Abstract

Informal financing methods like trade credit have emerged as a key approach to ease corporate financial constraints. Based on the data of A-share listed manufacturing companies from 2011 to 2019, we empirically investigate the influence and mechanism of industrial robot adoption on a firm’s trade credit. The findings show that the industrial robot adoption enhances a firm’s trade credit, specifically functioning through strengthening the firm’s supply chain resilience, enhancing operational efficiency, and easing financing constraints. Further analysis shows that the impact is more pronounced in firms with a higher degree of technical matching, in non-SOEs, and in firms facing fierce competition. Our study broadens the understanding of how artificial intelligence is reshaping corporate financial behavior. It supplements the literature on the firm-level economic consequences of industrial robot adoption and the influencing factors of trade credit. The study also holds important practical implications for cultivating high-quality productivity and empowering corporate high-quality development.

Similar content being viewed by others

Introduction

With the rapid advancement of artificial intelligence (AI) technology, its application has become one of the core driving forces for the global economic transformation and innovation (Zhang, 2023; Makridakis, 2017). At the firm level, AI adoption significantly enhances production efficiency, optimizes operational processes, and strengthens firms’ financial performance and competitiveness (Liang et al., 2023). As a typical manifestation of AI in manufacturing, industrial robots, with their high precision and strong flexibility, are not only the core of intelligent manufacturing but also provide a key path for firms to improve quality and efficiency (Zhao et al., 2022; Wang et al., 2024). This technological transformation is especially critical for China’s manufacturing industry. Although China has become a global manufacturing power, its manufacturing sector has long faced the dual challenges of “low−end lock−in” and the weakening of labor cost advantages (Zhang and Wang, 2025; Xiao et al., 2020). Adopting advanced technologies such as industrial robots to achieve automation and intelligent transformation has become an inevitable choice for Chinese firms to break through bottlenecks and build competitiveness.

Nowadays, the industrial robotics market in China achieved strong growth with a new record of 243,300 installations in 2021, with a rise of 44% compared to the previous yearFootnote 1. China provides an ideal setting to examine the economic consequences of industrial robot adoption. It features a unique combination of large-scale traditional industries and rapidly developing high-tech sectors, along with strong government involvement and significant regional heterogeneity. This unique setting enables an in-depth examination of how automation influences corporate behavior and transformation. Findings from China’s experience offer valuable insights into how industrial automation reshapes firm strategies and resource allocation in both emerging and developed economies.

Existing research has extensively examined how industrial robot adoption influences labor markets. The industrial robot adoption can reduce unit labor costs (Zhang et al., 2023) and increase new employment opportunities (Jung and Lim, 2020). Beyond the labor market, previous studies have primarily examined the effects of industrial robot adoption on firm’s value (Li et al., 2024), green innovation (Gan et al., 2023), and corporate misconduct behaviors (Bai et al., 2025; Zhou et al., 2024). However, there is limited research exploring the role of industrial robot adoption from the standpoint of corporate financing, especially trade credit. This research gap is particularly significant under China’s financial market structure.

As a financial system dominated by bank credit, many firms in China (especially private small and medium-sized enterprises) are confronted with severe credit rationing and financing constraints due to information asymmetry (Cheng and Yang, 2022). Compared to formal bank loans, trade credit, which is embedded in daily business operations, allows upstream and downstream partners to achieve short-term liquidity through accounts payable and prepayments, offering relatively lower costs (Petersen and Rajan, 1997). Against this backdrop, trade credit embedded in supply chains, as a crucial informal financing channel, is of paramount importance. We argue that robot adoption can strengthen firm’s supply chain reputation by promoting supply chain resilience and operational efficiency, thereby improving their access to trade credit financing. Ultimately, improving firm’s trade credit contributes to sustainable and high-quality corporate development. Therefore, this study aims to provide new insights into how AI is reshaping corporate financial behavior in emerging economies by investigating the relationship between robot adoption and trade credit, and also offer practical inspirations for optimizing financing and supply chain management in China’s manufacturing industry during its intelligent transformation.

Using a sample of China’s A-share manufacturing listed firms from 2011 to 2019, we investigate the effect and mechanism of industrial robot adoption on trade credit. Empirical findings show that the adoption of industrial robots significantly enhances a firm’s trade credit through three channels: strengthening supply chain resilience, improving operational efficiency, and mitigating financing constraints. Further analysis shows that this impact is more pronounced in firms with higher technological compatibility, non-state-owned enterprises (non-SOEs), and industries with intense competition.

Compared to existing literature, our paper’s marginal contributions are as follows:

First, we construct a theoretical framework encompassing supply chain resilience, operational efficiency, and financing constraints to systematically elucidate the mechanisms through which industrial robot adoption affects a firm’s trade credit. Our study broadens the understanding of how technological transformation extends beyond internal production outcomes to influence firms’ financial relationships. Our research further provides comprehensive heterogeneity analysis based on CEO background, company type, and market environment. Such mechanistic and contextual investigation offers a more complete and contextualized understanding than prior studies that primarily examined how industrial robots affect firms’ innovation activities, labor allocation, and firm value (Gan et al., 2023; Jung and Lim, 2020; Li et al., 2024). Moreover, compared with existing research focusing on the relationship between robots and trade credit (Mao et al., 2024), we not only identify but empirically show the underlying channels, thereby extending the research boundaries on the firm−level economic consequences of emerging technologies from a supply chain finance perspective.

Second, our study enriches the literature on the determinants of a firm’s trade credit by introducing industrial robot adoption as an important explanatory factor. Existing research emphasizes internal and external governance mechanisms (Fisman and Love, 2003; Fabbri and Klapper, 2016; El Ghoul and Zheng, 2016; Abdulla et al., 2017). We contribute to this research stream by demonstrating that technology-driven operational strategies, particularly those enabled by industrial robots, play a significant role in shaping trade credit decisions. This perspective highlights that trade credit provision is not merely a function of governance and financial constraints but is also closely linked to technological upgrading.

Third, our paper also has important practical implications. Our research enhances the understanding of the relationship between artificial intelligence and corporate financing from the perspective of supply chain finance. We provide a mechanistic and contextual analysis of how industrial robot adoption shapes a firm’s trade credit, deepens the understanding of the role of AI in firms’ production processes, and clarifies how industrial robot adoption shapes firms’ financing behavior. These insights offer empirical evidence for policymakers to cultivate high-quality productive forces and provide theoretical guidance for firms to better harness the positive effects of AI and optimize technology−driven strategies.

The remainder of this paper is structured as follows: “Theoretical analysis and hypothesis” presents the theoretical analysis and develops our hypothesis. “Research design” outlines the research design. “Empirical results” presents the empirical findings, including the main regression results, robustness checks, and mechanism tests. “Cross-sectional analysis” provides cross−sectional analysis. “Conclusion” concludes the study.

Theoretical analysis and hypothesis

In the context of China’s economic transition, firms facing financing constraints increasingly rely on trade credit, a lower−cost alternative to formal bank loans, to secure short-term liquidity and avoid cash flow disruptions (Wang et al., 2021). Suppliers’ willingness to extend trade credit largely depends on buyers’ bargaining power (Fabbri and Klapper, 2016), such as a firm’s operational stability, governance quality, and capacity to mitigate risks. At the same time, among upstream and downstream firms, factors such as information sharing among suppliers, operational efficiency, and the improvement of their ability to withstand external shocks play a crucial role in trade credit (Allen et al., 2019).

The adoption of industrial robots significantly strengthens firms’ operational capabilities, risk resilience, innovation potential, and market competitiveness (Ralston and Blackhurst, 2020). Meanwhile, a firm’s technological upgrade sends strong positive signals to all participants within the supply chain ecosystem, reinforcing the perception of sustained growth and stability. This dual effect manifests as follows:

On the one hand, the firm’s adoption of industrial robots enhances suppliers’ confidence. Suppliers are more willing to offer trade credit when encouraged by the reduced operational uncertainties, increased productivity, and innovation of robot-adopting firms. This credit is a sign of trust in the company’s stability and future prospects.

On the other hand, supply chain partners, recognizing the benefits and innovative capacity of robot-adopting firms, are inclined to establish closer trade credit links. Prior researches show that supply chain partners align their interests together through extending trade credit (Bentley et al., 2013; Fisman and Raturi, 2004). They not only foster closer collaboration but also participate in and benefit from the innovative advances and efficiency gains achieved through robot adoption. This aligns their interests and ultimately enhances the supply chain’s overall resilience and competitiveness.

Based on the above discussion, we propose the following hypothesis:

H1: The industrial robot adoption can significantly improve firm’s trade credit.

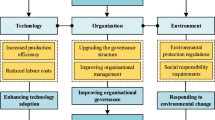

Specifically, firms adopting industrial robots can improve their ability to obtain trade credit mainly through the following channels. Our study’s conceptual framework is illustrated in Fig. 1.

Conceptual framework.

According to supply chain resilience theory (Soni et al., 2014), supply chain resilience encompasses not only the ability to manage disruption risks but also highlights the importance of a firm’s responsiveness and predictive capabilities. As a result, these related competencies directly influence how effectively a firm can obtain trade credit within the supply chain. The industrial robot adoption enhances corporate resilience, strengthening firm’s ability to respond to external disruptions and thereby increasing their access to larger-scale trade credit guided by dynamic capability theory (Teece et al., 1997).

On one hand, industrial robots enable rapid adaptation to changes in production processes, such as switching product models or adjusting output levels, allowing firms to flexibly address fluctuations in market demand (Rüßmann et al., 2015). This stability in production and operations safeguards supplier interests, reduces transaction risk, and increases trust among suppliers, ultimately reinforcing their willingness to extend trade credit.

On the other hand, industrial robots reduce reliance on manual labor amid labor shortages or rising labor costs. This not only helps firms sustain production during operational crises but also lowers costs and risks associated with workforce turnover (De et al., 2020). From a risk management perspective, industrial robots assist firms in better predicting and planning for potential production risks. Through real−time monitoring and data analytics, robots can promptly identify and address issues in production processes, minimizing the impact of unexpected events on operations (Cohen et al., 2019). Furthermore, industrial robot adoption eliminates the instability of manual production processes and reduces supervision requirements, resulting in significant improvements in the quality of products and services and mitigation of performance risk (Dixon et al., 2021). In conclusion, as default risk and transaction costs decline, suppliers are more willing to extend credit, thereby expanding the supply of trade credit. Besides, by improving production efficiency and reducing costs, industrial robot adoption helps firms achieve higher profit margins (Wilson and Daugherty, 2018). Such financial stability enables firms to maintain operations during economic volatility, ensuring suppliers can recover funds in a timely manner. In essence, firms with greater resilience are better positioned to guarantee suppliers’ financial security, thereby securing more favorable trade credit terms.

Based on this, we propose Hypothesis 2a:

H2a: The adoption of industrial robots enhances firm’s trade credit by improving supply chain resilience.

Industrial robots enhance firm’s productivity, improve delivery reliability, and reduce uncertainty in production processes (Gan et al., 2023), which builds firm’s competitive market advantages and strengthens their capacity to secure trade credit. Depending on the supply chain collaboration theory, suppliers can participate in cooperating with customers’ technological improvements through trade credit, form strategic alliances, and thereby enhance their own competitiveness. At the same time, prior research suggests that suppliers tend to select firms with superior business performance and stronger capabilities when forming alliances (Bentley et al., 2013; Fisman and Raturi, 2004).

Specifically, on one hand, robots excel at performing highly repetitive and precision-demanding tasks with uninterrupted operation, ensuring efficient and continuous production line workflows, thereby significantly boosting productivity (Leng et al., 2023). The automation of production lines through industrial robots also shortens production cycles, improves product quality, and reduces defect rates (Acemoglu and Restrepo, 2020). These improvements not only elevate a firm’s market competitiveness but also foster greater customer trust and market share, which in turn incentivizes suppliers to extend trade credit.

On the other hand, industrial robots drive innovation capabilities. With robotic assistance, firms can rapidly test new designs and production methods, accelerating product development cycles (Wang et al., 2021). Automation further reduces resource and energy consumption, lowering production costs and freeing capital for innovation investments (Impullitti et al., 2022). Enhanced innovation capacity allows firms to launch new products faster, meet evolving market demands, and solidify their competitive edge. This dual impact of operational efficiency and innovation not only strengthens supplier confidence in the firm’s financial health and growth prospects but also boosts the willingness of both sides to form strategic alliances, ultimately improving the firm’s access to trade credit.

Based on the above discussion, we propose the following hypothesis:

H2b: The adoption of industrial robots enhances firm’s trade credit by improving operational efficiency.

Information asymmetry is a critical factor contributing to corporate financing difficulties (Aktas et al., 2012). Based on signaling theory (Spence, 1973), the industrial robot adoption signals technological competence to external stakeholders, alleviating financing constraints and thereby enhancing a firm’s trade credit rooted in financial intermediation theory (Diamond, 1984). Within the supply chain, suppliers can more readily access soft information and tacit knowledge about a firm through both trade credit channels and everyday social interactions. This increased access helps build trust in the firm’s value and potential, which in turn influences the firm’s trade credit standing.

Specifically, the adoption of industrial robots mitigates financing constraints through two dimensions. On one hand, adopting industrial robots allows firms to signal a “smart manufacturing” image to suppliers, reducing information asymmetry and increasing suppliers’ willingness to extend trade credit. On the other hand, industrial robot adoption signals technological sophistication and innovation capabilities to capital market participants (Ballestar et al., 2022). This enhanced reputation attracts more clients and investors, boosting market competitiveness and mitigating information asymmetry between the firm and external stakeholders (Cui et al., 2024).

The resulting virtuous cycle expands the firm’s financing channels, consolidates its market position, and ultimately significantly improves its ability to obtain trade credit. Based on the signaling theory framework, the adoption of industrial robots sends positive signals that enhance corporate image, alleviate financing constraints, and thus improve trade credit, offering a more efficient and convenient financing method compared to the stringent criteria and lengthy processes of bank loans.

Based on this, we propose Hypothesis 2c:

H2c: The adoption of industrial robots enhances firm’s trade credit by sending positive signals and alleviating financing constraints.

Research design

Sample and data sources

We select A-share listed companies in the manufacturing industry from 2011 to 2019 as the sample, excluding listed companies with ST and ST*, and excluding listed companies in the manufacturing industry with missing financial data. Our sample ends in 2019 due to the economic impact of the COVID-19 pandemic, which may affect suppliers’ willingness to extend trade credit to manufacturing firms. The financial data comes from the China Stock Market and Accounting Research (CSMAR) database. The independent variable is the firm’s industrial robot adoption, which is measured by the penetration of industrial robots at the firm level. Given the widespread adoption of industrial robots in manufacturing, we select the listed manufacturing firms as our research sample (Lee et al., 2022). Industrial robot data are obtained from the International Federation of Robotics (IFR). Manufacturing industry codes (based on the China Securities Regulatory Commission’s 2012 classification) are manually matched with IFR’s industry codes using the first two digits of the sector codes. Since China’s industrial robot adoption surged post-2010, the sample period begins in 2011. After sample screening, 11,162 firm-year observations are finally obtained. To mitigate outlier effects, continuous variables are winsorized at the top and bottom 1%.

Variable measures

Dependent variable

The dependent variable is the firm’s trade credit (Credit). Referring to Chen et al. (2019), it is measured as the ratio of the sum of accounts payable, notes payable, and advances from customers to total assets. The specific formula is as follows:

In the robustness checks, we follow Ding et al. (2023) by re−examining the model using the ratio of accounts payable to total assets as an alternative measure. Additionally, the denominator in Formula (1) is replaced with total liabilities to further validate the findings.

Independent variable

The independent variable is industrial robot adoption (lnexposure), which is measured by the firm-level industrial robot penetration rate. Drawing on the methodologies of Acemoglu and Restrepo (2020), we construct a robot penetration rate indicator for Chinese manufacturing firms. The specific measurement approach is as follows:

First, we develop an industry-level industrial robot penetration rate indicator (\({{PR}}_{i,t}^{{CH}}\)) as shown in Formula (2).

where \({MR}_{i,t}^{{CH}}\) represents the stock of industrial robots in Chinese industry i in year t, \({L}_{i,t=2010}^{{CH}}\) denotes the employment in Chinese industry i in the base year 2010, and \({{PR}}_{i,t}^{{CH}}\) is the indicator of industrial robot penetration for Chinese industry i in year t.

Next, the firm-level industrial robot penetration indicator (CHexposure) is constructed, as shown in Formula (3).

where \({{CH}{exposure}}_{j,i,t}\) is the industrial robot penetration for firm j in industry i in year t. \(\frac{{\mathrm{PWP}}_{j{,}i{,}t=2011}}{{\mathrm{ManuPWP}}_{t=2011}}\) is the ratio of firm j’s share of production workers in industry i in the base year 2011 to the median share of production workers across all manufacturing firms in 2011. This ratio serves as a weight to disaggregate the industry-level robot penetration rate to the firm level.

Finally, the natural logarithm of the firm-level industrial robot penetration rate (lnexposure) is used to measure industrial robot adoption in manufacturing firms to achieve a more uniform distribution.Footnote 2 We also re-estimate the model using the untransformed values of exposure in the robustness checks to make our conclusion more convincing.

Control variables

Drawing on previous studies (Ding et al., 2023; Li et al., 2021), we select the following variables as control variables, including the natural logarithm of the company’s total assets (Size), number of years since the firm’s IPO (Age), the return on total assets (ROA), the leverage ratio (Lev), the annual growth rate of operating revenue (Growth), fixed assets ratio (PPE), shareholding of the largest shareholder (TOP1), shareholding of institutional investors (Inst), shareholding of independent directors (Indep), nature of the company’s property rights (SOE), which is assigned the value of 1 if the listed company is a state-owned enterprise, and 0 otherwise, the natural logarithm of the size of the board of directors (Board), Dual (Dual), which equals 1 if the chairman and general manager positions are held by the same individual, and 0 otherwise, firm’s revenue divided by total industry revenue (Market Share), and total number of employees divided by total assets (Staff Intensity).

Research model

In order to test the impact of industrial robot adoption on firm’s trade credit, we refer to Ding et al. (2023), and construct the model as shown below:

where \({{Credit}}_{i,t}\) is the firm’s trade credit, \(\mathrm{ln}{{exposure}}_{i,t}\) is the natural logarithm of the firm’s industrial robot penetration, and \({{Controls}}_{i,t}\) is a series of control variables. In addition, model (4) controls for firm level fixed effects and year fixed effects. We focus on the coefficient of industrial robot penetration (\({\beta }_{1}\)), if \({\beta }_{1}\) significantly positive, indicating that the adoption of industrial robots can significantly improve the trade credit of firms, H1 holds. The definitions of all variables in the model and how they are calculated are shown in Table A1.

Empirical results

Descriptive statistics

Table 1 presents the descriptive statistics of the main variables. Columns (1) to (8) report the number of observations, mean, standard deviation, minimum, maximum, 25th percentile, median, and 75th percentile, respectively. As shown in Table 2, the mean value of firm’s trade credit (Credit) is 0.157, which aligns with the findings of Xie and Tian (2023) and Hoang et al. (2023). The mean value of the natural logarithm of industrial robot penetration (lnexposure) is 2.269, indicating that there remains potential for increased adoption of industrial robots among China’s listed manufacturing firms. The remaining control variables are generally consistent with prior research, reflecting heterogeneity in fundamental financial characteristics and corporate governance attributes among Chinese listed firms. This further validates the rationality of the control variables selected.

Industrial robot adoption and trade credit

To test the research hypothesis 1, the baseline regression results are presented in Table 2. Column (1) excludes both control variables and firm and year fixed effects. Column (2) incorporates control variables, and Column (3) further includes firm and year fixed effects. The results in Column (3) of Table 2 demonstrate that industrial robot adoption significantly enhances firm’s trade credit among listed manufacturing firms, with a coefficient of 0.005 (t-statistic = 2.48, significant at the 5% level). These findings provide support for Hypothesis 1.

Robustness and endogeneity tests

Robustness checks

We conduct a series of robustness tests. Column (1) and (2) of Table 3 change the measurement of the dependent variable, using the proportion of accounts payable to total assets as a proxy for trade credit (Credit2), and replace the denominator in Eq. (1) with total liabilities (Credit3) for re-testing. Column (3) and Column (4) use the original values of industry-level and firm-level industrial robot penetration rates (without natural logarithm transformation) as independent variables for re-testing. The results in Table 3 show that after changing the measurement of trade credit and industrial robot adoption, the conclusion still holds. It shows that the adoption of industrial robots helps improve firm’s trade credit.

Due to the potential lag in the signaling effect of industrial robot adoption, Column (1) of Table 4 lags the independent variable by one period and re−examines the effect. Since the dependent variable, trade credit, is always above 0 and the data may be more suitable for a Tobit model, Columns (2)−(3) of Table 4 use it to re-examine the relation between industrial robot adoption and trade credit, with the independent variable being current-period and one-period lagged values, respectively. Also, to eliminate the impact of the 2015 stock market volatility on trade credit supply willingness, Column (4) of Table 4 excludes 2015 samples and re-examines the effect. In addition, since the robot exposure variable is constructed based on firm-level employment shares in 2011 and is limited to manufacturing firms, we re-estimate the model after removing samples that have been initially non-manufacturing sector in 2011 but are later reclassified into the manufacturing sector in Column (5). The results in Table 4 show that after lagging the independent variable by one period, changing the regression model, and altering the sample, the conclusion still holds: industrial robot adoption boosts firm’s trade credit.

Endogeneity test: instrumental variable approach

To mitigate the effect of reverse causality, where listed companies with high trade credit levels are more likely to adopt industrial robots, we further use the instrumental variable method for the regression. Referring to the existing literature (Liu et al., 2025; Chen et al., 2024), we use U.S. industry-level industrial robotics data as an instrumental variable (AMexposure) for the regression. The calculation formula is shown in Eq. (5).

where \({{MR}}_{i,t}^{{US}}\) is the stock of industrial robots in U.S. industry i in year t and \({L}_{i,t=2010}^{{US}}\) is the number of people employed in U.S. industry i in 2010 (base period).

The U.S. leads globally in industrial robot adoption, significantly impacting the independent variable. Yet, its relevance to Chinese manufacturing firms’ trade credit is insignificant, meeting the requirements for a valid instrumental variable. The diffusion of robotics technology in U.S. is difficult to affect Chinese firms’ access to trade credit, primarily due to multilevel structural isolation between the two contexts. Industrial robot adoption’s improvements in U.S. firms mainly affect product market competition and are difficult to transmit to China’s informal financing ecosystem, which relies heavily on localized networks, reputation mechanisms, and soft information such as social capital. Informal financing decisions like trade credit remain largely unaffected by foreign technological shifts. Therefore, this instrumental variable satisfies the exogeneity condition.

As shown in Table 5, Column (1) presents the first-stage regression results. Column (2) shows the exogeneity test of instrumental variable, and Column (3) shows the second-stage regression results. Column (1) reveals a significant positive relationship between U.S. industrial robot penetration and the industrial robot adoption in Chinese manufacturing firms. Column (2) shows that the instrumental variable has no significant relationship with firms’ trade credit. In Column (3), after addressing the endogeneity problem and validating the exogeneity of the instrumental variable, the main conclusion still holds: industrial robot adoption significantly enhances firm’s trade credit. Besides, the instrumental variable passes the weak instrument test, with both the Cragg-Donald Wald F statistic and Kleibergen-Paap rk Wald F statistic exceeding 16.38.

Endogeneity test: propensity score matching (PSM) method

Due to potential unobservable specific differences in industrial robot adoption levels that might impact regression results, propensity score matching (PSM) can mitigate bias from unobservable variables. We further employ a logit model for PSM, using control variables as matching variables. Samples are classified by annual median of industrial robot adoption levels: those samples above (or equal to) the median are classified into the high-adoption group, others the low−adoption group. We match high- and low- adoption samples to eliminate inherent differences. We first estimate firm’s probability of high industrial robot adoption, then conduct 1:3 nearest-neighbor matching, yielding 9795 matched samples. Regression results based on these samples are in Column (1) of Table 6.

Also, referencing McMullin and Schonberger (2022), we use entropy balancing to avoid sample loss from logit-model matching. Regression results are in Column (2) of Table 6. Table 6 shows that after matching, industrial robot adoption still boosts corporate credit, proving that our conclusion remains unchanged.

Endogeneity test: difference-in-differences model

In order to further mitigate the reverse causality problem, “The Intelligent Manufacturing Development Plan (2016–2020)” is selected as a quasi-natural experiment. Then we use the Difference-in-Differences (DID) model to test the relationship between industrial robot adoption and firm’s trade credit. “The Intelligent Manufacturing Development Plan (2016–2020)” promotes the introduction of artificial intelligence technologies such as high-end CNC machine tools and industrial robots in key industries, providing institutional assurance for accelerating intelligent transformation. After the release of this document, the intelligent transformation in key industries such as industrial robots, and aviation equipment has made significant progress, so the policy has a significant impact on firm’s industrial robot adoption, while it does not have a significant link with the firm’s trade credit. The regression model is shown in Eq. (6).

Footnote 3where Treat is a dummy variable assigned a value of 1 for the year in which the firm is in the key industries prioritized for the development of intelligent manufacturing, as outlined in the document,Footnote 4 and 0 otherwise, and Post is a time dummy variable assigned a value of 1 for 2016 and subsequent years, and 0 otherwise. The regression result is shown in Column (1) of Table 7. We further use the PSM−DID model to minimize systematic differences between different firms and mitigate bias in the DID estimation. The result is shown in Column (2). The regression coefficients of the cross−multiplier term (Treat*Post) are significant at the 10% and 5% level, respectively, which shows that our conclusion is robust.

Mechanism tests

Enhancing firm’s supply chain resilience

We further examine whether the adoption of industrial robots enhances firm’s trade credit by strengthening supply chain resilience, with broader implications for financing conditions and operational stability of small and medium-sized enterprises (SMEs) within global supply networks. Industrial robots leverage digital technologies and big data algorithms to perform production tasks, fundamentally transforming traditional manufacturing paradigms. This technological shift significantly improves corporate resilience (Marcucci et al., 2022), particularly within supply chain operations, thereby contributing to systemic stability across interconnected production ecosystems.

Supply chain resilience reflects a firm’s ability to maintain stable operations amid disruptions, encompassing preparedness, resistance, recovery, and adaptation. Industrial robots enhance these capabilities in several ways: they increase production flexibility, improve demand responsiveness, reduce reliance on labor, mitigate operational risks, and strengthen end-to-end visibility through data integration. These advantages not only build a more resilient supply chain for adopting firms, but also generate positive spillover effects to upstream and downstream SME partners by reducing volatility and strengthening transactional reliability.

For suppliers, firm’s resilient supply chain signals greater operational stability and a higher likelihood of fulfilling payment obligations. This reduces perceived counterparty risk and safeguards suppliers’ working capital. Consequently, the diffusion of industrial robots helps alleviate financing constraints for SMEs embedded in global supply chains, while also reinforcing the network-wide stability against external shocks.

Thus, embedded within the supply chain resilience framework, we argue that industrial robot adoption boosts trade credit access by reinforcing the firm’s ability to withstand shocks and maintain continuous operations. This mechanism not only benefits the adopting firms, but also promotes financial inclusion and operational solidity for SMEs globally, ultimately fostering a more stable, efficient, and trustworthy supply network.

We define the supply chain resilience as a firm’s capacity to maintain the stability of its own chain when facing adverse external shocks, while dynamically adjusting the network structure and operational modes to achieve an orderly recovery to the pre-shock state, further develop and evolve, and ultimately upgrade the chain. According to the identification, we refer to Li and Wang (2024) and use the entropy value method to construct firm’s supply chain resilience indexFootnote 5 from the five dimensions of corporate predictive ability, resilience, recovery capability, human capital, and government support for testing. The regression results are shown in Table 8.

Column (1) of Table 8 shows that the higher the penetration of industrial robots, the higher the firm’s supply chain resilience. Column (2) shows that the higher the firm’s supply chain resilience, the higher their trade credit (significant at the 5% level). Columns (1)−(3) indicate that industrial robot adoption contributes to higher firm’s supply chain resilience, which in turn increases the willingness of suppliers to provide trade credit to them. Based on the above analysis, our H2a is validated.

Improvement of operation efficiency

We further examine whether the adoption of industrial robots helps to improve firm’s operational efficiency of firms, thereby increasing their trade credit. Industrial robots lower labor costs and improve operational efficiency by automating repetitive tasks and reducing errors caused by human factors. Their high precision, flexibility, and adaptability to changing production requirements decrease the risks of interruptions and delays. Moreover, robots enable continuous, high-speed, and accurate operations, which shorten production cycles and accelerate overall processes, significantly boosting operational efficiency (Wang et al., 2023). These efficiency gains strengthen the firm’s production stability and supply chain reliability, making it a more credible partner in the eyes of suppliers. As a result, suppliers become more willing to offer trade credit, facilitating smoother financial flows and reinforcing supply chain relationships.

Referring to Ang et al. (2007), the total asset turnover (Turnover) is used to measure the firm’s operational efficiency, and the regression results are shown in Table 9.

Column (1) of Table 9 indicates that the higher the penetration of industrial robots in a firm, the higher the operational efficiency of the firm (significant at the 5% level). Column (2) shows that the higher the firm’s operational efficiency, the higher its trade credit (significant at the 1% level). Columns (1) to (3) indicate that industrial robot adoption helps increase the operational efficiency of the firm, which in turn increases the willingness of suppliers to provide trade credit to them. The results in Table 9 show that our H2b is validated.

Easing financing constraints

The adoption of industrial robots helps alleviate corporate financing constraints, thereby enhancing access to trade credit. By integrating advanced automation and data-driven processes, industrial robot adoption significantly improves firm’s operational stability and production efficiency. These enhancements serve as credible signals to suppliers regarding the firm’s reduced operational risk and strengthened repayment capacity. As a result, suppliers are more inclined to offer trade credit, a form of financing that is not only often more cost-effective than bank loans, which involve stringent criteria and lengthy approval processes, but also helps maintain collaborative relationships within the supply chain. Trade credit offers greater flexibility and efficiency, making it an attractive financing alternative especially for firms exhibiting technological maturity and operational resilience.

Thus, based on signaling theory, the adoption of industrial robots plays a crucial role in expanding trade credit availability by conveying positive signals that enhance corporate image, alleviate financing constraints, and ultimately improve firm’s trade credit.

Referring to Whited and Wu (2006), the WW index is used to measure the financing constraints (WW) faced by firms. The specific formula is shown in Eq. (7).

where Div is the cash dividend payment dummy variable, which is assigned the value of 1 if the firm pays cash dividends, and 0 otherwise; ISG is the average sales growth rate of the industry (based on the 2012 CSRC industry classification), and the rest of the variables are measured in the way as shown in Table A1. The higher the WW index, the higher the degree of financing constraints that the firm faces.

Column (1) of Table 10 shows that the higher the penetration of industrial robots, the lower the degree of financing constraints faced by firms. Column (2) shows that suppliers of firms with higher financing constraints have lower willingness to provide trade credit (significant at the 5% level). Columns (1)−(3) indicate that industrial robot adoption alleviates the financing constraints faced by firms, thereby enhancing trade credit. Based on the above analysis, our H2c is validated.

Cross-sectional analysis

Technology background

The adoption of industrial robots exhibits distinct characteristics of technological advancement, and whether it can exert positive effects on firms is closely related to their technological background (Chung, 2021; Lee et al., 2022). The compatibility between industrial robot adoption and firm’s industry attributions, management characteristics, and labor structure varies significantly. Consequently, the enhancement effect of industrial robot adoption on firm’s trade credit is shaped by these features. When firms possess a strong technological foundation, industrial robot adoptions align more effectively with their operational characteristics, leading to a more pronounced improvement in trade credit. Specifically, from the perspective of industry characteristics, the development of firms in high−tech industries relies on technology-intensive products, and their production and operation are dominated by technological innovation. Therefore, compared with non-high-tech industry firms, high-tech firms experience more pronounced trade credit improvements from robot adoption.

In terms of management characteristics, when directors, supervisors, and senior executives possess information technology backgrounds, they place greater emphasis on the adoption of advanced technologies (Zhang and Bu, 2024), leading to higher technological compatibility with industrial robots. Therefore, listed companies with IT-experienced management achieve greater trade credit enhancement through industrial robot adoption compared to others.

Regarding labor structure, technical personnel engaged in highly-skilled unconventional work demonstrate better collaboration with industrial robots. Firms with low technical staff ratios show poorer human-robot compatibility, hindering positive effects. Thus, we predict that firms with higher technical personnel proportions obtain more significant trade credit improvements through robot adoptions.

To validate the above hypotheses, we draw on the methodology of Li et al. (2025). High-tech industries are defined according to the CSRC 2012 industry classification and the National Key Supported High-Tech Fields. Following Campbell et al. (2023), senior management, which includes directors, supervisors, and executives, is considered to have an IT background if they possess relevant educational or professional experience in information management or technology. Such cases are assigned a value of 1; otherwise, 0. Furthermore, samples are divided into high-technician proportion and low-technician proportion groups based on the annual median ratio of technical personnel within companies. The regression results are presented in Table 11.

Columns (1), (3), and (5) of Table 11 indicate that high-tech firms, firms with IT-background management, and those with high proportions of technical personnel exhibit significantly higher trade credit as industrial robot penetration increases. In contrast, no significant relationship is observed in other groups.

This finding underscores that the technological compatibility between firms and industrial robots plays a critical role in amplifying the positive effect of industrial robot adoption on trade credit. From an industrial perspective, firms with pre-established digital infrastructure can integrate robot adoptions more seamlessly into production and supply chain operations. This enhances operational stability and production efficiency more rapidly, thereby strengthening supplier confidence in the firm’s ability to meet payment obligations. The signaling effect of technological maturity thus directly facilitates greater willingness among suppliers to extend trade credit.

From a policy standpoint, these results emphasize the need to move toward holistic support for enabling technological absorption and design targeted policy tools that foster high-tech sector development and enhance human capital readiness. Policies should prioritize attracting and retaining high-tech leadership and specialized technical talent. By cultivating an ecosystem rich in both advanced technological capacity and specialized human capital, policymakers can significantly magnify the broader economic benefits of robot adoption, which includes strengthened supply chain resilience and improved financial inclusion for small and medium-sized enterprises.

In essence, the relationship between robot adoption and trade credit is not merely mechanistic but contingent on a firm’s embeddedness within a supportive technological and institutional environment.

Equity structure

In terms of employment systems, state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs) exhibit distinct characteristics. SOEs face stricter external supervision in employee hiring, maintain more comprehensive labor protection systems, and incur higher economic costs for employee dismissal, resulting in a more stable workforce and limited impact from industrial robot adoption. In contrast, non-SOEs demonstrate greater flexibility in hiring decisions and lower dismissal costs (Huang et al., 2024). For non-SOEs, adopting industrial robots significantly reduces labor costs and enhances market competitiveness, thereby increasing suppliers’ willingness to provide trade credit. Consequently, higher industrial robot penetration in non−SOEs correlates with elevated trade credit levels.

Regression results in Table 12 confirm our hypothesis. In non-SOEs, industrial robot penetration significantly boosts trade credit (coefficient = 0.005, significant at the 1% level) while no significant relationship is observed in SOEs.

This underscores that the flexibility of labor management in non−SOEs amplifies the positive effects of industrial robots on trade credit, whereas the employment structure of SOEs mitigates such impacts. This outcome reflects deeper structural and institutional differences between enterprise types, with significant implications for both industrial modernization and policy design. Non−SOEs typically exhibit greater flexibility in labor allocation, performance incentives, and organizational adaptation, allowing them to more effectively reconfigure workflows and retrain employees in response to industrial robot adoption. This agility enhances operational efficiency and supply chain reliability, which are key signals that reassure suppliers and strengthen trust in extending trade credit. By contrast, SOEs are often influenced by administrative priorities, social stability mandates, and institutional path dependency. Their limited ability to adjust staffing roles, compensation structures, or recruitment practices in alignment with technological needs constrains the operational gains from robot adoption, thereby muffling its positive impact on trade credit.

These findings highlight the need for differentiated and targeted approaches in response to robot adoption and labor market regulation. Firms should seek to reinforce their flexibility through access to informal financing like trade credit through technological upgrading and the development of sectoral standards that support smooth operational integration of robots. More broadly, this underscores that technological innovation cannot be divorced from institutional context: successful robot adoption depends not only on technical capability but also on organizational adaptability. Policies that foster both technological and institutional readiness will be essential to unlocking the full benefits of robot adoption across all enterprise types.

Market competition

When industry competition is high, firms adopt industrial robots to reduce labor costs. This helps them establish a competitive advantage in the market. At the same time, the adoption of industrial robots can also send positive signals to the market, which can help firms optimize their image and encourage suppliers to increase their willingness to supply trade credit. Therefore, we expect that the higher the penetration of industrial robots, the higher the trade credit level of the firms when market competition is fierce.

We use the Lerner index to measure the market competition firms face (Fare et al., 2024). The higher the value of the index, the lower the degree of market competition. When the firm’s Lerner index is lower than the annual median, it is classified into the group with a high degree of industry competition, otherwise, it is classified into the group with a low degree of industry competition. The group regression results are shown in Table 13. When the firm is in the industry with a high degree of competition, the firm’s industrial robot adoption can significantly improve its trade credit (the coefficient is 0.007, which is significant at the 5% level), while in the group with a low degree of market competition, there is no significant relationship between the two.

The results show that the market competition amplifies the positive effects of industrial robots’ adoption on trade credit. This outcome reflects how market competition shapes the strategic behavior and signaling value of robot adoption, with meaningful implications for both corporate practices and public policy. In highly competitive environments, firms face stronger pressure to differentiate themselves in terms of operational efficiency, product quality, and supply chain responsiveness. The adoption of industrial robots under such conditions serves as a credible signal of a company’s commitment to enhancing productivity and stabilizing output. Suppliers perceive robots in competitive sectors as a strategic move to sustain market position and financial health, thereby increasing their willingness to offer favorable trade credit. Furthermore, in contested markets, firms are more likely to leverage industrial robots not only to reduce costs but also to strengthen coordination with supply chain partners, making them more reliable counterparts in the eyes of suppliers.

From the perspective of public policy, our findings suggest that fostering competitive and well-functioning markets can enhance the broader benefits from robot adoption. Policies that encourage open competition can amplify the incentive of firms to adopt industrial robots in ways that also improve their financial stability and credit. At the same time, policy support for technology diffusion should be designed with an awareness of market structure: in less competitive or concentrated industries, firms may lack the motivation to adopt robots effectively. Thus, complementary measures may be necessary to encourage firms’ high-tech investment across diverse market contexts. These findings reinforce that technological innovation’s benefits can help firms stand out in the highly competitive market environment.

Conclusion

Under the current thriving environment of high-quality productive forces, the adoption of industrial robots is of great significance for enabling China’s manufacturing sector to better address the pressures arising from the decline in labor cost advantages. Firms bear the critical mission of deeply integrating industrial robot adoption with production and manufacturing development. At the micro-level, existing studies primarily explore the relationship between industrial robot adoption and corporate investment behaviors, along with their economic consequences, while research focusing on the impact of industrial robot adoption on corporate financing behaviors remains relatively scarce. Therefore, we aim to investigate the effects of industrial robot adoption on firm’s corporate financing from the perspective of supply chain.

Based on a sample of A-share manufacturing listed companies in China from 2011 to 2019, our study examines the impact of industrial robot adoptions on firm’s trade credit and its underlying mechanisms. Empirical results demonstrate that industrial robot adoption significantly enhances firm’s trade credit. These findings remain robust after reconstructing key variables, accounting for the lagged signaling effects of robot adoption, modifying regression models, changing the sample, and addressing endogeneity through instrumental variable (IV) approaches, propensity score matching (PSM) methods and Difference-in-Differences (DID) models. Mechanism tests reveal that industrial robots improve firm’s trade credit by strengthening supply chain resilience, enhancing operational efficiency, and alleviating financing constraints. Cross-sectional analysis shows that the positive impact of industrial robot adoption on firm’s trade credit is more pronounced in high-tech industries, firms with IT-experienced management, firms with high proportions of technical personnel, non-state-owned enterprises, and industries facing fierce market competition.

Our paper contributes to the literature on the firm-level economic impacts of industrial robot adoption by exploring how this technological transformation influences corporate financing behaviors from the perspective of trade credit. We also clarify the intrinsic logical chain by which industrial robot adoption increases suppliers’ willingness to provide trade credit, thereby enriching existing studies on the economic consequences of industrial robots and the determinants of trade credit. In addition, the findings provide managerial implications by highlighting that firms can strategically leverage industrial robot adoption to strengthen supply chain stability and improve financing credibility. For policymakers, the results suggest that fostering technological upgrading and supply chain resilience could enhance both financing inclusion and industrial competitiveness.

China’s unique industrial and institutional environment provides valuable insights that enrich the global understanding of industrial automation and corporate behavior. Beyond China, these insights also hold relevance internationally, as industrial robot adoption may similarly reshape SME financing and supply chain stability across global markets. Whether in developed or emerging economies, the potential for industrial robot expansion remains considerable, driven by technological progress and the need for greater efficiency. In emerging economies, where SMEs face persistent financing frictions, industrial robot adoption can act as a credible signal of operational reliability that improves access to trade credit. In developed economies, industrial robot adoption enhances supply chain resilience by mitigating labor shortages and ensuring production continuity. Thus, examining China’s experience offers a broader perspective on how automation transforms financing channels and supply chain coordination under diverse institutional settings worldwide.

However, our study focuses on informal financing channels (trade credit) and does not address formal financing mechanisms like bank credit. Additionally, it centers on industrial robots as a representative form of advanced manufacturing technology, leaving the impacts of other AI technologies on corporate financing unexplored. Future research could conduct multidimensional analyses of the interplay between AI adoptions and corporate financing behaviors.

Data availability

The data that support the findings of this study are available on request from the corresponding author.

Notes

A logarithmic transformation is applied to the “exposure” variable to obtain a more uniform distribution, given its wide range ([0.011, 370.9]) and large standard deviation (58.99).

In the model, the Treat and year terms are absorbed by firm fixed effects and year fixed effects, hence, they are not displayed in the model.

“The Intelligent Manufacturing Development Plan (2016−2020)” emphasizes promoting the intelligent transformation in key industries such as: high−end CNC machine tools and industrial robots, aviation equipment, offshore engineering equipment and high−tech ships, advanced rail transit equipment, energy−saving and new energy vehicles, power equipment, agricultural equipment, new materials, biopharmaceuticals and high−performance medical devices, light industry, textiles, petrochemicals and chemicals, steel, non−ferrous metals, building materials, and civil explosives.

See indicators in Table A2 for detail.

References

Abdulla Y, Dang VA, Khurshed A (2017) Stock market listing and the use of trade credit: evidence from public and private firms. J Corp Financ 46:391–410. https://doi.org/10.1016/j.jcorpfin.2017.08.004

Acemoglu D, Restrepo P (2020) Robots and jobs: evidence from US labor markets. J Political Econ 128(6):2188–2244. https://doi.org/10.1086/705716

Aktas N, De Bodt E, Lobez F, Statnik JC (2012) The information content of trade credit. J Bank Financ 36(5):1402–1413. https://doi.org/10.1016/j.jbankfin.2011.12.001

Allen F, Qian Y, Tu G, Yu F (2019) Entrusted loans: a close look at China’s shadow banking system. J Financ Econ 133(1):18–41. https://doi.org/10.1016/j.jfineco.2019.01.006

Ang JS, Cole RA, Lin JW (2007) Agency costs and ownership structure. J Financ 55(1):81–106. https://doi.org/10.1111/0022-1082.00201

Bai C, Yao D, Xue Q (2025) Does artificial intelligence suppress firms’ greenwashing behavior? Evidence from robot adoption in China. Energy Econ 142: 108168. https://doi.org/10.1016/j.eneco.2024.108168

Ballestar MT, García-Lazaro A, Sainz J, Sanz I (2022) Why is your company not robotic? The technology and human capital needed by firms to become robotic. J Bus Res 142:328–343. https://doi.org/10.1016/j.jbusres.2021.12.061

Bentley KA, Omer TC, Sharp NY (2013) Business strategy, financial reporting irregularities, and audit effort. Contemp Account Res 30(2):780–817. https://doi.org/10.1111/j.1911-3846.2012.01174.x

Campbell JT, Bilgili H, Crossland C, Ajay B (2023) The background on executive background: an integrative review. J Manag 49(1):7–51. https://doi.org/10.1177/01492063221120392

Chen S, Ma H, Wu Q (2019) Bank credit and trade credit: evidence from natural experiments. J Bank Financ 108: 105616. https://doi.org/10.1016/j.jbankfin.2019.105616

Chen S, Mu S, He X, Han J, Tan Z (2024) Does industrial robot adoption affect green total factor productivity? Evidence from China. Ecol Indic 161: 111958. https://doi.org/10.1016/j.ecolind.2024.111958

Cheng C, Yang L (2022) What drives the credit constraints faced by Chinese small and micro enterprises? Econ. Model 113:105898. https://doi.org/10.1016/j.econmod.2022.105898

Chung H (2021) Adoption and development of the fourth industrial revolution technology: features and determinants. Sustainability 13(2):871. https://doi.org/10.3390/su13020871

Cohen Y, Naseraldin H, Chaudhuri A, Pilati F (2019) Assembly systems in Industry 4.0 era: a road map to understand Assembly 4.0. Int J Adv Manuf Technol 105:4037–4054. https://doi.org/10.1007/s00170-019-04203-1

Cui H, Liang S, Xu C, Junli Y (2024) Robots and analyst forecast precision: evidence from Chinese manufacturing. Int Rev Financ Anal 94: 103197. https://doi.org/10.1016/j.irfa.2024.103197

De Vries GJ, Gentile E, Miroudot S, Wacker KM (2020) The rise of robots and the fall of routine jobs. Labour Econ 66: 101885. https://doi.org/10.1016/j.labeco.2020.101885

Diamond DW (1984) Financial intermediation and delegated monitoring. Rev Econ Stud 51(3):393–414. https://doi.org/10.2307/2297430

Ding F, Liu Q, Shi H, Wang W, Wu S (2023) Firms’ access to informal financing: the role of shared managers in trade credit access. J Corp Financ 79: 102388. https://doi.org/10.1016/j.jcorpfin.2023.102388

Dixon J, Hong B, Wu L (2021) The robot revolution: managerial and employment consequences for firms. Manag Sci 67(9):5586–5605. https://doi.org/10.1287/mnsc.2020.3812

El Ghoul S, Zheng X (2016) Trade credit provision and national culture. J Corp Financ 41:475–501. https://doi.org/10.1016/j.jcorpfin.2016.07.002

Fabbri D, Klapper LF (2016) Bargaining power and trade credit. J Corp Financ 41:66–80. https://doi.org/10.1016/j.jcorpfin.2016.07.001

Fare R, Grosskopf S, Margaritis D (eds) (2024) Market power, economic efficiency and the Lerner Index (Vol. 19). World Scientific

Fisman R, Love I (2003) Trade credit, financial intermediary development, and industry growth. J Financ 58(1):353–374. https://doi.org/10.1111/1540-6261.00527

Fisman R, Raturi M (2004) Does competition encourage credit provision? Evidence from African trade credit relationships. Rev Econ Stat 86(1):345–352. https://doi.org/10.1162/003465304323023859

Gan J, Liu L, Qiao G, Zhang Q (2023) The role of robot adoption in green innovation: evidence from China. Econ Model 119: 106128. https://doi.org/10.1016/j.econmod.2022.106128

Hoang CH, Ly KC, Xiao Q, Zhang X (2023) Does national culture impact trade credit provision of SMEs? Econ Model 124: 106288. https://doi.org/10.1016/j.econmod.2023.106288

Huang Y, Mukherjee T, Wang W (2024) Labor protection and financing decisions of firms: the case of China. Int Rev Econ Financ 94: 103396. https://doi.org/10.1016/j.iref.2024.103396

Impullitti G, Licandro O, Rendahl P (2022) Technology, market structure and the gains from trade. J Int Econ 135: 103557. https://doi.org/10.1016/j.jinteco.2021.103557

Jung JH, Lim D-G (2020) Industrial robots, employment growth, and labor cost: a simultaneous equation analysis. Technol Forecast Soc Change 159: 120202. https://doi.org/10.1016/j.techfore.2020.120202

Lee CC, Qin S, Li Y (2022) Does industrial robot adoption promote green technology innovation in the manufacturing industry? Technol Forecast Soc Change 183: 121893. https://doi.org/10.1016/j.techfore.2022.121893

Leng Y, Shi X, Hiroatsu F, Kalachev A, Wan D (2023) Automated construction for human–robot interaction in wooden buildings: Integrated robotic construction and digital design of iSMART wooden arches. J Field Robot 40(4):810–827. https://doi.org/10.1002/rob.22154

Li C, Wang Y (2024) Digital transformation and enterprise resilience: Enabling or burdening? PLoS ONE 19(7):e0305615. https://doi.org/10.1371/journal.pone.0305615

Li J, Wu Z, Yu K, Zhao W (2024) The effect of industrial robot adoption on firm value: evidence from China. Financ Res Lett 60: 104907. https://doi.org/10.1016/j.frl.2023.104907

Li X, Ng J, Saffar W (2021) Financial reporting and trade credit: evidence from mandatory IFRS adoption. Contemp Account Res 38(1):96–128. https://doi.org/10.1111/1911-3846.12611

Li Y, Wang Y, Ma R, Wang R (2025) Research on the impact of financialization of high-tech manufacturing listed companies on real investment. Appl Econ 57(9):1010–1023. https://doi.org/10.1080/00036846.2024.2311060

Liang L, Lu L, Su L (2023) The impact of industrial robot adoption on corporate green innovation in China. Sci Rep 13(1):18695. https://doi.org/10.1038/s41598-023-46037-8

Liu X, Cifuentes-Faura J, Yang X, Pan J (2025) The green innovation effect of industrial robot adoptions: evidence from Chinese manufacturing companies. Technol Forecast Soc Change 210: 123904. https://doi.org/10.1016/j.techfore.2024.123904

Makridakis S (2017) The forthcoming artificial intelligence (AI) revolution: its impact on society and firms. Futures 90:46–60. https://doi.org/10.1016/j.futures.2017.03.006

Mao H, Zhang Q, Chen G (2024) Impact of industrial robot adoption on trade credit financing in manufacturing firms. Acad J Business Manag 6(2). https://doi.org/10.25236/AJBM.2024.060202

Marcucci G, Antomarioni S, Ciarapica FE, Bevilacqua M (2022) The impact of Operations and IT-related Industry 4.0 key technologies on organizational resilience. Prod Plan Control 33(15):1417–1431. https://doi.org/10.1080/09537287.2021.1874702

McMullin J, Schonberger B (2022) When good balance goes bad: a discussion of common pitfalls when using entropy balancing. J Financ Rep 7(1):167–196. https://doi.org/10.2308/JFR-2021-007

Petersen MA, Rajan RG (1997) Trade credit: Theories and evidence. Rev Financ Stud 10(3):661–691. https://doi.org/10.1093/rfs/10.3.661

Ralston P, Blackhurst J (2020) Industry 4.0 and resilience in the supply chain: a driver of capability enhancement or capability loss? Int J Prod Res 58(16):5006–5019. https://doi.org/10.1080/00207543.2020.1736724

Rüßmann M, Lorenz M, Gerbert P, Waldner M, Justus J, Engel P, Harnisch M (2015) Industry 4.0: the future of productivity and growth in manufacturing industries. Boston Consult Group 9(1):54–89

Soni U, Jain V, Kumar S (2014) Measuring supply chain resilience using a deterministic modeling approach. Comput Ind Eng 74:11–25. https://doi.org/10.1016/j.cie.2014.04.019

Spence M (1973) Job market signaling. Q J Econ 87(3):355–374. https://doi.org/10.2307/1882010

Teece DJ, Pisano G, Shuen A (1997) Dynamic capabilities and strategic management. Strat Manag J 18(7):509–533. https://www.jstor.org/stable/3088148

Wang KL, Sun TT, Xu RY (2023) The impact of artificial intelligence on total factor productivity: empirical evidence from China’s manufacturing enterprises. Econ Change Restruct 56(2):1113–1146. https://doi.org/10.1007/s10644-022-09467-4

Wang K, Zhou J, Li G, Hu Y, Hu F (2024) Industrial automation and product quality: the role of robotic production transformation. Appl Econ 1–16. https://doi.org/10.1080/00036846.2024.2364120

Wang L, Liu Z, Liu A, Tao F (2021) Artificial intelligence in product lifecycle management. Int J Adv Manuf Technol 114:771–796. https://doi.org/10.1007/s00170-021-06882-1

Wang X, Han L, Huang X, Mi B (2021) The financial and operational impacts of European SMEs’ use of trade credit as a substitute for bank credit. Eur J Financ 27(8):796–825. https://doi.org/10.1080/1351847X.2020.1846576

Wang X, Liu M, Liu C, Ling L, Zhang X (2023) Data-driven and knowledge-based predictive maintenance method for industrial robots for the production stability of intelligent manufacturing. Expert Syst Appl 234: 121136. https://doi.org/10.1016/j.eswa.2023.121136

Whited TM, Wu G (2006) Financial constraints risk. Rev Financ Stud 19(2):531–559. https://doi.org/10.1093/rfs/hhj012

Wilson HJ, Daugherty PR (2018) Collaborative intelligence: Humans and AI are joining forces. Harv Bus Rev 96(4):114–123

Xiao Y, Ma D, Cheng Y, Wang L (2020) Effect of labor cost and industrial structure on the development mode transformation of China’s industrial economy. Emerg Mark Financ Trade 56(8):1677–1690. https://doi.org/10.1080/1540496X.2019.1694887

Xie W, Tian H (2023) The effect of the COVID-19 pandemic on firm’s trade credit financing. Econ Lett 232: 111339. https://doi.org/10.1016/j.econlet.2023.111339

Zhang K, Bu C (2024) Top managers with information technology backgrounds and digital transformation: evidence from small and medium companies. Econo Model 132:106629. https://doi.org/10.1016/j.econmod.2023.106629

Zhang Q, Zhang F, Mai Q (2023) Robot adoption and labor demand: a new interpretation from external competition. Technol Soc 74:102310. https://doi.org/10.1016/j.techsoc.2023.102310

Zhang Z (2023) The impact of the artificial intelligence industry on the number and structure of employments in the digital economy environment. Technol Forecast Soc Change 197:122881. https://doi.org/10.1016/j.techfore.2023.122881

Zhang Z, Wang L (2025) The driving effect of industrial robots on international industrial transfer: empirical evidence from China. Emerg Markets Finance Trade 1–15. https://doi.org/10.1080/1540496X.2025.2473491

Zhao Y, Said R, Ismail NW, Hamzah HZ (2022) Effect of industrial robots on employment in China: an industry level analysis. Comput Intell Neurosci 2022(1):2267237. https://doi.org/10.1155/2022/2267237

Zhou Z, Li Z, Du S, Cao J (2024) Robot adoption and enterprise R&D manipulation: evidence from China. Technol Forecast Soc Change 200:123134. https://doi.org/10.1016/j.techfore.2023.123134

Acknowledgements

This work is supported by the PhD Research Startup Fund of Jiangsu University of Science and Technology (Grant No. 1042932504) and the General Project of Philosophy and Social Science Research in Jiangsu Universities (Grant No. 2025SJYB1641).

Author information

Authors and Affiliations

Contributions

Yiyun Ge (First Author): Conceptualization, methodology, investigation, visualization, writing−original draft, writing−review and editing. Ruixuan Zhang (Corresponding Author): Methodology, supervision, software, formal analysis, data curation. Hanbin Zhu: Methodology, supervision, software, formal analysis, data curation. Qiaohe Wang(Corresponding Author): Methodology, supervision, software, formal analysis, data curation. We declare that this manuscript is original, has not been published before, and is not currently being considered for publication elsewhere. We confirm that the manuscript has been read and approved by all named authors and that there are no other persons who satisfied the criteria for authorship but are not listed. We further confirm that the order of authors listed in the manuscript has been approved by all of us.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Ge, Y., Zhang, R., Zhu, H. et al. The impact of industrial robot adoption on firm’s trade credit. Humanit Soc Sci Commun 13, 177 (2026). https://doi.org/10.1057/s41599-025-06476-2

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-06476-2