Abstract

Since the end of the 1970s, the European Union (EU) has formalized and developed its member States’ longstanding and significant presence in the waters of developing coastal States through fishing access agreements. This study provides the first comprehensive analysis of the change in scope and scale of these agreements since their inception 45 years ago. Facilitated by the EU’s relatively high levels of transparency, we use data from legal texts and vessel authorizations to examine trends in species targeted, financial allocations, and geopolitical dynamics. We show that these agreements have shifted from targeting diverse species to focusing predominantly on tuna. However, we also show that a minor fraction of the EU’s fleet engaged in these agreements benefited from a disproportionate share of public subsidies, as small pelagic fisheries indeed accounted for 63.9% of the overall EUR 4.8 B allocated, while they only accounted for 7.6% of the fishing capacity (in tonnage). As of January 2025, the number of active agreements has declined to nine, reflecting shifting geopolitical and economic interests. EU fishing access agreements illustrate ongoing tensions between economic interests, resource sustainability, and equity. Future agreements will have to balance support to the EU’s distant-water fleet with fairer, more cooperative arrangements to ensure equity and long-term sustainability. This paper provides a clear historical overview of the change in EU access agreements over time to support future analyses comparing the relative merits of different approaches to access arrangements for both resource seekers and owners.

Similar content being viewed by others

Introduction

In 1982, decades of international negotiations came to fruition with the signature of the ‘Constitution’ of the global ocean, the United Nations Convention on the Law of the Sea (UNCLOS)1. Besides inscribing the now widely accepted concept of ‘Exclusive Economic Zones’ (EEZs) in international law, UNCLOS also formalized a number of practices that already existed in less formal or specific ways. One of them is Article 62, on the utilization of living resources, which stipulates that coastal States “shall promote the objective of optimum utilization of the living resources” (paragraph 1). In practice, this means that any coastal State that does not have sufficient capacity to harvest its entire allowable catch “shall, through agreements or other arrangements […] give other States access to the surplus” (Article 62.2); essentially formalizing and providing a global legal basis for pre-existing ‘fishing access agreements’, i.e., commercial contracts that govern the exploitation of the waters of one party by the fishing fleets of another party, sometimes in a reciprocal manner.

Largely as a result of this new legal framework, the fleets of wealthy fishing countries, whose fishing capacity often already exceeded what their own waters could sustainably support, expanded southward into the waters of developing coastal countries under newly negotiated access arrangements (which include formal agreements, as well as other forms of access such as ‘joint ventures’, excluded for this study’s scope)2,3,4,5,6. Scholars have argued that developing coastal States were generally not opposed to formalizing the ingress of foreign fishing vessels as it allowed them to generate an important (and sometimes substantial7) income8. However, access arrangements are not solely economic in nature. Scholars now suggest that they may exacerbate unequal distributions of fishing opportunities, restrict local access to nutritious seafood, and undervalue the wealth being extracted9,10,11.

Access relations are a long-standing area of investigation in social analyses of extractive industries and are something more than property and tenure. Ribot and Peluso described “property as [only] one set of factors (nuanced in many ways) in a larger array of institutions, social and political-economic relations, and discursive strategies”12, whereas the heuristic of their ‘theory of access’ identifies “a bundle of powers [as] a set of relationships through which people and their institutions realize benefits from things”13 (see also ref. 14). The ‘powers of exclusion’15 that access relations thus entail are shaped and shoved by a variety of factors. In debates over fisheries access and governance relations, this requires moving beyond sociologically-flat and ahistorical framings of common pool resources and black-letter law applications of the Law of the Sea, such as within liberal institutionalist and mainstream economic traditions, which tend to reduce fisheries access to a set of technical relations to do with fisheries management and property rights regimes undertaken by ‘rational’, efficiency-maximizing actors. In contrast, the historical practices of access relations tend to involve negotiation based on formal or informal juridical-institutional claims, whether at the international scale under the Law of the Sea governing distant-water fishing (referred throughout as ‘DWF’) fleets’ (i.e., resource seekers) access to fishing opportunities in the EEZs of coastal States (i.e., resource owners)16, the national scale through domestic struggles over access relations in national legislation17, or the local scale where questions of customary tenure and community-based processes of inclusion and exclusion shape who can access a particular bay or fishery18,19. Relations of power tend to sit at the heart of access negotiations, which, in regard to DWF fleets, tend to be highly unequal vis-a-vis developing coastal States; not least because coastal States generally lack the industrial, fiscal, and financial capacity to develop internationally competitive domestic fishing capacity, otherwise they would not be renting access to their ‘surplus fish’ in the first place.

Historicizing fisheries access relations and placing power at the heart of the analysis is compatible with those theoretical approaches to fisheries governance that deploy a systems lens, including those working on the political economy and political ecology of capitalist competition in fisheries20,21,22,23, and those that approach fisheries governance from perspectives that center on questions of the multidimensionality of fisheries, ‘blue justice’, equity, and/or decoloniality24,25,26,27. In this paper, we are concerned with trends in the scope, scale, and support of interstate relations, and the European Union’s (EU) use of access agreements to advance the access relations of certain EU member States’ DWF fleets in the waters of coastal States in Africa and, to a lesser extent, Oceania. Underpinning these relations are geopolitical and geoeconomic power relations that enmesh colonial histories, contemporary trade agreements, spheres of military influence, and official development assistance28,29,30. We do not seek to offer an ex-ante evaluation or propose policy alternatives to the trends identified and analyzed in this article in terms of the reach, design, and utilization of EU access agreements on a global scale since their inception. We thus deliberately avoid normative framings on questions of justice. However, this research can nonetheless inform and support work that deploys such a frame. But we do stress a methodological point in the study of access relations, which is that access is a complex process that is negotiated. Taking specificity into account is imperative to a nuanced understanding and, the inverse follows, i.e., that a ‘general theory’ of access is not possible precisely because of the distinctive historical, juridico-institutional, political-economic, and ecological conditions of each fishery in each EEZ, which can change over time and is often negotiated differently with each DWF entity. We do claim, however, to offer a thorough longitudinal overview of a set of EU-flagged fishers (i.e., resource seekers) as a single entity using the same legal access agreements, but we do not claim to offer systematic conclusions on the fished (i.e., resource holders) because of the diversity of their interests, histories, geographies, etc. We offer two short vignettes on two coastal States in the discussion — Morocco and Senegal — to demonstrate the differentiated and articulated factors that shape access relations, including domestic politics.

We focus on the EU as it has historically been and remains today one of the main incumbents of fishing access in foreign waters, with its DWF fleets benefiting from a wide network of fishing access agreements throughout Africa and Oceania31. The European Commission’s early justifications for agreements to access the fish-rich and (at the time) ‘under-exploited’ waters of African States included the opportunity for EU member States to rebuild some of their overfished domestic fisheries by redistributing the excess capacity to new locations, to supply the growing seafood consumption of the EU population32 and to formalize the existing presence of EU-flagged vessels in various African EEZs (e.g., the Spanish fleet in the waters of Morocco, prior to the entry of Spain into the EU33). The EU is not alone in this expansionary practice, as a small number of other DWF nations also have networks of access arrangements, such as China, Japan, Russia, South Korea, Taiwan, and the USA34,35,36,37. Our case study selection was guided by the EU being the only major DWF entity that makes the legal texts of its State-to-State access agreements freely available in the public domain. In contrast, the access arrangements of other DWFs are notoriously opaque, with the legal agreements generally being confidential, and the role of the State in supporting ‘home’ fleets in negotiations, such as through tied official development assistance, discounted loans, etc., is often obscured. Less transparent and less well understood is the practice of EU companies and citizens establishing ‘joint ventures’ (i.e., ownership divided between a local government or private firm and an EU-based DWF company38), which are excluded from the present paper’s scope because of the limited availability of data.

Although the EU possesses one of the largest fishing fleets in the world in terms of engine power39, it was reported in 2021 that only 259 of its vessels were engaged in fishing activities outside domestic waters40, particularly in Africa and Oceania, where fishing agreements exist, many of which were former colonies. To contextualize this number, there were 75,006 vessels registered in the EU as of January 202141. Furthermore, access agreements appear to only marginally contribute to securing the EU’s food supply, providing around 4–8% of fish consumption according to industry representatives42 and the European Commission43. Despite the obvious marginal contribution of the vessels engaged in DWF in terms of vessel number and fish consumption, they however contribute a significant part of the EU’s total landings in terms of volume and value for the involved countries: for instance, the EU’s Scientific, Technical and Economic Committee for Fisheries (STECF) reported that, in 2019, the 22 French tuna purse seiners operating in distant waters accounted for 12% of the national fleet’s income, while Spain’s more complex DWF fleets (which include tuna purse seiners but also a variety of other fleets) accounted for 42% of the national fleet’s income40. These vessels are also disproportionately supported by the range of fisheries subsidies that the EU — though not uniquely — historically provides44,45.

EU access agreements have substantially changed in scope and content since the first agreement with Senegal in 1979. First, in scope, they have moved from targeting a wide range of species — including coastal and demersal ones, also targeted by local communities — to predominantly offshore, large pelagic species such as tuna31. Second, in content, they gradually abandoned their original and much-criticized ‘cash for access’ model to increasingly include social and environmental clauses, at least on paper31. Although numerous criticisms remain regarding their structural weaknesses in monitoring, control, and surveillance (MCS), their impact on marine ecosystems, and competition with local fishers31, EU agreements are widely recognized as the most transparent, in stark contrast with other DWF fleet arrangements such as China’s agreements, or joint ventures36. This higher level of transparency stems from EU policies, as well as historical endeavors by certain non-governmental organizations (NGO). In particular, all texts pertaining to these agreements are available in raw format on the ‘EUR-Lex & Legal Information Unit’ website of the Publications Office of the EU46 (and see Table S1 for the list of such texts used in the present study). In 2008, Regulation (EC) 1006/2008 on fishing authorizations (also known as the ‘FAR’ regulation47) notably resulted in lists of fishing authorizations to be compiled and accessed through ‘freedom of information’ requests. In July 2015, the (now discontinued) ‘WhofishesFAR’ platform48 was created by a group of environmental NGOs led by Oceana, with the aim of improving the transparency of the EU fishing fleets by rendering accessible the lists of authorizations compiled under the FAR regulation. As a result, this platform published the first-ever list of fishing vessels that were granted authorizations to operate in non-EU waters through public access agreements or international conventions between 2008 and 2014, later updated to 2015. Finally, in January 2018, Regulation (EU) 2017/2403 on the sustainable management of external fishing fleets (also known as the ‘SMEFF’ regulation) entered into force49 and replaced the FAR regulation. Under this new regulation, the European Commission started to publish weekly lists of fishing authorizations, and eventually launched in mid-2023 an online platform providing up-to-date information50, which effectively replaced the NGO-ran ‘WhofishesFAR’ platform.

Despite these substantial improvements with regards to the transparency of the EU’s DWF fleet, the precise extent and nature of EU fleets that have been (and remain) active in the waters of Africa and Oceania is, to date, largely lacking, as neither the agreements nor the authorizations have been compiled, analyzed, and summarized in a way that provides a digestible information on ‘who has fished far’. The primary contribution of the present paper is to fill this data gap. To do so, we extracted data from legal texts and vessel-level authorizations to provide the first historical and comprehensive overview of ‘who has fished far’ as part of the EU network of fishing access agreements since the inception of the first one, with Senegal, 45 years ago. We provide key statistics and time-series on (i) which EU countries have been involved, (ii) in the waters of which developing countries, (iii) to target which species, (iv) with which fishing gears, and (v) against which financial counterpart. This is the first-ever longitudinal study of a DWF fleet’s access arrangements that covers multiple fisheries (location, gear types, and species). We reveal dynamics of change over time in terms of the relative rise or decline of distinct gear types and continuity and change in access agreement partners, insofar as these are with EU-flagged vessels.

Results

Expansion of fishing access agreements over time

The number of active EU fishing access agreements has widely varied over time, geographically expanding to cover a large number of African and Oceanian EEZs (Fig. 1). Three periods can be described:

-

First period: During the 1980s, the number of agreements starkly increased, from a unique agreement with Senegal at the very beginning in June 1979, to five by December 1984 (Equatorial Guinea, Guinea, Guinea-Bissau, and São Tomé & Príncipe having joined), and to 12 by the end of the decade (Angola, Comoros, Gambia, Madagascar, Mauritania, Morocco, Mozambique, and Seychelles having joined) (summarized in Table 1);

-

Second period: Throughout the 1990s and 2000s, the number of agreements continued to expand and reached its highest, with an average of 14 active agreements. The peak of 16 active agreements was attained in the years 1991, 1992, and 2007. Over this period, Cape Verde, Côte d’Ivoire, Gabon, Kiribati, Mauritius, Micronesia, and Solomon Islands signed agreements with the EU. Also, the agreement with Angola stopped in August 2004 and was then denounced51;

-

Third period: Since 2010, the number of active agreements has decreased to a slightly lower and relatively stable level, with an average of 12 active agreements. Over this period, the Cook Islands and Liberia signed an agreement with the EU, and two other agreements stopped and were denounced, with Guinea (in December 2012) and Comoros (December 2016)52.

Map of the network of fishing access agreements developed by the EU around Africa (A) and in the Pacific Ocean (B). The contested zone of Western Sahara (top-left corner) is hatched. The color of the EEZs shows the year of inception of the agreement, countries in parentheses do not currently have protocols in force (i.e., ‘expired’ status), and striked-through countries saw their agreements denounced (see Table 5 for details). NB: this map does not include other types of access arrangements such as private agreements and joint ventures, but see, e.g., FAO36,37. (C) shows the evolution of the number of agreements over time.

By January 2025, the number of active agreements was nine, with the agreements with Angola, Comoros and Guinea being denounced, and the agreements with Cook Islands, Côte d’Ivoire, Equatorial Guinea, Liberia, Micronesia, Morocco, Mozambique, São Tomé & Príncipe, Senegal, and Solomon Islands having expired (i.e., agreements still exist but without a protocol to enforce them) (Table 1).

Engagement of the EU’s fleet in fishing access agreements

These fishing access agreements between the EU and third countries have involved the entire spectrum of the EU’s fishing fleet, from the smallest vessels — e.g., the ANGEL CUSTODIO (ESP000054315), a 5.7 meter-long vessel from the ‘pelagic trawlers & seiners’ category, registered in Spain and targeting small pelagics in Morocco — to the largest fishing vessel in the world, i.e., the ANNELIES ILENA (IRL000I13000), a 144.6 meter-long vessel also from the ‘pelagic trawlers & seiners’ category, currently registered in Poland and targeting small pelagics in Mauritania. Nonetheless, the overwhelming majority of small EU vessels do not operate beyond coastal European waters — besides a few vessels from Spain operating in Morocco, and a number of vessels operating in UK waters since it withdrew from the EU. However, all EU vessels larger than 100 meters except one (SAKALAS-1, which was exported to Comoros in 2008) have operated, at some point, in the EEZs of third countries under access agreements (Fig. 2). Over the 2008–2024 time-period, the mean length of EU vessels engaged in fishing agreements was 45.2 m (sd = 30.1 m), the mean tonnage was 725.8 GRT (sd = 1115.7 GRT), and the number of vessels engaged in agreements has consistently been very low, as it decreased from 0.4% of the entire EU fleet in 2008, to a mere 0.1% in 2024.

Overall proportion (%) of the EU’s fleet that has been engaged in DWF operations under access agreements between 2008 and 2024, by class of length (m) and vessel type. See Fig. S1 for annual proportions.

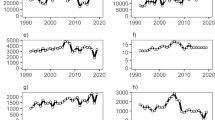

The cumulated capacity in terms of number of vessels has drastically decreased in recent years, from a peak of 1812 vessels in 1999 to a median of 676 vessels since 2020 (i.e., 62.7% decrease). This decrease was largely driven by the reduction in the number of bottom trawlers & dredgers from Spain, which fell from 522 in 1988 to a median of 55 since 2020 (i.e., 89.5% decrease) (Fig. 3A, C). Yet, in terms of tonnage (GRT), the cumulated capacity has decreased at a slower pace, with a peak of 927,426 GRT in 1991 to a median of 620,379 GRT since 2020 (i.e., 33.1% decrease).

Cumulated fishing effort in number of vessels and tonnage (GRT) (from left to right) by A EU fishing country, B coastal country, C vessel type, and D target species, as part of the network of fishing access agreements developed by the EU with countries across Africa and in Oceania, 1979–2024. For each panel, overall proportions are provided as a bar chart next to the time-series. The black line represents the estimated size of the fleet (in vessel number, left, and tonnage, right).

Overall, bottom trawlers & dredgers accounted for 33.3% of the cumulated capacity in terms of number of vessels over the first half of the agreements’ time-series (i.e., June 1979 to March 2002), but only 16.6% in terms of tonnage. In contrast, over the second half of the agreements’ time-series (i.e., April 2002 to December 2024), the cumulated number of tuna purse seiners accounted for 41.3%, which corresponds to 79.0% in terms of tonnage. Over the same time-period (i.e., April 2002 to December 2024), bottom trawlers & dredgers have downgraded to the third rank, with 12.2% of the cumulated capacity in terms of vessel number, and 3.9% in terms of tonnage (Fig. 3C).

Overall, Spain and France consistently dominated the cumulated capacity in terms of number of vessels (56.9% and 25.6%, respectively) and tonnage (49.6% and 37.5%, respectively). Their capacity is composed of large fleets of three sets of gear types: bottom trawlers (23.9% and 9.6% of the overall fishing effort, in number and tonnage) targeting demersal species (34.2% and 11.4% of the overall fishing effort, in number and tonnage); and tuna purse seiners (36.5% and 75.8% of the overall fishing effort, in number and tonnage) and pole-and-liners and surface longliners (25.3% and 5.3% of the overall fishing effort, in number and tonnage) targeting large pelagics (61.8% and 81.1% of the overall fishing effort, in number and tonnage) (Fig. 3A, C, D).

In contrast with the variations observed above in terms of the relative weighting of vessel category active in the first half of the agreements’ time-series (i.e., June 1979 to March 2002) versus the second half (i.e., April 2002 to December 2024), Spain and France have remained consistently dominant over time. In the first half of the agreements’ time-series, these countries accounted for 55.8% and 24.2%, respectively, in terms of vessel number, and 49.4% and 39.0% in terms of tonnage; and in the second half of the agreements’ time-series, they accounted for 58.2% and 27.3%, respectively, in terms of vessel number, and 49.7% and 36.2% in terms of tonnage.

We also estimated the size of the EU’s DWF fleet operating under access agreements by considering that a given vessel may be operating under several agreements. Although less pronounced than the ‘cumulated capacity’ described above, the estimated ‘size of the fleet’ also shows decreasing trends, with a peak of 635 vessels in 1996 to a median of 194 vessels since 2020 (i.e., 69.4% decrease). In terms of tonnage, the size of the fleet peaked at 233,457 GRT in 1999 but only slightly decreased to a median of 183,625 GRT since 2020 (i.e., 21.3% decrease) (Fig. 3, black lines).

This decrease is essentially due to the reduction in scope of the agreements with Morocco and Mauritania, which saw an important reduction around the turn of the century of the number of authorized bottom trawlers and other small vessels using longlines, pots, gillnets, etc. to target demersal species. Considering the estimated size of the fleet without these two agreements, the number of vessels only decreased from a peak of 242 vessels in 1987 to a median of 134 vessels since 2020 (i.e., 44.9% decrease) but, in contrast, the overall tonnage has remained virtually stable, peaking at 151,598 GRT in 2004 and only slightly decreasing to a median of 148,348 GRT since 2020 (i.e., 2.1% decrease).

As explained above, the fact that the size of the fleet is lower than the cumulated capacity is to be expected, as a given vessel may be operating under several agreements. On average, over the entire 1979–2024 time-period, we estimate that pelagic trawlers & seiners targeting small pelagics have been operating under 1.9 agreements in the Atlantic Ocean; pole-and-liners & surface longliners targeting large pelagics have been operating under 7.2 agreements in the Atlantic Ocean, 3.2 agreements in the Indian Ocean and 1.5 agreements in the Pacific Ocean; and tuna purse seiners targeting large pelagics have been operating under 6.8 agreements in the Atlantic Ocean, 3.7 agreements in the Indian Ocean and 1.5 agreements in the Pacific Ocean. These figures have only slightly varied between the first half and the second half of the period considered (not shown here).

Finally, the actual authorizations granted to individual EU vessels — available since 2008 — show a level slightly lower than the fleet size we estimated. Indeed, the actual utilization of licenses is rarely 100% of those allowed for under the agreements, as explicated in the ‘Methods’ section, with the example of French tuna purse seiners in the Indian Ocean on 1 January 2015 (i.e., 18.4 vessels allowed for vs. 12 authorizations granted). This is unsurprising because European Commission negotiators will want to ensure the strategic provision of resource access to the outer range of the number of vessels in the relevant EU fleet(s) so as to avoid renegotiating an agreement during its term. The behavior of the EU fleet is known to be opportunistic, and vessel managers will switch capacity between oceans, depending on fishing conditions and other commercial considerations53, so negotiators will work from the number of vessels that have permission to fish in a given RFMO region, which is higher than the operational number. The number of authorizations decreased from 410 vessels in 2008 (when the database starts) to a median of 126 vessels since 2020 (i.e., 69.3% decrease). In terms of tonnage, the number of authorizations peaked at 209,056 GRT in 2011, to a median of 116,156 GRT since 2020 (i.e., 44.4% decrease) (Fig. 4).

Evolution of the number of authorizations granted to EU vessels, by A EU fishing country, B vessel type, and C target species, 2008–2024.

As highlighted above with the estimation of the true ‘size of the fleet’, the list of actual authorizations confirms that tuna purse seiners were involved, on average across oceans, in 4.1 agreements at any given time, whereas other vessel categories were involved in 1.1, 1.0, and 1.5 agreements. This can be explained by the need to follow tuna populations on their migratory routes across vast expanses of ocean, traversing multiple jurisdictions. Given that tuna purse seiners are also, on average, larger than other types of vessels (except pelagic trawlers & seiners, see Table 2), their relative weight is therefore multiplied in the cumulated capacity shown in Fig. 3C.

Typically, for the vessels operating in the Atlantic Ocean between 2008 and 2024, ‘bottom trawlers & dredgers’ were mostly active in Guinea-Bissau, Mauritania and Morocco, ‘Pelagic trawlers & seiners’ and ‘other vessels’ (which would include various gears such as pots, bottom longlines, gillnets, etc.) in Mauritania and Morocco, ‘pole-and-liners & surface longliners’ in Cape Verde, Guinea-Bissau, Mauritania, Morocco and São Tomé & Príncipe, and ‘tuna purse seiners’ in Cape Verde, Côte d’Ivoire, Gabon, Gambia, Guinea-Bissau, Liberia, Mauritania, Senegal and São Tomé & Príncipe. While for the vessels operating in the Indian Ocean, ‘pole-and-liners & surface longliners’ were mostly active in Madagascar, Mauritius, and Mozambique, and ‘tuna purse seiners’ in Comoros, Madagascar, Mauritius, Mozambique, and Seychelles.

Overall, pole-and-liners & surface longliners and tuna purse seiners dominated the fishing effort in terms of the actual number of authorizations, with 37.6% and 25.6%, respectively. In terms of tonnage, however, tuna purse seiners and pelagic trawlers & seiners overwhelmingly dominated the EU fleet, with 60.2% and 27.5%. The tonnage of tuna purse seiners appears to have remained steady over time (Fig. 4B).

The significance of tuna purse seiners is reflected in the EU fishing countries and target species covered under the fishing access agreements, and Spain and France dominated the fleets authorized under EU agreements since 2008, with 67.4% and 21.1% of the number of vessels, respectively. Also, given that many of these two countries’ vessels almost exclusively target large pelagics, it is also logical that tuna and tuna-like species dominated, with 63.3% of the vessel number and 67.2% of the overall tonnage (Fig. 4).

Allocation of subsidies

Another way to look at EU fishing agreements — beyond the evolution of fleet size and fishing effort, as described above — is to look at them in terms of the provision of public subsidies. By doing so, the panorama of the EU’s fishing agreements is radically different. In fact, out of the 22 countries with which the EU has signed a fishing agreement at some point (see Table 1), only two — Mauritania and Morocco — account for the overwhelming majority of the monetary value of agreements in terms of public subsidies being provided from the EU to the coastal State (i.e., the two components borne by the EU, ‘access fees’ and ‘sectorial aid’). Even though these two agreements were already important in terms of fishing effort, in terms of the cost to the EU of the agreements, those with Mauritania and Morocco together accounted for 73.3% — i.e., EUR 3.5 B of the EUR 4.8 B — of subsidies allocated since 1979, or 40.9% and 32.4%, respectively (Fig. 5B and Table 3). It is important to note that, more generally, revenue from EU access agreements is often embedded in many coastal State economies, which, after up to 45 years of access relations, constitutes a structural linkage, especially for the national budgets of small island developing States such as Madagascar and the Seychelles.

Subsidies allocated by A EU fishing country, B coastal country, C vessel type, and D target species, as part of the network of fishing access agreements developed by the EU with countries across Africa and in Oceania, 1979–2024. For each panel, overall proportions are provided as a bar chart next to the time-series.

The different perspective on trends provided by focusing on public subsidies can be explained by the importance of the fleet targeting small pelagics under these two agreements, with quotas of 240,000 tonnes in 2024 for Mauritania and 185,000 tonnes in 2023 for Morocco (last years of active agreement, respectively). As a result, we also observe an inversion of the contribution by target species in terms of subsidies, compared to the panorama in terms of fishing effort (the same applies for the vessel type, with pelagic trawlers & seiners becoming dominant; not shown here). While large pelagics dominate the fishing effort, with 61.8% of the vessel number and 81.1% of the tonnage, this segment only accounts for 10.2% of the allocated subsidies (still a substantial monetary value of EUR 482.4 M over 45 years). In stark contrast, while small pelagics only account for 4.0% of the vessel number and 7.6% of the tonnage, they account for 63.9% of the allocated subsidies (Table 4), i.e., EUR 3.0 B over 45 years.

As a result of this dominance of the small pelagics component, Spain and France are no longer the sole dominant countries. Another important group emerges in terms of subsidies, those targeting small pelagics, i.e., Netherlands, Lithuania, Latvia, Ireland, Poland, and Germany, which together account for 85.8% of the fishing effort (in GRT) targeting small pelagics (Table 5). Together, these countries appear to account for 42.5% of all subsidies, although they only account for 1.6% and 6.5% of the fishing effort in vessel numbers and tonnage, respectively.

Overall, Tables 3–5 can be summarized in terms of ‘subsidy intensity’ (see ref. 54 for discussion on this concept), i.e., the amount of subsidies received per unit of tonnage (in GRT) as shown in Fig. 6. As highlighted above, this figure shows that:

-

The vessels targeting ‘small pelagics’, i.e., ‘pelagic trawlers & seiners’ benefited from the highest subsidy intensity overall, with 3.95 EUR/GRT. In stark contrast, the vessels targeting ‘large pelagics’, i.e., ‘tuna purse seiners’ and ‘pole-and-liners & surface longliners’ benefited from the lowest subsidy intensity overall, with 0.06 EUR/GRT, i.e., 66.9 times less than the former category;

-

Consequently, the EU countries that are the main users of this vessel type, i.e., Netherlands, Lithuania, Latvia, Ireland, Poland, and Germany, benefited from the highest subsidy intensity overall, with 3.10 EUR/GRT. The countries that mostly targeted large pelagics, i.e., Spain and France, only benefited, in contrast, from a subsidy intensity of 0.24 EUR/GRT;

-

Finally, the coastal countries that offered the most possibilities to target small pelagics are those that benefited from the highest subsidy intensity, i.e., Morocco (2.83 EUR/GRT; small pelagics accounting for 83.4%) and Mauritania (1.51 EUR/GRT; small pelagics accounting for 83.0%).

Subsidy intensity in EUR received per unit of tonnage (GRT), for each vessel type, EU country, and coastal country engaged in EU agreements, with the color of the bar showing the contribution of the target species to the subsidy intensity.

Discussion

Our results illustrate significant trends in the composition, distribution, and economic scale of EU fishing access agreements with third countries over the past 45 years. Overall, 22 agreements were signed, but only nine remain active to date (Table 1), the others having been denounced or are idle (i.e., expired) for a variety of reasons discussed below. Several key points drawn from our analysis can be highlighted:

-

The scope of EU agreements has drastically reduced over time, from targeting a wide diversity of species in their first years of existence (Fig. 3), to now essentially targeting tuna (Figs. 3 and 4). Mauritania is the only remaining substantial ‘non-tuna’ agreement (Fig. 1 and Table 1);

-

These agreements have involved the entire spectrum of the EU fleet, but the largest vessels (tuna purse seiners as well as small pelagics trawlers and seiners) have accounted for the vast majority of the concerned vessels, although they account for a small fraction of the overall EU fleet (Figs. 2 and S1);

-

Fishing opportunities to target ‘small pelagics’ have accounted for the majority of the agreements’ value in terms of allocated subsidies (63.9% of the overall EUR 4.8 B) (Fig. 5D), although they have only accounted for 4.0% and 7.6% of the cumulated capacity in number of vessels and tonnage, respectively (Fig. 3D). It is beyond the scope of this paper to explain the dynamics among actors within the EU that underline such a gap between the apparent weight of the small pelagics fleet (in terms of vessel number or tonnage) and the subsidies it benefit from. We suspect that any explanation will need to go beyond the monetary value of the fish landed, especially considering that the European Court of Auditors has previously raised concerns about the value for money of EU access agreements, including the high unit cost of fish compared to negotiated prices55. Instead, the understanding of this fleet’s apparent disproportionate political clout will require further research on the relationship between seafood lobbying and policy, and the financial and other linkages among entities owning different fleets;

-

In contrast, fishing opportunities to target ‘large pelagics’ have accounted for the majority of fishing effort, with 61.8% and 81.1% of the cumulated capacity in number of vessels and tonnage, respectively (Fig. 3D), but have only accounted for 10.2% of the overall EUR 4.8 B in subsidies (Fig. 5D). Nonetheless, this figure still amounts to EUR 482 M;

-

Overall, it can therefore be said that a minority of the vessels involved in access agreements — which in themselves account for a minority of the overall EU fleet (Figs. 2 and S1) — have benefited from these substantial amounts of public money (Fig. 6), by making the costs of fishing in third countries’ EEZ artificially low compared to if they had to pay for the access themselves. Further research on the political-economic power of fishing entities is needed to explain these outcomes (e.g., is there any inter-penetration and concentration of ownership among the various fishing firms that compose the membership of lobbying bodies? Is there a relationship between dominant industry representatives and public bodies at the scales of regional, national, and/or EU authorities? And from an understanding of the “social conditions and processes that drive ongoing and concerning environmental changes”56, what are the implications for sustainability governance?).

Access arrangements have been identified as being shaped by geopolitical and geoeconomic dynamics, and those with the EU are no exception28. The combination of evolving EU policies, coastal States’ agency, and competition from other foreign industrial fleets has impacted several EU access agreements, and only nine out of 22 are currently active: as shown in Table 1, the agreements with Angola, Guinea, and Comoros stopped being active in 2004, 2012, and 2016, respectively, and have since been denounced, while the agreements with Equatorial Guinea, Micronesia, Solomon Islands, and Mozambique have been idle for 24, 15, 13, and 10 years, respectively. There are diverse rationales for coastal States’ decisions to not renew agreements with the EU — and vice versa — including domestic politics such as prioritizing access for coastal fishing communities, national development aspirations such as policies to not allow foreign-flagged vessels to fish (e.g., in Angola51), competition from other DWF fleets, the failure of the EU and/or coastal State to comply with sub-regional or EU policies, civil unrest (e.g., in Guinea-Bissau57), etc.36. Although it is beyond the scope of this paper to investigate these fisheries once the EU-flagged vessels have exited (e.g., whether other DWF fleets or domesticated foreign fishing vessels replaced EU fleets and to what effects), we do identify this type of comparison as a fruitful area for future research, not least in equipping coastal States with an understanding of the relative merits (or demerits) of different access relations.

With regards to domestic policies not to allow foreign-flagged vessels to fish, Senegal is a striking example. The agreement between the EU and Senegal is the oldest — initiated in 1979 — but was first terminated in 2006 under the presidency of President Abdoulaye Wade. The official justification was the protection of Senegal’s overexploited fish stocks and the need to prioritize local artisanal fishers58. However, the decision was also politically motivated, appealing to nationalist sentiments and the influential fishing communities that form a significant voter base59. In 2014, under President Macky Sall, Senegal signed a new access agreement with the EU, but this reinstatement faced strong opposition from local fishers and environmental groups, who argued that the agreements exacerbated resource depletion and marginalized artisanal fisheries. The 2024 presidential election further complicated the socio-political landscape and has left an uncertain policy environment regarding all fishing arrangements between Senegal and DWF nations. Tensions between rural coastal communities reliant on artisanal fishing and urban elites benefiting from foreign investments, including fisheries, have grown60. Eventually, the depletion of fish stocks due to overfishing by industrial fleets (both legal and illegal, from EU and non-EU fleets) has dire consequences for local fishers, pushing many into economic hardship and contributing to irregular migration, with Senegalese fishers and youth undertaking perilous journeys across the Atlantic in search of better opportunities in Europe61,62. As such, the socio-political consequences of these fishing agreements thus ripple across borders, influencing migration policies and bilateral relations between coastal States and the EU. In late 2024, the EU and Senegal failed to renew their agreement, both sides claiming that it was their choice63, and it remains to be seen whether a new protocol will be agreed on or if Senegal will once again terminate its agreements with foreign fleets.

With regards to the failure by coastal States to comply with EU policies, a prime example is that of the Comoros. In that case, the EU terminated its agreement with the coastal State due to the latter’s persistent failure to address illegal, unreported, and unregulated (IUU) fishing activities, according to the EU64. Besides criticism of Comoros’ inadequate monitoring, control and surveillance (MCS) capabilities, its outdated legal framework, and non-compliance with certain international obligations such as catch reporting to the Indian Ocean Tuna Commission (IOTC), the EU also highlighted that the Comoros operated an open vessel registry, thereby allowing foreign-owned vessels to fly its flag without ensuring a genuine link to the nation65. However, as briefly highlighted below but thoroughly investigated in66, this practice of using ‘flags of convenience’ is a key part of the fishing strategy of many EU companies, including those operating under EU access agreements66. In fact, this EU decision came after the Comoros flag was used eight times between 2009 and 2015 by Lithuanian vessels to circumvent the catch limits authorized by the fishing agreements with Morocco and Mauritania67.

Several agreements have also seen their scope reduced over time, the prime example being Morocco. At its peak, between December 1995 and November 1996, this agreement offered — in return for a colossal annual subsidy of EUR 127 M — important fishing opportunities for small pelagics (i.e., an annual quota of 60,000 tonnes allocated to 49 small to medium vessels totaling 7400 GRT), demersal species (514 vessels targeting black hake, cephalopods, shrimp, and sponge, for a total fishing capacity of 57,811 GRT), and, marginally, large pelagics68. In 2023 (i.e., the last year of activity), the scope of the agreement was radically different: for an annual subsidy of 42.4 million EUR, major opportunities for small pelagics remained (an annual quota of 85,000 tonnes allocated to 26 small vessels totaling 1434 GRT, as well as another 100,000 tonnes allocated to 13 large vessels totaling 41,617 GRT), but a much reduced possibility to target demersal species, with 61 vessels totaling a fishing capacity of 3255 GRT69, i.e., 17.8 times less than at the 1995–96 peak. The evolution of these agreements’ scope will also depend on the impacts of climate change and continued marine biodiversity loss in the regions where these fisheries occur. Other authors have highlighted how increased GHG emissions and subsequent oceanic heating would affect fish stocks targeted under these agreements70,71. Similarly, a recent global assessment on the need for transformative change to address biodiversity loss pointed out that policy instruments such as access arrangements illustrate some of the underlying causes of biodiversity loss through the power imbalances they generate72. These aspects could be explored in future research, with a potential focus on the agreements and fisheries we unpack in this paper.

Similarly to the agreement with Senegal, the future of the agreement with Morocco has recently become uncertain, as the Court of Justice of the EU ruled in October 2024, in the case opposing the Front Polissario to the European Commission, that the agreement with Morocco was “in breach of the principles of self-determination” and therefore illegal73. Given that these contested waters are of strategic importance for the vessels targeting small pelagics, this judgment could be the “nail in the coffin” for the interested companies — as hinted by EU industry representatives74 — which will only be left with the Mauritanian agreement to target these species. In fact, we posit that the agreement may soon be denounced as well, given that it will no longer allow for the exploitation of small pelagics, that possibilities for demersal species have become scarce (see above; likely a combination of domestic overexploitation and lack of interest by Morocco, given its strong domestic fleet and little impact of the EU agreement on its finances75), and that possibilities for large pelagics are virtually non-existent (estimated quota of 235 tonnes in 2023).

Finally, besides those vessels that were scrapped, a number of vessels have also stopped operating under access agreements, and instead started operating under other arrangements such as joint ventures, chartering, etc. Since the first agreement was signed with Senegal in 1979, the EU has indeed implemented stricter rules on illegal fishing, forced labor, transparency, etc., in particular the ‘Common Fisheries Policy’ (CFP), which was implemented in 1983, with the explicit goal to “ensure the protection of fishing grounds, the conservation of the biological resources of the sea and their balanced exploitation on a lasting basis and in appropriate economic and social conditions”76, and was then reformed in 199277, 200278, and 201379. This has likely pushed some of the companies to exit the EU fleet to ‘optimize’ their business model by potentially avoiding many of the rules and regulations that they would have to adhere to fishing under an EU flag or under an EU access agreement. In addition, the use of flags of convenience is not only an opportunistic strategy used by fishing vessels around the world to circumvent regulations, but it is also a response to coastal State policy shifts to domesticate fishing capacity under the national vessel registry, and thus, reflagging by DWF fleets is a way to expand fishing opportunities. Explanations for the decline in the number of vessels in the EU fleet, as identified in our research, are thus varied. To understand why there is such a change would require empirical analysis of individual vessels’ lives after the EU flag. While we suspect that reflagging could be key in explaining a large part of the trends highlighted here, it is beyond the scope of the present paper and should be the subject of future research.

Conclusions

Our results reveal a complex tapestry of social, economic, environmental, and political implications of EU fishing access agreements with third countries. After 45 years of existence, it is clear that these agreements are not merely exchanges of fishing possibilities for financial income but rather emblematic examples of broader struggles over sovereignty, equity (including within the EU, with a small number of vessels targeting small pelagics benefiting from the vast majority of the subsidies), and sustainability. Returning to mobilizing the ‘theory of access’, we showed that these agreements have been a pivotal access mechanism to fishing grounds. They have provided the EU DWF fleets with relative stability in access conditions, while changes in gear types, business strategies, and levels of subsidies have shaped their historical trajectories. They also expose multiple tensions between immediate economic gains, perceived value for money, and the long-term viability of marine resources, as well as the delicate balance between local livelihoods and global industrial interests.

As a result of these tensions, the network of agreements between the EU and third countries has always been in constant evolution, as demonstrated in the present article, either in terms of fishing effort, targeted species, or geographic scope. This evolution will certainly continue into the future, as both the oldest agreement (Senegal, since 1979) and the second largest agreement in terms of subsidies (Morocco; 32.4% of the overall 4.8 billion EUR subsidies) are in jeopardy.

In the near future, the EU will likely continue to support, and perhaps expand, its network of agreements, potentially by increasingly focusing on large pelagics, which are the last segment that has remained relatively unchanged until now. However, given the rising tensions that rapidly evolve around the access to these resources as well, for instance in the Indian Ocean9,80,81, we expect that tensions will continue to grow and questions will continue to be raised regarding the sustainability and balance of benefits provided by these agreements, especially in a world of intensifying competition among DWF nations, that is increasingly politically polarized and facing major risks of climate and biodiversity collapse82,83. At the end of the day, the EU is facing a ‘catch 22’ situation in which it may have to choose between its continued support of its industrial fleets in third countries’ EEZ while fueling local and regional resentment against them, or to engage in truly cooperative arrangements. The latter could mean a strong emphasis on fair benefit-sharing, local onshore development, and prioritization of the well-being of artisanal fishers and coastal communities, which might imply more financial cost for the EU and its fleets and a change of paradigm, letting go of historical privilege and economic power. Coastal States will also continue exploring various arrangements, including with EU or non-EU fleets, to optimize the use of their fishing grounds. This ongoing evolution will lead to multiple forms of access arrangements, of which the modalities and benefits compared to EU agreements remain unknown.

Future research on access arrangements by other DWF fleets, as well as alternative strategies by EU corporations to gain foreign access, could draw on the longitudinal EU case study analyzed here for the purposes of comparing access relations over time. However, the opacity of other DWF fleet arrangements will be a major constraint without major reform of transparency and public disclosure.

Methods

We assembled two datasets by extracting and harmonizing data from documents publicly available on the internet or obtained from the European Commission: (i) a dataset of fishing access agreements established between the EU and third countries, and (ii) a dataset of fishing authorizations delivered by the EU for individual vessels to operate under such agreements. Below, we provide an overview of the methods used to produce these datasets. These methods are thoroughly described in a step-by-step methodological document available in an open-access Mendeley repository at: https://doi.org/10.17632/7xzpjc73mf.1.

Dataset #1: Fishing access agreements (1979–2024)

To constitute this dataset, we manually extracted the following data from the official texts of the EU fishing access agreements, which are available on the ‘EUR-Lex & Legal Information Unit’ website of the Publications Office of the European Union (https://eur-lex.europa.eu/)46 (see Table S1 for references):

-

The time-periods covered by each agreement;

-

The ‘value’ of each agreement, in terms of public subsidies (i.e., ‘access fee’ and ‘sectorial aid’ components, which are both funded by the EU’s tax revenue). This does not include subsequent top-up payments for catch outside of the ‘reference tonnage’, nor does it include the costs borne by the fishing industry, both excluded from the scope of this analysis (but see refs. 31,84);

-

The fishing effort allowed as part of each agreement, in terms of number of vessels and/or tonnage (in either gross tonnage, GT, or gross registered tonnage, GRT; when available), for each category of fishing activity, e.g., tuna purse seiners, bottom trawlers targeting demersal species, etc.;

-

The origin of this fishing effort, i.e., the flag of registration of the allowed vessels.

These data were harmonized and transformed according to a simple methodology (see Mendeley repository) to obtain a dataset of fishing access agreements covering the years 1979 to 2024. We harmonized each record to provide the allowed fishing effort both in number of vessels and tonnage (GRT), converted all values to Euros (EUR) (values were adjusted for inflation, in 2020 EUR; not presented here), and allocated these values to the different fishing categories of fishing activity.

Overall, this dataset contains 1,695,473 records, each of which corresponds to a certain capacity allowed for a given fee to operate in a given EEZ, by a certain type of fishing vessel from a given country targeting a certain species, as exemplified in Table 6. We aggregated the target species and vessel types as follows:

-

‘Large pelagics’ correspond to ‘tuna and tuna-like’ species, often simply identified as ‘tuna’ (e.g., in Côte d’Ivoire85), although ‘swordfish’ is also identified in a few instances (e.g., in Angola86). Over the years, this group has increasingly been identified as ‘highly migratory species’ in a number of agreements (e.g., in Cape Verde87). Under EU agreements, these species are targeted by either ‘tuna purse seiners’ or ‘pole-and-liners & surface longliners’;

-

‘Small pelagics’ correspond to smaller species, lower in the trophic network and often referred to as ‘forage fish’ in the literature. In the EU agreements, they are mostly directly identified as ‘small pelagic species’ (e.g., in Mauritania88) or ‘small pelagics’ (e.g., in Guinea-Bissau89), but additional details are sometimes provided, e.g., ‘mackerel and horse mackerel’ (e.g., in Angola90) or ‘sardine, sardinella, mackerel, horse mackerel and anchovy’ (e.g., in Morocco69). Under EU agreements, these species are exclusively targeted by ‘pelagic trawlers & purse seiners’. Note that the purse seiners in this category operate a similar gear as the ‘tuna purse seiners’ targeting ‘large pelagics’, but they consist of an entirely different fleet in terms of flag, fishing grounds, vessel size, etc.

-

‘Demersal species’ correspond to all species that are neither ‘large pelagics’ nor ‘small pelagics’, i.e., a variety of demersal, bottom-dwelling species often generically identified in the agreements as ‘demersal species/fish’ or simply ‘fish’ (e.g., in Gambia91) or ‘finfish’ (e.g., in Guinea-Bissau89), although additional details are sometimes provided, e.g., ‘black hake’ (e.g., in Mauritania88), ‘cephalopods’ (e.g., in Morocco68), or ‘shrimp’ (e.g., in Guinea-Bissau89). Similarly to the species that compose this category, the vessels that target ‘demersal species’ operate a variety of bottom-contacting gears, predominantly ‘demersal trawlers’ (e.g., in Angola92), but also sometimes ‘bottom longliners’ (e.g., in Cape Verde93), or ‘pots’ (e.g., in Mauritania94).

Dataset #2: Fishing authorizations (2008–2024)

Three distinct sources of fishing authorizations were used to constitute this dataset: (i) one published by ‘WhoFishesFAR’ and downloaded prior to its phasing out48, (ii) one provided by the European Commission following an access to information request in July 2022, and (iii) one published by the European Commission in January 2025 on its new official platform50.

A simple set of operations was then applied to these different datasets (see Mendeley repository) to clean and harmonize them. In particular, we replaced any codes (e.g., ISO3 country codes or fishing gear codes) with actual names (e.g., country names or fishing gear names), and added key characteristics for the authorized vessels, such as length, tonnage, or engine power, using the EU’s fleet register41 (see below). Following these steps, the three datasets were then compared to each other and merged to create a thorough and complete time-series of unique records covering the years 2008 to 2024.

Overall, this dataset contains 2,303,315 daily records, each of which corresponds to an authorization granted to a specific vessel to operate under a specific agreement, as exemplified in Table 7 (same filters as in Table 6).

Other external datasets

The EU’s fleet register41 contains all historical records relating to fishing vessels flagged in EU Member States (including the United Kingdom prior to withdrawal from the EU). As part of this study, we used data downloaded in January 2025, to which we applied a series of simple operations to filter and organize it. The original dataset contained 1,259,433 rows and 40 columns, many of which were of no interest for the purpose of our study (e.g., port of registration, main and subsidiary fishing gears, segment). As such, we simplified this dataset by keeping only the variables of interest (i.e., CFR, IMO, MMSI, length, tonnage, and engine power). Intervals of time with similar values for these variables were combined to reduce the number of rows. As a result, we obtained a reduced dataset of 290,601 rows and 9 columns, which we used to complement our own datasets #1 and #2.

We also used this dataset to estimate the proportion of EU vessels that were engaged in fishing access agreements between 2008 and 2024, by comparing the list of authorized vessels (i.e., dataset #2) to the EU’s entire fleet (see “Engagement of the EU’s fleet in fishing access agreements” section).

Derived time-series

From these datasets, we derived three time-series to analyze the fishing effort that was deployed as part of the fishing access agreements developed by the EU with coastal States across Africa and Oceania:

The ‘cumulated capacity’ corresponds to the sum of all vessels from a certain category allowed to operate at a given date across all agreements. For instance, on 01 January 2015, our agreements’ dataset (i.e., ‘dataset #1’) provides that the following fishing effort is allowed for French tuna purse seiners as part of agreements with coastal States in the Indian Ocean: 21 vessels in Comoros, 19 in Madagascar, 16 in Mauritius, 20 in Mozambique, and 16 in Seychelles. We therefore considered that 92 French tuna purse seiners were allowed to operate in this area, as part of the ‘cumulated capacity’ time-series. In other words, a single vessel that is allowed to operate in three agreements at a given time is counted three times for this indicator.

The ‘size of the fleet’ corresponds to the estimated number of active vessels at a given time, irrespective of the number of agreements under which they operate. Using the example provided above, this does not mean that 92 French tuna purse seiners operate in the area, but rather 18.4 vessels, i.e., the mean number of vessels operating in the various agreements at that date. In other words, if a similar group of vessels is allowed to operate at a given time in two, three, or more agreements within a restricted area (e.g., the Indian Ocean), then each vessel is counted only once for this indicator.

Finally, the ‘actual authorizations’ time-series corresponds to the list of nominal authorizations delivered by the European Commission to operate under the fishing access agreements. This time-series is only available since 2008. Applying the same parameters as those used above, our authorizations’ dataset (i.e., ‘dataset #2’) shows that 12 French tuna purse seiners were actually granted an authorization to operate in the Indian Ocean on 1 January 2015 (Table 8), thus the fleet was either under-utilizing the right to fish at that point in time, or the agreements included fishing capacities beyond the actual capacities of the concerned fleets.

Data availability

The underlying datasets generated and/or analyzed during the current study are available in a Mendeley repository and can be accessed via this link: https://doi.org/10.17632/7xzpjc73mf.1.

Code availability

The underlying code generated and/or analyzed during the current study is available in a Mendeley repository and can be accessed via this link: https://doi.org/10.17632/7xzpjc73mf.1.

References

United Nations United Nations Convention on the Law of the Sea (UNCLOS), Montego Bay (Jamaica), 10 December 1982. Treaty Ser. 1833, 3–581 (1982).

Bonfil, R. et al. The footprint of distant water fleet on world fisheries. http://awsassets.panda.org/downloads/distant_water1.pdf (1998).

Swartz, W., Sala, E., Tracey, S., Watson, R. A. & Pauly, D. The spatial expansion and ecological footprint of fisheries (1950 to present). PLoS ONE 5, e15143 (2010).

Coulter, A. et al. Using harmonized historical catch data to infer the expansion of global tuna fisheries. Fish. Res. https://doi.org/10.1016/j.fishres.2019.105379 (2019).

Le Bail, J. Les accords de pêche C.E.E.-Pays A.C.P Outil de développement ou facteur de crise ?. Rev. Geogr. Norte Gd. 21, 43–49 (1994).

Anon. Evaluation of the relationship between country programmes and fisheries agreements. https://bloomassociation.org/wp-content/uploads/2025/12/Anon-2002-Evaluation-of-fisheries-agreements.pdf (2002).

Gillett, R. & Fong, M. Fisheries in the economies of Pacific Island Countries and Territories (Benefish Study 4) https://purl.org/spc/digilib/doc/ppizh (2023).

Carroz, J. & Savini, M. Les accords de pêche conclus par les Etats africains riverains de l’Atlantique. Annu. Fr. Droit Int. 29, 674–709 (1983).

Sinan, H. et al. Subsidies and allocation: a legacy of distortion and intergenerational loss. Front. Hum. Dyn. 4, 1044321 (2022).

Andreoli, V. et al. Fisheries subsidies exacerbate inequities in accessing seafood nutrients in the Indian Ocean. npj Ocean Sustain. 2, 23 (2023).

Okafor-Yarwood, I., Kadagi, N. I., Belhabib, D. & Allison, E. H. Survival of the richest, not the fittest: how attempts to improve governance impact African small-scale marine fisheries. Mar. Policy 135, 104847 (2022).

Ribot, J. C. & Peluso, N. L. A theory of access. Rural Sociol. 68, 153–181 (2003).

Peluso, N. L. & Ribot, J. Postscript: a theory of access revisited. Soc. Nat. Resour. 33, 300–306 (2020).

Myers, R. & Hansen, C. P. Revisiting a theory of access: a review. Soc. Nat. Resour. 33, 146–166 (2020).

Hall, D., Hirsch, P. & Li, T. M. Powers of Exclusion — Land Dilemmas in Southeast Asia. National University of Singapore (2011).

Havice, E. & Reed, K. Fishing for development? Tuna resource access and industrial change in Papua New Guinea. J. Agrar. Chang. 12, 413–435 (2012).

De Alessi, M. The political economy of fishing rights and claims: the Maori experience in New Zealand. J. Agrar. Chang. 12, 390–412 (2012).

Durrenberger, E. P. & Pálsson, G. Ownership at sea: fiishing territories and access to sea resources. Am. Ethnol. 14, 508–522 (1987).

Fabinyi, M., Dressler, W. & Pido, M. Access to fisheries in the maritime frontier of Palawan Province, Philippines. Singap. J. Trop. Geogr. 40, 92–110 (2019).

Campling, L., Havice, E. & McCall, H. P. The political economy and ecology of capture fisheries: market dynamics, resource access and relations of exploitation and resistance. J. Agrar. Chang. 12, 177–203 (2012).

Havice, E. & Campling, L. Industrial fisheries and oceanic accumulation. In Handbook of Critical Agrarian Studies (eds Akram-Lodhi, A. H., Dietz, K., Engels, B. & McKay, B. M.) 374–386 (Edward Elgar Publishing, 2021).

Barbesgaard, M. The class dynamics of ocean grabbing: who are the ‘fisher peoples’? J. Agrar. Chang. https://doi.org/10.1111/joac.70011 (2025).

Andriamahefazafy, M. & Kull, C. A. Materializing the blue economy: tuna fisheries and the theory of access in the Western Indian Ocean. J. Political Ecol. 26, 323–465 (2019).

Basurto, X. et al. Illuminating the &&multidimensional contributions of small-scale fisheries. Nature 637, 875–884 (2025).

Jentoft, S. & Chuenpagdee, R. Blue justice in three governance orders. In Blue Justice: Small-Scale Fisheries in a Sustainable Ocean Economy (eds Jentoft, S., Chuenpagdee, R., Bugeja Said, A. & Isaacs, M.) 17–32 (Springer International Publishing, 2022).

Ertör, I. We are the oceans, we are the people!’: Fisher people’s struggles for blue justice. J. Peasant Stud. 50, 1157–1186 (2023).

Standen, S. Marine degradation and market dependency in Ghana: food sovereignty as a critique of capital in aquatic food systems. J. Agrar. Chang. https://doi.org/10.1111/joac.70013 (2025).

Campling, L. et al. A geopolitical-economy of distant water fisheries access arrangements. npj Ocean Sustain. 3, 26 (2024).

Alder, J. & Sumaila, U. R. Western Africa: a fish basket of Europe past and present. J. Environ. Dev. 13, 156–178 (2004).

Andriamahefazafy, M., Kull, C. A. & Campling, L. Connected by sea, disconnected by tuna? Challenges to regionalism in the Southwest Indian Ocean. J. Indian Ocean Reg. 15, 58–77 (2019).

Le Manach, F. et al. European Union’s public fishing access agreements in developing countries. PLoS ONE 8, e79899 (2013).

European Commission Proposals relating to structural policy in the fisheries sector. Off. J. C. 243, 1–15 (1980).

Carroz, J. E. & Savini, M. J. The new international law of fisheries emerging from bilateral agreements. Mar. Policy 3, 79–98 (1979).

Pauly, D. et al. China’s distant-water fisheries in the 21st century. Fish. Fish. 15, 474–488 (2014).

Mallory, T. G. China’s distant water fishing industry: evolving policies and implications. Mar. Policy 38, 99–108 (2013).

FAO. Mapping distant-water fisheries access arrangement. https://doi.org/10.4060/cc2545en (2022).

FAO. Institutional and economic perspectives on distant-water fisheries access arrangements. https://doi.org/10.4060/cd1243en (2024).

Crutchfield, J. A., Hamlish, R., Moore, G. & Walker, C. Joint ventures in fisheries. IOFC/DEV/75/37. https://openknowledge.fao.org/server/api/core/bitstreams/4c0be7b4-0fe5-4771-83f9-339b72bb76e6/content (1975).

Rousseau, Y., Watson, R. A., Blanchard, J. L. & Fulton, E. A. Evolution of global marine fishing fleets and the response of fished resources. Proc. Natl. Acad. Sci. USA 116, 12238–12243 (2019).

STECF. The 2021 Annual Economic Report of the EU Fishing Fleet (STECF 21-08). (2021) https://doi.org/10.2760/60996. (2021).

European Commission. Fleet register. https://webgate.ec.europa.eu/fleet-europa/search_en (2024).

Europêche. European fishing access in Africa — Sustainable Fishing Partnership Agreements (SFPAs). http://chil.me/europeche/infographics (2015).

Johnson, A. F. et al. The European Union’s fishing activity outside of European waters and the Sustainable Development Goals. Fish. Fish. 22, 532–545 (2021).

Skerritt, D. J. et al. A 20-year retrospective on the provision of fisheries subsidies in the European Union. ICES J. Mar. Sci. https://doi.org/10.1093/icesjms/fsaa142. (2020).

Skerritt, D. J. et al. Mapping the unjust global distribution of harmful fisheries subsidies. Mar. Policy 152, 105611 (2023).

Union European. EUR-Lex — Access to European Union Law. https://eur-lex.europa.eu/ (2022).

Council of the EU. Council regulation (EC) no. 1006/2008 of 29 September 2008 concerning authorisations for fishing activities of Community fishing vessels outside Community waters and the access of third country vessels to Community waters, amending Regulations (EEC) No 2847/93 and (EC) No 1627/94 and repealing Regulation (EC) No 3317/94. Off. J. L 286, 33–44 (2008).

Oceana. WhoFishesFAR — Database on EU External Water Fleet. http://www.whofishesfar.org/ (2015).

European Parliament and Council of the EU Regulation (EU) 2017/2403 of the European Parliament and of the Council of 12 December 2017 on the sustainable management of external fishing fleets, and repealing Council Regulation (EC) No 1006/2008. Off. J. L 347, 81–104 (2017).

European Commission. Fishing authorisations. https://ec.europa.eu/oceans-and-fisheries/fisheries/fishing-authorisations/screen/agreements (2023).

European Community Council Regulation (EC) No 1185/2006 of 24 July 2006 denouncing the agreement between the European Economic Community and the Government of the People’s Republic of Angola on fishing off Angola and derogating from Regulation (EC) No 2792/1999. Off. J. L 214, 10–11 (2006).

Council of the EU Council Decision (EU) 2018/757 of 14 May 2018 denouncing the Partnership Agreement in the fisheries sector between the European Community and the Union of the Comoros. Off. J. L 128, 13–15 (2018).

Campling, L. The tuna ‘commodity frontier’: business strategies and environment in the industrial tuna fisheries of the Western Indian Ocean. J. Agrar. Chang. 12, 252–278 (2012).

Skerritt, D. J. & Sumaila, U. R. Broadening the global debate on harmful fisheries subsidies through the use of subsidy intensity metrics. Mar. Policy 128, 104507 (2021).

European Court of Auditors. Special report — Are the Fisheries Partnership Agreements well managed by the Commission? https://www.eca.europa.eu/lists/ecadocuments/sr15_11/sr_fisheries_en.pdf (2015).

Longo, S. B., Isgren, E. & Carolan, M. Critical sustainability science: advancing sustainability transformations. Sustain. Sci. https://doi.org/10.1007/s11625-025-01667-x (2025).

European Parliament. Recommendation on the draft Council decision on the conclusion, on behalf of the European Union, of the Protocol on the implementation of the Fisheries Partnership Agreement between the European Community and the Republic of Guinea-Bissau (2024–2029). https://www.europarl.europa.eu/doceo/document/A-10-2025-0028_EN.pdf (2025).

Carver, E. To renew or not to renew? African nations reconsider EU fishing deals. Mongabay (2024).

Poteete, A. R. Electoral competition, clientelism, and responsiveness to fishing communities in Senegal. Afr. Aff. 118, 24–48 (2018).

Philippe, J. EU-Senegal fisheries partnership: transparency is essential at all levels. https://www.cffacape.org/publications-blog/eu-senegal-fisheries-partnership-transparency-is-essential-at-all-levels (2023).

Garcia, H. & Dione, N. Senegal’s fishermen head for Spain as fish stocks dwindle at home. https://www.reuters.com/world/africa/senegals-fishermen-head-spain-fish-stocks-dwindle-home-2024-03-22/ (2024).

Gil, C. G. Debates y controversias en la cooperación al desarrollo — Fondos privados de ayuda, acuerdos neocoloniales y ayuda a refugiados (Publicacions de la Universitat d’Alacant, 2020).

Atuna. Senegal lashes out at EU over ‘untruth’ about tuna SFPA. www.atuna.com/news/senegal-lashes-out-at-eu-over-untruth-about-tuna-spfa/ (2024).

European Parliament EU-Comoros fisheries partnership agreement: denunciation (Resolution) — European Parliament non-legislative resolution of 15 March 2018 on the draft Council decision denouncing the Partnership Agreement in the fisheries sector between the European Community and the Union of the Comoros (14423/2017 – C8-0447/2017 – 2017/0241(NLE) – 2017/2266(INI)). Off. J. C. 162, 116–118 (2019).

European Commission Commission Decision of 1 October 2015 on notifying a third country of the possibility of being identified as a non-cooperating third country in fighting illegal, unreported and unregulated fishing (2015/C 324/07). Off. J. C. 234, 6–14 (2015).

Froment, T. et al. Hidden costs and propped-up profits: unraveling the economics of Europe’s purse-seine tuna fishing industry. npj Ocean Sust. https://doi.org/10.1038/s44183-025-00165-y (2025).

EJF, Oceana, The Pew Charitable Trusts & WWF. Ensuring better control of the EU’s external fishing fleet — Reflagging by EU fishing vessels — The need for stricter standards. https://europe.oceana.org/wp-content/uploads/sites/26/d_files/reflagging_by_eu_fishing_vessels_eng.pdf (2016).

European Union Protocole fixant les possibilités de pêche et les montants de la compensation financière et des appuis financiers. Off. J. L 306, 32–43 (1995).

European Union Protocol on the implementation of the Sustainable Fisheries Partnership Agreement between the European Union and the Kingdom of Morocco. Off. J. L 77, 18–55 (2019).

Bell, J. D. et al. Pathways to sustaining tuna-dependent Pacific Island economies during climate change. Nat. Sustain. 4, 900–910 (2021).

Guillotreau, P., Campling, L. & Robinson, J. Vulnerability of small island fishery economies to climate and institutional changes. Curr. Opin. Environ. Sustain. 4, 287–291 (2012).

Frantzeskaki, N. et al. Overcoming the challenges of achieving transformative change towards a sustainable world. In Thematic Assessment Report on the Underlying Causes of Biodiversity Loss and the Determinants of Transformative Change and Options for Achieving the 2050 Vision for Biodiversity of the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (eds. O’Brien, K., Garibaldi, L. & Agrawal, A.) (IPBES secretariat, 2024).

Court of Justice of the European Union. Judgments of the Court in Joined Cases C-778/21 P and C-798/21 P | Commission and Council v Front Polisario and in Joined Cases C-779/21 P and C-799/21 P | Commission and Council v Front Polisario. https://curia.europa.eu/jcms/upload/docs/application/pdf/2024-10/cp240170en.pdf (2024).

Pelagic Freezer Trawler Association. PFA responds to Court of Justice of the European Union decision on EU-Morocco fisheries agreement. https://www.pelagicfish.eu/pfa-responds-to-court-of-justice-of-the-european-union-decision-on-eu-morocco-fisheries-agreement/ (2024).

European Parliament. Recommendation on the draft Council decision on the conclusion of a Protocol between the European Union and the Kingdom of Morocco setting out the fishing opportunities and financial compensation provided for in the Fisheries Partnership Agreement between the European Community and the Kingdom of Morocco. https://www.europarl.europa.eu/doceo/document/A-7-2011-0394_EN.html (2011).

Council of the European Communities Council Regulation (EEC) No 170/83 of 25 January 1983 establishing a community system for the conservation and management of fishery resources. Off. J. L 24, 1–13 (1983).

Council of the European Communities Council Regulation (EEC) No 3760/92 of 20 December 1992 establishing a community system for fisheries and aquaculture. Off. J. L 389, 1–13 (1992).

Council of the EU Council Regulation (EC) No 2371/2002 of 20 December 2002 on the conservation and sustainable exploitation of fisheries resources under the common fisheries policy. Off. J. L 358, 59–80 (2002).

European Parliament and Council of the EU Regulation (EU) No 1380/2013 of the European Parliament and of the Council of 11 December 2013 on the Common Fisheries Policy, amending Council Regulations (EC) No 1954/2003 and (EC) No 1224/2009 and repealing council regulations (EC) No 2371/2002 and (EC) No 639/2004 and council decision 2004/585/EC. Off. J. L 354, 22–61 (2013).

Andriamahefazafy, M. et al. Fishing access arrangements, catch attribution and allocation — IOTC-2023-TCAC11-INF02. https://iotc.org/sites/default/files/documents/2022/12/IOTC-2023-TCAC11-INF02_ANCORS_Info_Paper_on_Access_Agreements_and_Catch_Attribution_for_TCAC_2023.pdf (2023).

Andriamahefazafy, M. et al. Advancing tuna catch allocation negotiations: an analysis of sovereign rights and fisheries access arrangements. npj Ocean Sustain. 3, 16 (2024).

Ripple, W. J. et al. The 2024 state of the climate report: perilous times on planet Earth. BioScience https://doi.org/10.1093/biosci/biae087 (2024).

Trust, S. et al. Planetary solvency — Finding our balance with nature — global risk management for human prosperity. https://actuaries.org.uk/document-library/thought-leadership/thought-leadership-campaigns/climate-papers/planetary-solvency-finding-our-balance-with-nature/ (2025).

Walmsley, S. F., Barnes, C. T., Payne, I. A. & Howard, C. A. Comparative study of the impact of Fisheries Partnership Agreements. Tech. Rep. Marine Resources Assessment Group Ltd (MRAG), Cambridge Resource Economics, and Natural Resources Institute (2007).

European Union Protocol setting out, for the period from 1 July 2004 to 30 June 2007, the fishing opportunities and financial contribution provided for in the agreement between the European Economic Community and the Republic of Côte d’Ivoire on fishing off the coast of Côte d’Ivoire. Off. J. L 76, 4–15 (2005).

European Economic Community Protocol defining, for the period 3 May 1989 to 2 May 1990, the fishing opportunities and financial compensation provided for in the Agreement between the European Economic Community and the People’s Republic of Angola on fishing off Angola. Off. J. L 341, 9–18 (1989).

European Union Protocol on the implementation of the Fisheries Partnership Agreement between the European Community and the Republic of Cape Verde (2019-2024). Off. J. L 154, 3–29 (2019).

European Union Protocol implementing the Sustainable Fisheries Partnership Agreement between the European Union and the Islamic Republic of Mauritania. Off. J. L 439, 14–101 (2021).

European Union Protocol on the implementation of the Fisheries Partnership Agreement between the European Community and the Republic of Guinea-Bissau (2019-2024). Off. J. L 173, 3–34 (2019).

European Union Protocol setting out, for the period from 3 August 2002 to 2 August 2004, the fishing opportunities and the financial contribution provided for by the Agreement between the European Economic Community and the Government of the Republic of Angola on fishing off Angola. Off. J. L 351, 92–111 (2002).

European Union Protocol establishing the fishing rights and financial compensation provided for in the Agreement between the European Economic Community and the Republic of The Gambia on fishing off the coast of The Gambia for the period 1 July 1993 to 30 June 1996. Off. J. L 79, 2–10 (1994).

European Union Protocol Defining, for the period from 3 May 1999 to 2 May 2000, the fishing opportunities and financial compensation provided for in the Agreement between the European Community and the Government of the People’s Republic of Angola on fishing off Angola. Off. J. L 17, 3–21 (2000).

European Union Protocol setting out the fishing opportunities and financial contribution provided for in the Agreement between the European Economic Community and the Republic of Cape Verde on fishing off the coast of Cape Verde for the period from 1 July 2001 to 30 June 2004. Off. J. L 47, 25–33 (2002).

European Union Protocol setting out the fishing opportunities and financial contribution provided for in the Fisheries Partnership Agreement between the European Community and the Islamic Republic of Mauritania for the period 1 August 2008 to 31 July 2012. Off. J. L 203, 4–59 (2008).

Acknowledgements

This study is part of a research program funded by OAK Foundation, The Waterloo Foundation, the Agence Française de Développement (AFD), and BLOOM’s individual donors. The funders played no role in study design, data collection, analysis, and interpretation of data, or the writing of this manuscript.

Author information

Authors and Affiliations

Contributions