Abstract

Amid intensifying climate urgency, decarbonizing marine economic sectors presents both a critical challenge and a pivotal opportunity in global mitigation strategies. However, systematic approaches to assessing reduction potential remain limited. Here, we developed an integrated analytical framework with statistical data and found a 28.35% increase in greenhouse gas emissions in China’s marine economic sectors during 2000–2020. The decoupling trajectory of emissions from economic growth improved during 2005–2015 but deteriorated thereafter. Energy intensity reduction offsets 81% of cumulative emission growth driven by economic expansion. Scenario comparisons indicate that adopting the sustainability pathway could constrain the emissions peak to 126.4–143.2 Mt carbon dioxide equivalent during 2022–2028, achieving dual advantages of 10–35% lower peak volumes and 3–6 years earlier than the fossil-fueled development pathway. This study establishes a transferable framework for coastal nations to align blue economy growth with Paris Agreement targets through targeted peaking strategies.

Similar content being viewed by others

Introduction

The ocean economy has emerged as a pivotal engine of global development1, expanding 2.5-fold since 1995 at rates surpassing global gross domestic product (GDP) growth2. This maritime expansion, however, carries substantial climate costs: core marine sectors like marine capture fisheries3, offshore oil and gas4,5, and maritime transport6,7 collectively generated 120-180 Mt CO2 emissions in 2019, accounting for approximately 3.43%–4.97% of global emissions8. Particularly concerning is the maritime transport sector, whose emissions escalated from 9.77 Mt CO₂ (2.76% global share) in 2012 to 10.76 Mt CO₂ (2.89%) in 20189, directly hindering progress toward the International Maritime Organization’s Carbon Intensity Indicator, which mandates a 40% emission reduction by 203010. Moreover, current projections suggest the global ocean economy will reach $3 trillion by 2030, surpassing 3% of global GDP11. This economic expansion underscores the urgency of modelling and forecasting emissions trajectories to explore potential mitigation pathways and ensure alignment with the goals of the Paris Agreement.

Existing research on reducing marine economic sectors’ emissions has focused on three main methodologies: technology-centric assessments12,13,14,15,16, system-based simulations17,18,19,20,21,22,23, and historical trend extrapolations for near-term projections24,25. Technology-centric assessments, which often quantify maximal abatement capacities under idealized substitutions using life cycle analysis, can be broadly divided into two approaches. The first approach examines fuel-switching strategies to reduce combustion-related emissions. Studies demonstrate that adopting zero-carbon alternatives could achieve substantial decarbonization in marine transportation, particularly when considering regional fuel infrastructure readiness12,13. In contrast, the second approach focuses on operational process optimization14. Representative cases, including spatial reorganization of shipping routes15 and modernization of offshore energy systems16, both of which show considerable potential to reshape emission profiles across maritime value chains. System-based methodologies predominantly employ two analytical frameworks: integrated system dynamics with multi-scenario projections and standalone multi-sector scenario assessments. The former combines causal feedback loops with scenario planning, as exemplified by studies that model optimal emission trajectories through interactions among shipping capacity, economic benefits, and energy consumption19,23. Conversely, the standalone multi-sector scenario assessments typically aggregate emission trajectories linearly, potentially overlooking cross-sectoral feedback and interdependencies17. Historical trend extrapolation methodologies, as the third methodology—some now enhanced by machine learning techniques—are increasingly used to improve short-term forecasting accuracy. These approaches leverage time-series pattern recognition and have shown promise in projecting emissions for specific sectors like maritime transport24,25. However, their application across the broader marine economy remains fragmented and underdeveloped.

Persistent limitations in existing methodologies can be identified in three dimensions. Firstly, technology-centric assessments disproportionately prioritize deep-sea shipping, often neglecting coastal emission hotspots such as marine aquaculture and capture fishery, which are responsible for 8–21% of regional marine emissions8. Secondly, system-based simulations typically rely on deterministic growth assumptions, failing to capture uncertainties arising from economic volatility, technological innovation, and policy adjustments. Furthermore, while data-driven projections achieve high short-term accuracy, their reliance on historical trends restricts their capacity to accommodate structural transformations induced by climate policies. Beyond methodological limitations, the primary concern is the lack of clarity regarding global mitigation potential and essential pathways for decarbonizing the marine economy. This information is crucial as establishing a low-emission development trajectory for the marine economic sector is pivotal to mitigating global warming and achieving carbon neutrality.

To address these gaps, we developed an integrated analytical framework for the first time. This framework synergizes decoupling theory, factor decomposition, and stochastic scenario modeling, enabling a systematic evaluation of the greenhouse gas (GHG) reduction potential and pathways in marine economic sectors. China is selected as the case study for quantitative demonstration, given its dominant role in the global marine economy. We aim to explore the following four questions: What are the spatiotemporal emission patterns across heterogeneous marine economic sectors? How effective is the decoupling between economic growth and emissions? What are the key driving factors of emissions, and what are their relative contributions? What are the projected emissions peak and their timing under different action plans?

To answer these questions, our analytical framework advances marine emission reduction potential research through four methodologically integrated phases (Supplementary Fig. 1). Firstly, we construct a provincial-level emission inventory (2000–2020), capturing the spatiotemporal dynamics of GHG fluxes across five critical marine sectors: maritime transportation, marine capture fishery, marine aquaculture, offshore oil and gas production, and ocean renewables. Secondly, we apply the Tapio decoupling model to quantify the dynamic tradeoff between marine economic expansion and emission trajectories, thereby identifying structural barriers to economic growth-emission decoupling. Third, we innovatively extend the conventional Kaya identity through logarithmic mean divisia index (LMDI) decomposition, enabling mechanistic isolation of five driver contributions—emission intensity, energy consumption intensity, employment ratio, labor productivity, and population dynamics that collectively shape maritime emission dynamics. Finally, to overcome the deterministic scenario limitations, we develop probabilistic emission pathways based on three classical shared socioeconomic pathways (SSP, SSP1: sustainability, SSP2: middle-of-the-road, and SSP5: fossil-fueled development), using Monte Carlo simulation to assess emissions trajectories (like emissions peak and time) through 2040 under policy uncertainties. This framework advances marine climate governance through two synergistic dimensions: empirically delineating the nonlinear emission reduction potential of China’s marine economy while providing a transferable paradigm for global blue economy transition.

Results

GHG emissions in China’s marine economic sectors increased by 28.35% from 2000 to 2020

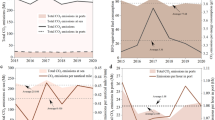

China’s marine economic sectors experienced a 28.35% cumulative growth in GHG emissions between 2000 and 2020, rising from 95.6 Mt carbon dioxide equivalent (CO2e) to 122.7 Mt CO2e (Fig. 1a). After 2005, however, the national total no longer showed a sustained upward trajectory and instead fluctuated within a relatively narrow range. This post-2005 stabilization was largely shaped by developments in two dominant emitters, maritime transportation and marine capture fishing, which together accounted for 76–88% of total sectoral emissions. Maritime transportation emerged as the largest emission source, nearly doubling its emissions from 30.0 Mt CO2e to 58.3 Mt CO2e (+94.33%) and accounting for 48% of total sector emissions in 2020. Its trajectory fluctuated considerably after 2005, shaped by changing demand, market uncertainties, and external shocks such as climate variability and geopolitical disruptions26. In parallel, the marine capture fishery, the largest emitter before 2005, achieved a 34% emission reduction (from 52.9 to 35.1 Mt CO2e) due to declining fishery resources and industrial restructuring. After 2005, this transition was reinforced by the expansion of low-carbon marine aquaculture and stricter enforcement of vessel reduction policies27, accelerating the shift toward less carbon-intensive production. Although aquaculture is less carbon-intensive than capture fisheries, its steady expansion still drove a 3.9% annual rise in emissions, partially offsetting the reductions from capture fisheries. Together, the volatility of shipping emissions and the transition of marine fisheries curbed sustained national emission growth after 2005, producing the observed oscillating trend. Additionally, new pressures are emerging from the rapid growth of previously lower-emitting sectors. Emissions from offshore oil/gas production expanded at 4.9% annually (6–14% sectoral share). Notably, even marine renewable energy, often considered a low-carbon alternative, contributed to emissions through the manufacturing, installation, and maintenance of infrastructure28, leading to an increase of 0.6 Mt CO2e in sector emissions by 2020.

a Temporal trends of sectoral GHG emissions from 2000 to 2020. b Spatial distribution and sectoral composition of emissions across 11 coastal provinces in 2000, 2010, and 2020. Blank base map was made with Natural Earth (https://www.naturalearthdata.com/).

Geospatial disparities highlight both the concentration and divergence of provincial marine-sector emissions (Fig. 1b, Supplementary Fig. 1). Overall, marine-sector GHG emissions are highly concentrated in a few provinces. Shanghai, Guangdong, Shandong, Zhejiang, and Tianjin together account for about 71% of national emissions, while provinces such as Hainan, Guangxi, and Hebei contribute only marginal shares. This concentration is also evident at the industry level: maritime transportation emissions are dominated by Shanghai and Guangdong, jointly representing 63% of the national total, while capture fishery emissions are largely clustered in Zhejiang (27%) and Shandong (17%). Marine aquaculture is clustered in Guangdong and Shandong (43% of national marine aquaculture emissions), offshore renewable energy development is dominated by Jiangsu (63%), and offshore oil and gas production is concentrated in Tianjin (59%) and Guangdong (29%). Against this background of concentrated emissions, provinces have followed divergent trajectories, reflecting differences in industrial structure, resource endowment, and regional policy dynamics. Shanghai remains a consistently high emitter, sustained by its shipping-intensive economy. Guangdong, by contrast, has undergone a sharp surge in emissions since 2013, driven mainly by the rapid expansion of maritime transport linked to the 21st-Century Maritime Silk Road29. Shandong has experienced the opposite pattern, with steady emission declines due to shrinking capture fisheries30. Meanwhile, provinces around the Bohai Rim (Tianjin, Hebei, and Liaoning) also have seen marked post-2010 decreases, largely linked to shipping-route consolidation, reduced port activity, industrial restructuring, and strengthened regulatory measures31. For Tianjin, we also note that declines in transport emissions have been partly offset by increases in offshore oil and gas activity, but the net effect has still been a reduction in total marine-sector emissions.

The decoupling of emissions from China’s marine economic sectors initially improved up to 2015 but deteriorated thereafter

Between 2000 and 2020, the decoupling state in China’s marine economic sectors exhibited marked temporal volatility—initial improvement followed by subsequent deterioration (Fig. 2a). In the first phase (2000–2005), emissions climbed by 23% while gross ocean product (GOP) rose by only 15%, indicating expansive negative decoupling. This pattern reflected disorderly, scale-inefficient expansion, reliance on outdated, high-carbon production technologies, and unregulated demand for pollution-intensive outputs. From 2005 to 2015, the decoupling state shifted to weak decoupling, as GHG growth slowed sharply to 2% (2005–2010) and 1% (2010–2015) while GOP surged by 20% and 11%, respectively. This transition was underpinned by the nationwide rollout of the Marine Economic Accounting System in 2007 and the 12th Five-Year Development Plan, which focused on energy efficiency, technological upgrades, and higher-value, lower-carbon marine economic activities32. After 2015, however, the sector returned to strong negative decoupling: GOP contracted by 10% relative to 2015 levels, while emissions remained 1% higher. This reversal may be linked to multiple factors, including the 2018 reorganization of the State Oceanic Administration into the Ministry of Natural Resources (which may have influenced statistical methodologies and regulatory priorities), the global economic slowdown, and the economic disruptions from the COVID-19 pandemic.

a Changes in GHG emissions and GOP, and decoupling states for each period at the national level. t0 and t represent the initial and final year of each period, respectively. b The decoupling states of marine economic sectors in coastal provinces over four periods.

Provincial decoupling patterns reveal marked heterogeneity (Fig. 2b). Shandong, Hainan, and Guangxi emerge as consistent leaders, largely because their marine economies are dominated by relatively low-carbon fisheries, such as capture fisheries and aquaculture, which account for 79%, 50%, and 79% of their respective provincial GOP. In particular, Hainan’s performance has been reinforced by its early policy commitment to ecological civilization and low-carbon development. As early as 2011, the provincial government emphasized expanding low-carbon marine industries and structural adjustment33, consolidating its position as the best-performing province among the 11 coastal regions after 2015. In contrast, Guangdong and Shanghai consistently lag behind the national average. Both provinces rely heavily on the high-carbon sector of maritime transportation, which accounts for 69% of Guangdong’s GOP and nearly 99% of Shanghai’s GOP. Guangdong remained in a weak negative decoupling state from 2000 to 2010, briefly improved to weak decoupling from 2010 to 2015, but slipped back to expansive negative decoupling from 2015 to 2020. Shanghai has remained behind or only on par with the national average since 2005. These contrasts highlight how economic structural composition and policy orientation jointly shape the divergent decoupling trajectories across provinces.

Energy intensity is a key to reducing marine economic sectors emissions

We used the Kaya-LMDI decomposition method to identify the drivers of marine sector emissions, with changes in each factor directly corresponding to changes in emissions. Nationally, energy consumption intensity (EI) was the only mitigating factor, reducing emissions by 118.4 Mt CO2e and offsetting 81.43% of the cumulative growth induced by other drivers during the past two decades (Fig. 3a). Conversely, the other four factors contributed to emissions growth, though varying in magnitude. Among these, marine sector labor productivity (MSLP), which was directly influenced by GOP, was the dominant growth contributor, responsible for 73.6 Mt CO2e (50% of the total growth). It grew rapidly from 2000 to 2015, then fell back slightly during 2015–2020, and ultimately increased by 113% over the study period (Supplementary Fig. 3). This reflects that higher productivity allowed each worker to generate more output, which in turn expanded energy demand and emissions when not accompanied by sufficient efficiency gains. The marine sector’s rising labor force also contributed: marine sector employment ratio (MSER) grew 48% and contributed 43.9 Mt CO2e to emissions (30% of the total growth). Population expansion (from 518 million in 2000 to 627 million in 2020) added 21.7 Mt CO2e, while emission intensity (ESI) played only a marginal role with 6.2 Mt CO2e emissions due to its relatively small degree of increase.

a National-scale decomposition of emission intensity (ESI), energy consumption intensity (EI), marine-sector labor productivity (MSLP), marine-sector employment ratio (MSER), and provincial population (PE). b Provincial-level decomposition of ESI, EI, MSLP, MSER, and PE.

At the provincial scale, the contributions of emission drivers exhibited clear geographic heterogeneity (Fig. 3b). Excluding Guangdong, EI reductions offset 33–139% of emission growth across coastal provinces. Whereas most provinces had experienced a downward trend in EI, Guangdong’s EI fell initially but rose again after 2014, as GOP growth lagged behind surging energy consumption (Supplementary Fig. 3). This reversal added 1.6 Mt CO2e (approximately 13% of net emissions growth), showing that efficiency improvements alone are insufficient if energy demand grows unchecked, and highlighting the need for stricter, region-specific regulations in Guangdong’s marine economy. Similarly, MSLP expanded on an annual basis in most provinces, contributing 22–65%. However, Liaoning’s stalled structural transformation and limited resource development34 led to a 63% decline in MSLP after 2012, turning its contribution to emissions negative. ESI made only marginal contributions in most provinces (−4.6 to +1.6 Mt CO2e), but in Tianjin, its sharp increase drove a disproportionate 27.0 Mt CO2e rise, highlighting inefficiencies in local energy use.

Emission peak pathways of China’s marine economic sectors vary across scenarios and provinces

Future GHG emissions predictions reveal that stricter mitigation efforts result in an earlier and lower GHG emissions peak in China’s marine economy (Fig. 4a). The SSP2, approximating current policies, is projected to peak near 2029 at approximately 150.5 Mt CO2e. Thereafter, the decline slows to around 1.7% per year, characterizing a linear‑gradual mitigation trajectory. Under the SSP1, emissions are projected to peak earliest, around 2025, at roughly 131.9 Mt CO2e. After this inflection, emissions decline sharply at about 3.1% per annum, yielding a cumulative reduction of 49.7 Mt CO2e by 2040 relative to the SSP2, and embodying a rapid‑inflection decarbonization profile. Under the SSP5, peak is deferred beyond 2034 and rises to about 174.2 Mt CO2e, and subsequently enters a protracted descent, reflecting a late‑and‑slow‑decline transition.

a National-level projections of future GHG emissions under three SSP pathways. b Provincial-level distribution of emissions peak times and magnitudes across coastal provinces under three pathways. Blank base map was made with Natural Earth (https://www.naturalearthdata.com/).

Aggressive decarbonization strategies under the SSP1 could advance the emissions peak by up to 4 years, reduce cumulative emissions by 18.6 Mt CO2e, and lower the peak level by 12%. Conversely, delayed action could postpone the peak by 5 years, thereby increasing cumulative emissions by 23.8 Mt CO2e and raising the peak by 14%. Such strategies encompass (i) the direct capital and operating expenditures for clean technology deployment and equipment retrofits, (ii) the opportunity costs from reduced output in carbon-intensive activities, and (iii) the policy and compliance costs associated with carbon pricing, emissions trading, and monitoring, reporting, and verification systems35. Although high emission reduction costs are often portrayed as a constraint on macroeconomic growth, this perspective overlooks the substantial economic and social benefits of avoided climate damages35. The average emission reduction cost is estimated at $90–120/t CO2e35, whereas the social cost of carbon due to delayed mitigation action is approximately $ 92–181/t CO2e36. The cumulative emission gaps between SSP1 and SSP5 reach 42.2 Mt CO2e, underscoring the substantial cost of delayed mitigation efforts.

Uncertainties in these projections stem primarily from variations in ESI, EI, and PE (Supplementary Fig. 4), particularly under the SSP2 scenario, where both peak timing (2026–2035) and peak magnitude (136.7–175.3 Mt CO2e) exhibit the widest confidence intervals. For the SSP1, the emissions peak is expected between 2022 and 2028, ranging from 126.4 to 143.2 Mt CO2e, while the SSP5’s peaks span 2031 to 2036 with a broader range of 159.9 to 193.4 Mt CO2e.

Regionally, the SSP1 enables most coastal provinces (excluding Guangdong and Shanghai) to attain emissions peak below 20 Mt CO2e (Fig. 4b) before 2030, followed by rapid declines (Supplementary Fig. 5). Under the SSP2, although over half of the coastal provinces could still peak relatively low (2.7–17.1Mt CO2e) by 2030, the emission peak occurs later and at a higher level compared with SSP1. Among them, Hebei exhibits the longest delay, with its peak postponed by up to 8 years. Guangdong’s peak, however, rises by 23% (8.0 Mt CO2e) relative to SSP1 (Supplementary Fig. 5). Importantly, neglecting marine sector decarbonization under SSP5 would not only increase peak values, but also postpone peaks in all coastal provinces beyond 2030. Notably, Guangdong’s emissions would not peak until 2040. Additionally, Tianjin, due to its highly emission-intensive marine economy, would see both a delayed peak time after 2030 and a peak value exceeding 20 Mt CO2e, standing out alongside Guangdong as one of the most challenging provinces for mitigation.

Discussion

Our findings indicate that, under the SSP1, the marine economic sectors could narrow the gap in China’s 2030 Nationally Determined Contributions by up to 20%37. This potential can be further enhanced with more ambitious sector-specific measures, such as imposing stricter growth limits38 to align with the Paris Agreement targets. In this scenario, China’s marine economic sectors emissions could peak by 2025, 4 years earlier than under the SSP2, with cumulative reductions reaching 42.8 Mt CO2e by 2040. Compared to the SSP5, the SSP1 scenario not only demonstrates a 24% lower emissions peak but also advances the peak by 9 years, underscoring both the urgency and cost-effectiveness of early intervention. However, historical emissions trends reveal that decoupling marine economic growth from emissions remains difficult, requiring targeted, climate-focused strategies that address sectoral and regional disparities.

To achieve the carbon peak target, technological innovation that reduces EI must be paired with effective measures to contain sectoral expansion. Since 2015, China has pursued EI policies for marine transport39 and supported the adoption of energy-saving technologies and low-carbon fuels40,41. However, these achievements have been substantially offset by rapid sectoral expansion. In particular, gains in MSLP, MSER, and PE42 have amplified aggregate output, generating a rebound effect where efficiency improvements lower unit emissions but rising scale drove up total emissions. This dynamic is particularly evident in the shipping sector, where a 30% reduction in EI during the 13th Five-Year Plan period (2016–2020) compared with the 12th Five-Year Plan (2011–2015) was offset by an average 6% annual growth in deadweight tonnage, leaving absolute emissions largely unchanged43,44. These findings highlight that productivity and scale expansion, rather than efficiency improvements alone, have been the primary drivers of emission growth, underscoring the necessity of coupling EI improvements with robust measures to constrain sectoral expansion.

Given this imperative, the design of future interventions should be guided by the distinct growth drivers, such as MSLP (efficiency-driven), MSER (input-driven), and PE (demand-driven), and by the mechanisms through which they influence emissions. For MSLP, institutional and cost-based constraints are needed to offset efficiency-driven expansion. One effective approach is the use of emissions trading systems that require firms to offset their emissions with allowances. Illustratively, the Shanghai carbon market has incorporated maritime transportation since 2016, with sector-specific allowance transactions reaching 770,000 tonnes in 202345. For MSER, targeted regulation and optimized labor allocation can prevent disorderly expansion. China’s push for digitalization and automation reduces labor requirements46, as demonstrated by Jiaxing Port’s automated river-sea intermodal terminal, which employs autonomous guided vehicles and intelligent remote-control systems47. For PE, fiscal instruments are key in moderating both demand volume and structure. Incremental increases in China’s refined oil product consumption tax since 2015, including a fuel oil tax rise from 1.1 to 1.2 yuan/liter and a scheduled import tariff increase from 1% to 3% by 202548, have raised operational costs and directly suppressed vessel fuel demand. These higher costs incentivize shipping firms to optimize routes, consolidate voyages, or transition to cleaner fuels without expanding fleet capacity, thereby curbing total end-use energy demand.

Building upon these sectoral mechanisms, emission-reduction strategies should also be tailored to the specific challenges of each pathway. Under the SSP1 scenario, EI remains the dominant driver of peak magnitude (37% contribution) (Supplementary Fig. 6), reflecting the importance of clean technology substitution49. PE plays an equally critical role, contributing 44% to shifting the emissions peak year. By strategically optimizing population settlement and resource demand in coastal regions, the effectiveness of technological mitigation measures can be amplified. This dual mechanism under SSP1 necessitates mitigation strategies that prioritize the systemic deployment of renewable energy infrastructure and carbon-neutral technologies, alongside structural demand-side reforms through coastal urban planning and consumption pattern realignment. In contrast, the SSP5 entrenches carbon lock-in dynamics, where emission intensity exerts a dominant 54% influence on peak delays, prolonging mitigation timelines by 3–6 years through persistent fossil fuel dependence. Moreover, the high labor employment rate in traditional high-carbon sectors drives 25% of emissions peak magnitude, perpetuating carbon-intensive growth trajectories. To disrupt this dual mechanism, mitigation strategies must enforce stringent workforce transition protocols, including mandatory reductions in fossil-sector employment quotas. Additionally, displaced workers should be rapidly redeployed into emerging low-carbon industries, particularly offshore carbon capture and storage (CCS) systems46,50, which project 721.9 Mt CO2e annual sequestration capacity by 2040 under the fossil-fueled development pathway constraints51. For the SSP2 scenario, peak magnitude is primarily influenced by labor productivity (35% contribution), while peak timing is governed by labor employment rates (43% contribution). These factors are closely interrelated: increased employment in traditional high-carbon sectors delays the emissions peak, while improvements in labor productivity often drive industrial expansion, thereby elevating emissions. To reconcile this growth-emission nexus, mitigation strategies must adopt synchronized interventions: (1) targeted reallocation of high-carbon workforce into emerging sectors like offshore renewables and blue carbon monitoring through subsidized retraining programs, and (2) implementation of stringent productivity standards that mandate emission-intensity reductions through low-carbon technologies to decouple economic growth from emissions.

Regional variations in emission drivers necessitate localized policy adaptations in emission reduction strategies (Supplementary Fig. 7). Guangdong’s emissions trajectories under the SSP1 and the SSP2 closely mirror national trends, reflecting its important role in shaping national emissions. In contrast, in other provinces, the choice of scenario pathway markedly alters the sensitivity of key drivers to peak magnitude. Broadly, densely populated provinces tend to exhibit stronger demand- or consumption-related sensitivities under the sustainability pathway, whereas sparsely populated provinces show heightened population-driven impacts under fossil-dependent development. For instance, under the SSP1, the contribution of PE to peak magnitude in Shandong and Hebei increases sharply by 78% and 71% respectively, compared to the SSP5, reflecting the amplification of demand-side pressures in provinces that together account for 28% of the coastal population. In contrast, in Hainan, which represents only 1.5% of the coastal population, the contribution of population to peak magnitude rises by 77% under the SSP5 relative to the SSP1, indicating that in low-population contexts, fossil-dependent growth disproportionately magnifies the role of demographic change. Changes in driver sensitivity for peak timing are less regular, but EI shows the most pronounced variation. In Zhejiang, its sensitivity to peak timing under SSP1 increased by 85% and 81% compared with the SSP5 and the SSP2, respectively. This far surpasses the second-ranked Hainan, whose corresponding increases were only 40% and 30%. These results suggest that Zhejiang’s earlier peak would require accelerated low-carbon energy development. Overall, under the SSP5, these regional differences diminish notably, with provincial emission trajectories converging towards national averages—a reflection of the homogenizing effects of fossil fuel dependency. This spatial analysis provides two critical insights: Firstly, national mitigation frameworks must incorporate place-specific mechanisms via differentiated emission allocation protocols. Secondly, the convergence trend under the SSP5 underscores the climate resilience advantages of diversified development models. In Guangdong, where carbon-intensive industries dominate, strategies should prioritize sectoral containment through maritime carbon budgets and expedited adoption of clean port technologies. Meanwhile, other provinces should focus on targeted interventions for energy efficiency upgrades and workforce transitions to low-carbon marine sectors, leveraging local comparative advantages.

We acknowledge that the lack of detailed, industry-specific statistics constrained the scope of emission drivers. Specifically, the absence of granular data, such as the composition of fuel types in fleets or R&D expenditure52, likely hindered our ability to capture the effects of technological progress, equipment upgrades, and local policies on energy and emission intensity. Future research should improve the granularity of energy consumption and emission statistics through collaborations with industry associations, enterprise-level microdata, or remote sensing, and integrate these datasets with advanced decomposition methods to enhance attribution accuracy. While sectoral level indicators (e.g., GOP, LF) may contain measurement uncertainties, consistent definitions and long-term comparability help mitigate their effects on our results. Nonetheless, these limitations do not undermine the robustness of our key conclusions.

Despite these limitations, this study introduces an integrated analytical framework that regards marine economies as important yet underexplored areas in global climate governance. It challenges the common assumption used when projecting emission reduction pathways of marine economic sectors. Previous studies typically treated emission reduction curves as static across sectors and scenarios17,38. Our findings indicate that emission reduction pathways exhibit noticeably intertemporal variations, and accounting for such dynamics is essential for identifying the sectors’ emission reduction potential. It elucidates the complex interactions between emission drivers and mitigation strategies in China’s coastal regions. Our findings show that achieving sustainable transitions requires systemic reforms targeting the fundamental causes of emissions, rather than just incremental efficiency improvements. These reforms include redefining productivity benchmarks to emphasize emission efficiency over industrial expansion, speeding up workforce shifts away from carbon-heavy industries, and enhancing marine spatial governance to prevent clustering of high-emission sectors. Although derived from China’s coastal provinces, these insights can be applied to develop strategies for aligning global blue economies with climate goals—particularly through spatial planning, proactive workforce adaptation, and comprehensive demand-side measures. The urgency lies not in small adjustments but in fundamentally rethinking marine governance frameworks to ensure that economic growth remains sustainable.

Methods

GHG emissions from marine economic sectors

This study quantified three GHG emissions (CO2, N2O, and CH4) from China’s five principal marine economic sectors across 11 coastal provinces (2000–2020) through an integrated life-cycle assessment framework. These provinces, supported by abundant resources, well-developed infrastructure, and supportive policies, collectively represent the entirety of China’s marine economy. They are geographically categorized into three economic circles: the North (Liaoning, Hebei, Tianjin, and Shandong), the East (Jiangsu, Zhejiang, and Shanghai), and the South (Fujian, Guangdong, Guangxi, and Hainan) (Supplementary Fig. 8). The five pivotal economic sectors—maritime transportation, marine capture fishery, marine aquaculture, offshore oil and gas production, and ocean renewables—formed the backbone of China’s marine economy between 2000 and 2015, collectively accounting for 41–77% of its total output53 and supporting over 7 million coastal jobs54. Although coastal tourism surpassed its combined economic contribution after 2016, this sector is excluded due to ambiguities in attributing emissions specifically to marine activities. GHG emissions were converted into CO₂-equivalents using global warming potential indexes from the IPCC AR6 guidelines.

For the maritime transport sector, we calculated GHG emissions using the International Maritime Organization’s Well-to-Wake framework, which encompasses the full life cycle emissions from upstream fuel production and vessel operation to downstream effects.

Where FTV is the freight turnover volume (tkm); \({{EI}}_{{transportation}}\) represents the GHG emission intensity under freight shipping in the total life cycle (t CO2e/MJ); \(\omega\) means the conversion factor from ce to J (1 kg ce=29.27 MJ); CF is the energy consumption intensity (t ce/tkm).

Emissions from the marine capture fishery sector include emissions from the capture of fuel production throughout the operational life cycle of a fishing vessel.

Where \({C}_{{fishery}}\) means the fishing catch (t), \({{EI}}_{{fishery}}\) means the GHG emission intensity (t CO2e/t catch).

Emissions from the marine aquaculture sector include GHG from all inputs (e.g. feed production, energy use) during farming (from seeding to harvesting).

Where \({E}_{{aquaculture}}\) is the GHG emissions from marine aquaculture (t), \({P}_{a}\) means the aquaculture production (t), \({EI}\) means the GHG emission intensity of aquaculture (t CO2e/t production).

Emissions from the renewable energy sector cover the manufacturing, installation, operation, maintenance, and decommissioning of infrastructure for offshore wind power and tidal current energy.

Where \({EO}\) represents the carbon dioxide emissions of ocean energy (g), \({{EO}}_{i}\) means carbon emission of different types of ocean energy(g) (offshore wind, wave, tidal, and current). \(C\) is power capacity of ocean energy (kW), \(H\) means operation time of the equipment every year (hour), \({RO}\) presents the lifecycle emissions rate of ocean energy (g CO2e/kWh).

GHG from offshore oil and gas production is calculated using production data and emission intensity, including emissions from processes such as capture exploration, extraction, processing, and refining (e.g., the upstream portion).

Where \({P}_{{oil}}\) and \({P}_{{gases}}\) means the offshore crude oil and gases production (boe), \({{EI}}_{{oil}}\) and \({{EI}}_{{gases}}\) means the GHG emission intensity of offshore oil and gas production (g CO2e/MJ), \(f\) means the conversion factor from boe to J (1 barrel of crude oil = 6.193 GJ).

We defined the calculated boundaries and detailed data sources for each sector (Supplementary Table 1 and 2).

Decoupling analysis

We used Tapio’s decoupling model based on an elasticity approach to quantify the relationship between changes in GHG emissions and gross ocean product (GOP), addressing whether marine economic growth occurs independently of rising emissions55. The decoupling index (D) is defined as:

Where ΔE and ΔGOP represent the change in marine economic sectors’ emissions and gross ocean product, respectively, from a base year o to a target year t respectively.

We classified the decoupling states into eight categories based on three indicators (ΔE, ΔGOP, and D)55, ranging from strong decoupling (the ideal state where emissions decrease as economic growth continues) to strong negative decoupling (the worst state, where emissions increase while the economy contracts) (Supplementary Fig. 9 and Supplementary Table 3).

Decomposition analysis

The Kaya identity is renowned for its conceptual simplicity, residue-free decomposition, and clear representation of key driving factors such as population, economic activities, energy efficiency, and emissions intensity56,57.

where C presents the total emissions. \(\frac{C}{E}\) is the carbon emission intensity of energy, representing the ratio of emission (C) to energy consumption (E), and reflects the emission coefficient. \(\frac{E}{{GDP}}\) is the energy intensity, the ratio of energy consumption to gross domestic product (GDP). \(\frac{{GDP}}{P}\) represents the economic development, which is the ratio of GDP to population size, while P denotes population size.

In this study, we extended the conventional Kaya identity to capture the unique dynamics of the marine economic sectors. PE denotes coastal provincial population size. Specifically, we replaced GDP with GOP as it can more accurately reflect the changes in the output value of the marine economic sectors. We converted the energy consumption (\({E}_{{nergy}}\)) of each marine economic sector using emission coefficients. In sector-level empirical analyses, industrial carbon emissions are driven not only by population size but also by labor input58. Accordingly, we incorporate the labor force (LF) in the marine economic sector into the metrics. This extension refines the pathway linking sector scale to emissions and enhances the policy relevance of our findings. The inclusion of LF generates two additional driving factors: marine economic sectors labor productivity (MSLP, GOP/LF), which proxies economic activity, and marine economic sectors employment rate (MSER, LF/PE), which represents sectoral development dynamics. Meanwhile, the continued use of PE indicators reflects the dependence of each coastal province on marine resources. All underlying GOP and LF data are obtained from official sectoral statistics, ensuring that the decomposition is grounded in the internal dynamics of the marine economic sectors rather than in aggregated macroeconomic measures. The extended Kaya identity is expressed as follows:

Where each variable represents key driving factors such as ESI (\(\frac{{E}_{{ocean}}}{{E}_{{nergy}}}\)), EI (\(\frac{{E}_{{nergy}}}{{GOP}}\)), MSLP (\(\frac{{GOP}}{{LF}}\)), MSER (\(\frac{{LF}}{{PE}}\)) and PE (provincial population). We use official marine sectors data to calculate driver values (Supplementary Table 4).

We applied the LMDI method59 based on the extended Kaya identity to evaluate each driving factor’s contribution to in GHG emissions changes. LMDI is chosen for its precise decomposition capacity, accurately attributing emissions changes to specific driving forces50,60. Using the additive form of LMDI, the total emissions change (\(\Delta {E}_{{ocean}}\)) is expressed as:

where \(\Delta {E}_{{ocean}}\) represents the change value of total emissions of marine economic sectors from t0 to t; the subscripts ESI, EI, MSLP, MSER, and PE represent the effects contributed by the above five factors, respectively.

The specific calculations of these factors are expressed as follows:

Multi-scenario analysis based on the Shared Socioeconomic Pathways

To predict the emission trajectory of the marine economy from 2021 to 2040, we integrated the extended Kaya identity with three shared socioeconomic pathways (SSPs) scenarios. The SSPs framework defines futures along two axes: challenges to climate mitigation and challenges to adaptation61. In this study, we focus on contrasting mitigation stringency while keeping adaptation challenges low, in order to investigate the effects of decarbonization policies on marine economy sectors. Accordingly, we selected three representative pathways: the SSP1 (high mitigation), the SSP2 (medium mitigation) and the SSP5 (low mitigation). The SSP1 represents a sustainability pathway characterized by strict energy conservation and emissions reduction plans to achieve national dual carbon goals. The SSP2 reflects a middle-of-the-road pathway in which energy consumption, technological development, and population size largely follow historical trajectories, with marine policies remaining broadly consistent with past practices. The SSP5 is a fossil-fueled development pathway, where rapid economic growth is prioritized and marine economic activities highly depend on fossil fuels and human capital, with limited adoption of green and low-carbon measures.

To minimize subjectivity in scenario design, we used official SSP assumptions and datasets to determine scenario parameters. We adopted PE projections from Chen et al.62 to analyze the demographic changes under different SSPs. As there is no existing literature or data on future MSER, we adopted a proxy approach based on demographic trends. Since changes in the working-age population (aged 16–64) profoundly impact the labor market and the broader economy, we assumed that MSER under the SSP1, SSP2, and SSP5 would align with the projected working-age population share for each province, also obtained from Chen et al.62. Subsequently, MSLP was calculated for each SSP scenario by combining provincial GDP projections from Tong et al.63 (as a proxy for GOP) with the estimated LF, which is defined as a function of total population, labor force participation rate, and MSER. Annual change rates of these parameters were subsequently derived and integrated into the extended Kaya identity using the derivative method (see Supplementary Note 1 for detailed equations).

China’s national policy, as outlined in the 14th Five-Year Plan for National Economic and Social Development and the Long-Range Objectives Through the Year 2035, mandates continuous carbon emission reductions64. Reflecting this overarching directive, we assumed that both EI and ESI would decline across all scenarios. To operationalize this, EI and ESI were scaled using scenario-specific annual adjustment rates, calibrated to reflect the relative stringency of decarbonization efforts: high under SSP1, medium under SSP2, and low under SSP5 (Supplementary Table 5). This approach is consistent with methodologies established in prior studies65,66.

To solve systematic uncertainties in the scenario parameters, we employed Monte Carlo simulations (100,000 iterations) to quantify confidence intervals (Supplementary Note 2). Parameter variances were standardized through inter-scenario differential analysis, with deviations in SSP2 benchmarked against the SSP1/SSP5 maximum relative differences in 2040, and other scenarios were scaled by the time dimension (Supplementary Note 3). Finally, we visualized the changing trends across these five driving indicators at both national and provincial scales for each pathway from 2021 to 2040.

Supplementary information

Details on derivation formula of change rate of MSER and MSLP in SSPs scenarios (Supplementary Note 1); sensitivity analysis of Monte Carlo simulation method (Supplementary Note 2); details on multi-scenario analysis uncertainty range (Supplementary Note 3); study schematic (Supplementary Fig. 1); GHG emission in coastal regions (Supplementary Fig. 2); annual decomposition analysis of GHG emission in coastal regions (Supplementary Fig. 3); the change trends and uncertainty intervals of driving factors of China’s marine economic sectors under SSPs scenarios (Supplementary Fig. 4); prediction of the emission trajectories of marine economic sectors in China's coastal region (Supplementary Fig. 5); the contribution of driving factors to the peak time and magnitude of emissions in China and coastal regions’ marine economic sectors (Supplementary Fig. 6 and 7); the study area of 11 Chinese coastal regions (Supplementary Fig. 8); eight decoupling states between marine economy and GHG emissions and the explanations of eight specific decoupling states (Supplementary Fig. 9 and Supplementary Table 3); system boundaries for marine economic sectors emission caculations (Supplementary Table 1); the detailed description and data sources (Supplementary Table 2); description of the variables and resources in extended Kaya identity (Supplementary Table 4); parameter setting for each factor in different pathways (Supplementary Table 5).

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

All data for figures supporting this study have been deposited in Zenodo and are publicly available at 10.5281/zenodo.17388569. The repository contains provincial-level sectoral emissions (2000–2020), tapio decoupling indices (2000–2020), LMDI decomposition contributions (2000–2020), and probabilistic scenario trajectories (2020–2040).

References

Eyzaguirre, C. V. & Prabhakar, D. Advancing the Potential of Sustainable Ocean-Based Economies: Trade Trends, Market Drivers and Market Access. https://unctad.org/system/files/official-document/ditctedinf2021d2_en.pdf (2021).

UNCTAD. The ocean economy is booming. But for how long? United Nations Trade and Development https://unctad.org/news/ocean-economy-booming-how-long (2025).

Chen, J., Fei, Y. & Wan, Z. The relationship between the development of global maritime fleets and GHG emission from shipping. J. Environ. Manag. 242, 31–39 (2019).

Hachem, J. et al. Exhaust gas recirculation applied to single-shaft gas turbines: An energy and exergy approach. Energy 238, 121656 (2022).

Stewart, R. J. & Haszeldine, R. S. Can Producing Oil Store Carbon? Greenhouse Gas Footprint of CO2EOR, Offshore North Sea. Environ. Sci. Technol. 49, 5788–5795 (2015).

Walker, T. R. et al. Chapter 27 - Environmental Effects of Marine Transportation. in World Seas: An Environmental Evaluation (Second Edition) (ed. Sheppard, C.) 505–530 (Academic Press, 2019).

Sofiev, M. et al. Cleaner fuels for ships provide public health benefits with climate tradeoffs. Nat. Commun. 9, 406 (2018).

Feng, C., Ge, S., Zeng, J., He, L. & Ye, G. Mapping the Global Carbon Emissions of Marine Sectors. Environ. Sci. Technol. 58, 18508–18519 (2024).

IMO. Fourth Greenhouse Gas Study 2020. https://www.imo.org/en/OurWork/Environment/Pages/Fourth-IMO-Greenhouse-Gas-Study-2020.aspx (2021).

IMO. UN body adopts climate change strategy for shipping. https://www.imo.org/en/MediaCentre/PressBriefings/Pages/06GHGinitialstrategy.aspx (2018).

OECD. The Ocean Economy in 2030. https://doi.org/10.1787/9789264251724-en (2016).

Dettner, F. & Hilpert, S. Modelling CO2 emissions and mitigation potential of Northern European shipping. Transp. Res D.-Tr. E 119, 103745 (2023).

Lindstad, E., Lagemann, B., Rialland, A., Gamlem, G. M. & Valland, A. Reduction of maritime GHG emissions and the potential role of E-fuels. Transp. Res D.-Tr. E 101, 103075 (2021).

Bouman, E. A., Lindstad, E., Rialland, A. I. & Strømman, A. H. State-of-the-art technologies, measures, and potential for reducing GHG emissions from shipping – A review. Transp. Res D.-Tr. E 52, 408–421 (2017).

Wang, X.-T. et al. Trade-linked shipping CO2 emissions. Nat. Clim. Chang. 11, 945–951 (2021).

Li, Z. et al. Reducing carbon footprint of deep-sea oil and gas field exploitation by optimization for Floating Production Storage and Offloading. Appl Energ. 261, 114398 (2020).

Feng, C. et al. The contribution of ocean-based solutions to carbon reduction in China. Sci. Total Environ. 797, 149168 (2021).

Hoegh-Guldberg, O. et al. The ocean as a solution to climate change: Five opportunities for action. in The Blue Compendium: From Knowledge to Action for a Sustainable Ocean Economy (eds. Lubchenco, J. & Haugan, P. M.) 619–680 (Springer International Publishing, Cham, 2023).

Gao, X., Zhu, A. & Yu, Q. Exploring the carbon abatement strategies in shipping using system dynamics approach. Sustainability 15, 13907 (2023).

Wada, Y., Yamamura, T., Hamada, K. & Wanaka, S. Evaluation of GHG Emission Measures Based on Shipping and Shipbuilding Market Forecasting. Sustainability 13, 2760 (2021).

Müller-Casseres, E. et al. International shipping in a world below 2 °C. Nat. Clim. Chang. 14, 600–607 (2024).

Chen, X., Di, Q., Hou, Z. & Yu, Z. Measurement of carbon emissions from marine fisheries and system dynamics simulation analysis: China’s northern marine economic zone case. Mar. Policy 145, 105279 (2022).

Jing, D. et al. CO2 emission projection for arctic shipping: A system dynamics approach. Ocean Coast Manag. 205, 105531 (2021).

Chen, Z. S., Lam, J. S. L. & Xiao, Z. Prediction of harbour vessel emissions based on machine learning approach. Transp. Res D.-Tr. E 131, 104214 (2024).

Cammin, P., Yu, J. & Voß, S. Tiered prediction models for port vessel emissions inventories. Flex. Serv. Manuf. J. 35, 142–169 (2023).

Lau, Y., Chen, Q., Poo, M. C.-P., Ng, A. K. Y. & Ying, C. C. Maritime transport resilience: A systematic literature review on the current state of the art, research agenda and future research directions. Ocean Coast Manag. 251, 107086 (2024).

Su, S., Tang, Y., Chang, B., Zhu, W. & Chen, Y. Evolution of marine fisheries management in China from 1949 to 2019: How did china get here and where does china go next? Fish Fish 21, 435–452 (2020).

GWEC. Global Wind Report 2024. https://powerlibrary.theelectricityhub.com/2024/04/16/gwec-global-wind-report-2024/ (2024).

Zia, H. Guangdong – a key hub on the maritime silk road. https://global.chinadaily.com.cn/a/201809/25/WS5ba9e159a310c4cc775e7fbc.html (2018).

Kang, B. et al. Fisheries in Chinese seas: What can we learn from controversial official fisheries statistics? Rev. Fish. Biol. Fish. 28, 503–519 (2018).

National Bureau of Statistics of China. China Port Yearbook 2008. (People’s Communications Press, Shanghai, 2009).

China Briefing. China releases 12th five-year plan for the marine economy. https://www.china-briefing.com/news/china-releases-12th-five-year-plan-for-the-marine-economy/ (2013).

The People’s Government of Hainan Province. Opinions of the People’s Government of Hainan Province on Low-Carbon Development. https://www.hainan.gov.cn/hainan/szfwj/201103/865c48449ec84bf58bada2e396125a98.shtml?ddtab=true (2011).

Xu, S. Strategic exploration of marine economic development in liaoning. in Proceedings of 2013 IEEE International Conference on Service Operations and Logistics, and Informatics 563–566. https://doi.org/10.1109/SOLI.2013.6611477 (2013).

Shukla, P. R. et al. Climate Change. 2022: Mitigation of Climate Change. https://www.ipcc.ch/report/ar6/wg3/ (2022).

Kalkuhl, M. & Wenz, L. The impact of climate conditions on economic production. Evidence from a global panel of regions. J. Environ. Econ. Manag 103, 102360 (2020).

Climate Analytics. What is China’s pathway to limit global warming to 1.5 °C? https://1p5ndc-pathways.climateanalytics.org/countries/china/ (2024).

Hoegh-Guldberg, O. et al. The Ocean as a Solution to Climate Change: Updated Opportunities for Action. (World Resources Institute, Washington, D.C., 2023).

Liu, H., Mao, Z. & Li, X. Analysis of international shipping emissions reduction policy and China’s participation. Front Mar. Sci. 10, 1093533 (2023).

Global Times. China delivers world’s first FPSO vessel with carbon capture, storage system - global times. https://www.globaltimes.cn/page/202502/1328757.shtml (2025).

Hu, M. & Dong, Y. China’s shipping emissions governance: Status and prospects under the dual carbon goal. Front Mar. Sci. 11, 1405312 (2024).

Zhong, S. & Su, B. Assessing the effects of labor market dynamics on CO2 emissions in global value chains. Sci. Total Environ. 768, 144486 (2021).

UNCTAD. Merchant fleet by flag of registration and by type of ship, annual. https://unctadstat.unctad.org/datacentre/reportInfo/US.MerchantFleet (2025).

Xinde Marine News. COSCO Shipping has adopted these methods and technologies for carbon emission reduction. https://www.xindemarinenews.com/topic/yazaishuiguanli/32056.html (2021).

ICAP. China - shanghai pilot ETS. https://icapcarbonaction.com/en/ets/china-shanghai-pilot-ets (2024).

State Council of the People’s Republic of China. Outline of the National Comprehensive Multi-dimensional Transportation Network Plan. https://www.gov.cn/gongbao/content/2021/content_5593440.htm (2021).

Portnews. Jiaxing port adds a new sea-river intermodal operation area. https://en.portnews.ru/news/369727/ (2024).

Xu, D. Rising fuel oil tax burden forces Chinese independent refineries to scale back operations. S&P Global Commodity Insights https://www.spglobal.com/commodity-insights/en/news-research/latest-news/crude-oil/022025-rising-fuel-oil-tax-burden-forces-chinese-independent-refineries-to-scale-back-operations (2025).

Riahi, K. et al. The shared socioeconomic pathways and their energy, land use, and greenhouse gas emissions implications: An overview. Glob. Environ. Chang 42, 153–168 (2017).

Luo, X., Liu, C. & Zhao, H. Driving factors and emission reduction scenarios analysis of CO2 emissions in Guangdong-Hong Kong-Macao Greater Bay Area and surrounding cities based on LMDI and system dynamics. Sci. Total Environ. 870, 161966 (2023).

Sun, L. et al. Source-sink matching and cost analysis of offshore carbon capture, utilization, and storage in China. Energy 291, 130137 (2024).

Liu, J., Yang, Q., Ou, S. & Liu, J. Factor decomposition and the decoupling effect of carbon emissions in China’s manufacturing high-emission subsectors. Energy 248, 123568 (2022).

Ministry of Natural Resources of the PRC. China Marine Economic Statistics Bulletin. https://www.mnr.gov.cn/sj/sjfw/hy/gbgg/zghyjjtjgb/ (2016).

Ministry of Natural Resources of the PRC. China Marine Statistical Year Book 2017. (China Ocean Press, 2018).

Shuai, C., Chen, X., Wu, Y., Zhang, Y. & Tan, Y. A three-step strategy for decoupling economic growth from carbon emission: Empirical evidences from 133 countries. Sci. Total Environ. 646, 524–543 (2019).

Bersalli, G., Tröndle, T. & Lilliestam, J. Most industrialised countries have peaked carbon dioxide emissions during economic crises through strengthened structural change. Commun. Earth Environ. 4, 1–11 (2023).

Yang, J. et al. Driving forces of China’s CO2 emissions from energy consumption based on kaya-LMDI methods. Sci. Total Environ. 711, 134569 (2020).

Hao, Y., Zhang, Z.-Y., Yang, C. & Wu, H. Does structural labor change affect CO2 emissions? Theoretical and empirical evidence from China. Technol. Forecast Soc. 171, 120936 (2021).

Ang, B. W., Zhang, F. Q. & Choi, K. H. Factorizing changes in energy and environmental indicators through decomposition. Energy 23, 489–495 (1998).

Lu, Z.-L., Wang, L.-L., Guo, X.-P., Pang, J. & Huan, J.-J. Decoupling effect and influencing factors of carbon emissions in China: Based on production, consumption, and income responsibilities. Adv. Clim. Chang Res. 15, 1177–1188 (2024).

O’Neill, B. C. et al. A new scenario framework for climate change research: The concept of shared socioeconomic pathways. Climatic Change 122, 387–400 (2014).

Chen, Y. et al. Provincial and gridded population projection for China under shared socioeconomic pathways from 2010 to 2100. Sci. Data 7, 83 (2020).

Jiang, T. et al. National and provincial population and economy projection databases under shared socioeconomic pathways(SSP1-5)_v2. Science Data Bank. https://doi.org/10.57760/sciencedb.01683 (2024).

The State Council of the People’s Republic of China. China’s 14th Five-Year Plan. https://en.ndrc.gov.cn/policies/202203/P020220315511326748336.pdf (2021).

Wang, D., He, W. & Shi, R. How to achieve the dual-control targets of China’s CO2 emission reduction in 2030? Future trends and prospective decomposition. J. Clean. Prod. 213, 1251–1263 (2019).

Liu, C. & Zhang, Y. China’s carbon emission prediction from the perspective of shared socioeconomic pathways and machine learning. Energy Strateg Rev. 60, 101778 (2025).

Acknowledgements

This research was supported by Ministry of Science and Technology of the People’s Republic of China (2023YFE0113105), National Natural Science Foundation of China (42176216), Science Technology Department of Zhejiang Province (2024C03235) and (2023C03119), and China Postdoctoral Science Foundation (2023M743061).

Author information

Authors and Affiliations

Contributions

S.G.: conceived and designed the study; acquired and compiled the data; conducted the analyses and produced the figures; led the drafting of the manuscript; interpreted the results; reviewed and approved the manuscript prior to submission. L.H.: supervised the project; co-designed the study; contributed to result interpretation; reviewed and approved the manuscript prior to submission. C.F.: supervised the project; reviewed the manuscript. G.Y.: supervised the project; reviewed the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests

Peer review

Peer review information

Communications Earth & Environment thanks Yixin Hu and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. Primary Handling Editors: I-Yun Hsieh and Alice Drinkwater. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

43247_2025_2967_MOESM2_ESM.docx (download DOCX )

Supplementary Materials for Sustainability pathways enable China's marine economic sectors to reach a 2030 emissions peak

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Ge, S., He, L., Feng, C. et al. Sustainability pathways enable China’s marine economic sectors to reach a 2030 emissions peak. Commun Earth Environ 6, 1004 (2025). https://doi.org/10.1038/s43247-025-02967-x

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s43247-025-02967-x