quasi-natural experiment in China. Environ. Sci. Pollut. Res. 31(7), 10119–10132 (2024).

Jia, L. et al. Impact of carbon emission trading system on green technology innovation of energy enterprises in China. J. Environ. Manag. 360, 121229 (2024).

Ren, S., Yang, X., Hu, Y. & Chevallier, J. Emission trading, induced innovation and firm performance. Energy Econ. 112, 106157 (2022).

Chen, Z., Zhang, X. & Chen, F. Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technol. Forecast. Soc. Change 168, 120744 (2021).

Jaffe, A. B. & Stavins, R. N. Dynamic incentives of environmental regulations: The effects of alternative policy instruments on technology diffusion. J. Environ. Econ. Manag. 29(3), S43–S63 (1995).

Yan, Y., Zhang, X., Zhang, J. & Li, K. Emissions trading system (ETS) implementation and its collaborative governance effects on air pollution: The China story. Energy Policy 138, 111282 (2020).

Wang, K. L., Zhao, B., Ding, L. L. & Miao, Z. Government intervention, market development, and pollution emission efficiency: Evidence from China. Sci. Total Environ. 757, 143738 (2021).

Choi, J. & Lee, J. Repairing the R&D market failure: Public R&D subsidy and the composition of private R&D. Res. Policy 46(8), 1465–1478 (2017).

Ying, J. J. & Sovacool, B. K. A fair trade? Expert perceptions of equity, innovation, and public awareness in China’s future emissions trading scheme. Clim. Change 164(3), 31 (2021).

Han, Y., Zhe, C. & Liu, X. Is the carbon emissions trading system conducive to the urban green technology innovation level? Evidence from China. Energy Rep. 9, 3787–3799 (2023).

Liu, C., Ma, C. & Xie, R. Structural, innovation and efficiency effects of environmental regulation: Evidence from China’s carbon emissions trading pilot. Environ. Resour. Econ. 75, 741–768 (2020).

Guellec, D. & Van Pottelsberghe De La Potterie, B. The impact of public R&D expenditure on business R&D. Econ. Innov. New Technol. 12(3), 225–243 (2003).

Wang, H., Qi, S., Zhou, C., Zhou, J. & Huang, X. Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 331, 129834 (2022).

Wang, M., Wang, X., Liu, Z. & Han, Z. How can carbon trading promote the green innovation efficiency of manufacturing enterprises?. Energy Strat. Rev. 53, 101420 (2024).

Wagner, S. & Wakeman, S. What do patent-based measures tell us about product commercialization? Evidence from the pharmaceutical industry. Res. Policy 45(5), 1091–1102 (2016).

Abadie, A. & Gardeazabal, J. The economic costs of conflict: A case study of the Basque Country. Am. Econ. Rev. 93(1), 113–132 (2003).

Powell, D. Quantile regression with nonadditive fixed effects. Empir. Econ. 63(5), 2675–2691 (2022).

Jingrong, D. et al. Analysis of the influence and coupling effect of environmental regulation policy tools on industrial green and low-carbon transformation. Sci. Rep. 14(1), 25873 (2024).

Funding

This research was funded by the China Scholarship Council [grant number CSC202306540099 and CSC202206540066] and Qinghai Province Philosophy and Social Sciences Planning Project [Grant Number: 25QN063].

Author information

Authors and Affiliations

Contributions

Study conception and design: Guocheng LI; writing—original draft, Ziwei Lyu; writing—review & editing, Guocheng LI; funding acquisition, Ziwei Lyu. The above authors contributed equally to this work and should be considered co-first authors. All authors reviewed the results and approved the final version of the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

No human participants were involved in the study. All authors listed have approved the attached manuscript.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Lyu, Z., Li, G. The impact of carbon emissions trading on innovation bubbles in manufacturing enterprises. Sci Rep 15, 43499 (2025). https://doi.org/10.1038/s41598-025-99814-y

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s41598-025-99814-y