Abstract

Hydrogen-based direct reduced iron (H2-DRI) is crucial for decarbonizing the steel sector but is limited by the availability of renewable energy. Here, we propose H2-DRI deployment schemes in China’s steel sector at moderate and aggressive scales, incorporating three renewable energy sources with a resolution of 1 km × 1 km across 570 steel units. Results indicate that 52.6–55.8% of China’s current steel units lack sufficient renewable energy supply for H2-DRI deployment due to uneven distribution of these energy sources. Renewable energy can fulfill 97-100% of hydrogen demand at the moderate scale, whereas the aggressive scale requires supplemented fossil fuels accounting for one-third to one-half. H2-DRI can decarbonize steel production to 0.15–0.91 t CO2 t-1 steel at the moderate scale, but the emissions would raise by up to over sixfold at the aggressive scale. Furthermore, H2-DRI fueled by solar and wind energy exhibits poorer economic and water usage performance at the aggressive scale. We highlight the necessity of avoiding excessive H2-DRI deployment and recommend prioritizing its implementation in steel units located in regions with abundant solar and wind sources nearby.

Similar content being viewed by others

Introduction

The steel sector is carbon-intensive and contributes to 7% of global carbon emissions1. The low-carbon transition of the steel sector is crucial for achieving both the global 1.5 °C and regional net-zero emissions targets2,3. However, the steel sector is a typical hard-to-abate sector since it traditionally relies heavily on fossil fuels as both energy sources and reducing agents4,5. Hydrogen-based direct reduced iron (H2-DRI) technology uses hydrogen to directly reduce iron ore, with pig iron products then used in steel production via electric arc furnace (EAF)6,7. This technology holds great promise for retrofitting the steel sector, as it can significantly mitigate carbon emissions by replacing fossil fuels with hydrogen. It is estimated that H2-DRI will account for over one-third of primary steel production by 20508,9.

A sufficient green hydrogen supply is essential for H2-DRI technology to enable low-carbon steel production. Currently, fossil-based methods such as coal gasification and steam methane reforming (SMR) account for 83% of global hydrogen production10, but they have high carbon intensities. In this situation, the use of fossil-based hydrogen would substantially weaken the carbon mitigation effectiveness of H2-DRI technology as it leads to numerous indirect emissions11,12. In contrast, green hydrogen, produced from renewable energy sources such as solar, wind, and biomass, generates significantly fewer carbon emissions, making it well-suited for retrofitting the steel sector13,14,15.

The uneven spatial distribution of the renewable energy resources poses a challenge to the deployment of H2-DRI technology. Given that hydrogen is combustible and unstable, large-volume and long-distance transportation of hydrogen has not yet been widely promoted16,17. Therefore, the hydrogen required for H2-DRI should be produced on-site utilizing nearby renewable energy sources. However, significant spatial heterogeneity exists in renewable energy supply due to varying natural resource endowments such as sunlight irradiation, wind power, and biomass stock. Furthermore, current steel production units are typically located near urban areas rather than in regions with abundant renewable energy sources, such as deserts or grasslands. Consequently, the spatial matching between renewable energy supply and demand should be considered in the deployment of H2-DRI technology. Previous studies have proposed H2-DRI deployment schemes for the steel sector at global and national scales18,19,20,21,22,23, while few have considered the spatial characteristics of the renewable energy sources and the steel units. As a result, these schemes might be too ambitious as they have to rely on supplemented fossil fuels, resulting in weakened carbon mitigation effects.

Meanwhile, H2-DRI involves numerous water consumption for renewable energy generation and hydrogen production24,25, leading to trade-offs between carbon reduction and water usage. These trade-offs might be particularly noticeable in regions with high steel outputs and limited water resources. For example, the provinces with the largest steel output in China - Hebei, Shandong, Liaoning, and Shanxi Province - account for over 45% of steel production, yet they have only ~10% of the national water supply26. While previous studies have revealed the water pressures from hydrogen production27,28,29, those associated with the H2-DRI technology, including the water consumption from renewable energy supply, hydrogen production, and relating regional water pressure, have not been fully investigated.

Here, we propose the deployment schemes of H2-DRI technology by considering the spatial matching of renewable energy supply and demand at a high-resolution scale. We focus on China’s steel sector, which accounts for 53.9% of global steel production outputs and contributes over 15% of domestic carbon emissions30,31. The deployment of H2-DRI technology is essential for decarbonizing China’s steel sector, as the conventional blast furnace - basic oxygen furnace (BF-BOF) method currently accounts for over 90% of China’s steel outputs, significantly higher than the global average of 71.1%32. We establish a China’s steel unit database and evaluate the supply potential of three types of renewable energy sources at a 1 km × 1 km scale. Utilizing this data, we develop a renewable energy supply-demand model to propose optimal deployment schemes of H2-DRI, aiming at meeting 2050 targets at the lowest cost. The carbon mitigation effects, economic costs, and water consumption of these schemes are then evaluated. We reveal that the mitigation effects of H2-DRI are affected by the renewable energy supply, and demonstrate the necessity in setting appropriate deployment scales for this technology in China’s steel sector.

Results

Spatial distribution of steel units and renewable energy sources

We establish a China’s steel production unit database, including the geographical locations, process, equipment, and production outputs of each steel unit. The spatial distribution of ironmaking units is analyzed as they are the core for primary steel production, including 570 units in 219 plants (Fig. 1a). The steel outputs from these units are 831.22 Mt yr-1, lower than the statistics at 918.21 Mt yr-1, mainly due to the exclusion of some units that have been announced for retirement32. The distribution of these units is spatially uneven. Hebei Province contributes 25.6% of domestic outputs, despite occupying less than 2% of the land area. Jiangsu and Liaoning Province rank as the second and third largest steel producers, accounting for 10.7% and 7.8% of steel outputs, respectively. In terms of production method, there are only a few H2-DRI projects so far, while the traditional BF-BOF method accounts for over 99% of primary steel outputs.

a Spatial distribution of steel units in China. Each point is a steel plant that includes one or more steel units. The size of the points is related to the annual steel output of the plant. b Electricity generation potential of solar energy. c Electricity generation potential of wind energy. d Biomass energy potential by stock of biomass. GWh: Gigawatt-Hour. Base map data of China are adapted from GS(2024)0650 sourced from http://bzdt.ch.mnr.gov.cn/ and created using ArcGIS 10.8. Detailed steel units and renewable energy potential data are provided in Zenodo repository89.

Furthermore, we consider the supply of three types of renewable energy—solar, wind, and biomass energy—due to their widespread distribution in China and the maturity of their utilization technologies. We evaluate their potential for supplying energy to the steel units at a 1 km × 1 km scale (see details in Methods), as shown in Fig. 1b–d. The annual power generation potential is 43.95 Petawatt hour (PWh) for solar energy and 20.55 PWh for wind energy, respectively, while the biomass potential is 1.43 billion tons. Our results are lower compared to previous studies33,34,35, mainly because we only assess the energy potential that can be specifically used for steel production via the H2-DRI method (see details in Supplementary Note 1).

We quantify the hydrogen supply from renewable energy sources and the demand for the steel units. The hydrogen production potential using solar, wind, and biomass energy is estimated at 63.59, 29.74, and 63.91 Mt yr-1, respectively. Given that 44.29 Mt yr-1 of hydrogen is required to retrofit the steel units, solar and biomass energy can fully meet the hydrogen demand for the entire sector, while wind energy can satisfy over two-thirds of the demand. However, there is a substantial spatial mismatch between hydrogen supply and demand (see provincial results in Supplementary Figs. 1–4). Northwestern and Southwestern China have the most abundant renewable energy potential, whereas steel units are concentrated in Northern and Eastern China. Hebei, Jiangsu, Liaoning, Shandong, and Shanxi Provinces are identified as major steel producers in China, collectively accounting for 56.7% of the hydrogen demand. Nevertheless, the solar, wind, and biomass energy potential in these provinces only constitutes 1.9%, 10.4%, and 21.7% of the national total, respectively. Therefore, renewable energy sources are insufficient for some steel units in these regions to deploy H2-DRI, hindering the achievement of carbon mitigation through this technology. It is necessary to consider the spatial matching between the renewable energy sources and the steel units at a high-resolution scale while deploying H2-DRI.

The deployment schemes of H2-DRI technology

We develop a renewable energy supply-demand matching model to optimize the energy supply routes from each land pixel to steel unit. It is a linear programming model that aims to satisfy the energy demand for deploying H2-DRI technology at the lowest cost (see details in Methods and Supplementary Notes 4, 5). The economic costs consist of four components: renewable energy acquisition, hydrogen production, H2-DRI and EAF equipment, and supplemented fuels. For each unit, the energy demand is met by one type of renewable energy and supplemented fuels, e.g. gridded electricity and coal gasification-based hydrogen. We prioritize using renewable energy sources to supply the energy for H2-DRI, with deficiencies filled by supplementary fuels until the energy demand is fully met.

The deployment of H2-DRI exhibits diverse renewable energy availability and economic costs across China’s steel units (Supplementary Fig. 5a). Solar, wind, and biomass energy can fully support the deployment of H2-DRI in 138, 178, and 115 units, respectively, with steel outputs at 118.62-202.30 Mt. In contrast, the renewable energy sources are completely unavailable for over half of the steel units, accounting for 52.6%-55.8% of steel outputs. In addition, we identify the regions with low renewable energy supply (Supplementary Fig. 5b). For example, renewable energy can only supply 2.6% (solar) to 12.5% (wind) of hydrogen demand in Hebei Province, primarily due to the concentrated steel units and the lack of renewable energy sources.

Based on the model results, we propose the deployment schemes of H2-DRI technology by 2050. The units with the highest renewable energy supply amount and lowest economic costs are selected as they have priority to be deployed (see details in Methods). We set six scenarios that combine two deployment scales, i.e. a moderate scale with steel outputs at 149.60 Mt and an aggressive scale at 408.00 Mt, with three types of renewable energy sources (see details in Supplementary Note 2). Figure 2 exhibits the spatial distribution of renewable energy supply and deployed units in the six scenarios. At the moderate deployment scale, 129, 127, and 147 units are selected to deploy H2-DRI with solar, wind, and biomass energy, respectively. The selected units are distributed in the regions with abundant renewable energy sources. In the solar-moderate scenario, most units are located in Northern China, such as Shanxi, Shaanxi, Inner Mongolia, and Ningxia, where sunlight irradiation is relatively high. Similarly, the wind-moderate scenario deploys the units concentrated in coastal areas with high wind speeds, such as Jiangsu, Shandong, and Liaoning provinces. Meanwhile, those in the biomass-moderate scenario are mainly in granary provinces, such as Jiangsu, Henan, and Shanxi provinces, with a large quantity of agricultural residues. These schemes require the installation of 662.24 Gigawatt (GW) of photovoltaic (PV) panels, 529.35 GW of wind turbines, and the collection of 175.65 Mt of biomass, which is feasible as they only account for 1.58–12.28% of the total renewable energy potential35. The spatial distribution of deployed steel units varies significantly at an aggressive scale. Compared to the moderate retrofit scale, the selected units are nearly tripled at 367–380 units, with the scales of renewable energy technology 1.40–2.28 times larger.

a Solar-moderate scenario. b Wind-moderate scenario. c Biomass-moderate scenario. d Solar-aggressive scenario. e Wind-aggressive scenario. f Biomass-aggressive scenario. The colored pixels are the renewable energy deployment amounts, including the deployment of PV panels for solar energy, wind turbines for wind energy, and the collection of biomasses for biomass energy. The triangles are the locations of steel plants that have one or more units to deploy H2-DRI. g The summary of energy sources of the schemes, including renewable energy and supplemented fuels. The supplemented fuels are gridded electricity for solar and wind energy scenarios and coal gasification-based hydrogen for biomass energy scenarios. S-M solar-moderate scenario, W-M wind-moderate scenario, B-M biomass-moderate scenario, S-A solar-aggressive scenario, W-A wind-aggressive scenario, and B-A biomass-aggressive scenario. Source data are provided as a Source Data file. Base map data of China are adapted from GS(2024)0650 sourced from http://bzdt.ch.mnr.gov.cn/ and created using ArcGIS 10.8.

Furthermore, we consider the energy supply of the deployment schemes in different scenarios (Fig. 2g). Renewable energy sources can support most of the hydrogen demand for H2-DRI at moderate deployment scale. The steel units can be deployed with full renewable electricity from solar and wind energy, while over 97% of the energy demand can be satisfied by biomass energy. In contrast, the proportions of supplemented fuel increase sharply to around one-third to one-half at aggressive scale. To fulfill the deployment, 805.93 Gigawatt-Hour (GWh) of gridded electricity, 582.45 GWh of gridded electricity, and 11.48 Mt of coal gasification-based hydrogen are required to retrofit the steel units. These fuels are mostly used to deploy the units in Hebei Province, where the units are concentrated at present (see provincial distribution in Supplementary Fig. 6). As there is low spatial overlap between the renewable energy sources and steel units, the units with poor renewable energy supply are selected at aggressive deployment scale, relying heavily on supplemented fuels.

Carbon mitigation effects of H2-DRI at different deployment scales

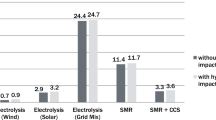

We evaluate the carbon mitigation effects of the six scenarios by estimating the emissions in four components: renewable energy acquisition, hydrogen production, steel production, and supplemented fuel (Table 1). In the solar-moderate and wind-moderate scenarios, the carbon intensity of steel production via H2-DRI technology is only 15.1% and 6.6% of the conventional BF-BOF method36, respectively. In this context, the carbon mitigation effects of H2-DRI technology on China’s steel sector amount to 294.56 Mt and 333.65 Mt in 2050. The mitigation effect in the biomass-moderate scenario is relatively lower at 219.91 Mt. Although SMR with carbon capture and storge (SMR-CCS) method can produce hydrogen with negative emissions, the collection and transportation of biomass lead to numerous indirect emissions and raise the total amounts. In a nutshell, the H2-DRI technology at moderate deployment scale can mitigate 13.4%-18.4% of emissions in China’s steel sector, consistent with the estimations by previous studies9,23,37,38,39.

However, the mitigation effects of H2-DRI technology at aggressive deployment scale are considerably lower. The carbon intensity in the wind-aggressive scenario is 0.96 t CO2 t−1 steel, which is more than sixfold of that in the wind-moderate scenario. Similarly, the carbon intensities in the solar-aggressive and biomass-aggressive scenarios increase significantly to 1.33 t CO2 t−1 steel and 1.12 t CO2 t−1 steel, respectively, higher than those in the moderate scenarios. These emission intensities are close to those of natural gas-based DRI, a currently mature steel production technology40. This is because a large amount of supplemented fuel is required to satisfy the hydrogen demand for the steel units at aggressive scale. Currently, the production of these fuels would lead to considerable carbon emissions, at 0.581 kg CO2 kWh−1 of gridded electricity and 21.6 kg CO2 kg−1 H2 via coal gasification12,41. The indirect emissions from supplemented fuel production may decrease the mitigation effects of the H2-DRI technology.

Economic cost of steel production in the deployment schemes

We estimate the economic cost of steel production in the deployment schemes in the six scenarios, as presented in Fig. 3 (see calculation method in Methods). In general, the deployment schemes with solar and wind power have lower costs. The schemes with solar energy have levelized costs of steel at 5232.89 Chinese Yuan (CNY) t−1 steel (solar-moderate) and 5732.59 CNY t−1 steel (solar-aggressive), respectively, while those with wind energy have similar cost levels at 5218.95 CNY t−1 steel (wind-moderate) and 5866.10 CNY t−1 steel (wind-aggressive). The cost indicators increase at aggressive deployment scale, mainly attributed to the purchase of supplemented gridded electricity. This result is consistent with the fact that the levelized costs of solar and wind electricity in China are lower than the price of gridded electricity42. In contrast, the costs of schemes with biomass energy decrease at larger deployment scale, amounting to 6323.74 CNY t−1 steel in the biomass-moderate scenario and 5793.46 CNY t−1 steel in the biomass-aggressive scenario. That is because hydrogen production via SMR-CCS method with biomethane has higher costs compared to water electrolysis with renewable energy.

The cost indicator is divided into seven items and is compared with the cost of steel production via the BF-BOF method without (blue dash line) and with emission trading cost (red dash line). S-M solar-moderate scenario, W-M wind-moderate scenario, B-M biomass-moderate scenario, S-A solar-aggressive scenario, W-A wind-aggressive scenario, and B-A biomass-aggressive scenario. Source data are provided as a Source Data file.

The deployment schemes with solar and wind energy can achieve cost-effective steel production in China. Assuming a future carbon price of 363 CNY t−1 CO243, the moderate retrofit schemes with solar and wind energy can achieve a net economic cost reduction in steel production by 12.12% and 13.55%, respectively, compared to the conventional BF-BOF methods44. At aggressive deployment scale, the schemes exhibit higher economic costs than the conventional methods. On the contrary, the scheme fails to offset the rising economic cost in the retrofit schemes with biomass, which are still 9.03% (biomass-moderate) and 1.75% (biomass-aggressive) higher. Consequently, establishing an appropriate carbon pricing scheme is necessary to help achieve the synergy between carbon mitigation and cost reduction for H2-DRI technology.

Water pressure from renewable energy supply and hydrogen production

Renewable energy supply and hydrogen production for H2-DRI could result in numerous water consumption, posing potential water pressure (see Supplementary Fig. 7 for schematic)45,46. We evaluate the water consumption related to renewable energy supply and hydrogen production across the deployment schemes (Fig. 4a). The scheme in the wind-moderate scenario exhibits the lowest water consumption at 230.76 million m3, while that in the solar-moderate scenario reaches the highest at 853.90 million m3. The significant difference in water consumption can be attributed to the dramatic discrepancy in the water footprint of power generation module production. Water usage for PV panel production is over ten times the amount for wind turbines with the same capacity, due to water-intensive processes such as metallurgical grade silicon manufacturing, ground-mounted system construction, and substation construction47. This results in significantly higher water consumption in the H2-DRI deployment schemes with solar energy. The water consumption rises sharply at aggressive deployment scale, as the schemes in the solar-aggressive and wind-aggressive scenarios consume 3008.82 million m3 and 1765.67 million m3 of water, respectively. The water intensity for crude steel production, together with water used for iron ore mining, water used in the EAF process, and water recycled from the by-products of iron reduction, is equivalent to 1.47–7.30 m3 t−1 steel. Compared to the traditional BF-BOF method48,49, the deployment schemes in the wind-moderate and biomass-aggressive scenarios can achieve net water conservation in steel production. In contrast, the schemes in the solar-moderate, solar-aggressive, and wind-moderate scenarios would impose higher water stress (see details in Supplementary Note 6).

a Water consumption by item (columns) and water intensity (points) from hydrogen production in the six scenarios. b Water consumption by province under the six scenarios. S-M solar-moderate scenario, W-M wind-moderate scenario, B-M biomass-moderate scenario, S-A solar-aggressive scenario, W-A wind-aggressive scenario, and B-A biomass-aggressive scenario. Source data are provided as a Source Data file.

Our results reveal increasing water-carbon trade-off along with higher deployment scales with solar and wind energy. The water intensity for carbon mitigation, i.e. water consumption in mitigating per ton of carbon emissions, rises from 2.90 m3 t−1 steel to 7.22 m3 t−1 steel and from 0.69 m3 t−1 steel to 3.07 m3 t−1 steel in the schemes with solar and wind energy, respectively. The increase in water intensity is primarily due to the generation of supplemented gridded electricity. In contrast, the increase in water consumption with biomass energy is relatively lower, from 566.21 million m3 to 1097.50 million m3, with water intensity gently decreasing from 2.64 m3 t−1 steel to 2.25 m3 t−1 steel. That is because hydrogen production via SMR-CCS method is more water-intensive than coal gasification. Five of the six schemes, except for that in the wind-moderate scenario, have higher water intensity than other carbon mitigation technologies such as CCS50,51.

Furthermore, we examine regional water pressure from hydrogen production by quantifying the water consumption by province (Fig. 4b). At the moderate deployment scale, the provinces with heaviest water consumption are Shanxi Province at 127.31 million m3 (solar energy), and Jiangsu Province at 48.25 million m3 (wind energy) and 97.57 million m3 (biomass energy). At the aggressive deployment scale, Hebei Province has the greatest water consumption at 621.63 million m3, 538.54 million m3, and 175.82 million m3 with the three energy sources. This heavy water consumption would pose significant water pressure on Hebei province, as its regional industrial water consumption may increase by up to 175.0% compared to the current level (see details in Supplementary Note 5). The regional discrepancy in water consumption results from two factors. One factor is the uneven distribution of retrofitted steel units, which has been explained previously. The other factor is the varying efficiency of renewable energy acquisition. For example, the capacity of solar PV installation for per ton of steel production ranges from 3.13 Milliwatt (MW) t−1 steel (Qinghai) to 4.50 MW t−1 steel (Hunan) due to varying solar irradiation conditions, resulting in differences in water consumption associated with PV panel production.

The deviation of the assessment results from uncertainty factors

We conduct an uncertainty analysis to examine the effects of various uncertainty parameters on the assessment results. We consider three uncertainty factors: renewable energy potential, hydrogen production technology performance, and H2-DRI technology performance (see details in Supplementary Table 12). In addition, we refer to previous studies on renewable energy potential from different representative concentration pathways52, energy consumption for hydrogen53, and hydrogen consumption for iron reduction54, to establish the parameter fluctuation ranges at ±20%. Figure 5 exhibits the results, in which fluctuations in parameters related to hydrogen production and H2-DRI technologies lead to unbiased deviations in carbon emissions, costs and water consumption of the deployment schemes. H2-DRI technology performance has the most significant impact, causing deviations in the results by 17.1%-26.9%. That is because this factor influences the processes including renewable energy acquisition, energy storage, hydrogen production, and steel production. Furthermore, our results reveal the risk associated with uncertain renewable energy potential, particularly for the scheme in solar-moderate scenario, which will result in an increase in carbon emissions by up to 33.7%. As the decrease in solar energy potential leads to insufficient hydrogen supply, the supplementary gridded electricity will be used, rapidly raising carbon emissions. Given that the availability of renewable energy depends on weather and climate conditions, high renewable energy technology efficiency will be a significant prerequisite for low-carbon steel production. In contrast, the deviation ranges of carbon emissions in the schemes with biomass energy are much smaller, mainly attributed to the low difference in carbon emission performance between coal- and biomass-based hydrogen production.

a Carbon intensity. b Levelized cost of steel. c Water intensity. The black dots are the original assessment results of the deployment schemes. The red, black, and blue bars represent the variation in the results due to a ± 20% fluctuation in parameters related to the renewable energy potential factor, hydrogen production performance factor, and H2-DRI performance factor, respectively. S-M solar-moderate scenario, W-M wind-moderate scenario, B-M biomass-moderate scenario, S-A solar-aggressive scenario, W-A wind-aggressive scenario, and B-A biomass-aggressive scenario. Source data are provided as a Source Data file.

Discussion

The steel sector is a typical hard-to-abate sector, for which H2-DRI is an essential technology to achieve deep decarbonization. Nevertheless, the performances of H2-DRI technology depend on the availability of renewable energy sources. We evaluate high-resolution renewable energy potential and unit-level energy demand for deploying H2-DRI in China’s steel sector, and propose a series of deployment schemes considering various deployment scales and renewable energy sources. Our results indicate that the renewable energy potential is abundant in the Northwestern, Southwestern, and Southern China, which are not major steel-producing regions. This spatial mismatch leads to the unavailability of renewable energy for over half of China’s steel units. In this situation, the mitigation effects of H2-DRI technology would be decreased. In our case, carbon intensities for steel production via H2-DRI at aggressive deployment scales are up to six times higher than those at moderate deployment scales. This finding is inconsistent with some studies, which suggested that the mitigation effects of H2-DRI technology are positively correlated with its deployment scale in China’s steel sector55,56,57, and therefore reveals the potential risk of its excessive deployment. Other technical performances in the solar and wind energy scenarios also decrease along with higher deployment target, including higher levelized cost of steel and water consumption from hydrogen production.

We integrate the deployment schemes across the six scenarios to estimate the renewable energy supply potential for H2-DRI deployment in China’s steel sector. Results indicate that renewable energy can fully meet the hydrogen requirements for 226 units to deploy H2-DRI technology, with a steel output of 263.95 Mt (see details in Supplementary Note 7). This finding suggests that less than 35% of current steel units have an adequate supply of green hydrogen. Apart from renewable energy supply, several technical and market factors also constrain the performance of H2-DRI deployment. The technical factors are related to the steel production process, including the degree of metallization in iron reduction and the capacity for steel refining23,58. Meanwhile, the market factors, such as substantial initial fixed investment, the availability of high-quality iron ore, and the demand for steel products, significantly impact the decision to retrofit steel units. These factors should be considered when deploying H2-DRI technology in China’s steel sector. We recommend setting a moderate deployment target that should be dynamically updated in response to changes in these multiple factors over time.

Furthermore, we demonstrate that the supplemented fuels constrain the mitigation effects of H2-DRI. During our study period, supplemented fuels cannot achieve low-carbon hydrogen production as effectively as renewable energy. For example, the emission factor of China’s gridded electricity by 2050 is estimated to be still much higher than solar and wind electricity59,60,61,62. Therefore, the availability of renewable energy should be a significant criterion for the green transition of the steel sector. According to our findings, it is recommended to prioritize the deployment of H2-DRI in regions with abundant renewable energy sources, such as Shanxi (solar energy) and Jiangsu Province (wind and biomass energy), and avoid excessive implementation in the steel units located in Hebei province. Apart from the selected three types of energy resources, other renewable energy resources, such as hydroelectricity, also exhibit strong performance in terms of low carbon footprint and cost-effectiveness. Therefore, they can be considered as viable options for producing hydrogen for steel units, especially those located in Sichuan, Yunnan, and Hubei Provinces. This finding inspires potential spatial transition strategy in China’s steel sector. In the past, the availability for raw materials and market demand were crucial factors in determining the steel units’ locations, while the access to sufficient renewable energy supplies will become increasingly important under stricter decarbonization targets. The steel units without adequate renewable energy supply can either be eliminated or retrofitted with CCS, a technology that can decarbonize the conventional BF-BOF units at low economic costs63,64. These findings highlight the significance of plant-level mitigation strategy and inform its development65. In the long term, renewable energy supply will no longer be a constraint as China’s electricity sector undergoes the deep decarbonization, enabling hydrogen production with low-carbon gridded electricity. At that time, the economic costs of power transmission system would become a significant factor in determining the spatial distribution of steel units.

We propose several policy suggestions to facilitate the deployment of H2-DRI technology in China. First, wind and solar energy are recommended to supply the energy demand for H2-DRI, as they can achieve low-carbon steel production with net economic benefits. Wind energy, in particular, has the advantage of low water consumption. Emphasizing the improvement of renewable solar and wind energy technologies is crucial, as they influence the renewable energy potential and significantly impact the performance of the deployment schemes, according to the results of uncertainty analysis. In contrast, although biomass energy can produce hydrogen with negative emissions via SMR-CCS, it faces the challenges of high carbon emissions and economic costs. Therefore, biomass energy can be prioritized to decarbonize the steel sector by replacing sintering fuel, coking coal, and coke in the traditional BF-BOF process66,67. Second, a proper carbon pricing scheme should be established. We estimate that the deployment schemes with solar and wind energy can achieve net economic benefits with carbon price at 363 CNY t-1 CO2, which is over five times the current level (70 CNY t-1 CO2). The carbon price should be increased steadily in the coming decades to cover the renewable energy-related investments. Third, the supply of water resources should be prioritized to mitigate the water pressure associated with H2-DRI technology. Although the H2-DRI deployment schemes in the solar-moderate and wind-moderate scenarios can achieve synergistic effects in carbon mitigation and cost reduction, all scenarios lead to increases in water consumption. Therefore, this technology exhibits a trade-off between climate benefits, economic gains, and water usage. This conflict is particularly significant in some provinces and should be addressed. For inland provinces, e.g. Shanxi Province, water consumption can be fulfilled through inter-provincial diversion. Meanwhile, coastal provinces, e.g. Hebei and Jiangsu Province, can integrate water electrolysis and seawater desalination. Finally, long-distance hydrogen transportation technology should be developed. The long-term transportation of hydrogen can solve the uneven renewable energy supply issue as it enables the off-site hydrogen production. However, there are only a few projects in China for pure hydrogen transportation at present, with a total length less than 100 kilometers68. We suggest establishing clusters for hydrogen production in areas with abundant renewable energy and for hydrogen consumption in regions with steel and other hydrogen consuming units, and constructing hydrogen transportation pipelines between them.

Although our research specifically focuses on China’s steel sector, the proposed framework can be replicated to the analysis in other regions and other hard-to-abate sectors, such as cement and coal chemical sectors. While applying the method, the production outputs and equipment of each unit in these sectors should be obtained to determine the hydrogen demand for the utilization of hydrogen-based technology. Then, the renewable energy potential assessment method and the renewable energy supply-demand model can be used to analyze the availability of renewable energy for each unit. These approaches enable us to map the deployment schemes of hydrogen-based technology at a high-resolution level, thereby facilitating the implementation of green hydrogen to decarbonize multiple hard-to-abate sectors. Meanwhile, there exist several challenges during the replication, such as the acquisition of localized data on the units and the identification of regional-specific decarbonization pathways.

This study has two limitations. One is that we propose several one-step deployment schemes in different scenarios. However, the deployment of H2-DRI is a continuous process that may last for several decades, during which the availability of renewable energy sources, economic costs, and renewable energy technology performance may change significantly. Therefore, future studies should develop dynamic optimization model and propose the multi-phase deployment schemes to improve this model. The other limitation is the lack of considerations on other environmental and social impacts. While we assess the carbon mitigation effects, economic costs, and water consumption, additional factors, such as air pollutant emissions, land consumption, and labor market impacts, could also affect the performance of the retrofit schemes. These impacts should be considered in future studies.

Methods

Research framework

We develop a six-module research framework to fulfill the study (Fig. 6). We first build a unit-level database of China’s steel sector, which reflects the spatial hydrogen demand in the deployment of H2-DRI technology. Simultaneously, we assess the potential of three types of renewable energy - solar, wind, and biomass energy—at high-resolution level. Then, we establish a renewable energy supply-demand matching model to optimize the distribution of renewable energy for each unit at lowest cost. The model results provide the basis for determining deployment schemes of H2-DRI under six scenarios, combing two deployment scales—moderate and aggressive—and three types of renewable energy sources. In the fifth module, we assess the carbon mitigation effects of each deployment scheme in different scenarios. Finally, we quantify the potential water pressure from hydrogen production in each scheme.

The framework includes six modules: steel unit database, renewable energy potential evaluation, renewable energy supply-demand model, deployment scheme determination, carbon mitigation effect assessment, and water consumption assessment. H2-DRI: hydrogen-based direct reduced iron.

China’s steel unit database

We establish a China’s steel unit database, including the spatial location, equipment, process, and production output of each steel unit. This database is developed and updated by referring to various data sources69,70,71,72,73. Note that the steel production units using the scrap-based EAF method are not included, as they do not involve the ironmaking process and cannot be retrofitted with H2-DRI technology. The database is recorded in Zenodo repository and their statistics are summarized by province in Supplementary Table 1.

The assessment of renewable energy potential

We assess the potentials of the solar, wind, and biomass energy at a 1 km×1 km scale. Here, we use the electricity generation to reflect the potentials of solar and wind energy, and use the biomethane production to reflect the potential of biomass energy, respectively. The concept of “renewable energy potential” refers to the total amount of energy that can be generated through the full exploitation of renewable sources, such as the deployment of PV panels and wind turbines on all feasible land, or the complete utilization of biomass. We collect the data from multiple high-resolution geodatabases to fulfill the assessment74,75,76,77,78, which is summarized in Supplementary Table 2. The potential assessment results are fed into the renewable energy supply-demand model that is introduced in the next section.

Electricity generation potential of solar energy

We assess the potential of solar energy by considering several factors, such as the tilt angle of solar panel, packing factor, land suitability, and the modifications. As most solar panels are fixed-tilt, the optimal tilt angles of the panels at different locations should be clarified to get the best exposure to direct-beam sunlight radiation. Here we refer to the study by Jacobson et al.79 that proposed the optimal tilt angle estimation method based on the experiment results of hundreds of cities. This method is presented in Eq. (1):

where Σ is the optimal tilt angle of the solar panel and φ is the latitude. As the land of China is located between 3°51’N and 53°33’N, the optimal tilt angles of solar power in China should range from 5.79 to 36.76 degree.

The next step is to estimate the packing factor, which is the PV panel area per square meter of land area. According to a Chinese standard Code for Design of photovoltaic Power Station (GB50797-2012)80, the PV panels should not have mutual shading during 9 am to 3 pm in each day. Therefore, the packing factor between the panels are calculated based on the solar position at 9 am or 3 pm at the winter solstice—the worst sunlight condition over the year—which is presented at Eq. (2)81:

where ω is the packing factor, β and θ are the solar altitude angle and solar azimuth angle of the sunlight at 9 am at the winter solstice, respectively.

We then consider the land suitability of solar PV deployment. The land suitability is defined as the ratio of suitable area for PV panel deployment to the total area. By referring to a study82, we set the land suitability indicator of sparsely woodland, woody savanna, grassland, deserts, and bare land as 0.15, snow and ice land as 0.10, and other land use type as 0. In addition, the area with ground slope larger than 5% and the natural conservation district should be excluded. We obtain the land cover type of China by Xu et al.83 at a 1 km×1 km scale. The solar electricity generation capacity can be therefore estimated via Eq. (3):

where P is the electricity generation capacity of solar energy, lu is the land use type, S is the land area, ls is the land suitability indicator, and SD is the standard power capacity density of PV panels.

Finally, the annual electricity generation potential of the land can be calculated based on the generation capacity, solar radiation, and a series of coefficients. The solar irradiation is the energy of sunlight received by the ground. We obtain the high-resolution, hourly solar irradiation data from the ECMWF Reanalysis v5 (ERA5) database76, and use the average value between 2019 and 2023 to reflect the solar irradiation levels. Meanwhile, the coefficients are used to modify the electricity generation potential by considering the energy losses, including shading coefficient, temperature coefficient, and system coefficient84. Based on these factors, we quantify the annual electricity generation potential of the solar energy using Eq. (4):

where Esolar is the electricity generation potential of solar energy, t is the time by hour, si is the solar irradiation, si0 is the solar irradiation by default under the standard test condition, γshading is the shading coefficient, γtemp,t is the temperature coefficient at time t, and γsys is the system coefficient (see parameters in Supplementary Table 3).

Electricity generation potential of wind energy

The electricity generation of wind energy is affected by the performance of wind turbine, wind speed, land suitability, and the modifications. Here we only consider the onshore wind energy due to the long distance between the offshore projects and the land. We select the GE 2.5 MW-100 m as the representative wind turbine model, with the maximum capacity of 2.5 MW and the diameter (D) at 103 m82. The distance of wind turbine is set as 5D × 10D35. The land suitability of wind power is set as 1.0 for shrubland, savanna, grassland, cropland, desserts, and bare land and 0 for other land use types. The area with ground slope larger than 20% and altitude higher than 3000 m, as well as the natural conservation area, are all excluded. By integrating these factors, the power generation capacity of the wind energy can be calculated via Eq. (5):

where Pwind is the power generation capacity of wind turbine, Pw is the maximum capacity (2.5 MW), and D is the diameter of the wind turbine (103 meters).

In practice, the power generation efficiency of the wind turbine depends on the instant wind speed. We obtain the high-resolution wind speed data by hour from ERA5 during the average level between 2019 and 2023, which is used to estimate the power generation efficiency. Moreover, two modifications are made in the calculation, including the energy conversion coefficient and array efficiency coefficient. In summary, we calculate the annual electricity generation potential of the wind energy using Eq. (6):

where Ewind is the electricity generation potential of wind energy, PEwind,t is the power generation efficiency of wind turbine in time t, γconv is the energy conversion coefficient, and γarray is the array efficiency coefficient (see Supplementary Table 4).

Biomethane production potential of biomass energy

Biomethane is produced via the anaerobic digestion of biomass. We obtain the spatial distribution of biomass production from the database developed by ref. 78, including nine types of agricultural residues and one type of energy crop, i.e. switch grass, which has wide cultivation potential and high biomethane production yield. The biomethane production potential can be estimated by integrating several factors: the collection rates of agricultural residues and energy crop, and the biomethane production rates of them, which is exhibited in Eq. (7):

where Ebiomass is the biomethane production potential of biomass energy, m is the biomass type, Y is the annual production of biomass, CR is the collection rate, and BPY is the biomethane production yield per ton of biomass (see the value of CR and BPY of the biomass in Supplementary Table 5).

Renewable energy supply-demand model

We establish a renewable energy supply-demand model to optimize the energy supply in each steel unit to deploy H2-DRI at the lowest cost. The decision variables contain two parts: The first part is the amount of renewable energy supply from each land pixel to the steel unit, and the second part is the amount of supplemented fossil energy for each unit. The objective is the minimum economic cost, which can be calculated by Eq. (8):

where TC is the total cost, Crenew is the cost from the acquisition of renewable energy, Chydro is the cost from hydrogen production, Cequip is the cost for installation with H2-DRI and EAF equipment, and Csup is the cost from purchasing the supplemented fuel. These sub-cost indicators are calculated via Eqs. (9)–(14). Note that two cost items—raw material cost and operation and maintenance cost - are excluded in this model as they are constant for each steel unit and would not affect the model results (See details in the sub-cost items in Supplementary Note 3).

where a is the renewable energy type, including solar, wind, and biomass, i is the land pixel at the resolution of 10 km×10 km, j is the steel unit, Costa is the cost for deploying solar panel or wind turbine to the suitable land, including the costs of their manufacturing, installation, and operation, Disi,j is the distance between the pixel and steel unit, which is calculated from the geographic coordinates of the pixel center and the steel unit; Costeletran is the cost of electricity transmission; Costlu is the cost of land acquisition by land use type; Ym,I,j is the yield of biomass that is supplied from pixel i to the steel unit j; Costm is the cost of biomass collection and cultivation, and Costtrans is the cost of biomass transportation, which has a linear relationship with transport distance85.

where Ei,j is the electricity transmitted from pixel i to steel unit j, Coststo is the cost of energy storage, IPj is the iron output of the unit j, HC is the hydrogen consumption in producing one ton of reduced iron, Costew is the cost of hydrogen production via water electrolysis, and Costsmr is the cost of hydrogen production via the SMR-CCS method.

where Costequip is the cost of installing DRI and EAF equipment, f is the supplemented fuel, including the gridded electricity and hydrogen from coal gasification, Prif is the price of fuel f, and SEi,f is the quantity of supplemented fuel f in the unit j (see the parameter value and sources in Supplementary Tables 6-10).

Moreover, we set several natural and policy constraints to ensure the feasibility of the optimal solutions, including four categories: the energy balance constraint, the usable renewable energy constraint, the supply-demand distance constraint, and the non-negative constraint. The detailed description and equations of these constraints are summarized in Supplementary Note 4.

Deployment scheme determination

Based on the optimization results, we determine the deployment scheme of H2-DRI technology. First, we decide the target deployment scales of the technology. By referring to reports from the International Energy Agency37 and Lawrence Berkeley National Laboratory86, we analyze changes in societal steel demand, China’s industrial structure, and steel production methods, to predict that China’s steel outputs will decline to 680 Mt by 2050, with scrap-based steel production accounting for 40% of the outputs. We set two deployment scales, i.e. moderate and aggressive scales. At the moderate scale, we predict that H2-DRI is promoted gradually and contribute to 149.60 Mt of steel production per annum in the future. In contrast, at the aggressive scale, it is assumeed that all primary steel will be produced using the H2-DRI method by the mid-century, equivalent to annual steel outputs of 408.00 Mt. These two deployment scales form six scenarios with the three types of renewable energy sources (See details in scenario setting in Supplementary Note 2).

We then make several assumptions to determine the deployment schemes. First, we consider adjusting the equipment while maintaining the same production capacity, in which the hydrogen demand for each unit is estimated based on its current production outputs. Second, a unit will adopt only one production method—either the BF-BOF method or the H2-DRI method. If the H2-DRI is deployed, the BF-BOF method will not be used in those units. Third, units not selected for deploying H2-DRI will either be eliminated or upgraded with the BF-BOF method in the same location at the end of their operational lifespan. The lifetime of BF-BOF equipment is typically less than 30 years87,88, and thus most current units will reach the end-of-life stage by 2050. Finally, for deployment schemes utilizing solar and wind energy, energy demand for both the H2-DRI and the EAF methods is taken into account, as they both consume electricity that can be supplied by these two energy sources. In contrast, energy demand for the EAF is not contained in the schemes utilizing biomass energy, as biomass energy produces hydrogen through biomethane production and the SMR-CCS method, which does not generate any green electricity. Based on these assumptions, we consider the units that have the lowest supplemented fuel demand and the lowest levelized cost of steel for deployment, until their outputs reach or exceed the given scales.

Carbon mitigation effects assessment

We estimate the carbon mitigation effects of steel production using H2-DRI technology in the six scenarios. The carbon mitigation effects are estimated by comparing the emissions of steel production via the H2-DRI method and that via the traditional BF-BOF method. The emissions from the H2-DRI technology can be divided into several components, including renewable energy acquisition, hydrogen production, steel production, and production of supplemented fuel. The calculation methods are presented below (see the parameter used for carbon mitigation effects calculation in Supplementary Table 11).

The carbon emissions assoicated with renewable energy acquisition vary among different energy sources. For solar and wind energy sources, the emissions in this stage include the production of electricity generation modules, i.e. PV panels and wind turbines, and the production of wires for electricity transmission. Both facilities need one-time installation and will serve throughout their lives, and thus their annual emissions should be calculated by dividing them by the lifetime. Meanwhile, the emissions from the biomass energy source are generated during the collection and transportation of biomass from the land to the steel production unit site. The emissions in this stage can be summarized in Eqs. (15)-(16):

where CErenew,a is the carbon emissions from renewable energy acquisition of energy source a, LTa is the lifetime of the renewable facilities, CIeletran is the carbon intensity of electricity transmission wire, and CItrans is the carbon intensity of biomass transportation.

The carbon emissions associated with the hydrogen production include the one-time installation of hydrogen production facilities, such as energy storage, water electrolysis, and SMR-CCS with biomethane. Here we use the indicators of carbon intensity for hydrogen production to estimate the emissions, which is shown in Eqs. (17)-(18):

where CEhydro,a is the carbon emissions of hydrogen production by renewable energy source a, CIsto is the carbon intensity of energy storage, CIhydro,ew is the carbon intensity of hydrogen production via water electrolysis, and CIhydro,smr is the carbon intensity of hydrogen production via SMR-CCS with biomethane.

The carbon emissions associated with the steel production mainly originate from the EAF method, which uses electricity as the primary fuel. Therefore, the indirect emissions of electricity generation is calculated as carbon emissions in this component, as presented in Eq. (19):

where CEsp,a is the carbon emissions of steel production, SR is the iron-steel ratio indicator, which is the mass ratio of iron to the crude steel product, Eleceaf is the electricity consumption for steel production via EAF, and CIelec is the carbon intensity of electricity generation.

The carbon emissions associated with the supplemented fuel refer to emissions in generating the supplemented gridded electricity in the solar and wind energy scenarios and producing the supplemented fossil-based hydrogen in the biomass energy scenarios. We estimate this part of carbon emissions via Eq. (20):

where CEsup,a is the carbon emissions of supplemented fuel, and CIf is the carbon intensity of the supplemented fuel f.

Finally, the carbon mitigation effects can be calculated by Eq. (21), where CIbf-bof represents the carbon intensity of steel production via the conventional BF-BOF technology:

Water consumption assessment

In terms of water consumption, we mainly focus on the water usage associated with hydrogen production. Water is used for the raw material and cooler in hydrogen production, and is used in the manufacturing of electricity generation module. Meanwhile, the supply of supplemented fuel would lead to water consumption. Therefore, the hydrogen production-related water consumption can be evaluated by Eqs. (22)-(23):

where Wa is water consumption from hydrogen production by energy source, WIa is the water intensity of electricity generation modules, i.e. PV panels and wind turbines, WIew is the water intensity for hydrogen production via water electrolysis, WIelec is the water intensity of supplemented electricity generation, WIsmr is the water intensity for hydrogen production via SMR-CCS, WIbm is the water consumption for biomethane production, SEhydro-coal is the supplemented hydrogen via coal gasification, and WIhydro-sup is the water intensity of supplemented hydrogen via coal gasification (see parameters for carbon and water indicators in Supplementary Table 12, 13).

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

The data generated in this study are provided in the Supplementary Information and Zenodo repository89. Source data are provided with this paper.

Code availability

The code developed in this study is available via Zenodo repository89.

References

Lei, T. et al. Global iron and steel plant CO2 emissions and carbon-neutrality pathways. Nature 622, 514–520 (2023).

Watari, T., Hata, S., Nakajima, K. & Nansai, K. Limited quantity and quality of steel supply in a zero-emission future. Nat. Sustain https://doi.org/10.1038/s41893-022-01025-0 (2023).

Xu, R. et al. Plant-by-plant decarbonization strategies for the global steel industry. Nat. Clim. Chang. 13, 1067–1074 (2023).

Guo, Y. et al. Co-production of steel and chemicals to mitigate hard-to-abate carbon emissions. Nat. Chem. Eng. 1, 365–375 (2024).

Edelenbosch, O. Y. et al. Reducing sectoral hard-to-abate emissions to limit reliance on carbon dioxide removal. Nat. Clim. Chang. 14, 715–722 (2024).

Fan, Z. & Friedmann, S. J. Low-carbon production of iron and steel: technology options, economic assessment, and policy. Joule 5, 829–862 (2021).

Rechberger, K., Spanlang, A., Sasiain Conde, A., Wolfmeir, H. & Harris, C. Green hydrogen-based direct reduction for low-carbon steelmaking. steel Res. Int. 91, 2000110 (2020).

Hermwille, L. et al. A climate club to decarbonize the global steel industry. Nat. Clim. Chang. 12, 494–496 (2022).

Kang, Z., Liao, Q., Zhang, Z. & Zhang, Y. Carbon neutrality orientates the reform of the steel industry. Nat. Mater. 21, 1094–1098 (2022).

International Energy Agency. Global Hydrogen Review 2023 (2023). https://iea.blob.core.windows.net/assets/ecdfc3bb-d212-4a4c-9ff7-6ce5b1e19cef/GlobalHydrogenReview2023.pdf.

Palmer, G., Roberts, A., Hoadley, A., Dargaville, R. & Honnery, D. Life-cycle greenhouse gas emissions and net energy assessment of large-scale hydrogen production via electrolysis and solar PV. Energy Environ. Sci. 14, 5113–5131 (2021).

Li, J., Wei, Y.-M., Liu, L., Li, X. & Yan, R. The carbon footprint and cost of coal-based hydrogen production with and without carbon capture and storage technology in China. J. Clean. Prod. 362, 132514 (2022).

Wang, R. R., Zhao, Y. Q., Babich, A., Senk, D. & Fan, X. Y. Hydrogen direct reduction (H-DR) in steel industry—An overview of challenges and opportunities. J. Clean. Prod. 329, 129797 (2021).

Rosner, F. et al. Green steel: design and cost analysis of hydrogen-based direct iron reduction. Energy Environ. Sci. 16, 4121–4134 (2023).

Boretti, A. The perspective of hydrogen direct reduction of iron. J. Clean. Prod. 429, 139585 (2023).

Borsboom-Hanson, T., Patlolla, S. R., Herrera, O. E. & Mérida, W. Point-to-point transportation: The economics of hydrogen export. Int. J. Hydrog. Energy 47, 31541–31550 (2022).

Yu, Q., Hao, Y., Ali, K., Hua, Q. & Sun, L. Techno-economic analysis of hydrogen pipeline network in China based on levelized cost of transportation. Energy Convers. Manag. 301, 118025 (2024).

Ren, M. et al. Decarbonizing China’s iron and steel industry from the supply and demand sides for carbon neutrality. Appl. Energy 298 (2021).

Wang, P. et al. Efficiency stagnation in global steel production urges joint supply- and demand-side mitigation efforts. Nat. Commun. 12, 1–11 (2021).

Yu, X. & Tan, C. China’s pathway to carbon neutrality for the iron and steel industry. Glob. Environ. Chang. 76, 102574 (2022).

Huang, D. et al. Quantitative analysis of net-zero transition pathways and synergies in China’s iron and steel industry. Renew. Sustain. Energy Rev. 183, 113495 (2023).

Andrade, C., Desport, L. & Selosse, S. Net-negative emission opportunities for the iron and steel industry on a global scale. Appl. Energy 358, 122566 (2024).

Devlin, A., Kossen, J., Goldie-Jones, H. & Yang, A. Global green hydrogen-based steel opportunities surrounding high quality renewable energy and iron ore deposits. Nat. Commun. 14, 2578 (2023).

Woods, P., Bustamante, H. & Aguey-Zinsou, K.-F. The hydrogen economy—where is the water? Energy Nexus 7, 100123 (2022).

El-Shafie, M. Hydrogen production by water electrolysis technologies: a review. Results Eng. 20, 101426 (2023).

Ministry of Water Resources. China Water Resources Bulletin (2023) (in Chinese) https://www.gov.cn/lianbo/bumen/202406/content_6957291.htm.

Cassol, G. S. et al. Ultra-fast green hydrogen production from municipal wastewater by an integrated forward osmosis-alkaline water electrolysis system. Nat. Commun. 15, 2617 (2024).

Winter, L. R. et al. Mining nontraditional water sources for a distributed hydrogen economy. Environ. Sci. Technol. 56, 10577–10585 (2022).

Tonelli, D. et al. Global land and water limits to electrolytic hydrogen production using wind and solar resources. Nat. Commun. 14, 5532 (2023).

Wu, W. et al. Quantifying China’s iron and steel industry’s CO2 emissions and environmental health burdens: A pathway to sustainable transformation. Environ. Sci. Ecotechnol. 20, 100367 (2024).

Wang, K. et al. Tracking carbon flows in China’s iron and steel industry. Environ. Sci. Technol. 57, 11510–11519 (2023).

World Steel Association. World Steel in Figures 2024 https://worldsteel.org/data/world-steel-in-figures-2024/ (2024) .

Liu, C. et al. The biomethane producing potential in China: a theoretical and practical estimation. Chin. J. Chem. Eng. 24, 920–928 (2016).

Qiu, T. et al. Potential assessment of photovoltaic power generation in China. Renew. Sustain. Energy Rev. 154, 111900 (2022).

Wang, Y., Chao, Q., Zhao, L. & Chang, R. Assessment of wind and photovoltaic power potential in China. Carbon Neutrality 1, 15 (2022).

Hasanbeigi, A. & Springer, C. How clean is the U.S. Steel Industry? An international benchmarking of energy and CO2 Intensities (2019). https://static1.squarespace.com/static/5877e86f9de4bb8bce72105c/t/63652c97e4fc49276618c991/1667574956501/How+Clean+is+the+U.S.+Steel+Industry-Rev2.pdf.

International Energy Agency. Iron and Steel Technology Roadmap. https://www.iea.org/reports/iron-and-steel-technology-roadmap (2020).

Yang, X., Nielsen, C. P., Song, S. & McElroy, M. B. Breaking the hard-to-abate bottleneck in China’s path to carbon neutrality with clean hydrogen. Nat. Energy 7, 955–965 (2022).

Wan, F. & Li, J. Exploring hydrogen metallurgy to CO2 emissions reduction in China’s iron and steel production: An analysis based on the life cycle CO2 emissions – LEAP model. Energy Rep. 11, 4552–4563 (2024).

Nduagu, E. I. et al. Comparative life cycle assessment of natural gas and coal-based directly reduced iron (DRI) production: a case study for India. J. Clean. Prod. 347, 131196 (2022).

Ministry of Ecology and Environment. Notice on the work related to the management of corporate greenhouse gas emissions reporting in 2022 (in Chinese) https://www.mee.gov.cn/xxgk2018/xxgk/xxgk06/202203/t20220315_971468.html (2022).

International Renewable Energy Agency. Renewable Power Generation Costs in 2022 (https://www.irena.org/Publications/2023/Aug/Renewable-power-generation-costs-in-2022 (2022).

Lu, N. et al. Biophysical and economic constraints on China’s natural climate solutions. Nat. Clim. Chang. 12 (2022).

TransitionZero. Global steel production costs: a country and plant-level cost analysis (2022). https://www.transitionzero.org/insights/global-steel-production-costs.

Henriksen, M. S. et al. Tradeoffs in life cycle water use and greenhouse gas emissions of hydrogen production pathways. Int. J. Hydrog. Energy 49, 1221–1234 (2024).

Olaitan, D., Bertagni, M. & Porporato, A. The water footprint of hydrogen production. Sci. Total Environ. 927, 172384 (2024).

Yang, Q. et al. Water saving potential for large-scale photovoltaic power generation in China: Based on life cycle assessment. Renew. Sustain. Energy Rev. 167, 112681 (2022).

Tong, Y. et al. Life cycle water use and wastewater discharge of steel production based on material-energy-water flows: a case study in China. J. Clean. Prod. 241, 118410 (2019).

Ma, X. et al. Life cycle assessment and water footprint evaluation of crude steel production: A case study in China. J. Environ. Manag. 224, 10–18 (2018).

Rosa, L., Reimer, J. A., Went, M. S. & D’Odorico, P. Hydrological limits to carbon capture and storage. Nat. Sustain. 3, 658–666 (2020).

Rosa, L., Sanchez, D. L., Realmonte, G., Baldocchi, D. & D’Odorico, P. The water footprint of carbon capture and storage technologies. Renew. Sustain. Energy Rev. 138, 110511 (2021).

Gernaat, D. E. H. J. et al. Climate change impacts on renewable energy supply. Nat. Clim. Chang. 11, 119–125 (2021).

Gao, X. et al. Next-generation green hydrogen: progress and perspective from electricity, catalyst to electrolyte in electrocatalytic water splitting. Nano-Micro Lett. 16, 237 (2024).

Shahabuddin, M. et al. Process modelling for the production of hydrogen-based direct reduced iron in shaft furnaces using different ore grades. Ironmak. Steelmak. 03019233241254666. https://doi.org/10.1177/03019233241254666 (2024).

Speizer, S. et al. Rapid implementation of mitigation measures can facilitate decarbonization of the global steel sector in 1.5 °C-consistent pathways. One Earth 6, 1494–1509 (2023).

Liu, D., Wang, P., Sun, Y., Zhang, H. & Xu, S. Co-abatement of carbon and air pollutants emissions in China’s iron and steel industry under carbon neutrality scenarios. Renew. Sustain. Energy Rev. 191, 114140 (2024).

Wang, Y. et al. Decarbonization pathways of China’s iron and steel industry toward carbon neutrality. Resour. Conserv. Recycl. 194, 106994 (2023).

Kim, W. & Sohn, I. Critical challenges facing low carbon steelmaking technology using hydrogen direct reduced iron. Joule 6, 2228–2232 (2022).

Zhuo, Z. et al. Cost increase in the electricity supply to achieve carbon neutrality in China. Nat. Commun. 13, 3172 (2022).

Chen, R., Xu, P. & Yao, H. Decarbonization of China’s regional power grid by 2050 in the government development planning scenario. Environ. Impact Assess. Rev. 101, 107129 (2023).

Xu, K. et al. A comprehensive estimate of life cycle greenhouse gas emissions from onshore wind energy in China. J. Clean. Prod. 338, 130683 (2022).

Chen, S. et al. Deploying solar photovoltaic energy first in carbon-intensive regions brings gigatons more carbon mitigations to 2060. Commun. Earth Environ. 4, 369 (2023).

Wei, N., Liu, S., Jiao, Z. & Li, X. chun. A possible contribution of carbon capture, geological utilization, and storage in the Chinese crude steel industry for carbon neutrality. J. Clean. Prod. 374, 133793 (2022).

Tian, S., Jiang, J., Zhang, Z. & Manovic, V. Inherent potential of steelmaking to contribute to decarbonisation targets via industrial carbon capture and storage. Nat. Commun. 9, 1–8 (2018).

Li, Z. & Hanaoka, T. Article Plant-level mitigation strategies could enable carbon neutrality by 2060 and reduce non-CO 2 emissions in China’ s iron and steel sector Plant-level mitigation strategies could enable carbon neutrality by 2060 and reduce non-CO 2 emissions in. Chi. One Earth 5, 932–943 (2022).

Tan, W. & Xi, B. Toward carbon emission reduction in steel production by substituting pulverized coal and coke with biochar. ACS EST Eng. 4, 1253–1255 (2024).

Mousa, E., Wang, C., Riesbeck, J. & Larsson, M. Biomass applications in iron and steel industry: An overview of challenges and opportunities. Renew. Sustain. Energy Rev. 65, 1247–1266 (2016).

Xue, S. & Zhu, Z. How government policies promote transportation utilization in the national-level hydrogen supply chain: a case of China. Energy Sustain. Dev. 80, 101457 (2024).

China Iron and Steel Association. China Steel Yearbook (Metallurgical Industry Press, Beijing, 2020).

National Development and Reform Commission. Methods of Energy Conservation Monitoring (2016) (in Chinese). https://www.ndrc.gov.cn/xxgk/zcfb/fzggwl/201601/W020190905495012309539.pdf.

Ministry of Ecology and Environment. National Pollutant Emission Permit Management Information Platform (2018) (in Chinese). http://permit.mee.gov.cn/permitExt/defaults/default-index!getInformation.action.

Global Energy Monitor. Global Steel Plant Tracker (2024). https://globalenergymonitor.org/projects/global-steel-plant-tracker/.

Wang, Y., Wen, Z., Xu, M. & Doh Dinga, C. Long-term transformation in China’s steel sector for carbon capture and storage technology deployment. Nat. Commun. 16, 4251 (2025).

Xu, X. et al. China multi-period land use/land cover dataset https://www.resdc.cn/DOI/DOI.aspx?DOIID=54 (2023).

Resource and Environmental Data Platform. National Natural Reservation Area Boundary Dataset https://www.resdc.cn/data.aspx?DATAID=272 (2018).

European Centre for Medium-Range Weather Forecasts. The fifth generation ECMWF reanalysis dataset (ERA5) https://cds.climate.copernicus.eu/cdsapp#!/dataset/reanalysis-era5-single-levels?tab=overview (2024).

Space Shuttle Endeavour. Shuttle Radar Topography Missionhttps://www.earthdata.nasa.gov/sensors/srtm (2000).

Wang, R. et al. A high spatial resolution dataset of China’s biomass resource potential. Sci. Data 10, 384 (2023).

Jacobson, M. Z. & Jadhav, V. World estimates of PV optimal tilt angles and ratios of sunlight incident upon tilted and tracked PV panels relative to horizontal panels. Sol. Energy 169, 55–66 (2018).

China Electricity Council. Code for design of photovoltaic power station (GB 50797/2012) 50797–52012 (in Chinese). https://www.nssi.org.cn/cssn/js/pdfjs/web/preview.jsp?a100=GB (2012).

Masters, G. M. in Renewable and Efficient Electric Power Systems 385–443 https://doi.org/10.1002/0471668826.ch7 (2004).

Wang, Y. et al. Accelerating the energy transition towards photovoltaic and wind in China. Nature 619, 761–767 (2023).

Xu, Y. et al. Annual 30-m land use/land cover maps of China for 1980–2015 from the integration of AVHRR, MODIS and Landsat data using the BFAST algorithm. Sci. China Earth Sci. 63, 1390–1407 (2020).

Chen, S. et al. The potential of photovoltaics to power the belt and road initiative. Joule 3, 1895–1912 (2019).

Fan, J.-L. et al. Co-firing plants with retrofitted carbon capture and storage for power-sector emissions mitigation. Nat. Clim. Chang. 13, 807–815 (2023).

Hasanbeigi, A., Lu, H. & Zhou, N. Net-Zero Roadmap for China’s Steel Industry https://eta-publications.lbl.gov/sites/default/files/china_steel_roadmap-2mar2023.pdf (2023).

Li, J., Xie, C., Cai, W., Wang, J. & Wang, C. A facility-level phaseout strategy for china’s blast furnaces to address multiple policy objectives. Environ. Sci. Technol. 57, 10501–10511 (2023).

Vogl, V., Olsson, O. & Nykvist, B. Phasing out the blast furnace to meet global climate targets. Joule 5, 2646–2662 (2021).

Wang, Y., Chen, C., Tao, Y. & Wen, Z. Uneven renewable energy supply constrains the decarbonization effects of excessively deployed hydrogen-based DRI technology https://doi.org/10.5281/zenodo.14882843 (2025).

Acknowledgements

The authors acknowledge the support by National Natural Science Foundation of China with No. 72140008 (Z.W.) and 72304072 (C.C.), and the New Cornerstone Science Foundation through the XPLORER PRIZE (Z.W.). The work described in this paper was conducted in part by Dr. Chen Chen, Jockey Club Global STEM Post-doctoral Fellow supported by The Hong Kong Jockey Club Charities Trust.

Author information

Authors and Affiliations

Contributions

Y.W., C.C., and Z.W. co-designed the study. Y.W. and C.C. contributed to data collection and processing, Y.W. conducted technical analyses and results interpretation. Y.W. and C.C. wrote the paper, and Y.T. and Z.W. revised the paper.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Communications thanks Haibin Zuo and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Source data

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Wang, Y., Chen, C., Tao, Y. et al. Uneven renewable energy supply constrains the decarbonization effects of excessively deployed hydrogen-based DRI technology. Nat Commun 16, 4916 (2025). https://doi.org/10.1038/s41467-025-59730-1

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s41467-025-59730-1