Abstract

Government policies in many countries are actively promoting the transition to a green economy, and the influence of shadow banking has become increasingly important in this context. The academic community has sought to determine how shadow banking responds to policy directives, what role it plays in supporting green innovation and whether this influence is positive or negative. This study theoretically examines the impact of shadow banking on corporate green innovation using Chinese A-share manufacturing companies listed on the Shanghai and Shenzhen stock exchanges from 2007 to 2022 as the research sample. We construct traditional instrumental variable (IV) and deep neural network IV models to empirically investigate and causally infer the impact of shadow banking development on corporate green innovation. We also apply the local instrumental variables (LIV) to rigorously test the validity of the IVs used and examine their independence. The robust conclusions are threefold. First, shadow banking development promotes green innovation in manufacturing enterprises, and financing constraints inhibit corporate green innovation. Second, shadow banking development has a heterogeneous impact on corporate green innovation across different provinces, ownership structures, listing types and industry characteristics. Third, shadow banking development promotes corporate green innovation by reducing financing constraints, enhancing innovation efficiency and increasing government subsidies. The findings suggest that amid the regulatory authorities taking measures to prevent potential financial risks, vigorously promoting shadow banking development holds profound policy significance for the green innovation of enterprises and promoting high-quality development.

Similar content being viewed by others

Introduction

Since the turn of the 21st century, the innovation cycle within enterprises has continuously shortened, making innovation an indisputably crucial competitive tool for firms striving to distinguish themselves in an increasingly competitive market (Schumpeter, 1934). China’s economy is transitioning from rapid growth to high-quality development, accompanied by significant changes in the economic and financial landscape. In July 2024, the Third Plenary Session of the 20th Central Committee of the Communist Party of China passed the Decision on Further Deepening Reform and Advancing Chinese-style Modernisation (hereafter referred to as the Decision). The Decision emphasised the need to accelerate the transition to a green economy, implement green fiscal and financial policies and establish standardised systems to support green development.

As interest rate liberalisation accelerates and nears completion, the rapid development of financial innovation and disintermediation has increasingly undermined the effectiveness of China’s traditional quantity-based monetary control mechanisms (Feyzioglu et al. 2009; Liao and Tapsoba, 2014). Consequently, an urgent need to shift towards price control measures that align with has emerged to support the transition to high-quality development. According to the China Shadow Banking Report issued by the China Banking and Insurance Regulatory Commission, by the end of 2019, the broad measure of shadow banking had decreased to 84.8 trillion yuan, representing a nearly 16 trillion yuan reduction from its historical peak. The narrow measure of shadow banking, which carries higher risk, had decreased to 39.14 trillion yuan, down by 12 trillion yuan from its historical peak. Since the implementation of a ‘deleveraging’ policy in 2017, stricter shadow banking regulation has led to a shift from rapid expansion to contraction in scale (Adrian and Ashcraft, 2012). Despite this contraction, shadow banking still has a significant position in China’s contemporary economy.

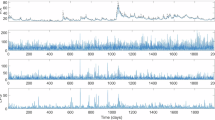

The Decision underscored the comprehensive advancement of financial reforms, with particular attention to shadow banking, calling for strengthened regulation and oversight of financial activities (particularly within the shadow banking sector) to mitigate systemic risks and enhance financial stability. As illustrated in Fig. 1, since January 2011, the Baidu search index for shadow banking has remained consistently high. Although corporate innovation has long been a focal point of attention, the focus on reaching the carbon peak by 2030 and carbon neutrality by 2060, which were clearly articulated goals from China in September 2020, has made dual carbon a popular topic in academic research. Concurrently, green innovation has emerged as an effective competitive strategy for enterprises (Gao et al. 2021).

The left axis represents the Baidu search index for shadow banking, corporate innovation and dual carbon, while the right axis represents the Baidu search index for financing, corporate innovation and dual carbon. Dual carbon refers to China’s carbon peak and neutrality goals.

With China’s continued economic development and increased demand for social credit, shadow banking has gradually become a significant participant in the financial system, while the influence of the traditional banking sector has been steadily declining (Chen et al. 2018). The global financial crisis shifted the academic focus towards financial regulation and the inherent shortcomings of the financial system. Issues such as the procyclicality of bank capital and regulation, regulatory arbitrage, systemic risk and macroprudential supervision have garnered considerable attention (Autor et al. 2020). As one of the root causes of the crisis, the micro-mechanisms and macro effects of shadow banking have become focal points for academic enquiry and concern for monetary authorities and regulatory bodies across various countries. Scholars generally agree that shadow banking’s excessive issuance of subprime loans, its high leverage in financing and a lack of regulation were significant contributors to the financial crisis.

The development of shadow banking in China has resulted in a transformative shift in the social financing structure, creating a trend that is capable of challenging the scale of commercial bank credit. The shadow banking system has diversified social investment and financing channels, reducing the gap in social financing demand, while also accelerating the pace of financial market innovation. Its market-oriented operational model has further promoted the process of interest rate liberalisation.

However, expanded shadow banking has also introduced a series of challenges. The growth of shadow banking activities disrupts the channel business of financial institutions, resulting in the phenomenon of capital circulating solely within the financial system, inflating financial asset prices and increasing risk (Ordonez, 2018). In contrast, as China’s financial system is predominantly driven by a bank-led indirect financing framework, monetary policy primarily influences the real economy through bank credit supply channels. With functions that are similar to those of commercial banks, shadow banking can provide financing services to the real economy, yet it operates outside the constraints of the primary regulatory indicators that govern traditional commercial banks, effectively escaping the regulatory framework. The liquidity created by the expansion of shadow banking has led to significant disintermediation in social financing behaviour, diminishing the role of bank credit channels in the transmission of monetary policy.

As global concerns over climate change and environmental protection intensify, driving green innovation is a critical pathway for enterprises’ sustainable development. Green innovation typically requires substantial initial investment and entails significant risk. The flexibility and innovativeness of shadow banking in providing capital may influence corporate decisions regarding green technology investments (Campiglio, 2016). While the funds provided by shadow banking often carry higher risk premiums, they may also supply the necessary financial support for green projects. However, the typically lower regulatory scrutiny of shadow banking could have complex implications for corporate green innovation.

Scholars have investigated the relationship between shadow banking development, financing constraints and corporate innovation extensively, resulting in a wealth of literature. However, some areas remain that could be further explored and refined. Previous research has not reached a consensus concerning the impact of shadow banking on corporate green innovation and has produced mixed evidence regarding the relationship between shadow banking and financing constraints. A review of the current literature reveals that only a few studies have examined the intersection of shadow banking development, financing constraints and green innovation, and the findings are not unanimous. Among these studies, some argue that the development of shadow banking has a positive influence on green innovation (Shahbaz et al. 2018; Herbohn et al. 2019; Kim et al. 2020). On the other hand, some believe that shadow banking may negatively impact green innovation (Cong et al. 2019; Abad et al. 2022; Zheng, 2023). This study addresses these gaps and controversies by integrating these variables and offering a new perspective for research across multiple interdisciplinary fields, enriching the previous research on shadow banking, financing constraints and corporate green innovation.

This study makes the following significant contributions:

This study is the first to explore the impact of shadow banking development on China’s manufacturing firms’ green innovation. While prior research has primarily focused on micro-level determinants of corporate green innovation (Tseng et al. 2018), few studies have examined this topic in the context of publicly listed Chinese manufacturing companies (Xie and Teo, 2022).

In addition, this study provides new causal evidence concerning the impact of shadow banking development on corporate green innovation. Existing literature on the consequences of shadow banking development (e.g., Chernenko and Sunderam, 2014; Grochulski and Zhang, 2019) lacks causal inference regarding its effects on corporate green innovation, this study addresses this gap by employing an instrumental variable (IV) model to empirically analyse and interpret the relationship. The study further ensures the validity of the IV using the method proposed by Kédagni and Mourifié (2020) and applies the deep neural network-instrumental variable (DNN-IV) method suggested by Hartford et al. (2017) for causal inference.

Finally, the results contribute to a more nuanced understanding of the impact of shadow banking in China. Conflicting views have persisted in the academic community regarding the expansion of shadow banking in China. One perspective has suggested that shadow banking expansion has promoted the development of credit markets (Chernenko and Sunderam, 2014), while another posits that it has amplified systemic financial risk. This study provides empirical evidence by examining the relationship between shadow banking development and corporate green innovation, offering new insights into the debate.

The subsequent sections of this paper are organised as follows: section “Literature review, theoretical analysis, and research hypotheses” offers theoretical analysis and research hypotheses; section “Research design” explores research design; section “Empirical results” presents the empirical findings; section “Additional mechanism analysis” presents additional mechanism analysis; and section “Conclusions and policy recommendations” summarises the study and provides policy recommendations.

Literature review, theoretical analysis, and research hypotheses

Literature review

The rise of shadow banking and the decline of traditional banking influence

With ongoing economic development and increasing demand for social credit, shadow banking has gradually become a significant participant in the financial system, while the influence of traditional banking has steadily declined (Adrian and Shin, 2010). The shadow banking system has facilitated the diversification of social investment and financing channels, effectively reducing the financing gap for corporate innovation while accelerating the pace of innovation in the manufacturing sector (Zheng et al. 2017). However, the expansion of shadow banking also introduces challenges, such as increased risks within the financial system due to capital circulating solely within it (Deng and Zhang, 2022).

Shadow banking development and corporate green innovation

As global concerns over climate change intensify, driving green innovation has become critical for sustainable development. Green innovation typically requires substantial initial investments and entails significant risks. Shadow banking can provide alternative financing options that traditional banks may not offer (Allen et al. 2005; Zhang, 2012). The flexibility of shadow banking in providing capital may influence corporate decisions regarding green technology investments (Campiglio, 2016). The interrelationship between shadow banking development and green innovation suggests that government policies and regulatory environments can simultaneously impact both (Elliott et al. 2015).

Research on related mechanisms

Shadow banking plays a role in alleviating financing constraints for firms, expanding their debt capacity, and stimulating innovative behaviour (Allen et al. 2005). The inherent uncertainties and risks associated with corporate R&D make it difficult for banks to lend, thereby necessitating external financing as a crucial source for innovation activities (Hottenrott and Peters, 2012; Ju et al. 2013). Numerous studies have confirmed that shadow banking development does promote green innovation financing among Chinese A-share listed companies. For example, Ehlers et al. (2018) point out that, under the Chinese economic context, the shadow banking system provides crucial funding support to firms unable to obtain traditional bank loans, especially for environmental technologies and projects. More recent empirical studies using data from 2007 to 2022 (Yang and Che, 2025) demonstrate that shadow banking development indeed enhances the green innovation resilience of Chinese listed companies.

Shadow banking innovation represents a form of financial innovation that can enhance liquidity in the financial market and promote corporate borrowing behaviour (Simsek, 2013). The expansion of shadow banking may widen financing channels and bolster corporate innovation capabilities. However, increasing market risk preferences during shadow banking expansion could also reflect heightened investments in emerging industries, including green technologies (Culp and Neves, 2017). This efficiency improvement is particularly crucial for green innovation, which often requires rapid responses to changes in environmental policies and market demand. Furthermore, shadow banking helps firms optimise the efficiency of capital utilisation (Laeven et al. 2015). More efficient financing options allow firms to allocate resources more rationally, directing more capital towards high-return green innovation projects. Effective resource allocation improves innovation efficiency and drives green technology progress. Additionally, as environmental regulations and policies become increasingly stringent, firms face growing pressure to innovate green technologies. By providing convenient financial support, shadow banking helps firms to quickly adapt to new policy requirements, enhancing the adaptability and efficiency of corporate innovation. By improving innovation efficiency, firms can implement green innovation strategies more effectively, align with policy directives and reap government incentives and market rewards.

Government subsidies are essential for driving R&D activities and enhancing firms’ innovation capabilities. As green finance policies advance, they may further promote the linkage between shadow banking and green innovation. Government innovation subsidies are intended to incentivise firms to conduct R&D activities in an orderly manner to improve innovation capabilities. Currently, government subsidies in China have a wide coverage, with increasing intensity and a growth trend in annual subsidy amounts. Representative studies on the effects of government subsidies on Chinese firms have indicated that these subsidies contribute to advancing corporate R&D activities (Zhang et al. 2012; Pan et al. 2022). Government subsidies effectively alleviate firms’ financial pressures, enabling increased investment in key R&D projects and expanding firms’ pool of talented R&D personnel, which enhances research capabilities and innovation performance. However, the systemic risks associated with shadow banking necessitate careful monitoring by regulatory authorities to mitigate potential adverse effects on innovation (Adrian and Jones, 2018).

Literature review

The literature indicates that shadow banking has become a crucial factor in facilitating corporate green innovation, particularly for publicly listed companies, by alleviating financing constraints. As the demand for social credit rises, shadow banking diversifies investment channels, effectively narrowing the financing gap crucial for innovation in the manufacturing sector (Adrian and Shin, 2010; Zheng et al. 2017). This flexibility enables listed companies to secure alternative funding sources for green technologies (Allen et al. 2005; Zhang, 2023).

Research shows that the development of shadow banking enhances the borrowing capacity of publicly listed firms, thereby stimulating innovative activities (Li et al. 2011). Moreover, shadow banking provides essential financial support for companies that struggle to obtain traditional bank loans, driving investments in environmental technologies (Ehlers et al. 2018). Empirical findings confirm that shadow banking positively affects the resilience of green innovation among Chinese A-share listed companies (Yang and Che, 2025).

Furthermore, shadow banking improves the efficiency of capital utilisation, allowing these firms to allocate resources more effectively towards high-return green innovation projects (Laeven and Levine, 2015). However, it is important to recognise that while shadow banking can enhance innovation efficiency, it also introduces risks associated with an over-reliance on short-term financial gains over long-term R&D initiatives (Rajan, 2003). Therefore, careful monitoring of shadow banking practices is essential to ensure that they contribute positively to sustainable innovation within publicly listed companies.

Theoretical analysis

Production Cost Theory

Production Cost Theory, articulated by Fandel (1991), posits that shadow banking plays a vital role in reducing operating costs and enhancing access to capital for firms. By providing alternative financial resources, shadow banking allows enterprises to bypass the stringent requirements imposed by traditional banks, especially during periods of capital scarcity. The supplemental financing from shadow banking enables these firms to allocate resources efficiently toward research and development (R&D) and green technologies, which often require significant upfront investment and entail prolonged payback periods.

Moreover, shadow banking facilitates a diversified funding structure, reducing reliance on traditional banking systems that may be risk-averse when assessing innovative projects. As highlighted by Yang and Che (2025), the infusion of additional financial resources through shadow banking not only lowers operational costs for firms but also promotes more aggressive investment strategies in R&D, thereby enhancing firms’ competitive edge in green innovation. This enables enterprises, including listed companies, to more effectively invest in R&D, technological innovation, and greener production processes.

Information Asymmetry Theory

Information Asymmetry Theory focuses on the disparities in knowledge between lenders and borrowers, which often lead to challenges in securing funding for innovative projects. According to Acharya et al. (2013), traditional banks operate under strict regulatory frameworks that require extensive due diligence and risk assessments. Consequently, they may be less willing to finance higher-risk ventures, such as green innovation projects, due to potential uncertainties surrounding their outcomes. This scenario creates barriers for firms seeking to pursue innovative technologies that could benefit from external funding.

Shadow banking, in contrast, offers more flexible financing options that can effectively address these information gaps. By permitting quicker and less cumbersome access to funds, shadow banking empowers firms to undertake innovative endeavours that would otherwise be deemed too risky by conventional lenders. This increased access to necessary capital encourages firms to invest in green technology initiatives, thereby enhancing their sustainability efforts and alignment with environmental policies (Ehlers et al. 2018).

Heterogeneous Firm Theory

Heterogeneous Firm Theory emphasises that firms do not possess uniform characteristics and thus respond differently to various financing sources. As noted by Yang and Che (2025), the impact of shadow banking on green innovation can vary significantly depending on a firm’s size, industry, and capital structure. Larger firms, particularly those engaged in capital-intensive segments, often have improved access to shadow banking resources, which allows them to capitalise on favourable financing conditions more readily than their smaller counterparts.

Furthermore, the theory suggests that individual firm attributes—such as operational scale and financing needs—play a crucial role in shaping the effectiveness of financing sources. This can lead to a scenario where larger, established firms may leverage shadow banking to enhance their innovation capabilities and expand their green technology investments, while smaller firms may struggle to access the same level of funding. Consequently, understanding the diversity among firms is essential for accurately assessing the overall impact of shadow banking on green innovation financing.

In summary, these theoretical foundations collectively illustrate the intricate relationship between shadow banking and corporate green innovation, supporting the notion that alternative financing can play a significant role in overcoming traditional financing constraints and promoting sustainability in various industries.

Research hypotheses

Foundational hypotheses

As shown in Fig. 2, the development of shadow banking in China exhibits a similar trend to the number of green innovation patents. This indicates that, on one hand, government policies and regulatory environments may simultaneously influence both shadow banking and green innovation (Elliott et al. 2015). On the other hand, the expansion of shadow banking signifies an increase in market risk appetite, which may also be reflected in investments in emerging industries, such as green technologies.

Data compiled by the authors. Source: CSMAR database, WIND database and the Statistical Database of the Survey and Statistics Department of the People’s Bank of China.

As the economy develops and the demand for social credit increases, shadow banking has become an important player in the financial system, while the influence of traditional banks has declined (Adrian and Shin, 2010). This diversification of financing channels reduces the gap in funding needed for corporate innovation and accelerates the pace of innovation in enterprises (Zheng et al. 2017). However, the challenges arising from shadow banking, such as the internal circulation of funds and increased financial risks, can negatively impact corporate innovation (Deng and Zhang, 2022). Based on this, we propose the following foundational Hypothesis 1.

Hypothesis 1. Shadow banking development promotes corporate green innovation.

The uncertainty and high risk associated with R&D investments make it difficult for banks to finance these activities (Ju et al. 2013; Hottenrott and Peters, 2012). With high loan interest rates, the cost of financing for enterprises rises, making it increasingly challenging to fund innovation efforts, consequently constraining the potential for green innovation (Yu et al. 2019; Gu and Zhang, 2020). As shown in Fig. 3, financing constraints in China and the number of green innovation patents exhibit an opposite trend, indicating that when companies face difficulties in financing, their ability to innovate in a green manner is often restricted. Accordingly, we propose the following foundational Hypothesis 2.

Data compiled by the authors. Source: CSMAR database, WIND database and the Statistical Database of the Survey and Statistics Department of the People’s Bank of China.

Hypothesis 2. Financing constraints inhibit corporate green innovation.

Research hypotheses

The evidence suggests that shadow banking alleviates financing constraints, enabling firms to pursue high-risk green projects with long return cycles that traditional banks might avoid due to their cautious lending practices (Ghosh et al. 2012). This ability allows enterprises to maintain momentum in their innovation activities despite the limitations of conventional financial channels. Based on this, we propose the following Hypothesis 3.

Hypothesis 3. Shadow banking development promotes corporate green innovation by reducing financing constraints.

Shadow banking improves the efficiency of resource allocation within firms, enabling a quicker response to environmental policy changes and market demands, which is critical for the success of green innovation (Allen and Gale, 2004; Laeven and Levine, 2015). By providing flexible financing options, shadow banking supports firms in implementing green innovation strategies effectively, aligning with policy directives while benefiting from government incentives. Therefore, we propose the following Hypothesis 4.

Hypothesis 4. Shadow banking development promotes corporate green innovation by enhancing innovation efficiency.

Governments can leverage shadow banking to increase subsidies for green innovation projects. As government subsidies rise, they effectively relieve financial pressure on firms, enhancing their capacity for research and development (Bai, 2011). Using shadow banking as a funding mechanism for subsidies allows governments to efficiently support green innovation efforts. Accordingly, we propose the following Hypothesis 5.

Hypothesis 1. Shadow banking development promotes corporate green innovation by increasing government subsidies.

Research design

Sample selection

This study focuses on A-share listed manufacturing enterprises on the Shanghai and Shenzhen stock exchanges, using data from 2007 to 2022. The sample is unbalanced panel data spanning 16 consecutive years, and as such, not all sample companies were operating throughout the entire period. Following established research methodologies, the initial sample data underwent the following processing. First, we excluded samples with missing data; second, we removed ST, *ST and PT companies to prevent abnormal circumstances of continuous loss from significantly impacting the empirical results; third, we excluded all non-manufacturing companies. To mitigate the influence of extreme values on the empirical results, all continuous variables were subjected to a 1% bilateral winsorisation. Based on these criteria, a total of 15,736 samples were obtained from 2007 to 2022. Financial data for listed companies are sourced from the China Stock Market & Accounting Research (CSMAR) and WIND databases, and shadow banking data are obtained from the Statistical Department of the People’s Bank of China.

Empirical model

Traditional instrumental variable model

▓.

where Gpatenti,t represents the number of green patents obtained by firm i in year t. shbanki,t−1 denotes the level of shadow banking development at the beginning of the period, and SAi,t−1 indicates the level of corporate financing constraint at the beginning of the period, which is measured using the SA index (Hadlock and Pierce, 2010). ln Tfpi,t−1 refers to the total factor productivity (TFP) at the beginning of the period, which is calculated using the Levinsohn–Petrin (LP) method (Levinsohn and Petrin, 2003). Xi,t−1 represents the control variables, including firm-specific characteristics. firmi and yeart represent firm and year fixed effects, respectively. εi,t is the error term. The regression employs robust standard errors clustered at the firm level. To ensure the results’ robustness, all explanatory and control variables are lagged by one period relative to corporate innovation.

Deep neural network-instrumental variable model

The DNN-IV approach combines the non-linear modelling capabilities of deep learning with the causal inference power of IV methods to effectively address endogeneity issues in complex datasets. As an emerging machine learning technique, DNNs have been increasingly applied to complement traditional econometric approaches for causal inference (Hartford et al. 2017; Qi et al. 2018). Although the integration of machine learning with traditional IV methods for causal identification is still relatively underexplored, the rapid growth in data volumes driven by technological advancements, the proliferation of the internet and the Internet of Things, digital transformation and the widespread use of mobile devices have significantly increased the availability of high-dimensional and high-frequency data (Hartford et al. 2017; Qi et al. 2018). This surge in data has exposed the limitations of traditional IV methods. Neural network models and traditional IV approaches each have strengths and weaknesses. Neural network models excel at navigating complex non-linear relationships and high-dimensional data, whereas traditional IV methods offer significant advantages in terms of theoretical simplicity, interpretability, data requirements, computational resource demands, robustness and broad applicability. Therefore, we reference the non-linear estimation approach proposed by Hartford et al. (2017), which involves using neural network models to estimate the first and second stages of the IV method. Specifically, the superior predictive capabilities of neural network models enhance the estimation accuracy of the IV method in both stages. Furthermore, the non-parametric nature of neural networks allows the DNN-IV algorithm to output heterogeneous individual treatment effects.

Specifically, the objective function estimated by the DNN-IV model is shown in Eq. (1). As noted by Hartford et al. (2017), Eq. (2) estimation can also be divided into two stages. The first stage involves estimating the conditional distribution function of the probability that an individual receives treatment. This is achieved by optimising the weights and thresholds in the neural network within the DNN model, yielding \(\hat{F}={F}_{\varphi }\left({p}_{i}\left|{x}_{t},{z}_{t}\right.\right)\), where φ represents the optimal parameter configuration obtained using the neural network model. After obtaining the first-stage estimation results, the estimated conditional probabilities of treatment can be directly substituted into Eq. (2) for further estimation, resulting in the following loss function:

The goal of model training is to minimise the loss function L, where D represents the sample size in the neural network training set. In the second stage, the neural network model uses the estimation results from the first stage-specifically, under the assumption of \(F\approx {\widehat{F}}_{\varphi }({p}_{i}|{x}_{t},{z}_{t})\)-to solve for h(p,x) and obtain the optimal second-stage neural network model parameters θ. After obtaining the second-stage estimation results, the trained neural network model is then used to estimate individual treatment effects by computing \({\widehat{h}}_{\theta }(1,{x}_{t})={\widehat{h}}_{\theta }(0,{x}_{t})\). This study employs the DNN-IV model proposed by Hartford et al. (2017) and conducts neural network training using the Keras library in Python.

Core indicator measurement

Dependent variable

Corporate green innovation

To quantify firms’ green innovation, we first obtained data on patent applications, patent grants and International Patent Classification (IPC) codes for manufacturing companies listed on the stock exchange using the China National Intellectual Property Administration (CNIPA) search portal. We then matched the IPC codes of the companies’ patents obtained from CNIPA with the green patent IPC codes listed in the International Patent Classification Green Inventory introduced by the World Intellectual Property Organization in 2010. This allowed us to calculate the annual number of green patents applied for and granted by each company. Referencing Qi et al. (2018), we categorise patents related to alternative energy production, waste management and energy conservation as specific types of green patents. We sum the total number of these three types of patents applied for by each company, adding 1 and taking the natural logarithm to construct the indicator for corporate green innovation (Gpatent), where a higher value indicates a greater green innovation level within the firm.

Key independent variables

Shadow Banking development

Following the approach used in existing literature (Allen et al. 2005; Simsek, 2013), this study defines shadow banking development as the ratio of the sum of increased entrusted loans, trust loans and undiscounted bankers’ acceptances to the total increase in social financing, which is specifically calculated as follows:

We also further categorise shadow banking development into three core components encompassing the ratio of the increase in entrusted loans to the total increase in social financing (wtdk), the ratio of the increase in trust loans to the total increase in social financing (xtdk) and the ratio of the increase in undiscounted bankers’ acceptances to the total increase in social financing (wtx). This allows us to separately examine the impact of these three key components of shadow banking on green innovation in China’s manufacturing firms.

Financing constraints

Commonly used measures include the KZ index (Lamont et al. 2001), the WW index (Whited and Wu, 2006) and the SA index (Hadlock and Pierce, 2010). A key limitation of these indices is that they incorporate financial variables that may be endogenous. To avoid endogeneity, Hadlock and Pierce (2010) developed a new SA index based on the KZ approach using only firm size and firm age—two variables that are relatively stable over time and strongly exogenous. The formula for calculating the SA index is as follows:

Since the SA index does not include endogenous financial variables, it is used in this study to measure firms’ financing constraints. A smaller SA index indicates greater financing constraints faced by the firm.

Total factor productivity

The TFP estimation is conducted using the method proposed by Berry et al. (2004), commonly referred to as the LP method. This method uses intermediate inputs as variable inputs affected by productivity shocks. The TFP measured using the LP method can be expressed as follows:

We use industrial value added as a proxy for firm output, which is deflated using the producer price index specific to each industry. Referencing Brandt et al. (2012), capital input is calculated using the perpetual inventory method to estimate capital stock, enabling a more detailed and accurate estimation of TFP.

Instrumental variables

Two potential factors may affect the reliability of our regression results. First, a bidirectional causal relationship could exist between shadow banking development and corporate green innovation. Firms’ increased green innovation activities may result in significant economic growth, which could subsequently accelerate shadow banking development, and the rapid growth of shadow banking might increase firms’ financing constraints, further enhancing green innovation efforts. Furthermore, rapid shadow banking development could initially increase corporate green innovation activities, which may then stimulate further shadow banking sector growth. In either scenario, the assumption of the independence between the explanatory variables and the error term is violated, resulting in biased estimates of the causal effect.

To ensure the reliability of the results, this study employs the IV approach to eliminate endogeneity. The IVs for shadow banking development should only be correlated with the likelihood of shadow banking but should not directly influence firms’ innovation behaviour, and these variables should vary over time. As a result, many firm-specific characteristics are unsuitable as IVs. Therefore, this study adopts the following indicators as IVs for shadow banking development.

Economic policy uncertainty index (EPU): Although the use of the EPU as an IV for shadow banking development has not been extensively explored in the literature, some related studies provide support and insights for this application. These studies have primarily examined how EPU affects financial markets and practices, including activities within the shadow banking sector. EPU can cause instability in financial markets, potentially influencing the development of non-traditional financial sectors like shadow banking (Baker et al. 2016). In contrast, corporate green innovation activities are less sensitive to EPU fluctuations, which is likely attributable to the long-term and strategic nature of green innovation investments (Hojnik and Ruzzier, 2016). Firms undertaking such investments tend to focus on long-term strategic goals rather than short-term policy changes. Moreover, many countries, including China, have consistently implemented policies and regulations that support green development. These stable policy frameworks provide reliable backing for corporate green innovation, mitigating the impact of EPU fluctuations.

Local government fiscal pressure: Local governments facing fiscal pressure (e.g., high local debt or budget deficits) may become more reliant on the shadow banking system to secure funding. However, this fiscal pressure is less directly related to corporate green innovation activities (Faccio et al. 2009), making it an exogenous shock that can serve as a suitable IV for corporate green innovation practices.

Satellite nighttime light index: This study constructs an IV using satellite nighttime light intensity data, using the annual average nighttime light intensity data from the study regions between 2007 and 2022. We adjust and aggregate the data referencing standard techniques used in previous research for regression analysis (Henderson et al. 2012). Urban expansion, which affects government investment in public infrastructure such as transportation, influences nighttime light intensity. However, urban expansion does not directly impact firms’ operational practices and thus has no direct effect on corporate green innovation activities.

Control variables

To include as many control variables as possible (Harvey et al. 2004), this study introduces the following: firm size (Size), firm age (Age), government subsidies (Subsidy), leverage ratio (Lev), return on assets (ROA), return on equity (ROE), asset turnover ratio (ATO), cash flow ratio (Cashflow), accounts receivable ratio (REC), inventory ratio (INV), fixed asset ratio (Fixed), revenue growth rate (Growth), shareholding ratio of the top 10 shareholders (Top10) and Tobin’s Q (TobinQ).

Table 1 presents the definitions of the study’s variables.

Descriptive statistics

Table 2 presents the descriptive statistics for the main variables after excluding outliers beyond the 1st and 99th percentiles. To ensure data consistency, the number of green patents, TFP, firm size, firm age and board size are all expressed as the natural logarithm of the variable plus one.

The sample data reveal that the average number of green patents for listed manufacturing firms is 0.720 with a standard deviation of 0.032. This suggests that green patent acquisition is relatively low among listed manufacturing firms in China. Additionally, the small variation in green patent numbers indicates that R&D investments are considerably homogeneous across these firms. This observation aligns with the generally limited innovation efforts of listed manufacturing firms in China (Yuan et al. 2023). The average value of the core explanatory variable of shadow banking development is 0.019, with a standard deviation of 0.120. This indicates that shadow banking constituted a notable proportion of the social financing scale during the sample period, with considerable variability in scale. The median value is 0.129, indicating that at least half of the companies in the sample have engaged in shadow banking development greater than or equal to 0.129. The average financing constraint is −3.887 with a standard deviation of 0.247, reflecting that listed manufacturing firms in China generally face significant financing constraints, with considerable variability between firms. This finding is consistent with the prevalent financing difficulties faced by Chinese manufacturing enterprises (Acharya et al. 2013). The average TFP value is 9.088, with a standard deviation of 1.008, indicating that production efficiency is generally low among listed manufacturing firms in China, with considerable differences across firms.

The means and medians of firm size, firm age, government subsidies and leverage control variables are closely aligned, suggesting that these variables are approximately normally distributed.

Empirical results

To explore the impact of shadow banking development on corporate green innovation and validate the primary hypothesis of this study, we use a sample of listed manufacturing firms on the Shanghai and Shenzhen A-shares markets, conducting an empirical analysis using 16 years of annual unbalanced panel data from 2007 to 2022. This study examines the effects of shadow banking development on corporate green innovation using traditional and DNN-IV models. To rigorously test the validity of our IVs, we apply the KM2020 method to test the independence of the instruments and conduct a series of robustness checks (Kédagni and Mourifié, 2020). Finally, we conduct heterogeneity tests based on manufacturing firms’ ownership attributes, market characteristics and industry-specific features.

Traditional IV regression

The first-stage regression results are presented in Table 3, indicate that EPU can lead to instability in financial markets, which may impact shadow banking development and other non-traditional financial sectors. Specifically, EPU is positively correlated with shadow banking development, and higher EPU is associated with faster growth in shadow banking. Additionally, higher government debt, which suggests that government expenditure exceeds revenue, is associated with more rapid shadow banking development. The F-test confirms that the IVs are correlated with the endogenous variables, and the DWH test indicates that the endogenous variables exhibit minimal serial correlation. The Sargan test results yield values >1 with p-values above 0.12, indicating that the null hypothesis of instrument validity cannot be rejected. All models pass the Sargan test, allowing us to proceed with two-stage least-squares (2SLS) regression.

The 2SLS regression results are presented in Table 4. We include firm and time fixed effects to mitigate the impact of firm characteristics and temporal variations on the primary causal relationship. The 2SLS results align closely with the direction of the ordinary least squares (OLS) results, although OLS underestimates the positive effect of shadow banking development on corporate green innovation.

Specifically, the regression results in columns (1)–(6) in Table 4 show that the lagged shadow banking development and its components—entrusted loan, trust loan and non-discounted bank acceptance bill ratios—are positively associated with corporate green innovation at the 1% significance level. This confirms that faster shadow banking development is associated with higher corporate green innovation levels, consistent with the findings of Giannetti et al. (2015) and Xu et al. (2022), who all concluded that shadow banking promotes corporate green innovation. Therefore, our baseline Hypothesis 1 is supported, indicating that shadow banking development does indeed promote manufacturing firms’ green innovation. Models (4)–(6) in Table 3 reveal that entrusted loans have the most significant positive effect on corporate green innovation compared with trust loans and non-discounted bank acceptance bills. This is likely because firms that easily access entrusted loans are often large state-owned enterprises (SOE) with strong government connections and substantial national funding, making it easier for them to acquire various innovation resources and overcome financing constraints.

The regression results for empirical columns (1)–(6) in Table 4 consistently demonstrate that the coefficient for financing constraints is significantly positive, confirming a significant negative correlation between financing constraints and corporate green innovation, wherein as financing constraints decrease (SA index increases), equity financing declines and innovation levels fall. This supports our baseline Hypothesis 1, indicating that financing constraints have a suppressive effect on corporate green innovation.

Regarding TFP, the regression results for empirical columns (1)–(6) indicate that the coefficients for TFP are significantly positive at the 1% level, suggesting that improved TFP contributes to increased corporate green innovation.

For the remaining control variables, empirical columns (4)–(6) show that the coefficients for lagged firm size and firm age are significantly positive. This indicates that increases in firm size and maturity lead to significant innovation improvement, consistent with the notion that expanding production scale has scale effects and positively impacts performance and innovation. This aligns with Schumpeter’s theory that larger firms experience weaker competitive effects and stronger innovation. The coefficient for lagged government subsidies is significantly positive, suggesting a notable contribution of Chinese government subsidies to listed manufacturing firms’ innovation. Conversely, the coefficient for lagged leverage is significantly negative, indicating that higher debt ratios are associated with decreased innovation.

Furthermore, comparisons across empirical columns (1)–(6) reveal minimal overall differences in the impact of shadow banking development on corporate green innovation across various indicators. The firm and year fixed effects in all models demonstrate the robustness of the regression results used in this study.

Furthermore, this paper introduces the squared term of shadow banking development in the basic regression section. The results in column (3) of Table 4 show a significantly positive effect, indicating that the regression results for the squared term of lagged shadow banking development do not satisfy the hypothesis of a nonlinear relationship between shadow banking development and corporate green innovation. Therefore, there is no nonlinear effect of shadow banking development on corporate green innovation. Although the introduction mentions that shadow banking may bring systemic risks and could suppress green innovation, in China, due to relatively strict financial regulation, these risks may have been effectively mitigated. In this context, the development of shadow banking does not have a negative impact on green innovation.

The possible reason is that, on one hand, the Chinese government has implemented stringent financial regulations to maintain the stability and security of the financial market. This regulation helps reduce the systemic risks associated with shadow banking activities, thereby providing a more stable financing environment for new enterprises and green innovation (Adrian and Shin, 2010). Effective regulation can ensure the transparency of shadow banking operations, limit non-compliant financing behaviour, and promote better investment decisions.

On the other hand, the Chinese government has adopted a series of policies to financially support green innovation, including the issuance of green bonds. These policies aim to guide funds towards environmentally friendly projects, thus promoting the research and application of green technologies by enterprises (Elliott et al. 2015; Zheng et al. 2017). Green bonds provide enterprises with dedicated financing channels for green projects, alleviating their financial pressure and allowing them to concentrate resources on green innovation.

Therefore, this paper builds on empirical column (1) by introducing interaction terms for financial regulatory intensity and shadow banking development, as well as for shadow banking development and green bonds, to validate the hypotheses of this study (results can be found in Appendix Table 1). The empirical results indicate that the interaction term of financial regulatory intensity and shadow banking development, as well as the interaction term of shadow banking development and green bonds, both have significantly positive regression coefficients on corporate green innovation, which confirms the hypothesis that the series of financial policies implemented by the Chinese government not only enhance the positive effect of shadow banking development on green innovation but also suppress its negative effects.

Instrumental variable validity test

To rigorously assess the validity of the IVs used in this study, we employ the method proposed by Kédagni and Mourifié (2020) (hereafter KM2020) and assess the independence of the instruments.

The KM2020 method is notable for providing precise, testable implications regarding IV independence and exclusion restrictions. The theoretical derivations suggest that IV independence and exclusion restrictions are equivalent to the generalised instrument inequality constraint, which relies on a set of conditions involving the joint distribution of the observed variables (outcome, treatment and instruments). Therefore, testing for IV validity violations essentially involves checking whether the generalised instrument inequality holds. When the inequality holds, the independence of the instruments is maintained.

In accordance with KM2020, we conduct various binarisations of the outcome variable (corporate green innovation). First, we create a binary variable based on whether Y is ≤0. Second, we binarise Y based on different quantiles {20%, 40%, 50%, 60%, 80%, 99%}. Finally, we perform tests with and without control variables. According to KM2020, under the hypothesis of IV independence, the upper bound should be ≤0. If the lower bound of the confidence interval for the upper bound is ≤0, we cannot reject the hypothesis of IV validity Table 5 reports the lower bounds of the confidence intervals for the upper bounds of the generalised instrument inequality. The results are negative across all cases, indicating that the IV independence assumption cannot be rejected and is satisfied.

Robustness checks and addressing endogeneity issues

Robustness checks

To mitigate the impact of potential measurement errors, this study follows the methodological framework established by Yang and Che (2025), integrating private lending, entrusted loans, and entrusted wealth management as the three core components of shadow banking development for a comprehensive assessment. The empirical results are presented in Table 6.

The regression results from columns (1)–(4) consistently indicate that the regression coefficient of lagged shadow banking development (lag_shbank) is significantly positive. This finding confirms that a faster development of shadow banking correlates with a higher level of corporate green innovation. These results are largely consistent with the regression outcomes presented in Table 2SLS, further underscoring the robustness of the empirical findings in this study.

Addressing endogeneity issues

Heckman two-stage model

In the study of corporate green innovation, there may be issues of sample selection bias. On one hand, not all firms engage in green innovation; thus, analysing only those with green patent applications might lead to sample selection bias, affecting the estimation of the impact of shadow banking development on green innovation. The Heckman two-stage model is designed to correct for endogeneity and selection bias that arise from missing observations or the absence of green innovation behaviour in a specific group of firms, ensuring the validity and robustness of the conclusions drawn (Heckman, 1979). The first stage of the Heckman two-stage model is a selection model that examines the influencing factors behind publicly listed companies’ decisions to engage in green innovation.

The dependent variable Gpatent_dummyi,t is a binary dummy variable that takes the value of 1 if firm i chooses to engage in green innovation in period t, and 0 otherwise. Control variables include financing constraints (SA), total factor productivity (lnTfp), firm size (lnSize), and firm age (lnAge), among others. σi,t represents the error term.

The second stage comprises the green innovation model, which examines the factors influencing corporate green innovation:

In this context, Gpatenti,t represents the level of corporate green innovation as previously measured, and Millsi,t denotes the inverse Mills ratio estimated from Eq. (7), which controls for sample self-selection issues. The inverse Mills ratio incorporates the unobserved information from Eq. (7) and is included in Eq. (8) to correct for the existing sample selection bias. Additionally, to mitigate potential endogeneity concerns within the model, we follow the methodology of Wang and Yuan (2019) by lagging all explanatory variables in Eqs. (7) and (8) by one period, while also incorporating firm and year fixed effects to account for the potential impacts of fluctuations in these factors.

To illustrate that this study effectively overcomes the sample self-selection problem and justifies the adoption of the Heckman two-stage model, we concurrently employ traditional ordinary least squares (OLS) and two-stage least squares (2SLS) estimation methods as a benchmark. Columns (1) and (2) of Table 7 present the regression results for OLS and 2SLS, respectively. It is evident that the coefficients and significance levels of the variables in the OLS and 2SLS regressions, which do not account for sample self-selection, differ notably from those in column (4). Furthermore, the statistically significant inverse Mills ratio in the Heckman two-stage model indicates the presence of self-selection bias, thereby validating the choice of the Heckman two-stage model.

Selection of different instrumental variables

In the foundational regression analysis, this study utilised the Economic Policy Uncertainty Index, local government fiscal pressure, and nighttime light intensity as instrumental variables for shadow banking development to mitigate potential reverse causality issues. To further address endogeneity concerns, we referenced the research logic of Fang et al. (2022), Kugler et al. (2020), Goldsmith-Pinkham et al. (2020), and Lewbel (1997) to construct additional instrumental variables: the industry average of shadow banking development (IV1), the industry average of shadow banking development excluding the focal industry (IV2), the share-moving method (IV3), and the higher-order moment instrumental variable method (IV4).

According to the first-stage regression results in column (1) of Table 8, regression coefficients for all instrumental variables are significantly positive at the 1% significance level, meeting the fundamental requirement for instrument relevance. Additionally, the Wald F-statistic values exceed the critical threshold for weak instruments (16.630) at the 10% significance level, indicating the absence of weak instrument problems and further confirming the validity of the instrumental variables. The second-stage regression results in columns (2)–(5) reveal that the coefficients representing the impact of shadow banking development on corporate green innovation are significantly positive, consistent with our baseline regression findings. This analysis shows that our research conclusions remain robust even after employing multiple instrumental variables to mitigate the endogeneity arising from potential reverse causation.

DNN-IV regression

Table 9 presents the second-stage empirical results using the DNN-IV method. Following the traditional 2SLS estimation and the validity checks for IVs, we apply the DNN-IV approach for further empirical analysis. The standard errors for the treatment effect estimates are obtained through bootstrap sampling.

The analysis reveals that shadow banking development has a significant positive impact on the total number of green patents, green invention patents and green utility model patents, and is associated with a significant 1.01 increase in the log-transformed number of green patents, which represents 140% of the sample mean. This result aligns with the earlier OLS and 2SLS estimates in direction, but is slightly lower than the 2SLS estimate and notably higher than the OLS estimate. This suggests that OLS estimates may substantially understate the positive effect of shadow banking development on corporate green innovation, whereas the 2SLS estimate, which is constrained by linear model assumptions, may overestimate this effect.

Figure 4 compares the predictive performance of the 2SLS and DNN-IV models. The results indicate that the DNN-IV model significantly outperforms the 2SLS model in terms of predictive accuracy and provides higher reliability in model specification. Compared with the 2SLS estimates, the DNN-IV model yields more balanced results with greater credibility. Additionally, due to the characteristics of the DNN-IV model, which non-linearises the original regression equation, the model’s fit more closely approximates the true underlying relationship.

Data compiled by the authors. Source: CSMAR database, WIND database and the Statistical Database of the Survey and Statistics Department of the People’s Bank of China.

Heterogeneity analysis

To further investigate the heterogeneous effects of shadow banking development on green innovation among Chinese manufacturing firms, we conduct a series of sub-group analyses, grouping firms based on the provinces in which they are located, ownership structure (state-owned vs. non-state-owned), the type of stock market (main board–listed vs. non-main board–listed) and industry characteristics. For industry classification, we reference Jiang et al. (2007) and categorise manufacturing industries into labour-, capital- and technology-intensive sectors based on the 2017 National Economic Industry Classification and Codes. We then conduct empirical tests on these sub-samples using the DNN-IV method.

Provincial heterogeneity analysis

Due to differences in policy implementation, firm characteristics and socio-economic factors across provinces, the impact of shadow banking development on corporate green innovation varies significantly by region. As illustrated in Fig. 5, shadow banking has had a more substantial influence on promoting green innovation in western provinces such as Ningxia and Qinghai. The primary reasons for this may include the scarcity of traditional financial resources in these western provinces, which makes it difficult for firms to secure sufficient funding through conventional financial channels. As a result, shadow banking serves as an alternative financing source, providing the necessary capital to support green innovation initiatives. Furthermore, western regions often benefit from favourable national policies such as the Western Development Strategy (Zhang et al., 2023), which may encourage the growth of shadow banking and indirectly promote corporate green innovation.

Data compiled by the authors. Source: CSMAR database, WIND database and the Statistical Database of the Survey and Statistics Department of the People’s Bank of China.

In summary, the regression coefficients for shadow banking development exhibit both positive and negative signs across different provinces, reflecting the complexity of its impact on green innovation. This also highlights the differences in policy implementation, economic development and data quality across cities. A detailed analysis of the specific conditions in each province can help better comprehend these differences and inform targeted policy improvements to enhance corporate green innovation and achieve high-quality economic development.

Ownership structure heterogeneity analysis

To investigate the differences in the impact of shadow banking development between state-owned and non-state-owned manufacturing enterprises, we introduce a dummy variable to indicate whether a firm is state-owned. State-owned enterprises are coded as 1, and non-state-owned enterprises as 0. Table 10 presents the empirical results.

The empirical results from column (3) show that the coefficient of the interaction term is 0.0597, but it is not statistically significant; therefore, we conclude that there is no substantial difference in the effect of shadow banking development on green innovation between state-owned and non-state-owned enterprises. Several reasons might explain this finding. First, shadow banking financing is widely applicable and has not demonstrated a significant bias towards state-owned or non-state-owned firms, and its flexible financing methods can meet the needs of various types of enterprises. Both state-owned and non-state-owned enterprises can access financing through shadow banking, particularly when traditional bank loans fall short of meeting their needs (Chen et al. 2011). Second, the widespread demand for green innovation driven by policy is another factor. Regardless of ownership structure, China’s policy environment strongly encourages firms to pursue green innovation. State-owned enterprises, under greater policy pressure, are compelled to fulfil more social responsibilities and actively engage in green innovation. Conversely, non-state-owned enterprises are also motivated to pursue green innovation due to market competition and policy incentives (Zhou et al. 2012). Moreover, the Chinese government promotes green innovation through direct intervention in state-owned enterprises and incentivising non-state-owned enterprises through policies and tax benefits. Therefore, in the context of green innovation, the role of shadow banking may similarly promote both types of enterprises.

Heterogeneity analysis based on listing type

We next investigate the differences in the impact of shadow banking development between A-share manufacturing enterprises listed on the main board and those listed on non-main boards, introducing a dummy variable indicating whether a firm is listed on the main board. Main board–listed A-share manufacturing enterprises are coded as 1, while non-main board–listed A-share manufacturing enterprises are coded as 0. The empirical results of this analysis are presented in Table 11.

Column (3) reveals that the coefficient of the interaction term is 0.0574, which is significant at the 10% level. This finding suggests that shadow banking development has a greater positive effect on green innovation in main board-listed manufacturing enterprises compared with non-main board-listed manufacturing enterprises. Several factors may explain this result. First, the main board-listed companies are generally larger in scale, and their green innovation projects often require substantial funding. As a result, these companies are more likely to leverage shadow banking as an additional financing channel to meet their significant capital needs, subsequently driving green innovation. Second, main board-listed companies typically have superior financing capabilities and higher credit ratings, which makes it easier to obtain financing from shadow banks. Shadow banks may prefer to lend to these companies due to lower risk and stronger repayment capacity. Additionally, main board-listed companies often have closer relationships with financial institutions, enabling them to more easily access shadow banking resources and use these funds to support green innovation. Moreover, main board-listed companies often hold dominant positions in market competition (Zhou et al. 2012). To maintain this leadership, such firms must continuously engage in green innovation. Financing from shadow banks helps these companies maintain a competitive edge in technological and product innovation.

Industry characteristics heterogeneity test

To examine the differences in the impact of shadow banking development across different sub-industries, we classify enterprises based on industry characteristics. Referencing Jiang et al. (2007) and using the 2017 National Economic Industry Classification and Codes, we divide 30 specific manufacturing industries into labour-, capital- and technology-intensive categories, presenting the empirical results in Table 12.

Labour-intensive manufacturing enterprises benefit the most from shadow banking development, followed by technology- and capital-intensive manufacturing enterprises; however, the differences are insignificant. This suggests that the financing provided by shadow banking is typically highly flexible and not restricted by the traditional banking system. Enterprises of all types—whether labour-, technology- or capital-intensive—can leverage shadow banking to obtain relatively flexible and expedient financial support. This flexibility likely mitigates the differentiated financing effects among different types of enterprises.

Specifically, although technology-intensive enterprises generally have stronger innovation capabilities, the associated financing needs and methods may be more diversified. As a result, the influence of shadow banking on these enterprises may be comparable to its influence on other types of enterprises. Although less technologically advanced, labour-intensive enterprises still have substantial capital requirements, and such firms can pursue necessary innovation activities with the backing of shadow banking. For capital-intensive enterprises that are more reliant on substantial capital investments, the funds provided by shadow banking may support capital needs but could seem relatively insufficient compared with overall financial demands.

Additional mechanism analysis

Building on the mechanism analysis presented in this study, we next investigate the indirect effects of shadow banking development on corporate green innovation by introducing the channel variables of financing constraints, innovation efficiency and government subsidies. This analysis employs the causal mediating analysis model to examine how shadow banking influences corporate green innovation through these channel variables, which is effective for identifying the causal mechanisms through which an independent variable affects a dependent variable via a mediator (Imai et al. 2011). The strength of this model is its ability to provide causal inference among continuous or discrete treatment variables, mediating variables and outcome variables. The model calculates the average mediating effect of compliance through the channel variables of financing constraints, innovation efficiency and government subsidies on corporate green innovation and the direct effect of shadow banking development on corporate green innovation.

To do so, we divide the examination of channel effects into two steps. In the first step, we analyse the impact of various factors on financing constraints, innovation efficiency and government subsidies channel variables by treating them as dependent variables. This step is used to explore the channel effects of shadow banking development on corporate green innovation. The second step treats corporate green innovation as the dependent variable, incorporating the treatment variable (shadow banking development), the channel variables and other independent variables into the model. The introduction of channel variables is modelled using a DNN-IV framework as follows:

where Gpatenti,t represents the number of green patents obtained by firm i in year t. pre_shbanki,t−1 indicates the initial shadow banking development level, which is obtained using neural network training in Python’s Keras library. SAi,t−1 denotes the initial level of corporate financing constraints, which is measured using the SA index. Channeli,t−1 refers to the initial channel variables, including financing constraints, innovation efficiency and government subsidies. firmi represents firm fixed effects and yeart denotes year fixed effects. σi,t and μi,t represent the random error terms in the first and second stages, respectively.

Financing constraint channel

Based on the theoretical analysis above, this study uses the SA index as a proxy variable for financing constraints. The regression results are presented in Table 13. In columns (1) and (2), the impact of shadow banking development and financing constraints on corporate green innovation is consistent in direction. The differences in the channel effect and the channel effect rate are only due to the varying number of variables included. The channel effect rate is 23.03%, indicating that financing constraints indeed have a mediating role in promoting the relationship between shadow banking development and corporate green innovation. This finding confirms Hypothesis 3, which posits that shadow banking development further promotes corporate green innovation by reducing financing constraints.

In column (2), the first-stage results show that more expedient shadow banking development results in lower financing constraints for enterprises. Since the causal mediating model is used for the empirical analysis, the positive effects of shadow banking development are not attributable to selection bias but are genuinely derived from factors strengthened by shadow banking growth. The second-stage results confirm that both shadow banking development and financing constraints significantly promote corporate green innovation. In practice, this reflects how shadow banking development indirectly secures financial innovation loans and counterpart funding through a signalling effect. The positive effects of shadow banking development can further enhance corporate green innovation by lowering financing constraints.

Innovation efficiency channel

Based on the above theoretical analysis, this study uses the quantity of patents obtained per unit of R&D expenditure as a comprehensive measure of green innovation efficiency, referencing Tong et al. (2014). Table 14 presents the regression results. Columns (1) and (2) reveal that the direction of the effects of shadow banking development and innovation efficiency on firms’ green innovation is consistent, with differences in channel effects and channel effect rates attributed to the number of variables included. The channel effect rate is 9.19%, indicating that innovation efficiency indeed has a mediating role in the relationship between shadow banking development and firm green innovation. This supports Hypothesis 4, which posits that shadow banking development further promotes firm green innovation by enhancing innovation efficiency.

In column (2), the first-step results show that faster shadow banking development is associated with lower innovation efficiency. Since a causal mediating model is used in the empirical analysis, the positive effect of shadow banking development is not attributable to selection bias but genuinely stems from factors within the development of shadow banking. The second-step results confirm that shadow banking development and innovation efficiency significantly promote firms’ green innovation. In practice, shadow banking may be more inclined than traditional banks to support high-innovation and high-potential green projects due to its risk diversification and return incentive mechanisms. Green innovation typically requires substantial initial investment and longer payback periods, and shadow banking can provide more targeted financial products to stimulate such innovations (Laeven et al. 2015), subsequently enhancing overall innovation efficiency. The positive effects of enhanced shadow banking development further improve green innovation by increasing innovation efficiency.

Government subsidy channel

The shadow banking system provides flexible financing tools that can help governments raise funds more efficiently, thereby increasing subsidies for firms’ green innovations. Based on this conjecture, the regression results for government subsidies as a channel variable in the impact of shadow banking development on firm green innovation are presented in Table 15. In columns (1) and (2), the direction of the effects of shadow banking development and government subsidies on firm green innovation is consistent, with variations in channel effects and channel effect rates attributed to the number of variables included. The channel effect rate is 50.47%, indicating that government subsidies indeed have a mediating role between shadow banking development and firm green innovation. This confirms Hypothesis 5, which states that shadow banking development promotes firm green innovation by increasing government subsidies.

In column (2), the first-step results show that faster shadow banking development is associated with lower government subsidies for firms. Since a causal mediating model is used in the empirical analysis, the positive effects of shadow banking development are not attributable to selection bias but genuinely result from factors within the development of shadow banking. The second-step results confirm that shadow banking development and government subsidies significantly promote firms’ green innovation. In practice, the shadow banking system enables governments to rapidly access more financial resources, which can be used to support green innovation projects. For example, the government can raise funds through financial instruments issued by shadow banking entities (such as special funds or trust products managed by shadow banks) (Hsu et al., 2014) and use these funds to subsidise green innovation firms, reducing financial pressures and accelerating the development and application of green technologies. Furthermore, through shadow banking, the government can design leveraged subsidy tools such as combining limited government subsidy funds with private capital through shadow banking trust products or asset management plans, thereby supporting firms’ green innovation on a larger scale.

Conclusions and policy recommendations

Research conclusions

As global attention to climate change and environmental protection intensifies, promoting green innovation is a crucial pathway for advancing enterprises’ sustainable development. Green innovation typically requires significant initial investments and a willingness to bear considerable risks. Although shadow banking provides funding that often comes with high-risk premiums, it can also offer necessary financial support for green projects. However, due to its typically less regulated nature, the impact of shadow banking on corporate green innovation can be complex.

This study empirically investigates the impact of shadow banking development on corporate green innovation and draws causal inferences using traditional IV and DNN‑IV models. To rigorously test the validity of the instruments, we employ the KM2020 method to examine their independence.

Our results show that shadow banking development promotes manufacturing enterprises’ green innovation, while financing constraints inhibit innovation.

We also find that the impact of shadow banking development on corporate green innovation varies across provinces. The promotional effect of shadow banking on green innovation does not differ significantly between state‑owned and non‑state‑owned enterprises; however, shadow banking development has a more substantial positive effect on green innovation among main board–listed manufacturing firms. Labour‑intensive manufacturing firms benefit the most from this promotional effect, followed by technology‑ and capital‑intensive firms, although these differences are not statistically significant.

Finally, shadow banking development further promotes corporate green innovation by reducing financing constraints, enhancing innovation efficiency, and increasing government subsidies.

Policy implications

The conclusions drawn from this study can serve as a reference for the government to develop, revise, and refine financial policies to foster a healthy financial system, optimise the business environment, and promote high-quality economic development. These findings can help the government, society, and the public to better understand the potential contributions of shadow banking to corporate green innovation. Regulatory authorities should implement timely measures to prevent potential financial risks while maintaining financial system stability and promoting financial market prosperity.

Shadow banking development is a key topic in the study of government–enterprise relations. Based on the findings of this study, the policy implications can be analysed from both government and corporate perspectives. First, efforts should be made to vigorously develop direct financing and establish a more inclusive modern financial system. Shadow banking funds primarily originate from household savings and investments driven by the pursuit of higher returns. Therefore, support for the newly established Beijing Stock Exchange, which focuses on financing innovative SMEs and caters mainly to qualified investors who typically prioritise value investment and long-term holdings, should be strengthened. Additionally, local governments should increase the establishment of government-guided funds for technological innovation (parent funds) to promote the development of venture capital and private equity funds.