Abstract

Since the 1980s, disproportionate top earnings growth in large cities has fueled a resurgence in the spatial concentration of top earnings across countries in the global north. Research attributes this trend to national top earnings growth or globalization but has left unanswered how national and local top earnings growth coincide and why this phenomenon occurs in cities less central to the global economy. Here we show that earnings growth in finance since the 1980s has concentrated top earnings in the few cities where financial market jobs cluster. Using administrative linked employer–employee data for ten countries in the global north from 1989 to 2019, we show that this pattern extends beyond major global cities to smaller financial cities. Comparing financial cities with similar domestic cities shows that this contribution is not just a byproduct of scale or urban growth. We thus emphasize the role of urban sectoral specialization and the labor markets within these sectors in driving the spatial concentration of top earnings.

Similar content being viewed by others

Main

Since about 1980, disproportionate earnings growth for the highest-paid individuals in the most affluent cities has led to a spatial concentration of top earnings in countries of the global north1,2,3,4,5. As top earnings grew disproportionately in large cities, the increasingly heavy tails of their earnings distributions reinforced the superlinear relationship between the scale of cities and both earnings levels and inequality6,7. This period of rising spatial concentration of top earnings in large cities contrasts sharply with the post-war period, when broadly shared earnings growth led to a convergence of earnings levels across regions and a decline in both national and urban inequality8,9,10. The implications of this trend are profound. Mobility scholars provide compelling evidence that the concentration of top earnings undermines equality of opportunity, as the economic conditions of communities shape the life chances of children11,12. Political scientists worry that the spatial concentration of advantages fosters political fragmentation and disenfranchisement, fueling the rise of reactionary populist movements13,14.

Existing research explains the increasing concentration of top earnings in large cities as a spatial articulation of national or global trends. One explanation emphasizes national trends: because earnings groups are unevenly distributed across locations, rising national top earnings lead to spatially uneven growth in local top earnings1,4. However, this statistical explanation does not address the social processes that cause top earnings growth in large cities. One process that could cause rising local top earnings is skill-biased technical change. Research predicts that the growing skill bias of agglomeration economies raises the urban wage premium for highly skilled workers, while lowering it for moderately and less skilled workers3,15,16,17. An increase in skill-based sorting could provide an additional explanation: highly educated individuals and productive firms increasingly cluster in amenity-rich ‘superstar cities’, where rising housing costs displace low-skilled workers18,19,20,21,22,23. However, it is unclear how these explanations account for the differences in the increase of top earnings among similarly sized cities with similar amenities, housing market constraints and skill composition. Why, for instance, did New York and Los Angeles, Paris and Lyon, Stockholm and Gothenburg, or Frankfurt and Hamburg experience such divergent trajectories of top earnings growth despite comparable endowments?

A second type of explanation for the increasing spatial concentration of top earnings emphasizes the sectoral specialization of ‘global cities’ that emerges in the most recent cycle of capitalist globalization. Saskia Sassen24,25 argues that global cities specialize as centers of advanced producer services—such as consulting, legal services and finance—that perform the key coordinating functions of global markets. This process attracts high-wage professionals while expanding low-wage service jobs, deepening earnings polarization within these cities and widening the gap with deindustrializing cities and rural areas. Recent empirical research, however, shows that the occupational structure of global cities such as New York, London and Tokyo is becoming increasingly professionalized, with high-skilled roles gaining in importance, rather than increasing polarization between high- and low-wage occupations26,27. Moreover, if globalization is driving the concentration of top earnings in global cities, it remains unclear why similar patterns are emerging in cities that are less central to the global economy28.

In this Article, we propose a new explanation for the resurgence of the spatial concentration of top earnings in countries of the global north. Bridging the literature on financialization and spatial inequality, we show that dramatic earnings growth in finance has concentrated top earnings in the few cities where financial market jobs are clustered. While earnings growth in finance is widely recognized as a driver of national earnings concentration29,30,31,32, we show that it is also an important mechanism explaining the confluence of rising national top earnings and spatially concentrated local top earnings growth. Extending insights from research showing that sectoral specialization drives divergence in average earnings levels among similarly sized cities33,34,35, we illustrate that concentrated earnings growth in finance helps to explain why large cities differ in their evolution of top earnings concentration. We suggest that concentrated earnings growth in finance can be explained by financial firms sharing rents with employees who oversee the financial market activities that surged in the 1990s and 2000s and who are clustered in cities hosting their main national stock exchange. Complementing existing frameworks of spatial inequality focused on skill-based sorting and the skill bias of agglomeration economies, our results thus point to the importance of cities’ sectoral specialization and the labor market dynamics within these sectors in explaining the resurgence of the spatial concentration of top earnings.

We present evidence for our explanation using a unique collection of administrative linked employer–employee earnings records with over one billion employer–employee year observations. Spanning ten countries (Canada, Denmark, Sweden, Norway, France, Germany, the Netherlands, Spain, the USA and Japan), these data cover the entire labor force in most countries and representative samples of 4–8% in Germany, Spain and Japan (see Supplementary Section 1). To assess the contribution of earnings growth in finance to the spatial concentration of top earnings, we decompose the difference in the evolution of top earnings concentration between two types of cities within each country: financial cities, which are national centers of financial markets and thus earnings growth in finance, and comparison cities, which are the closest in terms of population, employment and gross domestic product (GDP) share but lack a significant financial market presence (see Supplementary Section 2). Finally, our results show that the contribution of finance to the spatial concentration of top earnings is not limited to major global cities such as New York, London and Tokyo, but also applies to cities that are less central to the global economy such as Frankfurt, Toronto, Stockholm, Oslo, Amsterdam, Madrid and Copenhagen.

Financial cities and the rise in the spatial concentration of top earnings

In this section, we document trends in the spatial concentration of top earnings in financial cities. Building on research that has documented the increasing dispersion of top incomes between states, commuting zones and counties, as well as rapidly rising income inequality within large cities1,2,3,4,5,16, we focus on three dimensions. First, we examine how much of the increase in national earnings concentration has occurred in financial cities; second, we measure how much earnings of financial cities have become overrepresented in national top earnings shares; and third, we document increases in local earnings concentration within financial cities. The central question is not whether top earnings concentration has increased along these dimensions, but by how much compared with comparison cities. Because divergence in the concentration of top earnings between financial and comparison cities reflects dynamics in the financial sector as well as other sectors, the ‘Financial sector jobs and the rise in the spatial concentration of top earnings in financial cities’ section assesses the extent to which financial sector jobs account for these trends.

We begin by examining how much of the increase in the earnings share of the national top 1% is accounted for by the earnings of individuals working in financial cities. The period over which national top earnings shares increased in each country is identified by taking the year of the national minimum of the top 1% earnings share as the first year and the year of the maximum as the last year. During these periods, as shown in Table 1, national top 1% earnings shares increased significantly in all countries, with increases ranging from 0.05 percentage points per year in Denmark to 0.46 percentage points per year in the USA. We calculate the contribution of financial cities by dividing the change in the earnings share of individuals in the financial city who are in the national top 1% by the change in the national top 1% earnings share (see equations (1)–(3)).

The column ‘Contribution to top 1% growth’ shows that individuals working in financial cities account for major shares of the increases in national earnings concentration. On average, national top 1% earners working in financial cities account for 65% of the increase in national top 1% earnings shares. While the positive contribution is unsurprising, the magnitude is remarkable: in some countries, financial cities account for more than 100% of the increase in top earnings shares, as seen in Paris or Stockholm, implying a negative contribution from individuals in the rest of the country.

To adjust for differences in city size when comparing the contributions of financial and comparison cities, we rescale the contributions of each city by its employment share and estimate its contribution as if it represented 10% of the employed population at the beginning of the period. We use a 10% rescaling basis to ease comparison and because it roughly corresponds to the average employment share of all selected cities at the beginning of the period. Even with this rescaling, individuals in financial cities contribute significantly to the growth of top 1% earnings shares, with their contributions consistently exceeding the scaling factor (that is, 10%). On average, individuals in financial cities contribute six times more to the growth of top earnings shares than individuals in comparison cities. While these decomposition results also reflect changes in city size and the rescaling does not capture the superlinear relationship between population size and earnings levels, the results show that financial cities account for a much larger share of the rise in national earnings concentration than their population size would suggest.

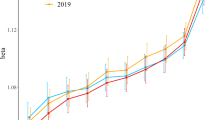

To measure the overrepresentation of financial cities’ earnings in national top earnings shares compared with comparison cities, as well as compare local earnings concentration of cities, Fig. 1 presents measures that we call the ‘overrepresentation of financial cities’ earnings’ in national (Fig. 1a) and local (Fig. 1b) top earnings shares.

a, The overrepresentation of financial city earnings relative to comparison city earnings in the national top 1% of earnings share. It is the odds ratio of two local earnings shares: the share of the financial city’s earnings above the national top 1% threshold, and the share of the comparison city’s earnings above the same threshold (see equation (5)). In 1990, earnings in financial cities were on average 1.7 times more likely to be in the national top 1% than those in comparison cities. In 2017, this average odds ratio increases to 2.4 at a growth rate of 1.3% per year. b, The overrepresentation of financial city earnings relative to comparison city earnings in local top 5% earnings shares. It is computed similarly to the previous one, replacing the national top 1% threshold with city-specific local top 5% thresholds. It shows that the overrepresentation of the top 5% in local earnings in financial cities over comparison cities increased from 1.10 in 1990 to 1.3 in 2017, a growth rate of 0.5% per year. The adjusted means were computed according to Supplementary Section 3.

Figure 1a measures the overrepresentation of financial cities’ earnings in national top 1% earnings shares (see equation (5)). This measure is the odds ratio of two proportions: the share of total local earnings in the financial city earned by workers in the national top 1% earnings bracket, relative to the corresponding share in the comparison city. Supplementary Fig. 1 shows time trends of the two underlying local earnings shares. In all countries, national top earnings are more concentrated in financial cities than in comparison cities, with odds ratios ranging from 1 to 3.6. In 1990, the earnings of financial cities were on average 1.7 times overrepresented in the national top 1% compared with comparison cities. By 2017, this overrepresentation had increased significantly to an average odds ratio of 2.4, representing an annual growth rate of about 1.3%. We observe a significant upward trend in all countries except Canada (Supplementary Table 1). Here too, the magnitude of the increase is substantial, demonstrating a substantial rise in the overrepresentation of financial cities’ earnings, accounting for differences in total earnings between the two types of cities.

Figure 1b measures the overrepresentation of financial cities’ earnings in local top 5% earnings shares. Analogous to the national-level measure, we compute an odds ratio comparing two local earnings shares: the share of total local earnings earned by individuals in the local top 5% in the financial city relative to the corresponding share in the comparison city (see equation (5); see Supplementary Fig. 2 for time trends of local top 5% earnings shares). This measure compares local earnings concentration between the financial and comparison cities, accounting for differences in total local earnings. It shows that, in almost all countries, local earnings concentration is significantly higher in financial cities. Only in Japan and Germany are the levels of local earnings concentration similar in the two cities, with odds ratios ranging from 0.96 to 1.04. Moreover, the magnitude of the divergence in local earnings concentration between financial and comparison cities increases substantially over time, with linear trends positive for nine countries and statistically significant for half (Supplementary Table 1).

These findings are broadly consistent with previous research showing that larger cities tend to have higher levels and faster increases in local inequality36. However, we provide new evidence by measuring local earnings concentration rather than local inequality. More importantly, we show that the growing divergence in local earnings concentration between financial and comparison cities is not simply a reflection of changes in their relative size; Supplementary Fig. 3 shows that the employment shares of cities have remained remarkably stable over this period.

In summary, financial cities account for large increases in national earnings concentration, their earnings are increasingly overrepresented in national top earnings shares and they exhibit much faster growth in local earnings concentration relative to the city in the same country that is closest in terms of population, employment and GDP share, net of differences in total earnings.

Financial sector jobs and the rise in the spatial concentration of top earnings in financial cities

To what extent does finance account for the growing spatial concentration of top earnings? We first conduct a decomposition of the rise in the national top 1% and local top 5% earnings shares to measure the contribution of financial sector jobs to the concentration of top earnings in financial and comparison cities (equations (8) and (9)).

Table 2 shows that, on average, financial sector jobs in financial cities account for 26% of the increase in national top 1% earnings shares, with contributions ranging from 2% in Frankfurt to 47% in Madrid. The magnitude is substantial—had employment and earnings levels in finance in financial cities stayed the same (assuming no second-order effects), the increase in national top 1% earnings shares would have been about one-third smaller on average. In comparison cities, the financial sector contributes much less to the growth of the national top 1% earnings share than in financial cities. Their contribution is only 0.5% on average. After rescaling the two cities to a 10% employment share at the beginning of the period, the contrast between the contribution of financial sector jobs in the financial cities (18%) and in the comparison cities (1%) remains very large.

Financial sector jobs in financial cities also account for a staggering 50% of the increase in local top 5% earnings shares on average, with the absolute contribution of financial sector jobs ranging from 4% in Tokyo to 78% in Amsterdam. In the comparison cities, financial sector jobs account for a much smaller share of the increase in local top 5% earnings shares, 14% on average. Like in Table 1, the measures in Table 2 are limited to the period of top earnings growth and are sensitive to population size change.

We show in Fig. 2 indicators of the overrepresentation of earnings from financial sector jobs from financial cities in national and local top earnings shares (equation (10)). Figure 2a shows that the earnings of financial sector jobs from financial cities are significantly overrepresented in the national top 1% compared with those from comparison cities, with odds ratios ranging from 1 to 20. This overrepresentation is increasing rapidly everywhere, with an average annual rate of increase of 2.4% per year, which is higher than the 1.3% observed in Fig. 1a, indicating the large contribution of financial sector jobs to the growing gap between the two types of cities. The picture is similar when we look at local earnings concentration (Fig. 2b). The earnings of financial sector jobs are significantly overrepresented in the local top 5% of financial cities compared with comparison cities, with odds ratios ranging from 1 to 10, and the average annual rate of increase is 1.6% per year, again a significantly higher rate than in Fig. 1b (+0.5%).

Shown is the overrepresentation of financial sector earnings from financial city over those from comparison cities in national top 1% and local top 5% earnings. a, The odds ratio of two local earnings shares: the earnings share of finance sector employees above the national top 1% threshold in financial cities and that in comparison cities. b, A similar ratio using the local top 5% threshold instead. The adjusted means were computed according to Supplementary Section 3.

Finally, to estimate the contribution of financial sector jobs to the rising overrepresentation of financial cities earnings in top earnings shares, we calculate the difference between two versions of our measures of the overrepresentation of financial cities’ earnings in national and local top earnings shares: one version includes earnings from financial sector jobs, while the other excludes them (equations (11) and (12)). In Supplementary Fig. 4a,b, and in the third and fourth columns of Supplementary Table 1, we replot the overrepresentation of financial cities’ earnings as in Fig. 1 excluding financial sector jobs from the sample. These graphs show that, when excluding financial sector jobs, the increase in the overrepresentation of financial cities’ earnings in national top 1% earnings shares, as well as local earnings concentration relative to the comparison cities, is significantly reduced. Table 3 summarizes our main finding: financial sector earnings account for 28% of the increase in overrepresentation of earnings from financial cities in the national top 1% and local top 5%.

In Supplementary Table 2, we present robustness checks to test that the relationship between earnings shares in local finance and the overrepresentation of financial cities’ earnings in national top earnings shares is not confounded by national-level population size, productivity, exposure to global trade, or differences in employment shares between cities. We estimate country-level panel regressions of financial cities’ overrepresentation in national top earnings shares on the difference in local finance earnings shares between the two cities. We control for national population size, GDP per capita, foreign direct investment (FDI) outflows and employment share differences between cities (equation (13). We present results with country and year fixed effects, and with country fixed effects and a linear year trend. These analyses show that the association between the difference in local finance earnings shares in the two cities and the overrepresentation of financial cities’ earnings in the national top earnings shares remains after controlling for these potential confounders.

How does finance concentrate top earnings in financial cities?

The contribution of finance to the spatial concentration of top earnings in financial cities may be explained by two factors: rising employment or rising earnings in the financial sector in these cities. However, stagnant or declining financial sector employment in financial and comparison cities during a period of rapidly rising earnings shares for finance in financial cities rules out employment growth as the cause (Supplementary Table 3).

Previous research shows that finance contributes to increases in national earnings concentration because of rising occupational premiums in financial markets, such as those for traders and investment bankers30,32,37,38. These premiums are largely driven by the rent-sharing of financial firms with employees overseeing the financial market activities that surged dramatically in the 1990s and 2000s, rather than by talent or returns on talent31,37,38,39. A key difference between financial and comparison cities is that, despite both having financial sectors that provide local banking and credit services, financial market firms are highly concentrated in financial cities (Supplementary Table 4). While our occupational data generally do not distinguish between financial market functions and other financial sector occupations, France provides an exception. In France, financial market occupations are concentrated in Paris and nearly absent in Lyon (Supplementary Fig. 5). For instance, 85% of financial market managers are employed in Paris, compared with only 1.5% in Lyon—a much starker contrast than that seen among commercial banking managers (40% versus 4.5%) or all financial sector jobs (22% versus 3.3%). Therefore, earnings of financial sector jobs in financial cities, but not in comparison cities, are shaped by the rent-sharing of increased financial market activity (Supplementary Fig. 5), which also explains how finance contributes to the increase in national earnings concentration. Although data limitations prevent us from formally evaluating the importance of agglomeration effects or skill-based sorting into finance in financial cities, these insights, together with the economically very large contribution of finance to national and local top earnings growth, suggest that earnings growth in finance is unlikely to be solely a reflection of these factors.

In Supplementary Table 5, we present additional robustness checks for the relationship between financial market activity and the overrepresentation of financial cities’ earnings in national top earnings shares, similar to the analysis in Supplementary Table 2. We use the same models with the overrepresentation of financial cities’ earnings in national top earnings shares as the dependent variable, but with the indicator volume of financial market activity relative to GDP as the independent variable. These models show that the relationship between financial market activity and the overrepresentation of financial cities’ earnings in national top earnings shares remains after controlling for a number of national-level confounders.

Discussion

Using administrative, linked employer–employee data from ten countries, we demonstrate that rapid earnings growth in the financial sector concentrates top earnings in a few large cities. Complementing existing frameworks of spatial inequality that focus on skill-based sorting and the skill bias of agglomeration economies, our findings point to the importance of sectoral specialization and the labor market dynamics in those sectors in explaining the resurgence of the spatial concentration of top earnings, and especially in explaining differences among similarly sized metropolitan areas.

Our findings are consistent with key predictions from the literature on spatial inequality and global cities but diverge in important ways. First, consistent with recent studies of the spatial concentration of top incomes, we find that national top earnings growth exacerbates the spatial concentration of top earnings when earnings groups are unevenly distributed across space1,3,4. However, by showing that earnings growth in finance is a key mechanism relating national top earnings growth to uneven local top earnings growth, we highlight the importance of studying the processes underlying this relationship. Although earnings growth in finance is one such mechanism, it is not the only one linking national top earnings growth to uneven local top earnings growth, suggesting that a similar framework could be applied to other spatially concentrated industries33,40. For the time period under study here, a simple comparison of the finance sector with the high-tech sector (Supplementary Figs. 9–11) suggests that finance plays a more distinct and consistent role in the spatial concentration of top earnings, while the influence of the high-tech sector is smaller and more context dependent.

Second, consistent with the global cities literature, we emphasize that capital concentration and the economic specialization of cities in advanced producer services are important to understand the spatial concentration of top earnings and differences between cities of similar size. However, we draw attention to the distinctive role of a particular type of advanced producer services firm and shift the focus from globalization to financialization, as the process we document also occurs in countries where the leading financial city would not qualify as a major global city, such as Oslo, Stockholm, Copenhagen or Madrid.

Our results highlight three key forms of cross-country variation in the spatial concentration of top earnings and the role of finance. First, in countries such as Spain, Sweden and Denmark, financial cities and financial sector jobs contribute substantially to modest increases in the spatial concentration of top earnings, whereas in Germany, the USA and Canada, financial cities play a smaller role in much larger increases in national top earnings concentration. Second, levels of the spatial concentration of top earnings are particularly high in Stockholm, Oslo and Madrid, due to the outsized role these cities play in highly centralized national economies. By contrast, Germany, Canada and the USA have much lower levels of spatial concentration of top earnings in financial cities, reflecting more decentralized economies shaped by histories of federalism. Third, in North America, finance contributed significantly to rising earnings concentration in the late 1980s and 1990s, but as wage-setting practices from finance spread to other sectors, the distinctive financial wage premium attenuated. Meanwhile, in Scandinavian countries, finance remained a niche sector with exceptionally high wages and limited spillovers to other sectors. This variation illustrates how national institutional arrangements shape cross-country differences in the dynamics of top earnings concentration, which merit further study.

Finally, although our analysis relies on high-quality administrative earnings records, there are some limitations to the data (see Supplementary Section 7). First, our analysis does not directly account for differences in the cost of living across locations. However, prior research has identified mixed effects of inflation heterogeneity on regional inequality in real earnings. Moretti41 finds that college graduates in expensive cities experienced slower real earnings growth than non-urban workers, while Diamond18 finds that improved amenities in high-skill cities offset cost-of-living increases. Most importantly for our analysis of top earnings concentration, Diamond and Moretti42 find that regional cost-of-living differences primarily affect low-income households and that top earners have similar costs of living across places. In addition, because our research design focuses on comparing cities within countries that often have similar costs of living, we minimize the influence of cost-of-living differences on our results. Second, we measure earnings as annual pre-tax earnings, which may introduce bias in the estimation of national and local disposable earnings concentration due to progressive earnings taxation1 and to cross-regional variation in the taxation of high earnings. Consequently, post-tax measures could moderate findings of the contribution of earnings growth in finance on the spatial concentration of top earnings.

Methods

Data

We use administrative linked employer–employee data for nine countries: Canada, Denmark, Sweden, Norway, France, Germany, Spain, the Netherlands and Japan (see Supplementary Section 1) and published estimates based on Internal Revenue Service (IRS) data for the USA. With these data, we base our analysis on nearly one billion employee–year observations and up to 210 million employee observations per year.

Most countries—Canada, Denmark, Norway, Sweden, the Netherlands and France—provide complete information on the labor force. This results in highly reliable earnings estimates, even for small groups that are difficult to study using common surveys. In the remaining countries—Germany, Spain and Japan—our administrative data cover sample sizes between 4% and 8% of the labor force. With these data, we obtain reliable estimates of national and local top earnings shares, and we can decompose local top earnings shares by sector within cities. However, estimates of top earnings shares in smaller metropolitan areas are less precise in countries where we use samples compared with countries with comprehensive labor force data. This is especially so in Germany, where in addition to a smaller sample, earnings are top-coded at the top decile. We follow common practice and impute top earnings for Germany (Supplementary Table 1).

For the USA, we combine county-level IRS tables and Sommeiller and Price’s estimates of state-level income concentration derived from IRS income tax returns. To compute local income shares, we first multiply the state-level income brackets and the average income per bracket by the ratio of average county income to average state income (see Supplementary Section 5). We then apply this distribution to the county and estimate the income share above the national and local top income thresholds according to Pareto law. Finally, we aggregate county estimates to obtain the income distribution of the metropolitan areas.

Unlike national series on employment or wages, local top earnings series show significant changes from one year to the next. These changes are largely due to the volatility of the phenomenon being studied, namely, high earnings at the local level that are largely fueled by the finance sector. However, sample size, changes in data collection and other data specifics also contribute to series volatility. We discuss the sources of volatility in detail in Supplementary Section 7.

Analytic strategy

We proceed in three steps to quantify the contribution of earnings growth in finance to the spatial concentration of top earnings. First, we estimate the spatial concentration of top earnings in each city along three dimensions: the city’s contribution to the national increase in top earnings concentration, the overrepresentation of a city’s earnings in national top earnings shares, and the city’s local level of earnings concentration. Second, we decompose the within-city change in these measures into the portion explained by financial sector jobs and the portion explained by other sectors within each city. Third, we decompose the difference in the evolution of top earnings concentration between financial cities—those hosting the national stock exchange and most financial market firms—to comparison cities, the closest domestic cities in terms of population, employment and GDP share.

Identifying financial cities is straightforward because secondary financial cities have largely disappeared as finance has become more centralized in the post-war period. In most of our countries, financial cities are major centers of global finance, including New York, Tokyo, Paris, Frankfurt and Toronto. Stockholm serves as a financial center for Sweden, Norway and Denmark, while Copenhagen, Oslo and Madrid are national financial hubs. To identify the comparison cities, we use Organisation for Economic Co-operation and Development regional statistics data to find the city closest to the financial city in terms of population, employment and GDP share (see Supplementary Section 2). In practice, we compare the two largest cities in each country in terms of employment and GDP share, with the financial city being the largest. The only exception is Germany, where we compare Frankfurt (ranked fourth in terms of employment and GDP share) with Hamburg (ranked third).

Under the assumption that the only difference between financial and comparison cities is earnings growth in finance, the comparison of top earnings concentration would identify the causal effect of earnings growth in finance on the spatial concentration of top earnings. However, this assumption is unlikely to hold, as differences in top earnings concentration may also reflect city-specific factors unrelated to finance, and the effects of finance-sector earnings growth in one city may spill over to others, unfold over time or vary depending on how that growth takes shape43.

To quantify the impact of earnings growth in finance, we use counterfactual decompositions to directly measure its contribution to the change in the difference in top earnings concentration between the two cities. We define our main theoretical estimand as the amount by which the increase in the overrepresentation of financial cities’ earnings in top earnings shares would be lower in a world where employment and earnings in the financial sector had not changed. We estimate this as the difference between the observed evolution of the overrepresentation of financial cities’ earnings in top earnings shares and the estimated evolution after mechanically setting earnings in finance to zero in both cities (equations (11) and (12)). Because the first evolution (1) captures the combined effects of financial and nonfinancial drivers of top earnings concentration, whereas the second evolution (2) reflects only nonfinancial drivers, the difference between the two quantifies the contribution of finance to top earnings concentration.

Under the assumptions that financial and nonfinancial drivers of top earnings are independent, and that the absence of earnings growth in finance is a well-defined intervention yielding consistent potential outcomes, this estimate can be interpreted as the causal effect of earnings growth in finance on the spatial concentration of top earnings44. These assumptions are probably violated because evolutions in financial cities differ from those in comparison cities in many ways; earnings growth in finance may stimulate or suppress earnings growth in other sectors or cities; and a world without earnings growth in finance would differ in significant other aspects. Our estimate fully characterizes population processes, capturing the causal effect of earnings growth in finance and how finance mediates as well as covaries with other processes driving top earnings concentration.

However, two key factors give us confidence that our estimates, corroborated with other methods in Supplementary Tables 2 and 5, approximate the causal effect of earnings growth in finance on the spatial concentration of top earnings. First, our decomposition identifies economically large contributions of finance within an accounting framework that are consistent with theoretically grounded expectations about how financial sector earnings growth redistributes earnings at the top. Second, prior research shows that earnings growth in finance is driven by factors such as deregulation and increased rent-sharing in financial firms, which are plausibly exogenous to local top earnings growth, agglomeration effects and skill-based sorting30,31,37,38,39. We encourage future work to leverage exogenous variation in earnings growth in finance to identify causal effects.

Measures

National earnings concentration

To estimate the absolute contribution of workers in a city to the increase in national top earnings shares reported in Table 1, we first identify the national top earnings share as

where wi is the earnings of individual i and Tn is the threshold of the national earnings distribution (that is, P99).

We define the national earnings share of workers who are in the national earnings bracket above the national earnings threshold Tn and who work in city k (k being either financial city or comparison city) as

The absolute contribution of individuals in city k to the growth of the share of total national earnings earned by individuals above the national earnings threshold Tn can be rewritten as

To estimate the overrepresentation of financial cities’ earnings in national top earnings shares relative to comparison cities reported in Fig. 1a, we first calculate the proportion L of local earnings in city k that go to workers from that city who earn more than the national earnings threshold Tn (Supplementary Fig. 1):

We then calculate the odds ratio of the earnings shares for the two areas Onat as follows:

where f represents the financial city and c the comparison city.

The local earnings odds (\({L}_{i,{T}_{n}}/1-{L}_{i,{T}_{n}}\)) capture the likelihood that a local unit of earnings in city i accrues to a national top 1% earner rather than to the bottom 99%, and the odds ratio compares this likelihood across the two cities. We use the 99th percentile threshold to compute our main measure of the overrepresentation of financial cities’ earnings in national top earnings shares. We nevertheless tried other thresholds such as the national P95 and P90 (Supplementary Fig. 7). The fact that earnings inequality has increased primarily due to growing dispersion at the top of the earnings distribution justifies prioritizing top earnings concentration over other inequality indicators (see Supplementary Section 6).

Local earnings concentration

To measure the overrepresentation of financial cities’ earnings in local top earnings shares reported in Fig. 1b, we first calculate the (local) top earnings share in city k above local threshold Tk in each of the two cities (Supplementary Fig. 2):

Similarly to equation (5), we then calculate the odds ratio between these two local top earnings shares:

We use the 95th percentile as the main threshold because the local 95th percentile is close to the national 99th percentile in most countries. Moreover, for countries where we use samples of the working population—Germany, Spain and Japan—estimates of the local earnings share are more robust than they would be under a higher threshold. We also report results for other thresholds such as local P90 and P99 in Supplementary Fig. 8.

Financial sector jobs’ contribution

Following the logic of equations (1) to (3), we estimate the absolute contributions of financial sector jobs b from city k (for example, financial cities or comparison cities) to the increase in national or local earnings above threshold T reported in Table 2 with the two following equations:

for the contribution to national earnings concentration and

for the contribution to local earnings concentration.

To estimate the overrepresentation of financial sector jobs earnings in the local top earnings shares reported in Fig. 2, we modify equations (5) and (7), and use the share of earnings of financial sector jobs b in the city (either financial city f or comparison city c) above threshold T (which could be either national top 1% threshold or local top 5% threshold).

The estimate that corresponds to our main theoretical estimand is the difference between the actual evolution of the overrepresentation of financial cities’ earnings in national earnings shares (equation (5)) and local top earning shares (equation (7)) and the evolution of the overrepresentation in a counterfactual in which neither city has financial sector employment. To measure it, we estimate the yearly trends as follows:

where O denotes the overrepresentation of financial cities’ earnings in top earnings shares; j indicates whether the reference is national (j = nat) or local (j = loc) top earnings shares; s distinguishes between the actual world with finance earnings included (s = all) and the counterfactual world with finance earnings excluded (s = −fi); c captures country fixed effects; and u denotes the residuals.

With these estimated trends, we calculate the contribution of finance to the spatial concentration of top earnings as

Regressions

As a robustness check for the association between earnings growth in finance and the overrepresentation of financial cities’ earnings in top earnings shares, we use country-level ordinary least squares (OLS) regressions (Supplementary Tables 2 and 5). We include two main dependent variables: first, the overrepresentation of financial cities’ earnings in national top earnings shares, and second, their overrepresentation in local top earnings shares (equations (5) and (7)). Although the two indicators appear similar, they may evolve differently over the same period. For instance, the earnings share of individuals in the national top 1% working in financial cities might increase due to an aggregate rise in local earnings, while local earnings concentration might simultaneously decrease when earnings growth at the bottom of the local distribution is faster than at the top.

In our base model, we estimate a simple panel model with country c and year t fixed effects and lagged independent variables (by one year). We use Driscoll–Kraay standard errors to account for autocorrelations of residuals. To allow comparison of coefficients, we use log constant dollars and country demeaned and standardized variables. We control for population size and GDP per capita, as well as scale effects, by using the difference in the national employment share of the financial city and the comparison city. In Supplementary Table 5, we use FDI outflow (stock) to GDP published by the United Nations Conference on Trade and Development (see https://unctadstat.unctad.org/wds/TableViewer/tableView.aspx, accessed 4 July 2022) to control a country’s involvement in global coordination functions.

We estimate equation (13) using two independent variables that represent the role of finance. Supplementary Table 2 uses the difference between the local earnings share of financial sector jobs in financial cities and in comparison cities. Assuming that the presence of financial markets in financial cities and their absence in comparison cities is the main driver of differences in local finance earnings shares, this measure captures the disparities in local financial market activity. However, our data do not allow us to measure the variable for the USA. Supplementry Table 5 uses the ratio of stock exchange volume to GDP (GFDD.DM.02) from the World Bank’s Global Financial Development Database as a measure of financial market activity commonly used in analyses of the effect of financialization on earnings inequality10,12,31,39. This measure does not capture the spatial distribution of financial market activity, but if financial market activity is heavily concentrated in financial cities, it captures the disparities in local financial market activity between financial and comparison cities.

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

This Article uses restricted-access data from nine countries. As described in the Supplementary Information, the data can be accessed by receiving permissions from the relevant data owners, including Statistics Canada; Statistics Denmark; the French Comité du Secret Statistique; the German Institute for Employment Research; the Japanese Ministry of Health, Labour and Welfare; the Central Bureau of Statistics of the Netherlands; Statistics Norway; the Ministry of Labor, Migration and Social Security of Spain; and Statistics Sweden. For the USA, the IRS county dataset can be downloaded at https://www.irs.gov/statistics/soi-tax-stats-county-data. The Sommeiller and Price dataset can be downloaded at http://go.epi.org/unequalstates2018data. The measure ‘stock market total value traded to GDP’ (series GFDD.DM.02) from the World Bank Global Financial Development Database (GFDD) is available at https://www.worldbank.org/en/publication/gfdr/data/global-financial-development-database). Data on the ratio of a country’s stock of FDI to its GDP is published by the United Nations Conference on Trade and Development (https://unctadstat.unctad.org/wds/TableViewer/tableView.aspx, accessed 4 July 2022). Aggregated data used in this study are available at https://doi.org/10.17605/OSF.IO/9K2CP.

Code availability

The code that supports the findings of this study is available at https://doi.org/10.17605/OSF.IO/9K2CP.

References

Gaubert, C., Kline, P. M., Vergara, D. & Yagan, D. Trends in U.S. spatial inequality: concentrating affluence and a democratization of poverty. AEA Pap. Proc. 111, 520–525 (2021).

Bauluz, L. et al. Spatial Wage Inequality in North America and Western Europe: Changes between and within Local Labour Markets 1975–2019. No. 1941 (Centre for Economic Performance, 2023).

Moretti, E. The New Geography of Jobs (Houghton Mifflin Harcourt, 2012).

Manduca, R. A. The contribution of national income inequality to regional economic divergence. Soc. Forces 98, 622–648 (2019).

Kemeny, T. & Storper, M. The fall and rise of interregional inequality: explaining shifts from convergence to divergence. Scienze Regionali https://doi.org/10.14650/97084 (2020).

Arvidsson, M., Lovsjö, N. & Keuschnigg, M. Urban scaling laws arise from within-city inequalities. Nat. Hum. Behav. 7, 365–374 (2023).

Heinrich Mora, E. et al. Scaling of urban income inequality in the USA. J. R. Soc. Interface https://doi.org/10.1098/rsif.2021.0223 (2021).

Butts, K., Jaworski, T. & Kitchens, C. Urban wage premium in historical perspective. Natl Bur. Econ. Res. https://doi.org/10.3386/w31387 (2023).

Alvaredo, F., Atkinson, A. B., Piketty, T. & Saez, E. The top 1 percent in international and historical perspective. J. Econ. Perspect. 27, 3–20 (2013).

Sommeiller, E. & Price, M. The New Gilded Age: Income Inequality in the US by State, Metropolitan Area, and County. (Economic Policy Institute, 2018).

Chetty, R., Hendren, N., Kline, P. & Saez, E. Where is the land of opportunity? The geography of intergenerational mobility in the United States. Q. J. Econ. 129, 1553–1623 (2014).

Sharkey, P. & Faber, J. W. Where, when, why, and for whom do residential contexts matter? Moving away from the dichotomous understanding of neighborhood effects. Annu. Rev. Sociol. 40, 559–579 (2014).

Beramendi, P. The Political Geography of Inequality: Regions and Redistribution (Cambridge Univ. Press, 2012).

Piketty, T. & Cagé, J. Une Histoire Du Conflit Politique: Elections et Inégalités Sociales En France, 1789–2022 (Seuil, 2023).

Yankow, J. J. Why do cities pay more? An empirical examination of some competing theories of the urban wage premium. J. Urban Econ. 60, 139–161 (2006).

Baum-Snow, N., Freedman, M. & Pavan, R. Why has urban inequality increased?. Am. Econ. J. Appl. Econ. 10, 1–42 (2018).

Autor, D. H. Work of the past, work of the future. AEA Pap. Proc. 109, 1–32 (2019).

Diamond, R. The determinants and welfare implications of US workers’ diverging location choices by skill: 1980–2000. Am. Econ. Rev. 106, 479–524 (2016).

Gyourko, J., Mayer, C. & Sinai, T. Superstar cities. Am. Econ. J. Econ. Polic. 5, 167–199 (2013).

Ganong, P. & Shoag, D. Why has regional income convergence in the U.S. declined?. J. Urban Econ. 102, 76–90 (2017).

Le Galès, P. & Pierson, P. ‘Superstar cities’ & the generation of durable inequality. Daedalus 148, 46–72 (2019).

Glaeser, E. Triumph of the City: How Our Greatest Invention Makes Us Richer, Smarter, Greener, Healthier, and Happier (Penguin Books, 2011).

Behrens, K., Duranton, G. & Robert-Nicoud, F. Productive cities: sorting, selection, and agglomeration. J. Polit. Econ. 122, 507–553 (2014).

Sassen, S. The Global City: New York, London, Tokyo (Princeton Univ. Press, 1991).

Sassen, S. Cities in a World Economy (Sage Publications, 2018).

van Ham, M., Uesugi, M., Tammaru, T., Manley, D. & Janssen, H. Changing occupational structures and residential segregation in New York, London and Tokyo. Nat. Hum. Behav. 4, 1124–1134 (2020).

Hamnett, C. The changing social structure of global cities: professionalisation, proletarianisation or polarisation. Urban Stud. 58, 1050–1066 (2021).

Le Galès, P. The rise and fall of the sociology of the global city. Annu. Rev. Sociol. https://doi.org/10.1146/annurev-soc-090523-042533 (2024).

Kus, B. Financialisation and income inequality in OECD nations: 1995–2007. Econ. Soc. Rev. 43, 477–495 (2012).

Philippon, T. & Reshef, A. Wages and human capital in the US finance industry: 1909–2006. Q. J. Econ. 127, 1551–1609 (2012).

Godechot, O. Financialization is marketization! A study of the respective impacts of various dimensions of financialization on the increase in global inequality. Sociol. Sci. 3, 495–519 (2016).

Godechot, O. et al. Ups and downs in finance, ups without downs in inequality. Socio-Econ. Rev. 21, 1601–1627 (2023).

Storper, M., Kemeny, T., Makarem, N. & Osman, T. The Rise and Fall of Urban Economies: Lessons from San Francisco and Los Angeles (Stanford Univ. Press, 2015).

Connor, D. S., Kemeny, T. & Storper, M. Frontier workers and the seedbeds of inequality and prosperity. J. Econ. Geogr. 24, 393–414 (2024).

Iammarino, S., Rodriguez-Pose, A. & Storper, M. Regional inequality in Europe: evidence, theory and policy implications. J. Econ. Geogr. 19, 273–298 (2019).

Baum-Snow, N. & Pavan, R. Understanding the city size wage gap. Rev. Econ. Stud. 79, 88–127 (2012).

Oyer, P. The making of an investment banker: stock market shocks, career choice, and lifetime income. J. Finance 63, 2601–2628 (2008).

Böhm, M. J., Metzger, D. & Strömberg, P. ‘Since you’re so rich, you must be really smart’: talent, rent sharing, and the finance wage premium. Rev. Econ. Stud. 90, 2215–2260 (2023).

Roberts, A. & Kwon, R. Finance, inequality and the varieties of capitalism in post-industrial democracies. Socio-Econ. Rev. 15, 511–538 (2017).

Moretti, E. The effect of high-tech clusters on the productivity of top inventors. Am. Econ. Rev. 111, 3328–3375 (2021).

Moretti, E. Real wage inequality. Am. Econ. J. Appl. Econ. 5, 65–103 (2013).

Diamond, R. & Moretti, E. Where is standard of living the highest? Local prices and the geography of consumption. Working Paper No. 29533 NBER https://doi.org/10.3386/w29533 (2021).

Imbens, G. W. & Rubin, D. B. Causal Inference in Statistics, Social, and Biomedical Sciences (Cambridge Univ. Press, 2015).

Hernán, M. A. & Robins, J. M. Causal Inference: What If (Chapman & Hall/CRC, 2020).

Acknowledgements

We thank A. Carpentier, L. Carroué, R. Casalis, J. Fournier and N. Woloszko for their excellent research assistance. We are also grateful to F. Accominotti, A. Baker, J. Beckert, P.-P. Combes, B. Cousin, A. Guironnet, S. Ginalski, T. van Gunten, M. Hyman, S. Kohl, P. Le Galès, A. Leaver, N. Mas, S. Moatti, S. Paugam, M. Piganiol, Y. Tadjeddine and T. Vitale for their insightful comments on earlier presentations of this research. In addition, we thank L. Chancel, A. Dvir-Djerassi, C. Aeppli, I. Feld, U. Lojkine, R. Manduca, T. Piketty and S. Killewald for their thoughtful feedback. The research leading to the results presented in this Article has received funding from the Agence Nationale de la Recherche ANR-17-CE41-0009-01 (O.G. and M.Sa.); Maxpo, Sciences Po (O.G. and N.N.), Sciences Po, SAB 2023 (O.G. and N.N.) and AxPo, Sciences Po (O.G. and N.N.). This research was also supported by grants from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement no. 851149, A.S.H.); Národní plán obnovy (NPO) Systemic Risk Institute LX22NPO5101 (A.K.); Carlsberg Foundation, grant CF19-0175 (L.F.H.); Independent Research Fund Denmark, grant 5052-00143b (L.F.H.); the Swedish Research Council for Health, Working Life and Welfare – Forte, grant 2024-01411 and grant 2025-00775 (M.T.): National Science Foundation, award 0525831 (A.P. and D.T.-D.); Research Council of Norway, grant 287016 (A.S.H.); the Spanish Ministry of Science and Innovation, grant PID2020-118807RB-I00/AEI/10.13039/501100011033 and the Social Trends Institute (M.M.E.). The findings and conclusions contained within this study are those of the authors and do not necessarily reflect positions or policies of the funders. We followed the relevant guidance and country-specific regulations to ensure the confidentiality and privacy of the administrative records used to create the dataset.

Funding

Open access funding provided by Stockholm University

Author information

Authors and Affiliations

Contributions

N.N. and O.G. were principal investigators on this project. They designed the study, wrote the code, supervised all country analyses, conducted the meta-analysis and wrote the paper. L.F.H., A.S.H., F.H., N.K., Z.L., S.M.M., H.S., M.T., P.A., D.A.H., N.B., I.B., M.M.E., G.H., A.K., A.P., A.P.R., A.R., M. Safi, M. Soener and D.T.D. conceptualized the analyses, provided intellectual input, interpreted the results and edited drafts of the manuscript. O.G. produced estimates from the French administrative records; L.F.H. produced estimates from the Danish administrative records; A.S.H. produced estimates from the Norwegian administrative records; F.H. produced estimates from the Canadian administrative records; N.K. produced estimates from the Japanese administrative records; Z.L. produced estimates from the Dutch administrative records; S.M.M. produced estimates from the German administrative records. M.M.E. and H.S. produced estimates from the Spanish administrative records; M.T. produced estimates from the Swedish administrative record.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests

Peer review

Peer review information

Nature Cities thanks Anthony Roberts, Masaya Uesugi, Jianfeng Wu and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary Information (download PDF )

Supplementary Sections 1–7, References, Figures and Tables.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Neumann, N., Godechot, O., Henriksen, L.F. et al. Rapid earnings growth in finance concentrates top earnings in a few large cities. Nat Cities (2026). https://doi.org/10.1038/s44284-026-00407-1

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1038/s44284-026-00407-1