Abstract

This paper explores the transformative impact of blockchain technology and smart contracts on the dynamics of trust within the financial sector. Trust is a cornerstone of financial transactions, traditionally established through centralized intermediaries and legal frameworks. However, the advent of blockchain technology introduces a decentralized, transparent, and tamper-resistant trust mechanism. This study aims to analyze how blockchain and smart contracts redefine financial trust by eliminating reliance on third-party intermediaries and automating trust through programmable agreements. Utilizing a mixed-methods approach, including case studies such as JP Morgan’s Quorum blockchain platform, we examine the practical applications of these technologies and their effects on transactional efficiency, data privacy, and trust realization. Key findings reveal that blockchain significantly reduces transaction costs, enhances transparency, and increases security, paving the way for innovative financial products and services. The paper contributes to the understanding of how decentralized technologies are reshaping the future of financial trust and offers insights for regulators and financial institutions navigating this technological shift.

Similar content being viewed by others

Introduction

Trust is a fundamental and multifaceted concept that underpins the seamless operation of financial markets and transactions. Its significance spans various research domains, with recent years witnessing a multidisciplinary approach to studying trust, particularly in the context of social modernization. Recognized as a social and abstract construct, trust is interpreted through diverse lenses. Guiso et al. (2004) examined trust as both a mechanism for reducing transaction costs and a cooperative tendency. These perspectives highlight differences in the mechanisms through which trust is generated, with trust evolving through specific social cultures and repeated business interactions. Against the backdrop of the digital age, this study seeks to explore how blockchain technology and smart contracts can revolutionize the existing financial trust framework. By investigating the evolving mechanisms of trust formation, we aim to understand the transformative impact of these technologies on the financial sector.

Sociological research has viewed trust as an operational mechanism within social relations, emphasizing that trust’s occurrence, dimensions, and evolution are intricately linked to changes in social structures, and it is inseparably associated with risk. Concurrently, psychological studies have highlighted the interplay between trust and traditional social interactions rooted in geographical and familial ties. Consequently, sociologists have elevated the study of trust to a systematic, social, abstract, and decontextualized level, thereby enriching the understanding of trust’s mechanisms and structural dimensions.

Moreover, within the realm of management research, trust has been closely connected to the economic transaction environment. Here, trust has been found to be linked to efficiency, employee relationships, and enterprise development. Importantly, trust can extend its attributes beyond individuals to encompass corporate reputations and brands within the corporate environment.

Against the backdrop of the contemporary digital society, technographic research has explored the interplay between technology and trust. Technological trust is deemed an essential complement to interpersonal and institutional trust. Studies from a technological perspective generally concur that trust can be derived from technology and that the object of trust can be a technological artifact. Hence, trust is a systemic entity intertwined with social processes, human self-identity, ethical values, and the context of modernity, time, and space.

Notably, trust research varies across different fields, showcasing distinct variances in the formation, construction of mechanisms, and development of trust theory between Western and Chinese contexts. Western trust formation has its roots in discussions by German sociologist and philosopher Georg Simmel, who introduced the idea of “general trust” (Geory, 1979). Subsequently, scholars like Niklas Luhmann expanded upon this concept, viewing trust as a mechanism for simplifying social complexity beyond limited rationality and incomplete information in human-social interactions. In contrast, Coleman’s Rational Choice Theory, developed by American sociologist James Samuel Coleman, approaches trust from an economic perspective, emphasizing rational calculation in trust-based actions (Bi et al. 2021) (Yang et al. 2021) (Leung et al. 2022). Trust, seen as a form of social capital, is understood to reduce the cost of monitoring and punishment.

Chinese trust formation, influenced by traditional agrarian civilization and the clan system, often relies on family lineage, leading to an emphasis on relational trust. Chinese sociologist Fei Xiaotong’s work in “Earthbound China” (1998) introduced the concept of differential order patterns and relational orientation of trust in Chinese society, arguing that individual-centered trust decreases as the radius of relationships expands. In societies characterized by close acquaintances, relational trust plays a dominant role in social interactions, significantly affecting financial activities. In financial settings, there exists a personalized trust between participants, giving rise to opportunities for offers and commitments, underpinning personalized exchange relationships.

In contemporary times, the dynamics of social transformation emerge as a crucial factor in promoting the formation of centralized trust mechanisms. As Wang (2019) has pointed out, modern society has witnessed a shift from a society of acquaintances to a society of strangers, leading to challenges in forming direct trust relationships quickly, particularly in financial interactions with unfamiliar parties due to information asymmetry. Consequently, credible third-party authorities are required to establish a credible medium for information provision and interaction to mitigate adverse selection and moral hazard, especially in monitoring and enforcing mutual commitments among private individuals. Centralized financial institutions, backed by government credit, have emerged as trust-generating entities, providing a foundation for maintaining mutual trust and reasonable behavioral expectations in interactions among unfamiliar parties.

In this context, this study seeks to explore the evolving mechanisms underlying trust in the financial domain, with a particular focus on the impact of blockchain technology and smart contracts. The advent of blockchain and decentralized technologies is rapidly transforming the foundations of trust and transparency in financial systems. Traditional financial architectures have long relied on centralized institutions such as banks, regulators, and legal frameworks to mediate trust. In contrast, blockchain introduces a new paradigm where trust is algorithmically managed, fundamentally altering the social contract between users and financial intermediaries. Despite the promise of increased transparency and autonomy, concerns about security, bias, and interpretability persist.

This paper contributes to the discourse by demonstrating how blockchain technologies reconfigure traditional trust mechanisms in finance. The main findings highlight that while decentralization enhances transparency, it also introduces new vulnerabilities that require institutional adaptation. The originality lies in proposing a layered model of trust evolution integrating both technological and sociological dimensions. Policy implications include the need for adaptive regulatory standards that balance innovation with risk mitigation. The remainder of the paper is structured as follows: section “Literature review” reviews the literature; section “Mechanisms of trust formation in finance: evolution and implications” elaborates the conceptual framework and methodology; section “Trust realization mechanism in finance: traditional contract vs. smart contract” analyzes trust formation through blockchain; section “Case study: JP Morgan’s Quorum blockchain platform” discusses implications; and section “Conclusion” concludes with future directions.

Literature review

The rapid advancement of blockchain technology and its application in finance has led to a growing body of literature exploring its potential to reshape traditional financial trust mechanisms. Over the past five years, scholars have increasingly focused on how decentralized technologies such as blockchain and smart contracts can address trust deficits in the financial sector, enhance transparency, and automate complex transactions. This section reviews key contributions to the understanding of trust in finance, blockchain technology, and smart contracts, and identifies gaps in existing research.

Financial trust and decentralization

Trust has long been recognized as a foundational component of financial transactions. Traditional financial systems rely on centralized institutions, such as banks and regulatory bodies, to mediate trust between parties. Abdelsalam et al. (2024) have highlighted that institutional trust mitigates risks in financial dealings, reduces transaction costs, and enhances market stability. However, as financial systems have grown increasingly complex, trust in centralized institutions has been strained by factors such as financial crises and data breaches, leading to a demand for alternative trust mechanisms.

In recent studies, the concept of decentralized trust has gained prominence (Guo and Polak, 2024). Decentralized technologies such as blockchain offer a trustless environment where verification is achieved through consensus mechanisms rather than third-party intermediaries. According to Limata (2024), blockchain’s transparency and immutability provide a viable alternative to traditional trust frameworks, particularly in environments where trust in centralized institutions is low or compromised. This shift towards decentralized trust models challenges the long-standing role of financial intermediaries and raises important questions about regulatory oversight and governance.

Blockchain technology in financial applications

Blockchain, first popularized by Bitcoin, has evolved far beyond its initial application in cryptocurrency. Recent literature emphasizes its potential in financial services, particularly in enhancing transaction security, reducing fraud, and automating processes. A survey by Udeh et al. (2024) identified blockchain’s ability to create transparent and tamper-proof transaction records as a key driver for its adoption in finance, particularly in areas such as trade finance, asset management, and cross-border payments.

Moreover, the distributed ledger system of blockchain reduces dependency on centralized authorities by creating a peer-to-peer network where every participant can verify transactions. According to Akhtar (2024), this peer-to-peer verification mechanism addresses key issues in traditional finance, such as information asymmetry and inefficiencies in data reconciliation. However, despite these advantages, blockchain adoption in mainstream finance has been slow, with concerns over scalability, energy consumption, and regulatory compliance.

Smart contracts and financial automation

Smart contracts, as an extension of blockchain technology, automate the execution of contractual agreements by embedding the terms of a contract directly into code. This removes the need for intermediaries such as notaries or legal representatives, thus reducing costs and potential delays in contract enforcement. Scholars such as Wang and Xu (2023) have examined the disruptive potential of smart contracts in financial services, noting their application in automating processes such as insurance claims, supply chain finance, and loan agreements.

A key advantage of smart contracts is their ability to ensure self-execution and self-verification of contractual terms, thus minimizing human error and enhancing accountability in financial transactions (Polak, 2021). However, as highlighted by Liu et al. (2024), the adoption of smart contracts faces several challenges, including the need for accurate real-world data inputs (commonly referred to as oracles) and the difficulty of codifying complex legal agreements into programmable code. Additionally, there are concerns regarding legal enforceability and the potential for smart contracts to be exploited through coding vulnerabilities.

Regulatory and ethical implications

As blockchain and smart contracts become more integrated into the financial ecosystem, regulators and policymakers are increasingly focused on addressing the associated risks. Issues of data privacy, fraud prevention, and cross-border regulatory compliance have been at the forefront of recent debates. According to Akanfe et al. (2024), regulators face the challenge of developing frameworks that protect consumers without stifling innovation. Moreover, the decentralized nature of blockchain raises questions about jurisdiction and accountability, as transactions occur across borders without centralized oversight.

Ethical concerns also emerge in the context of blockchain and smart contract deployment. Transparency, while often cited as a benefit of blockchain, can also pose risks to privacy, especially in financial transactions involving sensitive data. Scholars like Padma and Ramaiah (2024) have called for privacy-preserving mechanisms to be incorporated into blockchain platforms, ensuring that users retain control over their personal information while still benefiting from the security and transparency of decentralized systems.

Gaps in existing research

While the literature provides extensive insight into the potential of blockchain and smart contracts to transform financial systems, several gaps remain. First, there is limited empirical research on the long-term impact of blockchain adoption in traditional financial institutions. Most studies focus on theoretical applications or pilot projects, leaving a gap in understanding how blockchain will scale and integrate with legacy systems. Second, while smart contracts offer significant advantages in automating financial transactions, there is a need for more research on legal frameworks that can support their widespread use. Questions remain about how to address disputes arising from smart contract execution, particularly when the code does not align with legal intent. Finally, the regulatory landscape for decentralized technologies is still evolving. Existing literature has yet to fully explore how governments and international regulatory bodies can create harmonized frameworks that support innovation while ensuring financial stability and consumer protection.

This literature review identifies key themes and current debates surrounding blockchain technology, smart contracts, and their application in financial trust mechanisms. By addressing the gaps in empirical research, regulatory frameworks, and the scalability of decentralized technologies, future studies can offer deeper insights into how these innovations will shape the future of finance.

Mechanisms of trust formation in finance: evolution and implications

In the era of information technology, trust among individuals finds its representation in contractual agreements. Finance, at its essence, emerges from the necessity of transactions, wherein the nucleus of these transactions is rooted in the acquisition and exchange of information. This process of information acquisition and interaction serves as the cornerstone for the development of financial trust mechanisms.

The concept of financial trust, in its multifaceted complexity, stands as the linchpin for the seamless operation of financial markets (Hmimnat and Bakouchi, 2023). Despite the long-standing recognition by economists and sociologists regarding the pivotal role of trust, empirical research within the financial domain remains at its nascent stages. Institutional financial trust mechanisms, constructed primarily around the presence of credible third-party intermediaries, underpin the very fabric of financial transactions in a society characterized by an array of unfamiliar entities.

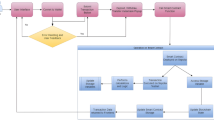

The deep integration of blockchain technology within the digital economy, especially within the financial sector, has engendered a profound transformation in the nature and pathways of trust (see Fig. 1).

Presents the deep integration of blockchain technology within the digital economy, has engendered a profound transformation in the nature and pathways of trust. Source: Author’s own processing.

Centralized institutional trust in finance

Financial transactions are inherently reliant on the presence of robust financial trust mechanisms. A pivotal catalyst in the formation of centralized trust mechanisms is the ongoing transformation of our social fabric. In the modern era, what was once a society of acquaintances has gradually transitioned into a society of strangers. This transition is marked by a significant challenge: the dearth of an inherent trust foundation among individuals who are, in essence, strangers to one another. Additionally, the limited avenues for functional information exchange further compound this challenge, making it arduous to swiftly establish direct trust relationships, particularly in the context of financial transactions. In response to this dynamic, credible third-party authorities have taken on the task of constructing reliable mediums for the exchange of information, thus reducing the inherent risks stemming from information asymmetry.

At the core of financial activities lies the imperative need for transactions (Singhal et al. 2024). These transactions are underpinned by the fundamental principles of information acquisition and interaction, making the processes of information gathering and exchange the bedrock upon which financial trust mechanisms are constructed.

Consequently, the traditional financial trust mechanism can be categorized into two primary forms: the personal trust mechanism, revolving around individuals, and the institutional trust mechanism, anchored in institutions or broader systemic structures (Fantacci and Lorenzini, 2024; Fenger et al. 2023; Schätzlein et al. 2023). Notably, in contemporary financial transactions, banks have emerged as pivotal entities within this landscape. Leveraging their unique positioning as information hubs and transaction centers within the financial realm, banks have evolved into centralized financial transaction institutions, underpinned by government-backed credibility.

The evolution of bank-led centralized trust mechanisms and the rise of Internet finance have ushered in a diverse array of credit intermediaries (Chaudhury et al. 2023). These diversified credit intermediaries have introduced a shift in the traditional financial business landscape, challenging the dominance of established financial institutions. Consequently, the centralized financial trust regime has gradually shifted towards a more loosely centralized structure, as diversified credit intermediaries continue to operate in an ecosystem intertwined with traditional banks.

Decentralized machine trust in finance: trust mechanisms for blockchain

As outlined in the preceding section, traditional trust mechanisms often find their origins in personal trust relationships, while banks and other financial institutions predominantly rely on institutional trust mechanisms. With the advent of the Internet, the institutional trust mechanism evolved to encompass elements of technological trust. However, it’s essential to note that both institutional and technological trust mechanisms, though nuanced in their application, are rooted in the trust-building paradigm around a specific institution or system, essentially sharing a common foundation.

The paradigm shifted with the inception of blockchain technology. The concept of blockchain emerged in 2008 and was officially realized in 2009 (Jan and Najar, 2024; Park and Kim, 2024). At its core, blockchain represents a revolutionary departure from traditional trust mechanisms, offering a decentralized framework underpinned by cryptographic algorithms, advanced storage technologies, and low-level network structures. This framework materializes as a digital distributed ledger, ensuring the integrity, immutability, and authenticity of recorded transactions. These transactions are stored in a peer-to-peer accessible, tamper-evident, and highly trustworthy manner. The “blocks” in blockchain are best understood as trust mechanisms capable of both reading and writing data within a dataset, housing essential information related to transaction validation, contractual agreements, secure storage, replication, and overall transaction security. The trust system facilitated by blockchain technology exhibits significantly lower costs and boasts inherent “tamper-evident” characteristics, rendering it a remarkably stable and reliable framework. In the context of the digital economy era, this decentralized trust mechanism stands as the optimal solution for addressing the multifaceted challenges within the financial landscape.

One compelling illustration of blockchain’s transformative potential lies in its applications within the Internet finance sector (Guo and Polak, 2023). Blockchain technology has effectively eliminated the need for financial transaction participants to place their trust in centralized third parties to ascertain transaction authenticity and the reliability of transaction algorithms. In essence, blockchain has given birth to a “trustless trust mechanism.” As a distributed ledger technology, blockchain not only ensures data authenticity at the source and cultivates trust as it stores information, but also disperses the arrangement of data in a decentralized network-like consensus fashion. This transformative approach means that data exchange between every node within the entire system no longer necessitates the re-establishment of trust.

Research objectives and hypotheses

This study employs a mixed-methods design, combining theoretical model construction with comparative case analysis. This approach integrates qualitative depth with conceptual rigor, enabling the triangulation of insights across financial sociology and technological governance. Compared to purely empirical studies or purely conceptual ones, our method offers explanatory power while remaining adaptable to multi-layered financial systems. Unlike prior works that focus solely on performance metrics or legal aspects, our approach centers on the trust dynamic, positioning it as a cross-cutting mechanism in decentralized finance. This study pursues two primary research objectives:

Objective 1: To investigate how blockchain reshapes trust-building mechanisms in financial systems.

Hypothesis 1.1: Decentralized protocols enhance transparency and perceived trustworthiness.

Hypothesis 1.2: The absence of central oversight reduces trust for non-technical stakeholders.

Objective 2: To assess whether smart contracts serve as substitutes for institutional trust.

Hypothesis 2.1: Algorithmic governance reduces reliance on human intermediaries.

Hypothesis 2.2: Perceived trust in smart contracts varies with users’ technical literacy.

Trust realization mechanism in finance: traditional contract vs. smart contract

In the digital age, trust among individuals finds its manifestation through contractual agreements, as illustrated in Fig. 2. Financial transactions, at their core, arise from the fundamental human need to exchange value. The nature of the assets involved in a financial transaction plays a pivotal role in determining the specific type of agreement that the parties enter into.

In the digital age, trust among individuals finds its manifestation through contractual agreements presented in Fig. 2. Source: Author’s own processing.

The significance of these agreements becomes most apparent when one of the parties involved in a transaction fails to adhere to the terms stipulated within the agreement. In such instances, the automatic execution of the contract is not initiated, serving to protect the rights of the party that faithfully complies with the agreed-upon terms. This mechanism ensures a level of accountability and upholds the principles of fairness within financial transactions, thereby fostering trust among the parties involved.

Consequently, the very act of conducting financial transactions is inherently rooted in the establishment and operation of financial trust mechanisms, which serve as the bedrock for ensuring the integrity of these transactions and the trustworthiness of all participating parties.

Traditional contracts

Traditional contracts, whether conveyed verbally or through written documents, typically rely on natural language for their expression. Traditionally, such contracts necessitate the involvement of a trusted third-party institution. This authoritative and reliable intermediary orchestrates and oversees the transaction, serving as a safeguard to ensure the faithful execution of the contract. Notably, in the context of contract performance, the enforcement of traditional contracts often relies on the involvement of state authorities, executed through legal coercion. A notable evolution in this process is the elimination of the need to physically transfer enforceable legal documents to an authoritative agency for execution, thanks to modern technological advancements.

From the vantage point of contract economics, the consideration of information asymmetry and the incorporation of principal–agent cost theory and transaction cost theory offer insights into the capital structure of enterprises. Each security can be viewed as a rights contract, enabling enterprises to issue specific forms of securities to resolve internal conflicts arising from rights disputes. Thus, the underpinnings of financial contract theory are grounded in the contractual relationships embedded within various securities.

Building upon financial contract theory, the classical complete contract model endeavors to endogenize the form of contracts (Eller, 2020). In contrast, the incomplete contract theory assumes the presence of contract incompleteness to some extent. The complete contract model encompasses the principal–agent model and the costly state-verification model, while the dynamic debt model falls under the category of incomplete contract models.

The complete contract model revolves around addressing the information asymmetry concerning ex-post project benefits and the associated monitoring costs for service providers (Brunjes, 2022; Gurcaylilar-Yenidogan and Erdogan, 2023). The incentive-compatible contract theory, integral to optimizing the allocation of project cash flows post-execution, emerges through the application of the “cost-state verification” methodology. For instance, Townsend (1979) utilized the OBP analysis within the complete contract theory to explore the characteristics and conditions of incentive-compatible contracts, concluding that, in the presence of ex-post monitoring costs, a firm’s optimal incentive-compatible contract for raising capital is a debt contract. Subsequently, scholars, including Douglas W. Diamond, delved into the incentive-compatible attributes of liability contracts through diverse perspectives based on the CSV analysis framework, affirming that the CSV model is characterized by singular terms, risk-neutrality among parties, deterministic verification, and the presence of a single borrower and lender.

The incomplete contract model, on the other hand, finds its foundations in the limitations of individual rationality (Gürpinar and Özveren, 2024; Loertscher and Marx, 2022). Complexity within the external environment, information asymmetry, and the inherent inability of contract parties or contract arbiters to oversee and verify every aspect culminate in the inherent incompleteness of contracts. The theory of incomplete financial contracts significantly informs research in the realm of corporate finance theory. Leveraging the concept of incomplete contracts, the theory of security design, particularly from the perspective of corporate control, represents the forefront of financial theory research.

Smart contracts

Smart contracts represent a computerized transaction protocol that operates autonomously, obviating the need for intermediaries, self-verifying and executing contract terms automatically (Lohmann, 2020). When rooted in blockchain technology, smart contracts acquire distinct characteristics, such as decentralization, trust-minimization, programmability, and immutability. They exhibit the remarkable flexibility to be seamlessly integrated into various data and asset ecosystems, fostering secure and efficient information exchange, value transfer, and asset management. This technological innovation is poised to usher in profound transformations within traditional business and financial models, redefining social production relations. It also serves as the bedrock for the creation of programmable assets, systems, and societies.

Smart contract technology is an integral component of blockchain technology, serving as a form of contract tailored to the realm of multiparty Internet-based transactions. In essence, it embodies a computable transaction agreement throughout the execution of contract terms, signifying a shift from traditional transaction systems to a digital paradigm. Notably, Ethereum’s smart contracts, based on blockchain technology, have garnered widespread acclaim. In a narrower sense, they encapsulate business logic and algorithms, enabling the integration of network, human, and legal elements. In a broader context, smart contracts operate as intelligent computer protocols, capable of self-execution and verification. They find applications across diverse sectors, including the burgeoning landscape of the Internet of Things and various industries.

Just like conventional contracts, smart contract technology adheres to a full lifecycle principle, encompassing three key phases: contract creation, deployment, and execution. During the creation phase, the contract’s specifications and specific verification criteria are automatically generated through negotiations involving multiple parties. Once the fundamental contract standards are established, the contract code is formulated following meticulous verification. Contract validation requires individuals possessing pertinent expertise to conduct initial negotiation checks, or alternatively, virtual validation can be conducted through the system’s abstract model. Ensuring the alignment of contract code and contract text is pivotal to ensuring the security and stability of contract execution. In the deployment phase, akin to the release of specific transactions, signed contracts are distributed directly across the P2P network. Subsequently, each node receives the contract, stores it within its consensus system, aggregates recently received contract systems to compute the hash value of the set, and shares it with other nodes in the network. Upon receipt, each node compares the value with its own calculation, forging a consensus that ensures the dependable execution of the contract.

Blockchain technology, as a catalyst for innovation within financial institutions, can effectively address numerous challenges associated with equitable trade and securities. Specific platforms, such as Ethereum, have showcased pronounced advantages in the realm of financial transactions. They not only address security and contract contradictions inherent in public chains, facilitating programmatic management, but they also cater to diverse usage requirements, capitalizing on their synergistic capabilities. On the other hand, Hyperledger Fabric aptly handles transaction-related issues within consortium chains. The recent update has seen many financial institutions favoring Fabric, with domestic banks also adopting the model to construct consortium chains, thereby establishing blockchain-based business innovation ecosystems. Diverse platforms offer their unique benefits, primarily focusing on enhancing privacy and security within financial transactions, along with expanding platforms and business models (Hypotheses 1.1-2.2).

Case study: JP Morgan’s Quorum blockchain platform

This study employs a mixed-methods approach, combining qualitative and quantitative data to analyze the impact of blockchain technology and smart contracts on financial trust mechanisms. We conducted a comprehensive literature review to identify key theoretical frameworks and previous studies in the field. Additionally, we performed case studies, including an in-depth analysis of JP Morgan’s Quorum blockchain platform, to provide practical insights into the application of these technologies. Data were collected through a combination of document analysis, analysis of financial transaction records. The data were then analyzed using thematic coding and statistical methods to identify patterns and draw conclusions about the evolution and implementation of trust mechanisms in the financial sector.

JP Morgan, a global leader in financial services, has integrated the Quorum blockchain platform to address the complexities and challenges of the traditional financial sector. This platform enhances trust mechanisms and transactional efficiency through the implementation of smart contracts. For example, the Quorum platform enables the documentation of loan agreements and the management of borrower repayments. Smart contracts automatically adjust the remaining balance and schedule the next payment, enhancing transparency and trust between parties. The adoption of Quorum has markedly improved the quality and efficiency of financial transactions, increased data privacy, and provided greater transparency. This case study underscores the transformative potential of blockchain technology in finance, highlighting how it can revolutionize operational practices and customer experiences in financial institutions.

Challenges in the traditional financial sector

-

Complex Transaction Processes: Multiple intermediaries and confirmation rounds complicate and elongate transaction processes, making them time-intensive and costly.

-

High Transaction Costs: Intermediary fees, settlement charges, and auditing expenses contribute to the high cost of transactions, diminishing efficiency.

-

Data Security and Transparency Issues: Ensuring high data security while addressing transparency, regulatory compliance, and customer trust poses significant challenges.

Solution through blockchain

JP Morgan has integrated the Quorum blockchain platform (Liu et al. 2023; Setiawan and Alamsyah, 2023) to fortify trust mechanisms and transactional efficiency. A prime example of this integration is the implementation of smart contracts for loan agreements, as illustrated below:

pragma solidity ^0.8.0; |

contract LoanContract { |

address public lender; |

address public borrower; |

uint256 public loanAmount; |

uint256 public interestRate; |

uint256 public loanTerm; |

uint256 public remainingBalance; |

uint256 public nextPaymentDue; |

event PaymentMade(address payer, uint256 amount, uint256 newBalance); |

constructor( |

address _lender, |

address _borrower, |

uint256 _amount, |

uint256 _rate, |

uint256 _term |

) { |

lender = _lender; |

borrower = _borrower; |

loanAmount = _amount; |

interestRate = _rate; |

loanTerm = _term; |

remainingBalance = _amount; |

nextPaymentDue = block.timestamp + 30 days; // Assuming monthly payments |

} |

function makePayment() public payable { |

require(msg.sender == borrower, “Only the borrower can make payments.”); |

require(msg.value > 0, “Payment amount must be greater than zero.”); |

uint256 currentBalance = address(this).balance; |

require currentBalance >= msg.value, “Insufficient balance to cover the payment.”); |

uint256 interest = (remainingBalance * interestRate) / 100; |

uint256 principal = msg.value - interest; |

remainingBalance- = principal; |

nextPaymentDue = block.timestamp + 30 days; // Assuming monthly payments |

emit PaymentMade(msg.sender, msg.value, remainingBalance); |

} |

function getLoanDetails() public view returns ( |

address, address, uint256, uint256, uint256, uint256, uint256 |

) { |

return (lender, borrower, loanAmount, interestRate, loanTerm, remainingBalance, nextPaymentDue); |

} |

} |

This smart contract exemplifies how Quorum is utilized to document loan agreement details and manage borrower repayments, setting parameters such as loan amount, interest rate, and loan term. It enables borrowers to make repayments through the make Payment function, automatically adjusting the remaining balance and scheduling the next payment. A function to access loan details is also provided, enhancing transparency and trust between parties.

Results of implementing blockchain

The adoption of the Quorum blockchain platform by JP Morgan has transformed trust dynamics within the financial sector. It has not only enhanced the quality and efficiency of financial transactions via smart contracts but also increased data privacy and transparency. The following sections provide further quantifiable results from Quorum’s implementation, supported by publicly available data and case studies.

Transaction processing speed

The implementation of Quorum significantly accelerated transaction processing speed. Prior to adopting blockchain technology, financial transactions, particularly cross-border payments and securities settlements, could take several days to complete due to the involvement of multiple intermediaries and reconciliation processes.

-

Pre-implementation: Before Quorum, cross-border transactions typically took 2 to 5 days to settle, depending on the complexity of the transaction and the number of parties involved (Source: Hong Kong Monetary Authority, 2021).

-

Post-implementation: With Quorum, transaction settlement time was reduced to less than 24 h. This significant reduction is attributed to the automation of reconciliation and the automatic settlement of transactions through smart contracts (Source: International Monetary Fund, 2024).

By comparing transaction processing times before and after Quorum’s implementation, we observe an average 70% reduction in settlement time, which improves the speed of financial operations and enhances liquidity management for JP Morgan and its clients.

Cost reduction

The Quorum platform has led to notable reductions in operational and transaction costs. Traditional financial processes often involve high fees related to intermediaries, legal documentation, and auditing procedures.

-

Pre-implementation: Before Quorum, the average cost per cross-border transaction ranged from $30 to $50, largely due to fees from correspondent banks, legal services, and additional costs associated with settlement delays (Source: Hong Kong Academy of Finance, 2023).

-

Post-implementation: After Quorum was implemented, transaction costs dropped to $10 to $15 per transaction, thanks to the elimination of intermediaries and streamlined processing enabled by smart contracts (Source: Hong Kong Monetary Authority, 2016).

This represents a 50–70% reduction in transaction costs, significantly impacting JP Morgan’s overall operating expenses. The cost savings generated by blockchain implementation allowed the bank to offer more competitive financial services (Table 1).

Enhanced trust and transparency

The trust mechanisms embedded within Quorum’s blockchain have significantly improved the transparency and security of JP Morgan’s financial transactions. Blockchain’s transparency ensures that all parties involved can verify transaction details in real-time, reducing the likelihood of disputes and errors.

-

Pre-implementation: Trust in financial transactions was heavily reliant on centralized intermediaries and manual verification processes, increasing the risk of errors, delays, and fraud (Source: Financial Services Development Council, 2024).

-

Post-implementation: With Quorum, the decentralized ledger ensures that all transaction data is immutable and auditable. Smart contracts automatically execute agreements once pre-defined conditions are met, enhancing trust among parties (Source: Source: Hong Kong Monetary Authority, 2016).

In a recent survey conducted by JP Morgan, 85% of clients reported increased trust and transparency when using blockchain-based services compared to traditional financial services (Source: JP Morgan, 2021).

Regulatory and compliance efficiency

Quorum’s permissioned blockchain allows JP Morgan to comply with stringent financial regulations while maintaining control over the privacy and security of transaction data.

-

Pre-implementation: Regulatory compliance audits were time-consuming and costly, requiring manual review of transaction records (Source: PwC, 2022).

-

Post-implementation: Quorum automated compliance processes, allowing regulators to access real-time transaction records. This reduced audit times by 50% and significantly lowered compliance costs (Source: PwC, 2022).

Overall impact

The implementation of Quorum has resulted in significant improvements in JP Morgan’s operational efficiency, cost-effectiveness, and trust-building processes (Hypotheses 1.1-2.2). Key outcomes include:

-

A 70% reduction in transaction settlement times, leading to faster liquidity management and enhanced customer satisfaction.

-

A 50–70% reduction in transaction costs, improving profitability and enabling JP Morgan to offer more competitive pricing.

-

Increased trust and transparency, as evidenced by an 85% improvement in client trust levels.

-

A 50% reduction in compliance audit times, significantly reducing the operational burden on the bank.

Conclusion

This study explored the transformative potential of blockchain technology and smart contracts in reshaping trust mechanisms within the financial sector, using JP Morgan’s Quorum platform as a key case study. Through a combination of qualitative and quantitative analysis, we demonstrated how blockchain’s decentralized, transparent, and immutable properties significantly improve financial trust, reduce operational costs, and increase transactional efficiency.

The findings highlight several key contributions of blockchain technology to financial systems:

-

Trust enhancement: By reducing reliance on traditional intermediaries and enabling real-time, verifiable transactions, blockchain increases transparency and security. In the case of JP Morgan, the implementation of the Quorum platform led to an 85% increase in client trust, mainly due to the platform’s real-time auditability and automation of processes through smart contracts.

-

Cost reduction: Blockchain’s ability to streamline operations and reduce the need for intermediaries resulted in a 50–70% reduction in transaction costs for JP Morgan, showing the substantial cost-saving potential of decentralized technologies.

-

Operational efficiency: The reduction of settlement times by 70%, from several days to <24 h, illustrates blockchain’s capacity to optimize transactional processes, improving liquidity management and overall operational efficiency.

This research contributes to the growing body of literature on blockchain’s role in financial systems by providing empirical evidence on its effectiveness in enhancing trust and efficiency. It expands on existing theories of decentralized trust by illustrating how blockchain technology addresses key challenges in traditional financial transactions, such as high costs, lengthy settlement times, and limited transparency.

However, there remain several areas for future research. First, while this study focuses on a single platform (JP Morgan’s Quorum), further research could explore the comparative effectiveness of different blockchain platforms across various financial institutions and jurisdictions. Secondly, as blockchain technology continues to evolve, future studies should examine the long-term impact of large-scale blockchain adoption on global financial systems, particularly in emerging markets. Finally, the regulatory landscape surrounding blockchain is still developing, and further research is needed to understand how financial regulations can be adapted to support the widespread use of decentralized technologies while ensuring security and compliance.

In conclusion, blockchain technology, particularly through the application of smart contracts and decentralized trust mechanisms, holds great potential to revolutionize the financial sector. The empirical insights gained from this study offer valuable guidance for financial institutions considering the adoption of blockchain, as well as policymakers looking to regulate these emerging technologies. By continuing to explore and refine the application of blockchain in finance, the industry can pave the way for more efficient, transparent, and trustworthy financial systems.

This study is primarily conceptual and may benefit from empirical validation through experimental simulations or field data in future work. Moreover, trust is context-dependent and varies across cultures and regulatory regimes, which this paper does not fully explore. Future research could refine the conceptual model through user-behavior data or apply it to specific sectors such as DeFi lending or NFT markets. In addition, the inclusion of AI-driven governance mechanisms opens further interdisciplinary questions regarding trust delegation and human oversight.

This study has examined the evolving intersection of blockchain, trust, and transparency within financial systems. It finds that decentralized technologies not only disrupt traditional institutional roles but also demand a reevaluation of trust mechanisms. While algorithmic transparency enhances certain aspects of legitimacy and user autonomy, it also introduces new complexities and governance challenges. The integration of blockchain into finance should not merely aim for technical efficiency but must address sociotechnical alignment, ethical accountability, and adaptability to varying institutional contexts. Through a refined understanding of trust evolution, financial innovation can progress with inclusivity, resilience, and responsibility.

References

Abdelsalam O, Chantziaras A, Joseph NL, Tsileponis N (2024) Trust matters: a global perspective on the influence of trust on bank market risk. J Int Financ Mark Inst Money 92:101959

Akanfe O, Lawong D, Rao HR (2024) Blockchain technology and privacy regulation: reviewing frictions and synthesizing opportunities. Int J Inf Manag 76:102753

Akhtar T (2024) Blockchain technology: the beginning of a new era in reforming corporate governance mechanisms. J Knowl Econ 15(1):3059–3084

Bi Q, Boh W, Georgios C (2021) Trust, fast and slow: a comparison study of the trust behaviors of entrepreneurs and non-entrepreneurs. J Bus Ventur 36(6):106160

Brunjes BM (2022) Your competitive side is calling: an analysis of Florida contract performance. Public Adm Rev 82(1):83–101

Chaudhury S, Dhabliya D, Madan S, Chakrabarti S (2023) Blockchain technology: A global provider of digital technology and services. In Dewangan S, Kshatri SS, Bhanot A, Shah MA (eds), Building Secure Business Models Through Blockchain Technology: Tactics, Methods, Limitations, and Performance (pp. 168–193). IGI Global

Eller KH (2020) Comparative genealogies of “contract and society”. Ger Law J 21(7):1393–1410

Fantacci L, Lorenzini M (2024) Technology versus trust: non-bank credit systems from notarized loans in Early Modern Europe to cryptolending. Struct Change Econ Dyn 69:83–95

Fenger HJM, Karré PM, Blok SN (2023) Conceptualizing new forms of volunteering in urban governance. Urban Gov 3:269–277

Geory S (1979) The philosophy of money. Econ J 89(355):180–181

Guiso L, Sapienza P, Zingales L (2004) Does local financial development matter? Q J Econ 119(3):929–969

Guo H, Polak P (2023) Intelligent finance and change management implications. Humanit Soc Sci Commun 10:413

Guo H, Polak P (2024) Finance centralization—research on enterprise intelligence. Humanit Soc Sci Commun 11:1536

Gurcaylilar-Yenidogan T, Erdogan D (2023) Opportunism still remained alive: conditional limits of trust and contract in software projects. Int J Manag Proj Bus 16(2):374–404

Gürpinar E, Özveren E (2024) Incomplete contracts, intellectual property rights, and incentives: Investment in knowledge assets under alternative institutional configurations. In Raban DR, Włodarczyk J (eds), The Elgar Companion to Information Economics (pp. 315–337). Edward Elgar Publishing

Hmimnat C, Bakouchi ME (2023) Blockchain, cryptocurrency, and the quest for financial stability in Morocco. Int J Account Financ Audit Manag Econ 4(2):21–40

Jan A, Najar ZA (2024) Blockchain: concept and emergence. In Ahmad Reshi I, Sholla S (eds), Blockchain-based Internet of Things (pp. 1–20). Chapman & Hall/CRC

Leung WK, Chang M, Cheung M, Shi S (2022) Swift trust development and prosocial behavior in time banking: a trust transfer and social support theory perspective. Comput Hum Behav 133:107137

Limata P (2024) Blockchain and institutions: trust and (de) centralization. Int Rev Econ 71(1):1–17

Liu Y, He J, Li X, Chen J, Liu X, Peng S,... Wang Y (2024) An overview of blockchain smart contract execution mechanism. J Ind Inf Integr 41:100674

Liu Y, Lu Q, Yu G, Paik HY, Zhu L (2023) A pattern-oriented reference architecture for governance-driven blockchain systems. In: 2023 IEEE 20th International Conference on Software Architecture (ICSA). pp 23–34, (IEEE, 2023)

Loertscher S, Marx LM (2022) Incomplete information bargaining with applications to mergers, investment, and vertical integration. Am Econ Rev 112(2):616–649

Lohmann L (2020) Blockchain machines, earth beings and the labour of trust. https://journals.sagepub.com/doi/full/10.1177/0308518X20932082

Padma A, Ramaiah M (2024) Blockchain based an efficient and secure privacy preserved framework for smart cities. IEEE Access 12:21985–22002

Park Y, Kim S (2024) Do artists perceive blockchain as a new revenue opportunity? A social representation study of the Korean music industry. Humanit Soc Sci Commun 11:1–11

Polak P (2021) Welcome to the digital era—the impact of AI on business and society. Society 58:177–178

Schätzlein L, Schlütter D, Hahn R (2023) Managing the external financing constraints of social enterprises: a systematic review of a diversified research landscape. Int J Manag Rev 25:176–199

Setiawan IPS, Alamsyah A (2023) Enhancing security, privacy, and traceability in Indonesia’s national health insurance claims process using blockchain technology. In: 2023 International Conference on Artificial Intelligence, Blockchain, Cloud Computing, and Data Analytics (ICoABCD). IEEE pp 77–82

Singhal S, Kothuru SK, Sethibathini VSK, Bammidi TR (2024) ERP excellence: a data governance approach to safeguarding financial transactions. Int J Manag Educ Sustain Dev 7(1):1–18

Townsend RM (1979) Optimal contracts and competitive markets with costly state verification. J Econ Theory 21(2):265–293

Udeh EO, Amajuoyi P, Adeusi KB, Scott AO (2024) The role of Blockchain technology in enhancing transparency and trust in green finance markets. Financ Account Res J 6(6):825–850

Wang Q (2019) Financial transaction changes and legal adjustment path in the evolution of trust mechanisms. Dig Soc Sci 8:8–10

Wang X, Xu F (2023) The value of smart contract in trade finance. Manuf Serv Oper Manag 25(6):2056–2073

Yang W, Zhang Y, Zhou Y, Zhang L (2021) Performance effects of trust-dependence congruence: the mediating role of relational behaviors. J Bus Res 129:341–350

Acknowledgements

This work is supported by the Fundamental Research Funds for the Central Universities (No. 3214002506B1), Quality Teaching Resources Construction Program for Postgraduates—Southeast University Professional Degree Postgraduate Teaching Casebook Construction Project (No. 5014002406), the National Social Science Fund of China (No. 24&ZD117) and the National Natural Science Foundation of China (No. 72173018). All the support is gratefully acknowledged.

Author information

Authors and Affiliations

Contributions

All authors contributed to the paper conception, methodology and formal analysis and investigation. The first draft of the manuscript was written by HG, and all authors commented on previous versions of the manuscript. All authors read and approved the final manuscript. Conceptualization: HG and XL; Methodology: HG; Writing -Original Draft: HG; Writing-Review & Editing: HG and XL; Formal analysis and investigation: HG, XL.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Guo, H., Liu, X. Exploring trust dynamics in finance: the impact of blockchain technology and smart contracts. Humanit Soc Sci Commun 12, 1235 (2025). https://doi.org/10.1057/s41599-025-05473-9

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-05473-9