Abstract

This study investigated the framework of reverse mortgage (RM) programs in Taiwan, with a particular emphasis on the perspectives of both debtors and creditors. Employing the Lee–Carter model, the research estimated mortality rates in Taiwan while utilizing the theoretical framework to analyze various aspects of RM. House prices were assessed using the house price index as a foundational metric for estimating prices, along with lump-sum loanable amounts and RM considerations. Empirical analysis was conducted on debtors’ loans and incomes and financial institutions’ perspectives. The study delved into parameters such as maximum loanable amounts and income replacement ratios for debtors based on demographic factors such as sex, age, and occupation. Furthermore, the structure of RM programs was scrutinized from the viewpoint of financial institutions, considering factors such as rental income, remaining house value, creditor insurance protection, premium expenses, and creditor profitability. A series of simulations were performed to gauge the effects of different variables on the outcomes. The normal distribution of the house price index (HPI), as verified through the Anderson-Darling (AD) test and Kolmogorov–Smirnov (KS) test, bolstered the theoretical findings. This study’s primary contribution lies in its comprehensive exploration of the structure and advantages of RMs from the dual perspectives of debtors and creditors, a departure from insights from previous research predominantly focused on financial institutions. This research can aid debtors and creditors in evaluating RM programs and making informed decisions regarding asset allocation, thereby facilitating the selection of more suitable programs tailored to debtor characteristics.

Similar content being viewed by others

Introduction

The demographic landscape of Taiwan has undergone a significant transformation, officially transitioning into an aging society in 1993. This shift has profound implications, particularly for older adults. By 2008, 10.7% of Taiwan’s population was aged 65 or over, projected to rise steadily. Concurrently, Taiwan grapples with subreplacement fertility rates, leading to a future where a substantial portion of retired older adults may lack familial support.

Whether increased life expectancy equates to an improved quality of life remains a topic of debate among scholars. While medical advancements have reduced disease prevalence, older adults face employment and financial stability challenges. Inadequate pensions might compel retirees to rely on their children or borrow money to sustain their livelihoods. In this context, meticulous financial planning becomes imperative for every retiree, especially considering Taiwan’s high homeownership rate, which leaves many older adults asset-rich yet cash-poor. According to data from the Department of Urban and Housing Development, Council for Economic Planning and Development, the homeownership rate in Taiwan in 2008 was 88.14%. This figure was drastically higher than that of developed countries implementing RM, such as Australia, the United States, Canada, and the United Kingdom. In Taiwan, approximately 39.93% of all older adults over the age of 65 have assets, mainly in the form of savings (82.97%), followed by houses, land, or other real estate (59.45%) (Wang et al., 2011).

In response to these challenges, Taiwan introduced Reverse Mortgage (RM) programs, offering a potential financial lifeline to older adults. Taiwan began trialing RM in 2013 and permitted adults over 65, single, childless, and had real estate to convert their houses to cash. However, the mortgage value must not exceed the real estate value of low-income and middle-low-income households (NT$8.76 million). The pilot program initially had few applications due to its stringent restrictions. However, as the application threshold was lowered and the program was promoted, Taiwanese people gradually began to understand the concept of RM. According to data from the Central Bank, Taiwan had 809 commercial RM cases as of July 2016, and the average age of the applicants was 73.32. Now, six banks offer RM programs to assist older adults in receiving a steady income to cover their everyday expenses and maintain their quality of life after they retire (Table 1).

However, understanding these programs, encompassing complex factors such as applicant age, loan terms, interest rates, and payment methods, presents a formidable challenge. Information imbalances between creditors and debtors further complicate decision-making, often leading to misjudgments during RM negotiations (Pu et al., 2012). This study delves deeply into these complexities, aiming to empower potential RM beneficiaries with comprehensive insights into the RM landscape, thereby addressing significant informational gaps faced by debtors.

To navigate this intricate landscape, our study employs a rigorous methodological approach. Utilizing the Home Equity Conversion Mortgage (HECM) pricing model developed by Szymanoski (1994) and Lee et al. (2012), we delve into the structural analysis of RM programs proposed by Lee and Lo (2016). Employing sophisticated financial engineering calculation methods, we evaluate RMs across various dimensions: the lump-sum loanable amount, rental income, remaining house value, creditor insurance protection, premium expenses, and creditor profits.

Our research extends beyond the surface, exploring the nuances of different occupational groups, age brackets, and gender categories. Through detailed simulations and sensitivity analyses, we dissect the impact of variables on income replacement ratios for fixed loanable amounts. Furthermore, we assess RM risks by evaluating financial institutions’ profits, employing current RM program parameters for meticulous evaluations and simulations.

Our study contributes vital insights into RM programs tailored to the diverse needs of retirees in Taiwan. By unraveling the complexities and providing detailed analyses, this research empowers potential debtors with knowledge and guides creditors in program valuation and asset allocation. The implications of our findings extend to both debtors and creditors, offering a comprehensive guide for making well-informed decisions in the realm of RM programs.

The subsequent sections will delve into the methodologies employed, the outcomes of our analyses, and their broader implications, offering a comprehensive understanding of the intricate world of RM programs in Taiwan. The subsequent chapters of this study are as follows: The second chapter is the literature review. The third chapter introduces the model hypotheses and the research method, including simulations and sensitivity analysis for current RM programs. The fourth chapter discusses the numerical results. The fifth chapter presents the conclusion and suggestions of this study.

Literature review

RM is the practice of older adults mortgaging their real estate assets to financial institutions in exchange for money to cover their cost of living; the principal and interest are repaid before or after their death. RMs have been used in other countries for some time; they were first proposed in the United States in the 1980s. Houses were used as financing tools to supplement an insufficient pension after retirement. RM has been developed for over 30 years in the United States. Initial RM development faced obstacles because the life expectancy of retirees increased, and the pension they were eligible to receive might exceed the total loan. Hence, banks were skeptical of RMs due to this risk. In 1989, the United States Department of Housing and Urban Development intervened and promoted the HECM program. It stated that the government would subsidize any amount that exceeded the loan, changing RM into a social welfare program and increasing its popularity. HECM is a financial mechanism that allows older adults to exchange their houses for liquidity; the home conversion loan is used to supplement a pension, and adults are not required to move away from or sell their residences. The United States federal government insures the HECM program, and the federal government promises that the creditor will receive the original contract amount. The Federal Housing Administration is responsible for ensuring that the loan recovered by creditors exceeds the value of the mortgaged house and compensates for accidental losses. The purpose of RM is to provide older adults with a stable source of income to improve their economic circumstances. Numerous studies have indicated that RM effectively increases the income and quality of life of retirees and subsidizes their living costs (Wang et al., 2011; Merrill et al., 1994; Mayer & Simons, 1994; Ong, 2008; Mitchell & Piggott, 2004; Huang et al., 2008). Nowadays, most (approximately 95%) of all RM programs in the United States are HECM plans. Although regulations specify that older adults over 62 are eligible to apply for RMs, statistics demonstrate that the average age of the applicants is 75. This reveals that the applicants apply based on their economic circumstances and needs, and the loan amount varies with the age and sex of the applicant, the location and value of the house, and the market interest rate (Wang et al., 2011; Lee & Lo, 2016).

The nonrecourse clause, a particular clause of RMs, specifies that when the contract terminates, financial institutions may only request the value of the mortgaged house. In general, to prevent the balance of the loan lent by financial institutions from exceeding the house’s value, the government usually provides RM insurance to compensate for the RM losses. It encourages financial institutions to provide RM services. In one study related to RM insurance, Szymanski (1994) used the HECM pricing model to calculate the principal limit factor and determine the maximum loanable amount that debtors may borrow and further explained how RM insurance eliminated the risk of loan loss. Wang et al. (2011) investigated an HECM-based model and used parameters such as the mortality rate in Taiwan, value of houses in the past, and treasury rates to calculate the ratio of the loanable amount. Huang et al. (2011) observed that insurance companies faced crossover risk if the balance of the loan exceeded the house’s value and provided a three-dimensional lattice method to simultaneously capture changes in the house’s value and short-term interest rates and numerically calculate a reasonable RM price. They also designed two crossover bonds that partially enable RM insurance companies to transfer crossover risk to the bondholders. Lee and Lo (2016) argued that analyses of RM programs should consider the rental income and remaining value of the debtors’ houses. They divided the initial value of a house into six segments: loanable amount, rental income, remaining value of the house, insurance protection of creditors, premium expense, and creditor profit. The structure of RM programs provided by financial institutions can be used to understand the profitability and risks of the programs (Badescu et al., 2022).

Academic literature has examined RMs from various perspectives. With the aging population in various countries, considering RMs has become crucial. Studies such as Hanewald et al. (2020) in China, Mayer, Moulton (2022) in the United States, and Whait et al. (2019) in Australia have continuously evaluated and researched the feasibility of RMs. Benavides Franco et al. (2022) explored the feasibility of reverse mortgages in Colombia, while Di Lorenzo et al. (2022) further utilized artificial intelligence to obtain a predictive analysis of the pricing process. Yang et al. (2020) employed extensive data analysis to examine reverse mortgages in Korea. Boj del Val et al. (2022) found that these families, particularly those with initial wealth less than a certain percentage of the property’s appraised value, are likely candidates for RMs.

From the supplier’s perspective, Di Lorenzo et al. (2022) assessed contract risks and proposed a securitization method. Lenders avoid risks by using insurance through a special-purpose vehicle and issuing bonds based on their gains/losses from the contract. De la Fuente et al. (2023) reveal that reverse mortgage providers encounter elevated risks when the initial advance amount is higher. Among these, lump-sum cases pose the most significant risk, especially for younger borrowers, females, and instances with higher interest rates and floating mortgage rates. Fuente et al. (2020) assess risk in lump-sum reverse mortgages using a Monte Carlo simulation with ARMA-EGARCH modeling for UK house prices (1952–2019). Younger borrowers, particularly females with high roll-up rates, face elevated risk. Moreover, Fuente et al. (2021) present a method for evaluating risk and calculating regulatory capital requirements, employing value-at-risk and expected shortfall in alignment with Basel II and Basel III standards. These findings impact policy decisions for Basel III and lender economic capital, significantly when rental yield surpasses the risk-free rate.

A literature review demonstrates that current studies have mainly investigated RMs from the perspective of RM supplier by calculating the maximum loanable amount or the risks faced by these institutions and their responses. Current studies have also explored the demand of debtors for RM or the economic benefits of RM. However, the asymmetric information between debtors and creditors causes the parties to view the maximum loanable amount differently (Pu et al., 2012). Therefore, this study referenced the structural analysis of Lee and Lo (2016) and used a dissection of the structure of RM programs to help debtors understand the characteristics of RM programs, protect their rights, increase the value of RM programs, and enable creditors to understand the risks of providing RM services.

Research method and empirical data

The research method of this study was selected concerning Lee and Lo (2016), and the lump-sum RM was used as an example to analyze RMs for retirees of different occupations, namely public servants, educators, military personnel, and laborers. The income replacement ratio of older adults who applied for RM after they retired was calculated for these four groups. The dynamic house value model used by this study was developed about the frameworks of Wang et al. (2011) and Lee and Lo (2016). This study assumed that the mortality rate followed the model proposed by Lee and Carter (1992) and used the mortality rate in Taiwan to estimate the rental income, loanable amount, remaining house value, premium expense, RM insurance cost, and creditor profit of lump-sum RM programs. Finally, the effect of crucial variables on the items mentioned above was observed for a fixed loanable amount. This dissection of the structure of RM programs enables debtors better to understand the characteristics and risks of RM programs, thereby helping them assess their circumstances and select the most suitable program.

Dynamic house value model

This study assumed that the dynamic house price model satisfies the requirements of a stochastic model and further assumed that the rate of return of a house is by geometric Brownian motion(GBM). Under the physical measure (P), which is the measurement of the actual value, the changes in the value of the house H(t) can be described as follows:

Where μH is the rate of return of the value of the house under the measure P, δ is the rental rate (or maintenance yield), σH is the fluctuation of the house value, and WP (t) is a normally distributed random term. Moreover, measure conversion was used to convert the measure P to the risk-neutral measure Q. The changes of H(t) under Q are as follows:

Where WQ (t) is a normally distributed random term N(0, 1). In reference to Chen et al. (2010) and Li et al. (2010), the rental rate (δ) was assumed to capture the rental income generated by real estate. Moreover, the value of houses was assumed to change by the suggestions of Chen et al. (2010), Li et al. (2010), Wang et al., (2011), and Lee and Lo (2016). The rental rate (δ)Footnote 1 In this study, the gross rental yield was set at 1.5% to calculate the rental income obtained by debtors from their houses. The fluctuation of house values was set to 10%.

Mortality rate model

Estimations of the mortality rate require numerous assumptions. This study used the Lee–Carter model (Lee & Carter, 1992) to estimate the mortality rate of debtors at each point in time. The Lee–Carter model assumes that at the times t, people aged x years exist and the mortality rate of people under the age of x mx,t is the Equation of the model is as follows:

Where αx is the average mortality rate of people aged x years, βx is the change of the relative mortality rate of people aged \(x\) years, \({k}_{t}\) represents the intensity of the mortality rate at t, and \({{\rm{\varepsilon }}}_{x,t}\) is the random error. In addition, the Equation must satisfy the condition ∑t kt = 0, ∑x βx = 1 to ensure that the model has only one optimal solution. For a more detailed explanation, please refer to Lee and Carter (1992) and Koissi and Shapiro (2008).

The probability of survival (npx) was defined by assuming that the debtors in the market were aged x and at the time t of the evaluation t = 0. After the debtors have lived n years, their probability (npx) of becoming x + n years old is as follows:

Where qx+n−1 is the mortality rate and represents the possibility of the debtor living x + n−1 years but dying in the next year. In other words, n−1px × \({q}_{x+n-1}\) is the probability of x year-old debtors dying on the n th year.

Lump-sum RM program design

For the RM programs, this study assumed that the risk-free interest rate is r, the loan rate is \({r}_{L}={\rm{r}}\) + \({\pi }_{r}\) (the loan rate is equal to the risk-free interest rate (\({\rm{r}}\)) plus a rate difference (\({\pi }_{r}\))), the initial value of a house is \(H(0)\), and the lump-sum received by the debtor after costs such as application and processing fees were excluded is \({BAL}\left(0\right)\). The debtor is responsible for paying the interest on the loan and the premium of the RM insurance. Applying for the RM insurance was assumed to include the one-time application fee and premium \({\pi }_{0} \%\) and the annual renewal premium \({\pi }_{m} \%\). Therefore, the application fee for the first year was \(H\left(0\right){\pi }_{0} \%\) of the initial value of the house, and the cost in each subsequent year was \({BAL}(t){\pi }_{m} \%\) of the remaining balance of the loan. The debtor does not pay expenses related to interest rates or costs during the term of the contract but instead tallies the annual premium with the annual remaining balance of the loan \({BAL}\left(t\right)\) until the termination of the contract. The HECM loan contract defines the termination of a contract as a debtor dying, auctioning the house and paying off the debt, or moving away from the mortgaged house for more than 12 months. Due to a lack of actual data, in this study, the contract termination date was defined as the end of each year, and if a debtor died, they were assumed to do so at the end of the year. The remaining balance of the loan at the end of year \(t\) would be the remaining balance of the loan at the end of year t − 1 plus the premium of year t − 1 and the accrued interest as in Eqs. (6) and (7):

These two equations can be simplified to obtain the remaining balance of the loan at the start of each year as follows:

Rental income

The rent is determined by the value of the house. This study assumed that the dynamic price of the house was as in Eq. (8), and the ratio of the rate of return of the rent and the value of the house was the rental rate (\(\delta\)). According to Merton (1973), the dynamic house valuation \(H(t)\) can be deduced using the risk-neutral measure \(Q\) as demonstrated in Eq. (8):

At the time of evaluation (t = 0), the value of the house can be calculated as follows:

This Equation includes the current value of the rent and calculates the value until the lease agreement of the house expires on the date \(T\). The rental income \({V}_{R}(0)\) that the debtor could receive after discounting the present value and the survival rate can be calculated using Eq. (10):

Where the debtor is x years old, ω is the maximum age to which the debtor will live, the probability of the debtor living \(t-1\) years is (t−1px, and the probability of the debtor dying in the following year is \({q}_{x+t-1}\). Finally, the probability of the debtor dying on the tth year was calculated as t−1px × \({q}_{x+t-1}\).

Remaining house value

The remaining house value is calculated by using the concept of real options. The mortality rate of debtors each year is multiplied by the dynamic house value and the changes in the remaining loan balance to deduce the real options value generated by the house and the remaining loan balance. The calculations are presented in the following two equations. For more detailed calculations, please refer to Lee and Lo (2016):

where\({d}_{1}(t)=\frac{{ln}\left(\frac{H(0)}{BAL(0)\pi (t)}\right)+(-\delta -{\pi }_{r}+\frac{1}{2}{\sigma }_{H}^{2})t}{\sqrt{{\sigma }_{H}^{2}t}},\,{d}_{2}(t)={d}_{1}(t)-{\sigma }_{H}\sqrt{t}\),

j = 0, 1, 2,…, and \(\Phi\) is the cumulative probability distribution function of standard normal distribution.

Premium expense (income)

The premium expense includes the initial premium and the renewal premium. The initial premium refers to the one-time expense and premium (\({\pi }_{0}\)) required for the application. Therefore, the initial value of the house is \(H(0){\pi }_{0}\), and the premium that must be paid annually before the termination of the contract is \({BAL}(t){\pi }_{m}\). This study calculated the expected remaining balance of the loan each year and multiplied it by the survival rate as in Eq. (12). Equation (13) further simplifies Eq. (14):

RM insurance cost (insurance protection received by the creditor)

From the perspective of a financial institution, if the debtor dies at year t, the financial institution that issued the insurance would suffer a loss between the remaining balance of the loan \({BAL}\left(t\right)\) and the value of the house \(H\left(t\right)\). Therefore, each year can be considered a put option. Because the debtor could die during each year, the mortality rate of the debtor in each year was multiplied, and the result is tallied in Eq. (15). This calculation is presented in Eq. (16):

Finally, the lump-sum loanable amount \({BAL}\left(0\right)\) was calculated. About Wang et al. (2016), the RM insurance cost (Eq. 14) was modified to be equal to the present value of the premium expense (Eq. 16), and Eq. (17) was used to obtain the optimal solution of the lump-sum loanable amount \({BAL}\left(0\right)\). The value of BAL(0) is determined using a nonlinear root-finding method.

The lump-sum loanable amount \({\rm{BAL}}\left(0\right)\) was further converted to an annuity, as demonstrated in Eq. (18), to enable the calculation of the actual annual loanable amount and the determination of the lifetime annuity of each debtor from the RM.

Where \(r\) is the market risk-free interest rate, and \(\omega\) is the maximum age (set at 110). Finally, the income replacement ratio was used to measure the increased income to the debtor from RM. The income replacement ratio was calculated by dividing TP the average monthly salary before retirement.

House price index

In order to ensure that the model used conforms to the statistical assumptions of GBM, this study uses statistical tests to measure whether the housing data conforms to GBM. Since the study illustrates the behavioral uncertainty generated by housing prices, Badescu et al. (2022) pointed out that a variety of realistic economic models are calibrated, and the House Price Index (HPI) is often considered a proxy variable for house price dynamics in line with the HPI. Specifically, this study performed the following processing on HPI data, calculated the quarterly change rate of HPI for each quarter, and converted the quarterly change rate into an annual change rate (annualized standard deviation = standard deviation of Quarterly returns \(\times \sqrt{4}\), annual change rate= Quarterly returns \(\times \sqrt{4}\)).

Statistical test

This study used the Anderson-Darling (AD) test (Stephens, 1974) and the Kolmogorov–Smirnov (KS) test (Chakravart et al., 1967) to verify whether the change rate of HPI conforms to a normal distribution and HPI index following a logarithmic normal distribution. The Anderson-Darling test is a powerful goodness-of-fit test that can compare a data sample to a hypothesized distribution. The test statistic, the Anderson-Darling statistic, measures the discrepancy between the data and the hypothesized distribution. The smaller the statistic, the better the fit. The p-value is used to assess the statistical significance of the test statistic. If the p-value is less than the chosen alpha level (e.g., 0.05).

The Kolmogorov–Smirnov test determines whether a sample comes from a specific distribution. It is a non-parametric statistical test that assesses if the sample’s empirical cumulative distribution function (ECDF) differs significantly from the hypothesized distribution. The null hypothesis states that the data come from a standard normal distribution, against the alternative hypothesis that they do not. The full technical description of the AD and KS tests can be found in the Appendix as supplementary files.

Empirical results and analysis

Actual examples and parameters were used with the equations in the previous chapter to calculate the income replacement ratio of applicants of various sexes and occupations who applied for RM at different ages. In addition, we used the HPI index of the first quarter of 2015 to measure house prices. The initial value is 73.21 (The base period is the entire year 2021 = 100, Adjusted based on economic changes), and the calculated annualized historical volatility is 0.0709. In the simulation results, we use the AD and KS tests to achieve significance at 0.05 levels; the assumptions of lognormality and normal distribution cannot be rejected.

Table 2 presents the results of Anderson-Darling (AD) tests conducted on two distinct datasets: the house price index change rate and the house price index itself. These tests aimed to assess the suitability of assuming a normal distribution for the former and a log-normal distribution for the latter. For the change rate of the house price index, the AD test statistic yielded a value of 0.6436 under the normal distribution assumption. At the same time, the corresponding p-value was calculated to be 0.0844. Although this p-value slightly exceeds the conventional significance level of 0.05, indicating a marginal departure from normality, it remains within a range susceptible to sampling error.

Consequently, the null hypothesis of normal distribution cannot be decisively rejected, suggesting that the data might conform to a normal distribution. Conversely, the AD test results for the house price index tell a markedly different story. With an AD test statistic of 1.3625 and an exceptionally low p-value of 0.0013, the null hypothesis of log-normal distribution is unequivocally rejected. This outcome underscores strong evidence that the house price index data diverges significantly from log-normal and may exhibit characteristics indicative of a non-log-normal distribution.

Table 3 uses the HPI index and the simulated housing price index path to conduct a two-sample Kolmogorov–Smirnov test. The simulation parameters of GBM are to use H(0) as the initial value of HPI and the historical change rate to simulate the changes in GBM. To determine the simulated house price index, it can conform to the change process of HPI. We simulate the path 10,000 times, that is, to test whether the changes in HPI and the house prices we simulated are in line with the normal distribution. Ozer-Imer, Ozkan (2014) to understand whether GBM meets significance and average the statistical results as shown in Table 3:

In Table 3, the p-value of the Kolmogorov–Smirnov test conducted on the Change Rate of HPI from 2016Q1 to 2023Q3 is reported as 0.8257, with a critical value of 0.2379. The failure to reject the null hypothesis suggests no significant difference between the observed and normal distributions. This indicates that the data may conform to a normal distribution. Furthermore, the results of the KS test conducted on the simulated HPI data using the Geometric Brownian Motion GBM model are presented. The average p-value across 10,000 simulations is calculated as 0.78298, which exceeds the conventional significance level of 0.05. Additionally, the hypothesis test result for this simulation stands at 0.0001, indicating that the null hypothesis remains unchallenged at a significance level of 0.0001. Hence, the change rate of the simulated HPI is consistent with a normal distribution. These findings provide comprehensive insights into the statistical properties of both the observed and simulated HPI data. The meticulous examination underscores the reliability of the data and enhances our understanding of its distribution characteristics, particularly in the context of future analysis and modeling.

In Fig. 1, we calculate the ECDF of the change rate of HPI and the normal distribution. The two lines on the graph represent the empirical CDF of the HPI change rate, the standard normal CDF, indicating that it captures similar probability distribution characteristics as the change rate of HPIs. The change rate of HPIs aimed to replicate the standard normal distribution, and the overlap between the ECDFs suggests a successful result.

This figure compares the empirical cumulative distribution function (CDF) of the House Price Index (HPI) change rate to the standard normal CDF. The blue line represents the empirical CDF of the HPI change rate, while the red line represents the standard normal CDF.

The lump-sum loanable amount for various types of debtors was analyzed. Debtors were classified by sex because men and women have different life expectancies. Due to the age restrictions of RMs, debtor ages were set between 60 and 95, and analyses were performed for ages multiples of 5 within this age range. Previous scholars’ assumptions for Taiwan’s life table were used, and debtors were assumed to live for up to 110 years to simulate the survival rate. The market indicates that banks currently offer loan rates of 1.86% to 2.73%. Therefore, loan rates were classified into five categories to analyze the sensitivity of the interest rate. The value of the houses eligible for RM were grouped as NT$6 million, NT$8 million, or NT$10 million. The average value of houses in RM programs is NT$5 million, and the standard RM value for financial institutions varies by the location of the house. Therefore, the assumptions of this study are consistent with those of the market. Finally, this study assumed the following for house value fluctuations: the fluctuation rate (\({\sigma }_{H}\)) was 0.1; the rental rate (\({\rm{\delta }}\)) was 1.5%; the risk-free interest rate (\(r\)) was the average interest rate of the Bank of Taiwan, the Taiwan Cooperative Bank, the First Bank, Hua Nan Bank, and the Land Bank of Taiwan (1.04%); and the difference between the loan rate and the risk-free interest rate (\({\pi }_{r}\)) was 1.5%. In addition, in reference to HECM, the initial premium (\({\pi }_{0}\)) and the renewal premium (\(\,{\pi }_{m}\)) were assumed to be 2% and 1.25%, respectively. The mortality rate in TaiwanFootnote 2 was fit to the Lee–Carter model to estimate the survival rate and mortality rate of people aged 60–110. Debtors were assumed to live up to at most 110 (the maximum age (ω) was 110). Occupation insurance classifications in Taiwan were used to classify retirees according to their occupation before retirement, namely educator, public servant, military personnel, or laborer. The assumed parameter values are listed in Table 4.

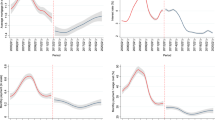

Figure 2 presents the life expectancy of men and women aged 60 or 70. In 2015, the life expectancy of 60-year-old women was 26.05, indicating that they typically live until 86.05, whereas that of 60-year-old men was 21.93, indicating that they typically live until 81.93. The life expectancy of 70-year-old women was 17.59, indicating that they typically live until 87.59, whereas that of 70-year-old men was 14.62, indicating that they typically live until 84.62. The average life expectancy at birth for Taiwanese was 82 years, according to estimates released by the Ministry of the Interior. Therefore, debtors should have sufficient information to determine how they should apply for an RM in accordance with their sex and age. This study can serve as a reference for retirees of different occupations when they apply for RM.

This figure shows the average life expectancy of male and female individuals aged 60 and 70 in Taiwan from 2003 to 2015. The blue and orange lines represent the life expectancy of male and female individuals aged 60, respectively. In contrast, the purple and yellow lines represent the life expectancy of male and female individuals aged 70, respectively. The figure illustrates a general trend of increasing life expectancy for all groups over the study period.

Table 5 demonstrates the maximum loanable amount for debtors of various ages; the maximum loanable amount increases as debtors age. Because a debtor’s remaining lifespan decreases as they age, the present value of the rental income decreases as a debtor ages. If a 70-year-old debtor borrowed the maximum loanable amount (NT$509,710), the debtor would have an expected rental income of NT$223,510 and a remaining house value of NT$189,150. Therefore, the debtor exchanged an NT$1 million house for a pension worth NT$922,370. The remaining NT$77,630 becomes the creditor’s profit. The financial institution that acted as the creditor paid NT$143,210 of the premium in exchange for insurance protection of the same value. Hence, the insurer’s profit and loss were equal because the insurance income was equal to the insurance cost (NT$143,210). It is important to note that the deviation between premium expenses and insurance costs observed in the fifth and sixth columns of Table 5 for older adults, precisely those aged 60 and above, aligns with the assumptions of our model. This discrepancy reflects the dynamic nature of insurance pricing, wherein premiums decrease with age while insurance costs remain fixed. It accurately captures the evolving relationship between premium expenses and insurance costs as debtors progress through different life stages. The loanable amount for women was higher than that of men. Banks’ profit would be lower if an RM were provided to a woman because women have a longer life expectancy. Table 6 utilizes the HPI to replace the initial price from Table 5. Upon comparing the two tables, we observe that Creditor profit increases while RM insurance cost decreases. The underlying reason is that the price reflected by the HPI corresponds to the year 2016. Specifically, the house price in 2021, indexed at 100, is 28% lower than the initial price—consequently, both overall profit and insurance cost exhibit relative reductions.

Table 7 presents the monthly pensions for various occupation groups. The data were published by the Pension Reform Committee.Footnote 3

This study analyzed the sensitivity of the lump-sum to the loan rate (Table 8); if the loan rate was higher, the lump-sum payment was lower. The loanable amount for female debtors was higher than that for male debtors. Therefore, selecting the appropriate loan rate can protect retired debtors more. Nearing the age of 95, as reproduction is obtained and estimates of reproduction rates are completed, the higher mortality rate as you get older and the increased risk of uncertainty will seriously affect the price estimate. Debtors with superior credit have an advantage when applying for an RM.

The income replacement ratio for various occupation groups was analyzed (Table 9), assuming that the amount borrowed was NT$8 million, the loan rate was 1.86%, and other parameters were unchanged. Table 9 demonstrates that younger debtors had lower income replacement ratios than older debtors. Moreover, the income replacement ratio of laborers was higher than that of the other three occupation groups because the monthly pension of laborers was lower than that of the other groups. Consequently, they have a higher income replacement ratio. Applying for RM at an older age resulted in a higher annuity.

Because laborers are the largest occupation group, this study analyzed the sensitivity of the income replacement ratio of laborers to the loan rate for various ages and sexes. The interest rate was classified into five intervals for debtors between 60 and 95. Table 10 demonstrates that higher age was associated with a higher income replacement ratio and that the income replacement ratio of women was higher than that of men. If the interest rate was lower, the income replacement ratio was higher, and the protection was more secure.

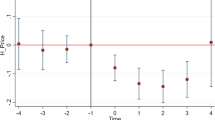

In Fig. 3, the graph shows that men have a higher replacement rate than women, and the difference grows with age. However, the interest rate increase will reduce this gap.

This 3D scatter plot explores the relationship between loan rates, income replacement ratio, and ages for both men and women. The blue and red dots represent data points for men and women, respectively. The x-axis represents loan rates, the y-axis represents the income replacement ratio, and the z-axis represents ages.

Table 11 continues the analysis in Table 10; the income replacement ratio of laborers for various loan rates and amounts was analyzed. Larger loans, lower interest rates, and older ages were associated with a higher income replacement ratio. If the loan rate was higher, the loanable amount was lower. Younger debtors did not receive more protection. Therefore, debtors applying for RM should make optimal judgments regarding their identity, age, and assets for optimal protection.

Conclusion and discussion

This study employed the HECM pricing model developed by Szymanoski (1994), Lee et al. (2012), and Lee and Lo (2016) to evaluate RM programs. Financial calculations determined the lump-sum loanable amount, rental income, remaining house value, insurance protection for creditors, premium expenses, and creditor profit for debtors of different occupations and ages. Age, sex, loan rate, debtor occupation, and house value significantly impacted the loanable amount.

The primary contribution lies in its debtor-oriented approach, exploring how RM programs can improve the economic circumstances of older adults. The results enable debtors to assess their situations and choose the most beneficial RM program based on occupation and age. The empirical results revealed that the female sex, lower interest rates, older age, and larger loans benefit debtors more, while creditor profit decreases when lending to older debtors. Applying for RM programs after age 75 is advantageous for debtors. Given the complexity of RM programs, it is recommended that the government require independent third-party consultation services for debtors to ensure complete understanding and reduce information asymmetry.

The research focused on the economic impact of RM programs on older adults in Taiwan. In a rapidly aging society like Taiwan, understanding the intricacies of RM programs is crucial. The study aimed to help debtors make informed financial decisions by exploring various conditions and limitations. This study addressed a gap in the literature by examining critical factors such as applicant age, loan period, interest rates, payment methods, and interest calculations, highlighting the complexities of RM programs in Taiwan. Detailed analysis is essential for ensuring that potential beneficiaries are well-informed. The research employed the HECM pricing model and a structural analysis framework, conducting simulations and sensitivity analyses to provide robust conclusions.

Our findings underscore the significant influence of factors such as applicant age, sex, interest rates, and loan amounts on RM program benefits. Our study highlights the advantages of applying after the age of 75 and offers actionable insights for potential debtors. The research provides valuable information for debtors and creditors, guiding program valuation and asset allocation.

Our results underscore the importance of tailored financial instruments for different demographic groups and the necessity for policy interventions and financial education initiatives for older adults. We propose practical recommendations, including increasing the maximum loan amount, reducing interest rates, expanding eligibility criteria, and implementing risk-sharing mechanisms to protect the government from potential losses. These measures aim to enhance the affordability and accessibility of reverse mortgages.

Limitations and future research

The study assumed specific parameters due to data limitations, such as fluctuations in house values, introducing uncertainties into the model. These limitations should be considered when interpreting the results and their applicability beyond the studied contexts.

Future studies should explore advanced stochastic modeling techniques to capture house price dynamics better. GBM can simulate potential future price paths considering trends and volatility but may miss features like abrupt changes. To refine house price estimations, integrating time series models such as ARIMA and GARCH can align house price dynamics with market fluctuations, enhancing prediction accuracy.

Researchers often use more complex models like stochastic differential equations or add factors like economic indicators and demographic trends to improve simulations’ realism. Future research can use predicted HPI prices to forecast RM-related variations, aiding more informed RM and financial strategy decisions. Incorporating comprehensive datasets can provide a nuanced understanding of RM-related risks. Exploring cross-regional variations and behavioral aspects in decision-making can offer a holistic perspective. Longitudinal analyses can identify trends over time, while a broader literature review of global studies can offer a comprehensive overview. Additionally, future research avenues include investigating policy and regulatory impacts, combining quantitative and qualitative research, and exploring technological advancements’ influence on RM programs. Understanding RM programs’ social and economic implications on individuals, families, and communities can provide valuable insights into these financial instruments’ broader consequences.

Data availability

The data that support the findings of this study have been enclosed as supplementary files.

Notes

Source: http://www.globalpropertyguide.com/Asia/Taiwan/rent-yields. The rental rate was approximately 1.57%; hence, we set the rental rate to 1.5%.

Human Mortality Database: http://www.mortality.org/.

The pension system of Taiwan: http://pension.president.gov.tw/cp.aspx?n=790F40C2F95C4DD3&s=F9E3ABBD197C8169.

References

Badescu A, Quaye E, Tunaru R (2022) On non-negative equity guarantee calculations with macroeconomic variables related to house prices. Insur Math Econ 103:119–138

Benavides Franco J, Alonso Cifuentes JC, Carabalí Mosquera JA, Sosa A (2022) On the feasibility of reverse mortgages in Colombia. Int J Hous Mark Anal 15(5):1195–1224

Boj del Val E, Claramunt Bielsa MM, Varea J (2022) Reverse mortgage and financial sustainability. Technol Econ Dev Econ 28(4):872–892

Chakravarti L, Roy (1967) Handbook of methods of applied statistics, vol. I. John Wiley and Sons, pp. 392–394

Chen H, Cox SH, Wang SS (2010) Is the home equity conversion mortgage in the United States sustainable? Evidence from pricing mortgage insurance premiums and nonrecourse provisions using the conditional Esscher Transform. Insur Math Econ 46(2):371–384

De la Fuente I, Navarro E, Serna G (2023) Proposal for calculating regulatory capital requirements for reverse mortgages. Socio-Econ Plan Sci 88:101659

Di Lorenzo E, Piscopo G, Sibillo M, Tizzano R (2022) Reverse mortgage and risk profile awareness: proposals for securitization. Appl Stoch Models Bus Ind 38(2):353–369

Fuente IDL, Navarro E, Serna G (2021) Estimating regulatory capital requirements for reverse mortgages. An international comparison. Int Rev Econ Financ 74:239–252

Fuente IDL, Navarro E, Serna GJM (2020) Reverse mortgage risks. Time evolution of VaR in lump-sum solutions. Math 8(11):2043

Hanewald K, Bateman H, Fang H, Wu S (2020) Is there a demand for reverse mortgages in China? Evidence from two online surveys. J Econ Behav Organ 169:19–37

Huang HC, Wang CW, Miao YC (2011) Securitization of crossover risk in reverse mortgages. Geneva Pap Risk Insur Issues Pr 36:622–647

Huang HC, Wu WC, Lin TC, Cheng YF (2008) The application of reverse mortgages in an aging society. J Risk Manag 10(3):293–314

Koissi MC, Shapiro AF (2008). The Lee-Carter model under the condition of variables age-specific parameters. Paper presented at the 43rd Actuarial Research Conference, University of Regina, Saskatchewan, 14–16 August 2008

Lee RD, Carter LR (1992) Modeling and forecasting US mortality. J Am Stat Assoc 87(419):659–671

Lee YT, Lo YH (2016) Structural analysis of reverse mortgages. NTU Manag Rev 26(2):139–171

Lee YT, Wang CW, Huang HC (2012) On the valuation of reverse mortgages with regular tenure payment. Insur Math Econ 51(2):430–441

Li SH, Hardy MR, Tan KS (2010) On pricing and hedging the no-negative-equity guarantee in equity release mechanisms. J Risk Insur 77(2):499–522

Mayer C, Moulton S (2022) The market for reverse mortgages among older Americans. In: Mitchell OS (ed) New models for managing longevity risk: public-private partnerships. Oxford, pp. 258–300

Mayer CJ, Simons KV (1994) Reverse mortgages and the liquidity of housing wealth. Real Estate Econ 22(2):235–255

Merrill SR, Finkel M, Kutty NK (1994) Potential beneficiaries from reverse mortgage products for elderly homeowners: an analysis of American housing survey data. Real Estate Econ 22(2):257–299

Merton RC (1973) Theory of rational option pricing. Bell J Econ Manag Sci 4(1):141–183

Mitchell OS, Piggott J (2004) Unlocking housing equity in Japan. J Jpn Int Econ 18(4):466–505

Ong R (2008) Unlocking housing equity through reverse mortgages: the case of elderly homeowners in Australia. Int J Hous Policy 8(1):61–79

Ozer-Imer I, Ozkan I (2014) An empirical analysis of currency volatilities during the recent global financial crisis. Econ Model 43:394–406

Pu M, Fan GZ, Deng Y (2012). Breakeven determination of loan limits for reverse mortgages under information asymmetry. IRES Working Paper Series

Stephens MA (1974) EDF statistics for goodness of fit and some comparisons. J Am Stat Assoc 69(347):730–737

Szymanoski EJ (1994) Risk and the home equity conversion mortgage. Real Estate Econ 22(2):347–366

Wang CW, Huang HC, Lee YT (2016) On the valuation of reverse mortgage insurance. Scand Actuar J 2016(4):293–318

Wang JL, Wang JW, Liu WP (2011) The impacts of the reverse mortgage on retirement income in Taiwan. J Risk Manag 13(1):25–48

Whait RB, Lowies B, Rossini P, McGreal S, Dimovski B (2019) The reverse mortgage conundrum: perspectives of older households in Australia. Habitat Int 94:102073

Yang J, Min D, Kim J (2020) The use of big data and its effects in a diffusion forecasting model for Korean reverse mortgage subscribers. Sustain 12(3):979

Author information

Authors and Affiliations

Contributions

Both authors conceived of the presented idea, verified the analytical methods, and performed the computations. All authors discussed the results and contributed to the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Chen, HM., Chen, JY. Structural analysis of reverse mortgages in Taiwan. Humanit Soc Sci Commun 11, 1204 (2024). https://doi.org/10.1057/s41599-024-03641-x

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-024-03641-x