Abstract

Since 2021, interest in non-fungible tokens (NFTs) and associated trading volume have increased substantially, as celebrities increasingly adopted profile picture non-fungible tokens (PFP NFTs) for their social media profile images. In this study, the factors influencing consumer decisions on purchasing a PFP NFT were analyzed by Conjoint analysis. The characteristics of profile picture and NFT were researched through previous studies, and key attributes and levels that affect purchasing of a PFP NFT were set through market research. The results of the study showed that consumers made decisions based on the number of promoting celebrities as the most important attribute when they buy a PFP NFT, followed by number of community members, floor price, and commercial use of NFT intellectual property. This research has value in that it suggests a forward-looking perspective regarding development of the NFT market, which is in its early stages.

Similar content being viewed by others

Introduction

As a new medium for enabling transactions of all kinds of digital assets and the proof of ownership thereof, interest in non-fungible tokens (NFTs) and the volume of transactions have been increasing (Valeonti et al., 2021). According to Statista (2024), NFT market revenue was expected to reach USD 2.378 billion in 2024, and revenue was expected to total USD 3.369 billion by 2028, showing an annual growth rate of 9.10% (CAGR 2024–2028). However, more recent data (Statista, 2025) indicate a sharp adjustment, with global NFT revenue projected at USD 504.3 million in 2025 and a negative annual growth rate of –5.0% (CAGR 2025–2026), representing an almost 80% decline in market size and a 14-percentage-point drop in growth expectations. This decline can be interpreted not as a mere market contraction but as a phase of structural maturation, during which the market has undergone a process of self-correction following the overheated growth of previous years. Following the speculative hype of 2021–2022, the NFT market has undergone a natural elimination of unsustainable projects, becoming more selective and utility-driven in the process. Recently, technological advancements such as scalable Layer-2 solutions and enhanced interoperability, along with growing efforts toward regulatory integration, have further contributed to rebuilding trust and structural maturity. As a result, the current market reflects a more sober and practical phase, focusing on real value creation and gradual mainstream adoption. The importance of the virtual world is expected to continue to grow (Khadijah et al., 2023; Jo et al., 2024), and therefore, the size of the NFT market is expected to grow for the time being. In the total NFT market, Collectible-type NFTs recorded the largest trade volume, and many celebrities led the trend of NFTs by changing their social network service (SNS) profile pictures to Collectible NFTs.

CryptoPunks, created by Larva Labs, was the first successful Collectible NFT and has maintained the highest average price in NFT markets for an extended period. However, the floor price of CryptoPunks decreased to 52.69 Ethereum (hereafter, ETH) in December 2021, lower than the 53.9 ETH floor price of the Bored Ape Yacht Club (BAYC) from Yuga Labs (Khatri, 2021). What differences between CryptoPunks and BAYC resulted in reversal of the floor prices of their tokens? As CryptoPunks has dominated the market in terms of trade volume, it has historical value. Despite this value, the NFT license and user agreement prevented the holders of CryptoPunks from using their NFTs for commercial purposes. On the other hand, BAYC was community-centered and focused on providing holders with various utilities and benefits. Moreover, the trend of celebrities using BAYC as their SNS profile pictures attracted public interest in BAYC, and use of NFTs by Adidas Originals led to continuous increase of the average NFT price of BAYC. For additional benefits, the holders could earn profits through creation of secondary works using their BAYC NFTs based on commercial rights to associated intellectual property. Through these differences, the floor price of BAYC, which is a relatively new project compared to CryptoPunks, surpassed that of CryptoPunks. In March 2022, BAYC issuer Yuga Labs acquired brands, art copyrights, and IPs for the NFT collections of both CryptoPunks and Meebits by Larva Labs.

The case of CryptoPunks and BAYC had a huge impact on the NFT industry. However, issues associated with NFTs have yet to be studied, including factors that increase the floor price of NFTs, user expectations, and developments. Even though NFTs have a tremendous potential impact on current digital asset markets and future business opportunities, only a few studies have researched judicial affairs, finance, and engineering of NFT (Aysan et al., 2024;) or the association of NFT prices with cryptocurrency prices (Ante, 2021). Therefore, the present study aims to determine whether the utilities (uses and benefits) offered by a Collectible NFT (hereafter, PFP NFTs) that is used as a PFP for consumers influence purchase intention. This study will suggest insights into the desired utilities for various future PFP NFT projects based on preferred attributes for purchase of PFP NFTs and consumer perceptions of incurred financial value from these attributes.

First, this research investigates the characteristics of general NFTs and the utility provided by PFP NFTs. Based on the investigation, the levels of important attributes of floor price, number of community members, number of celebrities, additional NFT project airdrops, NFT intellectual property (IP) usage rights, and benefits for NFT holders are set. Second, user data are collected using Conjoint Analysis and analyzed using the mixed logit method. Finally, based on the analyzed results, the study will present future directions regarding the utility and consumption value to be provided by future PFP NFTs.

This study is composed of the following sections. In Section 2, characteristics of PFP NFTs are summarized to understand an NFT used as a profile picture, and representative PFP NFT statuses are investigated. Section 3 selects important attributes and levels of utilities provided by PFP NFTs based on the previous investigation, and the section describes the questionnaire design for analysis. In Section 4, the mixed logit model among discrete choice models is presented. Section 5 presents empirical results. Finally, in Section 6, the results and implications are discussed and conclusions are drawn.

Research background and literature review

An NFT, referring to a non-fungible blockchain token, is a new concept derived from the cryptocurrency (Ante, 2021). Unlike Bitcoin and Ethereum, NFTs cannot be replaced since they have unique values for each token. Thus, NFTs serve as a unique certificate to claim ownership of an asset even if the type of asset is digital (Ante, 2021; Jafar et al., 2023). An NFT is closely related to the structure and technology of the blockchain. The biggest technical feature of the blockchain is that it processes and manages data through decentralization without a centralized server (Yli-Huumo et al., 2016). This means that transparency and reliability of transactions can be secured, and stable system operation can be achieved without an independent supervisory authority by sharing data on a distributed network (Wang et al., 2021b). In addition, information authenticity verification is possible, and it is impossible to change or delete recorded data arbitrarily, since information is stored in a blockchain network through a distributed network (Christidis and Devetsikiotis, 2016).

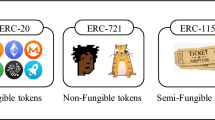

The NFT was first introduced at the Ethereum Developers Conference in London, England, starting as an Etheria project which can be trading virtual land using the Ethereum blockchain, and most of the NFTs currently in circulation are based on Ethereum (Wood, 2014). General tokens comply with the ERC-20 standard, but an NFT complies with ERC-721. Unlike ERC-20, which is a framework of alternative tokens, ERC-721 receives a variable in-code token ID and establishes separate ownership of the token (Wang et al., 2021b). The above technical characteristics of an NFT enable the proof of the original ownership by clearly specifying ownership as information, such as ownership and sales history of digital assets stored in the blockchain. In addition, it is impossible to falsify data, such as owner information or sales history, which compensates for the otherwise easy indiscriminate reproduction of digital assets. Due to these characteristics, an NFT is evaluated to be an indispensable core technology in the metaverse and creator economy, and NFTs have attracted a great deal of attention recently (Kati, 2021).

As the market for NFTs grows, the types of NFT are also diversifying. Among many types of NFT, the PFP NFT, which is used as a Profile picture, can be an example of the most representative type of NFT. A PFP NFT is a digital work that people use to express themselves online and is the most actively traded NFT in the current market. Although a single authoritative definition of a PFP NFT has not yet been established, the term PFP NFT is described as follows according to Steiner (2022).

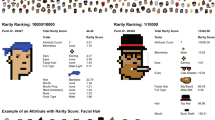

The PFP NFT consists of approximately 10,000 similar images based on a common template. Also, the images are mostly anthropomorphic, and each image has diversities with a random combination of certain elements, such as eyes, nose, mouth, and accessories. The uniqueness of each NFT depends on a given characteristic (e.g., background, eyes, mouth, hat, glasses, accessories, etc.). This PFP NFT is a form of Generative art and is digital art that is randomly generated based on an algorithm. Generative art creates various forms and generates millions of options through computers and algorithms (Kalpokiene and Kalpokas, 2023). In this way, Generative art is a combination of different characteristics under the same conditions, and each work has uniqueness and scarcity. Through Generative art-based NFTs, people can show their sense of belonging to a community, and they can express their identities by purchasing an NFT of an avatar that resembles themselves.

Therefore, the characteristics of PFP NFT that are mentioned above can be seen in a similar context as a profile picture used on social media. According to Berger and Calabrese (1974), the formation and management of impressions play important roles in social interaction, and people currently tend to make good impressions through self-expression online rather than offline (Utz, 2010). As use of the Internet and SNS platforms is constantly increasing and gives people a new identity online, there is no doubt that online profile pictures are one of the most important elements for self-expression (Ellison et al., 2006). Previous studies have shown that people who pursue social status can generally prove their financial strength through ostentatious consumption and unproductive use of time (Veblen, 1899). This is a phenomenon that appears not only offline, but also online, in which people present profile pictures to show travels to luxurious destinations or ownership of products related to specific classes (Faucher, 2014). Although the digital world seems to be full of various goods and information due to the ease of replication of digital information, there is a desire for competition to secure scarce resources because the economy of obtaining meaningful social capital (likes, status improvements, etc.) is linked to a scarcity economy (Faucher, 2014). Therefore, it can be inferred that an NFT is used as a tool to acquire social capital, along with the above examples, by being utilized as a PFP.

Properties affecting the purchase of a PFP NFT

Research on the attributes of value in consumer purchasing of NFT is not sufficient, this study established attributes and levels of NFTs by referring to previous studies on consumption value and by identifying the characteristics of NFTs in current market circulation. Specifically, for attribute selection, this study first drew upon the Theory of Consumption Values (TCV) by Sheth et al. (1991). Sheth et al. (1991) explained that consumers’ motivations for selecting a particular product or service stem from five distinct types of values: Social, Functional, Conditional, Emotional, and Epistemic Value. According to their framework, Social Value refers to the perceived utility arising from one’s association with specific social groups, while Functional Value captures the perceived utility derived from the practical, utilitarian, or physical performance of an alternative—including attributes such as price, quality, and durability. Conditional Value reflects the utility obtained under particular circumstances or situational conditions faced by the decision-maker, whereas Emotional Value pertains to the utility generated by an alternative’s capacity to evoke specific emotions or affective states. Epistemic Value, in turn, represents the perceived utility gained from satisfying a desire for knowledge (Sheth et al., 1991).

This study focuses on Social Value and Functional Value among the five value dimensions proposed by Sheth et al. (1991), as this study assumes that these two values constitute the primary consumption motives driving the purchase of PFP NFTs. This approach is informed by the assessment that the essential characteristics of PFP NFTs lie in their dual nature as markers of digital identity and as digital assets. First, PFP NFTs are expected to be primarily driven by Social Value, as they serve not merely as profile images but as tools for visually expressing one’s identity and constructing digital identity through community participation, a sense of belonging, and endorsement from prominent figures. Moreover, Functional Value is also expected to play a significant role, given that PFP NFTs function as digital assets that provide practical utility—such as opportunities for business activities through commercial IP rights, exclusive access to specific services or events, and investment value.

A noteworthy refinement comes from the subsequent research by Sweeney and Soutar (2001). They noted that the broad concept of ‘Functional Value’ defined by Sheth et al. (1991) contains both ‘quality’ and ‘price (economic)’ elements, prompting them to measure these as two distinct dimensions: ‘functional value (performance/quality)’ and ‘functional value (price/value for money)’. As PFP NFTs are not merely consumption goods but also possess the strong characteristics of an ‘investment asset’ reflecting expectations of future value, this study adopted this distinction, separating the concept into ‘Economic Value’ and ‘Functional Value’. As the next step, based on this three-value framework (Economic, Functional, and Social), we surveyed the key features and utilities competitively promoted in the PFP NFT market to identify corresponding attributes. This process led to the selection of six key attributes: ‘floor price’ (reflecting Economic Value); ‘number of community members’ and ‘number of celebrities’ (reflecting Social Value); and ‘NFT IP license’, ‘additional NFT project airdrop’, and ‘benefits for NFT holders’ (reflecting Functional Value). A detailed discussion of each follow.

Floor price

The floor price of an NFT refers to the lowest price that consumers can pay to purchase an NFT in a collection. In other words, the NFT floor price is the lowest price to become a member of a particular NFT project or to own an NFT. This does not mean that the floor price is the bid price because the floor price is the lowest price and not the average price of an NFT in a collection.

The NFT floor price is important in that it is possible to assess the demand for the NFT project and the degree of trust of holders through its fluctuations. Decrease of the floor price of an NFT indicates that the seller has lost faith in the project and indicates the NFT holder’s willingness to sell at a lower price. In addition, a decrease in floor price may raise doubts for potential new buyers who are thinking about whether to buy the NFT from that collection. In contrast, an increase in NFT floor price suggests that a typical project holder believes that the project will be highly valued in the future and has no intention of selling the NFT at the existing floor price. This support of NFT projects contributes to increase the rarity of the corresponding NFT and results in an increase in floor price.

According to Griffiths et al. (2024) and Vega and Camarero (2024), expectations of NFT’s future value has a positive effect on NFT purchase intention, and in this context, the floor price in an NFT market is expected to act as an attribute that influences NFT purchase decisions. This research assumed that the floor price was maintained or increased based on minting price, set at 500,000 KRW, which is the average minting price of the investigated PFP NFTs. At the time of this study, there were no notable declines in the floor price of NFTs. Future work will analyze consumer sentiments given a subsequent decline in NFT floor prices. Based on the minting price, the floor price was set at 500,000 KRW, 1 million KRW, or 2 million KRW, representing situations of price maintenance, doubling, or quadrupling, respectively.

Number of community members

The online community refers to a group of people who interact with one another online and develop a sense of belonging and attachment to each other (Blanchard et al., 2004). In general, when there is network externality, people tend to prefer products or services that are used by more 2023 people (Abu-Shanab et al., 2024). Previous studies related to online communities highlight the tendency of people to engage in online communities for social interaction (Iriberri and Leroy, 2009). This is because people can obtain various benefits, such as information exchange and social bonds, as members of an online community (Iriberri and Leroy, 2009). In addition, consumers become more loyal in the online community when they recognize the value of communication with other consumers about the products they have or want to purchase (Hagel and Armstrong, 1997). Furthermore, social identity tends to have a significant influence on the purchasing behavior of online community members based on previous studies related to community user behavior (Pentina et al., 2008). Therefore, online community participation has a key influence on related brand participation, and online community members may have a stronger brand commitment than general consumers (Kim et al., 2008).

According to Choi et al. (2022), herding behavior also appears in the cryptocurrency market, and even in the case of NFT, social value has a great influence on the price of NFT (Hofstetter et al., 2024; Vega and Camarero, 2024), and therefore in this context, the number of members of the PFP NFT community is expected to influence the intention to purchase NFT. Therefore, this study sets the number of NFT community members as a variable that influences the NFT purchase decision. The attribute level was classified into 10,000, 25,000, and 50,000 in consideration of the number of community members of major PFP NFTs.

Number of celebrities with NFTs

According to Hashemi Joo et al. (2020), its price tends to rise when a cryptocurrency is advertised, and therefore, endorsements from celebrities for products or services are advertising strategies for companies to increase the purchase intention of potential customers by building brand awareness (Ki et al., 2023). People tend to prefer the products or brands used by celebrities because they strongly identify with the celebrities (Hong, 2023). Therefore, many companies use celebrities for advertisements because they expect customers to purchase celebrity-related products (Fowles, 1996).

Such marketing with celebrities also occurs in NFT space. Many celebrities are directly involved in NFT purchases, and companies that mint NFTs promote NFT projects through celebrities (Gilbert, 2022). Also, NFT holders including celebrities use NFTs as their profile pictures on social media. Due to the transparency provided by the blockchain, it is easier for consumers to identify and recognize celebrity-associated NFT purchases (Thomas, 2022). This transparency would affect the intention to purchase NFT and stimulate consumers’ copycat sentiments.

In this context, participation of celebrities in the NFT market is expected to affect the intention to purchase an NFT. Therefore, in this study, the number of celebrities involved in NFTs was set as an attribute that influences a decision to purchase an NFT. The level of this attribute was classified into 0, 5, or 10 considering celebrity participation on major PFP NFTs.

NFT IP license

Before the advent of NFTs, it was difficult to claim ownership and intellectual property (IP) of digital creations in a digital environment. NFT technology allowed creators to claim IP by granting ownership of digital creations. However, while the ownership of the token of the NFT was transferred to the holders who purchased the NFT, the right to use the associated IP for generating profits of the digital asset is typically not transferred. Thus, the IP utilization rights of NFTs purchased in the current NFT market can be largely divided into two categories: Personal use and Commercial use. Personal use means that NFT issuers grant NFT holders a free license to use, copy, and display purchased NFTs, but do not authorize their individual commercial use. Additionally, some NFT projects allow limited commercial use for NFT holders but limit the income they can earn through secondary creation. Because this limits NFT holder’s IP right use, from this perspective, this research intends to treat the following cases as personal use.

Commercial use grants NFT holders a license to generate secondary works and earn profits without restriction. Therefore, unlike Personal use, Commercial use is similar to media content that is produced and distributed over the Internet by non-experts online. This is similar to the existing concept of User-Generated Content (UGC) in that users directly participate in the production process to create content. According to previous studies, UGC producers participate to establish their identity and make a profit (Jin and Feenberg, 2015). However, the culture of participation of the users who satisfy values such as autonomy, pleasure, and self-identity through content production led to is criticized for its lack of economic reward despite the labor provided by producers (Terranova, 2012). This UGC environment without such economic rewards may reduce people’s participation in the platform (Ingawale et al., 2013). From this perspective, the participation of users is expected to have an important impact on revitalizing the market as modern social media users play leading roles in the online media environment. Therefore, it is expected that NFTs will encourage user participation through secondary creations and would affect the activation of early NFT markets, linking to NFT purchase decisions.

In this context, the right to use IP in the NFT market is expected to act as an attribute that influences decisions regarding purchasing NFTs. Therefore, this study set two levels based on permission of the NFT holders for only Personal use or both Personal use and Commercial use for their NFTs.

Additional NFT project airdrop

In the blockchain industry, an airdrop refers to the free distribution of NFTs or rights related to a blockchain project to its user and owner community who meet specific criteria (Fröwis and Böhme, 2019). Users who receive an airdrop gain additional assets or benefits without any exchange of funds or reciprocal action (Allen et al., 2023). Airdrops are generally used to add value or to draw attention to a brand or experience. For example, Yuga Labs, the creator of BAYC, launched Apecoin in 2022 and airdropped it to BAYC NFT holders. A unique feature of Apecoin was that anyone holding a BAYC NFT could claim APE (Allen et al., 2023). This meant that anyone who purchased a BAYC NFT could immediately claim the APE airdrop and own both the NFT and APE (Barda et al., 2022). Furthermore, this enabled ‘flash loans’ (Wang et al., 2021a), allowing one to resell the purchased BAYC NFT and the airdropped APE to pocket the profit (APE sale proceeds) without using their own capital.

Then why do projects employ such unusual and costly token or additional value distribution strategies? Allen et al. (2023) explain that the reason for spending hundreds of millions of dollars is to attract new users and retain existing communities, while also building community and enhancing security by decentralizing project ownership and control. A common method for bootstrapping a user base is the use of airdrops, which distribute tokens, especially to a project’s early adopters (Messias et al., 2023). In this context, an additional NFT project airdrop is expected to influence the intention to purchase NFT. In this study, two levels were set based on performance of an additional NFT project airdrop to holders.

Benefits for NFT holders

Based on the situation in which NFT issuers are steadily striving to increase the value of NFTs, the demand and price of the NFT project increase when the majority of holders retain NFTs. In other words, incentives for holders to retain NFTs are desired for issuers. Unlike CryptoPunks, BAYC offered holders various benefits online to offline and economic benefits. Finally, economic benefits included an ApeCoin airdrop based on ERC-20.

This distribution of tokens can create a system of Tokenomics, in which rules are designed in a way that stakeholder behavior is consistent with the goals pursued by the issuer (Freni et al., 2020). For the economic part, the token empowers organizations to manage their own business models and allows users to interact with products. However, the price of NFTs and the typical user faith in a project would decrease if there was no actual utility (governance) of the token or if the utility was not attractive. In other words, Tokenomics is an incentive system that induces holders to retain NFTs without selling them.

In this context, the benefits provided to NFT holders are expected to influence the intention to purchase an NFT. This study divides the levels of benefit for NFT holders into three levels: online benefits only, online + offline benefits, and online + economic benefits.

Thus, the final attributes used in this study are floor price, number of community (discord) members, number of celebrities with NFT, additional NFT project airdrops, NFT IP licenses, and benefits for NFT holders.

Methodology

This study uses conjoint analysis to collect user preference data, and the discrete choice model is employed for analysis. Consumer preferences across various combinations of product or service attributes could be systematically assessed by conjoint analysis (Green and Srinivasan, 1978). For the analysis model, this study uses a discrete choice model based on random utility theory to estimate consumer utility. The multinomial logit model (MNL) is popular for its simplicity and closed-form solution. However, the MNL has a restrictive independence of irrelevant alternatives (IIA) assumption (Train, 2009). Due to the IIA constraint, the MNL model results could be inconsistent with reality. In addition, a simple MNL model cannot fully reflect consumer heterogeneity.

The mixed logit model can better explain reality by assuming a distribution in the consumer preference coefficient. Thus, the mixed logit model captures consumer heterogeneity and relaxes the IIA assumption, thereby providing a better fit to real market conditions (Train, 2009). This model is also widely used for new product prediction and analysis (Train and Sonnier, 2005). Therefore, we employ the mixed logit model among the discrete choice models. The utility function of the mixed logit model is shown in Eq. (1).

\({U}_{{njt}}\) is the utility that consumer \(n\) obtains when they choose alternative \(j\) in the choice set \(t\). This utility consists of the observable utility \({V}_{{njt}}\) and the unobservable portion \({\varepsilon }_{{njt}}\). \({V}_{{njt}}\) can be represented as \({\beta ^{\prime} }_{n}{X}_{{jt}}\), where \({\beta ^{\prime} }_{n}\) is an individual coefficient, and \({X}_{{jt}}\) is the attribute level of alternative j. \({\beta }_{n}^{{\prime} }\) is an attribute coefficient with mean b and variance-covariance matrix ∑, and the IIA constraint can be relaxed.

In the mixed logit model, the most commonly used distributions for the coefficients are normal and log-normal distributions. In this study, the coefficients of all attributes are assumed to follow a normal distribution. Therefore, in a mixed logit model with this utility function, the choice probability that consumer \(n\) will select an alternative \(j\) in the choice set \(t\) is multiplied by the coefficient distribution of the attribute and the choice probabilities of the simple logit model, as shown in Eq. (2).

In this study, estimation of parameters is intractable using the classical maximum likelihood estimation method because the choice probability is not in a closed form. Therefore, alternative methods should be used for estimation. In this study, we use the hierarchical Bayesian (HB) method for estimation (Allenby and Rossi, 1998; Train, 2001).

To derive comparable economic and management meanings of parameters, marginal willingness to pay (MWTP) and relative importance (RI) are calculated through the estimation results of \(\beta\). The MWTP indicates how much a respondent is willing to pay for a unit change in the level of an attribute. The value can be calculated by dividing the parameter estimate of each attribute by that of each parameter estimate (see Eq. (3)). \({\beta }_{a}\) and \({x}_{a}\) indicate the mean estimated parameters and attribute values of the attributes excluding the price attribute. \({\beta }_{{price}}\) and \({x}_{{price}}\) are the estimated parameter and the attribute level for the price attribute, respectively.

The RI is expressed as the sum of partial values for each attribute of a product and indicates the degree to which each attribute influences consumer choice. Here, \({part}-{{worth}}_{x}\) is calculated by multiplying the difference between the minimum and maximum levels of the attribute by a parameter. Equation (4) is as follows.

Results

Demographic distribution of the participants

The survey was commissioned and conducted by a reputable online research company in South Korea to ensure high data quality and representativeness. Data was collected from a total of 156 respondents, of whom 89 (57%) were male and 67 (43%) were female. The majority (89%) were in their 20 s and 30 s. 90% of respondents had experience purchasing cryptocurrency, and 77% had experience purchasing NFTs. Table 1 shows the sample statistics.

Analysis of the mixed logit model

The empirical model of this study is shown in the following equation.

where \({X}_{{price}}\) equals the Floor Price. \({X}_{{N\_community}}\) and \({X}_{{N\_celebrities}}\) represent the numbers of community members and of celebrities holding NFTs, respectively. \({D}_{{commercial}}\) is the dummy variable defined as 1 for a case in which the NFT IP license allows Commercial use and is defined as 0 for the case allowing only Personal use. \({D}_{{airdrop}}\) is the dummy variable that defined 1 as an NFT project with one or more Airdrops and defined as 0 for NFT projects without any airdrop. For holder benefits, ‘offering spaces for online holders only’ is the reference. \({D}_{{benefit}2}\) is 1 for ‘offering spaces for online holders only + offline benefits’ and 0 for not. \({D}_{{benefit}3}\) is 1 for ‘offering spaces for online holders only + economic benefits’ and 0 for not.

As shown in Table 2, price and N_celebrities were significant at the 1% significance level, while N_community and commercial were significant at the 10% significance level. All attribute variances were significant at the 1% level. Consumers tended to show greater preference for NFT projects with larger numbers of community members and of celebrities. Moreover, they showed a preference for allowing NFT IP to be used commercially. On the other hand, the preference was not significant for NFT airdrop and holder benefits with online holders only, offline benefits, and economic benefits.

To derive the value of money for attributes, MWTP analysis was conducted. Consumers were willing to pay an additional 416 thousand KRW when the number of community members increased by 10,000 and to pay an additional 553 thousand KRW when the number of celebrities who have an NFT increases by one. Consumers were willing to pay an additional 1043 thousand KRW for NFT IP Commercial use.

Relative importance analysis found that consumers rate the number of celebrities who own NFTs as the most important attribute, followed by number of community members, price, and commercial use availability.

Discussion and implications

Discussion

This study showed that NFT purchase intention increased as the floor price, which refers to the lowest price to be paid to own one NFT, decreased. However, a low floor price and a decrease in floor price have very different meanings. A decrease in floor price means that public interest and valuation of the NFT collection have declined. On the other hand, the value of a collection cannot be determined only with the information of a low current floor price. As we provided only three levels of floor price, respondents lacked information to evaluate the NFT collection. When it is difficult to apply the rules for maximizing utility with the option with the greatest possible value for the cost invested, respondents followed the lowest cost method and purchased the NFT with the lowest cost.

Second, as the number of celebrities increased, the NFT purchase intention significantly increased, with respondents willing to pay an additional 553 thousand KRW (about 374.83 USD as of December 19, 2025) for an NFT when the number of celebrities increased by one. In addition, by setting the sum of the relative importance of the seven individual attributes to 100, the relative importance of the number of celebrities who purchased NFTs was highest at 35.7.

The finding that celebrity affects consumer perception of products or purchase behavior has been verified through several previous studies (e.g., Lord et al., 2019). According to Atkin and Block (1983), in a complex media environment, celebrities capture the attention of audiences for advertising messages. Therefore, although there are various advertising methods that can draw audience attention to products and services, the use of celebrities easily evokes stopping power (Gnanapragash and Sekar, 2013). Also, Sabnavis (2003) mentioned that celebrity appearances in advertisements are a way to solve the ‘absence of ideas’ problem. This means that a celebrity purchase and endorsement of a product serves as a substitute for arguments why the product is valuable and necessary.

This study showed that the greater was the number of celebrities, the higher was the MWTP NFTs, which is also explained by the concept of mimicry, in which people want to purchase products owned by celebrities. According to Ki and Kim (2019), when people buy a product, it is important who else owns it. A typical example of mimicry consumption, which is purchasing a product based on the purchasing behavior of others, is buying clothes or accessories worn by celebrities or sports stars (Rahman, 2022).

The larger was the number of community members owning the NFT, the higher was the NFT purchase intention. Respondents MWTP increased by 416 thousand KRW for the NFT when the number of community members increased by 10,000. In addition, the relative importance of the number of community members was 15.6, the second most important factor among the seven attributes. A large number of community members not only enables a larger scale of social interaction, but also means that the public interest and value evaluation of the NFT project are high. Thus, as the number of community members increased, the NFT purchase intention increased as well.

In addition, a large number of community members indicates the possibility of NFT price maintenance or increase. The NFT community is a space where people who have already purchased NFTs and those who intend to purchase NFTs in the future gather together. Therefore, a large number of community members can be interpreted as (1) many people want to purchase a limited number of NFTs and (2) those who have already purchased a limited number of NFTs are continuing community activities without any intention to sell them to others. In other words, as the number of community members increases, people tend to expect the supply of NFTs to be low and the demand to be high. This suggests that the NFT price will be maintained or increased when the user intention to purchase the NFT increases.

When commercial use rights of NFT IP were allowed, consumers’ intention to purchase NFTs increased compared to NFTs that prohibited commercial use. Specifically, consumers were willing to pay 1043 thousand KRW more than the original NFT purchase cost if they could be granted the right to commercial use of IP.

In December 2021, BAYC outperformed the floor price of Larva Labs, the developer of CryptoPunks, the first PFP; BAYC acquired CryptoPunks and Meebits in March 2022. One of the reasons why BAYC, a latecomer, was able to outperform CryptoPunks is that Yuga Labs gave buyers the right to use NFT IP commercially. BAYC NFT holders earn profits in various ways, such as printing their brands on T-shirts or mugs. Just as AppleTV aired the animation ‘The Red Ape Family’ featuring BAYC characters, some companies have purchased NFTs and used the characters in their advertisements. In the current situation where businesses using NFT IP have expanded to product advertising, branding, animation, and books, such a conclusion may be expected. When the creative activities of general users or experts (writers, designers, companies, etc.) become viable, an additional NFT can be promoted, and the value of the original NFT work can increase. This expectation seems to have increased user MWTP NFTs with commercial use rights to use the IP of the underlying image.

Airdropping of an additional NFT project and receiving on/offline and economic benefits did not statistically affect NFT purchase intentions. It is presumed that this is because it is difficult to forecast whether an additional NFT project would be airdropped and to provide additional satisfaction or become a means of generating economic benefits. In addition, the benefits of on/offline events such as parties, goods pop-ups, and dinners for only NFT holders did not affect NFT purchase intentions. NFT providers sometimes provide tokens to its holders as an additional benefit. For example, BAYC holders established their own ApeCoin DAO, launched a cryptocurrency called ApeCoin, and provided it to NFT holders for use in the APE ecosystem (Dovbnya, 2022). However, even these Tokenomics benefits do not directly affect the purchase intention in a situation where the actual value of the token cannot be estimated. This study confirmed that provision of additional benefits, including additional NFT airdrops, is not a significant factor in determining the MWTP for NFTs.

Implications

Extension of ownership value

CryptoPunks, a leader in the NFT market, produced and issued 10,000 NFTs by combining pixelated faces, hairstyles, and accessory types. BAYC, which appeared after CryptoPunks, produced and issued 10,000 NFTs with different combinations of elements such as monkey faces, clothes, costumes, hats, accessories, and background colors rather than human faces. Buyers of both NFTs can “exhibit” their persona, such as using their NFT images as social media profiles. Because the buyer purchased a unique image that differentiates them from the other 9999 holders, the NFT can function as a symbol of the buyer. As such, major NFT projects allow buyers to freely ‘exhibit’ their images.

However, as mentioned earlier, BAYC was able to surpass the popularity of CryptoPunks, partly by granting NFT buyers the right to transform images or to commercially use IP, along with the “exhibition right”. The rights granted to BAYC NFT holders are “ownership and commercial usage.” Specifically, BAYC granted holders the right to “replicate” and sell products and emoticons using NFT images and the right to “create secondary works” to produce and sell other types of media content, such as games, books, advertisements, and TV shows, by creating new media using NFT images. BAYC holders can become entrepreneurs who can generate revenue using NFT images for display, reproduction, and transformation. While NFTs are new and untested by case law, the results of this study indicate that it is very important to users that ownership of an NFT conveys legal and commercial rights to the purchaser, even if most buyers presumably do not intend to obtain commercial income from their use of the NFT.

CryptoPunks, which was acquired by BAYC, is also expected to open the door to creative possibilities by announcing that it allows holders to use its IP license to avoid commercial restrictions in August 2022. Now, in addition to owning a rare artwork, NFT holders can utilize and enjoy full ownership, such as transforming the original work to create new value and commercially using it to generate profits. In addition, even if holders do not directly produce products or content, they have gained the advantage of increasing the awareness and popularity of the NFT through secondary creation of others. Global brands, including Adidas, have expanded public interest in NFTs by commercially utilizing the NFTs owned by companies. It is expected that the size of the NFT market will further expand through not only the primary value generated by NFT transactions, but also various additional contents.

In particular, the virtual online space is functioning as a participatory culture where prosumers consume and produce content at the same time. A participatory culture offers free and open artistic expression and civic engagement, with strong support for creating and sharing (Jenkins and Bertozzi, 2008). Just as the participatory culture of YouTube users drove the growth of the platform (Jung et al., 2022), when the NFT industry serves as a space for participatory culture, it is expected to experience large growth.

In-group identification value

Not only did the NFT purchase intention increase as the numbers of celebrities and community members increased, but also numbers of celebrities and community members were the most important attributes in the analysis of relative importance among NFT attributes. This means that social value, based on the perception of relationships with others, is the most important factor in the NFT purchase process. Yilmaz et al. (2023) have likewise demonstrated that ‘community,’ denoting a social sense of belonging, plays a significant role in driving value. Then, why does social value affect the individual purchase of NFTs?

Tajfel (1978), who first introduced the social identity theory, argued that all humans have a social and psychological tendency to distinguish between groups to which they belong and groups to which they do not belong. Social identity refers to the self-image recognition that one belongs to a particular social group and the emotional and value importance of members of the group to which one belongs (Tajfel, 1982, p.31) and is closely linked to the term social status (Tajfel and Turner, 1979). Our results that increased numbers of celebrities and community members increased NFT purchase intention suggest that those who want to purchase the NFT want to achieve in-group identification and increase their self-esteem. Purchase of an avatar in the PFP NFT project might come with expectation of the level of social identity and status as celebrities and community members who are early adopters or technology pioneers.

According to a study by Zolfagharian and Cortes (2011), identification with a group that shares artistic interests has a significant effect on purchasing behavior for artwork, collectibles, and antique products. The purchase behavior of an NFT, a product of digital artworks and collectibles, can be interpreted in line with these results. Accordingly, it is expected that the recent testing of Twitter and Instagram to provide the NFT profile function can contribute to the development of the PFP NFT market.

An individual can be described more accurately when considering both individual identity, which is relatively consistent within a person, and a social identity, based on shared characteristics (Turner, 1999). The result of a specific NFT purchase intention needs to be interpreted as a combined result of social identity and personal identity.

Limitations and further study

This study has limitations. First, few users are familiar with NFTs as the market remains in an early stage. In this study, a survey was conducted on people working in various blockchain societies and related companies in South Korea, and the number of samples was not large, at only 156 samples.

Second, an NFT is recognized not only as a consumer product, but also as an investment product. Therefore, users will tend to purchase an NFT when there is a possibility of NFT price increase, even if the floor price is already high. However, this research was conducted under the assumption that the floor price was fixed at one of three levels to measure the value of NFT attributes. In future studies, MWTP can be investigated based on estimated current value of an NFT.

Third, the benefits of ownership vary with individual consumption motives. One motive for purchasing NFTs is expectation of monetary profit, as a perspective of investment. Another may be motivated to buy NFTs to obtain satisfaction based on possession of the works of the NFT collection. Others may be motivated to pay for NFTs to receive additional utilities, such as participating in online and offline events as an exclusive member, launching a brand using IP rights, or receiving an airdrop. As purchase motives for NFTs are various, the purchase intention, range of MWTP, and type of NFT to be selected also will vary. Therefore, future studies should research purchase intention related to NFTs in accordance with purchase motives based on gratification theory and expectation-value theory.

Fourth, this study did not examine the impact of user characteristics on NFT preference or the interaction effects between attributes. Because many other factors likely influence NFT preference, we leave this for future research.

A further limitation of this study lies in the fact that the sample was drawn exclusively from participants residing in South Korea. The cultural and geographical specificity of this population may limit the extent to which the findings can be generalized to other contexts. Accordingly, future research should replicate this study in diverse cultural settings or employ cross‐cultural comparative designs to more rigorously evaluate the robustness and external validity of the results.

Data availability

The data supporting the findings of this study are not publicly available due to privacy and ethical restrictions associated with the correctional school setting, as public release may pose a risk of indirect participant identification. De-identified data can be made available from the corresponding author upon reasonable request and subject to approval by the Institutional Review Board of Sungkyunkwan University.

References

Abu-Shanab E, Al-Sharafi MA, Al-Emran M (2024) The influence of network externality and fear of missing out on the continuous use of social networks: a cross-country comparison. Int J Hum-Comput Interact 40(15):4058–4074

Allen DW, Berg C, Lane AM (2023) Why airdrop cryptocurrency tokens? J Bus Res 163:113945

Allenby GM, Rossi PE (1998) Marketing models of consumer heterogeneity. J Econ 89(1-2):57–78

Ante L (2021) The non-fungible token (NFT) market and its relationship with Bitcoin and Ethereum. Available at SSRN 3861106

Aysan AF, Gozgor G, Nanaeva Z (2024) Technological perspectives of Metaverse for financial service providers. Technol Forecast Soc Change 202:123323

Atkin C, Block M (1983) Effectiveness of celebrity endorsers. J Advert Res 23(1):57–61

Barda D, Zaikin R, Vanunu O (2022) AirDrop process of ApeCoin cryptocurrency found vulnerable, led to theft of millions of dollars in NFTs. Check Point Res. https://research.checkpoint.com/2022/airdrop-process-of-apecoin-cryptocurrency-found-vulnerable-led-to-theft-of-millions-of-dollars-in-nfts/

Berger CR, Calabrese RJ (1974) Some explorations in initial interaction and beyond: toward a developmental theory of interpersonal communication. Hum Commun Res 1(2):99–112

Blanchard AL, Markus ML (2004) The experienced “sense” of a virtual community: characteristics and processes. Data Base Adv Inf Syst 35:65–79

Choi KH, Kang SH, Yoon SM (2022) Herding behaviour in Korea’s cryptocurrency market. Appl Econ 54(24):2795–2809

Christidis K, Devetsikiotis M (2016) Blockchains and smart contracts for the internet of things. IEEE Access 4:2292–2303

Dovbnya A (2022) Bored Ape Yacht Club creators launch ApeCoin (APE). U.Today. https://u.today/bored-ape-yacht-club-creators-launch-apecoin-ape

Ellison N, Heino R, Gibbs J (2006) Managing impressions online: self-presentation processes in the online dating environment. J Comput-Mediat Commun 11(2):415–441

Faucher KX (2014) Veblen 2.0: Neoliberal games of social capital and the attention economy as conspicuous consumption. tripleC: communication, capitalism & critique. Open Access J Glob Sustain Inf Soc 12(1):40–56

Fowles J (1996) Advertising and popular culture, vol 5. Sage Publications, Thousand Oaks, CA, USA

Freni P, Ferro E, Moncada R (2020) Tokenization and blockchain tokens classification: a morphological framework. In: IEEE symposium on computers and communications (ISCC). IEEE, New York, USA, pp 1–6

Fröwis M, Böhme R (2019) The operational cost of Ethereum airdrops. In: International workshop on data privacy management. Springer International Publishing, Cham, pp 255–270

Gilbert S (2022) Crypto, web3, and the Metaverse. Bennett Institute for Public Policy, Cambridge, UK

Gnanapragash TJ, Sekar PC (2013) Celebrity-aided brand recall and brand-aided celebrity recall: an assessment of celebrity influence using the hierarchy of effects model. IUP J Brand Manag 10(3):47

Green PE, Srinivasan V (1978) Conjoint analysis in consumer research: issues and outlook. J Consum Res 5(2):103–123

Griffiths P, Costa CJ, Crespo NF (2024) Behind the bubble: exploring the motivations of NFT buyers. Comput Hum Behav 158:108307

Hagel III, Armstrong AG (1997) Net gain. Harvard Business School Press, Boston, MA, USA

Hashemi Joo M, Nishikawa Y, Dandapani K (2020) Announcement effects in the cryptocurrency market. Appl Econ 52(44):4794–4808

Hofstetter R, Fritze MP, Lamberton C (2024) Beyond scarcity: a social value-based lens for NFT pricing. J Consum Res 51(1):140–150

Hong FY (2023) Structural equation model analysis of Taiwanese teenagers’ attitudes and behaviors related to live stream watching. Int J Hum-Comput Interact 40:6091–6108

Ingawale M, Dutta A, Roy R, Seetharaman P (2013) Network analysis of user generated content quality in Wikipedia. Online Inform Rev 37(4):602-619

Iriberri A, Leroy G (2009) A life-cycle perspective on online community success. ACM Comput Surv (CSUR) 41(2):1–29

Jafar RMS, Ahmad W, Sun Y (2023) Unfolding the impacts of metaverse aspects on telepresence, product knowledge, and purchase intentions in the metaverse stores. Technol Soc 74:102265

Jenkins H, Bertozzi V (2008) Artistic expression in the age of participatory culture. In: Engaging art: the next great transformation of America’s cultural life: how and why young people create. Routledge, New York, NY, pp 171–195

Jin DY, Feenberg A (2015) Commodity and community in social networking: Mar x and the monetization of user-generated content. Inf Soc 31(1):52–60

Jo H, Park S, Jeong J, Yeon J, Lee JK (2024) Metaverse gaming: analyzing the impact of self-expression, achievement, social interaction, violence, and difficulty Behav Inform Technol 44(4):749–763

Jung S, Jeong M, Choi M (2022) Classification of K-Pop contents in YouTube on media repurposing. J Cybercommun Acad Soc 39(3):97–136

Kalpokiene J, Kalpokas I (2023) Creative encounters of a posthuman kind–anthropocentric law, artificial intelligence, and art. Technol Soc 72:102197

Kati (2021) Navigating the creator economy gold rush. https://www.voguebusiness.com/companies/navigating-the-creator-economy-gold-rush

Khadijah A, Pangaribuan CH (2023) The age of indulgence: an online impulsive and compulsive buying analysis. In: 8th international conference on informatics and computing (ICIC). IEEE, New York, USA, pp 1–6

Khatri Y (2021) Bored Ape Yacht Club NFTs flip CryptoPunks in terms of floor price. The Block. https://www.theblock.co/post/128338/bored-ape-yacht-club-nft-flip-cryptopunks-floor-price

Ki CWC, Kim YK (2019) The mechanism by which social media influencers persuade consumers: the role of consumers’ desire to mimic. Psychol Mark 36(10):905–922

Ki CW, Chow TC, Li C (2023) Bridging the trust gap in influencer marketing: ways to sustain consumers’ trust and assuage their distrust in the social media influencer landscape. Int J Hum–Comput Interact 39(17):3445–3460

Kim JW, Choi J, Qualls W, Han K (2008) It takes a marketplace community to raise brand commitment: the role of online communities. J Mark Manag 24(3-4):409–431

Lord KR, Putrevu S, Collins AF (2019) Ethnic influences on attractiveness and trustworthiness perceptions of celebrity endorsers. Int J Advert 38(3):489–505

Messias J, Yaish A, Livshits, B (2023) Airdrops: giving money away is harder than it seems. arXiv preprint arXiv: https://arxiv.org/abs/2312.02752

Pentina I, Prybutok VR, Zhang X (2008) The role of virtual communities as shopping reference groups. J Electron Commer Res 9(2):114

Rahman KT (2022) Influencer marketing and behavioral outcomes: How types of influencers affect consumer mimicry? SEISENSE Bus Rev 2(1):43–54

Sabnavis M (2003). Is celebrity advertising effective? Rediff.com. https://www.rediff.com/money/2003/dec/05guest.htm

Sheth JN, Newman BI, Gross BL (1991) Why we buy what we buy: a theory of consumption values. J Bus Res 22(2):159–170

Statista. (2024) NFT – Worldwide. https://web.archive.org/web/20240329102507/https://www.statista.com/outlook/fmo/digital-assets/nft/worldwide

Statista. (2025) NFT – Worldwide. https://web.archive.org/web/20250920144108/https://www.statista.com/outlook/fmo/digital-assets/nft/worldwide

Steiner AD (2022) Bored Apes & Monkey Selfies: copyright & PFP NFTs. Available at SSRN

Sweeney JC, Soutar GN (2001) Consumer perceived value: the development of a multiple item scale. J Retail 77(2):203–220

Tajfel H (1978) Differentiation between social groups. Studies in the social psychology of intergroup relations. Academic Press, London, UK

Tajfel H, Turner J (1979) An integrative theory of intergroup conflict. In: Williams JA, Worchel S (eds) The social psychology of intergroup relations. Wadsworth, Belmont, CA, pp 33–47

Tajfel H (1982) Social psychology of intergroup relations. Annu Rev Psychol 33:1–39

Terranova T (2012) Free labor. In: Scholz T (ed) Digital labor: the Internet as playground and factory. Routledge, New York, USA pp 33–57

Thomas J (2022) The impact of celebrity ownership on NFT collection value. Doctoral dissertation, Stern School of Business, New York

Train K (2001) A comparison of hierarchical bayes and maximum simulated likelihood for mixed logit. Working Paper, Department of Economics, University of California, Berkeley

Train K (2009) Discrete choice methods with simulation, 2nd ed. Cambridge University Press, Cambridge, UK

Train K, Sonnier G (2005) Mixed logit with bounded distributions of correlated partworths. In: Applications of simulation methods in environmental and resource economics. Springer Netherlands, Dordrecht, pp 117–134

Turner JC (1999) Some current issues in research on social identity and self-categorization theories. In: Ellemers, N, Spears R, Dossje B (eds) Social identity: Context, commitment, content. Blackwell, Oxford, UK, pp 6–34

Utz S (2010) Show me your friends and I will tell you what type of person you are: How one’s profile, number of friends, and type of friends influence impression formation on social network sites. J Comput-Mediat Commun 15(2):314–335

Valeonti F, Bikakis A, Terras M, Speed C, Hudson-Smith A, Chalkias K (2021) Crypto collectibles, museum funding and OpenGLAM: challenges, opportunities and the potential of non-fungible tokens (NFTs). Appl Sci 11(21):9931

Veblen T (1899) The theory of the leisure class. Macmillan, New York, USA

Vega E, Camarero C (2024) What’s behind the JPG? Understanding consumer adoption of non‐fungible tokens. Int J Consum Stud 48(2):e13014

Wang D, Wu S, Lin Z, Wu L, Yuan X, Zhou Y, Wang H, Ren K (2021a) “Towards a first step to understand flash loan and its applications in DeFi ecosystem.” In: Proc. 9th International workshop on security in blockchain and cloud computing. pp 23–28. https://doi.org/10.1145/3457977.3460301

Wang Q, Li R, Wang Q, Chen S (2021b) Non-fungible token (NFT): overview, evaluation, opportunities and challenges. arXiv preprint arXiv: https://arxiv.org/abs/2105.07447

Wood G (2014) “Ethereum: a secure decentralised generalised transaction ledger.” Ethereum Project Yellow Paper, 151:1–32

Yli-Huumo J, Ko D, Choi S, Park S, Smolander K (2016) Where is current research on blockchain technology?—a systematic review. PloS ONE 11(10):e0163477

Yilmaz T, Sagfossen S, Velasco C (2023) What makes NFTs valuable to consumers? Perceived value drivers associated with NFTs liking, purchasing, and holding. J Bus Res 165:114056

Zolfagharian MA, Cortes A (2011) Motives for purchasing artwork, collectibles and antiques. J Bus Econ Res 9(4):27–42

Acknowledgements

This research was supported by the "Regional Innovation System & Education (RISE)" through the Seoul RISE Center, funded by the Ministry of Education (MOE) and the Seoul Metropolitan Government. (2025-RISE-01-018-05).

Author information

Authors and Affiliations

Contributions

YB built the idea, DL supervised the manuscript. YB, JK, JS, YN, MC, and DL wrote the main manuscript text and reviewed the manuscript.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This study was reviewed and approved by the Ethics Committee of Sungkyunkwan University (Approval No. SKKU 2025-11-071) on January 3, 2025. The approval covered the collection and analysis of survey data from adult participants aged 20 years or older, with the review board determining that the study involved no more than minimal risk and that potential societal benefits were anticipated. As this research did not involve medical procedures or human experimentation, it posed no risk to participants. Data were collected via an online survey in accordance with the approved protocol and the ethical requirements of the approving institution. The research was conducted in accordance with the principles outlined in the Declaration of Helsinki.

Informed consent

Informed consent was obtained electronically from all adult participants prior to survey participation between January 4 and 8, 2025. Participation was entirely voluntary, and participants were informed about the purpose of the study, the anonymity of their responses, and the use of the data for academic research and publication. The consent procedure was administered by the online marketing company through an online consent form, and no foreseeable risks were associated with participation. Data were collected through an online survey, and all information was kept strictly anonymous, used solely for research purposes.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Baek, Y., Kim, J., Lee, D. et al. Conjoint analysis of key determinants of consumer purchase intentions for profile picture non-fungible tokens. Humanit Soc Sci Commun 13, 405 (2026). https://doi.org/10.1057/s41599-026-06694-2

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-026-06694-2