Abstract

The Saudi Arabian stock market is one of the top ten stock markets worldwide in terms of capitalization. The size of its capitalization has caused the stock market to draw the attention of local and foreign investors. This study investigates the macroeconomic variables that have the strongest effects on the behavior of the Saudi Arabian stock market (TSAI). The main variables are income, oil and the interest rate, with the aim of examining the long-run cointegration with consideration of the impact of the asymmetric behavior of oil and interest rates on the stock market. Thus, a nonlinear ARDL cointegration approach was used to test for the existence of a long-run cointegration relationship among the variables, which was confirmed by using an econometric model. The model also confirmed the asymmetric impact of oil and interest rates. Over the long run, income and negative oil attributes have positive impacts on the stock market, while the positive attributes of the real interest rate have a negative impact. However, the short-run dynamics showed the positive impact of income in the first moment and a statistically significant impact. On the other hand, the second moment of income showed a negative impact on the stock market. Furthermore, positive oil attributes have a negative impact on the stock market, as does the second moment of the negative attribute of oil. In addition, the negative attribute of oil showed a positive impact on the stock market in the first moment and over the long run. However, the asymmetric impact of oil on the Saudi Arabian stock market was confirmed by the model in terms of the short-run dynamics. These results can aid authorities as they implement fiscal policy to mitigate the impacts of these macroeconomic factors on the stock market.

Similar content being viewed by others

Introduction

The stock market is one of the main channels for savers to invest in the modern economy, especially with the recent technological development of stock market tools. The Saudi Arabian stock market first began alongside the process of establishing the Kingdom of Saudi Arabia in 1935 with one company called the Car Arabian Company, which was liquidated shortly after the inception of its IPOsFootnote 1 The next iteration of the Saudi Arabian stock market was in 1954 with the Arabian Cement Company IPOs. The number of publicly listed companies has grown since 1954, with 14 companies becoming publicly listed in 1970. Then, the mid-1970s’ oil boom caused the number of companies to reach 34. The development in Saudi Arabia as oil revenues hit unexpected levels motivated companies to publicly list, and the requirement to develop the stock market became a priority for the Saudi authorities.

Saudi Arabia has developed its stock market’s ability to accommodate fast and easy access to market investment tools, to enhance them, and to attract more investors to participate in the stock market, similar to the most developed countries. Today, Saudi Arabia is in the top 10 stock markets worldwide and first in the Middle East and North Africa in terms of capitalization, with a capitalization size of USD 3 trillion in stock, according to the Saudi Exchange’s monthly report from August 2023. Furthermore, the Saudi Arabian stock market cap was three times the country’s nominal GDP. The Saudi Arabian stock market, which is represented by the main index TASI, has 223 companies listed with diverse business activities. Eighteen companies made IPOs in 2022, at a value of almost USD 10 billion, making the Saudi Arabian stock market a potential investment opportunity for local and foreign investorsFootnote 2. In addition, the amount of capital that the Saudi Arabian stock market acquired for the IPOs shows the strength and trust in the Saudi Arabian economy and stock market. The average traded value of stock shares has reached USD 1.8 billion, with a volume of 181.90 million shares. These statistics position the Saudi Arabian stock market to be added to the MSCI emerging stock market index.

The Saudi Arabian government has launched its economic vision, Vision 2030. It aims to have a strong and reliable financial sector that can observe a financial surplus. Vision 2030 involves a program for developing and restructuring the financial sector. This development will enhance investment opportunities, income-diversifying abilities, and savings.

The reform will restructure the financial sector which will impact the economy and change the stock market behavior. Therefore, it is important to study the factors that impact the stock market to enable the authorities to mitigate the challenges and to control the stock market during the reform phase.

In this study, the focus is on the external factors that affect the stock market and that the authorities can control. Understanding these factors will provide a sense of their consequences in terms of how the behavior of the stock market responds to the factors’ changes. In this context, income, interest rates and oil are characterized as the main factors impacting the stock market. The choice of income and interest rates was based on the hypotheses of Hicks (1937), while oil was chosen based on its role in the Saudi Arabia economy (Alabdulwahab, 2021; Alkhathlan, 2013). However, the interest rate has been confirmed to play a role in stock markets by its mid and long-term span (Campbell, 1987). The assessment is framed in terms of the long-run impact and short-run dynamic impact in order to understand the behavior of the leading factors in both time periods, enabling the authorities to design their policies based on their desired time frame.

This study leveraged the analysis of the financial market relative to macroeconomic factors by focusing on the associations among the variables. Furthermore, this study has transformed the GDP to income per capita, unlike most studies in this field, which have used factors in their natural form. However, this study imposes the price level within the variables by using the real form of the variables. In addition, this study analyzes one of the fastest-growing stock markets in emerging countries; it has not been studied often, nor has the recent reform plan in Saudi Arabia. This study provides insight into the stock market’s behavior with respect to the changes in the macroeconomic variables, which can also provide the authorities with a sense of the consequences that they may anticipate. This article will be structured as follows: section “Literature review” serves as the literature review, section “Methodology” forms the econometrics model, section “Data” is the data description, section “Results” is the result and finally section “Conclusions” is the conclusion.

Literature review

Stock markets play an important role in the economy as venues for investors and companies. Investors can earn profits by investing in companies that are publicly listed, while the companies can raise money to finance their expansions. Stock markets are directly exposed to economic impacts through the expectation of future economic performance, and they are indirectly affected by the economy via the listed companies, as they respond to the changes in the economy. The direct effect can be controlled as the government has used its economic policy tools efficiently. The gross domestic product (GDP) is the main index for measuring economic performance, which is one of the factors that is analyzed by this study. Yartey (2008) investigated the determinants of the stock markets for 42 emerging countries using institutional and macroeconomic factors. Macroeconomic factors, such as the income level, gross domestic investment, banking development, private capital flow, and market liquidity, are important for emerging countries’ stock market performance. In addition, the political, law enforcement, and administrative qualities are also important determinants. These factors were found to have an important role in South Africa’s stock market performance.

The economic development and the size of the stock market are more correlated than the economic output (McGowan, 2008). In an examination of 102 countries, the result showed a positive and significant relationship between income per capita and stock market capitalization. Karacaer and Kapusuzoglu (2010) analyzed the relationships between inflation, industrial output, exchange rates, and the stock market in Turkey. The results showed a significant long-run relationship among the variables in the frame of analysis in the study. However, in the short run, there were unidirectional and bidirectional causal relationships among the variables. Gnahe (2021) investigated the impact of macroeconomic variables on stock market returns in Kazakhstan. He estimated the Johansen Cointegration to examine the relationship among the stock market returns, gross domestic product (GDP), exchange rates, interest rates, foreign direct investment (FDI), and inflation rates. The results showed that all the variables statistically significantly impacted the stock market returns, except for the GDP. On the other hand, Omar et al. (2022) implemented ARDL cointegration to examine the existence of a long-run relationship between stock market development and macroeconomic indicators in Pakistan. The test assessed the impacts of economic growth, inflation, financial development, foreign direct investment (FDI), and trade openness on stock market development. Furthermore, the ARDL cointegration confirmed the existence of a long-run relationship between the variables considered. Among all the variables, the GDP and financial development had a positive impact on stock market development in the short and long run, whereas the rest of the variables had a negative impact. Furthermore, the GDP and FDI had a positive impact on stock market development in the short run, whereas the rest of the variables had a negative effect.

The financial development and trade openness were statistically insignificant in the short run. Stock market participation was investigated in 19 European countries by Kaustia et al. (2023), using a panel analysis method. The framework of the analysis accommodated the institutional, traditional, and individual levels, as well as behavioral variables, to assess the effects of those variables on stock market participation. The methodological framework examined all factors with fixed effects, and the factors were decomposed to gain a more precise insight into the impact of each set of data on stock market participation. The results showed that income had a positive impact on participation in the stock market when the model involved all factors. In addition, the model of regulatory quality and the model of wealth and education showed a significant positive impact of income on stock market participation. On the other hand, equity share in financial assets showed a negative impact of income on stock market participation. The aphasias of most discussed studies imply a positive relationship between the stock market and income. This factor can be controlled via fiscal policy, like the other factor, which is the interest rate.

The interest rate is a monetary policy tool that has a direct impact on the financial sector. The aim of monetary policy is to direct the economy to attain economic goals such as price stability. However, a change in the interest rate changes the behavior of investors toward the expansion or reduction in their business activities. Therefore, the stock market is indirectly impacted by the interest rate via the performance of the listed companies. Alam and Uddin (2009) examined the existence of stock market efficiency for a set of developed and developing countries, including Australia, Canada, Germany, Italy, Japan, Spain, Chile, Mexico, South Africa, Bangladesh, Jamaica, Venezuela, Colombia, the Philippines, and Malaysia. A stationarity test was applied to the return of the stock market for each country, and it was found that none of these stock markets exhibited the behavior of a random walk model, which means that previous prices can predict future prices. These stock markets were not efficient and had a weak form in their stock market activities. For further investigation, the relationship between stock market prices and interest rates was tested, specifically, the relationship between the change in the stock market price and the change in the interest rate. The results showed a significant negative relationship between the stock market price and interest rate. On the other hand, six of the fourteen countries had a significant negative relationship between the change in stock price and the change in the interest rate. Uddin and Alam (2010) tested the efficiency of the Dhaka Stock Exchange (DSE). They found that the DSE was not efficient in its financial activities based on the stationarity test, which showed no behavior of a random walk model. However, the linear relationship between the stock market price and the interest rate was tested, as was the change in the stock market price associated with the change in the interest rate. The test results proved the existence of a negative relationship between the two variables in both tests.

The relationship between the interest rate and the stock market has also been shown to vary across stock market sectors (Moya-Martínez et al., 2015). A wavelet analysis was applied to the stock market of Spain to test the impact of the interest rate at the sectoral level of the stock market. The results showed that the interest rate’s impact was differentiated across the sectors in the stock market. Furthermore, the degree of sensitivity of each sector relied on the degree of exposure of this sector to financial activities and regulations. Sectors that were more exposed to regulations, such as telecommunication, real estate, and utility, as well as the banking sector, were highly impacted by the change in the interest rate. The relationship between the returns in those sectors and the interest rate was examined and showed a strong relationship even at the coarsest scales. Bissoon et al. (2016) examined the impact of the monetary policy in five open economies on the stock market returns using a panel framework. The results showed significant long-run and short-run relationships among the variables, proving the negative relationship between the stock market return and the interest rate. In addition, there was a significant direct link between money supply and stock market returns. However, the model confirmed the ability of monetary variables to explain the changes in the stock market in the short run and long run. Eldomiaty et al. (2020) investigated the impact of the real interest rate and inflation on the stock market price for DJIA30 and NASDAQ100. The Johansen panel cointegration framework was applied to test the existence of relationships among the variables in the investigation. The results confirmed the existence of the relationship among the variables, showing a negative relationship between inflation and stock market price. On the other hand, the relationship between the interest rate and stock price was positive.

The relationship between macroeconomic variables and the stock market has not been clearly confirmed. John (2019) examined the impact of macroeconomic variables in Nigeria on its stock market, including the exchange rate, money supply, interest rate, and inflation. The results showed a significant relationship between the stock market and money supply, as well as the interest rate. However, there was a positive relationship between the money supply and the stock market, unlike the interest rate, which had a negative relationship with the stock market. The exchange rate and inflation had a positive impact on the stock market, but they were insignificant. However, the long-run relationship among the variables was confirmed, with the conclusion that the money supply and interest rate were the macroeconomic factors that had the greatest impact on the stock market in Nigeria. The macroeconomic factors in the United States, such as the interest rate, have a global impact on worldwide stock markets. Kim (2023) assessed the response of Korean firms to the change in the US interest rate. The results showed that a sharp increase in the US interest rate would result in a high level of quality investors leaving emerging stock markets. Companies with a high export share of their products, foreign ownership, and large capitalization would perform well during an interest rate shock, unlike other firms with small capitalization, no foreign ownership, and a small export share. Furthermore, small companies with fixed financial abilities were less likely to suffer from shocks due to an interest rate hike. However, the stock market is subject to factors that are determined globally, which are beyond the control of the local authorities, such as oil.

In general, oil has an impact on the global economy, as it is a basic input in a variety of industrial sectors, either as a source of energy or a raw input material. A change in the oil market changes the stock market returns, and oil shocks impact the prices of stock market returns (Apergis and Miller, 2008). Oil price changes can be decomposed into three types of shocks: oil supply shocks, global oil demand shocks, and global aggregate demand shocks. The impacts of these shocks on stock market returns were assessed in eight developed countries, including the USA, Canada, the UK, France, Germany, Italy, Japan, and Australia. In addition, the vector autoregressive (VAR) model was estimated, which determined that oil shocks had a minimal effect on international stock market returns. However, Amri-Asrami and Jamkhane (2024) have assessed the oil impact on Tehran Stock Exchange (TSE) performance NARDL cointegration method. The result shows a symmetric impact between oil prices and stock market performance in the long run. Unlike the long run, the estimation shows asymmetric impact between oil price and stock market performance, as well as the performance of the petrochemical sector. In contrast, Arouri and Rault (2010) examined the relationship between oil prices and stock markets in the Gulf Cooperation Council (GCC). The result revealed that there was a significant causal relationship between the oil price and the stock market in GCC countries. However, this causal relationship was bidirectional in the case of Saudi Arabia, unlike the rest of the GCC countries. Furthermore, the rest of the GCC countries exhibited a causal direction from oil prices to the stock market. Alqattan and Alhayky (2016) examined the relationship between the oil price and GCC countries’ stock markets. The ARDL cointegration model was estimated to examine the existence of a long-run relationship among the variables, which revealed that there was no long-run relationship among the variables, except in the case of Oman. However, the model proved the cointegration among the variables for all GCC countries in the short run. Changes in the oil price play a role in stock market changes in the short run, with a positive effect across the GCC countries.

In Africa, there are countries producing oil, and oil can affect their stock markets’ performance. Olufisayo (2014) investigated the relationship between oil price differences and stock market differences in Nigeria. The results showed that there was a long-run relationship between oil price differences and stock market differences. However, there was unidirectional causation from oil prices to the stock market. Furthermore, the impulse response function (IRF) showed that there was a temporary positive impact of oil prices on the stock market in Nigeria. On the other hand, variance decomposition (VDC) suggested that the variations in the stock market in Nigeria were driven by oil shock changes. Moreover, Ojeyinka and Aliemhe (2023) investigated the impact of oil demand, global oil supply, and oil-market-specific demand on the Nigerian Stock Exchange (NSE) at the sectoral level, including the oil and gas, consumer goods, industrial, insurance, and banking sectors. Furthermore, the ARDL cointegration model was estimated to assess the linkage among the variables. The results confirmed the long-run association between oil price changes and stock market returns in Nigeria. In addition, the model indicated the positive relationship between oil demand, oil-market-specific demand, and aggregate stock market returns, as well as sectoral returns. On the other hand, the global oil supply had an insignificant impact on aggregate market returns, as well as the sectoral returns, except in the oil and gas sector. The model indicated that the global oil supply had a significant positive relationship with the oil and gas sector. However, Kelikume and Muritala (2019) implemented a dynamic panel data analysis to observe the impact of the oil price on the stock markets for five oil-producing African countries. The results showed a negative impact of oil on the stock market across the selected countries. However, unlike oil prices, GDP growth has a positive impact on these countries’ stock markets.

Asian stock markets can be affected by oil in oil-producing countries as well as oil-consuming countries. However, the impact of oil differed across stock market sectors. Rahmanto et al. (2016) investigated the impact of the oil price on the Indonesian stock market in a sector-level analysis. They found a positive impact of oil on all sectors of the Indonesian stock market. However, an asymmetric relationship among oil prices, agriculture sector returns, and consumer goods sector returns was confirmed. Shabbir et al. (2020) applied ARDL cointegration to examine the existence of a long-run relationship between the stock market, oil prices, and gold prices in Pakistan, which was confirmed. The oil price had a negative impact on the stock market in Pakistan in both the long run and the short run. Furthermore, the attribute of the long-run impact was minimal relative to the short run. In addition, in the model, the attribute of the oil price impact was greater than the gold price impact. Alamgir and Amin (2021) estimated a nonlinear ARDL cointegration model to assess the linkage between oil prices and the stock market for four South Asian countries. They found that the oil price had an asymmetric effect on the stock market. The relationship between oil prices and the stock market was positive, and the stock market was stimulated by higher oil prices, which indicated that the stock market exhibited inefficient financial activities.

European countries' stock markets are exposed to the oil changes due to their high economic openness. Furthermore, Castro et al. (2023) assessed three structural oil shocks to examine the time-varying impact of oil on European stock market returns. They used a time-varying parameter vector autoregression model to analyze the supply-side shock, aggregate demand shock, and oil-specific demand shock impact. They found that the impacts of those shocks varied over time; the European stock markets responded positively to sudden increases in oil supply in the period before the Global Financial Crisis (GFC) in 2007–2009 and negatively in the post-GFC period. However, the European stock markets responded positively to sudden increases in demand and responded negatively in 2003–2005 as a result of a growth-delay effect. Furthermore, the European stock markets responded negatively to a sudden increase in oil-specific demand in the pre-GFC period and positively in the post-GFC period. The studies have been focusing on either emerging markets as a group of markets or as individual markets. However, fewer studies have focused on the Saudi Arabian stock market as an individual market and their focus was driven by either financial motivation or oil prospect.

In recent years, the Saudi Arabian government has paid more attention to the financial sector as a path to attracting foreign investors. One of the goals of the Saudi Arabian government is to develop the stock market by developing regulations and introducing new trading tools, such as derivatives. This new development requires more studies investigating different aspects that impact the stock market to be aware of the future challenges of these structural changes. Many studies have analyzed the Saudi Arabian stock market, assessing the factors that affect it. Samontaray et al. (2014) examined the impact of macroeconomic variables on returns in the Saudi Arabian stock market. Furthermore, they examined the impacts of oil prices, exports, and the PE ratio on stock market returns. They found that the stock market was correlated with independent factors. In addition, the price-to-earnings (P/E) ratio was the most important factor impacting the stock market. Independent factors positively impact the stock market, and 93% of the variations in the dependent variables were explained by the independent variables. On the other hand, Tong et al. (2018) analyzed the impact of crude oil price volatilities on volatility in the Saudi Arabian stock market. They compared different econometric models and concluded that the Markov switching nonlinear model was the most consistent. Furthermore, in both estimated regimes, crude oil was found to have a positive and significant impact on the stock market.

Global factors had a negative and significant impact on the stock market. Khamis et al. (2018) studied the impact of oil price variations on the Saudi Arabian stock market at the sectoral level. They found that sectors in the stock market had a relationship in terms of Granger causality with respect to oil price variations. However, the sectors were affected by negative oil prices more than positive oil prices, which confirmed the asymmetric impact of the oil price on the Saudi Stock market. Aljifri (2020) examined the long-run relationship between the Saudi Arabian stock market and macroeconomic variables. The Johansen cointegration test was implemented to test for the existence of a long-run relationship among the variables under consideration, which was confirmed. Oil prices and the S&P 500 had a significant positive impact on the stock market. On the other hand, the money supply had a significant negative impact on the stock market. Furthermore, the stock market was highly affected by oil prices, while the money supply and S&P 500 had a relatively minimal effect on the stock market. Furthermore, Sadouni et al. (2022) investigated the existence of a long-run relationship between oil and the Saudi Arabian stock market using a cointegration approach. The Granger causality test was applied to assess the direction of causality among the variables under consideration. The results confirmed the long-run relationship among the variables, as well as the unidirectional causality from the Saudi Arabian stock market to the oil market for both BRENT and OPEC basket prices. Also, Abdou et al. (2024) examine the ability to predict the Saudi stock market performance via oil prices and the stock markets of five developed countries, incorporating China’s stock market as an extension to developing markets. The Machine Learning (ML) approach, as well as Generalized Method Moments, have been exercised to investigate the effect of these variables on the Saudi stock market. The result shows a strong impact of oil on the Saudi stock market after the 2006 Saudi stock market collapse. Furthermore, prior to 2006, the UK and Japan were the most influential markets to the Saudi stock market, while China’s stock market became the most influential after 2006, following the Saudi stock market's collapse.

The policy of fixed exchange rate of Saudi Riyal rise the question how the monetary policy of the US can affect the Saudi Arabi stock market. Almahfouz (2020) attempted to distinguish the impact of US monetary policy as represented by the change in the Fed’s fund target rate and the quantitative easing program on the Saudi Arabian stock market. The study revealed that the Saudi Arabian stock market was more significantly affected by US monetary policy than by the quantitative easing program.

In general, most studies have investigated the linear relationships between the chosen variables, like Gnahe (2021), Moya-Martínez et al. (2015), Khamis et al. (2018), Arouri and Rault (2010), and Alqattan and Alhayky (2016). Few studies have discussed the existence of a nonlinear relationship between the stock market and oil prices, like Alamgir and Amin (2021) and Amri-Asrami and Jamkhane (2024). In addition, income, which is an important factor affecting the stock market, has not been discussed in the Saudi Arabian context. Furthermore, no studies have investigated either the asymmetric impact of the interest rate on the Saudi Arabian stock market or the impact of income. However, the studies in the literature have discussed different factors that have an impact on the stock market, like trade openness, money supply and inflation, which are important to the structure of their study framework. On the other hand, this study will investigate the impacts of income, the interest rate, and oil on the Saudi Arabian stock market within a nonlinear analytical framework. The results of this study will help the authorities gain insights into policy implications and the effects of global economic events on the Saudi Arabian stock market.

Methodology

The stock market is affected by local and global economic factors. The Saudi Arabian stock market is similar to stock markets in countries with open economies exposed to global economic distortion. The literature review suggested that there were different factors with positive and negative impacts on the stock market. In this study, we focus on the factors that represent economic policies (the interest rate), global market interactions (oil), and local macroeconomic factors (income). Therefore, the stock market in Saudi Arabia, which is represented by TASI, is a function of these factors, as it is shown in Eq.1. However, focusing on these factors will strengthen the analysis on how economic policies, as well as global events, affect the Saudi Arabian stock market.

TASI is the Tadawul All Share Index, and it represents the main Saudi Arabian stock market; IN is the real income per capita, Oil is the oil rent, and R is the real interest rate. The expected sign of each variable is marked on top of each factor symbol. Most studies have indicated the positive impact of income on stock market returns (e.g., McGowan (2008) and Omar et al. (2022)). Hence, we expect the impact of an increase in income on the stock market to be positive, as income increases, the amount of savings will increase, and savings are transferred to investments. Thus, the stock market shares should increase due to future earnings expectations as a result of new business expansion in the companies that are listed in the stock market. The expectation for the impact of oil to be positive, as we consider that oil revenue increases as oil prices increase, and the Saudi Arabian economy relies on oil activities. Therefore, the wealth of Saudi Arabia increases, which will result in the demand for stock shares increasing. However, many studies on this topic have reported contradictory directions of the impact of oil on the stock market (e.g., Alamgir and Amin (2021) and Shabbir et al. (2020)) and Saudi Arabia, as surplus in the oil production exceeds oil consumption as relatively speaking. We expect that an increase in the interest rate will have a negative impact on the stock market; the theory explains that an increase in the interest rate will result in a decrease in borrowing activities. Therefore, the cost of investment financed by borrowing will increase, which will drive firms to shrink their business activities as a result. Investors in the stock market make their decisions with respect to future returns, and an increase in the interest rate minimizes their expectations, which directs the stock market toward bearish activities.

Equation1 has a functional form that represents the relationships among the variables, and it cannot be estimated. Therefore, Eq.1 should be transformed into a linear equation form for OLS estimation, as shown in Eq.2. However, \({TASI}\) is the dependent variable, and \(\propto\) is the constant term of the equation. In addition, \({\beta }_{1}\), \({\beta }_{2}\), and \({\beta }_{3}\) are the coefficients of the explanatory variables. This transformation can be done via a log form mechanism. Furthermore, \({\varepsilon }_{t}\) is the error term of the equation capturing the unexplained changes in the dependent variables that are not explained by the explanatory variables?

The ARDL cointegration is estimated based on the OLS estimation method; however, the estimation contains the I(0) and I(1) forms of the variables, as well as the first difference form. The main requirement of estimating the ARDL cointegration model is that none of the variables should take the I(2) stationarity rank, including the dependent variable (Pesaran and Shin, 2001; Pesaran et al., 2001). This requirement was imposed to ensure the validity of the ability of the ARDL bounds test to validate the F joint test of the estimation. Therefore, a variable with the stationarity rank I(2) will invalidate the F joint test, and this requires the stationarity test to be assessed ahead of the ARDL cointegration estimation. To satisfy this requirement, the Augmented Dickey–Fuller (ADF) and Kwiatkowski–Phillips–Schmidt–Shin (KPSS) methods were used to ensure that none of the variables had the I(2) rank.

Nonlinear ARDL cointegration model

The assumption that the relationship between variables is linear is questionable, especially when dealing with variables that have high volatility, such as oil prices and any component that uses the oil prices implicitly. In addition, nonlinear analysis can deal with variables that are controlled by changes in the behavior of other variables. Independent variables can have positive and negative attributes within short periods of time. Furthermore, several studies in this field have confirmed the existence of nonlinear relationships between oil and the stock market, and they characterized the effects of independent variables on the dependent variable as an asymmetric effect (Rahmanto et al., 2016; Alamgir and Amin, 2021; Khamis et al., 2018). Therefore, a method based on that of Shin et al. (2014) is used; the explanatory variables that are considered to have an asymmetric effect should be decomposed into positive and negative changes. Hence, Eq.3 and Eq.4 contain \({{Oil}}_{t}^{+}\), \({{Oil}}_{t}^{-}\), \({R}_{t}^{+}\), and \({R}_{t}^{-}\), which represent positive and negative changes in oil and the interest rates, respectively. \({{Oil}}_{t}^{+}\) indicates a positive change in oil, and \({{Oil}}_{t}^{-}\) represents negative changes in oil. \({R}_{t}^{+}\) indicates positive changes in the interest rate, and \({R}_{t}^{-}\) represents negative changes in the interest rate. This form of equation is a partial sum framework.

To ensure the asymmetric effect of the independent variable on the dependent variable, Eq. 5 and Eq. 6 should be assessed, as stated in Schorderet (2001).

The asymmetric relationship between the two variables is confirmed when \({S}_{t}\) is stationary in both equations. On the other hand, if \({\beta }_{0}^{+}=\,{\beta }_{0}^{-}\) and \({\beta }_{1}^{+}=\,{\beta }_{1}^{-}\), the relationship between the two variables is symmetric. Therefore, the Wald test was applied to confirm the existence of asymmetric phenomena between the independent variable and dependent variable. The test assesses whether \({\beta }^{+}=\,\frac{{\beta }_{1}^{+}}{{\beta }_{0}}\) and \({\beta }^{-}=\,\frac{{\beta }_{1}^{-}}{{\beta }_{0}}\) are equal or not. If they are not equal, then asymmetric phenomena exist, and if they are equal, then a symmetric relationship exists between the independent variable and dependent variable (Shin et al., 2014).

The nonlinear ARDL cointegration form is represented by Eq.7 based on Shin et al. (2014). The driving of this equation is based on Eq.2, which is OLS estimation.

In Eq.7, \(\beta,\,\partial,\delta,\,\psi,\,\gamma\), and \(\rho\) are the short-run dynamic coefficients, whereas \({\theta }_{0}\) to \({\theta }_{5}\) represents the long-run coefficients, as Pesaran et al. (2001) stated. To estimate Eq.7, the lag length was selected to determine the optimal lag of the model. There are several lag criterion selection methods, such as the AIC, SC, BIC, etc. In this study, the AIC was implemented, since the data that will be estimated are short-span data (Liew, 2004). Thus, p, q, m, r, and d are determined within the optimal level based on the AIC. In order to assess the long-run cointegration among the variables, t-statistic and F-statistic tests were applied based on Banerjee et al. (1998) and Pesaran et al. (2001), respectively. In addition, the F-test from Narayan (2005) was applied, since our dataset was relatively small. Furthermore, all tests were used to decide whether to accept or reject the null hypothesis via a bound test. The hypothesis for the existence of long-run cointegration is the following:

The test was applied to the transformation of the above hypothesis with the F-test in the following form:

The procedure of the test involves comparing the F-statistic of the estimation with the F-statistic in the work of Pesaran et al. (2001) and Narayan (2005). The rule of rejecting or accepting the null hypothesis is based on the bound test. If the F-statistic in the test is greater than I(1) for the calculated critical value in the table, then \({H}_{0}\) is rejected, and the alternative \({H}_{1}\) is accepted, which indicates long-run cointegration among the variables. However, if the F-statistic in the test is lower than I(0) for the calculated critical value in the table, then \({H}_{0}\) is not rejected, and there is no long-run cointegration among the variables. Furthermore, the t-test was applied based on Banerjee et al. (1998), and the same rule of rejecting or accepting the null hypothesis was followed. The hypothesis for the t-statistic test involves the t-statistic of the lag of the TASI, which is \({\theta }_{0}\) in Eq. 7. In addition, Giles’ (2013) test was applied as a robustness check to test the hypothesis and determine whether the lag of the dependent variable’s coefficient was negative and significant, as represented by the following:

The short-run dynamics were estimated based on the first part of Eq. 7, and an error correction term was added to ensure the convergence of the equation to long-run equilibrium if any distortion occurred in the short run. Equation 8 represents the short-run dynamics that are estimated with the optimal lags generated by the ARDL cointegration method for each variable (p, \(q\), \(m\), \(r\), \(d)\).

The term \({\varphi {ECM}}_{t-i}\) is the correction term of the equation, and it should be significant and negative to ensure the convergence from short-run dynamics to long-run equilibrium. \(\varphi\) is the coefficient of the error term and represents the speed of the adjustment, which should be \(-1\, < \varphi \, < 0\). On the other hand, some studies accept values of \(\varphi\) that are lower than −1 and not lower than -2 (Narayan and Smyth, 2006).

Diagnostic tests for the model

The ARDL cointegration requires that Eq. 2 should be normally distributed and serially independent. Therefore, the LM test was used to ensure that the independent variables were not correlated. The Jarque–Bera test was implemented to test the normality of the model. Furthermore, the Breusch–Pagan–Godfrey test was used to test for the existence of heteroscedasticity in the model. In addition, the CUSUM and CUSUM squares were used to test the stability of the model.

Granger causality

The cointegration econometric method analyzes the causal relationships among variables through a joint estimation. The Granger causality test analyzes the direction of causality between variables as a bivariate set Granger (1969). However, the Granger model is unlike other cointegration econometric methods due to the structure of its equations with the limitation of two variables at any given time. In addition, the Granger causality test assesses the direction of causality between two variables in the short-run dynamics. The Granger causality test is represented by Eq. 9 and Eq. 10.

The two equations are estimated to determine the existence of a relationship, as well as the direction of the relationship in the short-run dynamics. The hypotheses for Eq. 9 are set as follows:

\({H}_{1}:{X}{\rm{Granger\; causes\; Y}}\)

For Eq. 10, the hypotheses are as follows:

\({H}_{1}:{Y}{\rm{Granger\; causes\; X}}\)

The test process relies on the acceptance or rejection of the null hypothesis. If the test fails to reject the null hypothesis, there is no causation between the dependent variable and the independent variable. On the other hand, if there is not enough evidence to accept the null hypothesis, the alternative hypothesis is accepted, and we can then indicate the causation of the independent variable with respect to the dependent variable. However, if in both estimations, we accept the alternative hypothesis, there is feedback between the two variables. To ensure the reliability of the test, \({u}_{t}\) and \({\mu }_{t}\) should not be correlated, and they should be white noise. In addition, E[\({u}_{t}{u}_{s}\)] = 0 and E[\({\mu }_{t}{\mu }_{s}\)] = 0, with the conditions that \({t}\,{\ne}\,{j}\), and \(m\) does not exceed the size of the dataset estimated.

Data

This study included the following variables in the model: the Tadawul All Share Index (TASI), the Saudi Arabian GDP, the population size of Saudi Arabia, the Saudi Arabian CPI, oil rent, and 10-year yields of US government bonds as a proxy for the interest rate in Saudi Arabia. The data were obtained from different sources. The TASI data were acquired from the Capital Market Authority’s website via the Open Data Library (2023). Furthermore, the Saudi Arabian GDP was acquired from the SAMA Statistical Report (2023). In addition, the population size of Saudi Arabia and the Saudi Arabian CPI were acquired from the International Financial Statistics (IFS) database on the website of the International Monetary Fund (IMF) (2023). The oil rent was acquired from the World Bank (WB) database (2023). Finally, the interest rate was acquired from the database of the Federal Reserve Bank in St. Louis (2023). Estimated data were generated from the raw data by using the researchers’ calculations. The real term of the GDP per capita has been calculated by dividing the nominal GDP by the CPI and dividing the outcome by population. However, the real interest rate term has been calculated by subtracting the nominal interest rate from inflation, which is the growth of CPI. The final data were the TASI, real GDP per capita, oil rent, and real interest rate. However, the variables were in log form, except for the interest rate, which was the percentage rate. In addition, the data covered the period between 1994 and 2022 to represent the time when most Saudi citizens started transferring their savings to the stock market after Gulf War II. However, the data size is small, relatively speaking, which is an extra reason to apply the ARDL cointegration method to handle this property of the data.

Descriptive data

The descriptive data showed that the measures of the central tendencies of the variables were close to each other, as shown in Table 1. This indicates that the variables were symmetrically disrupted. However, the standard deviations for the levels of all variables were relatively small, except for the interest rate. Furthermore, the skewness was negative for all variables, which means that the variables’ observations were more concentrated on the right side of the distribution. However, the kurtosis was close to the expected value of 3, except for that of the interest rate, which was 4.8782. This value indicates that the interest rate data have an asymmetrical distribution, and this can be addressed with the Jarque–Bera results, which indicate a nonnormal distribution for the interest rate.

The first difference in the descriptive statistics is shown in Table 2. The measures of the central tendencies were close to each other, except for that of the oil variable. The standard deviation was higher than the mean for all variables. However, the skewness was negative, which means that most of the observations were concentrated on the right side, as with the level characteristics of the variables. Furthermore, the kurtosis was close to the expected value of 3, except for the difference in the TASI and interest rate. On the other hand, the Jarque–Bera results showed a nonnormal distribution for the TASI; however, the difference in the interest rate became normally distributed.

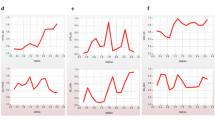

The visualization of the data showed an upward trend for the level of the TASI and income, while there was no trend for the level of oil. On the other hand, the interest rate showed a downward trend, as shown in Fig. 1.

The variables in their level term.

Figure 2 shows that the variables in the first difference fluctuated around the zero line.

Variables in their first difference.

Stationarity test

The stationarity test was conducted with two methods to ensure its reliability, the Augmented Dickey–Fuller (ADF) and Kwiatkowski–Phillips–Schmidt–Shin (KPSS) methods. We chose these two methods because their null hypotheses are opposite to each other. As shown in Table 3, the ADF test showed that all variables were non-stationary in terms of their levels and had no trends, while the same result applied when a trend was imposed, except for the interest rate, which was stationary in this case. For the KPSS test, all variables were non-stationary in terms of their level, except for oil, while the results showed that the interest rate was stationary when a trend was imposed, unlike the rest of the variables. We can see that the interest rate was stationary in both tests when a trend was imposed.

In Table 4, we can see that, in their first difference, all variables were stationary in both tests, and this result applied when a trend was imposed.

The most important consideration when applying a stationarity test for variables before estimating the ARDL cointegration model is ensuring that none of the variables are ranked I(2). From the previous results of the stationarity test, we can surmise that none of the variables were ranked I(2), and one of the variables is stationary in its level term. The ARDL cointegration method is suitable when we are dealing with variables that are in different integration ranks, like I(0) and I(1) (Nkoro and Uko, 2016). However, the data on fucus is of a small size, which is an extra inquiry to proceed toward the ARDL cointegration approach that has better performance over modified OLS, Pesaran and Shin (1999). This indicates the strength of using the ARDL cointegration, since one of the variables was I(0), then the rest that are in different ranks, as well as the data is a short span time series. However, we estimate nonlinear ARDL cointegration, which does not have a requirement for different ranks, but we commit to ensuring the reliability of the model by following the rules of the normal ARDL cointegration model.

Results

The model estimation began with the estimation of Eq. 2 with the decomposition of the positive and negative attributes for oil and the interest rate. The selection of the lag length for the model relied on the Akaike information criterion (AIC) method, since we are dealing with short-span data (Liew, 2004). The AIC suggested that a lag length of two was the optimal lag for the model based on the test value of -20.54569. Furthermore, as shown in Table 5, the NARDL cointegration model’s lag was optimally selected as follows: \(p=1,{k}=2,{q}=1,{m}=2,{r}=0,\,{\rm{and}}{d}=0\); the TASI is the dependent variable, and the rest of the components in the equation are the independent variables.

To estimate the long-run NARDL cointegration model, there is a set of requirements that the estimation of Eq. 2 should fulfill. The model should pass a normality test and be free of serial correlations among the independent variables. In addition, the model should be tested for heteroscedasticity and should be stable over the period of estimation (Pesaran and Pesaran, 1997). Table 6 shows the probability of the normality statistic indicating failure to reject the null hypothesis that the model was normally distributed. Furthermore, the probability for \({\chi }^{2}\) for the serial correlation and heteroscedasticity indicated failure to reject the null hypothesis in both tests, confirming that the model was free of serial correlations and did not exhibit heteroscedasticity.

Figure 3 shows the test of the CUSUM, which fluctuated within a 5% boundary and did not exceed the higher boundary or lower boundary.

Plot of the CUSUM test.

Figure 4 shows the CUSUMSQ test, which fluctuated within the 5% boundary without exceeding the upper boundary or lower boundary. Both tests of stability confirmed that the model did not exhibit any structural breaks over the estimation period.

Plot of the CUSUMSQ test.

NARDL cointegration

The NARDL cointegration model was ready for estimation after the clarification of the requirements from Pesaran and Pesaran (1997). Thus, the model could produce authentic results when determining the existence of relationships among the estimated variables. The existence or non-existence of a long-run relationship among the variables was confirmed based on the bound tests by Pesaran et al. (2001) and Narayan (2005). The estimation of the joint F-statistic was 10.24160 with k = 5, and the lag distribution for the model is (1,2,1,2,0,0). The null hypothesis was tested based on the bound F-test. In our case, the F-statistic of the model was greater than the I(1) F bound statistic at 1% significance, as shown in Table 7, with respect to the critical values from Pesaran et al. (2001) and Narayan (2005). Therefore, there was not enough evidence to accept the null hypothesis, and the alternative hypothesis was accepted, which stated that there was a long-run relationship among the variables.

The model was tested to confirm the existence of a long-run relationship among the variables, and for a cross-check, the dependent variable’s coefficient was tested to ensure that the requirements of Giles (2013) are fulfilled. As shown in Table 8, the coefficient of the dependent variable is negative, which satisfies the first requirement. Furthermore, the t-statistic of the dependent variable was tested based on the critical values of the t-statistic bound from Pesaran et al. (2001) (table CII (iii) case III p. 303) to ensure the significance of the coefficient of the dependent variable. The critical values of the t bound for 1%, 5%, and 10% at k = 5 were specified correspondingly with the lower bound I(0), as well as the upper bound I(1): [-3.43, -4.79], [-2.86, -4.19], and [-2.57, -3.86]. The t-statistic of the TASI was -4.936224, which was greater than the critical value of the t bound for I(1) at 1% significance. Thus, there was not enough evidence to accept the null hypothesis, and the alternative hypothesis was accepted, which means that the coefficient of the TASI fulfilled the requirements of Giles (2013). However, the coefficient of the IN was positive and significant at 1%, which was consistent with our expectation in Eq.1 and Table 8. This result was consistent with the findings of McGowan (2008) and Omar et al. (2022) that income positively impacts the stock market. However, this result contradicted Gnahe (2021), who found that income did not significantly impact the stock market. This difference could be attributed to the structure of the data; in this study, the GDP was transformed into the real GDP per capita, which is a suitable representation of the income, while Gnahe (2021) used the direct form of GDP. However, the positive shock of oil had an insignificant impact on the stock market, as the probability of the coefficient was greater than 5%. This means that the Saudi stock market did not respond to positive changes in the oil market. On the other hand, the coefficient of negative oil shocks had a negative and significant impact on the stock market. Thus, a decrease in oil would cause an increase in the stock market. This can be explained by how companies listed on the stock market rely on inputs related to oil. This result was consistent with Kelikume and Muritala (2019) and Shabbir et al. (2020) in terms of the direction of the impact. However, the impact of oil on the Saudi stock market is asymmetric in the long run, since the positive shock coefficient is insignificant relative to that of the negative shock. This result was consistent with Rahmanto et al. (2016), Alamgir and Amin (2021), and Khamis et al. (2018). Furthermore, the impact of the positive shock of the interest rate on the Saudi stock market was negative and statistically significant. This means that as the interest rate increased, the Saudi stock market decreased. This result was consistent with Alam and Uddin (2009), Uddin and Alam (2010), Bissoon et al. (2016), and Olufisayo (2014). In addition, this result was consistent with Eq. 1, as the expected sign of the interest rate is negative. On the other hand, the coefficient of the negative shock of the interest rate was insignificant, which means that the impact of the interest rate on the Saudi Arabian stock market was asymmetric.

Long-run normalizing coefficients

In the previous section, we discussed the direction of the impact of each independent variable on the dependent variables. However, in this section, we will discuss the size of the impact of each independent variable on the dependent variable. To be able to realize this objective, the long-run coefficients in Table 8 must be transformed into the size of the impacts by dividing each independent long-run coefficient by the dependent lag coefficient. However, prior to this procedure, we needed to ensure that the dependent lag coefficient was statistically significant; it fulfilled the requirements of Giles (2013), allowing the conclusion that the TASI (-1) was statistically significant at 1%. Table 9 shows the long-run normalizing coefficients for the independent variables. Furthermore, a 1% change in income led to a 2.3% change in the stock market. However, the positive attribute of oil was insignificant and had a negative sign, indicating that an increase in oil led to a decrease in the stock market. On the other hand, the negative attribute of oil was significant at 5% and had a negative sign, which means that a decrease in oil led to an increase in the stock market. In addition, a 1% decrease in oil caused a 0.78% increase in the stock market. The positive attribute of the interest rate was significant at the 1% level and had a negative sign, which means that a one-unit increase in the interest rate led to a 39.01% decrease in the stock market. However, the negative attribute of the interest rate was insignificant.

Short-run dynamics

The short-run dynamics showed a significant impact of income and oil on the Saudi Arabian stock market, with their positive and negative attributes. However, the real interest rate had no impact on the Saudi Arabian stock market in the short run due to the limitations of the stock market’s trading tools and the characteristics of the real interest rate (government bonds with a 10-year span). In its first moment, income had a positive impact on the stock market in the short run, which was similar to the long run, as shown in Table 10. However, in the second moment of the short run, income had a negative impact on the stock market, reflecting the uncertainty of the stock market due to investors. In addition, stocks were overpriced due to the increase in demand, causing the price-to-earnings ratio to increase in the stock market, which caused investors to sell their stocks and move to other high-return investments. Furthermore, the income coefficients of the first and second moments were significant at 1%. The positive attribute of oil in the short run had a positive impact, which means that an increase in oil led to a decrease in the value of the stock market. This indicates that companies listed on the stock market most likely depend on oil as an input for their operations, and this stock market is driven by petrochemical companies. However, the negative attribute of oil had a positive impact on the stock market, even though the sign of its coefficient was positive at the 1% level of significance. On the other hand, the second moment of the negative attribute of oil in the short run had a negative impact on the stock market, which means that a decrease in oil caused the Saudi Stock market to decrease as well. This consequence occurs due to the expectation that oil revenue will decrease as a response. Furthermore, a decrease in oil revenue leads to a decrease in income, which forces the demand to decrease and causes a distortion in firms’ profits. In summary, the Saudi stock market is impacted by oil with different attributes in the short run due to the complexity of oil as a source of income and source of energy in the Saudi Arabian economy. However, the impact of oil was asymmetric in the short run; the Wald test rejected the null hypothesis, as there was not enough evidence that the coefficient of the positive attribute of oil was equal to the coefficient of the negative attribute of oil at 5%. Furthermore, the short-run dynamics should have a fast speed of adjustment with a negative sign to ensure the convergence toward the long-run equilibrium. The coefficient of the ECM was negative and significant at 1% with a speed adjustment of 0.9655, which means that any distortion in the model in the short run would be corrected within almost a year.

Granger causality

Granger causality was used to test the causation between the variables in the short-run dynamics. This causality can be one signal in one direction or bidirectional. Table 11 shows that there was causality between the Saudi Arabian stock market and income, with a unidirectional signal being transmitted from the Saudi Arabian stock market toward income. There was unidirectional causality among the real interest rate, oil, and income, with the signal coming from the real interest rate. This provides an important insight into the short-run dynamics of NARDL results, as it shows that there is no short-run impact of the real interest rate on the Saudi Arabian stock market. However, the impact of the real interest rate on the Saudi Arabian stock market is indirect via income and oil in the short-run dynamics.

Conclusions

The Saudi Arabian stock market was examined in this study to analyze the impacts of income, oil, and the interest rate on its performance. Furthermore, the NARDL method was used to analyze the impacts of the long-run and short-run dynamics. In addition, the Granger causality test was implemented to examine the causal relationships among the variables. The results showed that there is a cointegration relationship among the variables in the long-run and short-run dynamics. The impact of an increase in income on the Saudi Arabian stock market is positive and significant in both the long-run and short-run dynamics. This result is consistent with the findings of Omar et al. (2022), McGowan (2008), Yartey (2008), Karacaer and Kapusuzoglu (2010), Gnahe (2021), and Kaustia et al. (2023). Those studies have found that income has a positive impact on the stock market performance, which is similar to this study’s findings. On the other hand, the second moment of the increase in income in the short run has a negative impact, which can be attributed to the uncertainty of the Saudi Arabian stock market and the increase in the price-to-earnings ratio, which motivates investors to move to relatively higher-return investments.

The oil rent variable was decomposed into positive and negative attributes to test the existence of an asymmetrical impact of oil on the Saudi Arabian stock market. The impact of an increase in oil in the long run as a positive attribute is insignificant, while the negative attribute has a significant positive impact. Thus, the asymmetrical impact is proved by the nature of the results, since the coefficient of the negative attribute of oil is the only significant coefficient. This result is consistent with those of Rahmanto et al. (2016), Alamgir and Amin (2021), and Khamis et al. (2018). Furthermore, these results show how the performance of companies listed on the stock market responds positively as the oil decreases, reflecting the impact of the reduction in the raw input cost. On the other hand, the Wald test showed that there is an asymmetric impact of the positive and negative attributes of oil on the Saudi Arabian stock market in the short-run dynamics. The positive attribute of oil has a negative impact on the Saudi Arabian stock market in the short-run dynamics. This behavior reflects the increase in the cost of raw materials associated with oil used by companies listed on the Saudi Arabian stock market. Therefore, the performance of these companies is affected negatively. On the other hand, the negative attribute in the first moment has a positive impact on the Saudi Arabian stock market, in contrast to the second moment. This result is consistent with those of Kelikume and Muritala (2019) and Shabbir et al. (2020) and contradicts those of Samontaray et al. (2014), Tong et al. (2018), Aljifri (2020), and Abdou et al. (2024). This differentiation in the results was due to the decomposition of the oil variable into the positive and negative attributes in our study, which was not part of the previous studies. On the other hand, Amri-Asrami and Jamkhane (2024) have similar findings to the result of this study. However, the oil has a symmetric impact in the long run, unlike our finding, where in the short run, the impact of oil is asymmetric.

The real interest rate variable was also decomposed into positive and negative attributes. This decomposition provided an opportunity to test whether the real interest rate had a symmetrical or asymmetrical impact on the Saudi Arabian stock market. The coefficient of the negative attribute of the real interest rate was insignificant, which proved the existence of an asymmetrical impact. However, this conclusion was withdrawn because the coefficient of the positive attribute of the real interest rate was significant. Furthermore, the impact of the positive attribute of the real interest rate was negative, which is consistent with the findings of Alam and Uddin (2009), Uddin and Alam (2010), Bissoon et al. (2016), and John (2019). On the other hand, this result contradicts that of Eldomiaty et al.’s (2020) findings, where the interest rate has a positive impact on the stock market performance.

The Granger causality test shows that the Saudi Arabian stock market has a unidirectional causal relationship with income, directed from Saudi Arabia to income but not vice versa. The causality test shows that the interest rate has a causal relationship with income and oil, moving from interest to those two variables. However, this result is inconsistent with Sadouni et al.’s (2022) findings. Our result shows no directional or unidirectional causal relationship between oil and the stock market in Saudi Arabia.

The stock market is an important channel through which savers invest to generate returns on their investments. The stability of the stock market attracts more local and foreign investors to invest. However, the Saudi Arabian stock market has expanded over time, with an increase in the number of companies and the sectors into which the industries of those companies are classified, which may have implications for the authorities when ensuring market stability. The authorities should take into consideration that an increase in income will result in increased stock market performance in the short run and the long run, which is an advantage of the stock market. However, the second moment in the short-run dynamics of income has a negative impact; it is important that the authorities implement fiscal policy to control the distortions in income that may accrue due to market inefficiencies. Furthermore, in the short-run dynamics, oil has an asymmetrical impact, which challenges the authorities to find regulations to address this issue. The authorities should advise companies to move toward sustainable resources rather than relying on oil as the source of their energy. The real interest rate has an impact on the stock market only in the long run, with its positive attribute. The impact of the positive attribute of real interest is negative and has a notable impact. The authorities should implement a subsidy program for companies to minimize the impact and motivate continued expansion, which will stabilize the future return expectations of these companies. In addition, the authorities could relax the taxation on raw materials to soften the impact of the real interest rate on companies’ operations.

This study investigated the impacts of different macroeconomic variables on the Saudi Arabian stock market in the form of whole stock market sectors via a stock market index. A future expansion of this study will investigate each stock market sector individually to assess the impacts of these variables on one sector at a time.

Data availability

The data that support the findings of this study are available from the corresponding author upon request.

Notes

EY Global IPO Trends 2022 report.

References

Abdou HA, Elamer AA, Abedin MZ, Bassam A, Ibrahim BA (2024) The impact of oil and global markets on Saudi stock market predictability: a machine learning approach. Energy Econ 132:107416. https://doi.org/10.1016/j.eneco.2024.107416

Alabdulwahab S (2021) The linkage between oil and non-oil GDP in Saudi Arabia. Economies 9(4):202. https://doi.org/10.3390/economies9040202

Alam MM, Uddin MGS (2009) Relationship betweeN Interest Rate and Stock Price: Empirical Evidence from Developed and Developing Countries. Int J Bus Manag 4(3):43–51. https://doi.org/10.5539/ijbm.v4n3p43

Alamgir F, Amin SB (2021) The nexus between oil price and stock market: Evidence from South Asia. Energy Rep. 7:693–703. https://doi.org/10.1016/j.egyr.2021.01.027

Aljifri R (2020) The macroeconomy, oil and the stock market: a multiple equation time series analysis of Saudi Arabia. Economics Discussion Papers em-dp2020-27, Department of Economics, University of Reading. https://www.reading.ac.uk/web/files/economics/emdp202027.pdf

Alkhathlan KA (2013) The nexus between remittance outflows and growth: a study of Saudi Arabia. Econ Model 33(C):695–700. https://doi.org/10.1016/j.econmod.2013.05.010

Almahfouz IA (2020) An Empirical Analysis of the U.S monetary policy impact on the Saudi stock market. Working Paper No. WP/20/14, Working Paper, Saudi Arabian Monetary Authority

Alqattan AA, Alhayky A (2016) Impact of oil prices on stock markets: evidence from Gulf Cooperation Council (GCC) Financial Markets. Amity J Financ 1(1):1–8

Amri-asrami M, Ebadi Jamkhane E (2024) The effect of oil price on stock market performance and petrochemical stock value using NARDL. J Ekon 6(1):25–33. https://doi.org/10.58251/ekonomi.1430729

Apergis N, Miller SM (2008) Do structural oil-market shocks affect stock prices? Economics Working Papers. 200851. https://opencommons.uconn.edu/econ_wpapers/200851

Arouri ME, Rault C (2010) Causal relationships between oil and stock prices: some new evidence from Gulf oil-exporting countries. Int Econ 122:41–56. https://doi.org/10.1016/S2110-7017(13)60029-3

Banerjee A, Dolado JJ, Mestre R (1998) Error-correction mechanism tests for cointegration in a single-equation framework. J Time Ser Anal 19:267–283. https://doi.org/10.1111/1467-9892.00091

Bissoon R, Seetanah B, Bhattu-Babajee R, Gopy-Ramdhany N, Seetah K (2016) Monetary policy impact on stock return: evidence from growing stock markets. Theor Econ Lett 6:1186–1195. https://doi.org/10.4236/tel.2016.65112

Campbell JY (1987) Stock returns and the term structure. J Finan Econ 18(2):373–399. https://doi.org/10.1016/0304-405X(87)90045-6

Castro C, Jiménez-Rodríguez R, Kizys R (2023) Time-varying relation between oil shocks and European Stock Market Returns. J Risk Financ Manag 16:174. https://doi.org/10.3390/jrfm16030174

Economic Reports and Statistics, Saudi Arabia Central Bank (2023) https://www.sama.gov.sa/en-US/EconomicReports/Pages/default.aspx. Accessed in 27/09/2023

Eldomiaty T, Saeed Y, Hammam R, AboulSoud S (2020) The associations between stock prices, inflation rates, interest rates are still persistent: empirical evidence from stock duration model. J Econ Financ Adm Sci 25(49):149–161. https://doi.org/10.1108/JEFAS-10-2018-0105

Federal Reserve Economic Data, Economic Research Division, Federal Reserve Bank of St. Louis. https://fred.stlouisfed.org. Accessed on 27/09/2023

Giles D (2013) Econometrics Beat: Dave Giles’ Blog: ARDL Models—Part 2. https://davegiles.blogspot.com/2013/06/ardl-models-part-ii-bounds-tests.html

Gnahe FE (2021) Do macroeconomic variables impact stock market returns? Evidence from Kazakhstan. Glob J Bus Econ Manag Curr Issues 11(3):255–274. https://doi.org/10.18844/gjbem.v11i3.5620

Granger CW (1969) Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37(3):424–438. https://doi.org/10.2307/1912791

Historical Reports, News and Reports, Saudi Exchange. https://www.saudiexchange.sa/wps/portal/saudiexchange/newsandreports/reports-publications?locale=en. Accessed in 27/09/2023

International Financial Statistic (IFS), International Monetary Fund (IMF). https://www.imf.org/en/Data. Accessed in 27/09/2023

John EI (2019) Effect of macroeconomic variables on stock market performance in Nigeria. J Econ Manag Trade 22(6):1–14. https://doi.org/10.9734/jemt/2019/v22i630110

Karacaer S, Kapusuzoglu A (2010) Investigating causal relations among stock market and macroeconomic variables: evidence from Turkey. Int J Econ Perspect 4(3):501–507

Kaustia M, Conlin A, Luotonen N (2023) What drives stock market participation? The role of institutional, traditional, and behavioral factors. J Bank Financ 148:106743. https://doi.org/10.1016/j.jbankfin.2022.106743

Kelikume I, Muritala O (2019) The impact of changes in oil price on stock market: evidence from Africa. Int J Manag, Econ Soc Sci 8(3):169–194. https://doi.org/10.32327/IJMESS/8.3.2019.11

Khamis R, Anasweh M, Hamdan A (2018) Oil prices and stock market returns in oil exporting countries: evidence from Saudi Arabia. Int J Energy Econ Policy 8(3):301–306. https://econjournals.com/index.php/ijeep/article/view/6541

Kim J (2023) Stock market reaction to US interest rate hike: evidence from an emerging market. Heliyon 9(5):E15758. https://doi.org/10.1016/j.heliyon.2023.e15758

Liew VK (2004) Which lag length selection criteria should we employ? Econ Bull 3(33):1–9

McGowan CB (2008) A study of the relationship between stock market development and economic growth and development for 1994 to 2003. Int Bus Econ Res J 7(2):79–86

Moya-Martínez P, Ferrer-Lapena R, Escribano-Sotos F (2015) Interest rate changes and stock returns in Spain: a wavelet analysis. BRQ Bus Res Q 18(2):95–110. https://doi.org/10.1016/j.brq.2014.07.004

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37:1979–1990. https://doi.org/10.1080/00036840500278103

Narayan PK, Smyth R (2006) What determines migration flows from low‐income to high‐income countries? An empirical investigation of FIJI–U.S. migration 1972–2001. Contemp Econ Policy 24(2):332–342. https://doi.org/10.1093/cep/byj019

Nkoro E, Uko AK (2016) Autoregressive Distributed Lag (ARDL) cointegration technique: application and interpretation. J Stat Econ Methods 5(4):1–3

Ojeyinka T, Aliemhe AE (2023) Disaggregated crude oil prices and stock market behaviour in Nigeria: evidence from sectorial analysis. Econ J Emerg Mark 15(1):42–55. https://doi.org/10.20885/ejem.vol15.iss1.art4

Olufisayo AO (2014) Oil price and stock market: empirical evidence from Nigeria. Eur J Sustain Dev 3(2):33–40. https://doi.org/10.14207/ejsd.2014.v3n2p33

Omar AB, Ali A, Mouneer S, Kouser R, Al-Faryan MAS (2022) Is stock market development sensitive to macroeconomic indicators? A fresh evidence using ARDL bounds testing approach. PLoS ONE 17(10):e0275708. https://doi.org/10.1371/journal.pone.0275708

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16:289–326. https://doi.org/10.1002/jae.616

Pesaran H, Shin Y (1999) An autoregressive distributed lag modeling approach to co-integration analysis. In: Econometrics and economic theory in the 20st century. The Ragnar Frisch Centennial Symposium. Ch. 11. Cambridge University Press, Cambridge

Pesaran MH, Pesaran B (1997) Working with Microfit 4.0: interactive econometric analysis. Oxford University Press, Oxford

Rahmanto, F, Riga, MH and Indriana, V (2016) The effects of crude oil price changes on the Indonesian Stock Market: a sector investigation. Indonesian Capit Market Rev 8(1), Article 2. https://doi.org/10.21002/icmr.v8i1.5442

Sadouni M, Keddam D, Boumimez F (2022) Examining the causal relationship between the Saudi stock market (TASI) and Oil prices. J Quant Econ Stud 8(1):433–446. https://www.asjp.cerist.dz/en/article/194969

Samontaray DP, Nugali S, Sasidhar B (2014) A Study of the Effect of Macroeconomic Variables on Stock Market: Saudi Perspective. International Journal of Financial Research 5(2):120–127

Schorderet Y (2001) Revisiting Okun’s Law: an hysteretic perspective. University of California San Diego, San Diego

Shabbir A, Kousar S, Batool SA (2020) Impact of gold and oil prices on the stock market in Pakistan. J Econ Financ Adm Sci 25(50):279–294. https://doi.org/10.1108/JEFAS-04-2019-0053

Shin Y, Yu B, Greenwood-Nimmo M (2014) Modeling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In: Horrace WC, Sickles RC (eds.) Festschrift in honor of Peter Schmidt: econometric methods and applications. Springer Science and Business Media, New York, pp. 281–314

Tong s, Baslom MMM, Alsharif HZH (2018) Investigating volatility in Saudi Arabia crude oil prices and its impact on oil stock market. Int J Energy Econ Policy 8(4):338–346. https://econjournals.com/index.php/ijeep/article/view/6849

Uddin MGS, Alam MM (2010) The impacts of interest rate on stock market: empirical evidence from Dhaka Stock Exchange. South Asian J Manag Sci 4(1):21–30

World Bank Open Data. https://data.worldbank.org/. Accessed on 27/09/2023

Yartey CA (2008) The Determinants of Stock Market Development in Emerging Economies: Is South Africa Different? International Monetary Fund (IMF), Working Papers, African Department, 2008(032), WP/08/32. https://doi.org/10.5089/9781451868944.001

Acknowledgements

The author acknowledges the Deanship of Scientific Research at King Faisal University for the financial support under Ambitious Researcher (Grant No. GrantA209).

Author information

Authors and Affiliations

Contributions

The author has developed and written the manuscript of this study.

Corresponding author

Ethics declarations

Competing interests

The author declares no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

This article does not include any studies involving human participants conducted by the Author.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Alabdulwahab, S. The influence of changes in income, oil, and the interest rate on the Saudi Arabian stock market. Humanit Soc Sci Commun 12, 888 (2025). https://doi.org/10.1057/s41599-025-05277-x

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-05277-x