Abstract

Geopolitical tensions, port congestions and pandemic have prompted unprecedented supply chain disruptions in the recent times. China’s pivotal role as a global manufacturing and trading hub makes it susceptible to these disruptions. In this backdrop, the following study investigates the relationship between global supply chain disruptions across sectors of the Chinese stock market by employing quantile-on-quantile regression. Our results reveal a predominant negative relationship for most of the sectors. Moreover, pronounced negative effects are observed for utilities and telecom sector. Lower quantiles of GSCP have strong negative (positive) influence when the market is bearish (bullish) across sectors, except for financial sector.

Similar content being viewed by others

Introduction

Global supply chains are the arteries of global trade and are responsible for the transportation of the goods across continents. However, they are exposed to external risks which may hamper their smooth functioning. In the recent times, the world has witnessed disruptions in the global supply chain emanating from pandemic (Kovács & Falagara Sigala, 2021), natural disasters (Wei et al., 2023) and rising geopolitical tensions (Bednarski et al., 2023). Apart from that, supply chain disruptions can also result from financial crises (Jüttner & Maklan, 2011), political conflicts (Kleindorfer & Saad, 2005) and even climate change (Ghadge et al., 2020). The recent Hamas-Israel war is one such event which has not only disrupted global supply chain owing to the attacks on vessels but the shipping costs have also experienced unprecedented hikes. Russia-Ukraine war has also influenced the global supply chain.

By aggregating data on manufacturing disruptions and transportation costs the Federal Reserve Bank of New York has recently developed Global Supply Chain Pressure Index (GSCPI) which is a valuable tool for gauging the intensity of these disruptions. The tool can provide valuable insights about the impact on the economic activity by providing information about the potential bottlenecks arising from uncertainty in the global supply chains. These vulnerabilities raise concerns not only for consumers but can have extreme consequences for the businesses and investors alike. Therefore, the following study aims to provide an insight into the consequences from the global supply chain pressure (GSCP) for the investors in the Chinese stock market.

Disruptions in the supply chain environment can be consequential for different markets i.e., commodity, industrial and renewable energy market as its dynamics are multifaceted and has potential implications for policymakers and investment strategists (Gozgor et al., 2023; Hendricks & Singhal, 2005; Hu et al., 2024; Li et al., 2023; Ren et al., 2024; Zhong et al., 2024). Since the GSCPI measures the global supply chain disruptions by capturing variations in transportation cost, backlogs, delivery times and stock levels, therefore an increase in GSCPI can lead to increased costs and delays in production. Resultantly, profit margins and investor sentiment are adversely affected thereby influencing the stock market. It is further to be noted that investors should account for the risks from supply chain disruptions and therefore hedge themselves by adjusting their portfolios (Su et al., 2023). Therefore, the results from the following study will provide them further evidence at the sectoral level about the effects of disruptions in the supply chain which will enable them to better hedge and manage their risk.

The global supply chains are interconnected more than ever, driven by the accelerating pace of globalization that has reshaped economies across the world. This intensifying integration is well-documented in the literature, with early studies highlighting the increasing connectivity of supply chain systems (Vidal & Goetschalckx, 1997). The deepening of these connections has reached a point where disruptions in a single node can have far-reaching consequences for the entire network and can lead to the paralysis of the entire system (Alessandria et al., 2023). The occurrence of cascading failures in the global supply chain has led to a series of crises with far-reaching consequences for the overall economic system (Bonadio et al., 2021; Ekinci et al., 2024). These disruptions in the supply chain have a significant impact on the production and distribution of goods ultimately affecting firms and thereby financial markets. This highlights the crucial role that supply chains play in the global economy. The impacts of these phenomena vary across sectors and regions, with certain industries and economies facing more severe consequences than others. Due to the difference in the vulnerability of different sectors of the stock market on the supply chain disruptions, the sensitivity also differs across sectors. Certain businesses may face greater risks from supply chain disruptions if they heavily depend on intricate international networks. Conversely, those with limited integration into the global supply chain may experience fewer negative impacts. Consequently, a study at sectoral level can provide valuable information about the implications of pressure from supply chain disruptions across variety of sectors.

Our study contributes in the extant literature in many ways. Unlike previous research that primarily focuses on broader macroeconomic indicators at country level, our study delves into sector-specific dynamics of stock market thus providing a nuanced understanding of the impact of supply chain disruptions. It also fills the gap in the previous research which mainly focused on the trade aspects and ignored the financial implications of the disruptions in the global supply chain. Furthermore, our study addresses a critical gap by contextualizing the risks in the supply chain within the unique structural and regulatory framework of China, the world’s largest manufacturing hub and a pivotal node in global supply chain. It is a pioneer study which not only have considered the financial aspect of the global supply chain but has also discussed it in the context of Chinese economy which holds key position in the global trade arena. The Chinese economy is at the global forefront as a major exporter and is vulnerable to the pressures form the global supply chain disruptions. Therefore, it is highly important to investigate how different sectors of the economy are affected by these disruptions. To grasp the impact of global supply chain pressure across variety of sectors of the Chinese stock market, we employ quantile on quantile regression model to better understand the asymmetric relationship under different market conditions. Moreover, fewer studies have examined the impact of the Global Supply Chain Pressure Index (GSCPI) on the economy, and it is particularly challenging to find research that investigates its effects on the stock market at the sectoral level. This is particularly important given the varying sensitivity of different sectors to the external factors. The results of the study indicate a predominant negative effect of global supply chain pressure (GSCP) across most of the sectors specifically at the lower quantiles. Utilities and telecommunication sectors exhibited pronounced negative returns in response to global supply chain disruptions. This study also employs quantile on quantile methodology which provides an insight into the relationship between the variables under different conditions of the market. The methodology is also appropriate owing to the non-linear nature of the financial returns.

Rest of the paper is organized as follows: Section 2 contains the review of literature; Section 3 briefly introduces the methodology. Section 4 includes the data and its descriptive statistics. Section 5 discusses the results and discussion followed by the conclusion in section 6.

Literature Review

Supply chain disruptions are responsible for wide range of risks including but not limited to increased costs, product unavailability and poor service on firms’ behalf as these risks trigger ripple effects which affect manufacturers, suppliers and distributors (Ali et al., 2017; Chowdhury et al., 2022; Yu et al., 2019). Organizations view mitigation of risks arising from supply chain disruptions as of utmost importance and it is achieved through the management of unexpected events in the supply chain so that the normal operations of the firm can be restored (Raj et al., 2022; Tukamuhabwa et al., 2015). It is also important to note that supply chain disruptions are not limited to one industry at one time as the consequences of disruption in one industry can spread its wings to other industries ultimately affecting the whole business environment (Grzybowska & Stachowiak, 2022). Therefore, supply chain disruptions are considered a critical factor in shaping corporate policies and act as major variable in shaping the overall financial health of the firms. An uncertainty in the supply chain environment can influence the leverage decisions of the firms thereby forcing firms to adjust their debt levels (Hupka, 2022).

Financial performance of firms is also associated with the volatility arising from the supply chain disruptions. It has been found that firms, which invest in supply chain resilience are better able to cope with the undesirable financial impacts of the supply chain disruptions as they are more flexible, have collaborative behavior and are continually innovating (Duong & Chong, 2020; Shekarian & Mellat Parast, 2021). Firms belonging to various industries have faced repercussion in the form of lower operational and financial performance owing to the disruptions caused by the pandemic as they became more vulnerable during that time (Schleper et al., 2021). Supply chain disruptions not only affect the stock prices of the firms but also inhibit their ability to access capital as the delays caused and increase in costs affect the market performance (Bier et al., 2020). The ripple effects propagated by these disruptions has lasting effects on the financial performance as firms take longer periods to recover from the negative effects and it subsequently impact their market valuations (Llaguno et al., 2022). Ginn, (2024) employed Bayesian Vector Autoregression model to examine the impact of disruptions on equity returns and revealed that disruption erupting from volatility in the supply chain has the potential to destabilize markets by causing a decline in output, an increase in inflation, thus resulting in lower equity returns.

The impact of inflation across the economy cannot be refuted as it results in lowering profits for the firms which ultimately affects their financial performance. The efficient operation of a financial market depends not only on the presence of sufficient funds but also on the accessibility of essential instruments and assets for industries. Within the framework of global financial markets, these assets play a crucial role and supply of essential resources for businesses play a key role in this regard. Regulatory changes coupled with market volatility in any sector can be consequential for the whole economic system which only results in inflation but also hampers economic growth. The disruptions caused by the supply chain have found to be an important contributor to the inflation across industries. Diaz et al., (2024) found supply chain bottlenecks to be a major contributor to the inflation and he further mentioned that this is especially true since 2010s and the surge in the prices accelerated in the period following the COVID-19 pandemic. There are various channels through which inflation emanating from the supply chain disruptions creeps in the economy ultimately affecting the industries. As the whole industrial structure is heavily reliant on the energy sector which is at the end at the mercy of smooth functioning of the global supply chain. Therefore, an increase in the energy prices would ultimately lead to inflation across the markets (Garzon & Hierro, 2021; Kumar & Mallick, 2024). Another way in which GSCP affects firms is by lowering production and this holds for economies which have larger portion of foreign value added in domestic manufacturing as shown by Celasun et al., (2022). They also posited that had the supply chain disruptions not happened half of the increase in manufacturing producer price inflation would not have happened. Igan et al., (2022) also confirmed this by signifying that supply chain disruptions contributed at least 1.5% to inflation in Europe and US in 2022. In case of Philippines and East Asian economies, (Platitas & Ocampo, 2024) indicated that GSCP is a major driver of inflationary effects in these economies and the effect is stronger in case of tradable segment of core inflation while the response of non-tradeable inflation is insignificant to the supply chain shocks. This inflationary pressure is not limited to the economies as a whole but also creeps in the commodity market as its effects has been observed on food, energy, and non-energy commodities (Gozgor et al., 2023). Tillmann, (2024) has estimated the impact of GSCP on inflation for panel of 28 EU economies and have found that adverse shocks exert a stronger and enduring impact in comparison to the favorable shocks. Following studies indicate that GSCP has a key role in exacerbating inflation which ultimately has negative consequences for the equity market (Boyd et al., 2001; Huybens & Smith, 1999). Apart from that, it also results in lower economic growth (Hung, 2003), while ultimately translates to depress financial performance of the firms. It is interesting to note that most of the studies have focused on the impact of GSCP on economies and industries through inflation perspective while ignoring its impact on the financial arena. Our study attempts to address this and add value to the extant literature by exploring the impact of global supply chain disruptions on the sectoral returns of the stock market.

The impact of GSCP varies across sectors and industries as each industry’s resilience to the external factors in the economic environment differs. Although, firms opt to equip themselves with resilience strategies to mitigates these risks; however, sectors with higher vulnerability to the supply chain disruptions experience greater volatility. The varying degree of exposure to disruptions from the supply chain across industries require that each sector and industry’s vulnerability to the external factors be assessed separately. Cagri Gurbuz et al., (2023) have highlighted that certain industries are more vulnerable to the supply chain shocks in comparison to their counterparts. Therefore, the following study aims to investigate the impact of GSCPI across different sectors of the Chinese stock market as we expect the exposure of each industry to the risk arising from GSCP to be different.

According to comparative advantage theory global supply chains are crucial to modern trade and networks (Ricardo, 2015). This theory underscores the importance of the global supply chain disruptions as these disruptions can decrease production efficiency, distort trade flows, and exacerbate cost structures ultimately affecting the profitability of the firms and their stock valuations. Global supply chain disruptions are considered to be macroeconomic shock and poses a systemic risk for the financial markets. According to the Capital Asset Pricing Model (CAPM), equity returns are influenced by the systemic risk emanating from macroeconomic shocks. In our study, although we expect that the financial returns be affected, however, the response of each sector to the supply chain disruptions varies based on the degree of dependence of each sector on the global supply chain. Therefore, we expect that the sectors with the highest dependency on international supply chains will exhibit greater sensitivity thus capturing heterogeneity across sectors which has not been studies in literature so far. Moreover, sectoral sensitivity also depends on the magnitude and persistence of disruptions in the global supply chain network.

Methodology

We employ quantile on quantile regression (QQR) as it provides a richer nonlinear information alongwith the asymmetric nature of the effects of a variable. Moreover, the Quantile-on-Quantile Approach (QQA) integrates the conventional quantile regression model with non-parametric estimates (Sim & Zhou, 2015). A non-linear approach is also more appropriate when the data exhibits non-linearity (Syed et al., 2024). The positive and negative relationship across various market states such as during bearish, normal and bullish states can provide valuable insights about the bond between GSCP and sectoral returns. The non-parametric quantile regression model applied in the following study is shown in the following equation

Where \(\theta\) denotes the \(\theta\) th quantile of the market returns (\(S{R}_{t}\)). \({\varepsilon }_{t}^{\theta }\) is an error term having zero \(\theta\) quantile. \({GSCP}{I}_{t}\) is the differential logarithm for the GSCP. Due to the lack of prior information about the relationship between GSCP and markets’ sectoral returns it is assumed that \({\beta }^{\theta }\left(\cdot \right)\) is an unknown function. This unknown function is further linearized by first order Taylor expansion and it yields the following:

The marginal effect or response denoted as \({\beta }^{{\theta }^{ \sim }}\) is the partial derivative of \({\beta }^{\theta }\,\left(S{R}_{t}\right)\) with respect to sectoral returns and is interpreted in a similar manner as of a slope coefficient in a linear regression model. Equation (2) also shows that \({\beta }^{\theta }({GSCP}{I}^{\gamma })\) and \({\beta }^{{\theta }^{ \sim }}({GSCP}{I}^{\gamma })\) are both functions of \(\theta\) and \(\gamma\) as they are affected by the changes in \(\theta\) and \(\gamma\). Being functions of \(\theta\) and \(\gamma\) these can be rewritten as \({\beta }_{0}\left(\theta ,\gamma \right)\) and \({\beta }_{1}(\theta ,\gamma )\) and Eq. (2) can be redefined as:

By substituting the Eq. (3) in Eq. (1) yields the following:

Here \((* )\) represents the \(\theta\) th quantile conditional quantile of \(S{R}_{t}\). A major difference between quantile regression and quantile on quantile regression is the double indexing of the parameters \({\beta }_{0}\) and \({\beta }_{1}\) in \(\theta\) and \(\gamma\) and therefore can provide the relationship of \(\theta\) th quantile of sectoral returns and \(\gamma\) th quantile of GSCP. Moreover, the indexing in this manner also provides a deeper understanding of the complex heterogenous relationship instead of a simple linear relationship.

By substituting \(S{R}_{t}\) and \(S{R}^{\gamma }\) in Eq. 4 with their estimated counterparts \(\widehat{{GSCP}{I}_{t}}\) and \(\widehat{{GSCP}{I}^{\gamma }}\) we obtain \({b}_{0}\) and \({b}_{1}\) from the following minimization problem:

Here \({\partial }_{\theta }\)[*] is absolute value function of the slope and can solved by the \(\theta\) th quantile of \(E{R}_{t}\). \(K(* )\) represents a Gaussian Kernel while h is the bandwidth parameter of it. With the help of Gaussian Kernel, we can weigh the observations in the neighborhood of \(\widehat{{GSCP}{I}_{t}}\). Moreover, the weights the inversely related between \(\widehat{{GSCP}{I}_{t}}\) and \(\widehat{{GSCP}{I}^{\gamma }}\) and is denoted as following for \(\overline{{GSCP}{I}_{t}}\):

Data

We use global supply chain pressure index (GSCPI) as a measure of disruptions in the global supply chain. The index was recently developed by The Federal Reserve Bank of New York by integrating Baltic Dry, Harpex, and airfreight cost indicesFootnote 1. The sectoral data of Shanghai Stock Exchange was sourced from the CEIC database for utilities, telecommunication, materials, information technology, industrial, health care, financial, energy, consumer discretionary and consumer staples sectors. Based on the availability of the data, our study covers the period from February 2005 to May 2024.

Table 1 presents the results for the descriptive statistics. Global supply chain pressure exhibits highest volatility among all the variables in this study which is also visible from the difference between maximum and minimum values. It is also reflected by the higher values of standard deviation which measure the variability or volatility. We can also observe numerous spikes in the recent times in Fig. 1 owing to the different geopolitical events which has heavily influenced the volatility in the GSCP. Among different sectors of the market information technology sector has shown the highest volatility as stocks in the IT sector experiences rapid technological advancements coupled with the risk of technological obsolescence. Chinese IT sector has been subject to various international restrictions in the recent times which resulted in a higher volatility. Materials sector also demonstrated higher volatility in comparison to other sectoral returns. Utilities and consumer staples remained stable as they exhibit the lowest standard deviations. The mean values for all the sectors of the market shows similar value with the exception of health sector for which we observe the highest value followed by financial sector. In terms of asymmetry represented by the skewness values, we observe a predominant negative skewness across variables. This indicates that extreme negative values are more common than extreme positive ones. Due to the inclusion of the data for the COVID-19 period we expect this as all the sectors experienced extreme negative returns during this period. Energy and telecommunication sector display pronounced left-skewness, while utilities remained an outlier as it exhibits slightly positive skewness. In case of sectoral returns, telecommunication sector and utilities sector display pronounced tail behavior as indicated by kurtosis values higher than 3 indicating a leptokurtic distribution. Owing to the frequent extreme disruptions, GSCP shows the highest kurtosis. The results of Jarque Bera test indicates asymmetric distribution of our data and the existence of non-normality further warrants the usage of QQR methodology.

The trend in GSCPI (Global supply chain pressure index).

Results and discussion

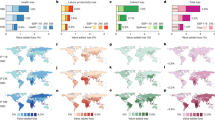

Figure 2 shows the quantile-on-quantile relationship between global supply chain pressure and different sectors of the stock market. The relationship between GSCP and utilities sector returns is predominantly negative in the lower, medium, and higher quantiles. The negative associations are primarily observed in lower to higher (0.1 to 0.90) quantiles. These outcomes infer that those inefficiencies in the global supply chain propels inflation, which, in turn, trim future cash flows. Many utilities produce income via long-term contracts having fixed prices, and Inflation can decrease profit margins if they cannot renegotiate these contracts. High inflation also pushes interest rates (Friedman, 1978; Sargent, 1973). Since utilities rely on high debts to finance their infrastructure, rising interest rates can influence borrowing costs and impact their profitability. We also observed positive relationship in selective quantiles, which entails that when global supply chain pressure is lower and market is bullish, investors opt for less risky sectors, potentially resulting in higher returns.

The 3-d graphs on the right show the estimates of the slope coefficient \({{\rm{\beta }}}_{1}\left({\rm{\theta }},{\rm{\gamma }}\right)\,\) in the z-axis against the quantiles of GSCP \(({\rm{\theta }})\) on the x-axis and the quantiles of sectoral returns \(({\rm{\gamma }})\) in the y-axis. On the left side 2-d map of the same are shown.

The negative effect of global supply chain on telecommunication sector manifests the reliance of these companies on global supply chains as they need equipment and raw materials. Higher GSCP can translate to higher costs for these items, impacting their profit, ultimately decreasing returns. The positive relationship between GSCP and telecommunication in 0.3 and 0.9 quantiles means that supply chain lapses may shift the consumer preferences towards e-commerce. This can increase online activity, increase demand for data and internet services, potentially increasing telecommunication sector returns. With the growing dependence of consumers on digital alternatives amidst supply-chain constraints in traditional markets, there is a potential for increased demand for data and internet services. This, in turn, could lead to higher returns for the telecommunications sector.

The GSCP also affects the materials, information technology industrial and health sectors asymmetrically as Fig. 2 report these outcomes. The lower quantiles of GSCP negatively affect the returns of the respective sectors. Concurrently, the higher quantiles of GSCP have positive correlation with the materials, information technology, industrial and health sectors. The negative association of the lower quantiles of GSCP with the lower quantiles of the materials, information technology, industrial and health sectors’ returns entails that supply chain disruptions decelerate production activities and curtails profit margins of the respective industries. Disruptions like these can impede the smooth flow of inputs and resources, resulting in decreased operational efficiency and ultimately, narrower profit margins in the affected sectors. The decrease in production processes highlights the susceptibility of these industries to external supply-chain disruptions, which can significantly harm their financial performance. A stressed global supply chain environment invigorates uncertainty and instills fluctuation in the market, impacting company returns. The positive relationship between higher quantiles of GSCP and higher quantiles of materials, information technology industrial and health sectors’ returns underscore the increased demand for materials, IT products, and healthcare services. This heightened demand can translate to higher returns for companies working in these sectors.

Chen et al., (2019) has also highlighted the importance of supply chain disruptions management in the information technology sector and were of the view that the sector is prone to supply chain disruptions. A predominant negative relationship exists for the industrial sector. Supply chain disruptions can depress stock returns of the industrial sector as the sector experiences increased operational costs coupled with the delayed production ultimately disrupting delivery schedules. The profit margins are further eroded due to higher transport expenses and inflated raw material prices. We also observe a predominant negative effect of GSCP on the industrial sector. Global supply chain disruptions negatively affect the industrial sector of the stock market by increasing operational costs, delaying production, and disrupting delivery schedules. Rising input prices for raw materials, higher transportation expenses, and logistical bottlenecks erode profit margins and strain cash flows. Additionally, extended lead times and supply shortages can reduce output and delay project completions, leading to revenue losses and potential contract penalties. Investor confidence in industrial stocks weakens as the sector’s capital-intensive nature magnifies the financial impact of supply disruptions, resulting in stock price volatility and underperformance relative to the broader market.

The quantiles of financial sector return (0.2-0.9) tend to have hostile response towards the quantiles of GSCP (0.2-0.9). Some plausible arguments for these outcomes are that supply chain pressure pushes market volatility, making investors more risk averse, slowing down the investment activities, resulting in stock prices decline. Financial institutions, especially banks, respond to these supply chain bottlenecks by adopting a more cautious approach. There is a possibility that access to credit could be tightened in order to address the potential risks linked to a decrease in economic output and an increase in volatility. The decrease in credit availability has a negative impact on business investment and consumer spending, which in turn hinders economic growth. During disruptions, firms with supply chain partners in affected regions experience an increase in credit risk, as indicated by abnormal credit default swaps (CDS) spreads (Ağca et al., 2023). In addition, banks have the potential to increase interest rates in order to offset the increased risks, resulting in higher borrowing costs for both businesses and households. The banks exhibit cautious attitude owing to high GSCP, tightening lending and raise the bar of interest rates; which dampen economic activity and hurt financial returns.

GSCP also decreases the returns of the energy, consumer staples and consumer discretionary sectors. Although, consumer staples exhibited resilience due to its inelastic demand but are also prone to GSCP. The relationship is predominately negative at the lower quantiles as the sector faces rising input costs owing to supply chain disruptions and it is hard to pass the effects on the consumers while the GSCP is still lower. However, the sectors’ returns respond positively to the supply chain disruptions due to the inelastic demand of the sector. Mazur et al., (2021) have also found that consumer staples sector which is mainly composed of food items earned positive returns during COVID-19 which further proves the inelastic demand of the sector. Consumer discretionary sector also behaved somewhat similar to the consumer staples with the exception that the negative effect was more pronounced at the lower quantiles. The sector heavily relies on consumer spending and economic cycles. During the period higher GSCP create a sense of scarcity, enabling companies to charge premium prices. Furthermore, firms with robust supply chain management can capitalize on competitors’ inefficiencies thereby boosting investors’ confidence by gaining market share. This decrease for energy sector is stipulated to high prices for oil, gas and metals required for energy production. This can squeeze profit margins for energy companies. A close relationship exists between supply chain and energy market as Kong et al., (2023) showed an increase in oil prices owing to supply chain pressures ultimately translating to higher transportation costs resulting in financial strain on firms. Therefore, sectors heavily reliant on energy such as logistics and manufacturing are influenced by the supply chain disruptions.

Difficulties in transportation also influence energy production and distribution particularly the renewable energy components, hampering the transition to cleaner energy sources. Consumer staples companies (e.g., food and personal care items) and discretionary companies (e.g., electronics, furniture etc.) are confronted by lower consumer demand and high inflation amid high global supply chain pressure. Uncertainty espoused by supply chains and inflation make consumers hesitant to allocate limited resources to non-essential items.

Robustness

Figure 3 showcases the robustness check for the main estimation approach (QQR) employed in the study. The results of the employed approach are deemed to be robust when estimation obtained via the SQR (standard quantile regression) approach are akin to the average estimated parameters of the QQR approach. In our case the trend line estimated via QR is alomost congruent to the trend dotted line obatined via the QQR approach for the respective return of different sectors which enatils that the QQR estimations exhibit validity or robustness.

The estimates of averaged QQR are symbolized by dashed orange line, while solid blue line represents the estimates of SQR at various quantiles.

Conclusion

The following study investigated the relationship between global supply chain pressure and Chinese sectoral return under different market conditions by employing quantile-on-quantile regression. Our results reveal significant insights into how supply chain inefficiencies and resultant inflationary pressures affect different sectors. In case of utilities sector, we observe negative association from lower, medium and higher quantiles with the exception of extreme bullish market conditions when investors seek refuge in utilities sector. Information technology, materials, industrial, and health sectors experience asymmetric effects, with lower quantiles of GSCP hindering returns due to production slowdowns, while higher quantiles benefit from increased demand. The telecommunications sector also faces negative impacts from GSCP due to increased equipment and material costs, with occasional positive effects at lower quantiles of GSCP in bullish market. The financial sector also exhibits mainly adverse response to GSCP, linked to market volatility and cautious lending during times of higher supply chain disruptions. We also witness negative association in case energy, consumer staples, and consumer discretionary sectors which can be attributed to high production costs, transportation issues, and lower consumer demand due to inflation and supply chain uncertainties.

This study’s findings provide substantial practical implications for policymakers, business executives, and investors navigating the effects of global supply chain pressures on financial markets. The asymmetric effects of GSCP on the sectors like information technology, materials, industrials, and health suggest investors to avoid these sectors during production slowdowns at lower GSCP quantiles. The investments in these sectors can be capitalized on increased demand at higher quantiles. Based on the results we suggest policymakers to focus on the enhancing the efficiency and resilience of supply chains to external pressures by fostering international cooperation, diversifying supply sources and investing in supply chain infrastructure. The adverse effects on the telecommunication sector can be avoided by fostering technological innovation and stabilizing input costs. Furthermore, the financial sector needs regulatory framework in order to improve lending during disruptions and to enhance market stability. Financial regulations should also aim at addressing market volatility and support lending practices during times of higher supply chain disruptions. Based on the results for energy, consumer staples, and consumer discretionary sectors it is also recommended to prioritize supply chain resilience through strategies like adopting forward-thinking logistics technologies and localizing supply chains. Future research should examine the role of technological advancements, such as automation and digital supply chain management, in mitigating supply chain disruptions that could offer valuable solutions for improving sectoral resilience.

Data availability

All data analyzed during this study are included in this published article as a supplementary information file.

Notes

Visit Federal Reserve Bank of New York website https://www.newyorkfed.org/research/policy/gscpi#/overview for details.

References

Ağca Ş, Birge JR, Wang Z, Wu J (2023) The impact of COVID‐19 on supply chain credit risk. Prod Oper Manag 32(12):4088–4113. https://doi.org/10.1111/poms.14079

Alessandria G, Khan SY, Khederlarian A, Mix C, Ruhl KJ (2023) The aggregate effects of global and local supply chain disruptions: 2020–2022. J Int Econ 146:103788. https://doi.org/10.1016/j.jinteco.2023.103788

Ali I, Nagalingam S, Gurd B (2017) Building resilience in SMEs of perishable product supply chains: enablers, barriers and risks. Prod Plan Control 28(15):1236–1250. https://doi.org/10.1080/09537287.2017.1362487

Bednarski L, Roscoe S, Blome C, Schleper MC (2023) Geopolitical disruptions in global supply chains: a state-of-the-art literature review. Prod Plan Control 0:1–27. https://doi.org/10.1080/09537287.2023.2286283

Bier T, Lange A, Glock CH (2020) Methods for mitigating disruptions in complex supply chain structures: a systematic literature review. Int J Prod Res 58(6):1835–1856. https://doi.org/10.1080/00207543.2019.1687954

Bonadio B, Huo Z, Levchenko AA, Pandalai-Nayar N (2021) Global supply chains in the pandemic. J Int Econ 133:103534. https://doi.org/10.1016/j.jinteco.2021.103534

Boyd JH, Levine R, Smith BD (2001) The impact of inflation on financial sector performance. J Monetary Econ 47(2):221–248. https://doi.org/10.1016/S0304-3932(01)00049-6

Cagri Gurbuz M, Yurt O, Ozdemir S, Sena V, Yu W (2023) Global supply chains risks and COVID-19: Supply chain structure as a mitigating strategy for small and medium-sized enterprises. J Bus Res 155:113407. https://doi.org/10.1016/j.jbusres.2022.113407

Celasun O, Hansen N, Mineshima A (2022) Supply Bottlenecks: Where, Why, How Much. IMF Working Paper, 31

Chen HY, Das A, Ivanov D (2019) Building resilience and managing post-disruption supply chain recovery: Lessons from the information and communication technology industry. Int J Inf Manag 49:330–342

Chowdhury MT, Sarkar A, Paul SK, Moktadir MA (2022) A case study on strategies to deal with the impacts of COVID-19 pandemic in the food and beverage industry. Oper Manag Res 15(1–2):166–178. https://doi.org/10.1007/s12063-020-00166-9

Diaz EM, Cunado J, de Gracia FP (2024) Global drivers of inflation: The role of supply chain disruptions and commodity price shocks. Econ Model 140:106860. https://doi.org/10.1016/j.econmod.2024.106860

Duong LNK, Chong J (2020) Supply chain collaboration in the presence of disruptions: a literature review. Int J Prod Res 58(11):3488–3507. https://doi.org/10.1080/00207543.2020.1712491

Ekinci E, Sezer MD, Mangla SK, Kazancoglu Y (2024) Building sustainable resilient supply chain in retail sector under disruption. J Clean Prod 434:139980. https://doi.org/10.1016/j.jclepro.2023.139980

Friedman BM (1978) Who puts the inflation premium into nominal interest rates? J Financ 33(3):833–845. https://doi.org/10.1111/j.1540-6261.1978.tb02024.x

Garzon AJ, Hierro LA (2021) Asymmetries in the transmission of oil price shocks to inflation in the eurozone. Econ Model 105:105665. https://doi.org/10.1016/j.econmod.2021.105665

Ghadge A, Wurtmann H, Seuring S (2020) Managing climate change risks in global supply chains: a review and research agenda. Int J Prod Res 58(1):44–64. https://doi.org/10.1080/00207543.2019.1629670

Ginn W (2024) Global supply chain disruptions and financial conditions. Econ Lett 239:111739. https://doi.org/10.1016/j.econlet.2024.111739

Gozgor G, Khalfaoui R, Yarovaya L (2023) Global supply chain pressure and commodity markets: Evidence from multiple wavelet and quantile connectedness analyses. Financ Res Lett 54:103791. https://doi.org/10.1016/j.frl.2023.103791

Grzybowska K, Stachowiak A (2022) Global Changes and Disruptions in Supply Chains—Preliminary Research to Sustainable Resilience of Supply Chains. Energies 15(13):4579. https://doi.org/10.3390/en15134579

Hendricks KB, Singhal VR (2005) An Empirical Analysis of the Effect of Supply Chain Disruptions on Long‐Run Stock Price Performance and Equity Risk of the Firm. Prod Oper Manag 14(1):35–52. https://doi.org/10.1111/j.1937-5956.2005.tb00008.x

Hu G, Gozgor G, Lu Z, Mahalik MK, Pal S (2024) Determinants of renewable stock returns: The role of global supply chain pressure. Renew Sustain Energy Rev 191:114182. https://doi.org/10.1016/j.rser.2023.114182

Hung F-S (2003) Inflation, financial development, and economic growth. Int Rev Econ Financ 12(1):45–67. https://doi.org/10.1016/S1059-0560(02)00109-0

Hupka Y (2022) Leverage and the global supply chain. Financ Res Lett 50:103269. https://doi.org/10.1016/j.frl.2022.103269

Huybens E, Smith BD (1999) Inflation, financial markets and long-run real activity. J Monetary Econ 43(2):283–315. https://doi.org/10.1016/S0304-3932(98)00060-9

Igan D, Rungcharoenkitkul P, Takahashi K (2022) Global supply chain disruptions: evolution, impact, outlook (Issue 61). https://econpapers.repec.org/RePEc:bis:bisblt:61

Jüttner U, Maklan S (2011) Supply chain resilience in the global financial crisis: an empirical study. Supply Chain Manag: Int J 16(4):246–259. https://doi.org/10.1108/13598541111139062

Kleindorfer PR, Saad GH (2005) Managing Disruption Risks in Supply Chains. Prod Oper Manag 14(1):53–68. https://doi.org/10.1111/j.1937-5956.2005.tb00009.x

Kong F, Gao Z, Oprean-Stan C (2023) Green bond in China: An effective hedge against global supply chain pressure? Energy Econ 128:107167. https://doi.org/10.1016/j.eneco.2023.107167

Kovács G, Falagara Sigala I (2021) Lessons learned from humanitarian logistics to manage supply chain disruptions. J Supply Chain Manag 57(1):41–49. https://doi.org/10.1111/jscm.12253

Kumar A, Mallick S (2024) Oil price dynamics in times of uncertainty: Revisiting the role of demand and supply shocks. Energy Econ 129:107152. https://doi.org/10.1016/j.eneco.2023.107152

Li J, Wang Y, Song Y, Su CW (2023) How resistant is gold to stress? New evidence from global supply chain. Resour Policy 85:103960. https://doi.org/10.1016/j.resourpol.2023.103960

Llaguno A, Mula J, Campuzano-Bolarin F (2022) State of the art, conceptual framework and simulation analysis of the ripple effect on supply chains. Int J Prod Res 60(6):2044–2066. https://doi.org/10.1080/00207543.2021.1877842

Mazur M, Dang M, Vega M (2021) COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Financ Res Lett 38:101690. https://doi.org/10.1016/j.frl.2020.101690

Platitas, RJC, & Ocampo, JCG (2024). From bottlenecks to inflation: Impact of global supply-chain disruptions on inflation in select Asian economies. Latin American Journal of Central Banking, 100141. https://doi.org/10.1016/j.latcb.2024.100141

Raj A, Mukherjee AA, de Sousa Jabbour ABL, Srivastava SK (2022) Supply chain management during and post-COVID-19 pandemic: Mitigation strategies and practical lessons learned. J Bus Res 142:1125–1139. https://doi.org/10.1016/j.jbusres.2022.01.037

Ren X, Fu C, Jin C, Li Y (2024) Dynamic causality between global supply chain pressures and China’s resource industries: A time-varying Granger analysis. Int Rev Financ Anal 95(PA):103377. https://doi.org/10.1016/j.irfa.2024.103377

Ricardo D (2015) On the Principles of Political Economy, and Taxation. Cambridge University Press. https://doi.org/10.1017/CBO9781107589421

Sargent TJ (1973) Interest Rates and Prices in the Long Run: A Study of the Gibson Paradox. J Money, Credit Bank 5(1):385. https://doi.org/10.2307/1991332

Schleper MC, Gold S, Trautrims A, Baldock D (2021) Pandemic-induced knowledge gaps in operations and supply chain management: COVID-19’s impacts on retailing. Int J Oper Prod Manag 41(3):193–205. https://doi.org/10.1108/IJOPM-12-2020-0837

Shekarian M, Mellat Parast M (2021) An Integrative approach to supply chain disruption risk and resilience management: a literature review. Int J Logist Res Appl 24(5):427–455. https://doi.org/10.1080/13675567.2020.1763935

Sim N, Zhou H (2015) Oil prices, US stock return, and the dependence between their quantiles. J Bank Financ 55:1–8. https://doi.org/10.1016/j.jbankfin.2015.01.013

Su CW, Wang Y, Qin M, Lobonţ OR (2023) Do precious metals hedge against global supply chain uncertainty? Borsa Istanb Rev 23(5):1026–1036. https://doi.org/10.1016/j.bir.2023.05.004

Syed AA, Ullah A, Kamal MA (2024) Impact of COVID-19 and lockdown stringency on foreign institutional investment in India: evidence from wavelet coherence and spectral causality approaches. Qual Quant 58(3):2433–2452. https://doi.org/10.1007/s11135-023-01754-0

Tillmann P (2024) The asymmetric effect of supply chain pressure on inflation. Econ Lett 235:111540. https://doi.org/10.1016/j.econlet.2024.111540

Tukamuhabwa BR, Stevenson M, Busby J, Zorzini M (2015) Supply chain resilience: definition, review and theoretical foundations for further study. Int J Prod Res 53(18):5592–5623. https://doi.org/10.1080/00207543.2015.1037934

Vidal CJ, Goetschalckx M (1997) Strategic production-distribution models: A critical review with emphasis on global supply chain models. Eur J Oper Res 98(1):1–18. https://doi.org/10.1016/S0377-2217(97)80080-X

Wei S, Zhou Q, Luo Z, She Y, Wang Q, Chen J, Qu S, Wei Y (2023) Economic impacts of multiple natural disasters and agricultural adaptation measures on supply chains in China. J Clean Prod 418:138095. https://doi.org/10.1016/j.jclepro.2023.138095

Yu W, Jacobs MA, Chavez R, Yang J (2019) Dynamism, disruption orientation, and resilience in the supply chain and the impacts on financial performance: A dynamic capabilities perspective. Int J Prod Econ 218:352–362. https://doi.org/10.1016/j.ijpe.2019.07.013

Zhong Y, Chen X, Wang Z, Lin RFY (2024) The nexus among artificial intelligence, supply chain and energy sustainability: A time-varying analysis. Energy Econ 132:107479. https://doi.org/10.1016/j.eneco.2024.107479

Funding

This work was supported by the 2024 Annual Open Fund Project of the Hanshui Culture Research Base, a Key Research Base of Humanities and Social Sciences in Hubei Province, Hanjiang Normal University, Shiyan (Project Number: HSWH2024001).

Author information

Authors and Affiliations

Contributions

Adeel Riaz: Conceptualization, Data curation, Methodology, Investigation, Formal analysis, Visualization, Writing-original draft, Funding acquisition; Assad Ullah: Validation, Writing-original draft, Investigation; Writing-review & editing; Bashir Muhammad: Conceptualization, Supervision, Writing-review & editing.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical Approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

Since this article does not contain any studies with human participants performed by any of the authors so therefore it does not require any informed consent.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Riaz, A., Ullah, A. & Muhammad, B. The impact of global supply chain pressure on the stock market: A sectoral view. Humanit Soc Sci Commun 12, 284 (2025). https://doi.org/10.1057/s41599-025-04634-0

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-04634-0