Abstract

The literature on organizational ambidexterity emphasizes the complex relationship between the balance of exploitation and exploration and its impact on performance. However, the empirical research, while granting special attention to the study of types of ambidexterity and factors conditioning this phenomenon, has largely neglected to analyze balance. Our study is novel in tackling two knowledge gaps in the literature on organizational ambidexterity: the absence of quantitative analyses to pinpoint the optimal exploration–exploitation balance, and the lack of attention paid to the effect of risk on this optimal balance and on organizational ambidexterity in general. In order to address these knowledge gaps, the paper analyzes the technological exploitation-exploration relationship in conditions of uncertainty and the balance that maximizes Value at Risk (VaR) of firm growth. The methodology includes the elaboration of VaR, using the expected value and degree of dispersion in firm growth, and the combination of quantitative methods for hypothesis testing. Results obtained from a sample of 87,911 European firms from all sectors confirm the positive effect on the growth of harmonious efforts in exploration and exploitation, determining technological balance according to an organization’s risk-taking. The findings are relevant to theory and decision-making by managers and policymakers.

Similar content being viewed by others

Introduction

Exploration and exploitation are associated with objectives, activities, cognitive processes, and antagonistic organizational routines that vie for the firm’s available resources (Stettner and Lavie, 2014). Exploiting activity has been associated with alignment, refinement, efficiency, selection, implementation, and mechanistic structures, whereas exploratory activity is linked with search, variation, risk-taking, experimentation, and organic structures in firms (March, 1991). Despite substantial differences separating these activities, the use of the exploration–exploitation paradigm in different fields of study has clearly revealed a contingent relationship between the two, whose influence generally affects business performances (Derbyshire, 2014; Feng et al. 2024; Gupta et al. 2006; Hill and Birkinshaw, 2014). Management of this “ecological interaction” between exploration and exploitation (March, 1991, p. 71) requires expertise in both areas and efficient handling of their interaction in the firm. The term organizational ambidexterity identifies the ability to dynamically balance exploration and exploitation levels to achieve the ideal equilibrium or combination in the context of both activities (Cao et al. 2009; Gibson and Birkinshaw, 2004; Luger et al. 2018; Roth and Corsi, 2023). This capacity is difficult to cultivate (Gupta et al. 2006; March, 1991), and its effects on performance (Raisch and Birkinshaw, 2008; Raisch et al. 2009) hinge on organizational and environmental factors (Fourné et al. 2019; Stettner and Lavie, 2014; Uotila et al. 2009).

A deeper inquiry into the paradoxical links between activities of exploitation and exploration of technological knowledge appears a plausible objective for achieving a realistic description of organizational ambidexterity and analyzing its implications from various perspectives (Audretsch and Guerrero, 2023). Market volatility and accelerated technological progress currently spur changing environmental conditions (Uotila et al. 2009) that decision-makers interpret according to their capacity to assume risks (Wilden et al. 2018). In this context, uncertainty amplifies the risks inherent to each decision (Johnson et al. 2014), rendering the study of exploration–exploitation balance under uncertainty especially relevant. Inquiry into this area could generate methodologies to aid in empirical research of organizational ambidexterity in more realistic conditions.

Analysis in conditions of uncertainty using Value at Risk (VaR) (McNeil et al. 2005) provides a more realistic view of the relationship between technological balance and performance, as, for example, in firm growth. In this case, while the expected value indicates the growth expected to occur, it does not show what growth could occur if negative scenarios arise (Chen, 2023). The appearance of a worse-than-expected result could have more or less dire consequences for the firm. Thus, it is crucial to calculate what growth could occur if something worse than expected were to happen (the value of worse-than-expected growth would be VaR). Increased dispersion of growth values from the mean (greater risk) generates more uncertainty in the predicted benefits of balance, whereas reduction of the variability of expected values (lesser risk) boosts certainty and, accordingly, the value of exploration–exploitation balance in decision-making by managers, owners, and investors. From the perspective of VaR, balance, in our case, consists in the exploration–exploitation mix that offers the greatest expected growth combined with a low level of uncertainty.

The economic importance of ambidexterity springs from both the benefits of exploration–exploitation balance (Wang et al. 2017; Wei et al. 2014; Wu et al. 2019; Yuan et al. 2021) and the predictable damages caused by an imbalance or strong specialization in one of the activities (Levinthal and March, 1993; Rojas-Córdova et al. 2023; Zhang et al. 2017). Thus, an excessive orientation toward exploration or toward exploitation can drive a firm into “self-reinforcing cycles that affect their performance negatively” (Luger et al. 2018, p. 467). Excess exploration can set the firm on a spiral of innovations without market success that compromise the firm’s very survival. Overemphasis on this dimension can cause firms to fall into a “failure trap”, or the attempt to correct a series of failures by introducing successive premature innovations to little market success. On the other hand, emphasis on exploitation can lead firms to the so-called “success trap”, in which success imposes a short-term view based on maximizing present benefits to the detriment of exploring new technologies for future competitive contexts (Junni et al. 2013; Luger et al. 2018). These negative consequences of specialization suggest that a competitive strategy based on the balance between exploration and exploitation is preferable for firms.

Analysis of the exploration–exploitation balance suffers practical limitations that hinder the advancement of knowledge on this phenomenon. Firstly, the exploration vs. exploitation dichotomy is difficult to define in a general manner (Lavie et al. 2010), and the researcher’s discriminating criteria may exert a decisive influence on study findings (Gupta et al. 2006; He and Wong, 2004; O’Reilly and Tushman, 2013). Secondly, the use of the theoretical framework of exploration–exploitation in fields as diverse as knowledge management, innovation, strategic orientation, competitive edge, and the mere survival of businesses has yielded a plethora of contradictory findings on balance and its consequences for firms (Patel et al. 2013; Raisch and Birkinshaw, 2008; Snehvrat et al. 2018; Turner et al. 2013; Wilden et al. 2018). Last but not least, the study of balance is conditioned by the selection of performance. Empirical research relates exploration–exploitation balance to a variety of performances, such as sales growth (He and Wong, 2004; Mura et al. 2021), internationalization (Hsu et al. 2013), innovation (Junni et al. 2013), survival (Hill and Birkinshaw, 2014), and longevity (Kim and Huh, 2015), financial outcomes (Uotila et al. 2009), patents (Petruzzelli, 2014), and the firm’s market value (Stettner and Lavie, 2014), as well as certain constructs of these variables (Mura et al. 2021; Raisch and Birkinshaw, 2008), producing often contradictory evidence on ambidexterity, balance and their effects on organizations.

This study’s main objective is to analyze, in conditions of uncertainty, the effect on the growth of the optimal exploration–exploitation combination, which we denominate technological balance, seeking answers to the following three research questions: (1) What type of relationship forms between technological exploration and exploitation at the firm level? (expressed in Hypothesis 1, abbreviated H1), (2) What technological balance maximizes expected firm growth? (question addressed in H2), and (3) What technological balance minimizes uncertainty in firm growth? (question addressed in H3). The responses to these three inquiries will shed light on central questions in the literature regarding the nature of the exploration-exploitation relationship and the effect of balance on performances (Gupta et al. 2006; Lavie et al. 2010).

Following this introduction, the next section discusses the theoretical background and states the research hypotheses. In the section next to that, the empirical research is described, with details on the sample, methodology, and results of said analysis. The penultimate section discusses the results obtained, and the last section treats the main conclusions, implications, limitations, and new lines of research emerging from this study.

Theoretical background

The theoretical framework of exploration and exploitation has been used widely in different fields of research, with the seminal area being the management of technological knowledge (Levinthal and March, 1993; March, 1991), where a prolonged research trajectory exists (e.g. Gibson and Birkinshaw, 2004; Laureiro-Martínez et al. 2015; Wang et al. 2024). The development of this area of inquiry has produced the concepts of technological exploration and technological exploitation (Phene et al. 2012; He and Wong, 2004) to make reference, firstly, to the search for new technological paradigms and markets and, secondly, to the efficient use of technological stock in the improvement of products and processes. Technological ambidexterity describes the organizational capacity to manage both sources of technological knowledge in the firm (Lavie et al. 2010; Stieglitz et al. 2016; Wei et al. 2014). This has led to identifying technological exploration in practice with the internal generation of technological knowledge and technological exploitation with the external acquisition of technological knowledge (Levinthal and March, 1993).

Promising lines of research in technological ambidexterity include those centered on the study of balance and its effect on performance. Research suggests that a balance between exploration and exploitation is key to organizational survival, prosperity, and success (Lavie et al. 2010; March, 1991). This affirmation, denominated in March’s balance hypothesis (Lavie et al. 2011), justifies the in-depth study of the relationship of reinforcement between technological exploration and exploitation and their joint effect on performance.

Though the balance between both organizational behaviors has often been broached in the literature (Lavie et al. 2011; Seo et al. 2023; Wilden et al. 2018), only limited empirical evidence exists on the way to obtain this optimal combination (Gupta et al. 2006) and its impact on performance (He and Wong, 2004). The nature of the exploration–exploitation relationship constitutes another important subject of debate in the literature (Uotila et al. 2009). Gibson and Birkinshaw (2004) detect a strong positive correlation between both dimensions, while Fang and Levinthal (2009) underscore the role also played by exploration in the short term. Lennerts et al. (2020) reveal the direct and indirect effects of exploitation and exploration on performance. Other authors question the synergetic effect between the two dimensions (He and Wong, 2004; Lavie et al. 2010), the beneficial effects of the optimal combination on performance (He and Wong, 2004), and March’s balance hypothesis itself (Lavie et al. 2011).

Scarcer attention has been paid to the quantification of balance between exploration and exploitation, as it is difficult to specify the optimum amount of both activities (Levinthal and March, 1993; Rothaermel and Alexandre, 2009). In fact, balance, or the optimal combination between exploration and exploitation, is contingent and different for each firm, depending on internal factors, such as age (longevity) (Riviezzo et al. 2015), resources, culture, leadership (Lavie et al. 2010) or learning (Levinthal and March, 1993), and external factors, such as the business environment (Geerts et al. 2018), conditions in the sector (Lavie and Rosenkopf, 2006), or market and technological dynamism (He and Wong, 2004; Uotila et al. 2009). The relevance of organizational and environmental conditioners emerges clearly in the determination of balance (Koryak et al. 2018; Rojas-Córdova et al. 2023). Other authors highlight the importance of internal factors, such as ambidextrous capacity and the leadership of the management team, in order to dynamically balance both dimensions (e.g. Dean, 2022).

The concept of balance remains debated in ambidexterity literature. Simply having both exploration and exploitation does not necessarily make an organization ambidextrous (Rothaermel and Alexandre, 2009), both behaviors must coexist in ambidextrous firms. Two juxtaposed theoretical viewpoints have been formulated (Cao et al. 2009; Gupta et al. 2006) to characterize the ambidextrous organization: the perspective of a balance or continuum—balance perspective—and that of orthogonal dimensions and combination—combination perspective (Junni et al. 2013; Lin and Ho, 2021). The first implies that an optimal balance could lie at the midpoint of the exploration–exploitation continuum (Lin and Ho, 2021), whereas the second perspective establishes that both behaviors should reach an elevated level (Junni et al. 2013). Both views have been used in empirical research, but without clarifying which is most suitable to the real situation (Cao et al. 2009; Lavie et al. 2010; Snehvrat et al. 2018; Wei et al. 2014). Empirical evidence of a positive correlation between exploration and exploitation would favor the combination perspective, whereas empirical evidence of a negative correlation between the two would support a balanced perspective (Fourné et al. 2019; Lavie et al. 2010). Additionally, theoretical refinements are needed to advance this question and clarify whether balance implies an equal orientation toward exploration and exploitation (Carmeli and Halevi, 2009). The term ambidextrous has been applied to organizations practicing exploration and exploitation in equal measure (He and Wong, 2004). Nuancing this balance of equal proportions, it has been suggested that “close to optimal balance between exploration and exploitation can be achieved by focusing on medium levels of exploration and high levels of exploitations” (Sirén et al. 2012, p. 36).

Selection of performance is another key question in the empirical analysis of balance. A segment of the literature shows a preference for long-term performances in the study of organizational ambidexterity. According to March (1991), the effects of exploration are unappreciable in the short term, while those of exploitation can be noted, meaning that any analysis of balance and its effects on the firm must be carried out over a more extensive time frame. The nature of organizational ambidexterity is better associated with long-term performance than with the maximization of benefits in the short term, and becoming ambidextrous constitutes a strategic challenge for the survival and growth of firms (March, 1991). Thus, firm growth is a mid- and long-term performance used in the study of organizational ambidexterity (e.g. Raisch and Birkinshaw, 2008; Patel et al. 2013). Empirical research has confirmed the positive effect of organizational ambidexterity on firm growth, measured through sales growth (He and Wong, 2004), variation in number of workers on staff (Andriopoulos and Lewis, 2009), or the average of sales and growth in number of employees (Patel et al. 2013). The influence of firm growth on organizational ambidexterity has also been verified, given that such growth tends to favor access to more internal resources, especially in small organizations (Raisch and Birkinshaw, 2008), while also allowing access to new technologies through networks (Snehvrat et al. 2018), alliances (Wu et al. 2019), and open innovation (Vrontis et al. 2017). This bidirectional positive effect between ambidexterity and growth establishes a virtuous cycle that deserves consideration by managers and policymakers.

In order to delve more deeply into the relationship between technological exploration and exploitation, determine their balance or optimum combination and analyze the influence of technological behavior on firm growth in conditions of uncertainty, the following hypotheses will be empirically tested:

Hypothesis 1: Synergies between exploitation and exploration favor firm growth, valued in conditions of uncertainty.

Hypothesis 2: The balance that maximizes expected growth implies achieving the same level of technological exploration and exploitation in the firm.

Hypothesis 3: The balance that minimizes uncertainty in growth implies achieving a higher level of technological exploitation in the firm.

Empirical research

Sample and variables

The empirical study uses data from The Community Innovation Survey (CIS 2012) by Eurostat, the statistical agency of the European Commission (European Union). Said survey includes data from 87,911 firms pertaining to the 2010–2012 time period. Of these firms, 90% were SMEs (<250 workers) and 10% were large firms (>250 workers). This sample distribution reflects the composition by size of the population of European companies during the years specified.

The variables referring to technological exploitation and exploration are expressed and defined in Section 5.1 of CIS 2012. Following the selection criteria of Levinthal and March (1993), technological exploration corresponds to the variables of In-house R&D and Training for innovative activities, whereas technological exploitation is represented by the variables of External R&D, Acquisition of existing knowledge from other enterprises or organizations, and Acquisition of machinery, equipment, software, and buildings, in the survey cited. The performance selected was firm growth, measured through variations in the staff from 2010 to 2012, information available in Section 12.2 of CIS-2012.

Table 1 contains the description and scale of research variables according to the CIS 2012 definition. Given that a firm may carry out different exploitation and exploration activities, the combination of the scales establishes a range of values (0,3), with 0 representing the absence of the activity and 3 representing the maximum level possible for the activity, in both technological exploration and technological exploitation. The combination (0,0) means that the firm carries out neither technological exploration nor technological exploitation, the combination (0,1) means the absence of exploration with a minimum of exploitation (e.g., only conducting Acquisition machinery), whereas the combination (1,2) means that the firm explores minimally, for example through In-house R&D, at a low level, in addition to carrying out External R&D and Acquisition machinery.

Methods

Value at Risk (VaR)

The evaluation of risk of a magnitude whose value implies a degree of uncertainty (represented by a random distribution) can be achieved through the calculation of Value at Risk (VaR) of said magnitude. The VaR of a random distribution consists of considering not the expected scenario but a worse one, with the premise that said “pessimistic” scenario has a reasonable expectation of occurring. The value obtained in the pessimistic scenario would be the evaluation of the uncertain magnitude. Among the various ways of constructing VaR for a magnitude of uncertainty, it is possible to use the expected value and degree of dispersion, in our case standard deviation, in the following manner:

The VaR we have calculated is literally the expected value minus a “penalization” that depends on the amount of uncertainty (σ) and the intensity (k) we wish to reflect in the expression “worse than expected”. The value of parameter k shows the degree of pessimism or risk aversion of the decision-maker who will evaluate risk using VaR. At k = 0, no pessimism exists, and the evaluation is simply the expected value, without considering the level of uncertainty (represented by the standard deviation). As k increases, we diverge from the mean, contemplating a greater degree of uncertainty. In any given continual distribution, each k is associated clearly with a particular quantile or probability of the magnitude exceeding said VaR. For example, Gaussian distribution, with values k = 0, 0.5, 1, and 1.5, would imply quantiles of 50%, 30.9%, 15.9%, and 6.7%, with probabilities equal to 50%, 69.1%, 84.1% and 93.3% of being exceeded by the magnitude. For this study, we have chosen k = 0.67 for several reasons. Firstly, in a Gaussian distribution, in which the magnitude of growth analyzed in the study follows very closely, the VaR obtained coincides with the first quartile (Q1), one of the quartiles most frequently used to represent moderately small values for a variable. Additionally, the term 0.67σ, denominated “probable error,” is widely used in physical sciences to represent intervals of reasonable variation for experimentally measured magnitudes. In this case, the VaR proposed is the expected value minus the probable error. The value k = 0.67 is not a critical value in the sense that a different choice would have implied a qualitative change to the results obtained, as is analyzed in the Appendix.

Testing of Hypothesis 1

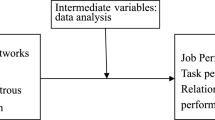

The following approach was used to analyze hypothesis 1. Given the current state (X = exploration, Y = exploitation), where X,Y ∈ {0,1,2,3}, there are two possible outcomes: (a) “Combination”: increasing the less practiced activity [min(X,Y)]. (b) “Specialization”: increasing the more practiced activity [max(X,Y)]. The first case seeks balanced effort in exploration/exploitation (e.g. after having carried out an exploitation activity, the firm conducts an exploration activity, seeking to continually compensate between the levels of both dimensions), whereas the second aims for specialization in the predominant activity, be it technological exploration or exploitation (e.g. after having carried out an exploitation activity, the firm continues to focus on this type of activity). In order to carry out the two scenarios and compare their results, it is necessary that X ≠ Y and X,Y < 3. In other words, one activity must possess predominance, with both activities capable of increasing to a greater degree. Each cell in Fig. 1 represents a combination of the level of exploitation and that of exploration. Options excluded from the selection, whether for being X = Y (main diagonal) or because X or Y was equal to 3 (last column or row in the figure), are marked in gray. The six possible current positions (X,Y) that comply with the initial premises appear in white.

Note: Each cell inthe figure represents a viable combination of exploitation and exploration levels. The arrows indicate possible movements, while infeasible options are shaded (X = Y, X,Y > 3). The combination strategy aims to maintain balance at each step, whereas the specialization strategy focuses on advancing along a single dimension.

Given that each position (X,Y) represents the “current” position of the firm in terms of strategy to devote more or fewer resources to exploitation or exploration, two options exist (“arrows” in Fig. 1) to increase the current position, through an increase in either exploitation or exploration. “Combine” represents the option of increasing the activity that is less developed in the current position, a decision that tends to even out levels of both dimensions. On the other hand, we designate as “Specialize” any increase to the activity that is already more developed, an option that augments the difference between exploration and exploitation. For example, if the current position were (X = 2, Y = 1), which is to say, higher levels of exploration than exploitation, both options would mean passing to (2,2) or to (3,1). In the first case, the tendency is to balance both activities (Combine more exploration and exploitation), whereas the second case implies focusing more on exploration (Specialization in exploration).

In the null hypothesis, the probability π of it being better to select the option Combine is 0.5. In other words, Combine and Specialize are equally valid alternatives as the best option in each stage of the trajectory. On the contrary, hypothesis 1 proposes the unilateral alternative that probability π is positive, meaning that the effect of Combine is better than Specialize at all times. In the null hypothesis, each one of the 6 valid positions indicated in the scheme is a dichotomous variable, with one signifying that it is better to Combine and 0 that it is better to Specialize:

If the null hypothesis proves true, the sum of these six variables will yield a Binomial distribution, in the following manner:

The hypothesis test is carried out comparing the estimator ν* = “number of times in which it was better to combine” with distribution ν in the null hypothesis for each of the six possibilities highlighted as possible in the scheme.

Testing of hypotheses 2 and 3

In hypotheses 2 and 3, the coefficient of correlation r was used as an estimator of population correlation. To calculate the p-value, an approximation was made using Fisher’s ζ, which is a transformation of the correlation coefficient through the arctanh (inverse hyperbolic tangent):

According to Fisher, the distribution of the sampling correlation coefficient r is

Firm growth variable

The original “firm growth” variable (annual growth rate of the firm’s staff, CIS-2012) underwent a process of transformation in order to avoid problems associated with values abnormally higher or lower than the majority. This high kurtosis causes increased errors in the estimation of correlations and population parameters in general, due to the excessive weight of outlying values in the estimation process. The transformation process was designed such that (1) the resulting variable has a distribution very close to the Gaussian distribution, and (2) the variable is highly similar to the original variable for “growth”, situated between –10% and +10% in most firms. The empirical study exclusively uses the transformed variable. The transformation of variable G (growth) consists of three steps:

-

i.

In variable G, growth lower than –0.9 (loss of 90% of staff) or >9 (staff 10 times larger than in the previous year) is winsorized. In other words, values lesser than –0.9 and >9 become equal to –0.9 and 9, respectively. Thus, we obtain a modified G.

-

ii.

The values of G are modified through a logarithm using the transformation:

$$G\longrightarrow {\mathrm{ln}}(1+G)$$ -

iii.

The resulting values undergo the following transformation, which is a generalization of the Box–Cox transformation:

This is an odd transformation that is close to the identity in a range around zero. Thus, for growth values in the usual range (between –10% and +10%), the transformed variable behaves in a similar manner to the original growth variable. The thresholds of the winsorization were chosen through observation of the values of growth collected in the sample. Basically, values considered statistically to be outliers (according to their z-value) and having a very exceptional significance in the habitual growth of firms (such as reducing the staff to less than a tenth in one year or increasing it to ten times the original number in one year) were removed.

Results

Table 2 shows the percentage of expected growth for each combination of technological exploration (rows) and technological exploitation (columns), with values ranging from 0.75% of expected firm growth, where the firm neither exploits nor explores technological knowledge (0,0), to expected growth of 3,69% (2,3). In business practice, combining technological activities means pursuing both exploration and exploitation simultaneously, while specializing refers to focusing on one over the other, with the balance being the combination associated with the greatest expected growth. The results obtained allow us to zero in on the optimum technological trajectory toward balance [(0,0), (0,1), (1,1), (1,2), (2,2), (2,3)], which occurs with medium levels of technological exploration and high levels of technological exploitation (2,3) on the scale (0–3) that measures the level of each activity (0 not carried out, 1 low level, 2 midlevel, and 3 high level). There are other feasible paths to achieving balance, but they are also less efficient in terms of expected firm growth, revealing the existence of an optimum technological trajectory toward balance starting from an initial situation of no exploration or exploitation in the firm.

Table 3 provides the values of spread (SD) of expected growth. The dispersion indicates the amount of uncertainty in the growth of firms exhibiting a particular strategical position (exploration, exploitation). In other words, it shows variability or sensibility in the growth, around the expected growth that these firms experience when diverse future events occur.

Table 4 provides the Value at Risk (VaR) of growth, combining expected growth and spread (SD) in Chebyshev’s interval k = −0.67 (Q1). The results in this table (cij) are obtained by combining the values of Table 2 (aij) and Table 3 (bij) in the following manner:

The results confirm the optimum technological trajectory [(0,0), (0,1), (1,1), (1,2), (2,2), (2,3)] and the optimal combination or balance (2,3) yielding the greatest VaR of growth (−3.23%) in the context of this study. As the VaR used coincides with quartile 1 (Q1) in this variable, which has a very close Gaussian distribution, this implies that, in 75% of cases, firm growth will not dip below 3.23% of its expected value (Table 4). On the other hand, when the firm neither explores nor exploits, growth will not decrease by more than 8.01%. The results show a gradual reduction of risk in firm growth when levels of exploration and exploitation are increased, especially through the optimum technological trajectory toward balance, as is represented in Table 4. There is a clear strategic incentive for the firm to combine growing levels of exploration and exploitation until reaching a balance between both dimensions (2,3). Increasing exploration beyond said optimal combination only generates greater risk in firm growth (3,3). Thus, finding the balance between exploration and exploitation is a strategic goal for firms.

To demonstrate that this increase in VaR (guaranteed 75% growth in Q1) does not occur randomly, the following null hypothesis is proposed: (1) given a higher level of exploitation than exploration, marginal increments in exploration carry a negative or null relationship over VaR of growth, and (2) given a higher level of exploration than exploitation, increments in exploration carry a negative or null relationship over VaR of growth. The rejection of this compound hypothesis will demonstrate that, at a given level of exploitation or exploration, increments in the other activity favor VaR of firm growth.

The estimator ν* = “number of times at which it has been better to Combine”, receives, in our case, the value ν* = 6, since on 6 occasions, it was better to “Combine” than to “Specialize”. The unilateral p-value of this amount is

Thus, the null hypothesis is ruled out and the unilateral hypothesis represented in H1 is accepted. Moreover, these results show that for firm growth, it has always been preferable to combine technological activities rather than to specialize, clearly revealing the existence of a relation of positive reinforcement between technological exploration and exploitation that favors VaR of growth. Acceptance of H1 implies that the Combine strategy is better than Specialize in most cases and highlights the importance of cultivating ambidexterity in order to employ this strategy. Table 4 shows the increase in VAR and the consequent reduction in risk in growth when combining activities, especially when this combination is achieved through what we denominate the optimum technological trajectory.

The combinations between technological exploration (Y) and exploitation (X) may be represented analytically in the following manner, with p denoting the proportion of exploiting activity and 1–p the proportion of exploratory activity:

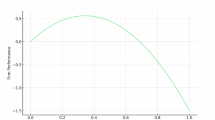

Figure 2 graphically illustrates the intensity of the relationship between said combinations of technological behavior and expected firm growth. The horizontal scale includes values for p, with 0 representing the option of only conducting technological exploration and 1 that of exclusively conducting technological exploitation. The vertical scale represents the correlation between expected growth and technological behavior. The coefficient r = 0.638, obtained in the maximum of Fig. 2, indicates a strong positive correlation between technological behavior (exploration–exploitation combination) and expected growth, with balance occurring at 49.5% technological exploration and 50.5% technological exploitation. The distribution represented in Fig. 2 allows us to observe similar benefits in combinations near 50%. As combinations diverge from this point, the positive effect on expected growth diminishes significantly. From a business viewpoint, this result means firms should aim in equal measure for exploitation and exploration. In other words, they should integrate both dimensions equally into their strategic planning. From a practical point of view, it means that they should invest in the exploration of new technologies to innovate while simultaneously using their technological capacities and refining their processes to maximize efficiency.

Note: The horizontal scale represents p values (0 for pure exploration, 1 for pure exploitation). The vertical scale indicates the correlation between expected growth and the exploitation/exploration balance (technological behavior). As the balance deviates from 50%, the positive impact on expected growth significantly diminishes.

The null hypothesis of Test 2 states that population correlation ρ is zero. Conversely, the hypothesis to be demonstrated states that said correlation is positive and is greatest when p = 0.5. The unilateral p-value corresponding to the maximum correlation of 0.638 in the sample is 0.003. This result implies the acceptance that population correlation is positive in the best exploitation–exploration combination and that maximum expected growth occurs with the same effort in technological exploration and exploitation, thus demonstrating Hypothesis 2.

Figure 3 shows the correlation between the combination of technological exploration and exploitation (technological behavior) and uncertainty of growth. In the abscissa axis, values for p are shown, with value 0 once more representing only technological exploration and value 1 only technological exploitation in firms, whereas the ordinate axis represents values for the uncertainty of growth. The coefficient of correlation between technological behavior and uncertainty of growth is r = −0.731. This strong negative correlation indicates that the higher the component of exploitation in technological behavior, the lower the uncertainty of firm growth (Fig. 3) will be. In other words, the uncertainty of growth rises with a proportion of exploration and diminishes when the proportion of exploitation in technological behavior increases, up to 80–90%, where the maximum negative correlation occurs, as can be observed in Fig. 3.

Note: The horizontal scale encompasses p values (0 representing pure exploration, 1 representing pure exploitation). A strong negative correlation is observed: growth uncertainty increases with higher levels of exploration and decreases as exploitation intensifies (up to 80–90%).

The null hypothesis of Test 3 is that the population correlation ρ is 0. The hypothesis to be demonstrated is that said correlation is negative and reaches its minimum (most negative) point when p is near to 1. The unilateral p-value corresponding to the minimum correlation –0.731 in the sample is 0.0004. Thus, it is demonstrated that population correlation is negative in the best exploitation-exploration combination and that achieving a balance that minimizes uncertainty in firm growth implies making nearly exclusive efforts in technological exploitation. Thus, Hypothesis 3 is demonstrated.

In addition, the relationship between technological behavior and VaR of growth was analyzed depending on the decision-maker’s level of risk-taking in the technological exploration-exploitation balance. Table 5 shows the results obtained with varying values for k and Fig. 4 represents the evolution of technological balance. With increasing k, or a greater aversion to risk (more pessimistic VaR), the optimum distribution begins to shift from equal effort in exploitation and exploration to dedicating nearly all efforts to exploitation.

Note: There is no single optimal combination of exploration and exploitation under uncertainty, as it depends on the decision-maker’s risk preference. k values of 0.25, 0.52, 0.67, 0.84, and 1.28 were selected to correspond to the 40%, 30%, 25% (Q1), 20%, and 10% percentiles, respectively, of a Gaussian distribution. The riskiest behavior involves ignoring uncertainty (k = 0), with a balance around 50% exploration and 50% exploitation. The most cautious behavior focuses solely on uncertainty, relegating expected growth (k = ∞), with the balance around 85% exploitation and 15% exploration. The most common risk behavior corresponds to the first quartile (k = 0.67), with the balance around 37% exploration and 63% exploitation.

Figure 4 shows the correlations between different technological behaviors (different values of parameter p) and firm growth. Different attitudes toward uncertainty were contemplated (Fig. 4), from k = 0.25 (little aversion to risk, granting more importance to the expected value and less importance to possible deviation from the expected), to k = 1.28 (high aversion to risk, granting great importance to possible deviation from the expected). The values for k: 0.25, 0.52, 0.67, 0.84, and 1.28, were chosen to coincide with percentiles 40%, 30%, 25% (Q1), 20%,10%, respectively, with a Gaussian distribution like the one we are analyzing. The optimum correlation occurs with a different exploitation–exploration combination according to the decision-maker’s risk-taking.

The k values correspond to the attitude toward risk in the context of technological exploration and exploitation. These values are associated with VaR, which indicates firm growth, in the case that unfavorable events arise. The level of severity of said events is associated with k. Accordingly, a high k value reflects consideration of unlikely events, and a low value indicates the consideration of relatively probably unfavorable events. From the standpoint of business practice, a high k value, for example, k = 1.28, reflects a conservative attitude toward risk, where firms prioritize strategies with less variability of expected growth. On the other end of the spectrum, a low k value, for example, k = 0.25, represents a more tolerant attitude toward risk that allows for the adoption of strategies with higher uncertainty but with greater potential for expected growth for the firm. The most balanced attitude corresponds in the graph to the value k = 0.67. This value reflects an intermediate position between the most conservative stance and the stance most tolerant of risk in expected growth. As conservatism increases, the balance shifts to the right of the abscissa axis, which is to say that the exploration level falls as the exploitation level rises. In our case, the most conservative or risk-averse strategy would be the combination of 14.8% exploration and 85.2% exploitation, according to the results in Table 5.

Discussion

The balance between technological exploration and exploitation is a crucial topic in the study of organizational ambidexterity. This paper seeks to more deeply comprehend the existing relationship between both sources of technological knowledge in firms and determine their ideal combination or technological balance in conditions of uncertainty. This type of empirical analysis, new to the area being studied, aims to promote the advancement of knowledge of balance and ambidexterity in the context of habitual risk in business decision-making.

About the technological exploration–exploitation relationship in conditions of uncertainty

The results of this study show an optimal technological exploration–exploitation mix, revealing a sequence of efficient combinations that foments technological potential, maximizing firm growth. The optimal technological trajectory is based on a relationship of positive reinforcement between technological exploration and exploitation that favors VaR of firm growth (H1), demonstrating at each step that the combination of both technological activities is generally preferable to specialization in one of them. The results reveal alternative itineraries or feasible options (Gibson and Birkinshaw, 2004; Lavie et al. 2010), albeit less efficient as regards to VaR of growth (Table 4). In our case, the optimal trajectory consists of a sequence of combinations (0,1), (1,1), (1,2), (2,2), and (2,3) which leads to balance in most cases, reconciling a medium-high level of exploration with a high level of exploitation (2,3), measured on a 0–3 scale of technological exploration–exploitation levels. Given the premise of a firm that neither explores nor exploits technologically or combination (0,0), the first step in developing technological potential would be to achieve a low level of technological exploitation or combination (0,1). Experience using the technology newly acquired in the technological market would ease the development of internal competencies and a basic level of technological exploration in a second step, or combination (1,1). This first transition appears consistent with the model of human techno-perception, which shows the transition between instrumentality and the pursuit of efficiency or exploitation toward exploration (Ahmedien, 2024). Any other combination starting at (0,1) yields poorer results in VaR of growth (Table 4). The successive combinations of optimal trajectory follow the same pattern: first, the level of technological exploitation increases, and subsequently, the level of technological exploration follows suit, improving performance at each step up to the greatest VaR of growth with the optimal combination of exploration and exploitation, which we call technological balance (Table 4).

The results of this study showcase the relevance of exploiting activity, in contrast with the secondary role other research has assigned to it (Fang and Levinthal, 2009). Light is likewise shed on the synergetic effect between exploration and exploitation (Geerts et al. 2018) and, consequently, the need to harmonize technological acquisition in the market with the development of internal technological capacity in most firms. Technological exploration and exploitation prove to be independent activities, not pitted against each other (Riviezzo et al. 2015) but rather complementary (Fourné et al. 2019), related in an interactive manner (Cao et al. 2009; Snehvrat et al. 2018), with better performances resulting from balance than from the imbalance between the two activities (Petruzzelli, 2014; Wang et al. 2017) or specialization in one of them (Geerts et al. 2018; Wei et al. 2014; Zhang et al. 2017). The results align with those of other studies that identify ambidexterity with the achievement of similar proportions of exploration and exploitation (He and Wong, 2004) and associate balance with medium levels of exploration and high levels of exploitation (Sirén et al. 2012).

On the determination of technological balance and the effect of uncertainty

The results reveal that developing technological potential is essential to the strength and survival of the European firm. The strong positive relationship of technological behavior with expected growth (R = 0.638) and the same variable’s strongly negative relationship with an uncertainty of growth (R = −0.731) show the relevance of technological level in a firm’s mid- and long-term success. This technological behavior requires a combination of technological exploration and exploitation, thus corroborating the value of technological ambidexterity in the growth of staff (Andriopoulos and Lewis, 2009; Patel et al. 2013) and, in general, its relationship with performances (Lavie et al. 2010; Raisch and Birkinshaw, 2008).

The increase in technological behavior oriented toward exploitation moderately and insignificantly affects the firm’s certainty of growth. However, the different feasible combinations do not exert the same effect on performance, with only the optimum combination of both activities showing the capacity to maximize firm growth. Technological balance without uncertainty is the combination associated with the greatest expected firm growth, specifically 49.5% in exploration and 50.5% in exploitation, and in general, the set of combinations near 50%, as can be observed in Fig. 2. This finding indicates that expected growth is more related with a 50% combination of exploitation (H2) than with other mixes, though existing studies suggest that this combination might not be ideal (Gupta et al. 2006; Rojas-Córdova et al. 2023). However, the proportion of technological exploitation and exploration that minimizes uncertainty of firm growth is the development of technological exploitation (H3).

This study proposes the novelty of analysis under uncertainty, with technological balance as the current technological exploration–exploitation mix that shows the greatest VaR of firm growth. Obviously, technological balance will now vary according to the level of risk-taking, quantified in parameter k of the Chebyshev interval. Table 5 shows results obtained for different values of k. When k = 0 (quantile 50%), risk-taking reaches its maximum level, implying the full acceptance of risk, which situates technological balance at 49.5% exploration and 50.5% exploitation. The opposite extreme is the absolute rejection of risk by the decision-maker, which implies that k = ∞ (quantile 0%), achieving technological balance with a combination of 14.8% exploration and 85.2% exploitation. The first quantile may represent a reasonable attitude toward risk for most decision-makers, representing the mid-point among the values below the median value. In this case, k = 0.67, and technological balance is reached at 37% exploration and 63% exploitation. In this manner, conservative technological behavior in regard to VaR of firm growth would place technological balance near 2/3 exploitation and 1/3 exploration, in the context of our research.

Conclusions

This paper contributes to the study of technological ambidexterity with an analysis under uncertainty of the exploitation–exploration relationship, technological balance, and their impact on firm growth. Likewise, the results obtained reveal the positive influence of developing organizations’ technological potential on strength and mid- and long-term survival within the European business sector. The main findings obtained can be synthesized in the following manner:

First, technological balance’s favorable effect on VaR of firm growth is revealed, an effect that occurs regardless of an organization’s level of risk-taking. An increase in technological behavior toward balance, raising levels of exploration and exploitation, benefits VaR of firm growth. Moreover, the results indicate the existence of alternative itineraries leading to technological balance and an optimum trajectory or sequence of exploration–exploitation mixes that gradually foster technological potential and efficiently achieve greater expected firm growth. The path established is a succession of efficient combinations leading to growth with minimum risk, demonstrating that planned alternation between both sources of technology is preferable for most firms to exclusive specialization in one technological dimension. Technological exploitation plays a noteworthy role in this process, both at the start of the trajectory and at each step of the sequence toward technological balance, revealing the importance of SMEs’ access to technological markets in order to develop their technological potential.

Secondly, a relationship of positive reinforcement exists between technological exploration and exploitation in firms, especially SMEs. Exploration and exploitation emerge as independent and complementary technological activities, whose synergetic effects benefit the performance analyzed. The results suggest that efforts made in exploitation are associated with the generation of technological exploration, and vice versa. This virtuous cycle implies a substrate of technological exploitation in technological exploration and a base of technological exploration supporting firms’ technological exploitation. These aspects bear weight in the management of learning and knowledge at the organizational level.

Thirdly, there is no single optimum combination of exploration and exploitation in conditions of uncertainty. In fact, a continuum of optimal combinations can be identified depending on the importance accorded by the decision-maker to reducing uncertainty in relation to the value of expected growth. Thus, the riskiest behavior for a decision-maker would consist of ignoring uncertainty and choosing the option associated with the greatest expected value (k = 0), in which case technological balance would be around 50% technological exploitation and exploration in our research context. The opposite extreme would be conducted exclusively preoccupied with the level of uncertainty, relegating expected growth (k = ∞) to a back seat, in which case technological balance would occur around 85% technological exploitation and 15% technological exploration. Both of these extreme strategies are difficult for firms to adopt. A more reasonable technological behavior would situate the firm at the midpoint of the continuum, determining the optimum combination through Value at Risk (VaR). The decision-maker's risk-taking determines, in the end, the best exploration–exploitation combination that provides the greatest future growth without compromising the firms’ basic safety. Thus, the common standpoint in regard to risk would probably situate the decision-maker in the first quartile (k = 0.67), in which case technological balance would occur at 37% exploration and 63% exploitation, in the context of this research. In general terms, more exploitation implies less uncertainty (σ) in growth (Table 3) and thus a reduced probability of lower than expected growth (µ). Accordingly, a decision maker especially concerned with a drop in firm growth would prefer to reinforce exploitation activity, as it produces less variability or sensitivity in growth. However, a decision maker who, rather than dwelling on the most negative scenarios, focuses only on the most probable negative scenarios would choose the most balanced combination of exploration and exploitation, given that these combinations yield a higher expected growth than solely conducting exploitation (Table 2).

Fourthly, technological ambidexterity is crucial to the efficient management of technological balance in firms. Technological behavior is the combination of exploration and exploitation activities according to the needs and circumstances that arise. The capacity to combine both activities opportunely and efficiently in the heart of the firm is vital to its adaptation to a dynamic competitive and technological context. The results of this research corroborate the positive influence of technological ambidexterity on growth and thus, on the mid- and long-term strength and survival of most firms. Likewise, our results align with those of existing studies that highlight the positive effect of ambidexterity on performances and identify this organizational capacity with similar levels of exploration and exploitation in the firm, without considering uncertainty. In this sense, our results showcase the benefits for most firms of balancing both types of technological activities rather than disproportionately specializing in one or the other.

Implications for theory and policy

This study clearly reveals the positive correlation between exploitation and exploration, the existence of different feasible trajectories between both dimensions, and the existence of an efficient path and an optimum combination in regard to firm growth. The efficient trajectory shows that any progress achieved in a technological dimension improves with a parallel, additional effort in the other dimension, indicating that it is generally preferable to accumulate efforts rather than delving into only one area, or to balance rather than to specialize. Technological advancement emerges in the context of our research as the fruit of symbiosis between two separate but interdependent and non-substitutable forces, supporting the combination perspective (Junni et al. 2013). The study likewise highlights the value of technological management on a micro level in the survival and development of the business system in the context of Europe’s economic recovery. Additionally, the technological trajectory of firms demonstrates that exploitation leads to exploration and vice-versa, with intertwining resources and shared experiences in the processes of learning and knowledge management in organizations.

The findings of this study could be useful to policymakers. Technological ambidexterity could facilitate European projects in the modernization and technological transformation of firms, especially SMEs. This organizational capacity could facilitate the spread and assimilation of external knowledge and the development of internal knowledge, aiding in firms’ adaptation to new technological contexts. The benefits of ambidexterity have been revealed in regard to growth and survival in contexts of crisis or uncertainty. Likewise, the research results demonstrate the positive reinforcement between technological exploration and exploitation in terms of firm growth. Thus, institutional support of firms’ technological ambidexterity could contribute to alleviating unemployment generated in sectors’ technological transformation, though the benefits of proximity and opportunities in the environment are strong conditioning factors in exploitation-exploration synergies and technological ambidexterity at a firm level (Geerts et al. 2018; Ossenbrink et al. 2019).

Limitations and new lines of research

This research suffers certain limitations in conditioning the empirical study. One such limitation is the use of Levinthal and March’s criteria (1991) to classify exploration and exploitation activities at a firm level, a factor that may affect empirical results. The selection of performance is another conceptual limitation of the study, as our analysis focused exclusively on firm growth. Likewise, the data used was derived exclusively from the official European statistical source.

The choice of any methodology of analysis inevitably implies certain limitations. Such is the case of the fundamentally qualitative approach employed in this study. Other focuses of a qualitative nature could also contribute significantly to the comprehension of dynamic aspects of balance between exploitation and exploration (Simsek et al. 2009). An especially noteworthy and novel area of inquiry is the study of the relationships or symbiosis between humans and technology. Interdisciplinary research on this subject could shed light on the complex relationships and fluctuations between exploration and exploitation. In the analysis of this phenomenon, it would be of interest to include diverse and non-convergent perspectives (see, e.g., Ahmedien, 2024; Tuuri and Koskela, 2020) that offer greater comprehension of the dynamics of organizational ambidexterity and its evolution in a highly complex technological setting marked by the sudden and dramatic entrance of AI.

This study could serve as a springboard for other potential lines of research. Firstly, it would be of interest to apply the study methodology in different areas, including the analysis of other business performances, such as profitability, innovation, patents, and market value of the firm, or constructs of these and other similar variables. The study could also be replicated in different time periods, under different socioeconomic circumstances, on a national and regional scale, by sectors, and by organizational size. Likewise, the methodology incorporating risk analysis could facilitate a deeper understanding of the relationship between technological behavior and VaR of performances and the role played by individual decision-makers’ risk-taking in ambidexterity and the balance between exploration and exploitation in firms. Finally, the consideration of uncertainty opens promising pathways to analyzing more realistically the complex phenomenon of organizational ambidexterity and decision-making in firms.

Data availability

The data that support the findings of this study are available on the secure platform S-CIRCABC of Eurostat, European Commission (EU) but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are, however, available from the authors upon reasonable request and with permission of EUROSTAT European Commission.

References

Ahmedien DA (2024) A drop of light: an interactive new media art investigation of human–technology symbiosis. Humanit Soc Sci Commun 11:1–20. https://doi.org/10.1057/s41599-024-03206-y

Andriopoulos C, Lewis MW (2009) Exploitation–exploration tensions and organizational ambidexterity: managing paradoxes of innovation. Organ Sci 20(4):696–717. https://doi.org/10.1287/orsc.1080.0406

Audretsch DB, Guerrero M (2023) Is ambidexterity the missing link between entrepreneurship, management, and innovation? J Technol Transf 48(6):1891–1918. https://doi.org/10.1007/s10961-023-10037-7

Cao Q, Gedajlovic E, Zhang H (2009) Unpacking organizational ambidexterity: dimensions, contingencies, and synergistic effects. Organ Sci 20(4):781–796. https://doi.org/10.1287/orsc.1090.0428

Carmeli A, Halevi MY (2009) How top management team behavioral integration and behavioral complexity enable organizational ambidexterity: the moderating role of contextual ambidexterity. Leadersh Q 20(2):207–218. https://doi.org/10.1016/j.leaqua.2009.01.011

Chen RR (2023) Global financial risk management—a quantitative guide. Fordham University

Dean BP (2022) Antecedents enabling team ambidexterity: moving beyond mere microfoundation. Int J Product Perform Manag 71(6):2432–2458. https://doi.org/10.1108/IJPPM-01-2021-0003

Derbyshire J (2014) The impact of ambidexterity on enterprise performance: evidence from 15 countries and 14 sectors. Technovation 34(10):574–581. https://doi.org/10.1016/j.technovation.2014.05.010

Fang C, Levinthal C (2009) Near-term liability of exploitation: exploration and exploitation in multistage problems. Organ Sci 20(3):538–555. https://doi.org/10.1287/orsc.1080.0376

Feng T, Si Z, Jiang W, Jiang W, Tan J (2024) Supply chain transformational leadership and resilience: the mediating role of ambidextrous business model. Humanit Soc Sci Commun 11:628. https://doi.org/10.1057/s41599-024-03099-x

Fourné SPL, Rosenbusch N, Heyden MLM, Jansen JJP (2019) Structural and contextual approaches to ambidexterity: a meta-analysis of organizational and environmental contingencies. Eur Manag J 37(5):564–576. https://doi.org/10.1016/j.emj.2019.04.002

Geerts A, Leten B, Belderbos R, Van Looy B (2018) Does spatial ambidexterity pay off? On the benefits of geographic proximity between technology exploitation and exploration. J Prod Innov Manag 35(2):151–163. https://doi.org/10.1111/jpim.12380

Gibson CB, Birkinshaw J (2004) The antecedents, consequences, and mediating role of organizational ambidexterity. Acad Manag J 47(2):209–226. https://doi.org/10.5465/20159573

Gupta AK, Smith KC, Shalley CE (2006) The interplay between exploration and exploitation. Acad Manag J 49(4):693–706. https://doi.org/10.5465/amj.2006.22083026

He ZL, Wong PK (2004) Exploration vs. exploitation: an empirical test of the ambidexterity hypothesis. Organ Sci 15(4):481–494. https://doi.org/10.1287/orsc.1040.0078

Hill SA, Birkinshaw J (2014) Ambidexterity and survival in corporate venture units. J Manag 40(7):1899–1931. https://doi.org/10.1177/0149206312445925

Hsu CW, Lien YC, Chen H (2013) International ambidexterity and firm performance in small emerging economies. J World Bus 48(1):58–67. https://doi.org/10.1016/j.jwb.2012.06.007

Johnson G, Whittington R, Scholes K, Angwin D, Regnér P (2014) Exploring strategy: text and cases. Pearson Education Limited

Junni P, Sarala RM, Taras V, Tarba SY (2013) Organizational ambidexterity and performance: a meta-analysis. Acad Manag Perspect 27(4):299–312. https://doi.org/10.5465/amp.2012.0015

Kim G, Huh MG (2015) Exploration and organizational longevity: the moderating role of strategy and environment. Asia Pac J Manag 32(2):389–414. https://doi.org/10.1007/s10490-014-9399-3

Koryak O, Lockett A, Hayton J, Nicolaou N, Mole K (2018) Disentangling the antecedents of ambidexterity: exploration and exploitation. Res Policy 47(2):413–427. https://doi.org/10.1016/j.respol.2017.12.003

Laureiro-Martínez D, Brusoni S, Canessa N, Zollo M (2015) Understanding the exploration–exploitation dilemma: an FMRI study of attention control and decision-making performance. Strateg Manag J 36(3):319–338. https://doi.org/10.1002/smj.2221

Lavie D, Kang J, Rosenkopf L (2011) Balance within and across domains: the performance implications of exploration and exploitation in alliances. Organ Sci 22(6):1517–1538. https://doi.org/10.1287/orsc.1100.0596

Lavie D, Rosenkopf L (2006) Balancing exploration and exploitation in alliance formation. Acad Manag J 49(4):797–818. https://doi.org/10.5465/AMJ.2006.22083085

Lavie D, Stettner U, Tushman ML (2010) Exploration and exploitation within and across organizations. Acad Manag Ann 4(1):109–155. https://doi.org/10.1080/19416521003691287

Lennerts S, Schulze A, Tomczak T (2020) The asymmetric effects of exploitation and exploration on radical and incremental innovation performance: an uneven affair. Eur Manag J 38(1):121–134. https://doi.org/10.1016/j.emj.2019.06.002

Levinthal DA, March JG (1993) The myopia of learning. Strateg Manag J 14(S2):95–112. https://doi.org/10.1002/smj.4250141009

Lin LH, Ho Y (2021) Ambidextrous governance and alliance performance under dynamic environments: an empirical investigation of Taiwanese technology. Technovation 103:1–12. https://doi.org/10.1016/j.technovation.2021.102240

Luger J, Raisch S, Schimmer M (2018) Dynamic balancing of exploration and exploitation: the contingent benefits of ambidexterity. Organ Sci 29(3):449–470. https://doi.org/10.1287/orsc.2017.1189

March JG (1991) Exploration and exploitation in organizational learning. Organ Sci 2(1):71–87. https://doi.org/10.1287/orsc.2.1.71.0

McNeil A, Frey R, Embrechts P (2005) Quantitative risk management: concepts techniques and tools. Princeton University Press

Mura M, Micheli P, Longo M (2021) The effects of performance measurement system uses on organizational ambidexterity and firm performance. Int J Oper Prod Manag 41(13):127–151. https://doi.org/10.1108/IJOPM-02-2021-0101

O´Reilly CA, Tushman M (2013) Organizational ambidexterity: past, present and future. Acad Manag Perspect 27(4):324–338. https://doi.org/10.5465/amp.2013.0025

Ossenbrink J, Hoppmann J, Hoffmann VH (2019) Hybrid ambidexterity: how the environment shapes Incumbents’ use of structural and contextual approaches. Organ Sci 30(6):1319–1348. https://doi.org/10.1287/orsc.2019.1286

Patel PC, Messersmith JG, Lepak DP (2013) Walking the tightrope: an assessment of the relationship between high-performance work systems and organizational ambidexterity. Acad Manag J 56(5):1420–1442. https://doi.org/10.5465/amj.2011.0255

Petruzzelli AM (2014) Balancing knowledge exploration and exploitation within and across technological and geographical domains. Knowl Manag Res Pract 12(2):123–132. https://doi.org/10.1057/kmrp.2012.46

Phene A, Tallman S, Almeida P (2012) When do acquisitions facilitate technological exploration and exploitation? J Manag 38(3):753–783. https://doi.org/10.1177/0149206310369939

Raisch S, Birkinshaw J (2008) Organizational ambidexterity: antecedents, outcomes, and moderators. J Manag 34(3):375–409. https://doi.org/10.1177/0149206308316058

Raisch S, Birkinshaw J, Probst G, Tushman ML (2009) Organizational ambidexterity: balancing exploitation and exploration for sustained performance. Organ Sci 20(4):685–695. https://doi.org/10.1287/orsc.1090.0428

Riviezzo A, Garofano A, Napolitano MR, Marino V (2015) Moving forward or running to standstill? Exploring the nature and the role of family firms’ strategic orientation. J Fam Bus Strategy 6(3):190–205. https://doi.org/10.1016/j.jfbs.2015.06.001

Rojas-Córdova C, Williamson AJ, Pertuze JA, Calvo G (2023) Why one strategy does not fit all: a systematic review on exploration–exploitation in different organizational archetypes. Rev Manag Sci 17(7):2251–2295. https://doi.org/10.1007/s11846-022-00577-x

Roth L, Corsi S (2023) Ambidexterity in a geographic context: a systematic literature review on international exploration and exploitation of knowledge. Technovation 124:102744. https://doi.org/10.1016/j.technovation.2023.102744

Rothaermel FR, Alexandre MT (2009) Ambidexterity in technology sourcing: the moderating role of absorptive capacity. Organ Sci 20(4):759–780. https://doi.org/10.1287/orsc.1080.0404

Seo E, Song J, Jin C (2023) Heterogeneity of optimal balance between exploration and exploitation: the moderating roles of firm technological capability and industry alliance network position. Ind Innov 30(4):423–451. https://doi.org/10.1080/13662716.2022.2036598

Simsek Z, Heavey C, Veiga JF, Souder D (2009) A typology for aligning organizational ambidexterity’s conceptualizations, antecedents, and outcomes. J Manag Stud 46(5):864–894. https://doi.org/10.1111/j.1467-6486.2009.00841.x

Sirén C, Kohtamaki M, Kuckertz A (2012) Exploration and exploitation strategies, profit performance, and the mediating role of strategic learning escaping the exploitation trap. Strateg Entrep J 6(1):18–41. https://doi.org/10.1002/sej.1126

Snehvrat S, Kumar A, Kumar R, Dutta S (2018) The state of ambidexterity research: a data mining approach. Int J Organ Anal 26(2):343–367. https://doi.org/10.1108/IJOA-06-2017-1182

Stettner U, Lavie D (2014) Ambidexterity under scrutiny: exploration and exploitation via internal organization, alliances, and acquisitions. Strateg Manag J 35(13):1903–1929. https://doi.org/10.1002/smj.2195

Stieglitz N, Knudsen T, Becker MC (2016) Adaptation and inertia in dynamic environments. Strateg Manag J 37(9):1854–1864. https://doi.org/10.1002/smj.2433

Turner N, Swart J, Maylor H (2013) Mechanisms for managing ambidexterity: a review and research agenda. Int J Manag Rev 15(3):317–332. https://doi.org/10.1111/j.1468-2370.2012.00343.x

Tuuri K, Koskela O (2020) Understanding human–technology relations within technologization and appification of musicality. Front Psychol 11:416. https://doi.org/10.3389/fpsyg.2020.00416

Uotila J, Maula M, Keil T, Zahra SA (2009) Exploration, exploitation, and financial performance: analysis of SandP 500 corporations. Strateg Manag J 30(2):221–231. https://doi.org/10.1002/smj.738

Vrontis D, Thrassou A, Santoro G, Papa A (2017) Ambidexterity, external knowledge and performance in knowledge-intensive firms. J Technol Transf 42(2):374–388. https://doi.org/10.1007/s10961-016-9502-7

Wang N, Chen B, Wang L, Ma Z, Pan S (2024) Big data analytics capability and social innovation: the mediating role of knowledge exploration and exploitation. Humanit Soc Sci Commun 11:864. https://doi.org/10.1057/s41599-024-03288-8

Wang P, Van de Vrande V, Jansen JJP (2017) Balancing exploration and exploitation in inventions: quality of inventions and team composition. Res Policy 46(10):1836–1850. https://doi.org/10.1016/j.respol.2017.09.002

Wei Z, Yi Y, Guo H (2014) Organizational learning, ambidexterity, strategic flexibility, and new product development. J Prod Innov Manag 31(4):832–847. https://doi.org/10.1111/jpim.12126

Wilden R, Hohberger J, Devinney TM, Lavie D (2018) Revisiting James March (1991): whither exploration and exploitation? Strateg Organ 16(3):352–369. https://doi.org/10.1177/1476127018765031

Wu J, Wang X, Guo B (2019) Co-evolution of exploration–exploitation strategy and weak-strong ties portfolios: a longitudinal case study. Eur Manag Rev 16:1043–1058. https://doi.org/10.1111/emre.12297

Yuan C, Xue D, He X (2021) A balancing strategy for ambidextrous learning, dynamic capabilities, and business model design, the opposite moderating effects of environmental dynamism. Technovation 103:102225. https://doi.org/10.1016/j.technovation.2021.102225

Zhang F, Wang Y, Li D, Cui V(2017) Configurations of innovations across domains: an organizational ambidexterity view J Product Innov Manag 34(6):821–841. https://doi.org/10.1111/jpim.12362

Acknowledgements

This paper has been elaborated from the project “Innovation and competitiveness in smart specialization sectors: a micro-level analysis and instruments for politics and management in Europe”, conducted under the auspices of Eurostat (European Commission) and the University of Seville, ref. RPP 369/2020-CIS-University of Seville (ES).

Author information

Authors and Affiliations

Contributions

Juan A. Martínez-Román: conceptualization, data acquisition, investigation, supervision, validation, writing-review and editing. Javier Gamero: methodology, data curation, formal analysis, and validation. Juan A. Tamayo: investigation, and validation. María de Loreto Delgado-González: data curation, and formal analysis.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

The CIS microdata have been anonymized by Eurostat and have been used in accordance with European Commission regulations for the processing and storage of official data for research purposes.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Martínez-Román, J.A., Gamero, J., Tamayo, J.A. et al. Empirical analysis of the technological exploration–exploitation balance and its impact on organizational performance under uncertainty. Humanit Soc Sci Commun 12, 221 (2025). https://doi.org/10.1057/s41599-025-04476-w

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-04476-w

This article is cited by

-

Strategic resource allocation: an agent-based model of ambidextrous strategies in the pharmaceutical industry

Cost Effectiveness and Resource Allocation (2026)