Abstract

Research on the impact of financial agglomeration on CO2 emissions is a vital avenue for advancing CO2 emissions reduction and aligning with the Sustainable Development Goals set forth by the United Nations. However, few studies have investigated the dynamic spatial spillover effect of financial agglomeration on CO2 emissions, and the concepts of “time inertia” and “spatial spillover effect” about CO2 emissions have received limited attention. To address this gap, we used provincial panel data from 30 provinces in China from 2006 to 2019. We employed the entropy method to measure the level of financial accumulation, constructed a dynamic spatial Durbin model, and analyzed the “time inertia” and “spatial spillover effects” of CO2 dioxide emissions in Chinese provinces. Additionally, we explored the dynamic spatial spillover effects of financial agglomeration on CO2 emissions. We examined the transmission mechanism of the impact of financial agglomeration on CO2 emissions through energy consumption and technology market development. The results show that CO2 emissions exhibit significant “time inertia” and “space spillover” effects and considerable regional differences. Financial agglomeration levels positively impact reducing CO2 emissions in the short and long term. Through two intermediary paths of energy consumption and technology market development, financial agglomeration can indirectly reduce CO2 emissions. Our research effectively provides information and serves as a decision-making reference for policy planning related to CO2 emissions reduction, especially in countries with high CO2 emissions, particularly developing nations.

Similar content being viewed by others

Introduction

Since the reform and opening up, China’s reform economy has developed rapidly. However, this development has been accompanied by highly polluting and energy intensive, resulting in ongoing issues such as CO2 emissionsFootnote 1 climate warming, and resource pollution. These environmental challenges not only impede economic progress but also have a profound impact on human society. It is also the biggest emitter of CO2 in the world, China recognizes the need to address environmental concerns, including CO2 and climate change. Therefore, during the general debate of the seventy-fifth session of the UN General Assembly, the Chinese government pledged to intensify its intended contributions and implement more effective policies and measures. China will be at the peak of its CO2 emissions by 2030 and on track for CO2 neutrality by 2060.

Financial agglomerationFootnote 2 refers to the rapid spatial concentration of the financial industry, guided by national policies and taking into account regional economic development, resource endowment, and location conditions (Zhou and Lin, 2020). In essence, FA entails the formation of a financial center resulting from spatial concentration within a specific region during the financial industry’s development (Jiang, 2020). Dynamic spatial spillover effect occurs when an activity, especially one involving a substance with spatial mobility, impacts neighboring regions as it is carried out within a particular area. For example, an increase in CO2 in Hebei Province leads to an increase in CO2 in the Neighboring provinces of Henan, Shandong, and Shanxi. This phenomenon exemplifies a dynamic spatial spillover effect.

As the financial industry continues to develop, a financial center develops within a particular region, creating an FA effect. Improving the level of FA can not only cut CO2 within the region but also reduce CO2 in Neighboring. This is called the dynamic spatial ripple effect of financial conurbation on CO2. In relevant studies, it is believed that there is an interactive correlation between the agglomeration of financial centers and CO2, both of which demonstrate a trend of spatial convergence. Short- and long-term FA can reduce CO2 intensity within the spatial domain, demonstrating a spatial-temporal locking effect (Yan et al., 2022). FA decreases the CO2 footprint in central cities and their surrounding areas, enhancing the regional level of green development and producing spatial spillover effects (Yuan et al., 2019).

Most of the studies on financial agglomeration and carbon emissions have focused on qualitative research, with fewer related quantitative studies and different conclusions. One is about the single linear effect of financial agglomeration on carbon emissions. At the beginning of the economy, economic development increases environmental pollution, but when the economy develops to a certain extent, the environmental pollution will be improved (Kijima et al., (2010)). Some studies have shown that financial development is beneficial to reducing a country’s total carbon dioxide emissions (Ozturk and Acaravci, 2013). The carbon emission effect of regional urbanization in China is to establish a balance between urbanization and relevant regional factors for low-carbon technology innovation (Niu, Lekse (2018)). Further, the carbon emission reduction and the economic impact of capital investment restriction policy on China’s industrial structure adjustment under the macro level is proposed, which confirms that the national investment restriction policy on high energy-consuming industries effectively promotes industrial structure adjustment and has significant carbon reduction effect (Gu and Wang, 2018). The second is about the nonlinear impact of financial agglomeration and carbon emissions. With the increasing level of financial development, the impact on carbon emissions and environmental pollution has an inverted U-shaped nonlinear relationship. A nonlinear relationship between economic agglomeration and urban environmental pollution emissions is found in Chinese city data (Yang, 2016). There is also a nonlinear relationship between industrial agglomeration and carbon emissions, and studies have shown that industrial agglomeration and carbon emissions in environmental pollution show an “inverted U-shaped” curve characteristic (Huang and Wang, 2016). According to the spatial mechanism of spatial agglomeration on carbon dioxide emissions, the analysis shows that there is an inverted U-shaped nonlinear relationship between agglomeration and carbon dioxide emissions and environmental pollution will inhibit the formation of agglomeration (Zhu et al., 2020; Yan et al., 2021).

The studies on the link between FA and CO2, as well as environmental pollution in the above literature are insufficient. There are still the following deficiencies: (1) Further discussion and research are required due to differences in the selection and calculation of FA indicators. (2) To study the impact of FA on CO2 and its spatial spillovers, most researchers only use static panel models and static SDM. They were unable to decompose the long-term and short-term spatial spillover effects, and could not identify the “time inertia” and “spatial spillover effects” of CO2. (3) The effect of FA on CO2 can be easily influenced by other social and economic factors. Yet, few studies pay attention to the mechanism of FA on CO2. They did not analyze the difference in the effect of FA on the CO2 in the different areas. The transmission mechanism of FA on CO2 and the regional variations in the impact of FA on CO2 still require further analysis. At the same time, China currently holds the highest position in global CO2. As a country with increasing CO2 globally, it holds great practical significance to study how to effectively reduce the CO2 of China.

Based on the importance of the questions listed above, we have conducted the following research: (1) From the point of view of financial accumulation, we constructed a dynamic spatial Durbin (SDM) model to study the spatial spillover effect of the agglomeration of financial centers on CO2. (2) We analyzed the “time inertia” and “space spillover effect” of CO2, decomposed the long-term and short-term effects, and provided policy suggestions for achieving a low-CO2 economy. (3) Considering whether FA has indirect effects on CO2, we incorporated energy consumption and technology market development into the theoretical framework of the study on linking financial conurbation to CO2. We built an intermediary effect model for the study of the transmission mechanism between energy consumption and technology market development.

We found that: (1) China’s CO2 shows a positive spatial spillover effect, meaning that CO2 in the same area during the previous period leads to increasing CO2 in the subsequent period. Simultaneously, increased CO2 in the same region leads to increased emissions in neighboring regions. (2) The spatial spillover of CO2 can be reduced through FA, indicating that FA significantly inhibits both local and nearby CO2. (3) Higher levels of FA can positively impact CO2 through reductions in energy consumption and improvements in technology development.

To address the issues about the relationship between economic development and environmental pollution, and at the same time centering on this central theme of the impact of financial agglomeration on carbon reduction in China at this stage, the marginal contributions of this paper are as follows. First, from quantitative analysis, we construct a financial agglomeration evaluation index system based on the four dimensions of financial scale, density, depth, and development, measure the level of financial agglomeration in 30 provinces across the country from 2006 to 2019, and analyze the development characteristics and regional differences presented by the measurement results. Second, based on the measurement, the key facilitating factors for carbon reduction are further analyzed, and it is clarified at the theoretical level how financial agglomeration, energy consumption, and technology market development can contribute to the reduction of carbon emissions in China. Third, we analyze the effects of financial agglomeration on carbon reduction at the national level and from a regional perspective, and discuss the results of the spatial effects, to put forward targeted recommendations for further carbon emission reduction and environmental protection and development.

Research hypothesis

Financial agglomeration and CO2 emissions

With the development of the financial industry, various provinces gradually exhibit significant FA characteristics, which strongly impact enterprise production, people’s lives, and the environment. FA can promote factor sharing, foster industrial agglomeration, reduce time and transportation costs, enhance efficiency, conserve energy, and lower CO2. Liu et al. (2024) studied the impact of financial agglomeration on carbon emissions, and the results showed that financial agglomeration has an “energy-saving effect” on carbon emissions in the agricultural sector. Liu et al. (2017) emphasized that spatial economic agglomeration represents a vital avenue for altering CO2 productivity. Diverse agglomeration models contribute to improved CO2 productivity, reduce energy consumption, and, consequently, lower CO2. Qu et al. (2020) studied the relationship between financial agglomeration and energy efficiency, and the study shows that financial agglomeration affects energy efficiency through the scale economy effect, innovation driving effect, information spillover effect and structural adjustment effect, better energy saving and emission reduction, green and sustainable development. Mahmood (2020) studied the determinants of per capita carbon dioxide emissions in 21 North American countries and found that per capita carbon dioxide emissions are spatially dependent, and financial market development and trade openness have an inverted U-shaped relationship with per capita carbon dioxide emissions. Zhang et al., 2024 green finance agglomeration can improve China’s carbon emission performance, and enhance the impact of carbon emission performance through capital formation, energy transition, and technological progress. As a result, hypothesis H1 is posited in this paper.

H1: Financial agglomeration can reduce CO2 emissions.

Financial agglomeration, energy consumption, and CO2 emissions

The agglomeration of financial centers accelerates the development of the tertiary sector and the optimization of the industrial structure increases the output value of the tertiary industry, reduces the heavy industry production that causes pollution to the environment, and lowers the energy consumption of heavy industry enterprises, primarily coal-based, resulting in reduced CO2. Wang and Xiang (2014) proposed that industrial structure adjustment should encourage the rationalization and modernization of the industrial structure, thereby reducing energy consumption in production and CO2. Xu et al. (2014) suggestion advocates for the management and mitigation of CO2 through the “modification of methods and the adjustment of structure.” Fitriyah (2019) delves into the interconnection among financial development, energy consumption, and CO2 in the context of Indonesia, showing that the financial sector can reduce harmful CO2. Ding et al. (2020) showed that an increase in the level of financial development can significantly curb per capita energy consumption and thus reduce environmental pollution. Ra Ggad (2021) considered the asymmetric effect of economic growth, energy use, and financial development on carbon dioxide emissions, with positive shocks to economic growth and energy consumption increasing carbon dioxide emissions, while positive shocks to financial development reduce emissions. Therefore, at a high level of financial development, urban FA becomes increasingly significant, and energy consumption shifts from increasing to decreasing, reducing regional CO2. Based on this, hypothesis H2 is proposed in this paper.

H2: Financial agglomeration can reduce CO2 by curtailing energy consumption.

Financial agglomeration, technology market development, and CO2 emissions

When enterprises reduce the cost of economic activities through FA, they take into account the impact of enterprise production on the ecological environment. Consequently, enterprises increase capital investment and expand the scale of technology market development. They aim to enhance the technical level and technological innovation capacity, opting for green production lines and environmentally friendly production technologies. The research conducted by Li et al. (2018) investigated how financial advancement and technological sophistication influence CO2 efficiency. The outcomes indicated that both financial development and technological prowess can enhance CO2 efficiency. He et al. (2019) selected technological innovation as the intermediary variable for financial development to restrain environmental pollution and the research results showed that financial development could improve the current situation of environmental pollution by improving the level of technological innovation of enterprises. Razzaq et al., (2021) explored the relationship between helping to develop the tertiary sector, technological innovation, and CO2, the research results show that tourism development and technological innovation significantly reduce the low level of CO2 in the long term. Hence, the FA effect reduces the cost of economic activities of enterprises, encouraging them to invest more funds in expanding the scale of technology market development, improving technology level and innovation ability to reduce the emission of CO2, and improving the quality of the ecological environment. Based on this, hypothesis H3 is proposed in this paper. The framework for analyzing the impact of CO2 is shown in Fig. 1.

Mechanistic analysis of the impact of financial agglomeration on CO2.

H3: Financial agglomeration can reduce CO2 emissions by expanding technology market development.

Measurement and spatial distribution characteristics of financial agglomeration

Selection and construction of financial agglomeration level index

The evaluation index system of the FA level lacks uniformity. Through the review of the literature, this paper finds that most scholars mainly use the single index method and comprehensive index method based on location entropy when describing FA. Wang et al. (2019) used the single indicator method to measure the degree of FA in various provinces of the country by location entropy. Simultaneously, some scholars have adopted a comprehensive index method to construct an FA evaluation index system from multiple dimensions such as financial development, financial scale, and financial density, and adopted the entropy weighting method to comprehensively measure and measure, which has gradually enriched research conclusions in this field. Ru et al. (2014) formulated the FA-level index system, encompassing four dimensions: the financial development context, the magnitude of financial undertakings, the concentration of financial operations, and the intensity of financial service engagement. Fang, Chang (2020) selected three dimensions: financial scale, depth, and spatial density, measuring the FA index with principal component analysis. Utilizing insights from prior scholarly research and taking into account the accessibility and representativeness of data, this study establishes a comprehensive financial aggregation evaluation index system. The system comprises four dimensions: financial scale, density, depth, and development, detailed in Table 1. Through a comparative analysis of the single index method and the comprehensive index method, and to offer a more objective and rational assessment of the financial aggregation level in each province, the entropy method is applied to gauge the financial aggregation level of each region.

Financial agglomeration level measurement results

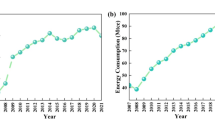

Within this manuscript, the entropy method is employed to compute each dimension of the financial aggregation (FA) level, derive the overall FA level, and scrutinize the outcomes of the calculations. Overall, from 2006 to 2019, China’s FA level continued to improve. Financial development and system construction continued to deepen, and the national FA level increased from 1.376 in 2006 to 5.635 in 2019 (Fig. 2).

Development trend of financial aggregation level in China from 2006 to 2019.

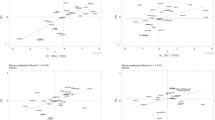

In 2006, the level of FA in Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu was significantly higher than that in other regions. In 2019, the level of FA in Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu remained higher than in other regions. Although the FA level of provinces and cities continues to increase, there are noticeable differences in the rate of improvement for each region, with a decreasing trend in the eastern, central, and western regions, and the gap continues to widen. Notably, Beijing increased from 0.191 to 0.618, Shanghai increased from 0.190 to 0.784. In contrast, the level of FA in Guizhou, Yunnan, and other western regions remains below 0.1. Consequently, the region exhibits a pattern of high-high and low-low FA phenomenon (Fig. 3).

Spatial pattern of financial agglomeration in 30 provinces of China in 2006 and 2019.

Study design

Data sources and Variable measurement

In this paper, panel data from 30 provinces in China from 2006 to 2019 are selected as research samples (Tibet was not selected). CO2 data is obtained from CO2 emission Accounts and datasets. The primary data utilized for assessing the financial aggregation (FA) level, along with the foundational data for other control variables, are sourced from the China Statistical Yearbook, China Regional Economic Yearbook, and China Energy Statistical Yearbook. The descriptive statistical summaries for each variable are presented in Table 2.

Explained variable: CO2 emission. CO2 is used by provinces for CO2 emissions. China’s CO2 Accounting Database has obtained a relatively objective and comprehensive estimate of China’s CO2 at the provincial level. Relevant scholars also put forward their ideas on calculating CO2 and measured CO2 emissions by CO2 dioxide emissions per unit of non-agricultural output (Shao et al., 2019). Hence, the carbon dioxide (CO2) emissions data spanning the years 2006 to 2019 for 30 provinces (excluding Tibet) were extracted from China’s CO2 emission accounting databases (CEADs).

Core explanatory variables: Financial aggregation. Construct an index system of financial aggregation level from four aspects: financial scale, financial density, financial depth, and financial development. We use the entropy method to calculate the comprehensive value of FA and use it as an indicator to reflect the level of FA in each province.

Control variables: As this paper investigates the impact of FA on CO2, it also integrates a large body of literature on this study. Per capita disposal income. We use the natural logarithm of per-capital disposable income (Yang and Zhang, 2023). Population size. We use the natural logarithm of the total population (resident population) at the end of the year (Lei et al., (2021)). Outward foreign direct investment. We use non-financial outward direct investment as a share of GDP. Foreign direct investment can reduce regional CO2 emissions. Foreign direct investment. We use the gross foreign direct investment as a share of GDP (Ren et al., 2022). Industrial structure optimization. We use the ratio of value added of the tertiary industry to GDP (Zhang et al., 2024). Investment intensity. We use the internal expenditure of R&D test funds as a percentage of GDP (Zhu and Wang, 2013).

Intermediary variables: energy consumption and technology market development. Energy consumption. We use total energy consumption (10,000 tons of standard coal). Energy development and energy consumption have formed the development trend of high CO2 emissions (Edelenbosch et al., (2024)).

Technology market development. We use we employ the turnover in the technology market. In their 2016 study, Kang and Wang (2016) investigated the influence of the technology market on the advancement of the urban low-CO2 economy, revealing a noteworthy driving impact. The descriptive statistics for each variable are presented in Table 2.

Spatial correlation test

Based on the study of the impact of FA on CO2, it is found that FA and CO2 exhibit liquidity and diffusion. Considering the possibility of spatial correlation between the two, it becomes necessary to conduct spatial autocorrelation tests on the level of FA and CO2, respectively, before selecting a spatial econometric model for analysis. If the spatial autocorrelation exists, the appropriate spatial measurement model is further selected, and the empirical analysis is carried out. If no spatial autocorrelation is detected, the spatial econometric model cannot be applied. In this paper, the global Moran’s I index is employed to assess the global spatial autocorrelation of financial concentration level and CO2 of the province. The following formula illustrates the calculation process:

In formula 1, \({{S}^{2}=\frac{1}{n}{\sum }_{i=1}^{n}({x}_{i}-\bar{x})}^{2}\) is Sample variance, \({x}_{i}\) is province, \({W}_{{ij}}\) is the spatial weight matrix. The value range of Moran’s I index is (−1,1). A value of 0 indicates the absence of spatial autocorrelation. When the index is greater than 0, it indicates a positive spatial autocorrelation between regional FA and CO2. Conversely, if the index is less than 0, it suggests negative spatial autocorrelation for both the level of regional FA and CO2.

Before calculating the Moran’s I index, Selecting a spatial weight matrix is crucial. Spatial weight matrices commonly encompass geographical distance, spatial adjacency, and economic distance as key factors. The influence on FA and CO2 extends beyond geographical distance, encompassing various economic factors as well.

Based on the dual consideration of geographic and economic factors. We construct the 0–1 spatial adjacency weight matrix (W1), the economic distance spatial weight matrix (W2), and the geographic distance spatial weight matrix (W3), and use the geographic distance spatial weight matrix as a robustness test for the spatial econometric model.

-

1.

The 0–1 neighborhood space weight matrix is a matrix constructed based on geographic location. If two regions are neighboring, it is represented by 1; if two regions are not neighboring, it is represented by 0. The formula is:

$${w}_{ij}=\left\{\begin{array}{ll}1,&\,i\ne j\\ 0,&\,i=j\end{array}\right.$$(2) -

2.

The economic distance spatial weight matrix is a matrix constructed based on the level of economic development. Economic distance, also referred to as the economic gap between two regions, is the inverse of the absolute value of the gap in the level of economic development (GDP) between the two provinces to construct the economic distance spatial weight matrix, the formula is:

$${w}_{ij}=\left\{\begin{array}{ll}\frac{1}{{\bar{Y}}_{i}-{\bar{Y}}_{j}},&\,i\ne j\\ 0,&\,i=j\end{array}\right.$$(3) -

3.

Geographic distance spatial weight matrix, which is a matrix constructed based on the geographic distance between two regions. We use the inverse of the geographic distance as the matrix for constructing the geographic distance spatial weights by measuring the geography between the two regions with the formula:

$${w}_{ij}=\left\{\begin{array}{ll}\frac{1}{{d}_{ij}},&\,i\ne j\\ 0,&\,i=j\end{array}\right.$$(4)

Spatial autocorrelation results analysis

This paper employed Moran’s I index to examine the spatial autocorrelation of FA and CO2 across provinces from 2006 to 2019, with the findings presented in Table 3. Table 3 reveals that, at a 5% significance level, both the significance test of FA levels and Moran’s I index for CO2 are positive, signifying a substantial spatial correlation between FA and CO2.

Model selection and construction

To ensure the reliability of the regression results of the spatial econometric model, this paper adopts Moran’s I test, LM test, and LR test to select the spatial econometric model and conducts the Hausman test to select the fixed effect or random effect of the test model. The test results are shown in Table 4. Observations from Table 4 are as follows: (1) Moran’s I test results show that all regions passed the spatial autocorrelation test. (2) The LM test outcomes indicate the rejection of the null hypothesis at a 1% significance level, affirming the suitability of both the SLM model and SEM model for this study. (3) The LR test results reject the null hypothesis that the SDM model can degenerate into the SLM model and the SEM model at the 1% significance level. This implies the simultaneous presence of spatial lag and spatial error effects. Consequently, the spatial Durbin model (SDM) is chosen for this paper. (4) To further determine whether to use the random effects model or the fixed effects model, the Hausman test is performed. The test results reject the original hypothesis of random effects, confirming that the following models are all fixed effects models.

To address endogeneity concerns arising from natural factors, Lee and Yu (2010) employed the biased modified maximum likelihood estimation (QMLE) for estimating the dynamic SDM model. This paper constructs both the static SDM model, examining the influence of FA levels on CO2, and the dynamic SDM model, accounting for the time lag effects of CO2. The formula is as follows:

Formula 2 is static SDM, formula 3 is dynamic SDM, \(i\) represents province, t represents the year CO2it represents CO2 emission, and CO2i(t−1) represents CO2 emission intensity with a lag of one stage. FCit represents the FA level, δXit represents the control variable, u represents regional, ε represents the random disturbance term, and corresponding spatial coefficients represent the spatial weight matrix.

Empirical analysis of the impact of financial agglomeration on CO2 emissions

Regression result analysis

Tables 5, 6 present the impacts of FA levels on CO2 in both static SDM and dynamic SDM models, along with the temporal lag effect and spatiotemporal lag effect of CO2 in dynamic SDM models.

Spatial spillover effect of CO2

In general, no matter whether static SDM or dynamic SDM, under the weight matrix W1 and W2, the CO2 dioxide spatial term coefficient of the spatial metrology model is significantly positive at the 1% level. This suggests that the CO2 of a province is influenced by the CO2 of other provinces. The reason for this spatial effect may be due to the close geographical distance or similar economic development. Production activities in adjacent regions promote the production and consumption of the two regions, promote regional development, and increase energy consumption and CO2 emissions.

Considering the dynamic SDM model in columns (2) and (4), the influence of the lagged CO2 from the prior period on the current period is accounted for Notably, in both the 0–1 adjacency space weight matrix (W1) and the economic distance space weight matrix (W2), the time lag coefficient of CO2 is notably positive at the 1% significance level. This implies that the CO2 resulting from residents’ activities and industrial production in the preceding period exerts a substantial positive influence on the region’s CO2 in the present period.

Upon incorporating both temporal and spatial dimensions, a noteworthy observation is the significantly positive time-space lag coefficient of CO2 at the 1% significance level. This indicates a substantial positive influence of CO2 from neighboring regions in the preceding period on the local CO2 in the current period. In simpler terms, the CO2 from adjacent areas in the prior period contribute significantly to the rise in local CO2 in the present period.

The spatial spillover effect of FA on CO2

As can be seen from the regression results in columns (1–4) of Table 5, in both the static SDM and dynamic SDM models, under the two weight matrices W1 and W2, the influence coefficient of FA on CO2 is negative at the 1% significance level. This suggests that an increase in regional FA effectively reduces CO2 in the region. In static SDM models (1) and (3), the influence of FA weighting on CO2 is not significant, while in dynamic SDM models (2) and (4), the influence coefficient of FA weighting on CO2 is significantly negative at the level of 1%. This signifies that dynamic SDM is more adept at capturing the spatial spillover impact of FA on CO2, offering a more precise representation. Locally and in adjacent regions, FA exerts a notable inhibitory influence on CO2, demonstrating its significant effect.

Robustness test of the model

As shown in Table 5, Paragraphs (5) and (6) represent the results of a robustness test of the spatial metrology model under geographical distance spatial weight matrix (W3). The spatial lag coefficient, time lag coefficient, and Spatiotemporal lag coefficient symbols of CO2 are consistent with the regression results under 0–1 adjacency space weight matrix (W1) and economic distance space weight matrix (W2). The primary difference lies in the specific values of the influence coefficients, which vary slightly. However, these minor variations do not impact the previously discussed analysis results. This consistency across different spatial weight matrices suggests that the regression results of FA on CO2 are robust.

Column (7) of Table 5 shows the OLS empirical results, which indicate that financial agglomeration hurts carbon emissions at the 5% significance level, indicating that an increase in financial agglomeration helps reduce carbon emissions. These results demonstrate that the significance and regression coefficient compliance of all variables are the same for both the OLS model and the spatial Durbin model.

Therefore, it proves the correctness of the spatial model setting in this paper, and the empirical regression results are more accurate. The empirical results are analyzed as follows. It shows that the regression results of financial agglomeration on carbon emissions in the previous paper are robust.

Decomposition of the effect of FA on CO2

Lesage, Pace (2010) proposed a study on the different scopes and objects of spatial effects and divided the influence of independent variables on dependent variables in spatial measurement models into direct effects, indirect effects (spatial spillover effects), and total effects. This paper further analyzes the spatial effects of FA on CO2 in the dynamic SDM model and adopts the partial differential method to decompose the dynamic SDM regression results in columns (2) and (4) in Table 5, and the decomposition results are shown in Table 6. In general, under the 0–1 adjacent spatial weight matrix (W1) or the economic distance spatial weight matrix (W2), the level of FA has a significant inhibitory effect on the short-term and long-term total effects of CO2. This means that the results of the short-term and long-term total effects are consistent with the regression results of Table 5 without considering the spatial feedback effect.

Overall, the total short-term and long-term effects of financial agglomeration on carbon emissions are significantly suppressed under the 0–1 neighborhood spatial weight matrix (W1) or the economic distance spatial weight matrix (W2), and the results of the short-term and long-term total effects are consistent with the regression results in Table 5, which do not take into account the spatial feedback effect. Under the 0–1 neighbor space weight matrix (W1), the short-term total effect of financial agglomeration level on carbon emission reduction is larger than the long-term total effect.

We analyze the reasons for this phenomenon. The increase in the level of financial agglomeration in the neighboring regions motivates the development of tertiary industries, such as the financial industry and the insurance industry, in the short term in both the neighboring regions and the region. At the same time, the number of energy-consuming secondary industries is reduced, and carbon dioxide emissions are reduced in the short term.

In the long-term consideration, the development of the region needs not only the tertiary industry but also the secondary industry as support, thus causing the short-term total effect of the financial concentration level on carbon emission reduction to be larger than the long-term total effect. Under the economic distance spatial weight matrix (W2), the short-term total effect of financial agglomeration level on carbon emission reduction is smaller than the long-term total effect.

We believe that the possible reason is that the economic distance spatial weight matrix uses the level of economic development as a factor in constructing the economic distance spatial weight matrix (W2). According to the level of financial agglomeration in each province from 2006 to 2019 (Fig. 2), there is a high-high and low-low distribution in the east-central and west-central regions, which leads to a higher reduction of carbon emissions by a high level of financial agglomeration in the long term than by a high level of financial agglomeration in the short term.

Regional heterogeneity test

Since the levels of FA and CO2 vary significantly across different regions in China, our analysis not only examines the impact of FA on CO2 from a national perspective but also delves into the differences in this impact across different regions. To accomplish this, the sample was stratified into the eastern, central, and western regions based on geographical location, allowing for a more in-depth exploration of the regional disparities in the influence of FA on CO2 emissions. Because of the examination of regional diversity, the spatial weight matrix for heterogeneity analysis employed the geographical distance (W3), with the regression outcomes depicted in Table 7.

Spatial spillover effect of CO2

The time lag coefficients for CO2 in both the eastern and western regions exhibit substantial positivity at the 1% level. This indicates a noteworthy positive influence of CO2 from both eastern and western regions on the current period’s CO2 levels. Moreover, CO2 from adjacent regions also exerts a significant positive impact on CO2 levels in the current period. In other words, the CO2 in the neighboring and local regions in the previous period resulted in increased local CO2 in the current period. Conversely, the time lag coefficient of CO2 and the time and space lag coefficient of CO2 in the central region are significantly negative at the level of 1%. This means that the CO2 from the surrounding region and the local region in the previous period does not increase CO2 in the central region in the current period.

According to the above regional analysis, carbon emissions in the eastern and western regions increase carbon emissions in the neighboring regions, while carbon emissions in the central region do not increase carbon emissions in the neighboring regions. We further discuss the reasons leading to regional heterogeneity.

Firstly, the rapid economic development in the eastern region requires more energy consumption for production and living, resulting in high carbon emissions. Most cities in the eastern region of China have heating facilities, while most cities in the central region do not have heating. Secondly, China’s Western development policy further accelerates infrastructure construction in the Western region, leading to an increase in the volume of industrial industry, and the increase in carbon emissions has a diffusion effect on neighboring cities. Thirdly, the central region has increased its industrial restructuring, gradually reducing the proportion of traditional high-carbon emission industries, increasing the proportion of clean energy and low-carbon industries, and adopting advanced energy-saving and emission-reduction technologies. Finally, most cities in the central region do not have corresponding heating facilities in winter, so the carbon emissions and impact on neighboring cities do not reflect the diffusion effect.

The spatial spillover effect of FA on CO2

In the eastern and central regions, the influence coefficients of FA and FA weights on CO2 are both significantly negative at the level of 1%, indicating that the FA in the eastern and central regions has a significant inhibition effect on the local and neighboring regions’ CO2. In other words, FA reduces CO2 in the eastern and central regions. However, in western China, neither FA nor FA weightings have a significant influence on CO2. Financial agglomeration reduces carbon emissions in the East and West but increases carbon emissions in the West. We further discuss the reasons for the regional differences.

First, compared with the East and Central regions, the Western regions have slower economic development and lower levels of financial agglomeration, which have not effectively contributed to the reduction of CO2 emissions. Second, most Eastern regions have completed the process of transition from heavy industry to high-tech and service industries, with a larger share of industries that have high technological content better energy efficiency, and relatively mature carbon emission management. In contrast, most Western regions are in the stage of rapid development of industrialization and urbanization, with a high degree of industrialization. Resource-based industries are still dominant, and the management of carbon emissions and emission reduction technologies are relatively outdated, leading to higher carbon emissions. Third, there is a lack of regional synergy. The financial and technological agglomeration in the Eastern region has helped reduce carbon emissions, but this effect may not have adequately covered the Western region, resulting in an uneven distribution of carbon emissions across different regions.

Mechanism analysis

Following the above examination and analysis of the spatial spillover impact of FA and CO2, it becomes apparent that bolstering FA plays a crucial role in promoting the shift towards a low-CO2 economy. We need to further clarify the transmission mechanism of FA to reduce CO2. Yan et al. (2022) argued that the higher the level of financial development, the higher the level of technology, and thus the lower the CO2 dioxide intensity. Ren et al. (2020) investigated the correlation between economic agglomeration and CO2 emission intensity. Their findings indicate that enhancing the degree of economic agglomeration not only aids in decreasing CO2 emissions but also can indirectly impact CO2 emission intensity through two avenues: environmental regulation and urbanization level. Based on previous studies, on the one hand, FA may affect CO2 emissions through the path of reducing energy consumption, that is, the improvement of FA is conducive to the development of the tertiary industry, the reduction of industrial industries dominated by coal and energy consumption, the reduction of energy consumption, and thus the reduction of CO2. On the other hand, FA may affect CO2 through the development path of the technology market, that is, the higher the FA, the faster the development of the technology market, and the faster the transformation of technological products from scientific research results to production factors, and the improvement of technological level to reduce CO2. Consequently, based on the method of the intermediary effect model, this paper tests whether the transmission mechanism between energy consumption and technology market development is established, and makes an analysis, as shown in Table 8.

According to Table 8, the test results for the intermediary effect of energy consumption are presented in paragraphs (1–3). In column (1), A substantial inverse relationship exists between FA and CO2 emissions, signifying that advancements in FA impede the generation of CO2. In column (2), there is a significant negative correlation between FA and energy consumption, indicating that the higher the level of FA, the development of finance, securities, and insurance industries will be promoted, and the energy consumption of industrial industries will be reduced. In column (3), FA has no significant impact on CO2, while energy consumption has a significantly negative impact on CO2 at the level of 1%, indicating the existence of a complete intermediary effect on energy consumption, that is, the higher the level of FA, the less energy consumption and the smaller CO2 emission intensity. This verifies the transmission mechanism of FA reducing CO2 emission intensity by reducing energy consumption.

In paragraphs (4–6), the test results for the intermediary effect of technology market development are presented. In column (4), FA has a significant negative correlation with CO2, indicating that the improvement of FA has an inhibitory effect on CO2. The FA in column (5) is significantly positively correlated with the development of the technology market, indicating that the higher the level of FA is, the more investment in science and technology will be increased, the level of industrial technology will be improved, and the development of technology market will be promoted. The FA in column (6) has no significant impact on CO2, while the development of the technology market has a significant negative impact on CO2 at the 1% level, indicating that the development of the technology market has a complete intermediary effect, that is, the higher the level of FA, the better the development of technology market and the smaller the CO2 emission intensity. This verifies the transmission mechanism of FA reducing CO2 emission intensity by accelerating the development of the technology market.

Conclusions and policy recommendations

Conclusion

Many cities are actively promoting the development of the financial industry, establishing financial centers, and fostering financial industry agglomeration. FA has become a very obvious phenomenon in the process of China’s economic development, and it is a major strategy widely implemented in many provinces (cities, districts) and cities in China at present. At the same time, with the development of the economy, environmental pollution, CO2 emissions, and other issues have become the focus of attention. Hence, in this study, the entropy method is employed to assess the degree of FA in China and its 30 provinces spanning the years 2006 to 2019. The dynamic spatial Durbin model is chosen for an empirical examination of the correlation between FA and CO2, and additionally, the intermediary effect model is applied to delve into the transmission mechanisms through which FA influences CO2.

Overall, the level of FA in the country continues to rise. However, notable regional disparities persist. That is, the level of FA presents a high-high, low-low agglomeration phenomenon. FA has a significant inhibition effect on CO2, that is, the improvement of the level of FA helps to reduce CO2. After effect decomposition, the level of FA has a significant inhibition effect on the short-term and long-term total effects of CO2. CO2 emissions have significant “time inertia” and “space spillover” effects, albeit with substantial regional variations. From the perspective of regional heterogeneity, the time lag of CO2 and the time and space lag of CO2 in the eastern and western regions both promote the increase of CO2 in the current period, while the reverse is true in the central region. FA can not only directly reduce CO2 emissions, but also indirectly reduce CO2 emissions through two intermediary paths of energy consumption and technology market development. On the one hand, FA reduces CO2 by reducing energy consumption; On the other hand, FA reduces CO2 by accelerating the development of the technology market and improving technology levels.

Policy recommendations

Improve the level of urban FA. Although economic development tends to increase energy consumption and CO2 emissions, the FA phenomenon in some central cities has effectively reduced CO2. According to the regional heterogeneity analysis, the eastern region with a higher FA level has reduced CO2 emissions, and most of the improvement of the FA level at this stage has shown a certain effect in reducing CO2. Therefore, strengthening the agglomeration of the financial industry in the provinces (cities and districts) and leveraging the benefits of FA to reduce costs and improve efficiency is recommended. Enhance the industrial structure by elevating the proportion of the tertiary sector. According to statistics, from 2006 to 2019, the secondary industry accounted for 73% of the total energy consumption on average, the secondary industry is the main industry of energy consumption in China and the main source of CO2 emissions.

Therefore, the government should promote the development of the tertiary industry, reduce the energy consumption of the secondary industry, guide enterprises to gather in a reasonable space to optimize the industrial structure, gradually deindustrialization, and realize a new model of regional development. Accelerate the development of technology markets to reduce CO2 emissions. The transformation of scientific research results into production factors depends on the development of the technology market. The development of the technology market is a crucial means of supporting enterprises in adopting green production lines and enhancing energy efficiency to reduce CO2 dioxide emissions. Therefore, expanding the scale of the technology market and elevating technical proficiency not only realizes the economic benefits of enterprises but also actively guides them in utilizing green production processes to achieve ecological effects.

Data availability

The datasets analyzed during the current study are available in the Dataverse repository: https://doi.org/10.7910/DVN/ACQ5SZ.

Notes

CO2, emissions in this paper will be referred to as “CO2”, below, and will not be repeated in subsequent appearances.

Financial agglomeration in this paper will be abbreviated as “FA”, below, and will not be repeated in subsequent appearances.

References

Ding Q, Li J, Wang Q (2020) Carbon emission effect of the dock-less bike-sharing system in Beijing from the perspective of life cycle assessment. J Environ Account Manag 9(1):31–41

Edelenbosch, OY, Hof, AF, van den Berg, M, de Boer, HS, Chen, HH, Daioglou, V, van Vuuren, DP (2024) Reducing sectoral hard-to-abate emissions to limit reliance on carbon dioxide removal. Nat Clim Change https://doi.org/10.1038/s41558-024-02025-y

Fang F, Chang L (2020) Financial agglomeration effect: urban agglomeration border VS provincial administrative border. Econ Geogr 40(9):53–61

Fitriyah N (2019) Financial development and environmental degradation in Indonesia: evidence from autoregressive distributed lag bound testing method. Int J Energy Econ Policy 9(5):394–400

Gu G, Wang Z (2018) China’s carbon emissions abatement under industrial restructuring by investment restriction. Struct Change Econ Dyn 47:133–144

He J, Chen R, Liu T (2019) Financial development, technological innovation and environmental pollution. J Northeastern Univ 21(02):139–148

Huang J, Wang MJ (2016) Technological Innovation, Industrial Agglomeration, and Environmental Pollution. J Shanxi Univ of Finan Econ 38(4):50–61

Jiang GG (2020) Research on the spatial spillover effect of financial agglomeration on regional economic growth in China. Yunnan University of Finance and Economics, Kunming

Kang SD, Wang J (2016) Research on the interaction effect between scientific and technological progress and urban low-carbon economic development. Macroeconomics 08:116–122

Kijima M, Nishida K, Ohyama A (2010) Economic models for the environmental Kuznets curve: a survey. J Econ Dyn Control 34(7):1187–1201

Lee L, Yu J (2010) A spatial dynamic panel data model with both time and individual fixed effects. Econom Theory 26(2):564–597

Lei W, Jiao L, Xu Z, Zhou Z, Xu G (2021) Scaling of urban economic outputs: Insights both from urban population size and population mobility. Comput Environ Urban Syst 88:101657

Lesage JP, Pace RK (2010). Introduction to spatial econometrics. CRC Press, Boca Raton, p 24–53

Li DS, Xu HF, Zhang SY (2018) Financial development, technological innovation, and carbon efficiency: theoretical and empirical studies. Inq Econ Issues. https://doi.org/10.1016/j.jclepro.2018.07.021

Liu LY, Zhang LY, Li B, Wang YL, Wang ML (2024) Can financial agglomeration curb carbon emissions reduction from the agricultural sector in China? Analyzing the role of industrial structure and digital finance. J Clean Prod 440:140862

Liu XP, Sheng SH, Wang KY (2017) Whether economic spatial agglomeration can increase carbon productivity or not? Econ Re (06):107–121

Mahmood H (2020) Carbon emissions, financial development, trade, and income in North America: a spatial panel data approach. SAGE Open 10(4):1–15

Niu H, Lekse W (2018) Carbon emission effect of urbanization at the regional level: empirical evidence from China. Economics 12(1):20180044

Ozturk I, Acaravci A (2013) The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ 36(1):262–267

Qu C, Shao J, Shi Z (2020) Does financial agglomeration promote the increase of energy efficiency in China? Energy Policy 146:111810

Ra GB (2020). Economic development, energy consumption, financial development, and carbon dioxide emissions in Saudi Arabia: new evidence from a nonlinear and asymmetric analysis. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-020-08390-3

Razzaq A, Sharif A, Ahmad P et al. (2021) Asymmetric role of tourism development and technology innovation on carbon dioxide emission reduction in the Chinese economy: fresh insights from QARDL approach. Sustain Dev 29(1):176–193

Ren S, Hao Y, Wu H (2022) The role of outward foreign direct investment (OFDI) on green total factor energy efficiency: Does institutional quality matter? Evidence from China. Resour Policy 76:102587

Ren XS, Liu YJ, Zhao GH (2020) The impact and transmission mechanism of economic agglomeration on carbon intensity. China popul resour environ 30(4):95–106

Ru LF, Miao CH, Wang HJ (2014) Research on the level and spatial pattern of financial agglomeration in central cities in China. Econ Geogr 34(02):58–66

Shao S, Zhang K, Dou JM (2019) Effects of economic agglomeration on energy saving and emission reduction: theory and empirical evidence from China. J Manag World 35(01):36–60

Wang RY, Wang ZG, Liang Q, Chen J (2019) Financial agglomeration and urban hierarchy. Econ Res J 54(11):165–179

Wang WJ, Xiang QF (2014) Adjustment of industrial structure and the potential assessment of energy saving and carbon reduction. China Industrial Econ (01):44–56

Xu CL, Ren JL, Gong CJ (2014) The influence of adjustment in industrial structures on carbon emissions in Shandong Province. J Nat Resour 29(02):201–210

Yan B, Wang F, Dong M et al. (2022) How do financial spatial structure and economic agglomeration affect carbon emission intensity? Theory extension and evidence from China. Econ Model 108:105745

Yang G, Zhang L (2023) Relationship between aging population, birth rate and disposable income per capita in the context of COVID-19. PLoS ONE 18(8):e0289781

Yang M (2016) The non-linear effects of economic agglomeration on pollution emission in city. Soft Sci 30(09):117–122

Yuan H, Zhang T, Feng Y et al. (2019) Does financial agglomeration promote green development in China? A spatial spillover perspective. J Clean Prod 237:117808

Zhang L, Lin G, Lyu X et al. (2024) Suppression or promotion: research on the impact of industrial structure upgrading on urban economic resilience. Humanit Soc Sci Commun 11:84

Zhou NN, Lin XY (2020) Financial agglomeration, technological innovation, and economic development: spatial econometric analysis based on panel data. Macroeconomic (11):34–48

Zhu H, Zheng J, Zhao QY, Kou DY (2020) Economic growth energy structure transformation and carbon dioxide emission—empirical analysis based on panel data. Res Econ Manag 41(11):19–34

Zhu YB, Wang Z (2013) Abatement control with R&D investment for China under the balanced economic growth path. Stud Sci Sci 31(04):554–559

Acknowledgements

Provincial Science and Technology Program of Guizhou Province “Research on methods and applications of ecological asset valuation in the context of big data - a case study of Guizhou Province” (No.20201Y288)”.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

Informed consent was not required as the study did not involve human participants.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Wan, J., Li, C., Yang, Z. et al. Dynamic spatial spillover effects of financial agglomeration on CO2 emissions: the case of China. Humanit Soc Sci Commun 12, 178 (2025). https://doi.org/10.1057/s41599-025-04455-1

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-025-04455-1