Abstract

This study utilizes Emissions Trading System (ETS) in China as a quasi-natural experiment, using the data of A-share listed companies during 2009–2018 and the difference-in-differences (DID) method, to examine the impact of ETS on corporate green strategic behaviors. Our findings indicate that the implementation of the ETS can significantly reshape corporate green strategic behaviors, which is reflected in promoting pilot firms to carry out both internal carbon reduction innovation activities and external green merger & acquisition (M&A). Besides, heterogeneous factors, including ETS design features, firm-specific characteristics, and industry attributes, exert differential impacts on firms’ green strategic behaviors. Further analysis confirms that internal innovation and external M&A are complementary.

Similar content being viewed by others

Introduction

Global environment caused by greenhouse gas (GHG) emissions has become an urgent challenge restricting the world’s sustainable development. It exerts far-reaching impacts on ecological balance, economic stability, and social well-being. Against this backdrop, traditional command-and-control environmental regulations struggle to balance the conflict between “rigidity in emission reduction” and “flexibility in economic development” (Bai et al., 2024). However, the market-based environmental regulatory tool, Emissions Trading Scheme (ETS), internalize environmental externalities through ‘carbon pricing’. The ETS builds a synergistic bridge between economic growth and environmental protection, and provide a market-oriented solution that combines flexibility and restraint to achieve the dual goals of economic and environmental benefits (Christian and Frank, 2023). For this reason, systematically exploring the policy effects of ETS has become a core issue of common concerns to policymakers and academics.

Unlike developed economies such as Europe and the United States, China—as the world’s largest carbon emitter and a major emerging economy—faces a more prominent growth-emission reduction conflict (Yu et al., 2023). Specifically, China’s manufacturing-dominated industrial structure, its energy consumption structure overly reliant on fossil fuels, and practical constraints, indicating that China must address dual pressures within ensuring economic growth and strengthening environmental governance for advancing carbon market development. This provides an unique research setting to test whether market-based environmental policies can drive green transformation strategies in emerging markets. More importantly, China’s ETS adopts a phased promotion model of “pilot first, then national implementation”, creating a plausibly quasi-natural experiment that makes rigorous causal identification. This advantage not only enhances the reliability of research conclusions but also offers new insights for other developing countries facing the “growth-emission reduction balance” dilemma to optimize their ETS designs.

Given that ETS pilot policies in emerging economies were implemented relatively late, previous studies on the effects of ETS have mostly focused on developed economies. The conclusions of these studies largely rely on mature regulatory systems and effective high-carbon-price signaling mechanisms (Antoine et al., 2023; Colmer et al., 2024). However, due to significant differences in market mechanisms, technological systems, and environmental regulatory capabilities, China’s carbon price remains relatively low, with a smaller market scale and weaker market efficiency (Fan and Todorova, 2017; Ren and Lo, 2017). This suggests that carbon market experiences from developed economies cannot be directly applied to China and other developing countries. In comparison, studies on ETS in developing countries mainly focus on macro-level emission reduction effects (Zhang et al., 2021; Feng et al., 2024a; Lu et al., 2024a). Micro-level studies have explored the policy’s impacts on corporate green innovation, investment efficiency, capacity utilization, sustainable development performance, and competitiveness (Hu et al., 2023a; Wang et al., 2023; Wang and Zhang, 2024; Zhang and Xi, 2024; Wang and Li, 2024). Yet few studies have systematically examined how the ETS reshapes firm’s green strategic behaviors from the dual perspectives of “internal independent innovation” and “external merger & acquisition (M&A)”, ignoring the potential trade-offs between these two aspects.

On the one hand, Porter Hypothesis depicts that well-designed and strict environmental regulations can drive enterprises to improve innovation investment. Through technological progress, enterprises may reduce emission reduction costs and ultimately achieve a “win-win” of environmental and economic benefits (Zhu et al., 2019; Qi et al., 2021; Hu et al., 2023a). On the other hand, institutional theory argues that under pressure from external environmental regulations, enterprises should actively seek ways to meet legitimacy requirements (Hoffman, 1997). Since internal innovation itself is characterized by high costs, long R&D cycles, and high uncertainty in outcomes, enterprises may—under the pressure of rising carbon costs brought by ETS—acquire target enterprises to obtain mature pollution control technologies, green projects, or carbon allowances. This helps them quickly achieve emission reduction targets and meet policy compliance requirements (Li et al., 2020; Zhang et al., 2024).

Then, how does the ETS affect corporate internal innovation and external green M&A? Furthermore, China’s ETS shows significant differences across pilot regions in terms of policy guarantee systems, offset ratio and carbon price. Under such differentiated institutional designs, systematically exploring how regional differences in ETS design reshape the green strategic behaviors of different enterprises holds important theoretical basis and practical value. Based on this, this paper examines how China’s ETS affects corporate green strategic behaviors from the dual perspectives of “internal innovation” and “external green M&A”, providing direct evidence for evaluating the micro-level policy effects of ETS.

Therefore, this study takes China’s ETS as a quasi-natural experiment by the DID method, and selects A-share listed companies from industries included in ETS pilot programs during 2009–2018 as the research sample to empirically test the impact of the ETS on corporate green strategic behaviors. The results indicate that the implementation of the ETS has reshaped enterprises’ green strategic behaviors: on the one hand, the policy effectively promotes pilot enterprises to carry out carbon reduction innovation activities, and this promotional effect is more prominent in carbon reduction invention patents; on the other hand, the policy also encourages pilot enterprises to conduct green M&A. To verify the robustness of the conclusions, this study conducts a series of robustness tests, including parallel trend test, placebo test, forward-shifting dependent variable, redefinition of treatment and control groups, matching method replacement, and model replacement, generally confirming the reliability of our conclusions. Meanwhile, heterogeneous factors exert differential impacts on enterprises’ green strategic behaviors: these factors include ETS design features (such as the completeness of policy guarantees, differences in offset ratio, and carbon trading price fluctuations), firm-specific characteristics (such as executives’ environmental background, green interlocking director networks, and green investor shareholding), and industry attributes (such as industry type). Extended research confirms that a significant complementary relationship between internal independent innovation and external M&A, and the ETS effectively reduces CO₂ emissions in pilot regions.

The contributions of our research are reflected in the following aspects: Firstly, this paper more accurately measures carbon reduction patents. To align with the carbon emission reduction goal of the ETS, this study constructs a more policy-matched indicator for carbon reduction patents by screening patents whose abstracts contain keywordsFootnote 1. At the same time, this paper further classifies carbon reduction patents into carbon reduction invention patents, carbon reduction utility model patents, and carbon reduction design patents. This not only avoids the ambiguity of general green patents used in previous studies but also more accurately captures the adaptability of different types of carbon reduction patents to the policy goals of the ETS.

Secondly, this study expands the research perspective on the policy effects of the ETS and enriches the literature on the interaction between environmental regulations and micro-level green strategic behaviors. Previous studies mostly focused on either “internal innovation” or “external M&A” alone, making it difficult to fully explain green strategic responses. This study breaks this limitation by systematically examining the influencing mechanisms of the ETS on enterprises from the dual perspectives of internal innovation and external green M&A. It confirms the applicability of the Porter Hypothesis in China’s carbon regulatory context, and also provides new insight for the compliance hypothesis. Overall, these two critical roles offer more comprehensive micro-level evidence for comprehensive understanding diversified green strategic choices under environmental regulatory pressure.

Finally, our exploration deepens the research on the heterogeneous impacts of ETS. Prior studies have paid little attention to the heterogeneous impacts of the ETS on different enterprises (Linghu et al., 2022). Instead of treating the ETS as a homogeneous policy tool, this study explores in depth how regional differences in its institutional design exert differential impacts on the green strategic behaviors of different enterprises. This corroboration provides factual basis for clarifying how market-based environmental regulatory tools transmit to micro-entity behaviors through institutional design differences; and offers guidance for optimizing subsequent ETS design and promoting corporate green transition.

The remaining parts are structured as follows: Section “Institutional background” sorts out the institutional background. Section “Theoretical analysis and hypothesis” proposes theoretical hypotheses. Section “Research design” introduces the research design. Section “Empirical result and analysis” presents and analyzes the empirical results. Section “Further Analysis” conducts further analysis. Conclusions and implications are depicted in Section “Conclusion”. Last but not least, we also draw the Fig. 1 to present the main conclusions.

The figure visually summarizes the core conclusions derived from empirical analysis, presenting the key logical relationships and research findings in a intuitive manner.

Institutional background

In recent years, China has actively advanced practical explorations, such as reducing energy intensity and controlling total carbon emissions, to build a nationwide low-carbon governance system. In October 2011, the National Development and Reform Commission (NDRC) issued the Notice on Launching Emissions Trading Pilot Work, officially approving seven provinces and cities—Beijing, Tianjin, Shanghai, Chongqing, Guangdong, Hubei, and Shenzhen—to launch emissions trading pilot programs. Subsequently, these regions rapidly advanced supporting work for carbon trading, and focused on building institutional frameworks, successively issuing special rules covering allowance management and data verification. Besides, related regions strengthened basic capacity: completing the construction of carbon emission registration systems, fostering third-party verification institutions, and implementing supervision mechanisms. Through a practice-while-improving model, they gradually streamlined the emissions trading process. Starting from June 2013, the carbon trading markets in the seven regions were successively launched, marking the official entry of the market-based carbon pricing mechanism into the pilot operation phase.

As the core market tool for China to address climate change, the ETS realizes market-based regulation of carbon emissions through a dual mechanism of “setting a total carbon emission allowance + allowing cross-entity circulation of allowances”. Its core goal is to promote carbon emission reduction at the lowest economic cost. With the deepening of the pilot process, the carbon markets in the seven regions have all formed rule systems adapted to their own operation rhythms, with trading activity and allowance transaction volume showing an upward trend. However, it should be noted that due to differences in regional industrial structure, policy orientation, and supervision capacity, the pilot regions exhibit significant heterogeneity in institutional design—specifically in key dimensions such as the completeness of policy guarantee systems, offset ratio, and carbon price fluctuation ranges. Against this institutional background, this study focuses on analyzing the core differential dimensions of carbon trading system design, aiming to provide efficient supports for systematically evaluating the micro-level policy effects and macro-level emission reduction value of ETS.

Policy guarantee system

A sound and efficient policy guarantee system is the fundamental support for the effective operation of market-based carbon emission reduction mechanisms (Yi et al., 2018). The policy guarantee system includes two core dimensions: policy supervision and enforcement, and liability constraints. The pilot regions show significant differences in both aspects.

Policy supervision and enforcement

All carbon trading pilots have introduced a third-party verification institution system to ensure the objectivity and independence of CO₂ emission verification. However, the access standards for verification institutions and verifiers vary across pilots. Specifically, Beijing, Shanghai, and Shenzhen have stricter qualification review for verification institutions: they not only set clear requirements for hardware conditions such as registered address, operation period, registered capital scale, and fixed office space, but also put forward specific demands for software capabilities including the institution’s work experience and internal quality control mechanisms.

In particular, Shenzhen further requires third-party verification institutions to establish risk response funds or purchase corresponding liability insurance, strengthening risk prevention and control in the verification process. These three regions also have refined standards for verifier qualification management, with detailed regulations on nationality, age range, education level, professional title, work experience, full-time requirements, professional qualification examination certification, and personal credit. In contrast, other pilot regions have not yet formed unified and clear provisions, resulting in relatively loose supervision. This difference can be attributed to three key factors. First, as China’s most economically dynamic and reform-oriented cities, Beijing, Shanghai, and Shenzhen bear the core mission of “exploring replicable experience and setting a national model” in the ETS pilots. This fundamental positioning compels them to ensure the objectivity and credibility of verification results through strict qualification review, providing a feasible and promotable model for the construction of the national carbon market. Second, their diverse economic structures and enterprise types lead to higher differentiation in enterprises’ verification needs—stricter qualification standards help match verification institutions/verifiers with industry-specific requirements. Third, the frequent activities of carbon trading and the wide impacts of price signal in these three regions require stricter qualification and personnel management to ensure the quality of emission data from the source, avoid market risks caused by verification loopholes, and maintain the fairness and price effectiveness of the carbon market.

Liability constraint system

Lin and Jia (2019) further pointed out that appropriate fines help strengthen the implementation effect of the ETS and enhance enterprises’ awareness of compliance. From the design of liability constraint systems across pilots, administrative penalties mainly include time-limited rectification and fines. Measures such as social credit punishment, incentive-compatible constraints, and linkage with assessment systems have also been gradually introduced, forming a multi-dimensional liability constraint system. Specifically, Chongqing and Tianjin have not included fines in their administrative penalties. Instead, they only adopt measures linked to incentive policies, such as revoking enterprises’ preferential qualifications and suspending relevant subsidies, resulting in relatively moderate overall intensity. Other pilot regions have designed stricter liability constraint systems.

Notably, Tianjin has a large number of traditional heavy industry enterprises, which occupy an important position in the economic structure and contribute significantly to employment and economic growth—while also being major carbon emitters. Strict penalty measures (such as high fines) may severely impact enterprises’ cash flows, even affecting their normal operations, and thus have negative impacts on local economy and employment. Chongqing has a large number of small and medium-sized enterprises (SMEs) in its industrial structure. SMEs have relatively limited resources and capabilities to meet carbon emission compliance requirements; overly strict fines may be unaffordable for them, even leading to the closure of some enterprises. Therefore, the two regions adopt relatively moderate penalty methods to provide enterprises with a buffer period, guiding them to gradually adapt to the ETS while ensuring the stable development of enterprises and promoting emission reduction.

Carbon offset ratio

China Certified Emission Reductions (CCER) refer to carbon emission reductions voluntarily undertaken by domestic enterprises, based on their circumstances and capabilities, which are then verified. These reductions mainly come from renewable energy projects, including wind power, photovoltaic power, hydropower, and biomass power generation. The trading systems of all pilot regions accept CCERs issued by the National Development and Reform Commission (NDRC) as a legitimate offset mechanism. This allows regulated enterprises to use a certain number of CCERs to offset part of their emissions when fulfilling their quota compliance obligations. Given that an appropriate offset ratio can promote enterprises’ efforts to innovate, Beijing and Shanghai have set the offset ratio at no more than 5% of the annual quota or emissions. In Chongqing, the limit is 8%, while Guangdong, Tianjin, Hubei, and Shenzhen have set a cap of 10%.

Carbon trading price

Carbon trading price is the core hub for the effective operation of the ETS, directly affecting the regulatory efficiency of market-based carbon emission reduction tools (Convery and Redmond, 2007). From the pricing logic, carbon trading price is essentially a market equilibrium price, mainly determined by the supply and demand relationship between buyers and sellers of emission rights. As a key signal, the level of carbon trading price directly affects the release of carbon market policy effects. If the carbon price is at a relatively high level, it will effectively stimulate the trading willingness of allowance buyers and sellers, promote free transactions among market entities, enhance the policy effect of the ETS, and drive pilot enterprises to adopt green strategic behaviors to achieve energy conservation and emission reduction goals.

Conversely, if the carbon price remains low for a long time, it will not only fail to reflect the scarcity of emission rights but also weaken enterprises’ emission reduction incentives. In the early stage of China’s carbon market construction, the pilot first model was adopted. During this period, the carbon trading platforms in various areas operated independently, and a unified national pricing mechanism had not yet been formed—leading to significant regional carbon price differentiation (Shan et al., 2016). In terms of average carbon trading price, Beijing, Shanghai, and Shenzhen were relatively higher than other pilot provinces and citiesFootnote 2. The core reason for this difference is that the carbon markets in these three regions have higher marketization levels and stronger independent trading willingness of market entities. Additionally, the strict control of total allowances in these regions highlights the scarcity of emission rightsFootnote 3, which further promotes the increase in trading frequency and allowance liquidity in their carbon markets—ultimately forming a higher carbon price level that better reflects the value of carbon resources.

The figure shows the trend of annual average carbon trading prices in each pilot region.

The figure presents the quantity of allowance allocations in each pilot at the early stage of carbon market establishment (2014).

Based on the differences in the design of carbon emission rights trading systems across different pilots, we have created a table (Table 1) that summarizes the conditions of various pilot projects to better clarify these differences.

Theoretical analysis and hypothesis

Impact of the ETS on corporate innovation

The implementation of the ETS requires pilot firms to purchase allowances for excess carbon emissions. Meanwhile, carbon price fluctuations may increase the uncertainty of future costs. Moreover, failing to meet compliance standards will result in multiple penalties, including fines, credit rating downgrades, and revocation of policy preferences. These penalties directly affect firms’ market reputation and financing capabilities, which intensifies the operational pressure on pilot firms. Facing this pressure, firms tend to re-evaluate their existing production models and cost structures, and explore strategic adjustment paths adapted to carbon constraints. Porter Hypothesis provides theoretical guidance for firms’ strategic choices. It points out that environmental regulations are not merely cost burdens, instead, they can stimulate firms’ motivation for low-carbon innovation. Specifically, pilot firms can transform carbon constraints into a ‘catalyst’ for low-carbon technology innovation through R&D on low-carbon technologies and process upgrades (Qi et al., 2021). In terms of practical benefits, breakthroughs in low-carbon innovation can reduce the marginal emission reduction cost per unit of output, and decrease firms’ long-term compliance expenditures that rely on purchasing external allowances—fundamentally alleviating carbon cost pressure. Factually, if a firm’s actual carbon emissions after technological upgrading are lower than the total allowances approved by the government, the remaining allowances can be sold on the carbon market. This converts “emission reduction achievements” into economic benefits, forming a positive “emission reduction-benefit” cycle and building a sustainable green development model (Hu et al., 2023a). Therefore, this study proposes Hypothesis 1.

H1: The ETS promotes pilot firms to carry out carbon reduction innovation activities.

Impact of ETS on corporate merger & acquisition

Institutional theory argues that under the pressure of external policy regulations, firms tend to seek rapid and effective emission reduction paths to meet policy compliance requirements (Hoffman, 1997). Compared with the gradual emission reduction through internal innovation, green merger & acquisition (M&A)—as a resource integration strategy—provide firms with a faster and more direct way to obtain pollution control technologies and expand market share in green sectors (Lu et al., 2024b).

By acquiring target firms with mature carbon reduction technologies, green projects, or low-carbon assets, firms can obtain key resources for emission reduction in the short term. This avoids the long cycle, high risk, and uncertainty that may accompany internal R&D (Hu et al., 2023b). From a cost-benefit perspective, this immediacy advantage helps firms quickly reduce total carbon emissions, thereby responding to policy requirements promptly and avoiding compliance risks. Besides, the low-carbon technologies and assets acquired through green M&A can also form a synergistic effect with firms’ existing businesses, improving overall carbon management efficiency and even laying the solid foundation for expanding into green business areas in the future. Therefore, this study proposes Hypothesis 2.

H2: The ETS encourages pilot firms to conduct green M&A.

Research design

Sample selection and data sources

The official operation of China’s ETS pilots in seven provinces and cities began in 2013 and 2014, respectively. When determining the research period, this study comprehensively considered two key interfering factors: (1) The 2008 global financial crisis impacted the macroeconomy and firms’ operational behaviors, which might have non-policy-driven effects on carbon emission reduction-related variables. (2) Significant adjustments were made to China’s accounting standards around 2007. Differences in accounting standards could reduce the comparability of financial data.

Based on this, this study finally selects 2009–2018 as the research period (four years before and after the implementation of the pilot policy). This choice minimizes the interference of external shocks and data standard differences on the research conclusions. The initial sample of this study includes firms covered by the ETS pilots and A-share listed companies in their respective industries. Industry classification refers to the Guidelines for Industry Classification of Listed Companies (2016 Revision) issued by the China Securities Regulatory Commission (CSRC).

Meanwhile, to ensure sample quality and research reliability, the initial sample is screened through the following three steps: (1) Exclude samples of firms in special trading status, including those under ST, *ST, and PT. This avoids interference from abnormal financial conditions or unstable operations on the research results. (2) Exclude samples of firms listed after 2009. This ensures that all sample firms have complete operational data and market behavior records at the start of the research period. (3) Exclude samples with missing data for core research variables to ensure the completeness of samples for econometric regression analysis. To further control the potential impact of extreme values on empirical results, all continuous variables are winsorized to eliminate estimation biases caused by outliers. Data are obtained from the Wind Database and the CSMAR Database. Data on firms’ carbon reduction patent applications and green M&A is obtained through manual search and collation.

Model specification

This study constructs Model (1) to test the impact of ETS on firms’ internal innovation. If Hypothesis 1 holds, the regression coefficient (α₁) of the interaction term Post×Treat is expected to be significantly positive. This would indicate that the implementation of the ETS encourages pilot firms to carry out carbon reduction innovation activities. In Model (1), Treat is a dummy variable: it takes the value of 1 if a firm is covered by the ETS pilot, and 0 otherwise. Post is a dummy variable for the implementation of the ETS: it takes the value of 1 in the year of the ETS implementation and subsequent years, and 0 in the years before implementation.

The dependent variable in Model (1), Crpa is a proxy for carbon reduction patent applications. It specifically refers to carbon-related patents, identified by keywords such as “low carbon, emission reduction, greenhouse, GHG, carbon dioxide, CO2, ozone, O3, nitrous oxide, N2O, methane, CH₄, LED, large-unit-replace-small-unit, coal-to-gas conversion, waste heat power generation”, and others in the patent description. Additionally, we classify carbon-related patents into carbon reduction invention patent applications (Cripa) and carbon reduction other patent applications (Cropa), which include carbon reduction utility models patents and carbon reduction design patents.

This study also constructs Model (2) to test the impact of ETS on firms’ external green M&A. If Hypothesis 2 holds, the regression coefficient (α₁) of the interaction term Post×Treat is expected to be significantly positive. This would indicate that the implementation of the ETS promotes pilot firms to conduct green M&A.

The dependent variable in Model (2), Gma is a proxy for “whether to conduct green M&A”. It specifically refers to M&A events whose announcement contains keywords such as “environmental protection, energy conservation, green, low carbon, carbon neutrality, low energy consumption, emission reduction, pollution, recycling, renewable, sustainable”. To identify green M&A, this study conducts a comprehensive analysis of each M&A event: including the background and purpose of the M&A, the business scope of the acquiring firm and the target firm, and the impact of the M&A on the acquiring firm.

In addition, with reference to existing literature and considering factors such as firms’ financial and governance characteristics, the following control variables are selected: number of employees (Employ), debt scale (Debts), return on total assets (Roa), capital expenditures (Capital), net operating cash flow (Ocf), shareholding of the largest shareholder (Top1), proportion of independent directors (Indep), nature of ownership (Soe), political connections (Pc), and CEO-chairman duality (Dual). Furthermore, to mitigate the impact of clustering effects on standard errors, the regression analysis uses robust estimation and conducts clustering adjustment at the province level. Detailed definitions of all variables are presented in Table 2.

Selection of matching variables

Factually, it is impossible to observe the scenario where firms in the treatment group are not included in the ETS pilots. To further mitigate the omitted variable issues caused by model specification bias of observable variables, this study uses the Propensity Score Matching (PSM) method. Specifically, it adopts radius matching (with a radius of 0.01) to select samples from non-ETS pilot firms that are most similar to ETS pilot firms as the control group. By using the control group as a reference, this study examines the impact of the ETS pilot on firms’ green strategic behaviors. This approach helps reduce systematic differences between firms and lowers the estimation bias of using the difference-in-differences (DID) method alone. Besides, to satisfy the common support assumption, this study deletes samples in the non-overlapping region and then conducts a balance test of matching variables. This further verifies the matching quality and the validity of empirical results. This study plots a bias graph of variables for the treatment group and control group before and after matching (Fig. 4) to present the results more intuitively.

This figure depicts the covariate balance of treatment and control groups before and after matching.

Descriptive statistic

Table 3 presents the descriptive statistics of the main research variables. The data show that the mean value of carbon reduction patent applications (Crpa) is 0.3979. After classifying carbon reduction patents, the mean values of carbon reduction invention patent applications (Cripa) and carbon reduction other patent applications (Cropa) are 0.2821 and 0.2033, respectively. These results indicate that there are significant cross-sectional differences in the number of carbon reduction patent applications among different firms. The mean value of “whether to conduct green M&A” (Gma) is 0.2265. The mean value of the interaction term (Post×Treat) is 0.0414, meaning that 4.14% of the samples are covered by the ETS pilot policy. Other control variables are consistent with those in existing studies, and thus are not discussed in detail here.

Empirical result and analysis

Empirical test results and analysis

ETS and carbon reduction innovation

Columns (1) to (3) of Table 4 report the regression results of Model (1). In Column (1), where the dependent variable is Crpa, the coefficient of Post×Treat is 0.0454 and significantly positive at the 10% level. This indicates that the ETS has a positive incentive effect on corporate carbon reduction innovation. According to the Patent Law, patents are classified into three types: invention patents, utility model patents, and design patents. Among them, invention patents have the highest depth of technological innovation and originality, and contribute more significantly to enhancing firms’ core competitiveness and creating value. In contrast, utility model and design patents focus more on improving technology application or optimizing product form, with a relatively lower innovation level. To further analyze the ETS’s impact on the quality of carbon reduction innovation, this study tests carbon reduction patents by type: Column (2) uses Cripa as the dependent variable. The coefficient of Post×Treat is 0.0661 and significantly positive at the 1% level. This shows that the ETS has a more obvious incentive effect on firms’ high-quality carbon reduction innovation. Column (3) takes Cropa as the dependent variable. The coefficient of Post×Treat fails to pass the statistical significance test, indicating that the ETS has no significant promoting effect on low-level carbon reduction innovation.

A possible reason is that during China’s low-carbon transition stage, there is still room to improve the differentiated institutional supports for firms’ innovation. As a market-based environmental regulatory tool, the ETS uses carbon price signals and allowance trading mechanisms to guide firms to allocate innovation resources to carbon reduction invention patents—high in innovation and long-term profit potential. Such innovation not only reduces firms’ marginal emission reduction costs more efficiently, but also builds competitive advantages through technical barriers, indirectly making up for the lack of institutional supports, and validating Hypothesis 1.

ETS and merger & acquisition

Column (4) of Table 4 reports the regression results of Model (2). The coefficient of Post×Treat is 0.8345 and significantly positive at the 1% level. This indicates that the implementation of the ETS significantly increases the probability of pilot firms conducting green M&A. These estimation results confirm Hypothesis 2.

Robust tests

Parallel trend test

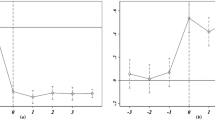

A necessary prerequisite for evaluating policy effects using the DID method is that the treatment group and control group have parallel trends before the policy implementation. Specifically, without the impact of the ETS pilot policy, Cripa, Gma should show similar characteristics and trends in both groups. The only difference is that the treatment group is included in the ETS pilot, while the control group is not. Therefore, this study uses the dynamic regression Models (3) and (4) to test whether the samples meet the parallel trend requirement. The dependent variables and control variables are consistent with those in Models (1) and (2). The newly added explanatory variables are dummy variables for the years before and after the implementation of the ETS pilot policy. The parallel trend requirement stipulates that the coefficients of the interaction terms for Before4, Before3, Before2, and Before1 should all be insignificant.

Table 5 presents the parallel trend test results of Models (3) and (4). The results show that regardless of whether the dependent variable is Cripa or Gma, the coefficients for Before4 to Before1 are all insignificant. The coefficients for Current to After4 are all significantly positive. This result reconfirms Hypotheses1 and Hypotheses2, indicating that the ETS pilot policy not only encourages pilot firms to carry out carbon reduction innovation activities but also promotes them to conduct green M&A. In addition, this study plots parallel trend graphs (Figs. 5, 6) to present the test results more intuitively.

This figure represents a parallel trend test where the dependent variable is the Cripa.

This figure represents a parallel trend test where the dependent variable is the Gma.

Placebo test

To reduce the impact of other shocks and unobservable factors, this study constructs a “false” interaction term between a pseudo-treatment group and a fake policy implementation year. This is done by randomly selecting the treatment group and generating a fake policy implementation time. Then, the benchmark regression is re-estimated. Figures 7,8 respectively present the kernel density plots of the false interaction term coefficients and the kernel density plots of t-values from 1000 placebo tests. These tests correspond to Cripa and Gma. It can be observed that after 1000 random samplings, the coefficients of the false interaction terms are concentrated around zero. In contrast, the coefficients of Post×Treat in the benchmark regression all lie outside the distribution of the placebo test coefficients and are outliers. This indicates that the previous conclusions are not severely biased by other policy shocks or omitted variables.

A Kernel density estimation of coefficients (Cripa). B Kernel density estimation of t-value (Cripa).

A Kernel density estimation of coefficients (Gma). B Kernel density estimation of t-value (Gma).

Redefining the treatment and control groups

To further reduce the measurement errors of the core explanatory variable Post×Treat and enhance the reliability of research conclusions, this study conducts a sensitivity test by adjusting the way policy timing is defined. In the benchmark regression, the definition of Post×Treat strictly follows the actual launch dates of each pilot region: Beijing and Shanghai implemented their carbon trading systems in November 2013, while Guangdong and Tianjin implemented theirs in December 2013. Considering that the launch dates of some pilots are close to the end of the year, this study uniformly adjusts the pilot launch dates of Beijing, Shanghai, Guangdong, and Tianjin to 2014 (the policy shock is recorded as 1 starting from 2014). Based on this new timing definition, Post is redefined, and regressions for Models (1) and (2) are re-estimated. Table 6 presents the regression results. The empirical results show that the core conclusions of this study are not affected by minor adjustments to policy timing and remain robust.

Alternative matching methods

To further mitigate differences in firm characteristics between the treatment group and the control group, this study uses Propensity Score Matching (PSM). Specifically, it selects samples not included in the ETS pilot and performs kernel matching. Then, Models (1) and (2) are re-estimated. Columns (1)–(2) of Table 7 reports the estimation results of kernel matching. It can be observed that in the DID estimation results after changing the matching method, the coefficients of Post×Treat all pass the statistical test at least at the 5% significance level, further supporting the above research conclusions.

Forward-shifting dependent variable

Considering that there may be a lag between firms’ engagement in innovation activities and their patent applications, we set the dependent variable to one period ahead. The empirical results in Column (3) of Table 7 show that this forward-shifted setting of the dependent variable does not change the research conclusions of this study, which indicates that the results of this study are robust.

Alternative model

To enhance the robustness of the previous conclusions, this study re-conducts empirical tests using the Probit model, Tobit model, and Poisson model respectively.

The results are presented in Table 8. It can be observed that regardless of the model used, the coefficients of Post×Treat all pass the statistical test at least at the 5% significance level. This further confirms the reliability of the previous research conclusions.

Heterogeneity test

Policy guarantee system

To reveal the heterogeneous impact of the different designs of the ETS policy guarantee system on firms’ green strategic behaviors, this study conducts a heterogeneity test from two core dimensions of the policy guarantee system: the policy supervision and enforcement system, and the legal liability constraint system. This aims to reveal differences in policy effects under different levels of institutional design intensity.

In the heterogeneity analysis of the policy supervision and enforcement system, samples are grouped based on the strictness of review for “third-party verification institution qualifications” and “verifier practice standards” in each pilot region. Columns (1)−(2) of Table 9 report the regression results. They show that the positive incentive effect of the ETS on pilot firms’ carbon reduction innovation and green M&A is only significant among pilot firms in regions with a strict policy supervision and enforcement system. A possible reason is that a strict supervision and enforcement system can effectively ensure the objectivity and accuracy of carbon emission data verification. This reduces opportunistic behaviors of firms, such as data fraud and compliance arbitrage, and strengthens the rigid constraints of the ETS. Moreover, a standardized supervision environment can also improve firms’ expectations of long-term policy stability, encouraging firms to respond to the policy through substantive strategies such as carbon reduction innovation and green M&A.

In the heterogeneity analysis of the liability constraint system, sample firms are grouped according to the severity of punishment in the liability constraints of each pilot region. Columns (3)−(4) of Table 9 report the estimation results. They show that the positive impact of ETS on firms’ carbon reduction innovation and green M&A is mainly concentrated in pilot firms in regions with strict liability constraints. A possible reason is that under the ETS, strict liability constraints expose firms to higher non-compliance costs. This forces firms to adopt green strategic behaviors, such as carbon reduction innovation and green M&A, to reduce carbon emissions and meet policy compliance requirements.

Offset ratio

To examine the heterogeneous impact of the differentiated designs of Offset ratio in the ETS on firms’ green strategic behaviors, this study groups samples based on whether the allowable offset ratio exceeds 5%. Columns (1)−(2) of Table 10 show that

The ETS has an obvious promoting effect on firms’ green M&A. However, its incentive effect on firms’carbon reduction innovation is mainly concentrated in pilot firms located in regions with higher offset ratios. The above results can be explained from the following perspectives. First, green M&A mainly serves as a rapid path for firms to obtain external green resources, technologies, and legitimacy, which is less restricted by regional offset ratio settings. Therefore, the ETS can significantly stimulate firms’ green M&A regardless of offset ratio levels. Second, carbon reduction innovation relies heavily on long-term R&D investment, high uncertainty, and strong policy support. In regions with higher offset ratio, firms enjoy greater flexibility in fulfilling emission obligations. This reduces short-term cost pressure and encourages enterprises to carry out long-term renewable energy innovation and renovation projects. Third, higher offset ratio helps stabilize firms’ emission reduction expectations and improves investment confidence in renewable energy projects. It provides firms with sufficient policy space to transform energy structure and conduct green technology innovation, thereby strengthening the incentive effect of the ETS on carbon reduction innovation.

Trading price

To explore the heterogeneous role of carbon trading price—a core market signal in the ETS—in firms’ green strategic behaviors, this study groups samples according to the annual median carbon trading price in each region. Columns (3)−(4) of Table 10 show that the ETS’s promoting effects on both firms’ carbon reduction innovation and green M&A are concentrated in pilot firms located in regions with higher carbon trading prices. The underlying logic of this difference can be explained through the dual mechanisms of cost pressure transmission and market value revaluation: From the perspective of cost pressure: Higher carbon trading prices directly increase firms’ carbon compliance costs. When carbon prices are high, if firms maintain their original high-emission production models, they not only have to pay higher fees for purchasing allowances for excessive emissions but also may face greater cost uncertainty due to future carbon price increases (Wu et al., 2024). This dual pressure of “explicit costs + implicit risks” forces firms to take actions: They may conduct internal carbon reduction innovation to reduce carbon emissions per unit of output, fundamentally reducing dependence on external allowances and avoiding long-term carbon cost pressure. They may also carry out green M&A to quickly acquire external low-carbon resources, reducing total carbon emissions in the short term and preventing a surge in compliance costs caused by high carbon prices.

From the perspective of market value revaluation: High carbon prices essentially reflect the market’s pricing of “the scarcity of carbon emission rights” and “the value of low-carbon resources”. When carbon prices are high, the capital market synchronously raises its value expectations for low-carbon technologies and green assets: On one hand, firms’ carbon reduction innovation achievements will be given higher market valuations, encouraging firms to increase R&D investment (Feng et al., 2024b). On the other hand, the M&A value of target firms with low-carbon technologies or green projects will increase as carbon prices rise. By acquiring such targets, pilot firms can not only achieve rapid emission reduction but also gain capital market recognition of value through the integration of low-carbon assets. This further encourages more firms to conduct green M&A.

Executives’ environmental background

To unveil the heterogeneous impact of the ETS on green strategic behaviors of firms with different executive backgrounds, this study defines executives with environmental backgrounds as those whose personal resumes include environmental-related keywords. These keywords include “environment, environmental protection, new energy, clean energy, ecology, low-carbon, sustainability, energy conservation”. Samples are grouped according to “whether executives have environmental backgrounds”. Columns (1)−(2) of Table 11 show that the ETS has an obvious promoting effect on firms’ green M&A. However, its incentive effect on firms’ carbon reduction innovation is mainly concentrated in pilot firms where executives have environmental backgrounds.

The core reason for this heterogeneous result lies in the cognitive empowerment and risk tolerance shaped by executives’ environmental backgrounds: Green M&A can help firms quickly reduce total carbon emissions in the short term, so they often become a direct choice for firms facing environmental regulations. In contrast, carbon reduction invention innovation is accompanied by high risks and long cycles. Thus, whether to choose this more difficult and uncertain green strategic behavior highly depends on executives’ value perception of low-carbon innovation. Executives with environmental backgrounds can more clearly identify the long-term value brought by carbon reduction innovation—such as competitive advantages from technical barriers, and potential benefits like policy subsidies and carbon asset appreciation.

Therefore, these executives have a higher risk tolerance for carbon reduction innovation and are more willing to promote firms to bear low-carbon innovation risks, overcome “short-term cost anxiety”, and allocate resources to carbon reduction technology R&D (Zhang et al., 2025). Meanwhile, executives with environmental backgrounds can better understand the impact of carbon price fluctuations on firms’ long-term costs and better grasp the low-carbon technology orientation of the industry. This allows them to accurately identify high-potential carbon reduction innovation directions, avoiding misallocation of R&D resources due to cognitive biases. In addition, the implementation of carbon reduction innovation also relies on the control of compliance details. Executives with environmental backgrounds are more familiar with compliance requirements such as carbon emission accounting standards and data disclosure norms. They can avoid risks in advance during the carbon reduction innovation process, preventing innovation achievements from failing to be implemented due to technologies not meeting policy standards or non-standard data.

Green interlocking directors

To disclose the heterogeneous impact of the ETS on green strategic behaviors of firms with different statuses of green interlocking directors, this study defines green interlocking directors as those who hold positions in the top management team, board of directors, or board of supervisors of two or more firms simultaneously, and whose personal resumes include keywords such as “green, environmental protection, environment, sustainability, circular, reuse”. Samples are grouped according to “whether a firm has green interlocking directors” to reveal the green strategic empowerment role of green interlocking directors. Columns (3)−(4) of Table 11 show that the ETS has an obvious promoting effect on firms’ green M&A. However, its incentive effect on firms’ carbon reduction innovation is mainly concentrated in pilot firms with green interlocking directors.

A possible reason is that green M&A, with their notable advantage of “ready-to-use”, often become the preferred response path for firms under environmental regulatory constraints. In contrast, carbon reduction invention innovation requires substantial R&D investment and technical accumulation. Green interlocking directors can leverage their green-related professional knowledge and external networks to accurately interpret ETS policy details (such as carbon price fluctuation rules and future allowance adjustment directions) and industry low-carbon technology trends, identifying high-potential low-carbon innovation directions. The cross-firm position advantage of green interlocking directors allows them to transfer low-carbon innovation experiences from other firms to their own firms, helping reduce the cost of information acquisition (Zhao et al., 2025). Additionally, relying on their industry network, green interlocking directors can help firms convey their low-carbon innovation intentions, enhance creditor trust, and expand financing channels such as green credit and carbon-neutral bonds. This “resource effect” effectively eases the capital pressure of carbon reduction innovation, thereby promoting firms to conduct low-carbon innovation.

On the contrary, firms without green interlocking directors often struggle to obtain professional low-carbon innovation information and resources, facing high information asymmetry and financing constraints. Due to insufficient funds and inaccurate grasp of technical trends, these firms may hesitate to engage in carbon reduction innovation activities. Instead, they are more inclined to quickly acquire external low-carbon resources by merging mature green businesses or firms to meet the emission reduction requirements of the ETS.

Green investor

To verify the heterogeneous impact of the ETS on green strategic behaviors of firms with different green investor shareholding statuses, this study identifies green investors by screening funds whose investment objectives, scopes, or strategies include keywords such as “environmental protection, ecology, green, new energy development, clean energy, low-carbon”. These green investors are then matched with the investment records of listed firms. Samples are grouped according to “whether a firm has green investor shareholding” to examine the empowerment role of green investors in firms’ green strategic choices. Columns (1)−(2) of Table 12 show that the ETS has an obvious promoting effect on firms’ green M&A. However, its incentive effect on firms’ carbon reduction innovation is mainly concentrated in pilot firms with green investor shareholding.

A possible reason is that green M&A, which can quickly reduce total carbon emissions in the short term, align with firms’ short-term interests and strategic development needs—making them a direct policy response path for firms to cope with carbon constraints. In contrast, carbon reduction innovation has the triple attributes of “high investment, long cycle, and high risk”, and firms often face difficulties in “accessing financing and high financing costs”. Green investors, with their investment philosophy centered on “environmental protection and sustainable development”, better recognize the long-term value of carbon reduction innovation (Li et al., 2025). They are more willing to support firms’ carbon reduction innovation by holding shares or helping firms connect with specialized financing channels such as green credit and carbon-neutral funds. Second, the shareholding behavior of green investors also has a “reputation endorsement” effect. This not only helps firms attract more environmentally conscious consumers and partners but also enhances their image in the capital market—further expanding financing channels and reducing financing costs, thus providing stable resource support for carbon reduction innovation. Finally, the long-term nature of carbon reduction innovation may conflict with the “short-term performance orientation” of management. Without external supervision, management may worry that low-carbon R&D investment will affect short-term profits, and thus tend to choose “quick-result” paths such as green M&A rather than long-term carbon reduction innovation.

Green investors, however, can rely on their professional knowledge in the environmental field to urge firms to allocate resources to carbon reduction innovation that aligns with long-term development, avoiding management myopia (Lv et al., 2024). In contrast, firms without green investor shareholding often face limited financing channels and cannot afford the high costs of carbon reduction innovation. Moreover, without the reputation endorsement and professional supervision of green investors, firm management is more likely to prioritize short-term financial performance. They choose to quickly meet the compliance requirements of the ETS through green M&A rather than investing resources in long-term carbon reduction innovation.

Industry pollution attribute

To corroborate the heterogeneous impact of the ETS on green strategic behaviors of firms in different industry categories, this study refers to the measures for the Administration of Environmental Information Disclosure of Listed Companies issued by the Ministry of Ecology and Environment of China and the industry classification standards of the China Securities Regulatory Commission (CSRC). It defines high-energy-consumption and high-emission industries—such as thermal power, iron and steel, cement, chemicals, and non-ferrous metals—as heavy-polluting industries. Samples are grouped according to “whether a firm belongs to a heavy-polluting industry”. Columns (3)−(4) of Table 12 show that the ETS has an obvious promoting effect on firms’ green M&A. However, its incentive effect on firms’ carbon reduction innovation is mainly concentrated in pilot firms in heavy-polluting industries.

The potential reasons are that green M&A help firms quickly achieve carbon emission reduction targets in the short term, often becoming a direct option for firms to consider and implement when facing environmental regulations. The core logic behind this heterogeneous result lies in the fundamental differences between heavy-polluting and non-heavy-polluting firms in two aspects: the intensity of carbon emission constraints, and the cost-benefit trade-off logic. Specifically, for heavy-polluting firms, green M&A can quickly ease the urgent pressure of high allowance purchase costs caused by excessive emissions. For non-heavy-polluting firms, green M&A can quickly improve green competitiveness at a relatively low cost. Thus, green M&A, with their advantage of “short-term results”, become a common choice for firms to cope with carbon constraints.

However, the baseline carbon emissions of firms in heavy-polluting industries are much higher than those of non-heavy-polluting firms. If they maintain their original production models, they need to purchase a large number of allowances to cover excessive emissions, leading to extremely high long-term carbon compliance costs (Liu et al., 2025). On the other hand, with the advancement of the “dual carbon” goals (carbon peaking and carbon neutrality), environmental standards for heavy-polluting industries will continue to tighten. If firms only rely on green M&A and lack independent carbon reduction technologies, they will always face risks such as dependence on external resources and uncontrollable costs—even potentially affecting normal operations. Driven by both short-term cost pressure and long-term survival anxiety, heavy-polluting firms often take carbon reduction innovation as a core strategy. This not only helps fundamentally reduce carbon emissions per unit of output, reduce long-term dependence on external allowances, and control carbon compliance costs at the source but also transforms core technologies from carbon reduction innovation into competitive barriers.

Therefore, for heavy-polluting firms, carbon reduction innovation is not only a short-term compliance need but also a green strategic behavior that aligns with long-term survival and competition. Unlike heavy-polluting firms, non-heavy-polluting firms have relatively low baseline carbon emissions and can often meet compliance requirements through green M&A. In addition, the core competitiveness of non-heavy-polluting firms is mostly concentrated in non-environmental fields, so carbon reduction innovation is not their core strategic need. If they invest a large amount of funds and human resources in carbon reduction R&D, they may face the risk of “resource misallocation”. This not only fails to generate direct benefits in the short term but may also squeeze investment in core businesses and affect corporate financial performance. Therefore, under the ETS, non-heavy-polluting firms are more inclined to acquire firms with mature green technologies to quickly obtain necessary resources for low-cost compliance and respond to emission reduction policies.

Further analysis

To explore the relationship between firms’ internal independent carbon reduction innovation and external green M&A, this study uses the Ordered Logit model. It classifies firms’ green strategic behaviors into four discrete choices: only carbon reduction innovation activities (Cripa2), only green M&A (Gma), both carbon reduction innovation activities and green M&A (Cripa2&Gma), and neither carbon reduction innovation activities nor green M&A. Taking “no green strategy” as the reference group, this study examines the differential impact of the ETS on firms’ choices of different green strategic behaviors. The test results in Table 13 show that the ETS has a significantly positive impact on pilot firms’ choices of two green strategic behaviors: only green M&A (Gma) and both carbon reduction innovation activities and green M&A (Cripa2&Gma).

The essence of this strategic choice difference lies in firms’ balance between short-term compliance needs and long-term competitive advantages under the pressure of the ETS: From a short-term perspective, internal carbon reduction innovation requires bearing high R&D investment costs and technical failure risks. It also has a long R&D cycle and high uncertainty in result transformation, making it difficult to quickly meet the carbon emission reduction compliance requirements under the ETS. In contrast, green M&A enable firms to acquire external low-carbon resources (such as core technologies, professional talents, and carbon assets) on a “ready-to-use” basis by purchasing target firms with mature low-carbon technologies, green projects, or surplus allowances. This helps firms quickly reduce total carbon emissions in the short term, meet policy compliance standards efficiently, and effectively offset the risks and lag of internal innovation—making it the preferred path for firms to cope with short-term carbon cost pressure. From a long-term development perspective, although green M&A can alleviate short-term emission reduction pressure, over-reliance on external resources may trap firms in a “technology dependence” dilemma. Firms may fail to develop independent and controllable core green technologies, thus losing technological discourse power in future low-carbon competition.

However, internal carbon reduction innovation—through independent R&D of low-carbon technologies and optimization of low-carbon processes—helps firms build unique technical barriers (Yu et al., 2017) and form green core competitiveness that is difficult for competitors to imitate. This lays the foundation for long-term sustainable low-carbon development (Xie et al., 2019). It is based on the dual insights of short-term compliance and long-term competition that pilot firms show differentiated strategic choices: Some firms prioritize “only green M&A (Gma)” to quickly alleviate short-term emission reduction pressure. Other firms tend to combine the two strategic paths: using green M&A to quickly ease short-term carbon cost pressure, while relying on internal innovation to build long-term technological advantages. Eventually, this forms a strategic synergy effect of “M&A supplement weaknesses, innovation builds barriers”, enabling firms to more calmly respond to the short-term challenges and long-term competition brought by the ETS.

Conclusion

This study takes the implementation of China’s ETS as a quasi-natural experiment and the DID model to test the policy effects of ETS. The findings show that the implementation of ETS can significantly restructure corporate green strategic decisions. Specifically, it promotes pilot firms to carry out internal carbon reduction innovation to consolidate their technological foundation and integrate low-carbon resources through external green M&A.

Meanwhile, heterogeneous characteristics at three levels exert heterogeneous impacts on firms’ green strategic choices and the implementation effects of the ETS policy. At the institutional design level, the completeness of policy guarantees, differences in offset ratio, and fluctuations in carbon trading prices. At the firm-level, executives’ environmental backgrounds, green interlocking director networks, and green investor shareholding status. At the industry level, industry pollution attributes.

Extended studies further verify that firms’ internal independent innovation and external M&A are not mutually exclusive choices but show a complementary relationship. The above research results not only provide empirical evidence for systematically analyzing the policy effects of the ETS in emerging economies but also offer policy references for subsequent optimization of ETS design and precise guidance for corporate green transition—by revealing the heterogeneous impacts of factors such as institutional design and firm characteristics.

Based on these conclusions, this paper puts forward the following policy implications.

On the one hand, optimize ETS design and build a differentiated policy framework for diverse subjects. The ETS should avoid a “one-size-fits-all” approach and refine rules based on heterogeneous characteristics across different dimensions: Supervision and enforcement: In regions with sound policy guarantees and strong corporate compliance capabilities (such as Beijing, Shanghai, Shenzhen), further improve the qualification management of verification institutions and personnel, and strengthen penalties for violations. In regions with weak institutional foundations, first guide firms to adapt through “incentive-bound constraints” (such as replacing fines with subsidy cancellation) and gradually increase supervision intensity. Offset ratio: Implement a dynamic and differentiated offset ratio adjustment mechanism. Given that a higher offset ratio can effectively stabilize firms’ emission reduction expectations, alleviate short-term compliance cost pressure, and thereby incentivize long-term carbon reduction innovation, the regulator should moderately raise the allowable offset ratio to provide sufficient policy space for enterprises to invest in renewable energy innovation and technological transformation. Carbon price stability: Establish a carbon price stabilization mechanism. By adjusting allowance supply and improving price early warning systems, reduce the interference of sharp carbon price fluctuations on firms’ green strategic decisions and ensure clear institutional signals.

On the other hand, guide firms’ green strategic choices by category based on firm heterogeneity targeting firm-level heterogeneity, design hierarchical guidance paths. For firms with executives with environmental backgrounds, green interlocking director networks, or green investor shareholding: Provide supports through special subsidies and carbon financial instruments to encourage them to increase investment in internal carbon reduction innovation and play a leading role in technology. For firms with no executives with green backgrounds, green interlocking director networks, or green investor shareholding: Build a green M&A service platform to screen high-quality low-carbon targets and provide M&A financing convenience. These actions help firms quickly acquire emission reduction capabilities through external integration. Meanwhile, provide supporting low-carbon technology training to promote post-M&A technology digestion and absorption, and guide firms to gradually transition to a M&A+innovation synergy model. For firms in heavy-polluting industries: strengthen both allowance control and innovation incentives. For firms in non-heavy-polluting industries: focus on guiding them to achieve low-cost compliance through green M&A to avoid resource misallocation.

Data availability

The datasets generated and/or analysed during the current study are not publicly available due to licensing restrictions and third-party data use agreements associated with the original data providers, which prohibit unrestricted public redistribution. However, the data and replication materials are available from the corresponding author upon reasonable request for academic and research purposes, subject to compliance with the relevant data use conditions.

Notes

These keywords are as follow: low carbon, emission reduction, greenhouse, GHG, carbon dioxide, CO2, ozone, O3, nitrous oxide, N2O, methane, CH4, LED, large-unit-replace-small-unit, coal-to-gas conversion, waste heat power generation, and etc.

Fig. 2 shows the trend of annual average carbon trading prices in each pilot region.

Fig. 3 presents the quantity of allowance allocations in each pilot at the early stage of carbon market establishment (2014).

References

Antoine D, Daniel N, Frank V (2023) The joint impact of the European Union emissions trading system on carbon emissions and economic performance. J Environ Econ Manag 118:102758

Bai J, Rub H (2024) Carbon emissions trading and environmental protection: international evidence. Manag Sci 70(7):4593–4603

Christian O, Frank S (2023) The market value of decomposed carbon emissions. J Bus Financ Account 50(1-2):3–30

Colmer J et al (2024) Does pricing carbon mitigate climate change? Firm-level evidence from the European Union emissions trading system. Rev Econ Stud 92(3):1625–1660

Convery FJ, Redmond L (2007) Market and price developments in the European Union emissions trading scheme. Rev Environ Econ Policy 1(1):88–111

Fan JH, Todorova N (2017) Dynamics of China’s carbon prices in the pilot trading phase. Appl Energy 208(15):1452–1467

Feng T et al (2024b) The role of carbon price signal in green innovation: evidence from China. J Environ Manag 370: 122787

Feng XC, Zhao YP, Yan RY (2024a) Does carbon emission trading policy have emission reduction effect? An empirical study based on quasi-natural experiment method. J Environ Manag 351:119791

Hoffman AJ (1997) From Heresy to Dogma. New Lexington, San Francisco, CA

Hu H, Qi S, Chen Y (2023a) Using green technology for a better tomorrow: how enterprises and government utilize the carbon trading system and incentive policies. China Econ Rev 78:101933

Hu J, Fang Q, Wu H (2023b) Environmental tax and highly polluting firms’ green transformation: evidence from green mergers and acquisitions. Energy Econ 127(B):107046

Li B et al (2020) Green M&A, legitimacy and risk-taking: evidence from China’s heavy polluters. Account Financ 60(1):97–127

Li XZ et al (2025) Government-guided voluntary environmental regulations and the entry of green investors: evidence from the Chinese green factory program. Resour Energy Econ 84: 101530

Lin B, Jia Z (2019) Energy, economic and environmental impact of government fines in China’s carbon trading scheme”. Sci Total Environ 667(1):658–670

Linghu DZ et al (2022) Implementation strategy and emission reduction effectiveness of carbon cap-and-trade in heterogeneous enterprises. Int J Prod Econ 248: 108501

Liu GC et al (2025) Carbon emissions trading and corporate energy efficiency: evidence from a quasi-natural experiment in China. Technol Forecast Soc Change 212:123959

Lu H et al (2024a) Impacts of pilot carbon emission trading policies on urban environmental pollution: evidence from China. J Environ Manag 359:121016

Lu J, Li H, Guo F (2024b) Low-carbon mergers and acquisitions as a driver for higher energy efficiency: evidence from China’s high. Energy-consuming Co Energy 290:130116

Lv Q et al (2024) Institutional investors’ green activism and corporate green innovation: based on the behind-scene communications. Emerg Mark Financ Trade 60(14):3284–3307

Qi SZ et al (2021) Influence of a pilot carbon trading policy on enterprises’ low-carbon innovation in China. Clim Policy 21(3):318–336

Ren C, Lo AY (2017) Emission trading and carbon market performance in Shenzhen, China. Appl Energy 193(1):414–425

Shan YL, Liu Z, Guan DB (2016) CO2 Emissions from China’s lime industry. Appl Energy 166:245–252

Wang H et al (2023) The impact of carbon emission trading policy on overcapacity of companies: evidence from China. Energy Econ 126: 106929

Wang S, Li J (2024) How carbon emission trading mechanism and supply chain digitization affect manufacturing enterprises’ competitiveness? Evidence from China. J Clean Prod 452:142164

Wang W, Zhang YJ (2024) How does carbon emissions trading scheme affect the investment efficiency of companies? evidence from China. J Environ Manag 368:122273

Wu R et al (2024) Adjustment strategies and chaos in duopoly supply chains: the impacts of carbon trading markets and emission reduction policies. Int Rev Econ Financ 95:103482

Xie XM, Huo JG, Zou HL (2019) Green process innovation, green product innovation, and corporate financial performance: a content analysis method. J Bus Res 101:697–706

Yi L et al (2018) Comprehensive evaluation on the ‘maturity’ of China’s carbon markets. J Clean Prod 198(10):1336–1344

Yu B et al (2023) Approaching national climate targets in China considering the challenge of regional inequality. Nat Commun 14(1):8342

Yu W, Ramanathan R, Nath P (2017) Environmental pressures and performance: an analysis of the roles of environmental innovation strategy and marketing capability. Technol Forecast Soc Change 117:160–169

Zhang SL et al (2021) Shooting two hawks with one arrow: could China’s emission trading scheme promote green development efficiency and regional carbon equality?. Energy Econ 101(5):105412

Zhang W, Xi B (2024) The effect of carbon emission trading on enterprises’ sustainable development performance: a quasi-natural experiment based on carbon emission trading pilot in China. Energy policy 185:113960

Zhang XY et al (2025) The greening power of networks: spillover effect of environmental penalties in director networks. J Environ Manag 375: 124367

Zhang Y et al (2024) Can green technology mergers and acquisitions enhance sustainable development? Evidence from ESG ratings. Sustain Dev 32(6):6072–6087

Zhao JY, Zhao L, Yan TY (2025) Does interlocking directors’ green experience richness enhance the green innovation efficiency of Chinese listed companies?. Sustainability 17(5):2122

Zhu J et al (2019) Low-carbon innovation induced by emissions trading in China. Nat Commun 10(1):4088

Author information

Authors and Affiliations

Contributions

Lu Shen: Writing—original draft, Data curation, Project administration, Methodology, Resources. Shi Chen: Methodology, Formal analysis, Supervision, Writing—review & editing, Validation.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Shen, L., Chen, S. Does ETS reshape corporate green strategic behaviors? Evidence from innovation and merger & acquisition. Humanit Soc Sci Commun 13, 353 (2026). https://doi.org/10.1057/s41599-026-06854-4

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-026-06854-4