Abstract

The global economy has suffered greatly from the COVID-19 pandemic. Vietnam’s economic sectors also cannot avoid this general situation, particularly in the logistics area. This industry contributes a significant portion of the gross domestic product (GDP) and has been prioritized for development by the Vietnamese government in recent years. Additionally, this sector is desirable to investors, particularly foreign investors. However, the lack of research provides a comprehensive awareness of companies’ performance in the Vietnamese logistics industry, especially fluctuations before, during, and after the pandemic. Inspired by this context, this study evaluates the performance of listed logistics companies from 2019 to 2023 to fill the research gap. A three-phase framework methodology that integrates Criteria Importance Through Intercriteria Correlation (CRITIC) and ranking methods, including Technique for Order Preference by Similarity to Ideal Solution (TOPSIS) and Evaluation based on Distance from Average Solution (EDAS), is employed to evaluate objectively. The assessment is based on 10 financial variables that reflect firms’ profitability, operations, leverage, and growth ability. The findings indicate differences in the rankings by TOPSIS and EDAS; nonetheless, the difference is insignificant, and there is consistency between the two approaches at the highest rank. Among alternatives, VGP emerges as the company belonging to the highest-ranking group and is the most stable. In contrast, GMD and TMS are known as the most volatile businesses, yet they have experienced an impressive recovery following the pandemic. In fact, these findings help logistics companies prioritise digital transformation and sustainable development, governments increase support policies, and investors choose successful enterprises with high resilience and potential in the post-pandemic future.

Similar content being viewed by others

Introduction

Located in a strategic position within the Southeast Asian market, Vietnam boasts a coastline of over 3000 km and 34 seaports of various classifications (GSO, 2023). Consequently, the logistics industry in Vietnam has great potential for development in shipping commodities to nations inside and outside the region. Before COVID-19, the logistics sector contributed 20–22 billion USD annually, accounting for 20.9% of Vietnam’s GDP. Furthermore, based on the World Bank’s assessment, Vietnam ranked 64th among 160 nations in terms of logistics development, and it stands as the fourth-highest-ranking country in ASEAN, following Singapore, Malaysia, and Thailand (NIF, 2017). In 2018, Vietnam’s ranking improved to 38th, but it subsequently declined to 43rd in 2023 following the coronavirus epidemic (MOF, 2023). Initially emerging in Vietnam at the beginning of 2020, COVID-19 broke out aggressively in April 2020, severely impacting all aspects of the economy. Countries blocked their borders, and airlines ceased flights, which in turn affected import and export business. Simultaneously, the government locked down major cities, such as Hanoi and Ho Chi Minh City, directly and severely impacting Vietnam’s logistics sector. A report by the Vietnam Logistics Business Association (VLA) indicates that 485 companies in this sector closed during the first nine months of 2020. Furthermore, the overall volume of shipped commodities decreased by 7.3% compared to the same period last year (MOIT, 2020). Following the epidemic, the Vietnamese government has implemented several policies to support the rehabilitation and growth of the logistics sector. At the same time, the rapid growth of the e-commerce market has provided logistics companies with opportunities to overcome challenges and rebound. Still, many companies have not yet managed to get over the challenging circumstances.

Logistics is a key industry that has a significant impact on Vietnam’s economic development, with a high contribution to GDP and increasing over the years. Additionally, this field is prioritized by the government, which has implemented numerous support policies in accordance with the “Action Plan to Enhance Competitiveness and Develop Vietnam’s Logistics Services by 2025,” approved by the Prime Minister on 14 February 2017. Consequently, the performance of enterprises in this area influences not only the companies but also the overall economy. Therefore, the insights gained from analyzing the performance of logistics firms are a helpful reference for policymakers in formulating and enhancing support policies for this area, especially in the wake of the pandemic. Furthermore, the World Bank and HSBC classify Vietnam as a rapidly expanding economy, with an expected growth rate that is the second-highest in Southeast Asia. With the government’s goal of becoming an emerging market by 2025, Vietnam’s stock market is capturing the interest of both domestic and international investors, with the VN-Index sustaining a growth rate of 12% in 2024. Listed logistics companies, in particular, impress with prices increasing by 50% over the same period last year, exceeding the 20% increase of the VN-Index (Lam, 2024). Due to this, these enterprises draw substantial capital from investors, particularly from abroad. In this context, selecting an investment portfolio is a crucial decision for investors. Evaluating enterprises within the same industry can clarify a business’s position in relation to its competitors, categorizing the successful and unsuccessful organizations in this domain. This result will serve as valuable information for investors, in conjunction with economic data, company-specific information, and historical stock data, to inform their decision-making. Moreover, due to the Vietnamese government’s favourable policies promoting logistics development, along with the sector’s rapid growth over the years, there has been a substantial increase in the number of domestic and foreign firms entering the industry. Consequently, to survive and succeed in this competitive environment, logistics companies must continuously analyze the operations and financial efficiency of rivals to strengthen their market position. Comparative performance with industry counterparts elucidates the strengths, weaknesses, opportunities, and challenges of organizations. Based on it, along with insights gained from successful and leading companies, firms will design effective development strategies for the future. So, enterprise performance assessment is significant not only for corporations but also for the logistics sector.

The above analysis shows that the performance assessment of logistics enterprises in Vietnam is essential not only for enterprises and investors but also for policymakers. Therefore, this topic has garnered the interest of researchers in recent years. Wang et al. employed a hybrid multi-criteria decision-making (MCDM) methodology grounded in Industry 4.0 elements to identify the optimal third-party logistics (3PL) provider in Vietnam (Wang and Dang, 2024). In another study, fuzzy MCDM was used to evaluate and select container terminals in Vietnam, utilizing a combination of qualitative and quantitative criteria (Pham et al. 2024). In addition, Nguyen et al. also deployed MCDM to analyze the business performance of seaport enterprises in their study (T.K.L. Nguyen et al. 2024). Moreover, the authors employed data envelopment analysis (DEA) individually or in conjunction with Grey theory to assess and predict the performance of logistics firms in Vietnam in recent studies (Nguyen et al. 2025; P.-H. Nguyen et al. 2024).

Most prior studies assessing the performance of logistics firms in Vietnam have focused on specific subsectors of the logistics system, such as seaports, container terminals, and third-party logistics service providers. These works, while valuable, frequently represent only a fragment of the industry’s entirety. Additionally, financial variables are objective indicators that reveal a firm’s fiscal health and its potential growth. Consequently, assessing the company’s performance through financial indicators guarantees objectivity and effectively evaluates the enterprise’s efficiency. Besides, due to the distinct characteristics of each industry, financial indicators possess varying degrees of significance; therefore, it is essential to account for the weight of these variables during the evaluation process. However, the majority rely on non-financial criteria for evaluation, while others use financial metrics without considering their relative importance. Furthermore, while COVID-19 is viewed as an unexpected disruption that may reveal the genuine abilities of enterprises, it is not considered in these analyses.

Due to the significance and necessity of the topic, as well as the identified research gap, the authors were motivated to undertake this study. The research aims to address a gap in the literature by introducing, for the first time, a three-phase integrated MCDM strategy to evaluate the performance of firms in Vietnam’s logistics industry throughout the pre-, during, and post-pandemic phases. In this paper, the three-phase MCDM method is chosen to ensure the objectivity and comprehensiveness of the evaluation. First, the objective method, CRITIC, is employed to eliminate bias in the criteria weighting process. Subsequently, during the assessment and classification procedure, TOPSIS and EDAS are applied in parallel as a cross-validation strategy to ensure a comprehensive evaluation, based on the evaluating principles of superiority for TOPSIS, and balance and stability for EDAS. The assessment criteria are financial indicators derived accurately from publicly available annual financial statements for the periods from 2019 to 2023, encompassing the periods before, during, and after the COVID-19 pandemic. The highlighted contributions of this research are listed below.

-

(1)

Construct a complete set of financial indicators that precisely reflect the performance of the logistics companies.

-

(2)

This study provides the Vietnamese logistics industry and literature with a comprehensive and objective evaluation of corporations by utilizing multi-criteria decision-making methodologies in three stages. The study enables domestic and foreign stakeholders to understand the performance of logistics companies, making more informed strategic choices. Moreover, the research model can be used effectively in various domains.

-

(3)

Research analyzes businesses across multiple logistics subsectors, enabling the comparison of company performance within and between subsectors, and providing a more comprehensive view of the logistics industry’s performance. Thus, the research helps policymakers, industry associations, and enterprises design competitiveness and sustainability strategies.

-

(4)

Evaluating company performance before, during, and after the COVID-19 pandemic, showing actual corporate health. Additionally, analyzing typical firms to extract lessons from them will provide essential references for firms and policymakers to develop effective strategies and action plans.

The remainder of the paper will be organized as follows: The next section provides a comprehensive literature summary. Section “Methodology” introduces the three-phase methodology. Section “Numerical results” describes the collected companies, corresponding data, and computation results. The discussion is presented in the section “Discussion”. The final section summarizes the study’s findings and future research directions.

Literature review

Corporate performance evaluation refers to the systematic collection and analysis of data to assess the utilization of resources and the production of goods or provision of services (Ersoy, 2017). The assessment of logistics enterprise performance has historically been a significant subject in both academic research and practice. This topic has been extensively studied, with data envelopment analysis (DEA) and multi-criteria decision making (MCDM) being the most commonly employed methodologies. These methods were utilized individually (De Souza et al. 2022; Lee et al. 2023; Meng and Wang, 2022) or in conjunction with other techniques, such as the integration of revised DANP with mean group Utility and VIKOR (Tsai et al. 2024), combining of DEA with machine learning (Cui, 2021), a mixture of AHP and TOPSIS (Ding et al. 2021), and the combination of DEA models (DEA Malmquist method and the epsilon-based measure (EBM)) (Wang et al. 2021). The assessment criteria can be classified as qualitative or quantitative. The quantitative indicators can be categorized into financial and non-financial indices. Qualitative variables are either employed or not in fuzzy set theory. Furthermore, an extensive literature review on the performance evaluation of logistics enterprises in Vietnam reveals studies assessing logistics companies (Nguyen et al. 2025; P.-H. Nguyen et al. 2024) and others evaluating entities within the logistics subsector, including seaports (T.K.L. Nguyen et al. 2024), container terminals (Pham et al. 2024), and third-party logistics (Wang and Dang, 2024). As stated in section “Introduction”, the primary approaches employed are integrated MCDM and DEA. The popularly used evaluation variables are quantitative metrics, encompassing both financial and non-financial data.

Company performance evaluation based on financial metrics has attracted academics due to the objectivity of measurement indicators. There are several techniques for evaluating financial indices, and one commonly used non-parametric approach is data envelopment analysis (DEA). DEA can be used independently or in combination with other methods to enhance measurement efficiency. The Grey relational analysis, in conjunction with DEA, is deployed to analyze a balanced scorecard and rank 35 urban water and sewage companies in Iran (Sarraf and Nejad, 2020). Based on financial data, Deng et al. presented MCDM approaches, including SE-DEA, analytic hierarchy process (AHP), and PROMETHEE II, to assess the performance of Chinese nuclear power-related enterprises. Using SE-DEA to evaluate investment efficiency, PROMETHEE II is applied for ranking and determines the criteria weights by AHP (Deng et al. 2020). In another investigation, Najadat et al. combined the DEA and diverse ensemble creation by oppositional relabeling of artificial training examples (DECORATE) for classifying 53 industrial firms listed on the Amman Stock Exchange, using 11 financial variables as the basis for classification (Najadat et al. 2020).

Simultaneously, multi-criteria decision-making (MCDM) methods are also widely used to assess the performance of financial institutions (Ünvan and Ergenç, 2022) and non-financial enterprises (Abdel-Basset et al. 2020). We can categorize the studies applying MCDM for enterprise evaluation into three groups according to how the criteria’s weights are identified (Heidary Dahooie et al. 2019). The first group assigns equal weights to all rating criteria (ÜNVAN, 2020). The works in the second group employ the subjective judgment of experts to calculate the weights using well-known techniques such as AHP, fuzzy AHP, and fuzzy Decision-Making Trial And Evaluation Laboratory (DEMATEL) (Abdel-Basset et al. 2020; Deng et al. 2020). The final group comprises investigations that apply objective techniques to establish weights based on given quantitative data, such as CRITIC and entropy weighting approaches (Ünvan and Ergenç, 2022; Wu et al. 2022). CRITIC is an MCDM technique popularly applied to determine the weights of measurement criteria (Pamucar et al. 2022). CRITIC examines the intercorrelation among criteria to identify their relative significance (Diakoulaki et al. 1995). CRITIC provides a detailed evaluation of the importance of criteria by creating a correlation matrix and determining the weights of the criteria based on their eigenvalues. This approach is especially beneficial when dealing with correlated factors, as it prevents redundant data. Moreover, the method has been proven to be less computationally intensive than principal component analysis (PCA) in similar situations. As a result, numerous academics have used this method independently or in conjunction with other approaches to identify the weights of financial indicators in company performance evaluation problems (Krishankumar et al. 2022).

Among numerous MCDM approaches, TOPSIS has emerged as a satisfactory method, extensively used in various fields, including business and marketing management, logistics and supply chain management, engineering and manufacturing, human resource management, and other areas. The method was first introduced by Hwang et al. (1981). TOPSIS is also a dominant method in the MCDM approach (Chakraborty, 2022) and is recognized as a straightforward approach for ranking in both theoretical and practical applications (Behzadian et al. 2012). The technique aims to support decision-makers in selecting the best solution from many alternatives with multiple attributes. The proposal of the best solution is based on the distance of the alternative that is not only nearest to the positive ideal solution _ PIS but also furthest from the negative ideal solution_ NIS. Another advantage of TOPSIS is that, despite its simplicity, it can thoroughly solve complicated issues, such as evaluating and ranking problems with interval data (Jahanshahloo et al. 2009). Due to the aforementioned remarkable benefits, many scholars have employed TOPSIS individually or integrated it with other techniques to address business assessment and ranking challenges. Multiple studies utilize TOPSIS in conjunction with various weighting methods, including AHP (Abdel-Basset et al. 2020), Fuzzy AHP (Ban et al. 2020), and Fuzzy DEMATEL (Gayathri et al. 2021), to evaluate the efficiency of enterprises.

Additionally, a combined method of CRITIC and TOPSIS was applied in some studies (Babu Bhumula, 2024; Wang et al. 2024) in which TOPSIS was employed to provide the ranking of alternatives with criteria weighted by CRITIC. Additionally, Ünvan utilizes TOPSIS and fuzzy TOPSIS to evaluate and categorize the top 7 banks in Turkey. The financial indicators are assigned equal weights in the former method, whereas they are assigned different weights in the latter (ÜNVAN, 2020). In recent research, Roy et al. employed the fuzzy-TOPSIS-Sort-C strategy to assess various alternatives. They first determine the criteria weights using the fuzzy-BWM (best-worst method). This article offers the benefit of utilizing financial and non-financial variables for a comprehensive analysis. However, it is still constrained by the influence of human factors when determining the weighting (Roy and Shaw, 2022). Furthermore, several researchers have compared TOPSIS and other approaches in their works (Abdel-Basset et al. 2020). Typically, Türegün compared the Vlse Kriterijumska Optimizacija Kompromisno Resenje (VIKOR) and TOPSIS in assessing Turkey’s tourism businesses using the same entropy weighting technique (Türegün, 2022).

Another method within the category of distance-based MCDM techniques, also widely employed in numerous investigations, is EDAS (Mishra et al. 2020). The EDAS technique was presented by Ke-shavarz Ghorabaee et al. (2015), and has attracted interest from many scholars due to its simplicity and computational efficacy. In contrast to TOPSIS, EDAS rates alternatives by estimating their distances from the average solution across all criteria (Dhumras and Bajaj, 2023). This fundamental idea makes it suitable for scenarios in which decision-makers strive for balanced performance (Wang et al. 2024).

Additionally, COVID-19 presents a real challenge to the health and long-term growth capacity of firms. Consequently, considering this shock is essential in assessing enterprise performance and has been addressed in research (Darzi et al. 2025). Nonetheless, this has not been taken into account in the assessment of logistics enterprises in Vietnam.

In summary, the theoretical underpinnings of this study are rooted in the field of multi-criteria decision-making (MCDM), employing an integrated, three-phase framework designed to provide an objective and comprehensive performance evaluation of listed Vietnamese logistics companies. We propose the CRITIC-support TOPSIS and EDAS framework to multi-perspectively assess the performance of logistics companies listed on two stock exchanges in Vietnam, relying on the analysis of financial data. This recommendation is based on the findings of a comprehensive literature review and aligns with the current research issue. The proposed methodology is structured to address key limitations in prior research by focusing on objective financial indicators, incorporating the relative importance of these indicators, and analyzing performance fluctuations caused by unexpected global shocks, such as the COVID-19 pandemic. Initially, we conduct an in-depth review of relevant studies and get expert viewpoints to determine suitable financial indicators for evaluating the organization’s overall health. Next, the weights of financial indicators are objectively calculated using CRITC without expert views. Ultimately, the TOPSIS and EDAS are employed as a cross-validation to evaluate and classify the assessed businesses. The assessment procedure is conducted in three stages: before, during, and after the pandemic, to investigate fluctuations in the performance of the considered enterprises.

Methodology

Research framework

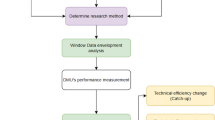

The proposed methodology in this research comprises three interconnected phases that collaborate harmoniously to establish an efficient decision-making procedure, as briefly outlined in Fig. 1. During Phase 1, the evaluation indicators are determined in two steps. First, the authors conduct a comprehensive literature review to assess the significance of the measurement indicators and identify appropriate criteria for this study. Second, in-depth interviews with experts are conducted to guarantee the thoroughness of the assessment index set, taking into account the specific features of the logistics industry in Vietnam. Subsequently, a selection process is implemented to narrow down logistics enterprises in Vietnam for evaluation. These firms are selected based on their scale and transparency of information. Following that, data of the identified assessment criteria and chosen enterprises are gathered from trustworthy sources and ensured to be up-to-date. Phase 1 finishes with constructing a decision matrix that integrates the collected data into a structured matrix. This step provides the initial matrix for determining the weight of the relevant indicators in Phase 2 and the ranking procedure in Phase 3, detailed in sections “Critic weighting method” and “Ranking methods”, respectively.

The framework of the three-layer MCDM method for evaluating the listed Vietnamese logistics companies.

Critic weighting method

In this study, CRITIC is employed to assess the relative importance of each performance indicator for a logistics company. Criteria’s weights are derived solely from numerical data, hence reducing subjective characters. The following steps (Babu Bhumula, 2024; Diakoulaki et al. 1995; Yılmaz et al. 2024) are described to obtain the relative importance of criteria in the study.

Step 1: Defining a decision matrix A of m alternatives and n criteria (Eq. (1))

while i = 1,…, m; j = 1,…,n.

Step 2: Normalize the decision matrix A by Eq. (2) for desirable criteria and Eq. (3) for undesirable criteria.

Step 3: Calculate the standard deviation \({\sigma }_{j}\) of xj to express the contrast intensity of the k criterion.

Step 4: Calculate the correlation coefficient \({r}_{{jk}}\) of each kth criterion by employing rij from the normalized matrix.

Step 5: The amount of information Cj is defined by Eq. (4).

Step 6: The criterion weight is obtained through Eq. (5).

Ranking methods

In Phase 3, two distinct ranking techniques, TOPSIS and EDAS, are employed to assess the performance of logistics firms thoroughly. These two systems have different evaluation concepts; TOPSIS emphasizes superiority, whereas EDAS focuses on the stability and balance of evaluation criteria.

Topsis ranking method

This study employs a combination of CRITIC and TOPSIS methodologies to evaluate the performance of a logistics company, utilizing objective weights for financial indicators. The following steps illustrate the calculation of TOPSIS (Babu Bhumula, 2024; Chakraborty, 2022; Yılmaz et al. 2024) in the study:

Step 1: Create a decision matrix of m alternatives and n criteria, as shown in Eq. (1).

Step 2: To facilitate evaluation, dimensionless units are required. The decision matrix is normalized as follows Eq. (6) to obtain that requirement.

Step 3: A weighted decision matrix is built in this step through Eq. (7)

where \({w}_{{j}}\): the weight of the corresponding criteria derived from CRITIC.

Step 4: PIS and NIS are denoted as A+ and A− and calculated by the following equations:

while,

J: is the desirable attribute.

J−: is the undesirable attribute.

Step 5: Measure the distance from each solution (the separation value) to the positive ideal solution (Gi+) by Eq. (10) and to the negative ideal solution (Gi−) by Eq. (11).

Step 6: The relative closeness to the ideal solution (Di*) of each alternative is revealed here through Eq. (12). The closer Di* to 1 is, the higher the rank of the alternative is.

Edas ranking method

Aiming to diversify the perspective, this study also evaluates and ranks logistics firms by integrating CRITIC and EDAS. This procedure focuses on assessing a firm that performs well consistently across all assessment variables rather than on superiority. The following steps provide a comprehensive outline of the EDAS calculation process.

Step 1: Based on the normalized decision matrix obtained via Eqs. (2) and (3), identify the average solution corresponding to each criterion.

Step 2: Estimate the weighted positive and negative differences (d+and d−) from the average solution using Eqs. (14)–(17).

If jth indicator is the desirable indicator

If jth indicator is the undesirable indicator

Step 3: Calculate the normalized sum of weighted positive and negative differences utilizing Eqs. (18) and (19).

Step 4: Determine the evaluation score for each alternative employing Eq. (20). A higher evaluation score correlates with a superior ranking.

Numerical results

Enterprise selection and evaluation criteria

The study samples comprise enterprises in the logistics sector listed on the two stock exchanges in Vietnam, namely the Ho Chi Minh City Stock Exchange (HoSE) and the Hanoi Stock Exchange (HNX). Currently, in Vietnam, in addition to these two exchanges, there is an Unlisted Public Company Market (UPCom) for companies that are not eligible to list on HoSE and HNX. However, in this study, the authors prioritize exploring alternatives among medium to large-sized firms that are respectable in the logistics industry and financially transparent. Therefore, businesses listed on UPCOM are excluded. The data is extracted from the annual public financial reports following the regulations of the State Securities Commission of Vietnam. In this study, the chosen companies must provide complete data on the determined financial indices from 2019 to 2023, covering the time frame preceding, during, and following the COVID-19 pandemic.

This study considers financial indicators as evaluation criteria, categorized into three groups to assess the enterprise’s overall performance: profitability and operation ratios, leverage, and growth ratios, as presented in Table 1. These criteria are derived from a two-step process that includes a comprehensive review of relevant research and in-depth interviews with experts. The experts involved in this work include one finance professor, one credit institution manager, and three managers from reputable logistics firms in Vietnam. Experts select financial indicators that comprehensively assess the health of enterprises in the logistics industry, relying on their vast expertise and considerable experience in the field.

In the first group, ROA is a metric that measures an enterprise’s ability to generate profits from its assets. It is frequently employed in financial performance evaluation, as it effectively demonstrates asset utilization efficiency. Multiple studies reveal a robust association between effective corporate governance and high ROA (Ho et al. 2018). The next one is the net profit margin (NPM). This index reflects a company’s operational efficiency and cost management by measuring the ratio of net profit to total revenue, expressed as a percentage. According to Delen et al., there is a positive correlation between a company’s performance and its NPM. Implementing efficient cost management strategies and optimizing operations can reduce expenses, resulting in higher profit margins (Delen et al. 2013). The level of NPM differs throughout different industries due to variations in cost structures and competitive dynamics. Molyneux et al. emphasize the influence of market conditions and industry-specific factors on NPM, observing that competitive pressures in particular industries might result in lower profit margins (Molyneux et al. 2019). The last ratio in this group is inventory turnover, which is essential for assessing operational efficiency and the effectiveness of inventory management. Efficient inventory management has a beneficial influence on a business’s overall profitability (Gaur et al. 2005).

Next, within the group of leverage ratios, the current ratio is a key measure for evaluating a company’s short-term liquidity and financial well-being (Kliestik et al. 2020). Companies with higher current ratios are deemed more capable of fulfilling their short-term financial obligations, improving their creditworthiness and overall financial stability. The appropriateness of the current ratio may vary across different sectors. According to Frank and Goyal, enterprises with high levels of debt are more susceptible to economic shocks and fluctuations in interest rates, which can have an adverse effect on their financial performance (Frank and Goyal, 2009). Due to constrained cash flow, high debt might restrict a company’s capacity to invest in growth prospects (Aivazian et al. 2005). The issue of underinvestment may impede the potential for sustained growth and long-term financial gains. Higher debt levels imply lower profitability indicators compared to companies with lower leverage levels (Margaritis and Psillaki, 2010). Besides, the interest coverage ratio (ICR) is a frequently used condition in debt agreements. Covenant violations associated with ICRs might result in loan acceleration, renegotiation, and higher capital expenses (Damodaran, 2011). Strong governance standards, such as having an independent board and an influential audit committee, are associated with improved financial management and reduced financial risk (Campbell et al. 2008). Alessi et al. presented the cyclic pattern of the ICR, demonstrating that it tends to enhance during periods of economic growth and deteriorate during periods of economic decline. The recurring nature of this behavior underscores the importance of having a buffer in the ICR during prosperous periods to protect against economic downturns (Alessi et al. 2021).

The final evaluated category is the growth ratio. The first is the revenue growth index, which is affected by various factors, including market expansion, product innovation, and competitive positioning. Companies that allocate resources to new markets and innovative goods observe an increase in their revenue growth (Srivastava et al. 1998). There is a positive correlation between revenue growth and total financial performance. More sales growth often leads to higher earnings and a higher market valuation. The relationship highlights the significance of strategic growth initiatives (Bharadwaj et al. 1999). Furthermore, the asset growth rate is a crucial metric for understanding a company’s investment and expansion strategy. Financial leverage has a direct effect on the accumulation of assets. Companies with higher leverage can build their assets at a faster rate, as they have greater investment capacity. However, this also entails a greater level of risk (Graham et al. 2005). Positive asset growth is often associated with enhanced financial performance. Companies with higher asset expansion rates usually demonstrate their ability to increase revenue and profit generation (Morck et al. 1988). Another aspect of this group is ROE growth, which is influenced by improvements in profitability, efficient capital management, and effective cost control. Demsetz and Villalonga found that companies with higher ROE growth rates exhibit superior overall financial performance, including increased profitability and higher market returns (Demsetz and Villalonga, 2001). Operational efficiency and smart financial management, such as debt restructuring and equity financing, also help to boost ROE growth (Epps and Cereola, 2008). The last is the P/E growth index, a critical factor in making investment selections. Empirical studies conducted in various marketplaces provide valuable insights into the practical application of P/E growth analysis.

Indicator weighting

In this phase, the CRITIC technique is executed in the following steps to ascertain the weight of financial indicators for each year from 2019 to 2023. Firstly, the (10 × 20) decision matrix is established following Eq. (1) for each year. In the next stage, utilize Eq. (3) for the debt ratio and Eq. (2) for the remaining indices to generate the normalized decision matrix. Then, the standard deviation (std) of each index is determined. Due to page limitations, only the normalized decision matrix in 2019 and the related standard deviation are presented in Table 2. The results indicate that the indicators exhibiting the greatest dispersion are the current and debt ratios, while the lowest variation occurs with the ROE growth rate. It demonstrates a significant distinction across the firms regarding their financial structure and liquidity management. The subsequent years also experienced significant variations in the leverage ratios group and substantial disparity of ROA in 2023. This outcome signifies a considerable difference in the post-pandemic recovery of enterprises.

Subsequently, construct the correlation matrix between the indices, as depicted in Table 3. Finally, the amount of information and the corresponding weight of each criterion are estimated using Eqs. (4) and (5). The weighting procedure is consistent throughout all observation years. Table 4 provides a concise overview of the amount of information and weight of all financial indicators across the years. An indicator containing greater information is considered more significant and has a higher weight.

The CRITIC technique estimates the weight of a variable by analyzing its variation and the level of correlation with other variables. In addition, the values of financial indicators exhibit year-to-year differences due to factors stemming from individual businesses, market conditions, macroeconomic context, and, especially, the impact of COVID-19. Hence, it is reasonable for the criteria weights to undergo significant changes throughout the years.

Performance prioritization

Applying topsis for ranking

According to the framework in Fig. 1, constructing a normalized matrix, as outlined in Equation 6, is the first step in Phase 3. Next, a weighted normalized matrix is created by assigning weights calculated in Phase 2 to each element. Equations (8)–(11) are utilized in the subsequent steps to estimate the distance from the alternatives to the positive and negative ideal points, followed by calculating the performance score and ranking according to Eq. (12), respectively. We follow a consistent procedure for calculation and classification across all observed years. The ranking outcomes from 2019 to 2023 are condensed in Table 5 due to page constraints. The findings indicate that logistics enterprises experienced significant fluctuations in rank before, during, and after the COVID-19 pandemic, with an average standard deviation of 4.6971 and a maximum deviation of 8.0436. In addition, the mean range of oscillations is 3, while the maximum range reaches 19.

In 2019, the top three companies were TOT, VMS, and GMD, respectively, as displayed in Fig. 2. The common features of these three businesses are a decline in ranking between 2020 and 2022, with GMD experiencing the most significant drop. Subsequently, VGP ascended to the top position from seventh in 2020, followed by TOT and TMS. In 2021, VGP experienced a minor decrease in the second position and maintained stability until 2023, while MHC dramatically rose from 14th to the top. Simultaneously, TMS retained its third rank in 2021. In 2022, PRC was evaluated as the highest-ranked enterprise, and DL1 secured a third position. Finally, GMD surprisingly moved to the first position in 2023 after three years in the lowest group of the rankings. Additionally, MHC made a significant breakthrough and jumped to the 3rd rank in the same year. On the other hand, the businesses ranked lowest over the years are in the sequence: STG, PJT, PRC, MHC, and DL1. Except for PRC and MHC, which show significant annual variations, the remaining companies exhibit average ranking fluctuations.

Applying the TOPSIS to evaluate and rank the listed Vietnamese logistics enterprises from 2019 to 2023.

Figure 3 displays a group of businesses that exhibit relatively stable rankings among the enterprises under consideration, with a mean standard deviation of 2.3607. Thirty percent of the ranked companies belong to this category. Among them, PVP is the most steady, with a standard deviation of 1.6432 and a fluctuation range of 3, followed by TOT and VGP.

Includes companies with a slight ranking change from 2019 to 2023.

In contrast, Fig. 4 highlights that 20% of evaluated businesses experience significant variations in rankings throughout the years. PRC has the most significant standard deviation of 8.0436, while the lowest is 7.2594, belonging to TMS. The variations in the ranking of each business over the years differ from those of other enterprises. However, when examining the period following COVID-19 in Vietnam, specifically from 2022 to 2023, the firms in this group could be categorized into three distinct patterns of variation. The first trend is to increase aggressively in 2022 but lose rankings in the next year, as seen with PRC. On the contrary, the second tendency is a significant drop in ranking in 2022, followed by a quick rise in 2023, as seen with MHC and TMS. GMD is the remaining case, maintaining rank in 2022 while making a breakthrough in 2023.

Includes firms with significant rating swings from 2019 to 2023.

Applying EDAS for ranking

In the EDAS phase, the average solutions for all indicators are initially computed from the normalized decision matrix utilizing Eq. (13). Then, based on the weights of the criteria obtained in Phase 2, the weighted positive and negative distances from the average solutions are determined using Eqs. (14)–(17). The subsequent step involves calculating the normalized sum of the weighted positive and negative distances employing Eqs. (18) and (19). Finally, each organization’s evaluation score and ranking are estimated using Eq. (20). The ranking outcomes of logistics firms from 2019 to 2023, corresponding to before, during, and after COVID-19, are assessed using the same process and depicted in Fig. 5.

Applying the EDAS to evaluate and rank the listed Vietnamese logistics enterprises from 2019 to 2023.

In 2019, the two companies with the highest performance were TOT and VGP, respectively. In 2020, when the pandemic broke out in Vietnam, VGP and TOT swapped positions, with VGP becoming the best company before declining slightly to second place in 2021, while MHC jumped to the highest rank. In the post-COVID-19 recovery period, from 2022 to 2023, VGP maintained the top position, while PRC and MHC occupied the second position in the corresponding years. On the opposite side, the worst ranking was held by PTS, PRC, PSC, and PJT, respectively, corresponding to each investigation year, with PSC continually occupying the lowest position from 2021 to 2022.

Among the assessed alternatives, 20% of enterprises exhibit stable rankings over the years, with an average standard deviation of 1.65, as illustrated in Fig. 6. Among them, VGP distinguishes itself with the least fluctuation, followed by PSC with corresponding standard deviations of 0.55 and 1.52. Specifically, these are the two companies that fall into the best and worst groups during the observation period. Conversely, some businesses experienced significant fluctuations in rankings before, during, and after the pandemic, with the most notable variation being PRC, as displayed in Fig. 7. Throughout the pre- and during-COVID-19 eras, PRC was consistently ranked among the bottom three companies. However, after the pandemic ended, the company jumped remarkably to second place in 2022, followed by a slight drop to fourth place in 2023.

Includes companies with a slight ranking change from 2019 to 2023.

Includes firms with significant rating swings from 2019 to 2023.

Discussion

The aforementioned ranking results indicate differences between TOPSIS and EDAS due to their distinct foundational principles. TOPSIS assesses alternatives based on distance to the ideal value, whereas EDAS focuses on proximity to the average value. Nevertheless, the disparity in outcomes between the two approaches is not significant for most enterprises. Notably, there is consistency between the two approaches in the highest position across all years of observation. This finding suggests that the leading firm not only excels but also demonstrates stability and equilibrium across all key criteria. Furthermore, this similarity shows that the criteria’s weights are precisely established, representing the actual impact of each variable on total efficacy. Additionally, a few enterprises reveal substantial discrepancies in the evaluation results of the two proposed techniques. An illustrative case is the PRC’s ratings in 2019, which are 5 according to TOPSIS and 19 according to EDAS. This outcome implies that PRC excels in specific important criteria but is uneven in performance related to the other indicators. Besides, the interval from 2020 to 2022 witnessed a greater similarity in the results of the two methods compared to 2019 and 2023. This phenomenon implies that prior to the pandemic, certain businesses demonstrated excellence in some crucial indicators. However, this noticeable superiority was absent during COVID-19 and the subsequent period. By 2023, some companies demonstrated exceptional performance in certain variables again.

Analyzing the ranking fluctuations of evaluated businesses reveals that the pandemic period (2020-2021) exhibited the least variability, whereas the intervals during and following COVID-19 (2021–2022) demonstrated the highest volatility. This conclusion is consistent in TOPSIS and EDAS methods with average standard deviations of (2.828, 4.172) and (2.192, 3.253), respectively. According to the evaluation results of the two proposed methods, each business has different fluctuations in ranking across the observed years. Among them, GMD and TMS emerge as the most volatile businesses, with an impressive recovery following COVID.

GMD aims to meet international standards, optimize operations, and mitigate environmental repercussions. GMD has invested in digital transformation projects such as the smart port, smart gate, river gate software, etc. These investments have substantially enhanced productivity, decreased time and costs, and saved energy. Furthermore, GMD enhances the utilization of sustainable energy sources within the company’s ecosystem. At the SCSC airport terminal and Mekong Logistics cold storage, solar energy currently replaces about 30–40% of annual grid electricity use. Additionally, GMD has established a robust risk management system consisting of three independent lines of defense and reciprocal oversight: (i) Risks are identified and controlled by production and business departments from the beginning. (ii) The enterprise, through functional departments, formulates regulations and policies and oversees adherence to them. (iii) Internal audit and operational audit programs focus on essential risks. GMD has successfully overcome a challenging period through adaptive and efficient methods, ultimately emerging as the foremost among considered enterprises.

In addition, TMS drives its growth towards sustainable development by using green logistics services and adhering to ESG standards. In an effort to reduce greenhouse gas emissions, this company has operated five solar power projects throughout its branches, with an average annual capacity of 7164 MWh. Additionally, to save expenses and optimise resources while enhancing service quality, TMS has executed digital transformation initiatives, including Transimex SPro and SFlash. Furthermore, TMS has employed other methods, such as diversifying services and developing advanced storage and distribution solutions, to recover and develop after COVID-19. Nevertheless, the two aforementioned strategies are crucial and decisive for the successful recovery of the enterprise.

Additionally, the study’s results show consistency with market realities; for instance, GMD’s ranking in the leading group in 2023 is entirely consistent with reality, as this company is also recognized by the stock market and the logistics industry as one of the leading enterprises (Giang, 2023). This result demonstrates that the proposed model not only possesses scientific value but also accurately reflects the industry’s actual situation, thereby further enhancing the reliability and applicability of the research results.

Managerial implications

COVID-19 is a significant test for Vietnam’s enterprises, particularly those in the logistics sector. The research findings highlight some significant strategic implications for stakeholders: (1) Logistics firms must proactively develop a digital transformation strategy to decrease costs, increase operational efficiency, and improve customer service, particularly in the context of expanding e-commerce. Furthermore, pursuing sustainable development objectives will help firms reduce costs, enhance their reputation, and meet international standards as they integrate into the global economy. (2) For the government and policy makers: The research results reinforce the importance of policies to support and encourage digital transformation in logistics. Issuing and maintaining these policies will motivate businesses to enhance their competitiveness, thereby contributing to the overall economic development. (3) Information on the performance and strategy of logistics organisations allows investors to analyse and select the optimal companies that can adapt, recover, and grow strongly following the pandemic shock. Finally, in terms of methodology, combining TOPSIS and EDAS results in an effective cross-validation procedure. TOPSIS emphasises the superiority of each alternative, whereas EDAS focuses on the balance and stability. This integration enables stakeholders to gain a more comprehensive view, leading to more informed and trustworthy decisions.

Conclusion

Evaluating company performance is crucial for various stakeholders, including investors, the assessed companies and policy makers. By analyzing assessment results, investors succeed in effectively choosing and optimizing portfolios. Meanwhile, enterprises recognize their position within the industry and adjust their strategies accordingly to enhance competitiveness. Additionally, policymakers can obtain essential reference material to formulate supporting policies for logistics firms. Moreover, assessing businesses’ performance before, during, and after the COVID-19 pandemic is vital to evaluating their ability to adapt, recover, and grow. As a result, for the first time, this study assesses the performance of listed logistics companies in Vietnam using financial metrics and analyzes fluctuation in ranking before, during, and following the pandemic.

To conduct a comprehensive evaluation, the authors thoroughly reviewed the literature and incorporated in-depth expert opinions to establish a set of financial criteria for assessment. Subsequently, the CRITIC approach is employed to determine the weights for the respective indices, thereby eliminating the impact of human subjective judgments. The ultimate ranks in the present study were cross-validated employing two distance-based MCDM methodologies (EDAS and TOPSIS). The research findings reveal differences in the ranking results obtained using TOPSIS and EDAS techniques, which stem from the distinct evaluation concepts employed by the two approaches. Nevertheless, this disparity is not significant, and especially, there exists a consistency in the rating between the two approaches in the best position. Particularly, TOPSIS and EDAS classify the best company each year as follows: TOT, VGP, MHC, PRC, and GMD; TOT, VGP, MHC, VGP, and VGP; correspondingly.

The logistics industry in Vietnam has faced a significant challenge posed by COVID-19. However, this crisis has also opened up new opportunities, with a surge in demand for e-commerce. Consequently, logistics businesses must undertake digital transformation to adapt and thrive in this landscape. Along with the Vietnamese government’s efforts to boost infrastructure investment and implement policies that promote the logistics industry, businesses that are agile and flexible in digital transformation have succeeded in recovering and developing. They have also focused on sustainable development and invested in new technology to reduce costs, enhance operational efficiency, improve customer service, and manage risk effectively. Among the approaches, digital transformation and sustainable growth remain key strategies. Despite numerous challenges, Vietnam’s logistics sector remains a key focus for investors, particularly foreign investors. With this research, the authors have provided a valuable analysis of the logistics industry in Vietnam, providing useful insights for investors and other stakeholders. Another highlight of the study is that, based on trustworthy data and objective methodologies, the authors have comprehensively assessed the businesses from different perspectives of excellence and stability.

Although this study has offered novel insights into the performance of logistics firms in Vietnam through the 3-phase MCDM method across the pre-, during-, and post-COVID-19 periods (2019–2023), certain limitations persist. First, the analysis only focuses on financial indicators. Financial indicators comprehensively reflect a business’s financial well-being and are commonly used to evaluate and rank enterprises in various research projects. However, they do not entirely reflect the multidimensionality of competitiveness in the logistics industry. In the current context, the extent of digital transformation, the capacity to deliver green logistics services, and adherence to ESG standards are significant factors influencing the competitiveness and sustainable development of firms in this sector. Second, the research data predominantly concentrate on enterprises listed on the stock exchange and publishing transparent financial reports, thereby excluding the small and medium-sized enterprises (SMEs) sector, which possesses distinct operational characteristics.

From these limitations, future research directions can be pursued in several ways. The first is to integrate financial indicators with non-financial criteria—such as extent of digital transformation, capacity to deliver green logistics services, and adherence to ESG standards—to construct a more comprehensive assessment framework. Another is to expand the data scope to include logistics SMEs, thereby providing a more thorough reflection of the industry landscape and facilitating the analysis of performance among different size categories. Finally, the implementation of the methodology suggested in this study across various domains is feasible in subsequent research.

Data availability

The data that support the findings of this study are available from the corresponding author upon reasonable request.

References

Abdel-Basset M, Ding W, Mohamed R et al. (2020) An integrated plithogenic MCDM approach for financial performance evaluation of manufacturing industries. Risk Manag 22(3):192–218. https://doi.org/10.1057/s41283-020-00061-4

Aivazian VA, Ge Y, Qiu J (2005) The impact of leverage on firm investment: Canadian evidence. J Corp Financ 11(1-2):277–291

Alessi L, Bruno B, Carletti E et al. (2021) Cover your assets: non-performing loans and coverage ratios in Europe. Econ policy 36(108):685–733

Babu Bhumula K (2024) Using CRITIC-TOPSIS and Python to examine the effect of 1-Hepatnol on the performance and emission characteristics of CRDI CI engine with split injection. Heliyon 10(11):e31484

Ban AI, Ban OI, Bogdan V et al. (2020) Performance evaluation model of Romanian manufacturing listed companies by fuzzy AHP and TOPSIS. Technol Econ Dev Econ 26(4):808–836

Behzadian M, Otaghsara SK, Yazdani M et al. (2012) A state-of the-art survey of TOPSIS applications. Expert Syst Appl 39(17):13051–13069

Bharadwaj AS, Bharadwaj SG, Konsynski BR (1999) Information technology effects on firm performance as measured by Tobin’s q. Manag Sci 45(7):1008–1024

Campbell JY, Hilscher J, Szilagyi J (2008) In search of distress risk. J Financ 63(6):2899–2939

Chakraborty S (2022) TOPSIS and Modified TOPSIS: a comparative analysis. Decis Anal J 2:100021

Cui H (2021) Performance evaluation of logistics enterprises based on non-radial and non-angle network SBM model. J Intell Fuzzy Syst 40(4):6541–6553

Damodaran A (2011) Damodaran on valuation: security analysis for investment and corporate finance. John Wiley & Sons

Darzi MA, Ahmadi S, Shokouhyar S (2025) Cross-cultural ranking of cellphone life cycle issues for strategic CSR marketing with social media-based AHP. Environ Dev Sustain 27(2):3201–3232

De Souza E, Kerber J, Bouzon M et al. (2022) Performance evaluation of green logistics: paving the way towards circular economy. Clean Logist Supply Chain 3:100019

Delen D, Kuzey C, Uyar A (2013) Measuring firm performance using financial ratios: a decision tree approach. Expert Syst Appl 40(10):3970–3983

Demsetz H, Villalonga B (2001) Ownership structure and corporate performance. J Corp Financ 7(3):209–233

Deng Y, Zou S, You D (2020) Financial performance evaluation of nuclear power-related enterprises from the perspective of sustainability. Environ Sci Pollut Res. 27:11349–11363

Dhumras H, Bajaj RK (2023) Modified EDAS method for MCDM in robotic agrifarming with picture fuzzy soft Dombi aggregation operators. Soft Comput 27(8):5077–5098. https://doi.org/10.1007/s00500-023-07927-1

Diakoulaki D, Mavrotas G, Papayannakis L (1995) Determining objective weights in multiple criteria problems: the critic method. Comput Oper Res 22(7):763–770

Ding J-F, Hsu C-T, Chou M-T et al (2021) A qualitative-quantitative fuzzy evaluation model for selecting an international ocean freight logistics provider. Int J Marit Eng 163(A4):89

Epps RW, Cereola SJ (2008) Do institutional shareholder services (ISS) corporate governance ratings reflect a company’s operating performance? Crit Perspect Account 19(8):1135–1148

Ersoy N (2017) Performance measurement in retail industry by using a multi-criteria decision making methods. Ege Acad Rev 17(4):539–551

Frank MZ, Goyal VK (2009) Capital structure decisions: which factors are reliably important? Financ Manag 38(1):1–37

Gaur V, Fisher ML, Raman A (2005) An econometric analysis of inventory turnover performance in retail services. Manag Sci 51(2):181–194

Gayathri C, Kamala V, Gajanand MS et al. (2021) Analysis of operational and financial performance of ports: an integrated fuzzy DEMATEL-TOPSIS approach. Benchmarking: Int J 29(3):1046–1066. https://doi.org/10.1108/BIJ-03-2020-0123

Giang H (2023) Attractive investment opportunities with logistics stocks. https://tapchikinhtetaichinh.vn/co-hoi-dau-tu-hap-dan-voi-co-phieu-logistics.html. Accessed 15 June 2024

Graham JR, Harvey CR, Rajgopal S (2005) The economic implications of corporate financial reporting. J Account Econ 40(1-3):3–73

GSO (2023) Sea Transportation continues to improve in the first 2 months of 2023. https://www.gso.gov.vn/tin-tuc-thong-ke/2023/03/van-tai-bien-tiep-tuc-khoi-sac-trong-2-thang-dau-nam-2023/#:~:text=Theo%20Quy%E1%BA%BFt%20%C4%91%E1%BB%8Bnh%20n%C3%A0y%2C%20danh%20m%E1%BB%A5c%20c%E1%BA%A3ng%20bi%E1%BB%83n,t%C3%A0u%20c%C3%B3%20tr%E1%BB%8Dng%20t%E1%BA%A3i%20l%E1%BB%9Bn%20ng%C3%A0y%20c%C3%A0ng%20nhi%E1%BB%81u. Accessed 15 June 2024

Heidary Dahooie J, Zavadskas EK, Vanaki AS et al. (2019) A new evaluation model for corporate financial performance using integrated CCSD and FCM-ARAS approach. Econ Res.-Ekon Istraž 32(1):1088–1113. https://doi.org/10.1080/1331677X.2019.1613250

Ho KLP, Nguyen CN, Adhikari R et al. (2018) Exploring market orientation, innovation, and financial performance in agricultural value chains in emerging economies. J Innov Knowl 3(3):154–163

Huang YL (2009) Prediction of contractor default probability using structural models of credit risk: an empirical investigation. Constr Manag Econ 27(6):581–596

Hwang C-L, Yoon K, Hwang C-L et al (1981) Basic concepts and foundations. In: Multiple attribute decision making: methods and applications: a state-of-the-art survey. pp 16–57

Jahanshahloo GR, Lotfi FH, Davoodi A (2009) Extension of TOPSIS for decision-making problems with interval data: Interval efficiency. Math Comput Model. 49(5–6):1137–1142

Keshavarz Ghorabaee M, Zavadskas EK, Olfat L et al. (2015) Multi-criteria inventory classification using a new method of evaluation based on distance from average solution (EDAS). Informatica 26(3):435–451

Kliestik T, K Valaskova K, Lazaroiu G et al (2020) Remaining financially healthy and competitive: the role of financial predictors. J Compet (1)

Krishankumar R, Pamucar D, Pandey A et al. (2022) Double hierarchy hesitant fuzzy linguistic information based framework for personalized ranking of sustainable suppliers. Environ Sci Pollut Res 29(43):65371–65390. https://doi.org/10.1007/s11356-022-20359-y

Lam M (2024) Why did the stock price of Logistics and Industrial Parks increase by 50%? Vietnam Econ Financ Rev https://tapchitaichinh.vn/vi-sao-gia-co-phieu-nhom-nganh-logistics-va-khu-cong-nghiep-tang-toi-50.html#

Lee PF, Lam WS, Lam WH (2023) Performance evaluation of the efficiency of logistics companies with data envelopment analysis model. Mathematics 11(3):718

Margaritis D, Psillaki M (2010) Capital structure, equity ownership and firm performance. J Bank Financ 34(3):621–632

Meng J, Wang S (2022) The performance evaluation of logistics enterprises in online supply chain finance based on analytic hierarchy process. Math Probl Eng 2022(1):8393223

Mishra AR, Mardani A, Rani P et al. (2020) A novel EDAS approach on intuitionistic fuzzy set for assessment of health-care waste disposal technology using new parametric divergence measures. J Clean Prod 272:122807. https://doi.org/10.1016/j.jclepro.2020.122807

MOF (2023) Vietnam logistics industry: developing technology and increasing value services. https://mof.gov.vn/webcenter/portal/btcvn/pages_r/l/tin-bo-tai-chinh?dDocName=MOFUCM279461 Accessed 15 June 2024

MOIT (2020) Vietnam logistics market report, September 2020. https://logistics.gov.vn/nghien-cuudao-tao/bao-cao-thi-truong-logistics-viet-nam-so-thang-9-2020 Accessed 15 June 2024

Molyneux P, Reghezza A, Xie R (2019) Bank margins and profits in a world of negative rates. J Bank Financ 107:105613

Morck R, Shleifer A, Vishny RW (1988) Management ownership and market valuation: an empirical analysis. J Financ Econ 20:293–315

Najadat H, Al-Daher I, Alkhatib K (2020) Performance evaluation of industrial firms using DEA and DECORATE ensemble method. Int Arab J Inf Technol 17(5):750–757. https://doi.org/10.34028/iajit/17/5/8

Nguyen NT, Nguyen DKT, Tran TT (2025) Application of DEA model and Grey system theory to analyze and forecast business performance of logistics enterprises in Vietnam. Grey Systems: Theory andApplication 15(4):709–731

Nguyen P-H, Nguyen L-AT, Nguyen T-HT et al (2024) Evaluating the Vietnamese logistics companies using the DEA-Malmquist model. In: International conference on artificial intelligence on textile and apparel

Nguyen TKL, Le HN, Ha BD et al. (2024) Evaluating the business performance of seaport enterprises in Vietnam. Sustainability 16(19):8576

NIF (2017) By 2025, logistics services contribution to GDP reaches 8–10%. https://mof.gov.vn/webcenter/portal/vclvcstc/pages_r/l/chi-tiet-tin?dDocName=MOFUCM096861 Accessed 15 June 2024

Pamucar D, Žižović M, Đuričić D (2022) Modification of the CRITIC method using fuzzy rough numbers. Decis Mak: Appl Manag Eng 5(2):362–371. https://doi.org/10.31181/dmame0316102022p

Pham TY, Truong NC, Nguyen PH et al. (2024) The fuzzy MCDM for container terminal choice in Vietnam from shipping lines’ perspective based on cumulative prospect theory. Asian J Shipp Logist 40(3):147–156

Roy PK, Shaw K (2022) An integrated fuzzy credit rating model using fuzzy-BWM and new fuzzy-TOPSIS-Sort-C. Complex Intell Syst. https://doi.org/10.1007/s40747-022-00823-5

Sarraf F, Nejad SH (2020) Improving performance evaluation based on balanced scorecard with grey relational analysis and data envelopment analysis approaches: case study in water and wastewater companies. Eval Program Plan 79:101762

Srivastava RK, Shervani TA, Fahey L (1998) Market-based assets and shareholder value: a framework for analysis. J Mark 62(1):2–18

Sun J, Li J, Fujita H et al. (2023) Multiclass financial distress prediction based on one‐versus‐one decomposition integrated with improved decision‐directed acyclic graph. J Forecast 42(5):1167–1186

Tsai J-F, Tran D-H, Wang C-P et al. (2024) Performance evaluation of logistics service providers under uncertain environment using a rDANP-U model. Stud Inform Control 33(3):61–71

Türegün N (2022) Financial performance evaluation by multi-criteria decision-making techniques. Heliyon 8(5):e09361

ÜNVAN YA (2020) Financial performance analysis of banks with TOPSIS and fuzzy TOPSIS approaches. Gazi Univ J Sci 33(4):904–923

Ünvan YA, Ergenç C (2022) Financial performance analysis with the fuzzy COPRAS and entropy-COPRAS approaches. Comput Econ 59(4):1577–1605

Wang C-N, Dang T-T (2024) Third-party logistics provider selection in the Industry 4.0 era by using a fuzzy AHP and fuzzy MARCOS methodology. IEEE Access 12:67291–67313

Wang C-N, Nguyen N-A-T, Fu H-P et al. (2021) Efficiency assessment of seaport terminal operators using DEA Malmquist and epsilon-based measure models. Axioms 10(2):48

Wang C-N, Nhieu N-L, Chiang C-T et al. (2024) Assessing Southeast Asia countries’ potential in the semiconductor supply chain: an objectively weighting multi-criteria decision-making approach. Humanit Soc Sci Commun 11(1):1–17

Wang C-N, Nhieu N-L, Liu W-L (2024) Unveiling the landscape of Fintech in ASEAN: assessing development, regulations, and economic implications by decision-making approach. Humanit Soc Sci Commun 11(1):1–16

Wu Q, Liu X, Qin J et al. (2022) An integrated generalized TODIM model for portfolio selection based on financial performance of firms. Knowl-Based Syst 249:108794. https://doi.org/10.1016/j.knosys.2022.108794

Yılmaz S, Güllü İ, Susuz A et al. (2024) Assessment of service quality in aviation using the CRITIC-supported TOPSIS method: a case study of Central Airports in Asia. J Aviat 8(1):56–65

Acknowledgements

It is an honor to express our thankfulness for the helpful comments and feedback received from anonymous Reviewers and Editors. No specific funding was provided to the authors for this study. This research is partially supported by the project of NSTC 114-2637-E-992-010 from the National Science and Technology Council, Taiwan.

Author information

Authors and Affiliations

Contributions

All authors contributed to the study’s conception and design. Material preparation, data collection, and analysis were performed by Tram Thi Mai Nguyen and Thien Dinh Nguyen. The first draft of the manuscript was written by Chia-Nan Wang, Yu-Chi Chung, and Thi Thanh Tam Nguyen. All authors commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval is not applicable because the study does not involve human participants.

Informed consent

This article does not contain any studies with human participants conducted by the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Wang, CN., Nguyen, T.T.M., Chung, YC. et al. Performance evaluation of listed Vietnamese logistics companies in the pre-, during, and post-COVID-19 based on a three-layer MCDM method. Humanit Soc Sci Commun 13, 43 (2026). https://doi.org/10.1057/s41599-025-06266-w

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-06266-w