Abstract

This study investigates the impact of intellectual Capital on European professional football clubs’ financial performance, with financial innovation as a mediating factor. Using Ordinary Least Squares (OLS) regression, we analyse panel data from 70 European professional football clubs over a ten-year period, encompassing the ‘Big Five’ leagues (English Premier League, Spanish La Liga, German Bundesliga, Italian Serie A, and French Ligue 1), with 350 yearly observations from 2013 to 2022. The mediating effect of financial innovation is further supported by the Sobel Z test, highlighting its significant role in translating intellectual capital into improved financial performance. A one standard deviation increase in intellectual capital efficiency is associated with a 9.4% increase in ROA. Additionally, financial innovation mediates the relationship between intellectual capital and financial performance, highlighting its crucial role in translating intangible assets into tangible financial outcomes. These findings contribute to the growing body of literature on intellectual capital in the sports industry, providing valuable insights for football club managers and policymakers on enhancing and developing human, structural, and capital employed efficiencies, alongside financial innovation strategies. They should focus on building staff expertise to strengthen club profitability and financial sustainability.

Similar content being viewed by others

Introduction

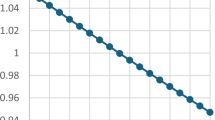

Over the past few decades, the landscape of the professional football industry has transformed from a sport-focused sector to a complex business ecosystem with economic implications (Bauer and Anzer 2021; Guseva and Rogova 2016; Yiapanas et al. 2024). The financial aspects of club management have become increasingly important, with intellectual Capital (IC) becoming a critical driver of competitive advantage and performance (Manzari 2024; Perechuda 2020; Rambe et al. 2023; Scafarto et al. 2021; Soewarno and Tjahjadi 2020; Trequattrini et al. 2021). The football industry now represents a substantial economic force, with the European market alone generating revenues of €28.4 billion in 2021/22 (Aygün et al. 2023; Deloitte 2024). As (Ricci et al. 2015) highlight, professional football is an ideal context for IC research due to its intellectually intensive business nature, unique recognition of human capital as investments on the balance sheet, and relatively under-explored sector. The industry has seen a surge in financial innovations to optimize revenue streams, manage risks, and comply with regulatory requirements like UEFA’s Financial Fair Play regulations (Derun and Mysaka 2020; Dimitropoulos and Scafarto 2021; López and Ratkai 2024; Storm and Nielsen 2012). Innovations in the industry, such as player transfer structures, tokenization, fan engagement platforms, securitization of future revenues, and sponsorship deals, significantly influence the financial landscape, enabling clubs to monetize their intellectual capital innovatively (Morrow 2013). While previous studies have explored individual factors, there is a significant gap in research on their combined effects and potential mediating relationships (Business 2023; Dimitropoulos and Scafarto 2021; Pratama et al. 2020). European football leagues, mainly the “Big Five” (England, Spain, Germany, Italy, and France), attract a massive global audience, making them influential cultural and commercial entities (Deloitte 2023b; Law 2023; Newswire 2025). Notably, the financial performance of the ‘big five’ European leagues has seen substantial improvement, as evidenced by the revenue trends from 2013/14 to 2022/23, with promising forecasts through 2024/25, as depicted in Fig. 1.

Source: Adapted from Sauer et al. (2024).

The value of a club is often more closely tied to its intellectual capital – including player talent, managerial expertise, and brand equity – than to its tangible assets (Occhipinti 2022; Rohde and Breuer 2016). This makes the football industry an ideal context for examining the relationships between various components of intellectual capital and financial performance (Guseva and Rogova 2016; Nufer 2024; Ruberti 2024). Human Capital, including players’ talent and coaching staff’s skills, is a vital component of intellectual capital in football clubs, contributing to their success and financial gain (Neri et al. 2023; Supino and Marano 2024). Client capital, referring to the brand and the team’s fan club size, has also significantly impacted financial performance (Dimitropoulos and Scafarto 2021; Trequattrini et al. 2021). Structural capital, encompassing organisational processes, systems, and databases, has also contributed to the financial performance of football clubs (Pratama et al. 2020; Rompotis 2024). Researchers have found that intangible assets are a key factor in creating value in the sports sector, alongside factors like investment, cost management, and debt (Marchi 2011). Most studies focus on determining the impact of key performance indicators (KPIs) on profitability, which may not be accurate in football business models, as these models offer diverse benefits to stakeholders (Perechuda 2020). The research aims to contribute to the growing body of literature on intellectual capital and financial performance in sports, providing practical insights for club managers, investors, and policymakers (Dingle and Donaldson 2024; Manzari 2024; Wilby et al. 2023). This study suggests that clubs should manage their resources effectively, adopt financial innovation strategies, and achieve sustainable financial performance in a competitive and complex industry (Almendra et al. 2020; Galvão 2017; Lozano and Barreiro-Gen 2022).

The study uses a theoretical framework from a resource-based view, dynamic capabilities theory, stakeholder theory, and legitimacy theory. The research methodology includes sample selection, data collection, variable measurements, and analytical techniques. The empirical results are presented, and robustness checks are provided to validate the findings. The study’s key findings are summarised, along with their theoretical and practical implications. The study acknowledges its limitations and suggests directions for future research. This structure allows for a thorough examination of the relationship between these factors while adhering to academic conventions. The empirical analysis reveals a complex interplay between intellectual capital, financial innovation, and financial performance in European professional football clubs. The findings indicate that human capital, structural capital, and capital employed all contribute to financial performance, but their impacts vary across clubs and leagues. Financial innovation emerges as a critical mediator, enhancing the translation of intellectual capital into tangible financial outcomes. This suggests clubs that effectively leverage financial innovation strategies can better capitalise on their intellectual assets to achieve improved financial results (Ricci et al. 2015; Scafarto and Dimitropoulos 2018). The study comprehensively analyses the complex dynamics by integrating multiple theoretical frameworks, including the resource-based view, dynamic capabilities theory, stakeholder theory, and legitimacy theory. The findings have practical implications for football club managers and policymakers, underscoring the importance of strategic management of intellectual resources and innovative financial practices in achieving sustainable financial success. Additionally, the study identifies avenues for future research, such as exploring these dynamics in other sports or regions, and contributes to ongoing discussions on sustainable financial management in professional sports. The remainder of this paper is organized as follows. Section “Literature review and theoretical background” presents the literature review and theoretical background. Section “Empirical literature and hypotheses” describes the data, sample, and variable measurements. Section “Materials and methods” outlines the empirical methodology and econometric models. Section “Empirical study” reports empirical results and robustness checks. Finally, Section “Conclusion and policy recommendation” concludes with key findings, managerial implications, and directions for future research.

Literature review and theoretical background

This research aims to contribute to the growing body of literature on intellectual capital and financial performance in the sports industry while providing practical insights for football club managers, investors, and policymakers (Dingle and Donaldson 2024; Manzari 2024; Wilby et al. 2023). The findings of this study may have implications for how clubs manage their intellectual resources, approach financial innovation, and ultimately achieve sustainable financial performance in an increasingly competitive and complex industry (Almendra et al. 2020; Daddi et al. 2021; Lozano and Barreiro-Gen 2022). This study adopts multiple theoretical frameworks to provide a comprehensive understanding of the factors influencing intellectual capital and financial performance in European professional football clubs. The resource-based view (RBV) is a foundational theory for this research, offering insights into how clubs’ unique resources, particularly intangible assets, contribute to competitive advantage (Kozlenkova et al. 2014). This theory is particularly relevant given the high intellectual capital intensity of football clubs, where player talent, managerial expertise, and brand value often constitute the most valuable assets (Ricci et al. 2015). Dynamic capabilities theory is crucial for understanding football clubs’ ability to navigate the fast-paced sports industry, regulatory changes, fan expectations, and technological advancements (Coutts et al. 2018; Morrow 2013). By examining financial innovation through the lens of dynamic capabilities (Komakech et al. 2024), we can gain a deeper understanding of how clubs leverage their intellectual capital to create and sustain competitive advantages (Trequattrini et al. 2021). Stakeholder theory examines how clubs balance the interests of fans, players, investors, and local communities in their financial and intellectual capital management decisions (Freeman 2010). Stakeholder theory can be used to understand how clubs’ approaches to intellectual capital and financial innovation are influenced by and shaped by their relationships with key stakeholders (Walzel et al. 2018). Legitimacy theory provides a framework for understanding how clubs maintain their social license to operate through financial and operational practices that align with societal expectations (Schubert 2014). The study employs legitimacy theory to analyse how clubs navigate the intricate balance between financial performance, regulatory compliance, and social acceptance in their intellectual capital (Dimitropoulos and Scafarto 2021). By integrating these theoretical frameworks, this study comprehensively analyzes the correlations between intellectual capital, financial innovation, and financial performance in European professional football clubs. This study addresses several important research gaps in the literature on intellectual capital and financial performance in the football industry.

-

1.

It focuses on the mediating role of financial innovation, which has been underexplored in previous research (Lombardi et al. 2020).

-

2.

The study also examines how financial innovation in professional football can enhance performance and competitive position (Birkhäuser et al. 2019; Morrow 2013).

-

3.

The research employs a multi-theoretical approach, integrating agency theory, stakeholder theory, resource-based view (RBV), and legitimacy theory, to provide a comprehensive understanding of factors influencing intellectual capital and financial performance in football clubs (Geeraert 2021; Kozma and Teker 2022; Sauer et al. 2024; Walzel et al. 2018).

-

4.

The study contributes to the ongoing dialogue on sustainable financial management in professional sports, offering implications for policymakers and regulators (Plumley et al. 2017).

-

5.

The study is based on the European football context, characterized by high intellectual capital intensity and rapid financial innovation, offering insights that may apply to other knowledge-intensive sectors(Giulianotti and Robertson 2007; Lardo et al. 2017).

In conclusion, this study aims to enhance our understanding of the intricate relationships between intellectual capital, financial innovation, and financial performance in European professional football clubs, providing valuable insights for effective management strategies, policy decisions, and the long-term sustainability of the football industry.

Innovation and intangible resources in organizational success

Market competition requires organizations to adopt continuous and growth-oriented practices, employing various strategies, with innovation being the primary driver of economic development and prosperity for companies, industries, and countries (Schettino et al. 2013). Innovation involves creating new products, improving existing ones, or implementing new processes, directly or indirectly impacting company growth and contributing to a country’s economic development. The industry’s reliance on human capital, brand value, and fan engagement makes it an ideal location to study the impact of innovation and intellectual capital on financial performance. “Our findings regarding the positive impact of intellectual capital on financial performance align with previous research in European football (Ricci et al. 2015; Scafarto and Dimitropoulos 2018), reinforcing the importance of intangible assets in this industry. Furthermore, while our study focuses on the English Premier League, future research should explore whether these relationships hold across different European leagues or even in football clubs from other regions (Verónico et al. 2024). Finally, using panel data techniques and GMM estimation builds upon prior methodological approaches (Blundell and Bond 2000), offering a robust analysis of the dynamic relationships between these constructs.

Empirical literature and hypotheses

Intellectual capital and financial performance

The relationship between intellectual Capital (IC) and financial performance has been a subject of increasing interest in the context of European professional football clubs. This section examines the empirical evidence supporting the hypothesized positive impact of intellectual capital on financial performance.

H1: Intellectual capital has a positive impact on financial performance

Recent studies have provided compelling evidence for the positive relationship between intellectual capital and financial performance in football clubs. (Guseva and Rogova 2016) Demonstrate that the VAIC model significantly explains variations in profitability and market capitalisation among European football clubs. It emphasises the significance of intangible assets in driving financial success in the football industry and necessitates a deeper understanding of its components. The resource-based view (RBV) suggests that firms can achieve a competitive advantage by leveraging their unique resources, particularly intangible assets like intellectual capital (Kozlenkova et al. 2014). In the context of European professional football clubs, intellectual capital is crucial due to its high reliance on human capital, brand value, and fan engagement. Guseva and Rogova (2016) found that intellectual capital significantly impacts European football clubs’ profitability and market capitalization. The football industry’s economic landscape, characterised by high intellectual capital intensity and rapid financial innovation, presents an ideal setting to study the impact of intellectual capital on financial performance. The industry’s reliance on intangible assets, such as player talent and brand equity, underscores the importance of intellectual capital in driving financial success.

As such, we propose the following sub-hypotheses: H1a: Human capital positively affects firm performance

Human Capital, comprising the knowledge, skills, and experience of players, coaches, and staff, is often considered the most critical component of intellectual capital in football clubs. (Pratama et al. 2020) A study found that human capital positively impacts Return on Assets (ROA) in English football clubs. The club’s resource-based view suggests valuable and rare human resources can provide a sustained competitive advantage (Kozlenkova et al. 2014). Dimitropoulos and Koumanakos (2015) Demonstrated that investments in human capital, particularly in player acquisitions, were positively associated with improved financial performance in Greek football clubs. The football industry’s unique recognition of human capital as investments on the balance sheet highlights its significance. Effective human capital management can improve team performance, increase fan engagement, and enhance financial outcomes.

H1b: Structural capital has a positive effect on firm performance

Structural capital, including organizational processes, systems, and databases, is crucial for supporting and leveraging human capital in football clubs, but its impact on financial performance is mixed. The study by (Pratama et al. 2020) found that structural capital negatively impacted the Return on Assets (ROA) in English football clubs despite other studies emphasizing its role in enhancing long-term financial sustainability. (Trequattrini et al. 2021) Emphasized the role of effective training systems and youth academies as structural capital components that contribute to financial performance. Dynamic capabilities theory suggests that these structural elements are crucial for adapting to changing environments and sustaining competitive advantages (Teece et al. 1997). Structural capital is vital in supporting human capital in the football industry. For instance, well-developed youth academies can produce talented players, reducing reliance on costly transfers and enhancing financial sustainability.

H1c: Capital employed has a positive effect on firm performance

Capital employed efficiency is essential to intellectual capital in the football industry and maximizing investment returns. The resource-based view suggests efficient physical and financial capital use can contribute to competitive advantage. (Dimitropoulos and Koumanakos 2015) Reported that efficient utilization of capital employed was positively associated with profitability in European football clubs. This relationship underscores the importance of effective resource management in translating tangible assets into financial performance. However, it is worth noting that (Pratama et al. 2020) found no significant effect of capital employed on ROA in English football clubs. Several recent studies support the positive relationship between intellectual capital and financial performance. (Scafarto and Dimitropoulos 2018) Analyzed a sample of European football clubs and reported that intellectual capital efficiency positively influenced accounting- and market-based performance measures. In the context of the football industry, capital employed includes physical assets like stadiums and financial assets like sponsorships.

H2. Intellectual capital has a positive impact on financial innovation

Intellectual capital, comprising human, structural, and relational capital, has been widely recognized as a key driver of innovation across various industries (Subramaniam and Youndt 2005). In the context of football clubs, intellectual capital can facilitate the development and implementation of financial innovations that address the unique challenges and opportunities in the industry.

H2a: Human capital has a positive effect on financial innovation

The resource-based view (RBV) posits that unique and valuable human resources can provide a sustainable competitive (Barney 1991). In financial innovation, human capital represents a key resource that can drive the development of new financial products and strategies. Goshunova (2013) and Morrow (2013) highlighted that clubs with more sophisticated human capital in their finance departments were better equipped to navigate complex financial regulations and develop creative funding mechanisms. Scafarto and Dimitropoulos (2018) found that clubs with higher levels of human capital were more likely to adopt advanced financial risk management techniques and explore alternative revenue streams. In the rapidly evolving landscape of football finance, human capital in the form of financial expertise is crucial for clubs to innovate and remain competitive.

H2b: Structural capital has a positive effect on financial innovation

Structural capital, encompassing organizational processes, systems, and databases, provides the infrastructure necessary for financial innovation. Dynamic capabilities theory (Teece et al. 1997) suggests that organizations must continuously reconfigure their resources and capabilities to address changing environments. Scafarto and Dimitropoulos (2018) Found that football clubs with more advanced financial management systems and data analytics capabilities were likelier to implement innovative revenue generation strategies and risk management techniques. In the context of digital transformation within the football industry. Lardo et al. (2017) demonstrated that investments in digital infrastructure and data analytics capabilities positively impacted revenue generation and cost efficiency in Italian Serie A clubs. The digital transformation of the football industry has made structural capital, particularly in the form of technological infrastructure and data management systems, increasingly important for financial innovation.

H2c: Capital employed has a positive effect on financial innovation

Capital employed, representing the efficient use of physical and financial capital, can provide the resources necessary for implementing financial innovations. The RBV suggests that clubs with superior capital resources are better positioned to invest in and develop innovative financial practices, technologies, and strategies. While direct studies on the relationship between Capital employed and financial innovation in football clubs are limited, research in other industries suggests a positive link. For instance, Mention and Bontis (2013) found a positive relationship between capital-employed efficiency and innovation performance in the banking sector, which shares some similarities with football clubs regarding financial complexity and regulatory scrutiny. In the context of football, clubs with higher capital-employed efficiency may have more resources available to invest in financial innovations.

H3: Financial innovation has a positive impact on financial performance

The relationship between financial innovation and financial performance in European professional football clubs is growing due to the complexity of football finance and the need for clubs to optimize their strategies. Financial innovation in football clubs includes new revenue generation methods, innovative financing structures, and advanced risk management techniques, often driven by compliance with financial regulations like UEFA’s Financial Fair Play rules (Dimitropoulos et al. 2016). Several studies have highlighted the potential positive impact of financial innovation on club performance. López and Ratkai (2024) and Morrow (2013) emphasizing that they provide increased financial flexibility and improved liquidity management. The rising financial complexity of the football industry, coupled with stringent regulations, has made financial innovation crucial for clubs’ financial performance.

H4: Financial innovation mediates the relationship between intellectual capital and financial performance

The mediating role of financial innovation in the relationship between intellectual capital and financial performance in football clubs is an emerging area of research. Intellectual capital, including human, structural, and relational capital, is a key driver of innovation and performance in various industries (Subramaniam and Youndt 2005). In football clubs, intellectual capital facilitates the development and implementation of financial innovations, leading to improved financial performance. Human capital, a critical component of intellectual capital, is crucial in driving financial innovation. Morrow (2013) and Pratama et al. (2020) highlighted that clubs with sophisticated human capital in finance departments are better equipped to navigate complex regulations and develop creative funding mechanisms (Scafarto and Dimitropoulos 2018; Scafarto et al. 2021). Advanced financial management systems and data analytics are more likely to implement innovative revenue generation strategies and risk management techniques, directly impacting financial performance by enhancing revenue streams and mitigating risks, as supported by research in other industries. For instance, Mention and Bontis (2013) found that innovation performance mediated the relationship between intellectual capital and financial performance in the banking sector, which shares some similarities with football clubs regarding financial complexity and regulatory scrutiny. In professional football’s knowledge-intensive and highly regulated environment, intellectual capital is crucial for developing financial innovations to improve performance. In conclusion, the mediation effect suggests that the impact of intellectual capital on financial performance in European professional football clubs is realized through its ability to drive financial innovation.

Materials and methods

Data and methodology

Data and sample construction

The study sample consists of 70 European professional football clubs from the ‘Big Five’ leagues (English Premier League, Spanish La Liga, German Bundesliga, Italian Serie A, and French Ligue 1) with 350 yearly observations from 2013 to 2022. This choice of starting data collection in 2013 is justified by the implementation of UEFA’s Financial Fair Play regulations, a significant financial turnaround in the industry, improved data quality and consistency, widespread adoption of advanced technologies, and the market’s maturity. These factors collectively provide a stable baseline for examining the relationships between intellectual capital, financial innovation, and club performance in the modern era of European football. Given the status of these leagues as among the world’s most popular and financially successful, with the European football market generating substantial revenues (Deloitte 2023a, 2023b), its significance in the global football industry is undeniable. Furthermore, as one of the major contributors to the sports economy, particularly in revenue generation and global viewership, European football clubs have become a pivotal starting point for understanding and addressing financial performance in professional football (Francois et al. 2022). Data for this study was sourced from clubs’ annual reports and financial databases such as Bloomberg and Thomson Reuters Eikon. Industry reports from Deloitte and KPMG, as well as the sample distribution, are categorised by year and club ownership structure.

Variables description

The variable Age (AGE) is measured as the Natural logarithm of years since the football club’s foundation, providing a direct indicator of the club’s longevity and operational experience. This measurement is consistently used throughout the descriptive statistics and regression analysis to facilitate interpretation and also helps reduce skewness, ensuring comparability across clubs with very different founding periods. Financial innovation is quantified using a principal component analysis that combines innovation inputs and outputs. Inputs include (club-level R&D investments) in football-specific technologies such as smart stadiums, wearables, performance analytics, and AI, sourced primarily from club annual reports and financial databases. Output includes (patents) filings that represent financial and technological innovation within the club’s operations. Where club-specific data are unavailable, league- or industry-level proxies are used; this limitation is acknowledged as potentially diluting the precision of financial innovation measurement at the individual club level. Results based on proxy data should therefore be interpreted as reflecting broader league or industry trends rather than purely club-specific innovation activity.

- Dependent Variable: Financial Performance

We use Return on Assets (ROA) to measure financial performance, following research by Chen et al. (Singh et al. 2024). ROA is calculated as:

ROA = Profit before tax / Total assets

This measure provides a comprehensive view of a club’s profitability relative to its total assets, offering insights into management efficiency and resource utilisation (Ghio et al. 2019; Rompotis 2024).

- Independent Variable: Intellectual Capital

We employ the Value Added Intellectual Coefficient (VAIC) model developed by Pulic (Marzo 2022; Pulic 2004) to measure intellectual capital efficiency. The VAIC is calculated as follows:

VAIC = HCE + SCE + CEE

Where:

HCE = Human Capital Efficiency = VA / HC

SCE = Structural Capital Efficiency = VA / SC

CEE = Capital Employed Efficiency = VA / CE

VA (Value Added) = Operating Profit + Employee Costs + Depreciation + Amortization

HC = Human Capital (total salaries and wages)

SC = Structural Capital = VA - HC

CE = Capital Employed (book value of net assets)

This model provides a comprehensive measure of intellectual capital, incorporating human, structural, and physical capital components (Xu and Li 2022).

- Mediating Variable: Financial Innovation

Following (Abdelbaky et al. 2025), we measure financial innovation using principal component analysis (PCA) that includes:

-

1.

Innovation inputs (R&D investments in the football industry from smart stadiums, wearables, immersive training, performance analytics, advanced streaming, esports, and artificial intelligence)

-

2.

Innovation outputs (patents from Citizens’ rights)

According to principal component analysis (PCA), financial innovation (INNOV) is measured as the following equation in Table 1:

INNOV = 0.60 R&D investments +0.40 Patents

This approach captures the multifaceted nature of financial innovation in the football industry, reflecting technological advancements and financial engineering (Merkel 2016).

- Control Variables:

-

1.

Club Size (log of total assets)

-

2.

Financial Leverage (total debt / total assets)

-

3.

Tangibility (fixed assets / total assets)

-

4.

Club Age (Natural logarithm of years since club foundation)

-

5.

Current Assets Ratio (current assets/ total assets)

These control variables account for various club-specific factors influencing financial performance and intellectual capital efficiency (Perechuda 2020; Xu and Wang 2018).

Econometric models and empirical approach

In line with leading studies on intellectual capital in professional football clubs (e.g., Guseva and Rogova 2016; Ricci et al. 2015), this study specifies a panel data regression model with fixed effects to examine the impact of intellectual capital (measured using the VAIC methodology) on financial performance, accounting for club-level heterogeneity across time. When investigating the mediating effect of financial innovation, structural equation modelling (SEM) is employed to capture both direct and indirect relationships among the constructs, following established approaches in sports management research.

To examine the relationships between intellectual capital, financial innovation, and financial performance, we employ the following econometric models:

The direct effect of intellectual capital on financial performance:

\({{\rm{FP}}}_{{\rm{it}}}={{\rm{\alpha }}}_{0}+{{\rm{\beta }}}_{1}{{\rm{VAIC}}}_{{\rm{it}}}+{{\rm{\delta }}}_{1}{{\rm{Controls}}}_{{\rm{it}}}+{{\rm{\varepsilon }}}_{{\rm{it}}}\)

The effect of Intellectual Capital on financial innovation:

\({{\rm{FI}}}_{{\rm{it}}}={{\rm{\alpha }}}_{0}+{{\rm{\beta }}}_{1}{{\rm{VAIC}}}_{{\rm{it}}}+{{\rm{\delta }}}_{1}{{\rm{Controls}}}_{{\rm{it}}}+{{\rm{\varepsilon }}}_{{\rm{it}}}\)

The effect of financial innovation on financial performance:

\({{\rm{FP}}}_{{\rm{it}}}={{\rm{\alpha }}}_{0}+{{\rm{\beta }}}_{1}{{\rm{FI}}}_{{\rm{it}}}+{{\rm{\delta }}}_{1}{{\rm{Controls}}}_{{\rm{it}}}+{{\rm{\varepsilon }}}_{{\rm{it}}}\)

Mediation model:

\({{\rm{FP}}}_{{\rm{it}}}={{\rm{\alpha }}}_{0}+{\rm{\beta }}{1{\rm{VAIC}}}_{{\rm{it}}}+{\rm{\beta }}2{{\rm{FI}}}_{{\rm{it}}}{{\rm{\delta }}}_{1}{{\rm{Controls}}}_{{\rm{it}}}+{{\rm{\varepsilon }}}_{{\rm{it}}}\)Where i represents clubs and t denotes time.

Three measures of Financial Performance (FP): Return on Assets (ROA), Return on Equity (ROE), and Net Profit Margin (NPM). Value-Added Intellectual Coefficient (VAIC) is a sum of Human Capital Efficiency (HCE), Structural Capital Efficiency (SCE), and Capital Employed Efficiency (CEE). Financial Innovation (FI) is measured by Innovation Inputs (R&D investments) and Innovation Outputs (Patents). Control Variables include Club Size (CSIZE), Financial Leverage (LEV), Tangibility (TANG), Club Age (AGE), and Current Assets Ratio (CATA). Table 2 defines the variables.

A potential concern in our models is the presence of multicollinearity among the VAIC components—Human Capital Efficiency (HCE), Structural Capital Efficiency (SCE), and Capital Employed Efficiency (CEE)—due to conceptual overlaps in measuring intellectual capital. Variance inflation factors and correlation diagnostics indicate moderate multicollinearity, which may affect coefficient precision but does not invalidate the overall findings. To account for unobserved heterogeneity and time effects, year fixed effects and clustered standard errors at the club level are retained throughout the analysis. Additionally, a robustness check employing club fixed effects is conducted to absorb all time-invariant heterogeneity at the club level, providing a stringent test of the results’ stability.

Empirical study

This section presents empirical findings in relation to the proposed hypotheses. The results provide robust support for the positive impact of intellectual capital, as measured by the VAIC framework, on financial performance, confirming Hypothesis 1. Among the components, human capital efficiency has the most pronounced effect, reinforcing its central role in club success. Financial innovation also demonstrates significant positive relationships with both intellectual capital and financial performance, supporting its mediating role as hypothesized in Hypothesis 4. Structural capital and capital employed contribute positively, though to a lesser extent. These findings support the theoretical frameworks underpinning the study, including the resource-based view and dynamic capabilities theory, emphasizing the crucial importance of managing intangible assets and promoting innovation to enhance financial sustainability in European professional football clubs.

Descriptive statistics

Table 3 shows the descriptive statistics for study variables. The results indicate that clubs exhibit negative financial performance, with a mean ROA of -3.1% (ranging from -24.4% to 9.4%) and a ROE of -1.3% (ranging from -70% to 51.3%), highlighting struggles with profitability. This aligns with previous studies that highlight the financial challenges faced by many football clubs (Dimitropoulos and Koumanakos 2015). The high standard deviations in performance measures suggest significant disparities across clubs, consistent with the competitive nature of the industry (Plumley et al. 2017). The standard deviations of ROE (0.301) and NPM (0.17) suggest substantial performance disparities across clubs. The Value-Added Intellectual Coefficient or Intellectual Capital Efficiency (VAIC) averages 1.451, with human capital efficiency (HCE) at 1.277, the highest among its components, indicating clubs ‘ reliance on human resources for value creation. Financial innovation shows a mean R&D investment (InnIn) of 0.025 and patent output (InnOut) of 0.026, with minimum values of zero, suggesting uneven engagement in innovation activities. Control variables reveal club size (CSIZE) at 8.536 (SD = 0.478), financial leverage (LEV) at 0.169 (SD = 0.862), and asset tangibility (TANG), which exhibits high dispersion (SD = 11.716), indicating diverse financial structures and strategies across clubs.

Correlation matrix

Table 4 shows that correlation analysis reveals that ROA exhibits a strong positive association with NPM (0.941, p < 0.05), indicating that professional football clubs with higher asset returns tend to achieve superior profit margins. The findings suggest that Value-Added Intellectual Coefficient (VAIC) shows a positive association with ROA (0.160, p < 0.05), ROE (0.133, p < 0.05), and NPM (0.172, p < 0.05), emphasizing the role of intellectual capital in profitability in addition to a significant positive correlation between intellectual capital measures (HCE, SCE, and CCE) and financial performance (ROA) (r = 0.136, 0.163, 0.112; p < 0.05) respectively. Financial innovation demonstrates a weak yet positive impact on club performance. Innovation input (InnIn) is positively correlated with ROA (0.066, p < 0.05) and ROE (0.119, p < 0.05), but its effect on NPM (0.063, p > 0.05) is insignificant. Similarly, innovation output (InnOut) shows weak positive correlations with ROA (0.092, p < 0.05) and ROE (0.130, p < 0.05), while its relationship with NPM (0.088, p > 0.05) remains statistically insignificant. These findings suggest that while financial innovation contributes to firm performance, its effect on profitability remains limited, supporting the resource-based view that intellectual capital is a key driver of competitive advantage and performance in knowledge-intensive industries, such as football (Kozlenkova et al. 2014; Ricci et al. 2015).

Among the control variables, club size (CSIZE) exhibits an insignificant correlation with ROA (0.035, p > 0.05) and ROE (-0.022, p > 0.05), suggesting limited direct effects on profitability. Financial leverage (LEV) shows a weak positive relationship with ROA (0.099, p > 0.05) and ROE (0.071, p > 0.05), implying that leverage may not substantially enhance financial returns. Conversely, current assets (CATA) show a negative correlation with ROA (-0.119, p < 0.05), suggesting that higher liquidity might decrease profitability. In contrast, tangibility (TANG) exhibits a positive correlation with ROA (0.118, p < 0.05), suggesting that higher tangibility (fixed assets) might increase profitability.

Main effects

Table 5 shows the main effects of intellectual capital on financial performance. The result highlights the critical role of intellectual capital in enhancing profitability, while excessive leverage and asset rigidity hinder financial performance. Intellectual capital significantly improves financial performance. Intellectual capital (VAIC) positively affects ROA (0.094, p < 0.01) and ROE (0.278, p < 0.01), with human capital efficiency (HCE) contributing to both ROA (0.028, p < 0.05) and ROE (0.118, p < 0.01). Structural capital (SCE) and capital employed efficiency (CEE) exhibit strong positive effects on ROA (0.057, p < 0.01) and ROE (0.214, p < 0.01). Among control variables, financial leverage (LEV) negatively impacts ROA (-0.074, p < 0.01). Still, it positively influences ROE (0.073, p < 0.05), indicating professional football clubs with higher debt face lower returns on assets but higher equity returns. Asset tangibility (TANG) and liquidity (LATA) significantly reduce both ROA and ROE, with TANG effects at (-0.258, p < 0.01) for ROA and (-1.105, p < 0.01) for ROE. R2 value shows that VAIC explains 30% of the variation in ROA, suggesting a substantial impact of intellectual capital on professional football clubs’ profitability. In contrast, it only explains 10.7% of the variation in ROE, highlighting that intellectual capital influences shareholder returns less than operational performance.

Table 6 presents the results of an OLS regression analysis examining the impact of intellectual capital on financial innovation, with InnIn (Innovation In) and InnOut (Innovation Out) as independent variables. The findings suggest that intellectual capital, particularly measured by VAIC (Value Added Intellectual Coefficient), is positively and significantly associated with both types of innovation (0.024, p < 0.01) for InnIn and (0.030, p < 0.01) for InnOut, indicating that higher intellectual capital enhances innovative capacity. Human Capital (HCE), Structural Capital (SCE), and capital employed efficiency (CEE) also exhibit positive effects, with significance at the 10% and 5% levels. Control variables, such as Leverage (LEV), show a consistent positive relationship with innovation, underscoring its role in fostering innovation. However, club-specific characteristics such as Club Age (AGE), Club Size (CSIZE), Liquidity (LATA), and Tangibility (TANG) exhibit insignificant effects. Intellectual Capital accounts for approximately 16% of the variation in financial innovation, indicating moderate explanatory power. These findings are consistent with previous studies in the football industry (Guseva and Rogova 2016; Scafarto and Dimitropoulos 2018), extending our understanding of these relationships.

Table 7 presents OLS regression results investigating the impact of innovation on financial performance. Financial innovation (InnIn and InnOut) is positively and significantly associated with financial performance; InnIn shows coefficients of 0.617 (p < 0.01) for ROA and 1.844 (p < 0.05) for ROE, while InnOut has coefficients of 0.641 (p < 0.01) for ROA and 1.828 (p < 0.01) for ROE, indicating that innovation fosters profitability. LEV (Leverage) negatively impacts performance, with coefficients of -0.079 (p < 0.01) for both ROA and ROE, suggesting that higher leverage diminishes profitability. Additionally, Liquidity (LATA) and Tangibility (TANG) have significant negative effects on both performance measures, with LATA coefficients of -0.305 (p < 0.01) and -0.303 (p < 0.01) for ROA and ROE, respectively. TANG showing coefficients of -0.231 (p < 0.01) and -0.229 (p < 0.01). Financial innovation accounts for approximately 29% of the variation in financial performance, indicating moderate explanatory power. The significant positive effects of human capital, structural capital, and capital employed efficiency on financial performance align with the theoretical framework of the resource-based view and dynamic capabilities theory (Teece et al. 1997).

Mediation using the Sobel test

Table 8 shows that intellectual capital (VAIC) has a direct positive effect on ROA (0.094, p < 0.05), while financial innovation (InnIn) has a positive influence on ROA (0.498, p < 0.05). The results indicate that intellectual capital has a positive influence on innovation inputs (0.024, p < 0.01). The mediation analysis in Table 7 reveals that innovation (InnIn) partially mediates the relationship between intellectual capital (VAIC) and financial performance (ROA). The Sobel test in Table 8 indicates a statistically significant indirect effect of 0.012 (p-value = 0.041), accounting for 12.8% of the total effect. This suggests that intellectual capital influences financial performance through innovation, but the direct effect of VAIC on ROA remains significant. According to Baron and Kenny’s approach, this constitutes partial mediation, while Zhao, Lynch, and Chen’s framework identifies it as complementary partial mediation.

We conducted an analysis of innovation outputs to explore the mediating role of innovation outputs on the relationship between intellectual capital and financial performance, as shown in the following Table 9. The findings indicate that intellectual capital (VAIC) exerts a direct positive impact on ROA (0.094, p < 0.05), while financial innovation (InnOut) significantly influences ROA (0.518, p < 0.01). Additionally, intellectual capital positively affects innovation outputs (0.030, p < 0.01). As shown in Table 10, innovation outputs (InnOut) partially mediate the relationship between intellectual capital (VAIC) and financial performance (ROA). The Sobel test results in Table 11 confirm a significant indirect effect of 0.015 (p-value = 0.02), representing 16% of the total effect. This suggests that intellectual capital impacts financial performance through innovation outputs, while the direct effect of VAIC on ROA remains substantial. Based on Baron and Kenny’s methodology, this represents partial mediation, whereas Zhao, Lynch, and Chen’s approach classifies it as complementary partial mediation.

Robustness check

We conducted a robustness check. We measured the financial innovation index using principal component analysis (PCA), in addition to assessing financial performance using the net profit margin (NPM) as an alternative measure, which is consistent with methodological approaches in similar studies (Pratama et al. 2020; Scafarto and Dimitropoulos 2018). This approach enhances the validity of the findings by demonstrating their consistency across different measurement techniques. The results confirm the findings from the last mediation. Table 12 indicates that intellectual capital (VAIC) directly enhances NPM (0.559, p < 0.05) and significantly boosts the innovation index (5.556, p < 0.01), with the innovation index also exerting a positive influence on NPM (0.011, p < 0.10) aligns with the work of (López and Ratkai 2024; Morrow 2013), who emphasized the importance of financial innovation in improving club performance.

The innovation index (Innova) partially mediates the VAIC–NPM relationship, as indicated by the Sobel test (indirect effect = 0.059, p = 0.082), which accounts for 10.6% of the total effect, as presented in Table 13. This finding is particularly relevant in professional football clubs, where rapid technological advancements and changing regulatory environments necessitate continuous innovation (Dimitropoulos and Scafarto 2021; Lardo et al. 2017).

These findings suggest that intellectual capital has a direct and indirect impact on financial performance, via the innovation index, consistent with partial mediation as proposed by Baron and Kenny and complementary partial mediation as suggested by Zhao, Lynch, and Chen. This multifaceted confirmation of the relationships between intellectual capital, innovation, and financial performance underscores the importance of these factors in the strategic management of professional football clubs.

Conclusion and policy recommendation

This study contributes to the existing literature by examining the impact of intellectual capital on financial performance in European professional football clubs and investigating the mediating role of financial innovation. Using the Value Added Intellectual Coefficient (VAIC) model to measure intellectual capital components, the research finds that intellectual capital has a positive impact on both financial performance and innovation in European Professional Football Clubs. Financial innovation also positively influences financial performance and mediates the relationship between intellectual capital and financial performance. The results suggest that clubs should prioritise developing and managing their intellectual capital components, including investing in human capital, improving structural capital, and optimising the efficiency of capital employed. Additionally, clubs should recognise the importance of financial innovation as a driver of long-term value creation and implement robust innovation management practices. The study underscores the importance of intangible assets and innovative financial practices in driving financial success in the football industry, with implications for clubs, stakeholders, and regulators.

While this study provides valuable insights into the relationships between intellectual capital, financial innovation, and financial performance in European Professional football clubs, it has limitations. The focus on European Professional clubs may limit the generalizability of findings to other leagues or sports; future research could explore these relationships across European leagues or continents to examine cross-cultural variations. Additionally, the study primarily focuses on quantifiable aspects of performance, leaving qualitative aspects such as sporting success or brand value underexplored. Future studies could incorporate alternative performance indicators or investigate other mediating factors, such as corporate governance or competitive intensity. The study’s cross-sectional design limits its ability to capture long-term dynamics; longitudinal research could provide deeper insights into trends and external influences. Furthermore, the linear relationships tested here may overlook potential non-linear effects or diminishing returns of intellectual capital on financial performance. These limitations present opportunities for future research to further enhance our understanding of how intellectual capital and financial innovation contribute to sustainable success in professional football clubs.

Data availability

The data used to support the findings of this study are available from the corresponding author upon request.

References

Abdelbaky A, Liu T, Mingyang X, Shahzad MF, Hassanein A (2025) Real earnings management and ESG performance in China: the mediating role of corporate innovations. Int J Financ Econ 30(4):3476–3499

Almendra R, Silva D, Silva T, Russo S, França A, Mann R (2020) Innovation and performance in brazilian football clubs. Int J Innov Educ Res 8:01–20. https://doi.org/10.31686/ijier.vol8.iss5.2216

Aygün M, Savaş Y, Alma Savaş D (2023) The relation between football clubs and economic growth: the case of developed countries. Humanit Soc Sci Commun 10(1):566. https://doi.org/10.1057/s41599-023-02074-2

Barney J (1991) Firm resources and sustained competitive advantage. J Manag 17(1):99–120

Bauer P, Anzer G (2021) Data-driven detection of counterpressing in professional football: a supervised machine learning task based on synchronized positional and event data with expert-based feature extraction. Data Min Knowl Discov 35. https://doi.org/10.1007/s10618-021-00763-7

Birkhäuser S, Kaserer C, Urban D (2019) Did UEFA’s financial fair play harm competition in European football leagues? Rev Manag Sci 13. https://doi.org/10.1007/s11846-017-0246-z

Blundell R, Bond S (2000) GMM estimation with persistent panel data: an application to production functions. Econom Rev 19(3):321–340

Business M (2023) ANALYSIS—new waves of investment in European football. Macau Business. https://www.macaubusiness.com/analysis-new-waves-of-investment-in-european-football1/

Coutts A, Kempton T, Crowcroft S (2018). Developing athlete monitoring systems: theoretical basis and practical applications. In: Kellmann M, Beckmann J (eds) Sport, recovery and performance: interdisciplinary insights. Routledge, Abingdon, pp 19–32

Daddi T, Todaro NM, Iraldo F, Frey M (2021) Institutional pressures on the adoption of environmental practices: a focus on European professional football. J Environ Plan Manag 1–23. https://doi.org/10.1080/09640568.2021.1927679

Deloitte (2023a) Annual review of football finance 2023. Deloitte. https://www.deloitte.com/global/en/Industries/tmt/research/gx-annual-review-of-football-finance.html

Deloitte (2023b) The break-even requirement. Deloitte. https://www.2deloitte.com/content/dam/Deloitte/uk/Documents/sports-business-group/deloitte-uk-the-break-even-requirement.pdf

Deloitte (2024) Deloitte Football Money League 2024. Deloitte. https://www.deloitte.com/uk/en/services/financial-advisory/analysis/deloitte-football-money-league.html

Derun I, Mysaka H (2020) Intellectual capital efficiency management in professional football clubs’ performance: problems of assessment. Sport Mont 18(2):61–66

Dimitropoulos P, Koumanakos E (2015) Intellectual capital and profitability in European football clubs. Int J Account Audit Perform Eval 11:202. https://doi.org/10.1504/IJAAPE.2015.068862

Dimitropoulos P, Leventis S, Dedoulis E (2016) Managing the European football industry: UEFA’s regulatory intervention and the impact on accounting quality. Eur Sport Manag Q 16(4):459–486. https://doi.org/10.1080/16184742.2016.1164213

Dimitropoulos P, Scafarto V (2021) The impact of UEFA financial fair play on player expenditures, sporting success and financial performance: evidence from the Italian top league. Eur Sport Manag Q 21:20–38. https://doi.org/10.1080/16184742.2019.1674896

Dingle G, Donaldson A (2024) Concept mapping perceptions of climate impacts on sport participation: perspectives from community-level managers. Manag Sport Leis 1–21. https://doi.org/10.1080/23750472.2024.2412000

Francois A, Dermit-Richard N, Plumley D, Wilson R, Heutte N (2022) The effectiveness of UEFA financial fair play: evidence from England and France, 2008–2018. Sport Bus Manag Int J 12(3):342–362

Freeman RE (2010) Strategic management: a stakeholder approach. Cambridge University Press

Galvão NDJ (2017) Analysis of the performance in generating economic benefits in Brazilian football clubs: the use of athlete as a strategic resource and intangible asset. Revista Contempânea de Contabilidade 14(32):21–47

Geeraert A (2021) National anti-doping governance observer. Final report. A. Play the Game. https://www.playthegame.org/publications/national-anti-doping-governance-observer-final-report/

Ghio A, Ruberti M, Verona R (2019) Financial constraints on sport organizations’ cost efficiency: the impact of financial fair play on Italian soccer clubs. Appl Econ 51(24):2623–2638. https://doi.org/10.1080/00036846.2018.1558348

Giulianotti R, Robertson R (2007) Sport and globalization: transnational dimensions. Glob Netw 7(2):107–112. https://doi.org/10.1111/j.1471-0374.2007.00159.x

Goshunova A (2013) The impact of human capital accounting on the efficiency of English professional football clubs

Guseva DM, Rogova E (2016) Intellectual capital contribution to the financial performance of football clubs

Komakech R, Ombati T, Kikwatha R, Wainaina M (2024) Resource-based view theory and its applications in supply chain management: a systematic literature review. Manag Sci Lett 15:1–12. https://doi.org/10.5267/j.msl.2024.6.004

Kozlenkova I, Samaha S, Palmatier R (2014) Resource-based theory in marketing. J Acad Mark Sci 42. https://doi.org/10.1007/s11747-013-0336-7

Kozma M, Teker F (2022) Business model innovation for sustainable operations in professional football: how supporters gain more control of the beautiful game. Soc Econ 44(4):420–438. https://doi.org/10.1556/204.2022.00022

Lardo A, Dumay J, Trequattrini R, Russo G (2017) Social media networks as drivers for intellectual capital disclosure: evidence from professional football clubs. J Intellect Cap 18:63–80. https://doi.org/10.1108/JIC-09-2016-0093

Law MS (2023) Financial Fair Play 2.0: the UEFA Club licensing and financial sustainability regulations. Morgan Sports Law. https://morgansl.com/en/latest/financial-fair-play-20

Lombardi R, Trequattrini R, Cuozzo B, Paoloni P (2020) Knowledge transfer in the football industry: a sectorial analysis of factors and determinants. Manag Decis. https://doi.org/10.1108/MD-08-2019-1100

López A, Ratkai M (2024) European football clubs and their finances. A systematic literature review. Revista de Contabilidad 27:75–91. https://doi.org/10.6018/rcsar.496271

Lozano R, Barreiro-Gen M (2022) Civil society organisations as agents for societal change: football clubs’ engagement with sustainability. Corp Soc Responsib Environ Manag 30. https://doi.org/10.1002/csr.2390

Manzari A (2024) The role of ESG performance in enhancing intellectual capital and sustainability in European football clubs: a first empirical application. Int J Bus Adm 15:22. https://doi.org/10.5430/ijba.v15n4p22

Marchi L (2011) L’evoluzione del controllo di gestione nella prospettiva informativa e gestionale esterna. Manag Control 3:5–16

Marzo G (2022) A theoretical analysis of the value added intellectual coefficient (VAIC). J Manag Gov 26(2):551–577. https://doi.org/10.1007/s10997-021-09565-x

Mention AL, Bontis N (2013) Intellectual capital and performance within the banking sector of Luxembourg and Belgium. J Intellect Cap 14(2):286–309

Merkel S (2016) The future of professional football: a Delphi-base

Morrow S (2013) Football club financial reporting: time for a new model? Sport 3. https://doi.org/10.1108/SBM-06-2013-0014

Neri L, Russo A, Di Domizio M, Rossi G (2023) Football players and asset manipulation: the management of football transfers in Italian Serie A. Eur Sport Manag Q 23(4):942–962. https://doi.org/10.1080/16184742.2021.1939397

Newswire G (2025) UEFA club competitions media and sponsorship rights business analysis report 2024-25 with kit supplier and front-of-shirt partnerships for all 108 competing teams. Globe Newswire. https://www.globenewswire.com/news-release/2025/01/17/3011312/0/en/UEFA-Club-Competitions-Media-and-Sponsorship-Rights-Business-Analysis-Report-2024-25-with-Kit-Supplier-and-Front-of-Shirt-Partnerships-for-All-108-Competing-Teams.html

Nufer G (2024) Sponsorship of the 2024 European Soccer Championship in Germany: overview, perspectives, special features and developments. Open J Bus Manag 12:275–292. https://doi.org/10.4236/ojbm.2024.121020

Occhipinti Z (2022) Rethinking intellectual capital accounting through professional sport organizations. J Mod Account Audit 18. https://doi.org/10.17265/1548-6583/2022.06.002

Perechuda I (2020) Intellectual capital determinants of football clubs in Europe. Pol J Sport Tour 27:8–13. https://doi.org/10.2478/pjst-2020-0008

Plumley D, Wilson R, Ramchandani G (2017) Towards a model for measuring holistic performance of professional Football clubs. Soccer Soc 18(1):16–29. https://doi.org/10.1080/14660970.2014.980737

Pratama B, Innayah M, Esita P, Winarni D, Setyawan A (2020) Intellectual capital and financial performance of English football club. https://doi.org/10.4108/eai.5-8-2020.2301086

Pulic A (2004) Intellectual capital–does it create or destroy value? Meas Bus Excell 8(1):62–68

Rambe P, Maksum A, Erlina, Zulkarnain (2024) Intellectual Capital as Sustainable Competitive Advantage inBusiness Performance. In Proceedings of the 2nd Maritime, Economics and Business International Conference (MEBIC 2023). 167–177. https://doi.org/10.5220/0012649800003798

Ricci F, Vincenzo S, Domenico C, Samantha GI (2015) Intellectual capital and business performance in professional football clubs. Evidence from a longitudinal analysis. J Mod Account Audit 11(9):450–465

Rohde M, Breuer C (2016) Europe’s elite football: financial growth, sporting success, transfer investment, and private majority investors. Int J Financial Stud 12. https://doi.org/10.3390/ijfs4020012

Rompotis GG (2024) The financial performance of the English football clubs. Int J Financ Res 5(2):181–203

Ruberti M (2024) Why does the European football market need a revolution? Account Audit Account J 37(2):649–660. https://doi.org/10.1108/AAAJ-06-2022-5885

Sauer T, Anagnostopoulos C, Zülch H, Werthmann L (2024) Creating value in football: unveiling business activities and strategies of financial investors. Manag Sport Leis 1–21. https://doi.org/10.1080/23750472.2024.2314568

Scafarto V, Dimitropoulos P (2018) Human capital and financial performance in professional football: the role of governance mechanisms. Corp Gov Int J Bus Soc 18(2):289–316

Scafarto V, Ricci F, Magnaghi E, Ferri S (2021) Board structure and intellectual capital efficiency: does the family firm status matter? J Manag Gov 25(3):841–878. https://doi.org/10.1007/s10997-020-09533-x

Schettino F, Sterlacchini A, Venturini F (2013) Inventive productivity and patent quality: evidence from Italian inventors. J Policy Model 35(6):1043–1056

Schubert M (2014) Potential agency problems in European club football? The case of UEFA Financial Fair Play. Sport Bus Manag Int J 4(4):336–350

Singh R, Gupta CP, Chaudhary P (2024) Defining Return on Assets (ROA) in empirical corporate finance research: a critical review. Empir Econ Lett. https://doi.org/10.5281/zenodo.10901886

Soewarno N, Tjahjadi B (2020) Measures that matter: an empirical investigation of intellectual capital and financial performance of banking firms in Indonesia. J Intellect Cap. https://doi.org/10.1108/JIC-09-2019-0225

Storm R, Nielsen K (2012) Soft budget constraints in professional football. Eur Sport Manag Q 12:183–201. https://doi.org/10.1080/16184742.2012.670660

Subramaniam M, Youndt MA (2005) The influence of intellectual capital on the types of innovative capabilities. Acad Manag J 48(3):450–463. https://doi.org/10.5465/AMJ.2005.17407911

Supino E, Marano M (2024) Capital gains from player transfers as a value creation tool: some evidence from European listed football clubs. Sport Bus Manag Int J 14(1):80–98. https://doi.org/10.1108/SBM-03-2023-0029

Teece DJ, Pisano G, Shuen A (1997) Dynamic capabilities and strategic management. Strat Manag J 18(7):509–533

Trequattrini R, Nappo F, Cuozzo B, Manzari A (2021) The emerging of enhanced intellectual capital: the impact of enabling technologies on the professional football clubs. pp 93–106. https://doi.org/10.1007/978-3-030-80737-5_7

Verónico NS, Macedo AC, Costa RV (2024) The influence of intellectual capital on the financial performance of European professional football clubs. Int J Learn Intellect Cap 21(2):150–174. https://doi.org/10.1504/IJLIC.2024.137577

Walzel S, Robertson J, Anagnostopoulos C (2018) Corporate social responsibility in professional team sports organizations: an integrative review. J Sport Manag 32:1–20. https://doi.org/10.1123/jsm.2017-0227

Wilby RL, Orr M, Depledge D, Giulianotti R, Havenith G, Kenyon JA, Matthews TKR, Mears SA, Mullan DJ, Taylor L (2023) The impacts of sport emissions on climate: measurement, mitigation, and making a difference. Ann N Y Acad Sci 1519(1):20–33. https://doi.org/10.1111/nyas.14925

Xu J, Li J (2022) The interrelationship between intellectual capital and firm performance: evidence from China’s manufacturing sector. J Intellect Cap 23(2):313–341

Xu J, Wang B (2018) Intellectual capital, financial performance and companies’ sustainable growth: evidence from the Korean manufacturing industry. Sustainability 10(12):4651. https://www.mdpi.com/2071-1050/10/12/4651

Yiapanas G, Thrassou A, Vrontis D (2024) The contemporary football industry: a value-based analysis of social, business structural and organisational stakeholders. Account Audit Account J 37(2):552–585. https://doi.org/10.1108/AAAJ-06-2022-5855

Acknowledgements

EA wishes to express sincere appreciation to his respected supervisor, Professor Xu Maowei, as well as to Wuhan Sports University and, in particular, the Department of Sports Economics and Management for the institutional support and academic training received during his doctoral studies. GH wishes to express sincere appreciation to Wuhan Sports University and, specifically, the Department of Sports Psychology for the institutional support and academic training provided during the pursuit of the doctoral degree. We wish to clarify that A.R. received PhD fellowships from the Missions Sector, Ministry of Higher Education, Egypt, in collaboration with the Chinese Scholarship Council (CSC). This research was supported by funding from Wuhan Sports University (Grant No. 1994022; Author with funding: MX).

Author information

Authors and Affiliations

Contributions

EA: conceptualization, methodology, software, data curation, writing --original draft preparation, supervision, and writing --reviewing and editing. MX: conceptualization, methodology, supervision, writing --reviewing and editing. GH: formal analysis, validation, visualization, writing --original draft preparation. AR: methodology, software, data curation, investigation, writing --reviewing and editing.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This paper contains no studies involving human participants that were performed by any of the authors.

Informed consent

This paper does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Abdelmawla, E., Xu, M., Hesham, G. et al. Intellectual capital and financial performance of European professional football club: the mediating role of financial innovation. Humanit Soc Sci Commun 13, 529 (2026). https://doi.org/10.1057/s41599-026-06918-5

Received:

Accepted:

Published:

Version of record:

DOI: https://doi.org/10.1057/s41599-026-06918-5