Abstract

Cryptocurrency has become a hot area of global investment. Despite the increasing regulation of cryptocurrencies, some investors are still obsessed with investing in cryptocurrencies, and the reasons behind this are worth exploring. Emerging studies from a cryptocurrency behavioural perspective demonstrate that investments in cryptocurrency are influenced by a variety of factors, but ignore the objective factor of the political environment. Based on social norms theory, this article explores the impact of group norms and policy norms on Chinese investors’ autonomous motivation to invest in cryptocurrencies. This article adopts a questionnaire and investigates 727 Chinese investors. Research has found that: (1) Cryptocurrency investment is influenced by group norms and policy norms, and autonomous motivation serves as a mediator in the process. Group norms promote autonomous motivation among investors, thereby increasing cryptocurrency investment. Conversely, policy norms inhibit investors’ autonomous motivation and reduce cryptocurrency investment. (2) Cryptocurrency knowledge plays a moderating role between social norms and autonomous motivation. The moderating effects of investors’ subjective and objective knowledge of cryptocurrency in the model have no significant differences, showing a consistent suppressing effect on autonomous motivation. The findings suggest governments should focus on both regulations and public opinion. On the one hand, the government needs to strengthen and improve the laws and regulations related to cryptocurrencies. On the other hand, the government also needs to strengthen social supervision and exercise necessary control in the dissemination of cryptocurrency information.

Similar content being viewed by others

Introduction

Since the creation of the first cryptocurrency Bitcoin in 2008, the cryptocurrency market has experienced exponential growth in the past decade. As of May 2023, CoinMarketCap.com, a cryptocurrency tracking website, listed 23,913 cryptocurrencies, with a market cap of 118.78 billion dollars. Due to its uncertain price fluctuations and high expected profits (Blau, 2017), “cryptocurrency” has become one of the most attractive and fascinating buzzwords among speculative investors, and created more investment myths than anyone could have imagined (Xi et al., 2020).

The rapid growth of cryptocurrencies has attracted the attention of the media, individual investors, institutional investors and regulators (Almeida and Gonçalves, 2023), and has become an important and practical topic in the field of academic research (Angerer et al., 2021). Emerging literatures have included investor behaviour in the cryptocurrency market and have shown that user investment in cryptocurrencies is influenced by a variety of factors such as investor sentiment (Anamika et al., 2023; Mattke et al., 2021; Guégan and Renault, 2021; Akyildirim et al., 2021; Drobetz et al., 2019), herding effects (Shrotryia and Kalra, 2022; Yousaf and Yarovaya, 2022; Papadamou et al., 2021; Bouri et al., 2019), social influence (Osakwe et al., 2022; Gupta et al., 2021), financial knowledge (Zhao and Zhang, 2021), perceived behavioural control (Veerasingam and Teoh, 2023; Pham et al., 2021), trust and suspicion (Osakwe et al., 2022; Arli et al., 2021; Gupta et al., 2021; Chouk and Mani, 2019).

There is no doubt that these studies are important to our understanding of the psychological determinants behind cryptocurrency investments. However, the role of the policy environment, an objective factor, in investor behaviour has been overlooked by many studies (Shahzad et al., 2018; Arli et al., 2021; Ooi et al., 2021). Although cryptocurrencies appear to be a viable investment option, many countries around the world have tightened regulatory restrictions on cryptocurrencies due to their potential risks (Dabbous et al., 2022; Albayati et al., 2020; Shahzad et al., 2018), including China. China has required the resolute prevention and control of financial risks, including cracking down on Bitcoin mining and trading, to prevent individual risks from being transmitted to society (China Daily, 2021). Surprisingly, Chinese investors are fearlessly investing in cryptocurrencies despite government regulation, prompting us to investigate Chinese investors’ willingness to invest in cryptocurrencies and, in particular, the motivating factors behind it. Considering both group and policy factors, we investigate the impact of descriptive norms (namely group norms) and injunctive norms (namely policy norms) on cryptocurrency investment based on social norms theory and provide a new insight that investors purchase cryptocurrencies out of autonomous motivation.

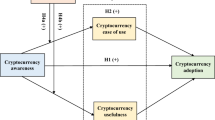

We believe that group norms and policy norms will cause conflicting reactions from investors. On one hand, according to the social identity theory (Ashforth and Mael, 1989), group norms set an example for investors and satisfy the need for individual belonging, which triggers an autonomous motivation for investing in cryptocurrencies. On the other hand, based on normative focus theory (Cialdini et al., 1990), policy norms control cryptocurrency behaviour in the form of penalties that increase investors’ perception of risk in cryptocurrencies, thereby inhibiting their autonomous motivation and reducing cryptocurrency investment. In this paper, these two contradictory effects are juxtaposed as the ambivalence hypothesis (Bartikowski et al., 2021). This shows that when investors consider cryptocurrency, they experience psychological conflict among group norms, policy norms, and cryptocurrency investment. We focus on answering two questions: first, what is the mechanism by which social norms influence cryptocurrency investment? The second is whether there is a boundary condition that makes investors change their investments in cryptocurrencies. We tested these research questions on Chinese cryptocurrency users. In the political context where the government has repeatedly banned cryptocurrency, China is still one of the most important cryptocurrency markets in the world (Kaiser et al., 2018). This background provides us with a suitable place for testing the ambivalence hypothesis, as well as strong empirical support. The research model in this paper is shown in Fig. 1.

The model shows the relationship between the main variables. The arrows indicate the mechanism of influence between the variables.

Literature review and hypotheses

Cryptocurrency investment under social norms

Social norms are spread among group members through communication and represent a behavioural standard widely recognized by members of a certain group in a specific situation (Rimal and Lapinski, 2015; Lapinski and Rimal, 2005), providing reference information for individuals to act or not. According to the content of norms, social norms are distinguished into descriptive and injunctive norms. Descriptive norms are descriptions of behaviours that most people in the social environment are doing, and are an individual’s perception of the behaviour of the majority of the social group; whereas injunctive norms are ways of behaviour that a person should follow, and convey the standards of behaviour that society favours or opposes for a particular behaviour.

As an emerging financial instrument, cryptocurrencies are becoming more and more popular with investors (Khan et al., 2020). News related to cryptocurrency investment has spread wildly on the Internet and investors have gradually formed a specific social group. For cryptocurrency, descriptive norms thus represent to a certain extent the attitudes or atmosphere of social groups that actively invest in cryptocurrency, and thus form group norms. Many people, stimulated by group pressure and a large amount of public opinions, have also begun to invest in cryptocurrencies. Studies have shown that the peer effect (Van Rooij et al., 2011) or herding behaviour (Bouri et al., 2019; Gurdgiev and O’Loughlin, 2020) in investment will make it easier for people to invest in cryptocurrency. In addition, when people are active users of social media, the opinions of important reference groups will also enhance their confidence in investing in cryptocurrency, becoming their psychological reason for adopting cryptocurrency (Anser et al., 2020). The Bank of Canada’s survey for Bitcoin in 2017 indicated that “a friend around me owns Bitcoin” is one of the main driving forces for users to invest in Bitcoin (Henry et al., 2018). Therefore, group norms may be related to cryptocurrency investment.

In contrast to group norms, it has become the consensus of many governments that the supervision of cryptocurrency must be strengthened. Cryptocurrencies are forbidden in Bangladesh, Bolivia, Ecuador, and Nepal (Bitcoin, 2017). Australia has also recently enacted laws to include cryptocurrency transactions and institutions that facilitate transactions within the scope of money laundering and counter-terrorism financing laws (Breidbach and Tana, 2021). Like other economies, China is also working hard to regulate cryptocurrency to avoid the financial risks and economic shocks it brings, and thus form policy norms. In 2017, within 24 h after China announced the ban on initial coin offering (ICO), the market value of Ethereum (ETH) decreased by 6 billion US dollars, while in the same 24 h, the price of Bitcoin fell by $200 (Okorie and Lin, 2020). In addition, the trading volume of China’s cryptocurrency exchanges has seen an unprecedented decline (Borri and Shakhnov, 2020). Okorie (2020) showed that the exogenous market pressure of China and other economies banning ICOs has significantly affected the Bitcoin market and changed the structure of the market. The government’s intervention in the cryptocurrency market can significantly change the relationship between the inherent rate of return and the transaction volume in the market, consequently reducing returns (Okorie and Lin, 2020). In summary, we propose the following hypotheses:

H1a: Group norms promote cryptocurrency investment. That is, the positive attitudes and atmosphere of social groups towards cryptocurrency will increase cryptocurrency investment.

H1b: Policy norms inhibit cryptocurrency investment. That is, the government’s regulatory restrictions or policy prohibitions on cryptocurrency will reduce cryptocurrency investment.

The mediating effect of autonomous motivation

Autonomous motivation is the motivation of an individual to engage in a behaviour spontaneously and actively out of self-will and free choice (Ryan and Deci, 2000). When group members buy cryptocurrencies actively, the positive atmosphere sends a “positive signal” to investors, thus creating a “role model” in their minds. Motivated by role models, investors are motivated by intrinsic beliefs to invest on their own and are motivated to buy. At the same time, social groups are an important source of information for investors, and the behaviour of the group plays a non-negligible role in shaping the external environment of investors. Social learning theory suggests that individuals’ environment influences their motivation and behaviour to learn (Bandura, 1978). Proactive groups create a proactive investment environment for investors. Therefore, investors in this environment will be infected and are more likely to want to be like the proactive groups around them, striving to be “winners” in their investments. Infected investors are then spontaneously motivated to invest, forming autonomous motivation. While in the context of cryptocurrencies, a series of regulatory policies set by the government may lead to a sharp decline in the ex-post returns and a decrease in the value of cryptocurrencies (Okorie and Lin, 2020), which will result in investors not capturing high returns or even losing material wealth. Investors’ exposure to external cues (policy risk and loss of wealth) enhances their self-control to purchase cryptocurrencies, thus inhibiting autonomous motivation (Sudzina et al., 2023).

In addition, research has shown that autonomous motivation is influenced by basic intrinsic needs such as autonomy, competence, and belonging. Among these, the need for autonomy refers to individuals having a sense of autonomous choice in their actions, rather than being controlled by others. The need to belong is defined as a person’s need to stay connected to others and to have a sense of belonging (Ryan and Deci, 2020). Group norms can strengthen an individual’s ties to the “group” and enhance a sense of belonging, and therefore may enhance autonomous motivation. Conversely, policy norms often compel individuals to adopt certain behaviours through rewards or punishments and do not support autonomous choices, thus policy norms usually negatively affect autonomous motivation (Chan et al., 2021; Pelletier and Aitken, 2014). Satisfaction of needs such as autonomy, competence, and belonging facilitate autonomous motivation, and autonomous motivation enhances individuals’ information-seeking (White et al., 2019), leading to greater enjoyment and more effort in the target activity (Dubnjakovic, 2018). Therefore, autonomous motivation may facilitate cryptocurrency investment. In summary, we propose the following hypothesis:

H2: Autonomous motivation plays a mediating role between social norms and cryptocurrency investment.

The moderating effect of cryptocurrency knowledge

Investors’ financial knowledge can be divided into subjective knowledge (SK) and objective knowledge (OK), which will influence their decision-making (Park et al., 1994). Subjective knowledge refers to the degree of an investor’s understanding of the product, while objective knowledge refers to the characteristic information related to the product stored in the investor’s memory (Rezvani et al., 2012). In other words, objective knowledge describes what a person knows, while subjective knowledge reflects the degree of confidence a person has in their knowledge.

In an environment of uncertainty and complex choices, subjective knowledge is a stronger motivator of behaviour than objective knowledge. In the field of financial decision-making, Hadar et al. (2013) proved that the improvement of investors’ subjective knowledge can increase the willingness to invest under uncertainty. Nazifi et al. (2021) also concluded that Bitcoin, as a more familiar cryptocurrency, will bring greater satisfaction to investors than less familiar cryptocurrencies such as EOS. Therefore, the improvement of subjective knowledge may increase investors’ autonomous motivation to invest. In other words, a high level of subjective knowledge can increase autonomous motivation, thereby enhancing the positive effect of group norms on autonomous motivation and weakening the negative impact of policy norms on autonomous motivation.

Although subjective and objective knowledge is strongly correlated (Van Rooij et al., 2011), however, some studies have shown that subjective and objective knowledge are different knowledge structures and they are not always perfectly aligned (Ryu and Ko, 2019). If investors are exposed to too much product information, their objective knowledge may be improved, but they may be discouraged from cryptocurrency (Hadar et al., 2013). The survey by Henry et al. (2019) also found that Canadian investors had improved their basic knowledge of Bitcoin during the years 2017 and 2018, but only a few people had adopted and invested in Bitcoin since many non-owners recognized that Bitcoin had no government support. Therefore, investors’ objective knowledge of financial decisions may reduce their autonomous motivation. That is to say, high objective knowledge can limit autonomy and guide people to manage their risky investments, thereby weakening the positive effect of group norms on autonomous motivation and enhancing the negative impact of policy norms on autonomous motivation. Based on the above reasoning, we propose the following hypotheses:

H3a: Subjective knowledge (SK) of cryptocurrency positively moderates the effect of group norms on autonomous motivation, while it negatively moderates the effect of policy norms on autonomous motivation.

H3b: Objective knowledge (OK) of cryptocurrency negatively moderates the effect of group norms on autonomous motivation, while it positively moderates the effect of policy norms on autonomous motivation.

Methodology

Sample and data collection

We targeted users who paid attention to cryptocurrency investment and collected data through an online research platform. In the process of data collection, the guidelines of Song and Parry (1996) were used. After reviewing the existing literature, we compiled an English questionnaire. To create the Chinese version of these measurement items, we adopted the translation and back translation technique to ensure concept equivalence and accuracy. The questionnaire was finalized through a pre-test in which a total of 256 questionnaires were collected. On this basis, we refined and improved the questionnaire and completed the survey process.

We issued this survey in June 2021 and collected data for a month. A total of 1100 questionnaires were collected, covering 31 provinces, municipalities, and autonomous regions in China. To ensure the validity of the samples, at the beginning of the questionnaire, we set items to test whether users knew about cryptocurrency investment. Through the screening process, 281 invalid cases were eliminated. In addition, based on the questionnaire traps identified by Krosnick (1991), the questionnaires are also screened according to the logical relationship between the items and whether a particular option was repeatedly selected to ensure the validity of the data. Seventy-two cases were excluded in this step, and 727 valid questionnaires were finally retained, for an effective recovery of 66%. As shown in Table 1, there was a small difference in the number of groups that had invested in cryptocurrency (44.8%) and those that had not invested in cryptocurrency but may be potential investors (55.2%). Gender difference was also relatively small (male 48.3%, female 51.7%). Therefore, the sample was sufficiently representative for the investigation of cryptocurrency investment.

Measures

Except for objective knowledge, all other constructs were measured by multiple items (see Appendix for details) and sorted in reverse order to minimize bias in the survey. Each item was rated on a seven-point Likert scale (1 = completely disagree; 7 = completely agree). Four items from Ryu and Ko (2019) were used to measure group norms. The scale assesses the influence of social groups on user investment. Based on previous research (Xie, 2019), we developed a scale of policy norms, including four items. We adopted an autonomous motivation measure from previous studies (Mustafa and Ali, 2019; Kuvaas, 2006). It consists of four items that reflect investors’ autonomous motivation to participate in cryptocurrency investment. We adopted Ryu and Ko’s (2019) four measurement items of subjective knowledge of Bitcoin. We also referred to their measurement methods of objective knowledge and developed 10 judgement questions about cryptocurrency knowledge with three options (true/false/do not know). Cryptocurrency investment was measured with the three items from Palamida et al. (2018) to evaluate users’ willingness to invest in cryptocurrencies. Finally, several control variables were considered, including gender, age, education, investment experience, and investment expenditure. These have been shown in previous studies to be factors that affect investment (Cole et al., 2014; Eckel and Füllbrunn, 2015; Korniotis and Kumar, 2011; Malmendier and Nagel, 2011; Titman et al., 2004).

Results

Measurement model

A measurement model including independent variables, moderators, mediators, control variables and dependent variables was constructed. Firstly, we conducted descriptive statistics and correlation analyses, as shown in Table 2. Then, we conducted reliability and validity analyses. The results (see Table 3) showed that Cronbach’s α value of each variable was >0.9, and the KMO value was >0.7, indicating that the scale had good reliability and validity. Confirmatory factor analysis was conducted through structural equation modelling to test construct validity. The results showed that the standardized factor loading of each variable was >0.8 and the composite reliability (CR) was >0.9, consistent with α. The average variance extraction (AVE) of each variable was >0.7, and the convergence validity was supported. Each square root of AVE (SAVE) was greater than the correlation coefficient between the corresponding variable and other variables, indicating that each variable had good discriminant validity. In addition, the overall fitting degree of the research model reached an acceptable level (χ2 = 471.08, χ2/DF = 3.32, GFI = 0.93, CFI = 0.98, IFI = 0.98, RMSEA = 0.06). In general, the measurement model was suitable for further analysis.

The main effect of social norms

We constructed a model of the relationship between group norms, policy norms, and investment behaviour. The main effect of the model was verified by examining the influences of group norms and policy norms on cryptocurrency investment. We took the average value of items belonging to each construct to perform the multiple linear regression. The results (Table 4) showed that the research model well explained the influence of independent variables on dependent variables (F (7719) = 25.172, p < 0.001, R2 = 0.197), group norms had a significant positive effect on investment behaviour (β = 0.354, p < 0.001), and policy norms had a significant negative suppressing effect on investment behaviour (β = −0.12, p < 0.01). Therefore, H1a and H1b were supported.

Mediating effect of autonomous motivation

Bootstrap was used to further explore the relationships among group norms, policy norms, autonomous motivation, and cryptocurrency investment. Using Process analysis, the confidence interval of the research was set to 95%, and the sample size was 5000. As shown in Table 5 and Fig. 2, after controlling for other factors, group norms significantly increased investors’ autonomous motivation (Model 1, β = 0.416, p < 0.001). The direct effect of group norms on cryptocurrency investment was 0.253, and the confidence interval was [0.177, 0.329], excluding 0, indicating that group norms had a significant positive impact on cryptocurrency investment. Also, the indirect effect of group norms on cryptocurrency investment was 0.139, and the confidence interval was [0.097, 0.184] and did not contain 0. Therefore, autonomous motivation partially mediated the influence of group norms on cryptocurrency investment. In addition, policy norms had a significant suppressing effect on cryptocurrency investment (Model 2, β = −0.417, p < 0.001). The direct effect of policy norms on cryptocurrency investment was 0.033, and the confidence interval was [−0.046, 0.112], including 0, indicating that under the mediation of autonomous motivation, policy norms had no significant direct impact on cryptocurrency investment. The indirect effect was −0.186, and the confidence interval was [−0.232, −0.140], excluding 0, indicating that autonomous motivation completely mediated the impact of policy norms on cryptocurrency investment. H2 was supported.

The confidence intervals for autonomous motivation in both group norms and policy norms paths do not contain 0, indicating a significant indirect effect of autonomous motivation with a mediating effect.

Moderating effect of cryptocurrency knowledge

Based on previous research (Ryu and Ko, 2019), we divided investors’ cryptocurrency knowledge into subjective knowledge (SK) and objective knowledge (OK). The bootstrap method was also employed to test the moderating effects of subjective knowledge and objective knowledge respectively. Since subjective knowledge is a continuous variable, the involved continuous variables were centralized to reduce the problem of collinearity. On the basis of considering relevant control variables, we tested the moderating effects of subjective knowledge between group norms and autonomous motivation (Model 1 in Table 6) and that between policy norms and autonomous motivation (Model 2 in Table 6) respectively. Since the investigation of objective knowledge was carried out by judging true or false, we used the number of questions that respondents answered correctly and divided respondents’ objective knowledge into high and low levels. Among the 10 objective questions related to cryptocurrency, respondents who answered fewer than 5 questions correctly were considered as having low objective knowledge and coded as 0; respondents who answered 5 or more questions correctly were considered as having high objective knowledge and coded as 1. After controlling for other factors, we tested the moderating effect of objective knowledge between group norms and autonomous motivation (Model 3 in Table 6) and that between policy norms and autonomous motivation (Model 4 in Table 6).

As shown in Model 1 of Table 6, group norms had a positive effect on autonomous motivation (β = 0.429, p < 0.001), while the interaction between group norms and subjective knowledge significantly inhibited users’ autonomous motivation (β = −0.174, p < 0.001), indicating that subjective knowledge negatively moderated the effect of group norms on autonomous motivation. A simple slope analysis showed that the slope of the positive influence of group norms on autonomous motivation was significantly smaller for the high subjective knowledge group than for the low subjective knowledge group (Fig. 3). In Model 2, policy norms were shown to have a negative effect on autonomous motivation (β = −0.356, p < 0.001), and the interaction of policy norms and subjective knowledge also had a suppressing effect on autonomous motivation (β = −0.145, p < 0.001), indicating that subjective knowledge positively moderated the effect of policy norms on autonomous motivation. A simple slope analysis showed that the slope of the negative influence of policy norms on autonomous motivation was steeper in the high subjective knowledge condition than in the low subjective knowledge condition (Fig. 3). The above results exactly contradicted the hypothesis, and H3a was not supported.

a Shows the moderating role of subjective knowledge in the relationship between group norms and autonomous motivation. b Shows the moderating role of subjective knowledge in the relationship between policy norms and autonomous motivation.

For objective knowledge, group norms had a positive impact on autonomous motivation (β = 0.517, p < 0.001, Model 3), while the interaction between group norms and objective knowledge inhibited users’ autonomous motivation (β = −0.269, p < 0.001), indicating that objective knowledge negatively moderated the effect of group norms on autonomous motivation. This was further confirmed by simple slope analysis, which revealed that the slope of the positive influence of group norms on autonomous motivation was flatter for users with high objective knowledge than for users with low objective knowledge (Fig. 4). In Model 4, policy norms were found to have a negative impact on autonomous motivation (β = −0.231, p < 0.001), and the interaction between policy norms and objective knowledge also inhibited autonomous motivation (β = −0.235, p < 0.001), implying that objective knowledge positively moderated the effect of policy norms on autonomous motivation. A simple slope analysis showed that the slope of the negative influence of policy norms on autonomous motivation was significantly smaller for users with high objective knowledge than for those with low objective knowledge (Fig. 4). The above results were consistent with the hypothesis, and H3b was supported.

a Shows the moderating role of objective knowledge in the relationship between group norms and autonomous motivation. b Shows the moderating role of objective knowledge in the relationship between policy norms and autonomous motivation.

Discussion and conclusion

The results of this research show that the behaviour of users investing in cryptocurrency is autonomous. Users who are more affected by group norms will react autonomously and then increase their cryptocurrency investment. Users who are more affected by policy norms will control and reduce their autonomous motivation, resulting in lower cryptocurrency investment. To prevent cryptocurrency investment, the government’s policy norms are very important. If strict policy norms are not formulated, autonomous motivation cannot be suppressed, leading to the occurrence of cryptocurrency investment. Moreover, this research proves the importance of cryptocurrency knowledge in the cognitive process of users’ cryptocurrency investment. Specifically, objective knowledge weakens the autonomous motivation to invest, thereby inhibiting cryptocurrency investment. However, contrary to the hypothesis, subjective knowledge does not strengthen autonomous motivation but weakens it. One possible explanation is that subjective knowledge is usually consistent with objective knowledge, and it is to a certain extent a reflection of objective knowledge, therefore presenting a similar moderation mechanism to that of objective knowledge.

Our study is one of the few studies to examine cryptocurrency investment behaviour from the perspective of users, which expands the current research scope on cryptocurrency behaviour. Although previous studies have contributed to the investigation of cryptocurrency, most of them ignored the objective influence of the political environment. Based on social norms theory, we considered both group and policy factors and provides new insight, that users’ investment in cryptocurrency is affected by group norms and policy norms. Therefore, this research supplements the existing literature on the use of macro variables and explains investors’ decisions on cryptocurrency investment. Cryptocurrency investment has become an irreversible trend, and its anticipated global persistence enhances the theoretical value of this research.

Our research provides new insights into understanding the behavioural mechanisms of users investing in cryptocurrencies. Previous studies have explored the psychological mechanisms of cryptocurrency investment in terms of trust, perceived risk, and perceived behavioural control. In contrast, we empirically analysed the role of autonomous motivation in users’ cryptocurrency investment behaviour based on self-determination theory. Our results showed that users who invest in cryptocurrencies are influenced by autonomous motivations because they want to satisfy their internal needs, such as a sense of belonging. Furthermore, self-determination theory is often applied in the fields of education and work, and we extend the applicability of self-determination theory by applying it to consumer investments, especially in emerging cryptocurrencies.

We also identify a boundary condition that influences users’ investment in cryptocurrencies, that is, their cryptocurrency knowledge. We showed that users tend to invest less in cryptocurrencies when they have a higher level of cryptocurrency knowledge (either subjective or objective), as they are more self-controlled and less motivated by autonomy. Although it has been demonstrated that financial knowledge plays an important role in users’ investment in cryptocurrencies, there is a distinction between cryptocurrency knowledge and it. Financial knowledge may be an investor’s understanding of financial information, while cryptocurrency knowledge is an investor’s knowledge of the cryptocurrency product itself. That is, a user may have a wealth of financial knowledge but not necessarily a wealth of cryptocurrency knowledge. At this level, our study also enriches the literatures on consumer investment knowledge and provides new perspectives.

The findings suggest governments should focus on both regulations and public opinion. On the one hand, the government needs to strengthen and improve the laws and regulations related to cryptocurrencies. It is also necessary to make simultaneous amendments and improvements to other related laws and to write cryptocurrency into the law as soon as possible so that the law can be followed and enforced. On the other hand, the government also needs to strengthen social supervision and exercise necessary control in the dissemination of cryptocurrency information. Some investors are teaching investment experience and advocating cryptocurrency investment in online forums and communities, which inevitably leads some potential targets to invest in cryptocurrencies after being exposed to such information. In response, the government can shut down website platforms dedicated to cryptocurrency marketing and advocacy and publishing tutorials on cross-border speculation in cryptocurrencies. At the same time, the government also needs to clean up and dispose of illegal and irregular information, accounts, and websites that speculate on cryptocurrencies, and increase its efforts to correct information content and accounts that induce cryptocurrency investments. In addition, the government needs to popularize and strengthen cryptocurrency knowledge education to enhance national financial literacy. Users with little financial literacy are willing to pursue high-risk investments, so people with lower cryptocurrency knowledge show a stronger motivation for autonomy, resulting in cryptocurrency investment. Investments that lack knowledge of cryptocurrencies should be strictly monitored and regulated. In this regard, what the government should do is promote and popularize the principles and knowledge related to cryptocurrencies and the essential differences between cryptocurrencies and other financial instruments in order to improve the subjective and objective knowledge of investors. For example, the government can promote and popularize cryptocurrency knowledge by making science videos online and holding regular educational seminars offline.

This study has several limitations. We adopted a questionnaire survey, which relied on the self-reported data of the participants. Because the participants may have exaggerated or downplayed their behavioural responses, the actual values of the constructs may be overestimated or underestimated. Future research may consider big data methods such as data mining to objectively measure these constructs so as to reduce research bias and provide more robust results. In addition, since the research on cryptocurrency is still in its early stages, the measurement methods of cryptocurrency investment have not been fully tested. Furthermore, we used the top ten cryptocurrencies in terms of market value to represent cryptocurrency in general during the survey. However, there are many types of cryptocurrencies, so the scope of our research may not be highly representative. Future research needs to expand the scope of the research to other cryptocurrencies to provide comprehensive coverage. In addition, we used a unified concept to represent all cryptocurrencies, which may have caused the research results to ignore the peculiarities of certain currencies (such as Bitcoin and Dogecoin). Future research can classify and discuss the types and characteristics of currencies, making the research focus more prominent. Finally, our research results may not be universal, for the sample was limited to a specific period and a specific country. Therefore, the results of this study must be interpreted with caution. Considering the importance of time and country characteristics in cryptocurrency, future research needs to apply specific methods, such as longitudinal analysis, and collect more data to closely observe and investigate the investment in cryptocurrencies in different periods and countries around the world.

Data availability

The datasets analysed during the current study are available in the Dataverse repository: https://doi.org/10.7910/DVN/MI0SUF.

Change history

31 August 2023

A Correction to this paper has been published: https://doi.org/10.1057/s41599-023-02057-3

References

Akyildirim E, Aysan AF, Cepni O, Darendeli SPC (2021) Do investor sentiments drive cryptocurrency prices? Econ Lett 206:109980

Albayati H, Kim SK, Rho JJ (2020) Accepting financial transactions using blockchain technology and cryptocurrency: a customer perspective approach. Technol Soc 62:101320

Almeida J, Gonçalves TC (2023) A systematic literature review of investor behavior in the cryptocurrency markets. J Behav Exp Financ 37:100785

Anamika, Chakraborty M, Subramaniam S (2023) Does sentiment impact cryptocurrency? J Behav Financ 24(2):202–218

Angerer M, Hoffmann CH, Neitzert F, Kraus S (2021) Objective and subjective risks of investing into cryptocurrencies. Financ Res Lett 40:101737

Anser MK, Zaigham GHK, Imran Rasheed M, Pitafi AH, Iqbal J, Luqman A (2020) Social media usage and individuals’ intentions toward adopting Bitcoin: the role of the theory of planned behaviour and perceived risk. Int J Commun Syst 33(17):e4590

Arli D, van Esch P, Bakpayev M, Laurence A (2021) Do consumers really trust cryptocurrencies? Mark Intell Plan 39(1):74–90

Ashforth BE, Mael F (1989) Social identity theory and the organization. Acad Manage Rev 14(1):20–39

Bandura A (1978) The self system in reciprocal determinism. Am Psychol 33(4):344

Bartikowski B, Fastoso F, Gierl H (2021) How nationalistic appeals affect foreign luxury brand reputation: a study of ambivalent effects. J Bus Eth 169(2):261–277

Bitcoin (2017) Five countries where Bitcoin is illegal. https://news.bitcoin.com/five-countries-where-bitcoin-is-illegal/

Blau BM (2017) Price dynamics and speculative trading in bitcoin. Res Int Bus Financ 41:493–499

Borri N, Shakhnov K (2020) Regulation spillovers across cryptocurrency markets. Financ Res Lett 36:101333

Bouri E, Gupta R, Roubaud D (2019) Herding behaviour in cryptocurrencies. Financ Res Lett 29:216–221

Breidbach CF, Tana S (2021) Betting on Bitcoin: how social collectives shape cryptocurrency markets. J Bus Res 122:311–320

Chan DK, Zhang CQ, Weman-Josefsson K (2021) Why people failed to adhere to COVID-19 preventive behaviours? Perspectives from an integrated behaviour change model. Infect Control Hosp Epidemiol 42(3):375–376

China Daily (2021) Government busts myth about virtual currency chasing wealth. https://global.chinadaily.com.cn/a/202105/26/WS60ad7caaa31024ad0bac15ec.html

Chouk I, Mani Z (2019) Factors for and against resistance to smart services: role of consumer lifestyle and ecosystem related variables. J Serv Mark 33(4):449–462

Cialdini RB, Reno RR, Kallgren CA (1990) A focus theory of normative conduct: Recycling the concept of norms to reduce littering in public places. J Pers Soc Psychol 58(6):1015

Cole S, Paulson A, Shastry GK (2014) Smart money? The effect of education on financial outcomes. Rev Financ Stud 27(7):2022–2051

Dabbous A, Merhej Sayegh M, Aoun Barakat K (2022) Understanding the adoption of cryptocurrencies for financial transactions within a high-risk context. J Risk Financ 23(4):349–367

Drobetz W, Momtaz PP, Schröder H (2019) Investor sentiment and initial coin offerings. J Altern Invest 21(4):41–45

Dubnjakovic A (2018) Antecedents and consequences of autonomous information seeking motivation. Libr Inf Sci Res 40(1):9–17

Eckel CC, Füllbrunn SC (2015) Thar she blows? Gender, competition, and bubbles in experimental asset markets. Am Econ Rev 105(2):906–20

Guégan D, Renault T (2021) Does investor sentiment on social media provide robust information for Bitcoin returns predictability? Financ Res Lett 38:101494

Gupta S, Gupta S, Mathew M, Sama HR (2021) Prioritizing intentions behind investment in cryptocurrency: a fuzzy analytical framework. J Econ Stud 48(8):1442–1459

Gurdgiev C, O’Loughlin D (2020) Herding and anchoring in cryptocurrency markets: Investor reaction to fear and uncertainty. J Behav Exp Financ 25:100271

Hadar L, Sood S, Fox CR (2013) Subjective knowledge in consumer financial decisions. J Mark Res 50(3):303–316

Henry CS, Huynh KP, Nicholls G (2018) Bitcoin awareness and usage in Canada. J Digit Bank 2(4):311–337

Henry CS, Huynh KP, Nicholls G (2019) Bitcoin awareness and usage in Canada: an update. J Invest Cryptocurr 28(3):21–31

Kaiser B, Jurado M, Ledger A (2018) The looming threat of China: an analysis of Chinese influence on bitcoin. arXiv preprint arXiv:1810.02466

Khan K, Zhao H, Zhang H, Yang H, Shah MH, Jahanger A (2020) The impact of COVID-19 pandemic on stock markets: an empirical analysis of world major stock indices. J Asian Financ Econ Bus 7(7):463–474

Korniotis GM, Kumar A (2011) Do older investors make better investment decisions? Rev Econ Stat 93(1):244–265

Krosnick JA (1991) Response strategies for coping with the cognitive demands of attitude measures in surveys. Appl Cogn Psychol 5(3):213–236

Kuvaas B (2006) Performance appraisal satisfaction and employee outcomes: mediating and moderating roles of work motivation. Int J Hum Resour Manag 17(3):504–522

Lapinski MK, Rimal RN (2005) An explication of social norms. Commun Theory 15(2):127–147

Malmendier U, Nagel S (2011) Depression babies: do macroeconomic experiences affect risk taking? Q J Econ 126(1):373–416

Mattke J, Maier C, Reis L, Weitzel T (2021) Bitcoin investment: a mixed methods study of investment motivations. Eur J Inform Syst 30(3):261–285

Mustafa G, Ali N (2019) Rewards, autonomous motivation and turnover intention: results from a non-western cultural context. Cogent Bus Manag 6(1):1676090

Nazifi A, Murdy S, Marder B, Gäthke J, Shabani B (2021) A Bit (coin) of happiness after a failure: an empirical examination of the effectiveness of cryptocurrencies as an innovative recovery tool. J Bus Res 124:494–505

Okorie DI (2020) Could stock hedge bitcoin risk (s) and vice versa? Digit Financ 2(1):117–136

Okorie DI, Lin B (2020) Did China’s ICO ban alter the bitcoin market? Int Rev Econ Financ 69:977–993

Ooi SK, Ooi CA, Yeap JA, Goh TH (2021) Embracing Bitcoin: users’ perceived security and trust. Qual Quant 55:1219–1237

Osakwe CN, Dzandu MD, Amegbe H, Warsame MH, Ramayah T (2022) A two-country study on the psychological antecedents to cryptocurrency investment decision-making. J Glob Inf Technol Manag 25(4):302–323

Palamida E, Papagiannidis S, Xanthopoulou D (2018) Linking young individuals’ capital to investment intentions: comparing two cultural backgrounds. Eur Manag J 36(3):392–407

Papadamou S, Kyriazis NA, Tzeremes P, Corbet S (2021) Herding behaviour and price convergence clubs in cryptocurrencies during bull and bear markets. J Behav Exp Financ 30:100469

Park CW, Mothersbaugh DL, Feick L (1994) Consumer knowledge assessment. J Consum Res 21(1):71–82

Pelletier LG, Aitken NM (2014) Encouraging environmental actions in employees and in the working environment: a self-determination theory perspective. In: The Oxford handbook of work engagement, motivation, and self-determination theory. Oxford University Press, Oxford, USA, pp. 314–334

Pham QT, Phan HH, Cristofaro M, Misra S, Giardino PL (2021) Examining the intention to invest in cryptocurrencies: an extended application of the theory of planned behaviour on Italian independent investors. Int J Appl Behav Econ 10(3):59–79

Rezvani S, Shenyari G, Dehkordi GJ, Salehi M, Nahid N, Soleimani S (2012) Country of origin: a study over perspective of intrinsic and extrinsic cues on consumers’ purchase decision. Bus Manag Dynam 1(11):68–75

Rimal RN, Lapinski MK (2015) A re-explication of social norms, ten years later. Commun Theory 25(4):393–409

Van Rooij M, Lusardi A, Alessie R (2011) Financial literacy and stock market participation. J Financ Econ 101(2):449–472

Ryan RM, Deci EL (2000) Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. Am Psychol 55(1):68

Ryan RM, Deci EL (2020) Intrinsic and extrinsic motivation from a self-determination theory perspective: definitions, theory, practices, and future directions. Contemp Educ Psychol 61:101860

Ryu HS, Ko KS (2019) Understanding speculative investment behaviour in the bitcoin context from a dual-systems perspective. Ind Manage Data Syst 119(7):1431–1456

Shahzad F, Xiu G, Wang J, Shahbaz M (2018) An empirical investigation on the adoption of cryptocurrencies among the people of mainland China. Technol Soc 55:33–40

Shrotryia VK, Kalra H (2022) Herding in the crypto market: a diagnosis of heavy distribution tails. Rev Behav Finance 14(5):566–587

Song XM, Parry ME (1996) What separates Japanese new product winners from losers. J Prod Innov Manage 13(5):422–439

Sudzina F, Dobes M, Pavlicek A (2023) Towards the psychological profile of cryptocurrency early adopters: overconfidence and self-control as predictors of cryptocurrency use. Curr Psychol 42:8713–8717

Titman S, Wei KJ, Xie F (2004) Capital investments and stock returns. J Financ Quant Anal 39(4):677–700

Veerasingam N, Teoh AP (2023) Modeling cryptocurrency investment decision: evidence from Islamic emerging market. J Islam Mark 14(7):1817–1835

White JK, Bromberg-Martin ES, Heilbronner SR, Zhang K, Pai J, Haber SN, Monosov IE (2019) A neural network for information seeking. Nat Commun 10(1):5168

Xi D, O'Brien TI, Irannezhad E (2020) Investigating the investment behaviors in cryptocurrency. J Altern Invest 23(2):141–160

Xie R (2019) Why China had to ban cryptocurrency but the US did not: a comparative analysis of regulations on crypto-markets between the US and China. Wash Univ Global Stud Law Rev 18:457

Yousaf I, Yarovaya L (2022) Herding behavior in conventional cryptocurrency market, non-fungible tokens, and DeFi assets. Financ Res Lett 50:103299

Zhao H, Zhang L (2021) Financial literacy or investment experience: which is more influential in cryptocurrency investment? Int J Bank Mark 39(7):1208–1226

Acknowledgements

This research is supported by Grant no. 72062031 of the National Natural Science Foundation of China.

Author information

Authors and Affiliations

Contributions

The authors confirm their contribution to the paper as follows: YG: conception and design, acquisition of data, analysis and interpretation of data, drafting the manuscript. XT: conception and design, revising theoretical framework, revising the manuscript. E-CC: drafting the manuscript, revising the manuscript critically for important intellectual content. All authors reviewed the results and approved the final version of the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

There was no approval required. Firstly, the method used in this article is a questionnaire, which has a low risk. Secondly, all respondents were given informed consent, volunteered to take the survey and were paid accordingly. Lastly, the survey pledged to protect the privacy of the respondents by using their data only for scientific research and not for other purposes. Therefore, the rights of respondents are safeguarded in this study, in line with the Declaration of Helsinki.

Informed consent

Respondents obtained informed consent while undergoing the questionnaire in June 2021. At the beginning of the survey, respondents were informed that the purpose of the survey is to investigate users’ attitudes towards cryptocurrencies and they can voluntarily choose to participate in the survey.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Gong, Y., Tang, X. & Chang, EC. Group norms and policy norms trigger different autonomous motivations for Chinese investors in cryptocurrency investment. Humanit Soc Sci Commun 10, 521 (2023). https://doi.org/10.1057/s41599-023-01870-0

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-023-01870-0