Abstract

The growing popularity of digital inclusive finance and the reduction of financial resource inequality are both benefits of digitization in the financial services sector; however, the uneven regional differences in the development of digital technologies have led to a digital divide, and exploring how this divide impacts the effect of digital inclusive finance on the promotion of common prosperity is highly practical. Drawing on panel data spanning 245 Chinese cities between 2012 and 2022, we constructed an economic distance matrix and explored the digital inclusive finance tool for promoting common prosperity via a spatial econometric model. The outcomes demonstrate that the advancement of common prosperity is greatly aided by digital inclusive finance, and the positive spatial spillovers are obvious. These results remain robust after substituting variables and removing a few examples. The connection between digital financial inclusion and shared prosperity is significantly influenced by the digital divide. There is a notable moderating influence of the digital gap on the link between common prosperity and digital inclusive finance. In terms of dimensional heterogeneity, breadth of coverage, depth of use, and digitization all contribute to shared prosperity. From the perspective of regional heterogeneity, the digital inclusive finance in the eastern region exerts a stronger effect on common prosperity than that in the central and western regions. Further improvements should be made to the building of digital infrastructure, the use of digital technology should be further increased, and the cultural literacy of residents should be further enhanced to encourage the prosperity of all people in common.

Similar content being viewed by others

Introduction

A report from the Twentieth National Congress of the Communist Party of China noted that the realization of common prosperity for all individuals is one of the essential requirements of Chinese modernization and that efforts should be made to safeguard and promote social justice, to work towards common prosperity, and to resolutely prevent polarization. Common prosperity represents the organic unity of the terms “common” and “rich,” which describes an “endurance race” that can neither wait nor be rushed (Yiyi et al., 2023). This is a journey in which the entire nation is united.

Digital inclusive finance refers to a financial service model developed through the utilization of digital technologies and innovative financial means. Leveraging its advantages, such as low cost, low barriers to entry, high efficiency, and convenience (Geng and He, 2021), it extends financial services to areas or populations that are beyond the reach of traditional finance, reduces information asymmetry, and enables more people to easily access financial services (Zeng and Sun, 2024). However, the “universality” of digital finance is also constrained; among them, the issue of the “digital divide” is particularly prominent. The digital divide refers to the gap that exists among different groups in terms of accessing, utilizing, and benefiting from digital technologies and services based on them. Its causes are multifaceted, manifesting not only in the possession of hardware facilities but also in aspects such as digital skills, digital literacy, as well as the awareness and acceptance of digital technologies (Fang, 2023). In addition, factors such as unbalanced regional economic development and uneven distribution of educational resources further exacerbate the formation of the digital divide (Chroufa and Chtourou, 2023). Digital inclusive finance aims to expand the coverage of financial services, enhance their accessibility, enable more people to seize development opportunities, and promote economic growth and social equity. This is highly consistent with the goal of common prosperity, which emphasizes “sharing the fruits of development and narrowing the wealth gap.” However, in reality, the digital divide prevents disadvantaged groups from fully enjoying the benefits of digital inclusive finance, further marginalizing them, widening the wealth gap between regions and groups, and impeding the realization of common prosperity. To transform this digital divide into a form of digital empowerment to promote the pursuit of common prosperity, attention should be given to the construction of digital infrastructure in rural and remote areas, the lowering of barriers to financial access, the conducting of digital financial popularization courses, and the improving of the relevant policy system to increase the entrepreneurial activity of rural dwellers, enhance rural citizens’ standard of living and promote the growth of the private sector (Huang et al., 2021; Lee et al., 2023). Because of this, digital inclusive finance is used as an entry point to create a matrix of economic distance, and the spatial lag model (SAR), spatial error model (SEM), and spatial Durbin model (SDM) are utilized to investigate the particular channels by which digital inclusive finance fosters common prosperity. This paper is focused on exploring the mechanism, spillover effect, and regional heterogeneity of the effects of digital inclusive finance on common prosperity and clarifying the moderating role of the digital divide in this relationship (Sha et al., 2024).

This article’s remaining sections are organized as follows. The study hypotheses and a review of related literature are provided in the second part; in the third part, the data is described and the empirical strategy is introduced; in the fourth part, the spatial regression results are reported in detail and the test for robustness is related; in the fifth part, the moderating role of the digital divide is explored; in the sixth part, An analysis is conducted on how heterogeneity in digital inclusive finance affects inequality in common prosperity; and in the seventh part, the conclusion and recommendations are provided.

Literature review and research hypotheses

Connotation of common prosperity

Achieving common prosperity is a multilevel, multi-connotation systematic project that requires a social change to reduce the wealth disparity between the affluent and poor so that people can obtain a sense of well-being (Liu et al., 2023). Essentially, this change would enable people to live better lives by continuously improving the production level and enhancing the level of comprehensive national strength within the framework of a socialist regime featuring Chinese features (Dong et al., 2023). The existing indicator system for common prosperity is still insufficiently comprehensive, and the indicator system changes according to its stage of development. Generally, the focus of the quest of common prosperity is placed on the questions of “what,” “how to do” and “how,” and based on the theoretical connotations of common prosperity and following the principles of coordination, continuity, comprehensiveness and foresight, an indicator system is constructed by accounting for individual differences in the assessment of the overall situation (Zhang et al., 2023). The factors influencing the realization of common prosperity are multifaceted and can be broadly classified into three categories: institutional, market-related, and technological. Institutional factors encompass aspects such as the adequacy of the social security system (Cheng and Zhang, 2022) and the effectiveness of tax regulation (Yang and Zeng, 2025). Market-related factors involve areas like industrial structure upgrading (Yang et al., 2024a) and market competition dynamics (Sun and Li, 2022). Within technological factors, the internet penetration rate (Li et al., 2023) and the coverage rate of digital infrastructure (Zhang and Qian, 2023) have emerged as novel enabling elements. Currently, the majority of research focuses on traditional approaches to exploring the pathways to common prosperity, while paying insufficient attention to the new driving forces that have emerged in the wake of the digital technology revolution. As the digital economy continues to evolve in depth, the role of digital inclusive finance in promoting common prosperity has become increasingly prominent. However, existing literature rarely conducts an in-depth analysis from the perspective of digital inclusive finance empowerment regarding its impact mechanisms, action pathways, and the challenges it faces in relation to common prosperity. This has led to a lack of comprehensiveness and depth in research on the realization paths of common prosperity. The theoretical vacuum stands in sharp contrast to the rapid penetration of digital inclusive finance in empowering common prosperity. Therefore, gaining a profound understanding of the development of digital inclusive finance is instrumental in enriching both the theoretical research and practical exploration of common prosperity (Sha et al., 2024).

Impact of digital inclusive finance on common prosperity

As a significant practical achievement of fintech innovation, digital inclusive finance shares a profound internal consistency with the concept of common prosperity in its core characteristics. This alignment is mainly manifested in the two dimensions of “inclusiveness” and “affordability,” corresponding respectively to the core connotations of “commonality” and “prosperity” in common prosperity (Wu et al., 2023). In terms of the “inclusiveness” aspect of digital inclusive finance, big data risk control technology effectively mitigates information asymmetry; the mobile payment network extends the service radius to the “last-mile” blind spots of traditional finance; blockchain technology enables transparent supervision of supply chain finance (Xu, 2024), Through a series of such measures, vulnerable groups who were previously on the fringes of the financial system can now be integrated into it, truly achieving widespread access to financial services (Zhang et al., 2024). The “commonality” in common prosperity means that all people share in the fruits of development. Hence, “inclusiveness” resonates with “commonality” (Zhou et al., 2023). The “affordability” aspect of digital inclusive finance can bring about value enhancement. Smart investment advisors lower the threshold for wealth management, cloud computing reduces the cost of loan approvals, and AI - powered customer service systems provide real - time online support (Jiang et al., 2024), by reducing the marginal cost of financial services, these measures effectively stimulate residents’ entrepreneurial enthusiasm and investment willingness, directly increasing residents’ property income and offering a quantifiable path to achieving the goal of “prosperity” (Jiao et al., 2024; Ololade, 2024).

There are multi-dimensional mechanisms through which digital inclusive finance influences common prosperity and its spatial effects (Gabor and Brooks, 2017). At the direct impact level, by leveraging the internet and big data technologies to break through time and space constraints, the emergence of services like online microloans and mobile payments enhances the accessibility of financial services (Beck et al., 2018). This enables groups such as rural entrepreneurs to access financial support, increase their incomes, and lay a solid material foundation for common prosperity. Through digital operation models, it reduces costs such as those for branch rentals and labor, and utilizes big data to accurately assess credit risks, thereby achieving low-cost service provision and optimizing the allocation of financial resources, which drives an increase in the incomes of all residents. Digital inclusive finance platforms also popularize financial knowledge through various channels, enhancing residents’ financial literacy and helping to narrow the wealth gap (Mader, 2018). In terms of indirect impacts, it provides convenient financing channels for entrepreneurs, lowers the barriers to entrepreneurship, spurs job growth and industrial upgrading and transformation, and boosts economic competitiveness (Acharya and Xu, 2017). It facilitates the digital and intelligent upgrading of traditional industries, drives the development of related service industries, and optimizes the income distribution structure. Moreover, it enhances social inclusivity, enabling vulnerable groups to enjoy equal access to financial services, creating development opportunities for impoverished regions and low-income groups, and promoting social equity (Liu et al., 2017). Regarding spatial effects, it breaks down geographical barriers, promotes the inter-regional flow of financial resources, achieves optimal allocation, and narrows the economic development gaps between regions. Its rapid development in a certain area generates spatial spillover effects, driving the development of surrounding regions. Meanwhile, it fosters the formation and diffusion of regional innovation networks, enhancing regional innovation capabilities and providing technological support for common prosperity (Ge et al., 2022). As a result, the following theory is suggested:

Hypothesis 1: Digital inclusive finance effectively encourages common prosperity.

Digital divide, digital inclusive finance, and common prosperity

In recent years, with the rapid development and widespread adoption of digital technologies, the issue of the digital divide has gradually become a focal point of academic attention (Scheerder et al., 2017). Although the internet theoretically provides all members of society with equal opportunities to participate in the digital society, significant disparities still exist in different groups’ access to and ability to use digital technologies due to differences in regional economic development levels, infrastructure construction, and resource endowments (Vassilakopoulou and Hustad, 2023). Particularly under the urban-rural dual structure, disparities in residents’ educational attainment and financial literacy further exacerbate the digital divide (Khera et al., 2022; Ugwuanyi et al., 2022). According to existing research, the digital divide can be divided into three levels: the access divide, usage divide, and capability divide (Feng et al., 2022a). Firstly, at the level of the access divide, with the in-depth implementation of the “Broadband China” strategy and the continuous improvement of digital infrastructure, the gap in network coverage between urban and rural areas is gradually narrowing. From 2014 to 2022, the proportion of administrative villages in China with broadband access increased from 65% to 100%, and the annual growth rate of internet penetration in rural areas reached 8.2% (Zhang and Qian, 2023). In particular, the construction of “Broadband China” demonstration cities fully reflects the government’s determination to eliminate the “last mile” obstacles to digital access (Arner et al., 2017). Secondly, the usage gap has become the primary manifestation of the current digital divide. According to the “Survey and Analysis Report on Digital Literacy in Rural China Under the Background of Rural Revitalization Strategy” released by the Information Research Center of the Chinese Academy of Social Sciences, there is a significant disparity in digital literacy between urban and rural residents. Urban residents scored an average of 56.3, while rural residents scored an average of 35.1, resulting in a gap of 21.2 points. Urban residents are able to leverage the internet for high-value activities such as online education and remote work, forming a “productive digital application” model. In contrast, rural residents predominantly remain at the level of basic communication and entertainment applications, trapped in a cycle of “consumptive digital use.” Even with similar hardware access conditions, there remains a notable difference in the efficiency of digital resource utilization between urban and rural populations. The limited diversity of technology application scenarios directly restricts the release of digital dividends in rural areas (Arner et al., 2020). Lastly, the impact of the capability gap is becoming increasingly pronounced, forming a deep-seated barrier hindering inclusive digital development. The core issue of the third-level gap lies in the generational and regional disparities in digital literacy: rural residents and elderly groups, constrained by the lack of basic educational resources, exhibit structural deficiencies in “meta-skills” such as financial literacy and cybersecurity awareness. This capability gap not only results in insufficient depth in digital technology usage but also creates a vicious cycle of “dare not use—cannot use—use poorly” due to weak risk prevention capabilities. Alarmingly, the capability gap is now compounding with the usage gap, subjecting vulnerable groups to dual exclusion in the digital economy and becoming a critical bottleneck impeding the achievement of digital inclusivity goals (Cao et al., 2021).

The advancement of digital inclusive finance relies on the support of digital technology and is therefore also affected by the digital divide. Early on in the evolution of inclusive finance through digital, the digital divide phenomenon between regions became serious, and the residents of regions with high digital technology levels took the lead in terms of enjoying digital dividends (Ozturk and Ullah, 2022); however, the income gap between poor and remote regions gradually increased due to their suboptimal facilities. With an increase in network coverage, the digital divide gradually narrows, and the promotion of common prosperity is amplified by digital inclusive finance (Appiah et al., 2022); however, digital inclusive finance does not always promote common prosperity, and digital inclusive finance even inhibits common prosperity when the digital divide reaches a certain level (Feng et al., 2022b; Mao et al., 2023). Therefore, the three dimensions of the digital divide each have a distinct moderating effect on the way that digital inclusive finance affects common prosperity for all (Wang et al., 2023). From a spatial perspective, in addition to having an impact on the common prosperity of a region, digital inclusive finance also radiates outward to influence the overall prosperity of nearby regions (Wang et al., 2021; He et al., 2022). The advancement of digital inclusive finance drives the radiation effect toward the most wealthy and uses the spillover effect to propel the growth of the economy of the relatively backward regions to obtain the dividends of development to achieve common prosperity (Wang et al., 2022; Xu et al., 2023). As a result, here are some theories that this study puts out:

Hypothesis 2: The digital divide serves as a moderating factor in the relationship between digital inclusive finance and common prosperity.

Hypothesis 3: There are spatial spillover effects from digital inclusive finance on common prosperity.

Design of research, choice of variables, and description of data

Overview of the study region

In the process of China’s active promotion of digital inclusive finance development and the common prosperity goals, different regions have exhibited differentiated development trends. Eastern coastal provinces represented by Zhejiang Province have demonstrated particularly outstanding performance. Benefiting from a vibrant private economy, well-developed digital infrastructure, and strong policy support, Zhejiang has witnessed rapid growth in digital inclusive finance, with innovative services such as mobile payments and online lending becoming widely adopted. This has not only significantly improved financial service accessibility but also facilitated its designation as the nation’s first common prosperity demonstration zone. First-tier cities like Beijing, Shanghai, and Shenzhen, leveraging their robust economic strength and technological innovation advantages, have utilized digital inclusive finance to drive industrial upgrading and foster innovation and entrepreneurship, achieving remarkable results in resident income growth and social security system improvement. Meanwhile, nationwide, digital inclusive finance supported by technologies such as mobile payments, big data, and blockchain has significantly expanded financial service coverage, effectively alleviating financing difficulties for traditionally underserved groups such as small and micro enterprises and low-income populations. It has become a crucial tool in narrowing urban-rural and regional disparities. Against this backdrop, this study focuses on the development trajectory of 245 Chinese cities from 2012 to 2022, a period marking the critical phase from the emergence to the rapid expansion of digital inclusive finance in China. Given the spatial interdependence of economic phenomena, the research constructs an economic distance matrix to incorporate intercity economic linkages into the analytical framework, thoroughly examining the mechanisms through which digital inclusive finance influences common prosperity and its spatial heterogeneity. Despite persistent challenges in regional balance, data security, and regulatory compliance, the continuous innovation in digital inclusive finance by lowering service barriers and optimizing resource allocation is providing vital support for China’s pursuit of common prosperity.

Research method

Setting the weighting matrix

To measure spatial correlation, an economic distance matrix is constructed as a spatial weighting matrix W. By comparing the per capita gross domestic product (GDP) of the cities, the utilization of the economic matrix facilitates the computation of the economic distance between them. The economic distance is shortest when there is more frequent economic transit between cities. The expression is:

The equation in formula (1) depicts the GDP per capita of city i in 2021.

Spatial correlation

Global spatial correlation refers to the distribution characteristics of the analyzed spatial data throughout the study area, and to determine the correlation coefficients between observations and geographically lagged variables, the global Moran’s I index is frequently utilized, which is calculated using the following formula:

Where the global Moran’s I measures spatial autocorrelation, n signifies the total number of regions, xi and xj indicate the level of common prosperity in regions i and j, respectively, and Wij represents the spatial weight matrix that captures the relationships between these regions.

Local spatial correlation is used to test for spatial aggregation in local areas. The Local Indicator Spatial Association (LISA), sometimes referred to as the local Moran’s I, is employed in this study to show the level of geographical connection in a region.

Where “high-high” and “low-low” aggregation are included in a positive LISA, suggesting that the high and low values within the research unit tend to cluster with similarly high and low values in their surroundings. Conversely, in a negative LISA, the high (or low) values of the research unit are encircled by low (or high) values, exhibiting a “high-low” or “low-high” aggregation pattern.

Spatial econometric model

The SAR, SEM, and SDM are the most widely utilized spatial measurement models. The specific models are shown below:

where y is the explanatory variable, X is the n × k dimensional matrix of explanatory variables, W is the spatial weight matrix, in the dependent variable, the spatial autocorrelation coefficient is denoted by ρ; in the independent variables, it is represented by θ; in the vector of correlation parameters, by β; and in the spatial error coefficient, by λ,\(\,{\rm{\alpha }}\) is the constant term, the random error terms are μ and ε, and the nth-order unit matrix is denoted as In.

(1) The SAR model is obtained when \({{\rho }}\) ≠ 0 and \({\rm{\theta }}\) = 0, \({{\lambda }}\) = 0;

(2) The model is an SEM when λ ≠ 0, ρ = 0, and \({\rm{\theta }}\) = 0;

(3) The model is an SDM when ρ ≠ 0, \({\rm{\theta }}\) ≠ 0, and λ = 0.

Variable selection

Explained variables

Common prosperity is the explanatory factor (cp). The evaluation index system for common prosperity is constructed around two core dimensions: “commonness” and “prosperity.” It systematically assesses the degree of economic development (“prosperity”) while scientifically measuring the level of sharing development outcomes (“commonness”). The “commonness” dimension focuses on the inclusive sharing of development achievements, encompassing both prosperity disparity and sharing mechanisms. By measuring disparities among regions, urban-rural areas, and different social groups, it reflects the realization of social equity and justice. The “prosperity” dimension emphasizes the coordinated development of material and spiritual civilization. It comprehensively characterizes the provision level of basic public services and ecological environment resources across multiple aspects, including economic development, cultural education, social security, ecological environment, and income-consumption patterns.

Based on existing research findings and data availability, this study establishes an evaluation system comprising 4 first-level indicators, 9 second-level indicators, and 12 third-level indicators (as shown in Table 1). To ensure the objectivity of indicator weighting, the entropy method is employed to scientifically calculate and synthesize the common prosperity development index for each city (Chen et al., 2021; Han et al., 2023).

Core explanatory variables

The development level of digital financial inclusion (dif) is measured using the Digital Financial Inclusion Index calculated by the Peking University Digital Finance Research Center and Ant Group. This index encompasses three key dimensions: coverage breadth (coverage), usage depth (usage), and digitalization level (digital). It covers 31 provinces, 337 prefecture-level cities, and 2800 counties in China, demonstrating strong credibility and reliability. To ensure the accuracy of regression results, all data values are divided by 100 to reduce scale differences among the variables (Fang, 2023).

Control variables

In this research, the study incorporates the use of the following control variables: industrial structure (is), as determined by the tertiary industry’s added value as a percentage of the city’s GDP; the maturity of traditional financial systems (loan), as measured by the proportion of the end-of-year financial institution loan balance to the regional GDP; innovation capacity (ino), represented as the number of awarded patents logarithmically; innovation capacity, expressed as the logarithm of the number of patents granted; proportion of total foreign trade that reflects a country’s degree of openness to the outside world; the total amount of import and export, expressed as a proportion of regional GDP; the level of technology (tech), stated as a percentage of the local GDP to the amount spent on research and technology; the government regulation (gov), expressed as a proportion of the public budgetary expenditure of the cities to regional GDP; and the basic education (edu), expressed as the logarithmic ratio of elementary and secondary school teachers to 10,000 urban residents.

Moderating variables

The access, usage, and efficiency divides are the three categories into which the digital divide may be split. The access divide (ac- divide) is caused by differences in “digital access,” which is characterized by differences in the density of fiber-optic cables, the density of mobile base stations, and the number of Internet broadband accesses in different regions. This hardware difference is also called the “hard divide” (Qiu et al., 2023). The inverse of Internet broadband coverage was chosen to gauge the degree of “access” in each region, examining the access divide.

The usage divide (us- divide) refers to the difference in the utilization of digital technologies based on the different conditions of digital infrastructure (Wei et al., 2011). This variable is mainly measured by the internet penetration rate and the popularity of smartphones, including both frequency and method of use. The inverse of the year-end number of users of cell phones per 100 individuals was chosen to measure the usage divide.

The efficiency divide (ef- divide) refers to individual differences in the level of access to and the use of digital technology due to educational differences and differences in economic capacity. Thus, the efficiency divide is closely related to individual cultural literacy, and the inverse of the proportion of the population with a general education degree or higher was chosen to measure the capability gap. The larger the three indicators, the deeper the digital divide.

Data description

Based on data availability and completeness, this study utilizes panel data from 245 prefecture-level cities spanning 2012 to 2022, comprising a total of 2695 sample observations. Data on digital financial inclusion were obtained from the Peking University Digital Financial Inclusion Index (2011–2023), while other variables were primarily sourced from the China Statistical Yearbook, China City Statistical Yearbook (2013–2023), as well as provincial and municipal statistical yearbooks and bulletins. Missing values for specific indicators were addressed using interpolation methods. To mitigate the influence of outliers, the core explanatory variable (common prosperity) and control variables were winsorized at the 1% level. The descriptive statistics for all variables are presented in Table 2 below.

Empirical analysis

Spatial correlation test

As indicated by Table 3, the Moran’s I value of common prosperity and digital inclusive finance over the period from 2012 to 2022 are both greater than 0 and significant at the 1% level, demonstrating the positive spatial correlations between digital inclusive finance and common prosperity and that both exhibit aggregation characteristics.

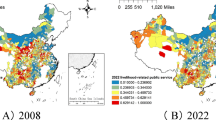

To examine the exact degree of spatial correlation in a particular region, a more intuitive expression is used in the form of a localized Moran scatterplot, and space constraints result in only the results for 2012 and 2022 for shared prosperity and digital inclusive finance being reported. As shown in Figs. 1 and 2, the first and third quadrants are primarily where shared prosperity and digital inclusive finance are found, respectively, suggesting that both exhibit positive spatial correlation within a certain range.

Localized Moran Chart of Common Prosperity for 2012 and 2022.

Localized Moran Chart of the Digital Inclusive Finance Index for 2012 and 2022.

Spatial measurement results and analyses

Model construction

The three spatial econometric models were subjected to the Hausman test, LM test, and LR test in turn, and the spatial Durbin fixed effect model was ultimately chosen to study the effects of digital inclusive finance on common prosperity. Here’s how the model is put together:

Where i symbolizes various cities, t denotes several years, W is a spatial weight matrix, μ is an individual effect, λ is a time effect, and ε is a random perturbation term.

Spatial benchmark regression

As shown in Table 4, under the SAR, SEM, and SDM models, at the 1% significance level, every coefficient related to digital inclusive finance is positive; they are all negative about the initial hypothesis, demonstrating that the achievement of common prosperity is facilitated by digital inclusive finance. In the SAR model, the spatial autocorrelation coefficient of common prosperity is 0.3033, which is noteworthy at the 1% level. This indicates that there is a positive spatial spillover effect of common prosperity, i.e., boosting the degree of common prosperity in a particular city can enhance the level of common prosperity across cities that engage in close economic interactions with the city via spatial transmission. According to the SEM results, with a substantial value of 0.2942 at the 1% level, the spatial error coefficient of common prosperity indicates that although different unobservable factors affect the degree of common prosperity in different directions, they generally exert a positive effect.

The SDM model estimation results show that the spatial lag term coefficient of digital inclusive finance is positive and statistically significant at the 1% level, indicating that digital inclusive finance has a positive spatial spillover effect. Due to the close inter-regional economic linkages formed by trade, industrial cooperation, capital flows, and other economic factors, the development of digital inclusive finance not only promotes common prosperity in the local region but also, through mechanisms such as financial resource flows, technology diffusion, and industrial synergy, effectively drives improvements in corporate financing conditions, increases in household income, and enhancements in social welfare in economically connected regions. This process is facilitated by the transmission effect of the economic weight matrix, thereby advancing the realization of common prosperity through coordinated regional economic development. The growth in output value of the tertiary industry has a negative and considerable impact on the prosperity of society, as indicated by the regression findings of the control variables, indicating that the realization of the common prosperity needs to give greater consideration to the improvement of the quality and quantity of the existing industrial structure and the development of the domestic market (Jiang et al., 2022). The negative and significant development of traditional financial level may be due to the fact that urban residents have easier access to bank financial services than rural residents, and the regional development is not balanced; the enhancement of technology level and basic education play a considerable role in the promotion of common prosperity in the region, probably because technology itself can result in economic expansion, increase employment opportunities, and raise the level of income, while the popularization and enhancement of education can help to enhance human capital and provide a strong support for common prosperity to provide strong support (Shen et al., 2023). Innovation capacity is a core driver of economic growth, and regions with strong innovation capacity are more able to attract investment and talent (Xu et al., 2020). In terms of government regulation, the local government can increase its support for poor groups through the promulgation of policies, increased financial subsidies, etc., in an effort to reduce the wealth disparity.

On this basis, Table 5 displays the findings of effect decomposition, which was carried out on the SDM using the partial differential approach. At the 1% level, the direct, indirect, and total effects are all significantly positive, indicating that digital inclusive finance in the region not only promotes the common prosperity of the city itself but can also promote the common prosperity of other regions. In other words, the advancement of common prosperity benefits from digital inclusive finance as a whole.

Robustness test

Excluding the sample of prefecture-level cities in Zhejiang Province

In 2021, Zhejiang became the pioneer area for common prosperity, carrying the future expectations of the whole country for a better life and taking the lead in exploring the path toward common prosperity. In recent years, Zhejiang Province has accelerated the development of its digital economy; network financial products are also increasingly rich and optimized; the residents of Zhejiang Province have a relatively high degree of acceptance for and application of digital financial services. The development of digital finance is leading. The market size, competition pattern, and technology applications may be different from those of other regions. Prefectural-level city samples from Zhejiang Province are not included in the sample to guarantee its representativeness and prevent research bias. Based on the regression analysis, each variable’s coefficients’ direction and significance in the three models after the exclusion of prefecture-level cities in Zhejiang Province are in accord with the initial outcomes, which indicates the strength of the above conclusions.

Primary explanatory factors trailing one period

The regression estimation of the explanatory variables digital financial inclusion index lagged one period, is helpful to alleviate the endogeneity problem. According to the regression results, the direction of the coefficients and the significance of each variable are consistent with the previous section, and the conclusion is robust.

Replacement of the spatial weight matrix

The geographical distance spatial weight matrix was used to replace the economic distance spatial weight matrix for regression analysis. Columns (7)–(9) in Table 6 show that the regression coefficients of the core explanatory variable (dif) remain significantly positive, consistent with the results based on the economic distance spatial weight matrix, and are statistically significant at the 1% level. This indicates that the findings are robust.

Analysis of the regulatory mechanism

The analysis described in Section 2.3 shows that the digital divide is one way that common prosperity can be impacted by digital inclusive finance, and the SDM is used to construct a moderating effect model with which to explore the moderating mechanism underlying the three dimensions of the digital divide on how common prosperity is impacted by digital inclusive finance.

Model design

Utilizing the model of moderating effects. Based on Model 7, constructing the moderating model that follows by adding the internet coverage in reverse, inverse of the number of mobile telephone subscribers per 100 population at the end of the year, the inverse of the proportion of the general population with a bachelor’s degree or higher, and their interaction term with digital financial inclusion:

where Dit are the moderating variables. The three dimensions of the digital divide include the inverse of the Internet coverage rate, the inverse of the number of end-of-year cell phone subscribers per 100 people, and the inverse of the proportion of the population with a general bachelor’s degree or higher.

Test of moderating effects

-

(1)

Access Divide

Column 1 of Table 7 reports the moderating effect of the access divide under the SDM. The findings of the regression show that the value of the coefficient for digital inclusive finance is positive, and the reciprocal of the proxy variable for access divide, Internet broadband coverage, has a significantly negative interaction term with digital inclusive finance (dif*ac-divide), demonstrating that with the rise in the percentage of consumers with broadband Internet access and the increasing improvement of the digital infrastructure construction, the digital access divide is getting smaller and smaller, and the digital inclusive finance has a noteworthy role in realizing common prosperity. The promoting role of digital financial inclusion for realizing common prosperity gradually strengthens. Additionally, the role played by hardware facilities shows a marginally decreasing trend, and the impact of the access divide on the development of digital inclusive finance for common prosperity is negatively reducing. In areas that have poor digital infrastructure conditions, residents have limited consumption levels and low affordability regarding the purchase of electronic devices and the payment of network access costs. Under its low threshold, the phenomenon of information asymmetry should be reduced, etc., to increase the income and consumption level of residents, improve the living standards of residents, and help promote common prosperity. As a result, communities should think about how to develop electronic equipment in each household and network infrastructure, close the digital access gap, and create a bridge that will allow digital inclusive finance to help more people.

Table 7 Moderating affect test results. -

(2)

Usage Divide

Column 2 of Table 7 details the moderating effect of the usage divide under the SDM. The findings of the regression indicate that the coefficient value for digital inclusive finance is positive, and the inverse of the interaction term between the proxy variable for the usage divide, the number of end-of-year cell phone subscribers, and digital financial inclusion (dif*us-divide) is remarkably favorable, showing that with an increase in the number of end-of-year mobile phone subscribers, the usage divide shrinks, and meanwhile, there is a decline in the impact of digital inclusive finance on advancing common prosperity, i.e., the usage divide exerts a reinforcing moderating effect in the impact of digital inclusive finance on promoting common prosperity. At present, with the development of digital technology, the internet penetration rate and the quantity of people using mobile phones by the end of the year have both gradually risen, and the ways that urban and rural dwellers make payments, engage in entertainment, and interact socially are still different. For most rural residents, the internet offers more convenience regarding social interactions and entertainment. In contrast, for those of higher socioeconomic status, the internet and digital information streamlined the office and increased the efficiency of utilizing social values, and the usage divide may further exacerbate the established inequalities when compared to them. When mobile phone penetration is low, digitally inclusive finance has a greater potential for promoting shared prosperity.

-

(3)

Efficiency Divide

Column 3 of Table 7 reports the moderating effect of the efficiency divide under the SDM. As can be seen from the regression results, the coefficient value of digital financial inclusion is positive, and the inverse of the proxy variable for the ability divide, the proportion of the population with a general bachelor’s degree or higher, is significantly positive in the interaction term (dif*ef-divide) with digital financial inclusion. As the quality of culture and ability improves, the efficiency divide narrows, and more and more of the population are able to enjoy the dividends of digital inclusive finance, and the efficiency divide strengthens the effect of digital inclusive finance on common prosperity The promotion effect may be because it is easier to obtain human capital investment in a region where the average education level is low. The higher that the education level of a regional population is, the faster the new technology spreads in that region. Furthermore, people with a higher education are better able to use information and network technology and to profit from such use, which improves the feedback mechanism for the development of the local economy.

Heterogeneity test

Dimensional heterogeneity

Three subdimensions make up the general idea of “digital inclusive finance”: the extent of coverage, the depth of use, and the degree of digitization, and different dimensions may exert different impacts on common prosperity. The three subdimensions are delayed by one period and used as the core explanatory variable for rerunning regression analyses via the SDM, along with Table 8 displaying the regression results.

As displayed in Table 8, breadth of coverage, depth of use, and digitization fulfill the 1% threshold for the significance test, and all three can advance common prosperity, as shown by the positive regression coefficients. After assigning spatial weights, the regression coefficient of breadth of coverage (W*coverage) is −0.0611, which passes the significance level but exhibits a negative externality. Digital finance’s account coverage is primarily distinguished by its breadth, such as the ratio of Alipay card-bound users to Alipay accounts, and the number of Alipay accounts per 10,000 persons, etc. With the expansion of financial coverage, regions with more complete financial services will attract more resources, exacerbate inter-regional inequality, and then negatively affect the common prosperity. Both depth of use (W*usage) and digitization (W*digital) are noteworthy at the 1% level, i.e., there are spatial spillover effects.

Regional heterogeneity

Due to the unbalanced economic development of each region, as well as regional resource bases, the policy implementation effect differs. The effect of digital inclusive finance on the promotion of common prosperity varies across regions by the geographic location of 245 prefectural cities, according to east, middle, and west group regressions, which included 92 eastern city samples, 83 central city samples, and 70 western city samples. Specific findings are displayed in Table 9 for the SDM with fixed effects, which was built independently to test for heterogeneity.

Regression analysis shows that, at the one percent level, the regression coefficients for digital inclusive finance are considerably positive in both the eastern and western areas, showing that the promotion of common prosperity in both the east and the west of China is aided by digital inclusive finance. A possible reason is that in the eastern region, economic development has accelerated, digital inclusive finance has developed earlier, the digital foundation has strengthened, and both urban and rural residents have wider recognition and acceptance, active thinking, and a greater ability to grasp opportunities. Based on these dynamics, digital inclusive finance gives full play to its own dividends. In the western region, due to an inclination towards western development and other policies, the infrastructure has gradually improved, and the effect of digital inclusive finance on the promotion of common prosperity has become increasingly prominent (Yang et al., 2024b; Zhao and Jiao, 2024). In the central region, digital inclusive finance has no appreciable impact on societal development, probably because the central region exhibits insufficient resource allocation; the siphoning effect causes the central region to lose talent and resources to the east and west. The amount of the influence of digital inclusive finance on each region’s overall prosperity can be compared to the size of the regression coefficient, and the outcomes demonstrate that the eastern region is the one with the greatest impact, proving the influence of digital inclusive finance on the shared prosperity of regional heterogeneity (Sun et al., 2023; Ji et al., 2021).

Conclusions and recommendations

Conclusion

Based on the panel data of 245 prefecture-level cities covering the period from 2012 to 2022, the mechanism underlying the link between digital inclusive finance and communal prosperity is investigated using the spatial econometric model, and the findings that follow are determined: common prosperity and digital inclusive finance both show positive spatial correlations in the economic distance matrix, and a spatial aggregation phenomenon, which manifests itself as a high-high aggregation and a low- low aggregation, occurs. Regardless of model, SAR, SEM, or SDM, common prosperity can be greatly enhanced by digital inclusive finance, and the conclusion still holds after excluding some samples for the robustness test. Further, Spatial spillover effects on common prosperity are observed in digital inclusive finance, since it fosters prosperity for everyone in the area as well as in other areas with a high degree of economic similarity, so its spatial component must not be disregarded. when exploring the relationship between the two. The different dimensions of the digital divide exert significant moderating effects on the link between digital inclusive finance and common prosperity. The access divide manifests an inhibitory moderating effect, while the use and ability divides manifest a reinforcing moderating effect; in terms of dimensional heterogeneity, the three dimensions of the digital divide have effectively contributed to the common prosperity. From a subregional perspective, common prosperity between the territories to the east and west is greatly enhanced by the growth of digital inclusive finance, and its spillover effect also promotes common prosperity in other regions with high degrees of economic similarity. Financial development significantly promotes common prosperity both in the east and the west, while the effect on the central region is nonsignificant.

Recommendations

First, strengthen regional coordination to unleash the cross-regional dividends of digital inclusive finance. Given the spatial autocorrelation of digital inclusive finance, which exhibits high-high and low-low clustering patterns, efforts should be made to enhance spatial connectivity among regions. On the one hand, regional collaboration and spillover effects should be strengthened. Advanced regions in digital inclusive finance should take the lead in forming cooperative alliances with neighboring underdeveloped areas, holding regular meetings to discuss development plans and formulate assistance programs, such as dispatching professionals for on-site guidance and establishing special funds to support projects. On the other hand, the advantages of high-development regions should be leveraged to accurately assess financial needs using big data, innovate financial products and services, and formulate targeted financial policies. Cross-regional flows of financial resources should be promoted by encouraging collaboration between financial institutions and technology companies to share digital dividends. At the same time, an early warning and monitoring mechanism should be established to mitigate the negative spillover effects of low-development regions. The differential impacts of the three subdimensions of digital inclusive finance on common prosperity should be precisely assessed, and digital technology barriers should be lowered. Policies should be promptly adjusted based on varying stages of development. Second, improve digital infrastructure and education to bridge the digital divide. Strengthening digital infrastructure construction is pivotal for advancing digital inclusive finance. Governments should increase investment in broadband network expansion, particularly in rural areas, with annual targets for connecting a specified number of additional administrative villages. A coordinated mechanism for allocating digital resources should be established to ensure equitable distribution of financial resources based on regional economic development levels and population distribution. Additionally, internet access and usage costs must be reduced through negotiations with service providers for lower tariffs and targeted subsidies for low-income groups and underserved regions, ensuring affordability for all households. Complementing these efforts, comprehensive internet education and training programs should be widely implemented. Schools, communities, and enterprises should offer diverse courses to encourage public participation. Traditional and new media channels should be leveraged to disseminate financial knowledge, enhancing residents’ financial literacy and digital application skills, thereby narrowing the digital divide. Third, implement differentiated strategies to promote balanced regional development. Tailored approaches should be adopted based on varying levels of digital inclusive finance development across regions. In eastern regions, where financial infrastructure is well-established and fintech adoption is advanced, efforts should focus on refining the digital financial ecosystem and relevant legal frameworks; strengthening regulatory oversight over fintech innovation; and deepening integration between digital finance and the real economy through pilot demonstration projects for broader replication. For western regions, which have seen progressive infrastructure improvements due to policy support and strategic initiatives, priorities include: sustaining efforts to attract external investments and corporate presence; enhancing local talent cultivation and recruitment in digital inclusive finance. Central regions should implement measures to retain resources and curb outflow, such as introducing incentives to anchor local capital and enterprises; fostering collaboration with advanced regions to facilitate knowledge transfer and resource sharing; leveraging spillover effects from developed areas to narrow inter-regional disparities and achieve balanced progress in digital inclusive finance. This tiered strategy ensures context-specific interventions while fostering nationwide synergy.

Data availability

Data are available upon request for it.

References

Acharya V, Xu Z (2017) Financial dependence and innovation: the case of public versus private firms. J Financ Econ 124(2):223–243

Appiah SO, Wiredu G, Adjei JK (2022) Fintech use, digital divide and financial inclusion. Digit Policy Regul Gov 24(5):435–448

Arner DW, Barberis J, Buckley RP (2017) FinTech, RegTech, and the reconceptualization of financial regulation. Northwest J Int Law Bus 37(3):371–413

Arner DW, Buckley RP, Zetzsche DA et al. (2020) Sustainability, FinTech and financial inclusion. Eur Bus Organ Law Rev 21(1):7–35

Beck T, Pamuk H, Ramrattan R et al. (2018) Payment instruments, finance and development. J Dev Econ 133:162–186

Cao S, Nie L, Sun H et al (2021) Digital finance, green technological innovation and energy-environmental performance: evidence from China’s regional economies. J Clean Prod 327:129458

Chen LJ, Yu JX, Xu Y(2021) The construction of common prosperity index model. Gov Stud 37(4):5–16

Cheng Y, Zhang D (2022) Analysis of the impact of social insurance on farmers in China: a study exploring subjective perceptions of well-being and the mechanisms of common prosperity. Front Psychol 13:1004581

Chroufa MA, Chtourou N (2023) Financial development threshold effect on wealth inequality-economic growth nexus: evidence from MENA economies. J Econ Asymmetries 28:e00324

Dong K, Wei S, Liu Y et al. (2023) How does energy poverty eradication promote common prosperity in China? The role of labor productivity. Energy Policy 181:113698

Fang X (2023) Can digital finance promote individuals’charitable giving? Empirical evidence from China. Comput Hum Behav 145:107768

Feng S, Chong Y, Li G et al. (2022b) Digital finance and innovation inequality: evidence from green technological innovation in China. Environ Sci Pollut Res 29(58):87884–87900

Feng S, Chong Y, Yu H et al. (2022a) Digital financial development and ecological footprint: evidence from green-biased technology innovation and environmental inclusion. J Clean Prod 380:135069

Gabor D, Brooks S (2017) The digital revolution in financial inclusion: international development in the fintech era. N. Political Econ 22(4):423–436

Ge H, Tang L, Zhou X et al (2022) Research on the effect of rural inclusive financial ecological environment on rural household income in China. Int J Environ Res Public Health 19(4):2486

Geng Z, He G (2021) Digital financial inclusion and sustainable employment: Evidence from countries along the belt and road. Borsa Istanb Rev 21(3):307–316

Han L, Peng Y, Meng Q (2023) Digital inclusive finance, entrepreneurial activity and common wealth—an empirical study based on inter-provincial panel data in China. Soft Sci 37(03):18–24

He Y, Li K, Wang Y (2022) Crossing the digital divide: the impact of the digital economy on elderly individuals’ consumption upgrade in China. Technol Soc 71:102141

Huang R, Kale S, Paramati SR et al. (2021) The nexus between financial inclusion and economic development: Comparison of old and new EU member countries. Econ Anal Policy 69:1–15

Ji X, Wang K, Xu H et al. (2021) Has digital financial inclusion narrowed the urban-rural income gap: the role of entrepreneurship in China. Sustainability 13(15):8292

Jiang Q, Li Y, Si H (2022) Digital economy development and the urban–rural income gap: intensifying or reducing. Land 11(11):1980

Jiang W, Hu Y, Cao H (2024) Does digital financial inclusion increase the household consumption? Evidence from China. J Knowl Econ 15:17333–17364

Jiao Y, Wang G, Li C et al. (2024) Digital inclusive finance, factor flow and industrial structure upgrading: evidence from the Yellow River Basin. Finance Res Lett 62:105141

Khera P, Ng S, Ogawa S et al. (2022) Measuring digital financial inclusion in emerging market and develo** economies: a new index. Asian Econ Policy Rev 17(2):213–230

Lee CC, Lou R, Wang F (2023) Digital financial inclusion and poverty alleviation: evidence from the sustainable development of China. Econ Anal Policy 77:418–434

Li C, Sha Z, Sun T (2023) Rural households’ internet use on common prosperity: evidence from the Chinese social survey. Soc Indic Res 170(3):797–823

Liu Y, Dong X, Dong K (2023) Pathway to prosperity? The impact of low-carbon energy transition on China’s common prosperity. Energy Econ 124:106819

Liu Y, Liu J, Zhou Y (2017) Spatio-temporal patterns of rural poverty in China and targeted poverty alleviation strategies. J Rural Stud 52:66–75

Mader P (2018) Contesting financial inclusion. Dev Change 49(2):461–483

Mao F, Wang Y, Zhu M (2023) Digital financial inclusion, traditional finance system and household entrepreneurship. Pacific-Basin Finance J 80:102076

Ololade YJ(2024) Conceptualizing fintech innovations and financial inclusion: comparative analysis of African and US initiatives. Financ Account Res J 6(4):546–555

Ozturk I, Ullah S (2022) Does digital financial inclusion matter for economic growth and environmental sustainability in OBRI economies? An empirical analysis. Resour Conserv Recycl 185:106489

Qiu Y, He N, Yan C et al (2023) Whether the digital divide widens the income gap between China’s regions? PLoS ONE 18(2):e0273334

Scheerder A, Van Deursen A, Van Dijk J (2017) Determinants of Internet skills, uses and outcomes. A systematic review of the second-and third-level digital divide. Telemat Inform 34(8):1607–1624

Sha Z, Ren D, Li C et al. (2024) Agricultural subsidies on common prosperity: Evidence from the Chinese social survey. Int Rev Econ Financ 91:1–18

Shen H, Luo T, Gao Z et al. (2023) Digital financial inclusion and the urban–rural income gap in China: empirical research based on the Theil index. Econ Res-Ekon Istraž 36(3):2156575

Sun F, Li J (2022) Research on the development mechanism of rural e-commerce based on rooted theory: a co-benefit-oriented perspective. Sustainability 14(20):13242

Sun Z, Cao C, He Z et al. (2023) Examining the coupling coordination relationship between digital inclusive finance and technological innovation from a spatial spillover perspective: evidence from China. Emerg Mark Financ Trade 59(4):1219–1231

Ugwuanyi U, Ugwuoke R, Onyeanu E et al. (2022) Financial inclusion-economic growth nexus: traditional finance versus digital finance in Sub-Saharan Africa. Cogent Econ Financ 10(1):2133356

Vassilakopoulou P, Hustad E (2023) Bridging digital divides: a literature review and research agenda for information systems research. Inf Syst Front 25(3):955–969

Wang D, Zhou T, Wang M (2021) Information and communication technology (ICT), digital divide and urbanization: evidence from Chinese cities. Technol Soc 64:101516

Wang J, Yin Z, Jiang J (2023) The effect of the digital divide on household consumption in China. Int Rev Financ Anal 87:102593

Wang Q, Liu C, Lan S (2022) Digital literacy and financial market participation of middle-aged and elderly adults in China. Econ Polit Stud 11(4):441-468

Wei K-K, Teo H-H, Chan HC et al. (2011) Conceptualizing and testing a social cognitive model of the digital divide. Inf Syst Res 22(1):170–187

Wu F, Cui F, Liu T (2023) The influence of digital inclusive finance on household wealth: a study based on CHFS data. Financ Res Lett 58:104460

Xu K (2024) Digital finance, social security expenditures, and rural-urban household income poverty. Evidence based on an area and household level analysis. Financ Res Lett 60:104845

Xu Y, Hu J, Wu L (2023) Efficiency evaluation of China’s provincial digital economy based on a DEA cross-efficiency model. Mathematics 11(13):3005

Xu Z, Zhang L, Liu Y(2020) Does the development of digital inclusive finance enhance regional innovation capability. Financ Econ 11:17–28

Yang J, Guo X, Zhang X (2024b) Analysis of the effect of digital financial inclusion in promoting inclusive growth: mechanism and statistical verification. Economics 18(1):20220078

Yang M, An Q, Zheng L (2024a) The spatial effect of digital economy enabling common prosperity—an empirical study of the Yellow River Basin. Systems 12(11):500

Yang Y, Zeng B (2025) Towards common prosperity: accelerated depreciation policy of fixed assets and labor income share. Int J Financ Stud 13(1):46

Yiyi S, Jialin S, Ying L et al. (2023) Economic poverty, common prosperity, and underdog entrepreneurship. J Bus Res 165:4–5

Zeng F, Sun H (2024) Spatial network analysis of coupling coordination between digital financial inclusion and common prosperity in the Yangtze River Delta Urban Agglomeration. Mathematics 12(9):1285

Zhang C, Zhu Y, Zhang L (2024) Effect of digital inclusive finance on common prosperity and the underlying mechanisms. Int Rev Financ Anal 91:102940

Zhang E, Yu F, Jiang T et al. (2023) Common prosperity level evaluation: a comprehensive method based on probabilistic linguistic ordered weighted distance measure, prospect theory, and TOPSIS. Front Psychol 14:1152333

Zhang J, Qian F (2023) Digital economy enables common prosperity: analysis of mediating and moderating effects based on green finance and environmental pollution. Front Energy Res 10:1080230

Zhao T, Jiao F (2024) Does digital financial inclusion promote common prosperity? The role of regional innovation. Electron Commer Res 24:1–26

Zhou Y, Liu Z, Wang H et al. (2023) Targeted poverty alleviation narrowed China’s urban-rural income gap: a theoretical and empirical analysis. Appl Geogr 157:103000

Acknowledgements

Henan Province Philosophy and Social Science Planning Annual Project (2022BZH010); Henan Province University Philosophy and Social Science Technology Innovation Talent Project (2024-CXRC-23); and Major Program of National Fund of Philosophy and Social Science of China (18VSJ036, 21ZDA115).

Author information

Authors and Affiliations

Contributions

Leiru Wei (first author) contributions in this paper are: conceptualization, formal analysis, funding acquisition, supervision, software, validation, writing—original draft, writing—review and editing. Jingxian Di (coauthor) contributions in this paper are: data curation, formal analysis, investigation, software, validation, writing—original draft. Qian Zhou (corresponding author) contributes to data curation, software, supervision, resources, funding acquisition, and writing—review and editing in this paper. All authors reviewed the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors. The work does not involve any hazards, such as the use of animal or human subjects. The information reported in the paper is accurate according to our best knowledge. The paper is entirely original work conducted by us without copying or plagiarism issues. The paper has not been and will not be submitted simultaneously to other journals. There is no financial or other substantive conflict of interest that might be construed to influence the results or interpretation of our manuscript. Declarations of interest: none.

Informed consent

The authors of the paper cited reported publications’ work and proper acknowledgment of the work of others has been given. All of the authors of the paper have participated in certain substantive aspects of this study, and they are acknowledged or listed as contributors. All of the authors of the paper have written and read the lasted edition. The authors have all agreed to publish the work in Humanities & Social Science Communications.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Wei, L., Di, J. & Zhou, Q. What is the role of digital divide between digital inclusive finance and common prosperity? Evidence from 245 cities in China. Humanit Soc Sci Commun 12, 1764 (2025). https://doi.org/10.1057/s41599-025-06053-7

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-06053-7