Abstract

Amid growing environmental challenges, enhancing Environmental, Social, and Governance (ESG) performance is vital for sustainable development. In China’s economic transformation, strengthened environmental regulations require greater corporate responsibility for carbon reduction and energy conservation. Using data from Chinese A-share listed firms (2014–2023), this study explores how green innovation influences corporate ESG performance and its underlying mechanisms. The results reveal that green innovation has a significant impact on ESG performance, with digital transformation acting as a partial mediator. In addition, executive green perceptions strengthen this relationship, while public emergencies weaken it. The positive effect of green innovation is more pronounced in Eastern regions, state-owned firms, non-growth enterprises, heavy-polluting industries, and the manufacturing sector. These findings suggest that firms should prioritize green innovation and digital transformation as strategic levers, while policymakers should implement targeted, region- and industry-specific incentives to support sustainable development.

Similar content being viewed by others

Introduction

Global environmental issues have become increasingly prominent in recent years, with climate change and biodiversity loss posing significant threats to sustainable economic and social development (Qaim et al. 2020). Against this backdrop, a company’s Environmental, Social, and Governance (ESG) performance has gradually become a crucial indicator of its sustainable development capabilities (Lokuwaduge and Heenetigala 2017; Zhou et al. 2022). This is particularly true for China, the largest emitter of greenhouse gases and the world’s largest manufacturing base, where rapid economic growth has put immense pressure on resources and the environment (Chen and Wang 2022; Maubane et al. 2014). In response to these challenges, the Chinese government has actively advanced sustainable development strategies in recent years, issuing a series of policies and regulations, such as the Environmental Protection Law of the People’s Republic of China, the “Dual Carbon” goals, and the release of the “Guidelines for the Sustainability Reports of Listed Companies”, signaling the mandatory disclosure of ESG information in China’s A-share market (Huo et al. 2022; Wang 2024; Wu and Habek 2021). These policies impose higher environmental requirements on companies and drive the capital market toward sustainable development.

Against this background, green innovation and digital transformation have emerged as two key drivers for improving corporate ESG performance, attracting widespread attention from academia and practice (Cai et al. 2023; Long et al. 2023). By developing environmentally friendly technologies and products, green innovation enables companies to reduce their environmental impact while enhancing market competitiveness (Long et al. 2023). Digital transformation, on the other hand, provides the data support and technological foundation for green development (Xu et al. 2024). However, existing research on the relationship between green innovation, digital transformation, and ESG performance needs to be more comprehensive, especially regarding the mechanisms involved and the differences across various business contexts. Therefore, examining how green innovation influences corporate ESG performance through digital transformation and exploring variations in performance across different contexts helps fill the gaps in theoretical research and provides effective pathways for companies to achieve sustainable development under policy pressures. This is important for promoting the green transformation of both the Chinese and global economies.

Given the increasing importance of sustainable development, improving ESG performance has become a hot research topic. Existing studies mainly focus on internal and external factors that influence ESG performance. Internal factors include research investment (Lian and Weng 2024), ownership structure (Doshi et al. 2024), management short-sightedness (Zhong et al. 2023), financing constraints (Guo et al. 2024), and corporate governance (Wu et al. 2023), while external factors cover supply chain (Yang et al. 2024), industry competition (Chen and Zou 2025), industrial concentration (Tai et al. 2024), climate risks (Chen et al. 2024), government subsidies (Na et al. 2024), and information asymmetry (Bilyay-Erdogan et al. 2024).

As a key factor in driving corporate environmental performance, green innovation is mainly reflected in green technology research and product innovation (Saether et al. 2021). It has been widely discussed in the literature. A company’s green innovation capability can directly improve its environmental performance and enhance its overall ESG performance by strengthening social responsibility and governance structures (Chen et al. 2023). Furthermore, green innovation is closely related to a company’s market competitiveness (Sun and Wei 2025). By implementing green innovation, companies can reduce the intensity of carbon emissions and thus gain a better competitive position in the market. Government environmental policies and market-driven regulations are also crucial in promoting corporate green innovation (Wang et al. 2022). Through effective environmental policies, governments can encourage companies to invest in green technologies, thereby facilitating the implementation of green innovation. This policy guidance helps companies enhance their ESG performance and drive sustainable industry development. However, some scholars have pointed out that green innovation may hurt corporate ESG performance (Yang et al. 2024). Green innovation typically requires substantial initial investment, and especially for small and medium-sized enterprises, it may lead to significant financial pressures, preventing the achievement of expected environmental benefits in the short term and thus affecting ESG performance (Ji et al. 2024). Additionally, immature technologies and low market acceptance of green innovation may result in companies not realizing the anticipated effects, which could add to the burden and negatively impact social and governance performance (Fahad et al. 2022).

On the other hand, digital transformation typically focuses on applying information technology to improve operational efficiency, reduce energy consumption, and optimize governance structures. Digital technologies optimize resource allocation and enhance ESG performance by improving the quality of information disclosure and supply chain transparency (Wang et al. 2023). However, some scholars have argued that the relationship between digital transformation and ESG performance is not always a positive one. The high investment, risks, and uncertainty associated with digital transformation may place considerable economic pressure on some companies, adversely impacting their financial performance and ESG outcomes in the short term (Skare et al. 2023). Furthermore, the rapid development of digital technologies may raise new data privacy and security issues, thereby increasing the complexity of corporate governance (Li and Xue 2021).

Although green innovation and digital transformation are widely regarded as key drivers of corporate ESG performance, prior research often examines their effects in isolation. Existing studies typically focus either on how green innovation enhances environmental (Abu Seman et al. 2019) and financial outcomes (Vasileiou et al. 2022) or on how digital transformation improves corporate governance (Manita et al. 2020) and information transparency (Chai et al. 2025). However, the potential synergistic effects between green innovation and digital transformation, namely, how digital tools may amplify the ESG benefits of green practices, remain underexplored in the literature. This fragmented approach limits our understanding of how these two dimensions may jointly promote sustainable development.

Moreover, while the majority of existing studies confirm the positive impact of green innovation and digital transformation on ESG performance, their findings are often derived from qualitative case studies or questionnaire-based surveys (Sun et al. 2024; Zhao et al. 2023), which may suffer from sample bias and limit the generalizability of results. More importantly, few studies have systematically examined how the relationship between green innovation and ESG performance varies across heterogeneous contexts, such as firm ownership structure, industry type, and regional institutional environments, particularly in emerging economies like China, where policy frameworks and institutional logics differ significantly from those in developed markets.

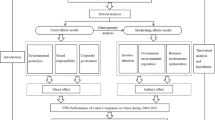

To address these gaps, this study constructs an integrated empirical framework that not only investigates the direct impact of green innovation on ESG performance but also introduces digital transformation as a mediating mechanism. In addition, the study explores the moderating effects of executives’ green perception—capturing internal cognitive tendencies—and public emergencies—representing external environmental shocks. Furthermore, it incorporates a heterogeneity analysis by examining how the relationship between green innovation and ESG performance varies across key contextual dimensions in China, including regional differences, enterprise types, and industry classifications. This comprehensive design enables a deeper understanding of the conditions under which green innovation is most effective and how digital transformation can act as a strategic bridge in diverse institutional and industrial contexts.

The main contributions of this study are threefold: (1) utilizing data from Chinese A-share listed companies to verify the relationship between green innovation and corporate ESG performance, providing theoretical insights for enhancing ESG performance; (2) examining the mediating role of digital transformation in the relationship between green innovation and ESG performance, exploring the moderating effects of executive green perceptions (EGP) and public emergencies, and uncovering the mechanisms by which green innovation impacts ESG performance; and (3) addressing the gap in existing literature regarding the relationship between green innovation, digital transformation, and ESG performance, particularly in terms of regional, corporate, and industry differences.

While China provides the focal context for this study due to its unique institutional environment and policy-driven ESG agenda, the findings carry broader implications for other emerging economies facing similar challenges, such as industrial upgrading, resource constraints, and the imperative of digital transformation. By employing green innovation and digital transformation as core indicators, this study emphasizes “early signals” of firms’ strategic investment and forward-looking behavior, capturing the dynamic nature of ESG performance and shedding light on the underlying behavioral drivers. Against the backdrop of institutional convergence and strengthened regulation, green innovation, mediated by digital transformation, significantly enhances ESG outcomes, facilitating improvements in corporate governance and the implementation of sustainable strategies. These insights offer both theoretical contributions and policy guidance for understanding and promoting sustainable development in emerging market contexts, while also providing a foundation for future comparative research on transitional economies.

Theoretical analyses and research hypotheses

Green innovation and corporate ESG performance

Green innovation typically refers to the innovation companies undertake in product design, production processes, services, and business models to reduce negative environmental impacts while generating economic and social benefits (Zhou et al. 2023). This concept encompasses technological innovations, such as environmentally friendly products and clean technologies, as well as managerial innovations, including green supply chain management and sustainable strategies (Hu et al. 2022). Green innovation is key in optimizing corporate ESG performance, as it supports sustainable development through technological breakthroughs and managerial innovations (Li et al. 2019).

Green innovation and environmental performance

Green innovation is essential to improving a company’s environmental performance (E), significantly reducing environmental burdens through technological advancements and resource optimization. Studies have shown that green innovation significantly reduces greenhouse gas emissions (Su and Moaniba 2017), optimizes energy efficiency (Sun et al. 2019), and lowers pollutant emissions (Peng et al. 2021). Based on the resource-based view (RBV) theory, green innovation is regarded as a strategic resource (VRIN) characterized by value, rarity, inimitability, and non-substitutability (Andersén 2021). First, its value lies in reducing production costs through clean technology and optimized resource utilization while expanding markets for environmentally friendly products. Second, its scarcity stems from the high barriers to entry in green technology R&D, including capital investment, specialized knowledge, and organizational commitment. Third, the interdisciplinary knowledge, patent protection, and complex processes required for green innovation make it difficult for competitors to replicate. Finally, its non-substitutability is evident in the inability of non-green alternatives to achieve equivalent environmental performance.

From the perspectives of resource integration, path dependence, and resource restructuring, when enterprises first invest in green innovation, they establish collaborative networks with suppliers, R&D institutions, and regulatory authorities (Melander 2017). As experience accumulates, these networks form institutionalized processes and continuously restructure internal resource allocation, enabling enterprises to maintain a sustained competitive advantage in a dynamic environment. Thus, green innovation not only directly improves environmental performance and supports sustainable development but also serves as a core strategic resource that continuously enhances long-term competitiveness, acting as an important internal driver for improving enterprise ESG performance (Khanra et al. 2022).

In specific practice, companies can effectively achieve energy-saving and emission-reduction goals by developing low-carbon technologies (such as carbon capture and storage) and improving the environmental sustainability of production processes (such as clean production techniques). These paths suggest that green innovation directly enhances a company’s environmental performance, garnering policy support and societal recognition. Moreover, according to stakeholder theory, companies can meet stakeholders’ expectations regarding environmental responsibility by engaging in green innovation, thus enhancing their environmental reputation (Zhou et al. 2024). Green innovation enables companies to proactively respond to increasingly stringent environmental regulations and consumers’ demands for sustainability, thereby maintaining a competitive edge in the marketplace (Zhu et al. 2023).

Green innovation and social performance

This alignment with stakeholder expectations not only significantly improves the company’s environmental reputation but also enhances its social performance (S) by demonstrating responsibility and transparency. Stakeholder theory argues that businesses must consider the interests of all stakeholders in their decision-making processes, rather than focusing solely on shareholders (Mahajan et al. 2023). By implementing green innovation, companies actively address the environmental concerns of various stakeholders, including customers, employees, regulatory agencies, and local communities. Green innovation has demonstrated multiple positive effects in promoting corporate social performance, particularly in employee welfare (Zhao et al. 2023), consumer demand (Lv and Li 2021), and social responsibility (Le et al. 2024).

From the perspective of stakeholders, employees, as key internal stakeholders, have their interests directly affected by green innovation. Regarding employee welfare, introducing green production methods and environmental technologies significantly reduces exposure to harmful substances and the incidence of occupational diseases, thereby enhancing employees’ sense of belonging and job satisfaction (Iranmanesh et al. 2017). Furthermore, green innovation is often accompanied by efficient resource utilization and energy-saving measures, which help foster employees’ sense of social responsibility and enhance their cohesion and loyalty to the company (Han 2024). Among external stakeholders, consumer demand for environmentally friendly products is growing. Green innovation can effectively meet consumer demand for green products by optimizing production processes and enhancing product design, thereby improving consumer satisfaction, strengthening public recognition of a company’s social responsibility, and increasing the company’s brand competitiveness. From a social responsibility perspective, green innovation further enhances a company’s social image and long-term social performance by improving supply chain management and strengthening community participation (Cherrafi et al. 2018). Specifically, the design and production of green products effectively reduce resource waste and environmental pollution, thereby lowering external environmental costs and generating direct economic benefits for companies, while also achieving broader social and public value.

Green innovation and governance performance

Green innovation’s role in promoting corporate sustainability is not limited to the social dimension; it also plays a crucial role in the governance (G) dimension. Green innovation helps enhance corporate compliance capabilities, thereby driving the optimization of governance structures. Existing research has shown that green innovation enables companies to adapt more effectively to, and even exceed, environmental laws and regulations, thereby reducing potential legal risks and regulatory pressures (Cui and Wang 2022). Regarding governance, green innovation relies on robust management systems and transparent information disclosure mechanisms to track and communicate sustainability efforts. This process aligns with the principles of good governance, emphasizing accountability and transparency, and constitutes a key component of the governance element within the ESG framework. At the same time, according to dynamic capability theory (DCT), enterprises must continuously identify changes in the external environment and adjust internal processes to maintain a competitive advantage (O’Connor 2008). As part of an enterprise’s dynamic capabilities, green innovation drives the continuous optimization of governance mechanisms during adaptive adjustments and resource restructuring, enhancing corporate resilience and adaptability in complex and evolving environments.

Against the backdrop of increasingly stringent carbon emission controls and the rapid advancement of green finance policies, green technology and management innovations enable companies to enhance governance performance and strengthen trust relationships with external investors (Dobrick et al. 2025). This high degree of alignment with institutional expectations holds significant strategic importance. According to institutional theory, organizations often adopt widely recognized practices within their institutional environments to gain legitimacy and reduce environmental uncertainty (Tang et al. 2024). In the context of green innovation, companies face coercive pressures from environmental regulatory bodies, normative pressures from industry associations and standard-setting organizations, and mimetic pressures from leading industry peers. By actively implementing green innovation initiatives, companies demonstrate compliance with and leadership in sustainable development practices, further enhancing their reputations and strengthening stakeholder trust, ultimately contributing to improving overall ESG performance.

In summary, green innovation strongly supports companies in achieving sustainable development goals (SDGs) by optimizing their environmental, social, and governance performance. Based on the aforementioned theories and research, the following hypothesis is proposed:

H1: Green innovation has a positive impact on corporate ESG performance.

The mediating role of digital transformation

Digital transformation and green innovation synergy

Digital transformation refers to the process by which companies adopt advanced digital technologies, such as big data, cloud computing, artificial intelligence (AI), and the Internet of Things (IoT), to optimize business processes, enhance operational efficiency, and create new business models. Digital transformation enhances production efficiency and provides technological support for green innovation, enabling companies to achieve their environmental goals more quickly (Xu et al. 2024).

Firstly, digital transformation enables enterprises to optimize resource management and enhance operational efficiency through the integration of advanced digital technologies. According to information systems theory, digital transformation promotes transparency in information disclosure, governance structures, and social responsibility and helps businesses improve their effectiveness in green innovation (Gao 2023). Specifically, businesses can utilize digital technologies, such as blockchain, to ensure the authenticity and reliability of their green innovations and ESG practices, thereby enhancing stakeholders’ trust in their social responsibility (DesJardine et al. 2025). This is of great significance for enterprises in attracting global investors, consumers, and social support, as well as improving their performance in the social and governance dimensions. Additionally, implementing digital technologies helps enterprises better track their social and environmental impacts throughout the supply chain and product lifecycle management, thereby enhancing transparency with consumers and regulatory authorities.

Furthermore, based on resource dependency theory, digital technology, as a key resource, effectively reduces companies’ reliance on traditional energy and raw materials, enhances resource controllability, and thereby improves the stability of green innovation (Xing et al. 2024). Digital technology enables companies to track energy usage more accurately, reduce waste emissions, and promote the greening of production processes. Through real-time monitoring and efficient management of environmental impacts, companies can take timely measures to promote energy conservation, reduce emissions, and achieve sustainable production goals (Zhang et al. 2023). Therefore, digital transformation enhances a company’s environmental performance and improves its green innovation capabilities, ultimately helping it achieve greater social responsibility and governance success. By enhancing transparency, reducing resource dependence, optimizing operational efficiency, and strengthening social responsibility, digital transformation fosters green innovation, thereby improving a company’s ESG performance and driving sustainable development.

More importantly, the dynamic capabilities theory (DCT) emphasizes that enterprises can significantly improve the efficiency and effectiveness of green innovation through the continuous development of sensing, seizing, and reconfiguring capabilities during the digital transformation process (Liu et al. 2022). Against this backdrop, digital transformation gives enterprises the necessary tools to adapt to market changes and promote green innovation. Specifically, sensing capabilities enable enterprises to gain real-time insights into market trends and changes in customer demand for green products and environmental protection (Darby 2020). With the help of big data analysis and IoT technologies, enterprises can accurately capture information on environmental changes and consumer preferences. Seizing capabilities manifest in enterprises that utilize advanced technologies, such as AI and blockchain, to quickly capitalize on green transformation business opportunities (Witschel et al. 2019). This enables them to improve efficiency and achieve SDGs through supply chain transparency and green production automation. Reconfiguring enables companies to flexibly adjust their resource allocation and production processes, continuously optimizing the implementation of green innovation through technologies such as cloud computing and smart manufacturing, thereby ensuring the efficient use of resources and green processes (Witschel et al. 2019). Therefore, digital transformation provides companies with the technological support to achieve green innovation and enhances their dynamic capabilities. It enables them to continuously drive green innovation and improve ESG performance in complex, ever-changing environments. Through this process, companies can respond efficiently to external challenges and take the lead in green innovation and sustainable development.

Under this framework, companies can utilize real-time data analysis to quickly adapt to shifts in market demand, thereby accelerating green innovation. Highly digitized companies can optimize product design and production processes through precise predictive analysis, meeting consumer demand for environmentally friendly products while minimizing environmental impacts. This digitally driven innovation significantly enhances corporate ESG performance within a shorter timeframe. Furthermore, the successful implementation of digital transformation relies on the acceptance of these technologies by key decision-makers within the organization. According to the technology acceptance model (TAM), the perceived usefulness and ease of use of digital technologies are key to their adoption (Marangunić and Granić 2015). In green innovation, when managers recognize that digital tools can effectively support sustainability initiatives (such as using the IoT for real-time environmental monitoring or blockchain for transparent supply chain management), they are more likely to invest in and use these technologies. This acceptance accelerates the pace of digital transformation, thereby enhancing a company’s green innovation capabilities and improving its ESG metrics.

Risks of low digitalization

When a company’s degree of digital transformation is lower, its performance in green innovation and ESG may be significantly constrained. Low-digitized companies often lack the necessary technological tools to optimize resource use and production processes. This may lead to energy waste, emissions exceeding limits, and other environmental issues, negatively impacting their environmental performance (Yang and Han 2023). Without precise data support for the green innovation process, companies may struggle to effectively identify and mitigate environmental burdens in their products and services, thereby delaying the progress of green innovation. Furthermore, companies with low levels of digital transformation typically face issues such as information asymmetry and weak governance structures (Wang et al. 2024). The absence of advanced information management systems makes it difficult for these companies to achieve high levels of transparency, particularly in ESG information disclosure, which may be delayed or incomplete (Zhang et al. 2024). This affects the fulfillment of corporate social responsibility and may also reduce investor, consumer, and stakeholder trust, thereby impairing social and governance performance (Dorobantu et al. 2024). Otherwise, since management cannot access real-time data related to green innovation, these companies may need more flexibility and efficiency to respond to external environmental changes. As a result, inadequate digital transformation can lead to the accumulation of technical debt, hindering the effective implementation of green innovation (Rinta-Kahila et al. 2023). This debt may create additional costs and management challenges when pursuing green innovation and improving ESG performance. Companies with low digitalization need help to fully utilize modern digital tools to optimize energy efficiency and waste management, thus impacting their environmental performance. Therefore, digital transformation provides the necessary technological infrastructure and capabilities to provide an intermediary between green innovation and improved ESG performance. Without digital transformation, the potential of green innovation may not be fully realized due to inefficiencies in resource management, data analysis, and process optimization.

In summary, the level of digital transformation has a direct impact on a company’s green innovation and ESG performance. A high level of digital transformation can significantly promote green innovation and corporate performance in the social, environmental, and governance dimensions by improving resource efficiency, enhancing information transparency, and optimizing decision-making support. However, companies with low digital transformation may face inadequate technology adaptation, slow innovation, and insufficient information disclosure, which limit their progress in green innovation and ESG performance. Based on the analysis above, this paper proposes the following hypothesis:

H2: Digital transformation mediates the relationship between green innovation and corporate ESG performance.

Research design

Sample selection and data sources

Considering the practical significance of the study and the availability of data, this study selects micro-panel data of Chinese A-share listed companies from 2014 to 2023 for empirical research, in which corporate patent information is obtained from the Chinese Research Data Services Platform (CNRDS), data on digital transformation, EGP are obtained from the annual reports released by the companies using Python crawler technology, and the ESG scores and control variables are obtained from China Stock Market & Accounting Research Database (CSMAR) database.

To ensure the reliability of the data, this research preprocesses the samples as follows: (1) excluding the financial sector and companies with abnormal status, including special treatment (ST, *ST) and special transfer (PT) companies; (2) removing the samples with missing key variables and the presence of obvious outliers; and (3) doing the Winsor treatment at the upper and lower 1% level for continuous variables to avoid the potential interference of extreme values—the pre-processing results in 2144 firms and 6512 observations. The tools used in this paper are Excel 2024, PyCharm 2021, and Stata 18.0 software.

Variable definition and measurement

Response variable

Measuring firms’ ESG management level using the ESG score of the Sino-Securities Index (SNSI). Based on China’s ESG disclosure system, SNSI ESG indicators refer to the structure of mainstream foreign ESG systems during the design process, fully demonstrating the applicability of each indicator, eliminating those indicators that are not applicable or whose data are unavailable, and adding indicators with Chinese characteristics, such as poverty alleviation, social responsibility reports, and penalties imposed by the Securities and Exchange Commission (SEC). At the same time, based on the characteristics of China’s listed companies, the definitions and calculation rules of certain indicators are modified, and corporate governance problems caused by objective reasons related to state-owned enterprises (SOEs), such as connected transactions, are addressed separately. Choosing this score as a measure of ESG management level helps to reflect the management status and potential risks of enterprises more objectively and comprehensively in promoting sustainable development. It provides a robust database for empirical research.

Explanatory variable

Green innovation (GI) is expressed as the sum of green patent applications following Bettarelli et al. (2025) and Yu et al. (2026), aiming to reduce the interference of external factors (e.g., approval time, market demand, policy fluctuations, etc.) on the measurement of green innovation to reflect more realistically the innovation investment and R&D intention of the firm’s internal investment in the field of green technology. Compared with the number of patents granted, the number of patent applications can promptly capture enterprises’ innovation trends and R&D vigor, and its data is highly comparable and current. Moreover, from a practical standpoint, patent application data are readily available, consistently structured, and widely used in innovation research, which enhances the feasibility and replicability of the measurement. To ensure environmental relevance, this study further filters patents using the WIPO green patent list (Sun et al. 2025; Wang et al. 2025) and the China National Intellectual Property Administration’s Green and Low-Carbon Technology Patent Classification Standard (Administration 2022), so that only patents with clear environmental benefits are counted.

The measurement of the degree of digital transformation (DT) of enterprises refers to the method of Jiang et al. (2025), Ma et al. (2025), and Meng (2025), which, through text analysis techniques, analyzes in depth the ‘Management Discussion and Analysis (MD&A)’ part of the annual reports of listed companies is analyzed in depth, and the frequency of digitalization-related terms is extracted. Specifically, keywords are associated with three core dimensions, including digital technology applications (DTA), intelligent manufacturing (IM), and modern information systems (MIS). The keyword dictionary comprises 82 terms, compiled based on prior academic studies and relevant policy documents. These terms encompass a broad spectrum of digital transformation concepts, including, but not limited to, big data, cloud computing, AI, the Industrial Internet, smart manufacturing, and information integration.

Considering the right-skewed distribution of the data, and to ensure the stability and comparability of the analysis results, this study adopts a plus-one smoothing procedure, which logarithmically transforms the sum of the number of green inventions and green utility models independently filed in the current year, as well as the frequency counts of DTA, IM, and MIS, to construct the indicators of green innovation and digital transformation, GI and DT. Although this measure emphasizes the quantity rather than the quality or impact of individual patents, it functions as an “early signal” of firms’ green innovation efforts. Combined with the text-based digital transformation index, these indicators capture firms’ real-time investments and strategic intentions in large-scale green innovation and digital transformation. Such early and forward-looking measures align with the dynamic nature of ESG performance and recent emphasis on strategic orientation and proactive corporate behavior, thereby enhancing the identification of the drivers behind corporate actions and improving the explanatory power of the study from a dynamic perspective.

Control variables

Based on the previous studies (Chen and Zou 2025; Feng et al. 2022; Lian and Weng 2024; Na et al. 2024; Tai et al. 2024), this paper controls for the following variables: listing age (Listdt), enterprise scale (Scale), debt-to-asset ratio (LEV), ratio of tangible assets (TA), return on assets (ROA), net operating profit margin (NOPM), Net profit growth rate (Grown), Herfindahl–Hirschman Index (HHI), Tobin’s Q-value (TobinQ), turnover rate (TR), Consolidated Market Annual Beta (Betavals), Shareholding concentration (Shrcr), Government grants (Grant), while controlling for year, individual firms. Table 1 provides a detailed explanation of these variables.

Model settings

To test Hypothesis 1, this study constructs the following model to analyze its theoretical foundation and empirical support:

To examine the partial mediating role of digital transformation in Hypothesis 2, the three-step method proposed by Wen et al. (2004) is employed for mediation effect testing. Based on Eq. (1), the following two models are established and analyzed step by step:

If the results of the model tests meet the following criteria: (1) the coefficient \(\beta\)1 in Model (1) is significant; (2) the coefficient \(\beta\)2 in Model (2) is significant; and (3) both coefficients \(\beta\)3 and \(\delta\)3 in Model (3) are significant, with the absolute value of \(\beta\)3 in Model (3) smaller than that \(\beta\)1 in Model (1), it can be concluded that digital transformation exerts a partial mediating effect in the relationship between ESG performance and green innovation, thereby supporting Hypothesis 2.

Result analysis

Descriptive statistics

Table 2 presents the descriptive statistics of the main variables. In the sample, the average ESG score is 74.651, with a standard deviation of 4.685 and a range from 48.900 to 89.240. Overall, the ESG performance of the sample firms is relatively high, indicating that most companies have made considerable efforts in ESG practices. However, there is still noticeable variation across firms, as some exhibit outstanding sustainability performance, while others score relatively lower, suggesting that ESG practices are not evenly distributed. GI shows greater variability, with a mean of 1.556 and a standard deviation of 0.932, reflecting significant differences in firms’ innovation efforts, ranging from 0.693 to 6.848. Similarly, DT has a mean of 3.625 and a standard deviation of 1.051, with values ranging from 1.099 to 5.984, highlighting varying levels of digital capabilities across firms.

Analysis of regression results

ESG and green innovation

Table 3 reports the regression results of the relationship between ESG performance, Green Innovation, and Digital Transformation. Column (1) reveals a significant positive relationship between GI and ESG, with a coefficient of 0.279 (t = 3.038, p < 0.01). In terms of economic significance, this coefficient implies that a one-unit increase in GI is associated with a 0.279-point increase in the ESG score. This indicates that firms investing more in green innovation tend to achieve higher ESG scores, likely because green initiatives align with environmental and sustainability goals. These efforts may enhance a firm’s public image and compliance with environmental regulations, thereby contributing directly to improved ESG performance. This finding supports Hypothesis 1, which posits that relative Green Innovation positively impacts ESG performance.

Partial mediating role of digital transformation

Table 3 regression results suggest that DT partially mediates the relationship between GI and ESG. Column (1) indicates that GI directly improves ESG (coefficient = 0.279, p < 0.01), which indicates that each additional unit of GI will increase the ESG score by 0.279 points. Moreover, GI has a statistically significant positive impact on DT with a coefficient of 0.025 (t = 2.395, p < 0.05) in column (2), which indicates that a one-unit increase in GI is associated with a 0.025-unit increase in DT. This suggests that firms engaged in green innovations are more likely to adopt digital transformation practices. Furthermore, in column (3), the inclusion of DT in the model reveals a positive and significant effect on ESG (coefficient = 0.413, p < 0.01), indicating that each additional unit of DT will increase the ESG score by 0.413 points. More importantly, the effect of GI on ESG becomes slightly smaller when DT is included (coefficient = 0.269, p < 0.01), suggesting that DT partially mediates the relationship by facilitating more efficient implementation of green innovations and improving sustainability practices. This finding underscores the importance of integrating green innovation with digital transformation to optimize ESG performance. This finding supports Hypothesis 2, indicating that Digital Transformation is an intermediary in the relationship between Green Innovation and ESG performance.

Endogeneity and robustness tests

Instrumental variables approach

Enhancing a firm’s green innovation may improve its ESG performance. However, it is worth noting that firms with higher ESG scores may also demonstrate higher levels of green innovation. This suggests a potential interactive relationship between green innovation and ESG performance. Furthermore, due to the incompleteness of the control variables, it is challenging to eliminate the effect of omitted variables. To address the potential endogeneity issue, this paper employs an instrumental variables (IV) approach to conduct further tests to verify the impact of green innovation on firms’ ESG performance.

Following the approach of Benlemlih and Bitar (2018), the average R&D investment ratio of enterprises operating within the same industry, city, and year was selected as an instrumental variable to address the potential endogeneity of green innovation. This aggregated measure captures the broader technological environment and peer effects within which firms operate. Firms located in similar industrial and regional contexts are often influenced by the innovation behavior of their peers due to knowledge spillovers, competitive pressures, and regional policy incentives, thereby making the average R&D intensity a strong predictor of a focal firm’s innovation decisions, including green innovation. This satisfies the relevance condition of an instrumental variable. At the same time, because this variable reflects general industry- and region-level R&D trends rather than firm-specific shocks or managerial discretion, it is unlikely to be directly correlated with the firm’s unobservable characteristics that affect ESG performance. Therefore, it satisfies the exogeneity condition.

The results of the first stage of the regression (Column 1 of Table 4) show that the coefficient of the IV is significantly positive at the 1% level, indicating that IV is highly correlated with GI. In addition, the F-statistic is 40.339, which exceeds the critical value of 10. These results indicate that the instrumental variable satisfies the correlation condition and is not weak. Column (2) of Table 4 reports the results of the second-stage regression, where the coefficient of GI (3.703) is significantly positive at the 1% level (t = 0.952). This suggests that higher green innovation capabilities continue to significantly improve firms’ ESG performance even after correcting for potential endogeneity issues and providing unbiased results. Therefore, the conclusions drawn in this paper remain unchanged.

Heckman two-stage model

When studying the impact of green innovation on ESG performance, it is possible that only companies with higher ESG performance choose to engage in green innovation. These companies may differ from others in terms of technological level, resources, and other factors, meaning that the sample of companies pursuing green innovation may not accurately represent the entire corporate population, which can lead to biased estimation results.

This study employs the Heckman two-stage model to address this potential endogeneity issue. Specifically, in the first stage, a probit model sets an indicator variable based on whether the company passes ISO 14001 certification (assigned a value of 1 if the company passes, and 0 otherwise) (Abid et al. 2022; He and Shen 2019). The inverse Mills ratio (IMR) is then calculated from the first-stage regression results and incorporated into the second stage for regression analysis. Column (1) in Table 5 shows that the IV (the average R&D investment ratio of firms operating in the same industry, city, and year) coefficient is significantly negative, suggesting that external innovation intensity may discourage firms from individually pursuing ISO 14001 certification, possibly due to free-rider behavior or resource constraints. This suggests the existence of strategic interdependence among firms in the adoption of environmentally driven innovation. Column (2) presents the results from the second stage of the Heckman model, where the IMR is statistically significant, confirming that selection bias is non-negligible. After adding IMR, the coefficient of GI on ESG is 0.6516, which is significant at the 1% level, reinforcing the hypothesis that green innovation contributes positively and substantially to a firm’s ESG performance. Overall, the research findings remain robust after effectively addressing the sample selection bias using the Heckman two-stage model.

E-score of replacement response variable

In the robustness test, the ESG score (ESG) is replaced by the environmental component score (Es) as a measurement variable of ESG performance. Replacing ESG with Es has a strong rationale and advantages. Firstly, the E-Score focuses on environmental performance, which can measure the impact of green innovation more directly and precisely, avoiding the interference introduced by social and governance factors in the ESG field (Wang and Zhang 2024). Secondly, the core objective of green innovation is to improve environmental performance, which is highly compatible with the measurement criteria of E-Score, making E-Score more reflective of the real role of green innovation (Rehman et al. 2021). In addition, Es, as a single environmental dimension indicator, is usually more transparent in its calculation and criteria, which helps to improve the explanatory power of research results and comparability among peers.

After replacing the response variable, the regression results of ESG performance and green innovation are shown in Table 6. As shown in column (1), the coefficient of GI is significantly positive at the 5% level, which supports hypothesis 1. Combining the data in columns (2) and (3) confirms the correctness of hypothesis 2. Meanwhile, most of the variables’ significance and direction of influence on the response variable are retained, despite changes in the regression coefficients. In addition, the model’s goodness of fit (R²) remains relatively unchanged, indicating no significant decrease in the model’s explanatory power after replacing Es. Overall, the rationality of the model design and the reliability of the results were verified.

Green development of replacement explanatory variable

To further improve the robustness of the regression results, this paper replaces the original green innovation indicator (GI) with green development (GD), according to Song et al. (2024), using textual analyses to analyze the firm’s annual report and then take the logarithm of the word frequency of green development keywords in the report plus one. The keyword dictionary comprises 113 terms that cover five dimensions of corporate green transformation: advocacy and initiatives, strategic vision, green technological innovation, pollution control, and environmental management, based on prior literature and national sustainability guidelines. This approach captures the firm’s strategic emphasis on sustainability as expressed in its official disclosures. This measure captures the firm’s strategic emphasis on sustainability as reflected in its official disclosures.

Although conceptually related, GI and GD represent distinct dimensions of corporate environmental orientation. GI reflects tangible innovation outputs, such as the development and application of environmentally friendly technologies, products, and processes. In contrast, GD captures the firm’s broader strategic intent and policy-level commitment to green growth, which may not necessarily translate into measurable technological achievements within a given period. As such, GD serves as an alternative lens to assess a firm’s environmental positioning, focusing on long-term sustainability narratives rather than specific innovation outcomes.

The results after replacing the explanatory variable are presented in Table 6. The coefficient of Green Development in column (4) of Table 6 is significantly positive at the 5% level, supporting Hypothesis 1. Considering the results in columns (5) and (6), we conclude that digital transformation mediates the relationship between green innovation and firms’ ESG performance. This finding is consistent with Hypothesis 2 and remains robust. These findings confirm the robustness of our main conclusions and demonstrate that the positive association between environmental strategy and ESG outcomes remains valid under an alternative conceptual framework, thereby enhancing the generalizability of the empirical results.

Replacement sampling interval

Considering that SynTao Green Finance launched China’s first ESG database for listed companies in 2015, which has significantly contributed to the advancement of green investment and sustainable development practices (Guo et al. 2024), this study adjusts the sample period to 2015–2023. Starting from 2015, the gradual implementation of this system has enhanced the transparency and accountability of corporate green transformation, providing a clearer and more actionable pathway for green development. Analyzing the data from this post-implementation period enables a more comprehensive understanding of how corporate green behaviors evolve under the influence of the policy framework, thereby strengthening the robustness of the main regression results across different sample periods and enhancing the relevance and academic value of the study’s conclusions.

Based on the regression results in Table 7, after adjusting the sample period, the regression coefficients of the core variables have increased, while their significance levels have remained largely unchanged. Moreover, it is noteworthy that in column (2), the significance level of GI has improved to 1%. These results suggest that establishing the ESG data system has effectively enhanced corporate investments and efforts in green innovation, further strengthening the positive impact of green innovation on corporate ESG performance. This shift reflects the growing importance of green innovation and digital transformation in corporate sustainability, as well as the ongoing guidance provided by policies and information systems in shaping corporate behaviors. Otherwise, the direction of the coefficients for all control variables remains consistent with the original model, indicating that the research conclusions hold steady across different time frames, thereby validating the robustness of the model and the reliability of the findings.

Further research

Moderating effect of unexpected public incidents

The study of the interaction between the COVID-19 pandemic lockdown and green innovation on ESG performance is crucial (Dai and Tang 2022). The crisis has forced businesses to adjust strategies and resources, with green innovation potentially impacted by the pandemic. This research aims to understand whether green innovation can enhance ESG performance during a crisis or if limited resources and market demand hinder its effectiveness. For businesses, it offers insights into responding to future crises and optimizing green innovation strategies. At the same time, it guides policymakers on the effectiveness of green recovery policies and future green economic recovery. The pandemic lockdown period spans from 2020 to 2022, covering the most significant phases of China’s COVID-19 lockdowns. This period includes the initial severe restrictions from early 2020, when Wuhan and other cities were placed under strict lockdowns, through the nationwide lockdown measures and gradual reopening process that continued into 2022. This three-year window allows for an analysis of both the immediate and longer-term impacts of the pandemic on green innovation and ESG performance. To investigate the moderation of the COVID-19 pandemic, the following model was constructed in this study:

COVID represents the outbreak of the COVID-19 pandemic, which is set as a dummy variable. This variable takes the value 1 during the pandemic lockdown period and 0 otherwise. Table 8 (1) presents the results of the moderating effect of COVID-19 obtained from a fixed-effects model regression, which show that the interaction term GI × COVID is significantly negative at the 5% significance level (t-value = −2.166). This indicates that the COVID-19 pandemic lockdown has somewhat weakened the positive impact of green innovation on corporate ESG performance. This could be due to the challenges faced by many companies during the pandemic, such as increasing resource constraints, supply chain disruptions, changes in employee work environment, and capital market volatility, which suppressed green innovation activities. Nevertheless, GI still has a significant positive effect on ESG (with a regression coefficient of 0.376), indicating that green innovation remains a crucial driver of corporate sustainable development and improved ESG performance.

Moderating effect of EGP

According to managerial cognition theory, EGP directly influence a company’s investment in green innovation and strategic positioning. In contrast, green innovation is a key factor in enhancing the company’s ESG performance (Venugopal et al. 2024). By analyzing the interaction between EGP and green innovation, this study helps to understand how strengthening executives’ environmental consciousness can promote green innovation, thereby enhancing the company’s overall ESG performance. This research not only aids companies in formulating more effective green innovation strategies but also provides empirical evidence for policymakers to optimize green development policies, promoting the transition of businesses toward sustainable development. To examine the moderating role of EGP, this study constructs the following model:

Following the method of measuring EGP proposed by Wang (2024), this study uses text analysis to examine the annual reports of listed companies. Keywords are selected based on three dimensions: green competitive advantage awareness, corporate social responsibility awareness, and awareness of external environmental pressures. EGP is constructed by dividing the frequency of keyword occurrences in the annual reports by the overall word frequency, which measures the level of green attention in corporate decision-making. Table 8 (2) presents the moderating effect of EGP based on the fixed-effects model regression results, which shows that the interaction term GI × EGP is significantly positive at the 5% significance level (t-value = 2.001). This indicates that EGP positively moderates the relationship between GI and ESG. In other words, the stronger the EGP, the more significant the impact of green innovation on ESG performance, further emphasizing the crucial role of EGP in promoting green innovation and improving ESG performance.

Analysis of the sample according to the type of region

Based on the unbalanced and diversified background of China’s regional economic development, regions exhibit significant differences in economic development, industrial structure, resource endowment, technological capacity, and policy orientation (Ruan et al. 2024). Such differences reflect the diverse characteristics of regions in terms of their development stages and resource conditions, and determine the different paths and priorities regions take in promoting digital transformation, green innovation, and high-quality development. Based on the division by the National Bureau of Statistics of China (NBSC), this paper categorizes the sample into eastern, central, and western firms to investigate the impact of green innovation on ESG performance across different regions.

The regression results in Table 9 reveal significant regional differences in the impact of green innovation and digital transformation on firms’ ESG performance. In the eastern region, GI (0.267) and DT (0.385) have a significantly positive effect on ESG, indicating that firms in this region effectively integrate green innovation and digital transformation to enhance their ESG performance. In the central region, although GI shows a positive effect (0.302), it is not statistically significant; in contrast, DT (0.795) has a significant and strong positive impact on ESG performance. This suggests that the central region relies more heavily on digital transformation to drive ESG development. In the western region, neither GI (0.165) nor DT (0.004) has a significant effect on ESG performance, indicating that these factors have weaker driving effects in this region.

These regional differences are primarily attributed to variations in economic development levels, resource endowments, industrial foundations, and regional policy support (Lan et al. 2024). Green innovation and digital transformation in the eastern region have a dual promotional effect on ESG performance, mainly due to the combined effects of favorable policies and market maturity. On the one hand, under the guidance of the “dual carbon” strategic goals, local governments in the eastern region have introduced many specific and operational local support policies, providing solid guarantees for green innovation in enterprises regarding financial support, tax incentives, and green finance. On the other hand, high levels of marketization, well-developed supply chain systems, and strong technological innovation capabilities have created a favorable environment for the deep integration of green innovation and digital transformation. These two factors interact to drive significant improvements in corporate ESG performance effectively.

As a hub connecting the eastern and western regions with a solid industrial foundation, the central region lags in leveraging green innovation to enhance ESG performance, primarily due to insufficient technological support and resource investment. Although the central region has a certain industrial foundation, it is constrained by limited investment in green innovation and insufficient technological R&D capabilities, leading enterprises to rely more on digital transformation measures to achieve efficiency optimization and resource integration. Otherwise, there are still significant shortcomings in terms of financial support, technological innovation investment, and the development of a green industrial system, which prevents green innovation from exerting a significant driving effect on ESG performance.

Western regions face even more severe challenges, including relatively weak infrastructure, insufficient resource allocation, and limited local policy support. Low corporate responsiveness and conversion capacity for relevant policies have resulted in limited effectiveness of green innovation and digital transformation in promoting sustainable corporate development, thereby failing to translate into effective improvements in ESG performance. Furthermore, differences among regions in policy implementation intensity, efficiency of policy resource allocation, and the extent of corporate policy response have also exacerbated the imbalance in ESG development levels across regions to a certain extent.

Analysis of the sample according to the type of enterprise

Nature of assets

According to previous research, firms with different ownership structures exhibit varying ESG performance (Chen et al. 2024). Consequently, the impact of green innovation on ESG performance may differ depending on the actual controller of the enterprise. Based on differences in ownership structure, this study divides the sample into SOEs and non-SOEs to explore the mechanisms and effects of green innovation and digital transformation on carbon performance under different ownership contexts.

The regression results in Table 10, Columns (1) and (2), show that the impacts of GI and DT on ESG performance vary significantly across firms with different ownership structures and market categories. For SOEs, both GI (0.473) and DT (0.500) have significant positive effects on ESG performance, with relatively high explanatory power (R² = 0.156), indicating that SOEs demonstrate a strong improvement in ESG outcomes through green innovation and digital transformation. Although GI (0.145) has a positive effect on non-SOEs, it is not statistically significant. At the same time, DT (0.438) significantly enhances ESG performance, reflecting the stronger reliance of non-SOEs on digital transformation to drive improvements in their ESG performance.

The enterprises’ ownership structure and market positioning are key factors contributing to this heterogeneity (Song et al. 2015). SOEs enjoy clear policy support, stronger resource acquisition advantages, and higher social responsibility requirements, giving them distinct advantages in promoting green innovation and digital transformation, significantly improving their ESG performance. Specifically, SOEs typically face strong government policy guidance and social responsibility pressures, which give them greater motivation and enthusiasm to implement green innovations. Policy supports and resource advantages enable SOEs to form effective synergies in areas such as technology research and development, green project investment, and digital infrastructure construction, thereby promoting the achievement of ESG goals. In contrast, although non-SOEs are equally concerned about ESG performance, their resource allocation and market positioning differ significantly from those of SOEs. As non-SOEs usually operate on a self-financing basis, they face greater market competition and have relatively limited resources. Therefore, non-SOEs rely more heavily on digital transformation to achieve cost reductions and efficiency improvements, thereby enhancing competitiveness and driving business development. This market-driven characteristic results in relatively lower investment in green innovation, leading to a lower implementation level and limiting improvements in ESG performance.

Startup

Given that enterprises at different development stages prioritize resource allocation, market positioning, and corporate social responsibility differently, analyzing the pathways and impact of green innovation on ESG performance from the perspective of enterprise development stages is crucial (Zheng et al. 2022). Therefore, this study further analyses the heterogeneity based on whether the company is listed on the growth enterprise market (GEM).

The regression results in Columns (3 and 4) of Table 10 show that, for GEM-listed companies, the impact of GI on ESG is positive but not statistically significant (0.222). At the same time, DT has a significant positive impact (0.478), indicating that while the effect of green innovation is weaker, digital transformation plays a more significant role in GEM companies. For non-GEM companies, GI (0.294) has a significant positive effect on ESG, indicating that green innovation plays a stronger role in driving ESG performance for these firms. Additionally, DT (0.413) also significantly enhances ESG performance, demonstrating that digital transformation contributes to improving ESG performance. The regression model for non-GEM companies is relatively low. Still, the high F-value suggests that green innovation and digital transformation significantly impact ESG performance in non-GEM companies.

This heterogeneity primarily stems from differences between firms in terms of their stage of development, resource allocation, and market positioning (Huang and Li 2018). GEM-listed companies are typically in the growth stage, facing dual pressures of rapid expansion and technological innovation; therefore, they tend to prioritize allocating resources toward rapid market share growth and technological breakthroughs. In contrast, green innovation, as a strategy that prioritizes medium- to long-term returns, has a relatively lower priority and struggles to secure sufficient resource allocation in the short term. As a result, digital transformation has become the primary means for GEM firms to enhance operational efficiency and market competitiveness, directly supporting their growth needs through optimized business processes and improved management efficiency. In contrast, non-GEM firms typically operate in more mature development stages, with robust resource accumulation and clear, sustainable strategic orientations for development. These companies have greater flexibility in allocating their resources. They can incorporate green innovation into their core development strategies, viewing it as an important means of enhancing long-term competitive advantages and fulfilling social responsibilities. Therefore, in non-GEM companies, green innovation plays a more significant role in enhancing ESG performance; simultaneously, digital transformation serves as an important supporting factor, synergizing with green innovation to drive corporate sustainable development and achieve ESG goals jointly.

Analysis of the sample according to the type of industry

Heavy pollution

Due to the significant differences in resource allocation, policy pressures, and market demands between heavy-pollution and non-heavy-pollution industries, analyzing the pathways and impact of green innovation on ESG performance from the perspective of industry type is of considerable importance (Huang 2024). Therefore, this study adopts the industry’s pollution level (heavy-pollution vs non-heavy-pollution) as a distinguishing dimension to explore the differential pathways and impacts of green innovation and ESG performance.

Table 11, Columns (1 and 2), presents the regression results examining the effects of green innovation and digital transformation on ESG performance in firms from different industries. In heavy-pollution enterprises (HPE), GI has a significant and positive influence on ESG performance (coefficient = 0.610, p < 0.05). At the same time, the impact of DT is even more pronounced, with a coefficient of 1.248, which is significant at the 1% level. These findings suggest that heavy-pollution enterprises experience a stronger ESG improvement effect from both green innovation and digital transformation, with the influence of digital transformation particularly noteworthy. For non-heavy-pollution enterprises (non-HPE), GI has a smaller yet still significant effect (coefficient = 0.202, p < 0.05), and DT also demonstrates a significant impact (coefficient = 0.291, p < 0.05).

The observed heterogeneity primarily stems from significant differences between HPE and non-HPE companies in terms of industry characteristics, environmental regulatory intensity, and social responsibility pressures (Donnelly 2022). HPE, due to the high environmental externalities generated during its production processes, typically faces stricter environmental regulations, policy constraints, and public oversight. This high external pressure has prompted HPE to increase its investment in green innovation and digital transformation, aiming to reduce environmental pollution, improve resource efficiency, and enhance its corporate social image, thereby significantly improving its ESG performance. Digital transformation, through smart manufacturing, green supply chain management, and data-driven environmental governance measures, can effectively optimize the operational efficiency and environmental performance of high-polluting enterprises, exerting a more significant positive impact on ESG performance. In contrast, non-HPE companies face less environmental pressure and focus more on efficiency improvements and cost control as part of their strategic priorities. Although green innovation also positively impacts ESG performance in non-HPE companies, its effect on ESG improvement is relatively limited due to its lower priority in resource allocation. At the same time, digital transformation is primarily used for internal management optimization and operational efficiency improvements, and its driving role in achieving SDGs is also relatively modest.

Manufacturing industry

Manufacturing and non-manufacturing industries differ in their core activities, resource usage, and focus on output, resulting in varying impacts on the relationship between green innovation and ESG performance (Shan et al. 2024). The sample is divided into manufacturing and non-manufacturing industries to explore these differences further for a more detailed industry comparison.

Table 11, Columns (3 and 4), presents the regression results for manufacturing (MFG) and non-manufacturing (non-MFG) sectors. Both GI and DT have a significant impact on ESG in MFG, with coefficients of 0.231 and 0.357, respectively, which is significant at the 5% level. This suggests that green innovation and digital transformation have a significant positive impact on ESG performance in the manufacturing sector. In non-MFG, the coefficient for GI is 0.320, which, while strong, is only significant at the 10% level. Conversely, DT has a more significant impact on ESG, with a coefficient of 0.542, which is significant at the 5% level. This suggests that although green innovation also plays a positive role in non-MFG, digital transformation has a more pronounced effect on enhancing ESG performance. The regression models for both sectors show similar explanatory power (R2), with the manufacturing sector having a higher F-statistic, indicating that the ESG performance of manufacturing firms is more strongly driven by green innovation and digital transformation.

MFG and non-MFG exhibit significant differences in the mechanisms through which green innovation and digital transformation impact ESG performance. These differences primarily stem from fundamental disparities in their production characteristics, resource consumption, supply chain complexity, and compliance cost structures (Wong et al. 2020; Yang and Lin 2020). MFG is characterized by high resource and energy consumption, intensive emissions, and long, cross-regional supply chains, resulting in more pronounced overall environmental impacts. Consequently, MFG faces stricter environmental regulations and higher compliance costs, including clean production audits, carbon emissions verification, and requirements for a green supply chain. This external pressure drives manufacturing companies to optimize their production processes through green innovation, aiming to reduce energy consumption and emissions. By leveraging digital transformation, they enhance supply chain transparency and resource allocation efficiency, achieve compliance objectives, and strengthen sustainable competitiveness. In contrast, non-MFG companies have lower overall resource consumption and smaller environmental externalities, resulting in relatively limited environmental regulatory and compliance cost pressures. While green innovation can also enhance ESG performance in non-manufacturing sectors, due to constraints on investment priorities, companies in these sectors primarily rely on digital transformation to optimize internal management, improve service quality, and boost operational efficiency, thereby indirectly promoting sustainable development.

Conclusions and implications

Conclusions

Based on data from A-share listed companies from 2014 to 2023, this study examines the intricate relationship between ESG performance, digital transformation, and green innovation. It draws the following key conclusions: (1) green innovation has a consistently significant positive effect on ESG performance, suggesting that it is a core driver of corporate sustainable development. (2) Digital transformation is not merely a direct way for companies to achieve sustainable development. Still, it also plays a partly mediating role between green innovation and ESG performance, further strengthening the positive effect of green innovation. (3) Various contextual factors, including public emergencies, executive perceptions, regional differences, firm characteristics, and industry diversity, moderate the impact of green innovation and digital transformation on ESG performance.

Discussions

Prior research has widely recognized the relationship between green innovation and ESG performance; however, the role of digital transformation as a mediator has received limited attention. This study is the first to investigate the mediating role of digital transformation in the relationship between green innovation and ESG performance, thereby addressing a significant gap in the existing literature. The findings reveal that digital transformation not only directly enhances ESG performance but also amplifies the impact of green innovation, thereby further improving ESG outcomes. These results align with previous studies (Sun et al. 2024; Zhao et al. 2023), emphasizing the critical role of digital technologies in promoting corporate sustainability. However, this study extends the theoretical framework by uncovering the enabling function of digital transformation in strengthening the effects of green innovation.

In addition, this study examines contextual factors, including the COVID-19 crisis and managerial cognition, and their moderating effects on the relationship. The results demonstrate the resilience of green innovation, which contributes significantly to ESG performance even during crises such as COVID-19, underscoring the necessity of institutionalizing green practices as a core corporate strategy. Furthermore, the study validates the critical role of managerial leadership in advancing green and digital transformations. Specifically, the moderating role of managerial green cognition underscores the pivotal leadership role in driving sustainable development strategies. These findings align with prior research (Dai and Tang 2022; Meng et al. 2023), offering novel insights into how these factors interact with digital transformation, green innovation, and ESG performance.

The study provides important implications for practice, emphasizing that companies should prioritize green innovation as a core strategy and leverage digital transformation to maximize its effects. Factors such as regional economic development levels, firm characteristics, and industry-specific traits are crucial variables that must be considered when implementing sustainable development strategies. Notably, the study finds that green innovation in non-SOEs has an insignificant impact on ESG performance, differing from Liu et al. (2024), potentially due to differences in the research sample. The exclusion of the financial sector in this study is justified by its unique operational characteristics and the ESG evaluation standards applicable to it. More importantly, regulatory policies and capital structures heavily influence ESG performance in the financial industry, which may obscure the effects of digital transformation and green innovation. Moreover, green innovation in the financial sector focuses on developing financial products and services, diverging from the innovation paths and frameworks of non-financial industries. Therefore, excluding the financial sector enhances the applicability and interpretability of the findings.

Moreover, the study finds that the government-led policy framework and incentive mechanisms profoundly shape the interplay between green innovation, digital transformation, and ESG performance within China’s unique institutional environment (Abdul et al. 2023). National strategies, such as “Made in China 2025” and “Digital China”, exemplify the role of central and local governments in driving the adoption of green technology through tax incentives, financial subsidies, green credit, and R&D investments. These efforts have been particularly effective in renewable energy, smart manufacturing, and digital infrastructure. SOEs, as the primary vehicles for policy implementation, leverage their institutional advantages in resource allocation and financing to spearhead green innovation projects and reinforce the institutionalization of sustainability practices through mandatory ESG disclosures and green credit evaluations. As a result, China has rapidly emerged as a global leader in sectors such as solar and wind energy, as well as industrial Internet technologies. In stark contrast, Western market-driven models prioritize firms’ responsiveness to consumer demand and capital market preferences, with innovation being primarily driven by market competition and relatively limited government intervention (de Bettignies et al. 2023). While the Chinese model offers the advantage of rapid deployment of green and digital technologies, it may suffer from rigid resource allocation due to potential misalignments between policy priorities and market signals. On the other hand, although the Western model progresses more slowly, it is more agile in adjusting strategic directions based on real-time market feedback (Wang 2018). This institutional divergence suggests that in the global context of sustainable development, it is essential to draw on the Chinese model’s strengths in large-scale deployment and institutional support, while also embracing the flexibility and innovation inherent in market-driven systems, to identify the most effective pathways for achieving green and digital transformation.

Implications

Based on the above findings and discussions, we put forward the following recommendations: